2013-14 northern territory government and public...

TRANSCRIPT

NORTHERN TERR ITORY GOVERNMENT AND P U B L I C A U T H O R I T I E S ’ S U P E R A N N U A T I O N S C H E M E

Annual Report2013-14

Published by the Department of Treasury and Finance© Northern Territory Government 2014Apart from any use permitted under the Copyright Act, no part of this document may be reproduced without prior written permission from the Northern Territory Government through the Department of Treasury and Finance.ISSN: 1032-1241Northern Territory Superannuation OfficeLevel 5, Cavenagh House, 38 Cavenagh Street, Darwin NT 0800GPO Box 4675, Darwin NT 0801Freecall: 1800 631 630Telephone: +61 8 8901 4200Facsimile: +61 8 8901 4222Email: [email protected]: www.super.nt.gov.au

Northern Territory Government and Public Authorities’ Superannuation Scheme (NTGPASS)Level 5 Cavenagh House, 38 Cavenagh Street DARWIN NT 0800

Postal Address GPO Box 4675 DARWIN NT 0801Tel 08 8901 4200 Fax 08 8901 4222

The Honourable Adam Giles MLA TreasurerGPO Box 3146Darwin NT 0801

Dear TreasurerIn accordance with the provisions of section 43 of the Superannuation Act, we are pleased to provide to you: the report of the Commissioner of Superannuation and the Superannuation Trustee Board on

the operation and management of the Northern Territory Government and Public Authorities’ Superannuation Scheme for the financial year ended 30 June 2014; and

the audited financial statements of the Northern Territory Government and Public Authorities Employees’ Superannuation Fund for the financial year ended 30 June 2014.

Yours sincerely

Sarah RummeryCommissioner of Superannuation26 September 2014

Marianne McAdieDeputy Chairperson, Superannuation Trustee Board26 September 2014

Table of ContentsAbout this Annual Report 2

Report of the Commissioner of Superannuation and the Superannuation Trustee Board 3

Highlights 4Year in Review 4Output Performance 8Future Priorities 8Fund Performance 8Investments 11Scheme Performance 18Membership Profile 21Governance 25Summary of the Report of the Actuarial Investigation of the Scheme 32

Financial Statements 33Overview of the Financial Statements 34Independent Auditor’s Report to Trustee Board 35Statement by the Superannuation Trustee Board 36Statement of Net Assets 37Statement of Changes in Net Assets 38Statement of Cash Flows 39Notes to the Financial Statements 40

About this Annual ReportWelcome to the Northern Territory Government and Public Authorities’ Superannuation Scheme (NTGPASS) Annual Report. NTGPASS was established by the Superannuation Act and provides superannuation benefits for eligible persons employed by the Northern Territory Government. NTGPASS commenced operation on 1 October 1986 and was closed to new members on 9 August 1999.

ObjectiveThe objective of this Annual Report is to provide information on the operations of NTGPASS to the Treasurer, as the Minister responsible for superannuation matters, and to members and other interested parties. This includes new developments and future directions of NTGPASS as well as the management, financial condition and investment performance of the Northern Territory Government and Public Authorities Employees’ Superannuation Fund (fund).

Quick Guide to the Annual ReportThis report of the Commissioner of Superannuation and the Superannuation Trustee Board (STB) provides an overview of the operation and management of NTGPASS and the fund’s investment performance during 2013-14. This section also includes information about the members of the Superannuation Trustee Board and the Superannuation Review Board and their activities during the year.Financial statements provided include the audited Statement of Net Assets, Statement of Changes in Net Assets, Statement of Cash Flows and Notes to the Financial Statements as at 30 June 2014.

Reporting RequirementsThe Superannuation Act requires, within six months of the end of each financial year, that: the Commissioner of Superannuation provides a report to the Treasurer on the operation and

management of NTGPASS; STB provides a report to the Treasurer on its operations during the year and audited financial

statements in respect of the fund; and the Treasurer tables the reports, together with the financial statements and the

Auditor-General’s report of the audit, in the Legislative Assembly within six sitting days of receiving the reports.

2

Report of the Commissioner of Superannuation and the

Superannuation Trustee Board

3

HighlightsFund Performance

NTGPASS investment options recorded strong investment returns in 2013-14. The fund’s return for the default superannuation growth option was 14.04 per cent and the pension growth option was 16.02 per cent.

NTGPASS Pension ClosureThe NTGPASS account-based pension product was closed to new accounts from 1 April 2014.

Superannuation Reform ProjectProgress on the Superannuation Reform Project continued during 2013-14 with drafting of amending legislation for a range of measures.

Superannuation ChangesSeveral superannuation changes have been introduced by the Commonwealth during the past year. Those that will affect NTGPASS members are changes to concessional contributions, including an increased annual cap and revised treatment for contributions in excess of the annual cap.

Year in ReviewFund Performance

All NTGPASS options ended the financial year with a positive investment return, despite some options experiencing periods of negative returns during the year. The NTGPASS growth option returned 14.04 per cent for superannuation accounts and 16.02 per cent for pension accounts. These returns are above the median return for options with a similar asset allocation (as reported by Super Ratings) of 12.66 per cent this year.

NTGPASS Pension ClosureNTGPASS introduced a standard and pre-retirement pension in 2008. Take up of the pension products has been modest and continued operation would have meant a significant increase in fees to pension members. As a result, the NTPGASS pension products were closed to new members from 1 April 2014. Existing pension members were notified of the closure and plans are in place to transfer their accounts to AustralianSuper early in 2015.

Superannuation Reform ProjectDrafting of legislation for a range of amendments progressed during the year. The main changes: allow the transfer of lost and unclaimed superannuation to the Australian Taxation Office; replace the Superannuation Review Board with the Northern Territory Civil and Administrative

Tribunal (NTCAT), when it is operational; introduce time limits for review of decisions; allow STB committees to be formed incorporating all relevant schemes; ensure that STB-related costs can be proportionately levied across the relevant schemes; change the definition of Public Authorities to more readily capture those listed in the

Public Sector Employment and Management Act and the Financial Management Act; remove the Northern Territory Government Death and Invalidity Scheme (NTGDIS)

Anticipatory Payments; remove NTGPASS medical entrant provisions;

4

broaden the interpretation of ‘dependant’ to include ‘interdependency of relationship’; increase the payment without grant of probate; update confidentiality provisions and convert penalty offences in the Superannuation Act to be

compliant with Part IIAA of the Criminal Code, as well as revise maximum penalties; enable compliance with Commonwealth legislation allowing release of superannuation money

for payment of a relevant tax liability; and allow the Commissioner to transfer pension accounts under a successor fund transfer.Legislation was introduced in August 2014 with anticipated passage in October 2014. Not all changes will commence immediately. The ability to transfer lost and unclaimed members is reliant on becoming prescribed under Commonwealth legislation. Replacement of the review mechanism with NTCAT and the associated time limits for review of decisions are dependent on NTCAT becoming operational.Work will continue during 2014-15 to implement these changes. Further cost-saving and efficiency measures may be considered.

Legislative AmendmentsMost NTGPASS members are also entitled to a benefit under the Northern Territory Supplementary Superannuation Scheme (NTSSS). The standard benefit is 3 per cent of final salary for each year of service since 1 October 1988. Previously, interest was paid on unclaimed benefits. The NTSSS Instrument was amended to remove the payment of 6 per cent interest on unclaimed benefits from 31 July 2013.

Superannuation ChangesA number of changes to the superannuation environment introduced in the 2014 Commonwealth Budget or otherwise announced apply from 1 July 2014. Changes include: increasing the concessional contribution cap to $30 000 for people aged 49 and under, and

$35 000 for people aged 50 and over; treatment of non-concessional contributions in excess of the annual cap; an increase in the superannuation guarantee to 9.5 per cent with a delay in the increase to

12 per cent, now to take effect from 1 July 2025; and increased tax on superannuation-related payments for the Medicare levy (to 2 per cent) and

Budget Repair levy (2 per cent) for 2014-15, 2015-16 and 2016-17.Key changes are outlined in more detail below.

Contribution capsConcessional contributions are contributions made from before-tax income, such as salary sacrifice contributions and employer contributions made when members exit the scheme, which are concessionally taxed at 15 per cent. From 1 July 2014, the concessional contribution cap is $30 000 for people aged 49 and under, and $35 000 for people aged 50 and over.Since 1 July 2013, contributions that exceed the caps are taxed at an individual’s marginal tax rate plus an interest charge and the excess contributions can be withdrawn. When a person’s annual income plus taxable superannuation contributions exceed $300 000, an additional 15 per cent tax is applied to the contributions over the $300 000 threshold. In addition to salary sacrifice contributions, for members of a defined benefit superannuation scheme such as NTGPASS, a notional amount of employer contributions, known as notional taxed contributions, are treated as concessional contributions and count towards the concessional cap.It is recommended that members take into account the notional taxed contribution to ensure their salary sacrifice contributions do not exceed the concessional cap. The notional taxed

5

contribution has been determined by the NTGPASS actuary to be a maximum 9.6 per cent of contribution salary.Non-concessional contributions are contributions made from after-tax income such as NTGPASS compulsory member contributions, spouse contributions and Commonwealth co-contributions. The annual non-concessional cap increased to $180 000, or $540 000 over three years for those aged under 65, from 1 July 2014.

Treatment of non-concessional contribution in excess of the annual capPrior to 1 July 2013, contributions in excess of the non-concessional cap were taxed at 46.5 per cent (including Medicare levy). With the increase in the Medicare levy and the introduction of the Budget Repair levy, the tax rate is now increased to 49 per cent. The 2014 Budget introduced changes for the treatment of non-concessional contributions, backdated to 1 July 2013. This allows a member to withdraw any excess non-concessional contributions made after 1 July 2013, thereby avoiding excess non-concessional contributions tax on these amounts.

SuperStreamSuperStream is a package of measures designed to enhance the ‘back office’ of superannuation, which primarily involves electronic transmission of information between superannuation funds. A SuperStream compliant information technology solution was implemented during the year. Where required, all superannuation benefit payments are now made via SuperStream.

Anti-Money Laundering and Counter-Terrorism FinancingThe Commonwealth Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF) imposes a range of governance and operational obligations designed to combat money laundering and terrorism financing activities.The main governance and operational obligations require compliance with an AML/CTF program, which includes a detailed risk assessment, member identification requirements, staff training and due diligence programs, as well as the maintenance of a range of records and regular reporting to the Australian Transaction Reports and Analysis Centre (AUSTRAC).The AML/CTF program implemented in early 2008 is reviewed annually and updated as appropriate. An annual compliance report is submitted to AUSTRAC by the end of March each year.

Member EducationThe Superannuation Office aims to provide informative material to assist members in understanding their NTGPASS entitlements, as well as superannuation in general.Information covering products such as investment options and pensions is available on the website along with a range of publications including forms, fact sheets and information books. Information is kept up to date and new items are developed as required.Superannuation Office staff are happy to talk to members over the phone or in person through arranged appointments. Members are encouraged to seek the services of a qualified professional as the Superannuation Office cannot provide personal financial advice.

WebsiteThe Superannuation Office website is a good source of information for NTGPASS members. The website is regularly updated for investment returns, ‘What’s New’ information and changes made to forms and fact sheets.

Information sessionsA total of 17 information seminars were held in Darwin and Alice Springs, including two webinars.

Annual Report

6

The NTGPASS Annual Report is available electronically, via website download or email, to minimise the impact on the environment. Summarised information is produced in the Report to Members, also available on the website.

7

MembershipsAssociation of Superannuation Funds of Australia

The Association of Superannuation Funds of Australia (ASFA) is a national not-for-profit and non-political organisation that represents the interests of superannuation funds, trustees and members. ASFA is the peak industry body for Australia’s superannuation funds. It undertakes extensive analysis and research on superannuation and provides education and professional development courses for trustees and fund administrators. ASFA hosts an annual national conference that is attended by board members and senior staff of the Superannuation Office.ASFA also hosts various superannuation discussion groups throughout Australia. The Northern Territory discussion group meets each month and meetings are attended by Superannuation Office staff and representatives from superannuation funds, financial planning organisations, the Australian Securities and Investment Commission and Centrelink. Meetings include presentations on topical issues and ASFA executives provide updates on superannuation policy issues by telephone. The group has facilitated ASFA educational seminars in Darwin and provides an important forum for discussions on topical superannuation issues.

Australian Institute of Superannuation TrusteesThe Australian Institute of Superannuation Trustees (AIST) is an independent professional body and registered training organisation offering a range of services for the superannuation industry, including professional development, national and international training, events, compliance services and member support.The board members and senior staff from the Superannuation Office continued their membership of AIST. Membership offers discounted prices for training and events, a number of which are held in Darwin. In addition, a board member attended the annual Conference of Major Superannuation Funds hosted by AIST.

AdministrationOnline member information statements

The annual Member Information Statement provides key information to members about their accumulation account and defined benefit. Member Information Statements from previous years can be viewed online by current Territory Government employees. Members must have access to ePASS to view the available information.In future, it is intended that active members will be able to choose between viewing their current year’s statement online or receiving it via post.

Education and TrainingThe Superannuation Office employs 23 full-time staff and also provides work and development opportunities for students and graduates through Treasury’s entry-level programs. The complexity and technical aspects of superannuation mean that ongoing professional development and education for board members and staff is a high priority.Educational seminars and short courses attended during the year include: ASFA 2013 National Conference; Government Superannuation Funds meeting; ASFA Roadshow; ASFA: RG146 Superannuation (Online); Clayton Utz: Statutory Interpretation; and EASA: Appropriate Workplace Behaviour.

8

The following summary reports on the progress of priorities identified for 2013-14.

Output PerformancePriorities for 2013-14 Results in 2013-14

Continue the Superannuation Reform Project with consideration of measures that can be readily implemented and result in cost savings or efficiencies. These include the removal of interest on unclaimed NTSSS benefits and transfer of lost and unclaimed monies to the Australian Taxation Office.

In progress – the NTSSS Instrument was amended to remove the payment of interest from 31 July 2013. A range of legislative amendments were approved for drafting. Resulting legislation was introduced in August 2014 with anticipated passage in October 2014.

Implementation of revised Heads of Government Agreement.

In progress – the revised agreement was signed by the Northern Territory Treasurer in February 2014. To date, the agreement has not been signed by all jurisdictions.

Continue to work with the Commonwealth and other jurisdictions to consider Stronger Super changes and their impact on Territory superannuation schemes.

Achieved – A SuperStream compliant information technology solution was implemented during the year.

Business continuity through internal training and documentation of procedures to ensure knowledge sharing and continuity of essential tasks.

Ongoing – a review of documentation was undertaken to identify current procedures.

Future Priorities Superannuation Reform Project – continuation and implementation of reforms to the Territory’s

superannuation schemes to simplify arrangements and reduce costs. Superannuation schemes rules – amend rules to improve efficiency and remove redundant or

superseded terms or requirements. Pension closure – finalise successor fund transfer of the NTGPASS pension product.

Fund Performance2013-14 Investment Returns

Table 1 details the fund’s superannuation and pension investment returns for 2013-14, as well as the average annual return (compound average effective rate of net earnings) since each option commenced. Options have been introduced at different times since 2007 and this information is provided in note form. The returns indicated below assume investment in that option for the full year.As Member Investment Choice was introduced in 2007, five-year average returns are now able to be calculated for all options except the pension assertive option. The growth option remains the only option that has been available for the full 10 years, with a return of 6.67 per cent per annum over 10 years and 8.50 per cent per annum since inception.

9

Table 1: 2013-14 Investment Returns

Investment Option 2014 20135-Year

Average10-Year Average

Since Inception

% %

Superannuation

Managed Cash1 2.16 2.76 3.24 - 3.24

Conservative2 7.57 7.83 6.92 - 4.33

Cautious2 10.33 10.69 8.56 - 4.39

Growth (default)3 14.04 15.40 10.24 6.67 8.50

Assertive2 15.57 17.16 10.88 - 3.53

Aggressive2 17.82 19.66 11.61 - 3.01

Pension

Managed Cash1 2.64 3.23 3.76 - 3.74

Conservative4 8.99 9.44 7.90 - 5.88

Cautious5 12.15 13.14 9.72 - 6.18

Growth4 16.02 18.83 11.21 - 5.66

Assertive6 17.57 20.22 - - 9.74

Aggressive4 19.62 23.92 13.20 - 5.04Commencement dates: (1) March 2009; (2) July 2007; (3) 1986; (4) April 2008; (5) June 2008; (6) March 2010

NTGPASS pensions commenced in early 2008. Under the implemented investment consulting arrangement, JANA Investment Advisers Pty Ltd (JANA) manages both NTGPASS superannuation and pension funds, but they are held in separate accounts. Although the same investment options are offered with the same target asset allocation, the actual allocations do vary. Superannuation funds are taxed at 15 per cent while pension funds are tax exempt. A combination of these factors and market conditions results in differing returns across the two accounts.NTGPASS members are further advantaged as the Territory Government meets the cost of administering the scheme. The Trustee has also negotiated favourable investment management fees, on average 0.49 per cent, which is low for professional funds management.Table 2 illustrates the net return over the last five years for the superannuation growth option after taking into account the effect of inflation, as measured by the consumer price index (CPI). The five-year average is calculated as a compound average in line with corporations regulations.

10

Table 2: Investment Returns After Inflation

2014 2013 2012 2011 20105-Year

Average

% % % % % %

Investment return 14.04 15.40 1.08 8.43 12.89 10.24

CPI 3.00 2.40 1.20 3.60 3.10 2.66

Real rate of return 10.72 12.70 - 0.12 4.66 9.50 7.39Note: Real rate of return = Investment returns – CPI

1 + CPI The five-year average annual return after inflation is 7.39 per cent per annum.

Market PerformanceInvestment conditions continued to be favourable in 2013-14. Growth assets such as equities performed well for most of the year, contributing significantly to overall returns in most of the investment options. Australian equities as measured by the ASX 300 Accumulation index rose 17.3 per cent during the year and global equities represented by the MSCI All-Countries World index (hedged) rose 23.9 per cent. Debt assets such as bonds were notably smaller contributors, with outright interest rates on bonds and cash near historical lows. This is evident in Australia’s official cash rate, which finished the financial year at 2.5 per cent.

Net AssetsNet assets represent the value of the fund after taking into account contributions, investment returns, benefit payments and other expenses made throughout the year. Table 3 details the net assets of the fund over the last five years.Table 3: Five-Year Summary of Net Assets as at 30 JuneChange in Assets 2014 2013 2012 2011 2010

$M $M $M $M $M

Net assets at beginning of year 877.2 750.9 736.6 654.4 532.5

Investment revenue 118.6 110.2 10.6 58.3 68.1

Member contributions and rollovers

140.5 124.0 106.1 110.8 106.4

Territory contributions 81.3 68.7 67.9 59.6 38.2

Benefits and other expenses - 229.4 - 176.6 - 170.3 - 146.5 - 90.8

Net assets 988.2 877.2 750.9 736.6 654.4

During the year, net assets increased from $877.2 million to $988.2 million, primarily due to an increase of about $118 million in the market value of investments.

11

InvestmentsInvestment Returns

Returns for superannuation accounts are calculated and applied weekly, while pension accounts are calculated and applied monthly. The current and historical NTGPASS investment returns are published on the Superannuation Office website.The amounts set aside for a general operating reserve are $250 000 (superannuation) and $15 000 (pension). This represents a small proportion of the fund and does not impact on investment returns to members. Net earnings of the fund are distributed among members to the extent possible.

Investment ChoicesMembers have six investment options from which to choose. Members are able to change (switch) the option in which their accumulation account is invested.Superannuation members can choose one option for their account balance and another option for their future contributions. Where superannuation members do not choose an investment option, their member accounts continue to be invested in the default (growth) option. As there is no default option for the pension product, pension members are required to choose at least one investment option but can choose up to six.The majority of NTGPASS superannuation members remain in the growth investment option. Table 4 shows the distribution of member funds across investment choices for member accounts as at 30 June 2014.Table 4: Member Investment Choice

Investment Option

Superannuation Accounts

% of FundsPension Accounts

% of Funds

Managed Cash 2.90 10.28

Conservative 4.84 18.93

Cautious 6.20 20.24

Growth (default) 80.96 45.90

Assertive 2.30 2.52

Aggressive 2.80 2.13

Total 100.00 100.00Note: Includes creditors who have ceased employment but not claimed their benefit. A total of 143 requests for superannuation account investment switches and 20 requests for

pension account switches were processed during the year.In developing the investment options, the Trustee has determined a pre-mixed asset allocation for each option containing a different mix of growth assets (property and shares) and defensive assets (fixed interest and cash). To improve diversity and reduce risk, low correlation and multi-asset strategies were introduced into relevant superannuation options in 2011-12.

Return and Risk Objectives

12

Each investment option has its own return and risk objective to assist members in choosing the investment option with the asset allocation that best suits their personal circumstances and tolerance towards investment risk.The return objective is the net return (that is, after fees and taxes) that the option is expected to achieve above the rate of inflation (as measured by the increase in CPI) over rolling five-year periods. For example, the return objective for the growth option is expected to be at least 3 per cent higher than inflation, when measured over a five-year period.The risk objective is expressed as an average number of years before the option is expected to have a negative return. For example, the growth option is expected, on average, to have a negative return once in every four years.Table 6 (see page 14 and 15) details the return and risk objective and the pre-mixed asset allocation for each of the six investment options as at June 2014.Return and risk objectives are measurable for all superannuation options over the five-year period. For 2013-14, the five-year average CPI is 2.66 per cent. The five-year average return exceeds the target for all options, therefore all options have met return objectives. The cautious and aggressive options have not met risk objectives, as negative returns have been experienced more frequently than the expected target.Table 5: Risk and Return ObjectivesInvestment

Option Return Objective5-Year

AverageObjectiv

e Met Risk Objective ResultObjectiv

e Met

Managed Cash CPI+0.5% pa 3.25% Yes Low probability 0 Yes

Conservative CPI+2.0% pa 6.93% Yes 1 in 7 years 1 in 7 years Yes

Cautious CPI+2.5% pa 8.60% Yes 1 in 4.5 years 2 in 7 years No

Growth (default) CPI+3.0% pa 10.37% Yes 1 in 4 years 3 in 28 years Yes

Assertive CPI+3.5% pa 11.06% Yes 1 in 3.5 years 2 in 7 years Yes

Aggressive CPI+4.0% pa 11.88% Yes 1 in 3 years 3 in 7 years NoCPI = consumer price index; pa = per annum

13

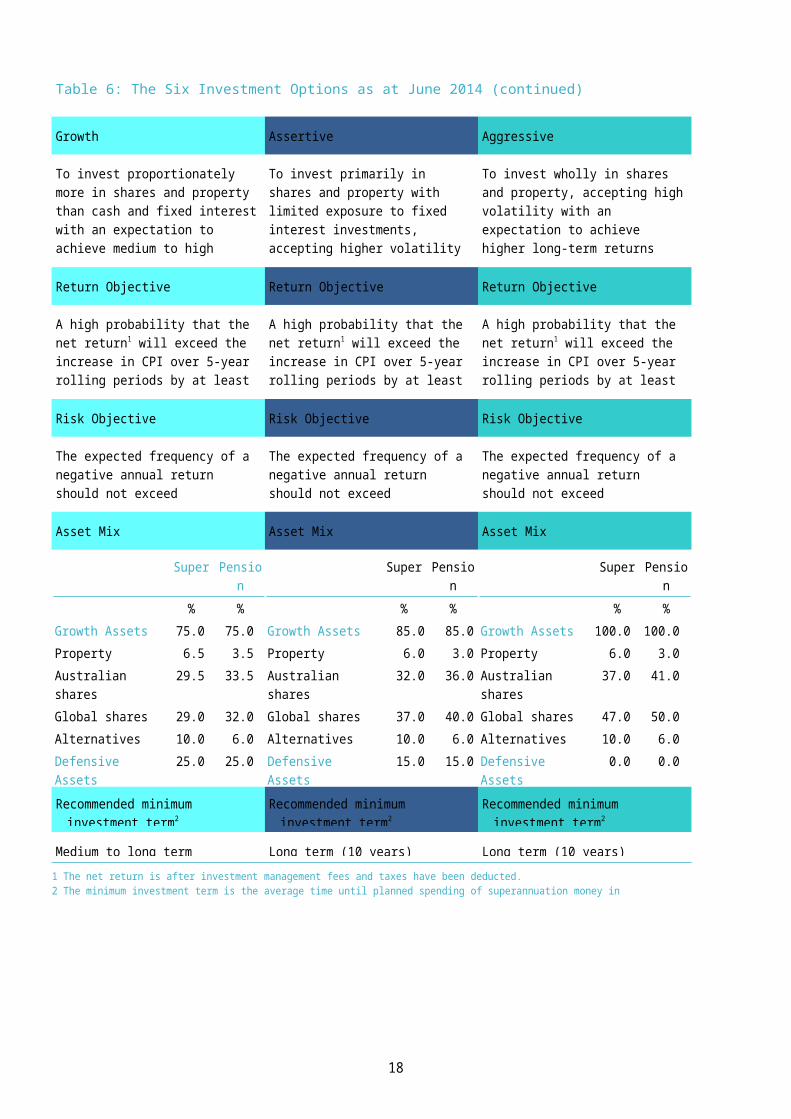

Table 6: The Six Investment Options as at June 2014

Managed Cash Conservative Cautious

To provide greater assurance on the security of assets by investing in cash investments with an expectation to achieve low long-term returns

To provide limited ups and downs in investment value by investing primarily in cash and fixed interest investments

To provide a balanced mix of assets, steady long-term returns and a low level of investment volatility

Return Objective Return Objective Return Objective

A high probability that the net return1 will exceed the increase in CPI over 5-year rolling periods by at least 0.5 per cent per annum

A high probability that the net return1 will exceed the increase in CPI over 5-year rolling periods by at least 2 per cent per annum

A high probability that the net return1 will exceed the increase in CPI over 5-year rolling periods by at least 2.5 per cent per annum

Risk Objective Risk Objective Risk Objective

A low chance of a negative annual return

The expected frequency of a negative annual return should not exceed 1 in 7 years, on average

The expected frequency of a negative annual return should not exceed 1 in 4.5 years, on average

Asset Mix Asset Mix Asset Mix

Super Pension% %

Growth Assets 0.0 0.0Property 0.0 0.0Australian shares 0.0 0.0Global shares 0.0 0.0Alternatives 0.0 0.0Defensive Assets 100.0 100.0Cash 100.0 100.0Fixed interest 0.0 0.0

Super Pension% %

Growth Assets 30.0 30.0Property 4.0 2.0Australian shares 9.0 10.0Global shares 12.0 16.0Alternatives 5.0 2.0Defensive Assets 70.0 70.0Cash 10.0 10.0Fixed interest 60.0 60.0

Super Pension% %

Growth Assets 50.0 50.0Property 6.0 3.0Australian shares 17.0 21.0Global shares 17.0 20.0Alternatives 10.0 6.0Defensive Assets 50.0 50.0Cash 5.0 5.0Fixed interest 45.0 45.0

Recommended minimum investment term2

Recommended minimum investment term2

Recommended minimum investment term2

Short term Short term (3 years) Medium term (5 years)1 The net return is after investment management fees and taxes have been deducted.2 The minimum investment term is the average time until planned spending of superannuation money in retirement.

14

Table 6: The Six Investment Options as at June 2014 (continued)

Growth Assertive Aggressive

To invest proportionately more in shares and property than cash and fixed interest with an expectation to achieve medium to high long-term returns

To invest primarily in shares and property with limited exposure to fixed interest investments, accepting higher volatility with an expectation to achieve higher returns over the long term

To invest wholly in shares and property, accepting high volatility with an expectation to achieve higher long-term returns

Return Objective Return Objective Return Objective

A high probability that the net return1 will exceed the increase in CPI over 5-year rolling periods by at least 3 per cent per annum

A high probability that the net return1 will exceed the increase in CPI over 5-year rolling periods by at least 3.5 per cent per annum

A high probability that the net return1 will exceed the increase in CPI over 5-year rolling periods by at least 4 per cent per annum

Risk Objective Risk Objective Risk Objective

The expected frequency of a negative annual return should not exceed 1 in 4 years, on average

The expected frequency of a negative annual return should not exceed 1 in 3.5 years, on average

The expected frequency of a negative annual return should not exceed 1 in 3 years, on average

Asset Mix Asset Mix Asset Mix

Super Pension% %

Growth Assets 75.0 75.0Property 6.5 3.5Australian shares 29.5 33.5Global shares 29.0 32.0Alternatives 10.0 6.0Defensive Assets 25.0 25.0Cash 3.0 3.0Fixed interest 22.0 22.0

Super Pension% %

Growth Assets 85.0 85.0Property 6.0 3.0Australian shares 32.0 36.0Global shares 37.0 40.0Alternatives 10.0 6.0Defensive Assets 15.0 15.0Cash 2.0 2.0Fixed interest 13.0 13.0

Super Pension% %

Growth Assets 100.0 100.0Property 6.0 3.0Australian shares 37.0 41.0Global shares 47.0 50.0Alternatives 10.0 6.0Defensive Assets 0.0 0.0Cash 0.0 0.0Fixed interest 0.0 0.0

Recommended minimum investment term2

Recommended minimum investment term2

Recommended minimum investment term2

Medium to long term (7 years) Long term (10 years) Long term (10 years)1 The net return is after investment management fees and taxes have been deducted.2 The minimum investment term is the average time until planned spending of superannuation money in retirement.

15

Growth OptionThe majority of members’ accounts are invested in the growth (default) option, which allocates approximately 75 per cent of the invested amounts to growth assets (shares and property) and 25 per cent to defensive assets (cash and fixed interest). As noted in Table 6, the Trustee’s return and risk objective for this option is to achieve a net return greater than CPI plus 3 per cent over rolling five-year periods and to limit the probability of a negative return to one year in every four years, on average. The key drivers to achieve the objective are the strategic asset allocation (to growth versus defensive assets) and the performance of the underlying investment markets in which these assets are invested.Figure 1 shows performance against the return objective for the growth option over the life of the NTGPASS fund. It illustrates that, when measured on this basis, the fund has met the return objective for the majority of the time. The performance target was met in 2013-14.Figure 1: Rolling Five-Year Real Return

Figure 2 shows performance against the risk objective for the Growth option over the life of the NTGPASS fund, demonstrating that the fund has exceeded expectations, with only three negative returns in 28 years.Figure 2: Frequency of Negative Return

16

Investment Manager StructureJANA is the implemented investment consultant for NTGPASS. In its role as consultant to the STB, JANA provides advice on investment objectives and strategies, and selects and monitors investment managers who manage the funds. JANA appoints investment managers with complementary styles across different asset classes, such as international and Australian shares, property and fixed interest securities. This style of management creates a well-diversified portfolio that helps minimise risk to produce positive long-term returns.As part of the role, JANA provides advice on risk and asset allocation. JANA reports to the STB on these matters, as well as investment performance, quarterly. As part of risk management, JANA applies a range of stress testing (scenario analysis) to the NTGPASS portfolio.Another function performed by JANA is portfolio re-balancing, to bring the actual asset mix in line with the target allocation. JANA aims to keep the actual asset allocation of each investment option in the fund within plus or minus 5 per cent of the STB’s target allocation. The asset allocation ranges are continually monitored to ensure they are within targets.As at 30 June 2014, JANA’s investment structure utilised 43 investment managers (excluding the multi-manager private market investments) listed in Table 7. JANA’s managers hold around 2000 bonds and invest in shares in around 1500 different companies across 60 industries and in over 40 countries.

17

Table 7 shows the investment managers used by JANA under each asset class as at 30 June 2014.Table 7: Investment ManagersAustralian shares Antares Capital

Balanced Equity ManagementConcise Asset ManagementFidelity Investment ManagementJCP Investment PartnersNorthcape CapitalVinva Investment ManagementFairviewInvescoParadice

International shares CarnegieDelawareDimensionalHarding LoevnerMondrianSands CapitalTweedy, BrowneWalter Scott

Property Morgan Stanley Investment ManagementResolution Capital

Diversified debt Antares CapitalUBS Asset ManagementGoldman SachsWellingtonRoggeDeutsche BankPGIAmundiFranklin TempletonPIMCOHuff High YieldOaktreeShenkmanApollo

Low correlation strategy BridgewaterNephilaBalestraBlue Mountain

Multi-asset strategy RufferPyrford

Cash MLCAntares

Private equity MLC

18

Investment GovernanceThe STB is committed to act in the long-term interests of NTGPASS members and has engaged Regnan, an investment governance company, to provide specialist research and advice to the fund. Regnan researches environmental, social and corporate governance (ESG) risks to the long-term sustainability of Australian companies listed on the ASX 200. The Regnan model is unique in that it engages in proactive, constructive and confidential dialogue with companies on ESG issues.During the year, Regnan undertook 72 engagements with 47 stocks reaching around half of the current ASX 200. The four key topics most discussed were: executive remuneration; effective disclosure on ESG issues; community relations and social licence risks; and climate change including the impact of a changing climate on business operations. In addition, Regnan made eight formal submissions to government or other bodies, held three director-investor dialogue events and presented at eight events hosted by others.

Scheme PerformanceScheme Overview

NTGPASS is established by the Superannuation Act (the Act), which sets out the arrangements for administration and management of the scheme. The NTGPASS Rules are established by way of a schedule to the Act and contain administrative instructions regarding contributions and benefits applicable under the scheme.NTGPASS is a defined benefit scheme that provides a lump sum benefit upon resignation, age retirement or retrenchment. Lump sum benefits generally comprise two components, a member accumulation component and a Territory-financed component. The member component is made up of member contributions, rollovers and investment earnings. Members are required to contribute between 2 per cent and 6 per cent of their salary to the fund.The Territory-financed component is calculated according to a formula based on the member’s length of membership in the scheme, final average salary and contribution rate. This component is unfunded, meaning it is only paid by the Territory when members claim their benefit. This generally occurs after ceasing employment with the Northern Territory Public Sector (NTPS). Members over preservation age (currently 55) who have retired from the public sector can elect to receive their superannuation benefit as an income stream in the form of a pension, rather than a lump sum.NTGPASS members are also entitled to a Territory-financed benefit from NTSSS. NTSSS is a non-contributory lump sum scheme that provides a 3 per cent productivity payment for each year of membership.Other publications (primarily the Member Information book) are available, which provide more information on how NTGPASS works.

19

Operational PerformanceThe following table reports on the operational performance of the Superannuation Office in its administration and management of NTGPASS. It shows the actual performance against targets, some of which are also published in the Department of Treasury and Finance Annual Report.Table 8: Performance Measures

Performance Measures2013-14 Target

2013-14 Actual

Benefits processed 1 602 1 590

Number of NTGPASS and NTSSS lost member accounts 3 460 3 297

Seminars held 17 17

Stakeholder satisfaction1 ≥ 5 5

Average days to make benefit payments: from date of receipt of all information2 30 10 where there is a delay in the receipt of information3 19

1 Stakeholders are the Treasurer, Trustee and superannuation scheme members. Measures range from a rating of 1: extremely dissatisfied to 6: extremely satisfied.

2 As a non APRA regulated superannuation fund, benefits are processed as soon as practicable, but within 30 days.3 All necessary information from the member and the employing agency must be received before a benefit can be paid. The most common contacts with members related to statement requests, lost members,

scheme rules and updates to member records.

Benefit PaymentsTable 9 illustrates the different categories of benefits paid. Of members leaving NTPS employment, resignation was the most common type of benefit category, although age retirement had the greatest value.Table 9: Total Benefits Paid for the Year Ended 30 June

2013-14 2012-13

Type of Benefit PaidNumber of Members Total Paid

Number of Members Total Paid

$M $MSuperannuationResignation 183 29.51 268 31.66Age retirement 167 83.29 154 67.50Retrenchment 30 17.70 13 5.25Invalidity 7 3.71 6 2.38Death 4 3.23 9 3.91Anti-detriment 12 0.06 16 0.20Transfer 0 0.00 2 0.37Retained 432 66.08 373 54.10Annuity bonus 0 0.00 0 0.00Total 835 203.58 841 165.37Pension n/a 14.92 n/a 7.20Note: Amounts reflect actual payments made and may be inconsistent with financial statements due to accounting treatment. Pension benefits paid include regular payments as well as lump sum withdrawals.

During 2013-14, 835 superannuation lump sum benefits were paid to members, totalling $204 million. This is an increase of $38 million from 2012-13.

20

ContributionsTable 10 shows the number and value of contributions received into the fund.Table 10: Total Contributions Received for the Year Ended 30 June

2013-14 2012-13

Type of ContributionNumber of

Contributors

Value of Contribution

sNumber of

Contributors

Value of Contribution

s

$M $M

Superannuation

Compulsory 3 737 18.02 3 993 18.78

Voluntary

Active 77 1.58 70 0.97

Retained 58 2.18 44 1.62

Salary sacrifice 636 6.53 700 6.95

Rollovers 800 78.64 1 062 72.761

Co-contribution 148 0.05 530 0.21

Spouse contribution 14 0.34 14 0.03

Total 5 470 107.34 6 413 101.321

Pension 56 30.26 45 22.401 2012-13 amounts have been adjusted to conform with current year presentation.Note: Contributions may differ to financial statements due to categorisation. Pension contributions do not include additional

contributions made by existing pension members. In 2013-14, there was an overall increase in the value of contributions received into the fund.

Information SeminarsFour information sessions, ‘Understanding your NTGPASS Benefit’, were held in Alice Springs in March 2014 and attended by 101 members. In addition, JANA provided an investment and financial markets update.Nine sessions were held in Darwin in November 2013 attended by 258 members. Following this, a webinar was trialled, with members logging on to view a slideshow presentation with verbal commentary. This is an effective method of reaching members outside the Darwin area. A webinar recording is available for members to access from the Superannuation Office website.

21

Membership ProfileWhen active members cease NTPS employment (or opt out of the scheme), they may choose to retain some or all of their NTGPASS benefit in the fund. Consequently, as the active membership declines, the retained membership generally increases. Figure 3 illustrates the decline in active NTGPASS membership since the scheme closed to new members in August 1999. In the financial year immediately prior to scheme closure, there were around 12 000 active members.Figure 3: Membership Since the Closure of NTGPASS in August 1999

During the year, active membership of NTGPASS decreased by 8 per cent to 3527. The number of retained members decreased by 2 per cent to 4396.

Active MembersActive members of NTGPASS are those members still employed by the NTPS and eligible to receive a Territory-financed benefit when they leave employment. Table 11 illustrates the changes in active NTGPASS membership.Table 11: Active NTGPASS Members

2013-14 2012-13Active members at beginning of period 3 829 4 109Less exits

Resignation 120 120Age retirement 131 92Retrenchment 37 5Invalidity 6 4Death 7 3Transfer 1 0Opt out 0 56

Total exits 302 280Members at 30 June 3 527 3 829

NTGPASS active membership reduced from 3829 to 3527.

22

Membership by EntityActive membership is widely distributed across NTPS as detailed in Table 12.Table 12: Active NTGPASS Membership by EntityEntity1 Name 2014 2013Batchelor Institute of Indigenous Tertiary Education 20 24Charles Darwin University 33 36Darwin Port Corporation 14 17Department of Arts and Museums 42 45Department of Business 62 80Department of Children and Families 40 37Department of Community Services 13 19Department of Corporate and Information Services 148 168Department of Correctional Services 128 142Department of Education 896 977Department of Health 771 817Department of Housing 50 61Department of Infrastructure 51 70Department of Land Resource Management 69 70Department of Lands, Planning and the Environment 71 72Department of Local Government and Regions 6 7Department of Mines and Energy 30 31Department of Primary Industry and Fisheries 92 101Department of Sport and Recreation 3 6Department of the Attorney-General and Justice 73 80Department of the Chief Minister 67 46Department of Legislative Assembly 8 7Department of Transport 40 47Department of Treasury and Finance 38 41Legal Aid Commission 11 11Menzies School of Health Research 13 15Northern Territory Police, Fire and Emergency Services 414 440Office of the Commissioner for Public Employment 7 9Parks and Wildlife Commission of the Northern Territory 59 65Power and Water Corporation 240 266Tourism NT 7 10Other2 11 12Total 3 527 3 8291 Entities listed are those as at 30 June 2014.2 ‘Other’ includes the Northern Territory Electoral Commission, Auditor-General’s Office, Land Development Corporation,

Ombudsman for the Northern Territory and Aboriginal Areas Protection Authority.

Around 49 per cent of active members are employed in the education and health sectors.

Member Contribution RatesActive members can maximise the Territory-financed component of their NTGPASS benefit by contributing at a higher contribution rate. Member contribution rates generally increase with age.

23

As members approach retirement they tend to increase their contribution rates to maximise their final NTGPASS age retirement benefit.Table 13 shows the number of members contributing at different rates.Table 13: Member Contribution Rates

2013-14 2012-13

Contribution RateNumber of Members Total

Number of Members Total

% %

2 per cent of salary 262 7.4 277 7.2

3 per cent of salary 97 2.8 99 2.6

4 per cent of salary 117 3.3 120 3.1

5 per cent of salary 185 5.2 182 4.8

6 per cent of salary 2866 81.3 3 151 82.3

81.3 per cent of active members choose to contribute at the highest rate of 6 per cent.Membership by Age and Gender

Membership by age and gender is illustrated in Figure 4. Women continue to represent the majority of active members at 63 per cent of the total membership.Figure 4: Membership by Age and Gender

The majority of men and women are in the 50 to 59 year age group.

24

Retained and Spouse MembersRetained members of NTGPASS include members who have retained all or part of their benefit in NTGPASS when they ceased active membership, as well as spouse account holders and non-member spouses who retained all or part of their family law benefit in NTGPASS. Retained members are not required to make contributions but can do so under the NTGPASS Rules.Table 14 illustrates the changes in retained NTGPASS membership. Usually, as active membership decreases, retained membership increases.Table 14: Retained NTGPASS Members

2013-14 2012-13Retained members at beginning of period 4 468 4 350Add new membersRetained members 229 367Spouse accounts 3 3Family law retained benefit 3 4Less exitsRetained members 301 254Spouse accounts 4 2Family law retained benefit 2 0Retained members at 30 June 4 396 4 468

The number of retained members decreased from 4468 to 4396.

Pension MembersNTGPASS pensions have been available to members since March 2008, with the first pension payments commencing in April 2008. Table 15 shows the change in the number of members.Table 15: NTGPASS Pension Members

2013-14 2012-13Pension members at beginning of period 181 150Add new members 57 45Less exits 26 14Pension members at 30 June 212 181

The number of members utilising the pension product increased from 181 to 212.

ComplaintsThe Superannuation Office has a complaints management policy and internal complaints management framework. The objective of the policy is to ensure that complaints are dealt with fairly, promptly and in an efficient and confidential manner. Three complaints were received and resolved during 2013-14.

25

GovernanceAdministration and Management of NTGPASS

The Superannuation Act requires: the Commissioner of Superannuation to administer NTGPASS; the STB to act as Trustee of the fund; and the Superannuation Review Board to advise the Treasurer on proposed amendments to

NTGPASS Rules and hear appeals against decisions of the Commissioner of Superannuation.Figure 5: NTGPASS Administrative Structure

The Superannuation Act requires the fund to pay expenses incurred by or on behalf of the Trustee in relation to the management of the fund. These expenses include investment management fees, governance expenses (Regnan) and the fund’s tax agent.The costs of day-to-day administration and management of NTGPASS are paid by the Territory. These costs include the salaries of Superannuation Office staff, actuarial fees, office accommodation and system administration costs. Some costs are recovered through fees.The Superannuation Office provides secretariat services to STB and the Superannuation Review Board. These services include recording minutes of meetings, preparation and distribution of board papers, financial and investment reports, travel arrangements, payment of sitting fees to board members and arranging their attendance at educational seminars and conferences.

Commissioner of SuperannuationSection 4 of the Superannuation Act provides for a Commissioner of Superannuation to be appointed by the Administrator. The statutory role of the Commissioner is to administer NTGPASS and to undertake and manage the investments of the fund as directed by STB.John Montague resigned as Commissioner of Superannuation during the year. Tony Stubbin (Deputy Under Treasurer) acted in the position from 3 May 2014, until Sarah Rummery was appointed on 9 June 2014.

26

Northern Territory Superannuation OfficeThe Commissioner of Superannuation manages the Northern Territory Superannuation Office, which is a division of Department of Treasury and Finance, a Territory Government agency. The primary role of the Superannuation Office is to: provide superannuation policy advice to the Territory; administer the Territory’s public sector superannuation schemes and NTGDIS; manage the investments of the Territory’s public sector superannuation funds as directed by

the trustees of the various schemes; and provide secretariat services for the Superannuation Review Board and STB.Further information on the Superannuation Office can be found in the Department of Treasury and Finance Annual Report.

Superannuation Trustee BoardThe STB is a body corporate established by section 8A of the Superannuation Act. The functions of the board are to act as trustee of the fund and to direct the Commissioner of Superannuation in managing the investments and the fund on its behalf. Additionally, the board may direct the Commissioner to: engage investment managers, actuaries, financial and legal advisers and other experts in

relation to the management of the investments of the fund; and invest the monies of the fund in investments that the board considers appropriate.With the Minister’s approval, the STB may also administer any other superannuation scheme and manage investments of the fund for any such scheme.The STB has nine members representing three schemes: NTGPASS; Legislative Assembly Members’ Superannuation Scheme; and Northern Territory Police Supplementary Benefit Scheme (NTPSBS).Membership of STB includes the Under Treasurer, a chairperson, a deputy chairperson and six nominated persons. Of the nominated persons, two must be nominated by the Under Treasurer, two must be nominated by unions, one must be nominated by the Commissioner of Police and one by the Northern Territory Police Association (NTPA). All members (except the Under Treasurer) are appointed by the Minister for a five-year term. There were no changes to STB membership during 2013-14.

27

Current members of the Superannuation Trustee BoardMs Kathleen Robinson FCPA BBUS (Acc) – ChairpersonKathleen is Chief Executive, Department of Corporate and Information Services. She has had a long career with NTPS, including extensive experience in senior positions in Shared Services and Treasury.Kathleen was appointed as Chair of the former Superannuation Investment Board on 22 March 2007. She was re-appointed as Chair (now Chairperson) of STB on 22 March 2012, for a five-year term.

Ms Marianne McAdie BBUDP – Deputy ChairpersonMarianne is a former public servant with the Territory government. She retired in 2013 after 35 years of service. Marianne is currently working as a consultant for the Department of Business.Marianne was appointed as Acting Chair of the former Superannuation Investment Board on 22 March 2007. She was re-appointed as Acting Chair (now Deputy Chairperson) of STB on 22 March 2012, for a five-year term.

Ms Jodie Ryan – Member, Under TreasurerJodie commenced as Under Treasurer from 1 July 2013. The Under Treasurer represents members of the Legislative Assembly Members’ Superannuation scheme.Jodie has had a long career in Treasury and previously held senior positions including Deputy Under Treasurer.

Mr Michael Martin OAM FCPA BA BCom Grad Dip (Admin)AdvDip (Superannuation) – Member, nominated by Unions NTMichael is a former senior public servant with both the Commonwealth and Territory governments and has been involved in the accounting and finance environment for over 30 years. He is currently Chairman of the Larrakia Trade Training Centre, a partner with a local Territory consultancy firm and a company director.Michael was appointed as Member of the former Superannuation Investment Board on 11 May 2004. His position carried over as Member of STB. Michael was re-appointed on 11 May 2014 for a five-year term.

Ms Naomi Porrovecchio – Member, nominated by Unions NTNaomi is currently the Manager Employee Relations for the Power and Water Corporation. She joined NTPS in 1993 and has held various roles within NTPS agencies. Naomi was the Regional Director of the Community and Public Sector Union from 2006 to 2008. Naomi is the current President (and former National President) of the Australian Labour and Employment Relations Association of the Northern Territory.Naomi was appointed as Member of STB for five years from 12 March 2013.

28

Mr Alex Pollon GAICD – Member, nominated by the Under TreasurerAlex is General Manager of the Northern Territory Treasury Corporation. He joined NTPS in 1998 and has more than 18 years experience in the Australian financial markets industry. Alex is a member of the Australian Institute of Company Directors and has been granted Australian Financial Markets Association dealer accreditation.Alex was appointed as Member of the former Superannuation Investment Board on 1 April 2009. His position carried over as Member of STB. Alex was re-appointed on 1 April 2014 for a five-year term.

Ms Vicky Coleman BBUS (Acc) CPA GAICD – Member, nominated by the Under TreasurerVicky is Manager Financial Administration of the Northern Territory Treasury Corporation. She is a Certified Practising Accountant, has completed the Australian Institute of Company Directors’ course, the Chartered Secretaries Australia’s Certificate in Governance and Risk Management, is a member of the Finance and Treasury Association and serves on a number of external boards. She joined NTPS in 2000.Vicky was appointed as Alternate Member of the former Superannuation Investment Board on 1 April 2009. Her position carried over as Member of STB. Vicky was re-appointed on 1 April 2014 for a five-year term.

Mr Mark McAdie BEc M Pub Pol Grad Cert App Mgt – Member, nominated by Commissioner of PoliceMark is a former Assistant Commissioner, Crime and Support Services of the Northern Territory Police. He retired in 2010 after 35 years of service.Mark is also President of Beat the Heat NT (Inc) and President of the Northern Territory Police Museum and Historical Society (Inc).Mark previously held an ongoing appointment as Chairman of Trustees of the NTPSBS (police representative). His appointment carries over as Member of STB from 25 May 2012 for a period of five years.

Mr Gowan Carter – Member, nominated by NTPAGowan is a former Sergeant of the Northern Territory Police, who retired in 2008 after 32 years of service. Gowan was a long-term Executive Member of the NTPA.Gowan was previously appointed as Trustee of the NTPSBS (member representative).His appointment carried over as Member of STB until 8 August 2013. He was reappointed for a further five years to 8 August 2018.

29

STB MeetingsSTB met four times during the year. The meetings related to general STB business and investment decisions of the fund. Representatives of JANA attended all meetings to provide an update on investment performance and present on contemporary investment topics.

Board ExpensesThe board resolved to apply its associated costs to the three funds administered according to the value of funds under management. On this basis, 93.8 per cent was attributed to NTGPASS for 2013-14. Board expenses for 2013-14 totalled $65 702, of which $61 615 was attributed to NTGPASS. Total costs are detailed below.

Sitting fees $5 320

Training and conferences $10 151

AIST membership $12 375

Governance expenses $37 856

Total $65 702

Costs include sitting fees, conference and training expenses (including accommodation and airfares), AIST membership fees, internal audit expenses and corporate governance fees (such as Regnan advisory services). These costs support activities that are considered appropriate for good governance.

RemunerationPayments to STB members are made in accordance with a determination under the Assembly Members and Statutory Officers (Remuneration and Other Entitlements) Act (AMSO), which sets the rates payable for attendance at meetings, travel and other STB-related activities. Remuneration is not payable where an STB member is also an employee of the NTPS, the Commonwealth or a state public service.The current remuneration rate applicable to STB members is set in the Statutory Bodies Classification Structure 2012, issued under AMSO. The rate is $304 per day or an hourly rate of one-fifth of the daily rate. In 2013-14, four STB members were entitled to receive sitting fees for meeting and conference attendance and the total amount of remuneration received was $5320. A portion was attributed to NTGPASS.

Conflict of InterestSection 8S of the Superannuation Act provides that an STB member who has a direct or indirect interest in any matter being considered by it must disclose the nature of that interest as soon as possible at an STB meeting.The disclosure of interest does not apply where an STB member has a direct or indirect interest in a matter because they are a member of NTGPASS, or if they are a member of an incorporated company with 25 or more members of which they are not a director.STB maintains a conflict of interest register as part of its best practice processes. At the commencement of each meeting, members are required to sign the register and record any disclosure in the minutes of that meeting.Where a disclosure is made in relation to a matter being considered, members cannot take part in deliberations or decisions made on that matter and the member is disregarded for constituting a quorum on that matter. During the year, there were no conflicts of interest registered.

30

Superannuation Review BoardThe Superannuation Review Board is established by section 9 of the Superannuation Act. The role of the board is to review decisions or actions of the Commissioner of Superannuation (on request or appeal of those whose benefits are affected by a decision or action of the Commissioner) and to advise the Treasurer, as the Minister responsible for superannuation matters, on amendments to the NTGPASS Rules.The Superannuation Review Board comprises an independent chair, a member nominated by Unions NT, a member nominated by the NTPA and a member nominated by the Treasurer. The nominee of the NTPA participates in an appeal hearing only where the appeal concerns a member of the Northern Territory Police. The nominee of Unions NT does not participate in police appeal matters.There have been two changes to Review Board membership. The Superannuation Office acknowledges the sad passing of Mrs Jane Large and her contribution to the Review Board. Mrs Large was the Chair of the Review Board from 2007 to 2013.Mr Graham Symons was appointed as Chair in November 2013, and Mr Guy Riley was appointed in January 2014 to replace Mr Stephen Herne.The current members of the Review Board are:Chair Mr Graham SymonsActing Chair Mr Christopher Hosking Member nominated by Unions NTMr Lynton SherryAlternate Member Mr Rod SmithMember nominated by NTPA Mr Gowan Carter Alternate Member Mr Andrew SmithMember nominated by Minister Mr Robert Bradshaw Alternate Member Mr Guy Riley

AppealsSection 46(5) of the Superannuation Act provides for a member or other person dissatisfied by a decision of the Commissioner of Superannuation to request the Commissioner to reconsider the decision. Section 47(1) of the Superannuation Act allows a person to appeal to the Superannuation Review Board in relation to a decision or action of the Commissioner, or the Commissioner’s failure to make a decision or take action.No appeals were lodged with the Review Board during 2013-14.

Compliance with Commonwealth Superannuation LegislationThe superannuation industry is regulated by an extensive and diverse legislative framework. Commonwealth legislation includes the superannuation industry supervision framework, resolution of complaints system, superannuation guarantee regime, superannuation contributions regime and the taxation of superannuation benefits and superannuation entities.Most state and territory public sector schemes, including NTGPASS, are regulated under their own legislation and have been classified as exempt public sector superannuation schemes under the Superannuation Industry (Supervision) Act 1993 (Cth) (SIS). SIS legislation treats exempt public sector superannuation schemes as complying funds for concessional taxation and superannuation guarantee purposes.A Heads of Government Agreement (HOGA) requires NTGPASS to conform to the principles of SIS and the Commonwealth’s retirement income policies. As a result, NTGPASS is not regulated under SIS but is required to comply with most other Commonwealth superannuation legislation, for

31

example, superannuation surcharge and family law. A revised HOGA incorporating changes since the original agreement signed in 1996, has been agreed, but not yet signed, by all jurisdictions.

AuditsThe results of the annual compliance audit and the NTGPASS Annual Report are provided to the Commonwealth each year to assist in its monitoring of NTGPASS under the HOGA.The Northern Territory Auditor-General’s Office provides audit services to both the scheme and the fund. Section 43 of the Superannuation Act requires the fund’s financial statements to be audited by the Auditor-General and tabled in the Legislative Assembly. The audited financial statements are presented from page 35.The audit services also include an annual compliance audit to ensure the scheme complies with the principles of SIS and other relevant legislation. To date, there have been no compliance issues arising from these audits.

Actuarial ServicesThe provision of actuarial services to the Department of Treasury and Finance and ad hoc actuarial advice to the Territory Government are available under a panel contract. A new panel contract is effective from 1 July 2013 for a five-year period, with Cumpston Sarjeant Pty Ltd and PricewaterhouseCoopers Securities Ltd on the panel.Actuarial services to the scheme are provided by PricewaterhouseCoopers Securities Ltd.Section 45 of the Act requires an actuarial review of NTGPASS to be undertaken every three years. The review examines the scheme’s experience during the previous three years, and prepares projections of the Territory-financed cash flows and accrued liabilities.The most recent actuarial review of the scheme was undertaken as at 30 June 2013 by PricewaterhouseCoopers Securities Ltd. A summary of the review is presented on page <OV>. The next review is due in 2016.The actuarial estimates of future cash flows to fund the Territory-financed component of NTGPASS benefits and accrued liabilities of the scheme (based upon nominal values) have been updated based on 2013-14 information as shown in Table 16.Table 16: Estimated NTGPASS Territory-financed Benefit Costs

Year to 30 June Estimated Cash FlowEstimated Accrued

Liability

$M $M

2015 79.3 826.8

2020 93.8 807.2

2025 96.9 676.1

2030 87.1 480.3

2035 64.7 272.7

2040 37.9 108.9

2045 12.9 24.1

2050 1.6 1.4

32

In addition to undertaking actuarial reviews, the actuary provides advice on superannuation policy matters, including advice on the offset provisions to apply where a member is retired on the grounds of invalidity and is entitled to workers compensation benefits for loss of earning capacity. The actuary also assists with advice in relation to taxation deductions available to the fund.

33

Summary of the Report of the Actuarial Investigation of the Schemeas at 30 June 2013

The last actuarial review of the scheme was performed as at 30 June 2013 by Catherine A Nance FIAA, from PricewaterhouseCoopers Securities Ltd and the results were provided in her report dated September 2013.The review dealt with the employer liabilities, which are guaranteed by the Territory under the Superannuation Act and met on an emerging cost basis. The future employer cash flows and accrued liabilities were projected to the year 2053.The scheme started in 1986 and was closed to new members from 9 August 1999. The employer cash flow for the year ended 30 June 2013 was $66.1 million. It is expected that the cash flow will continue to grow over the next nine years to peak at $98.0 million in the year 2021-2022. It is then expected to decline slowly, becoming zero by 2053.It was assumed that notional earnings rate (which in this case is possibly better described as a discount rate) (3.8 per cent) would be less than the rate of general salary inflation (4.5 per cent) by 0.7 per cent per year. On this basis the accrued employer liability was $948.1 million as at 30 June 2013. The accrued liability is expected to increase over the next three years to peak at $967.7 million by 2016. The last members are expected to leave by 2052, at which stage the liabilities will be zero.If a discount rate of 4.8 per cent, rather than 3.8 per cent was used, the accrued liability would be reduced from $948.1 million to $870.9 million (an 8 per cent reduction).If a discount rate of 2.8 per cent, rather than 3.8 per cent was used, the accrued liability would be increased from $948.1 million to $1037.4 million (an 9 per cent increase).Member contributions are invested in the scheme and credited with investment returns. Returns in relation to employee contributions are determined so that the market value of the assets of the scheme is very close to the sum of the member accounts, so members share fairly in the earnings on their own contributions.The financial soundness of the scheme arises from the Territory guarantee to meet the employer share of benefit entitlements as they arise. This is an appropriate way to meet benefits in a public sector scheme provided the extent and nature of the liabilities is disclosed and included within public sector accounts as is the case with NTGPASS.

34

Financial Statements

35

Overview of the Financial StatementsForm and Content

Financial statements for superannuation funds are prepared in conformity with Australian Accounting Standard (AAS) AAS25 Financial Reporting by Superannuation Plans. To reflect the overall change in the value of assets available to pay superannuation benefits to members, AAS25 requires that periodic changes in the net market value of assets be recognised as revenue. Recently, the Australian Accounting Standards Board (AASB) introduced AASB1056 for superannuation entities which will replace AAS25. The new accounting standard updates AAS25 to include financial statements more focused on member flows. Although the Superannuation Trustee Board (STB) will consider the early adoption of AASB1056 closer to the time of its mandatory application, Northern Territory Government and Public Authorities’ Superannuation Scheme (NTGPASS) will include the following from this financial year: a Statement of Changes in Net Assets; a Statement of Net Assets; and a Cash Flow Statement.

InvestmentsThe fund held investments of just over $1.007 billion with JANA Investment Advisers Pty Ltd (JANA) and $0.8 million with Super Loans Trust as at 30 June 2014. The investment with Super Loans Trust allows members access to low interest home loans and credit cards. Cash of approximately $1.5 million was held in the operating accounts for the day-to-day operations of the fund.

Benefit PaymentsA benefit payment comprises the member’s accumulation account and, where applicable, a Territory-financed component. The Territory guarantees to meet the employer share of benefit entitlements as it arises, and transfers the Territory-financed component to the fund at the time a benefit is paid. This funding method is known as emerging cost and is an appropriate way to meet benefits in a public sector scheme. The member accumulation account contains the member’s contributions and rollovers, accumulated with earnings at the fund’s crediting rate on an annual basis. If applicable, benefit payments are reduced by the amount of the member’s surcharge debt account at the time the benefit is paid.

Fund ExpensesExpenses paid by the fund relate to benefit payments, management expenses incurred in the investment of funds, membership of the governance advisory service and the provision of tax accounting services. All other administrative costs such as salaries, audit, actuarial, administration and operational costs are paid by the Territory.

36

Independent Auditor’s Report to Trustee Board

37

Statement by the Superannuation Trustee BoardIn the opinion of the Superannuation Trustee Board: the accompanying financial statements consisting of a Statement of Net Assets, Statement of

Changes in Net Assets, Statement of Cash Flows and Notes to the Financial Statements are drawn up to present fairly the financial position of the Northern Territory Government and Public Authorities’ Superannuation Scheme as at 30 June 2014 and the results of its operations for the year then ended in accordance with Australian Accounting Standards and other mandatory reporting requirements;

the financial statements have been prepared in accordance with the requirements of the Superannuation Act as amended; and

the scheme has operated in accordance with the provisions of the Superannuation Act as amended and in compliance with the requirements of the Superannuation Industry (Supervision) Act 1993 during the year ended 30 June 2014.

Deputy Chairperson

Date: 26 September 2014

M MCADIE

Member Date: 26 September 2014

A POLLON

38

Statement of Net Assetsas at 30 June 2014

Note 2014 2013

$000 $000

ASSETS

Cash and cash equivalents 1 531 5 736

Units in life policies 1 007 490

888 270

Super Loans Trust 792 1 060

Territory contributions receivable 17 951 16 571

Other receivables 118 207

Deferred tax assets 1 2

TOTAL ASSETS 1 027 883

911 846

Less

LIABILITIES

Benefits payable 4(a) 33 179 29 695

Sundry liabilities 19 10

Provision for surcharge contributions tax 1 866 2 195

Current tax liability 7(c) 1 885 188

Deferred tax liability 7(d) 2 690 2 481

TOTAL LIABILITIES (excluding net assets available to pay benefits)

39 639 34 569

Net assets available to pay benefits 988 244 877 277

Represented by:

Accumulated funds 987 979 877 012

Operational reserve 265 265

NET ASSETS AVAILABLE TO PAY BENEFITS 988 244 877 277

The statement of net assets should be read in conjunction with the notes to the financial statements.

39

40

Statement of Changes in Net Assetsfor the year ended 30 June 2014

Note 2014 2013$000 $000

REVENUEInvestment revenue 118 569 110 256Interest 169 257Distributions from investments 68 55Movement in net market value of investments 5 118 332 109 944

Contributions revenue 221 836 192 701Member contributions 61 433 49 635Surcharge payments received 393 330Government co-contributions 45 205Territory contributions 81 323 68 652Transfers from other funds and rollovers 78 642 73 879TOTAL REVENUE 340 405 302 957

EXPENSESBenefits paid 4 218 505 169 653Disablement benefits 3 710 2 699Retirement benefits 83 292 71 196Withdrawal benefits 113 292 86 853Death benefits 3 291 1 707Pensions paid 14 920 7 198

Other expenses 502 382Board expenses 62 58Administration expenses 375 243Superannuation surcharge contributions tax 65 81TOTAL EXPENSES 219 007 170 035

Net change for the year before income tax 121 398 132 922Income tax expense 7(a) 10 431 6 525Net change for the year after income tax 110 967 126 397

NET ASSETS AVAILABLE TO PAY BENEFITS AT THE BEGINNING OF THE FINANCIAL YEAR

877 277 750 880

NET ASSETS AVAILABLE TO PAY BENEFITS AT THE END OF THE FINANCIAL YEAR

988 244 877 277

41

The statement of changes in net assets should be read in conjunction with the notes to the financial statements.

Statement of Cash Flowsas at 30 June 2014

Note 2014 2013$000 $000

Interest received 169 257Investment distributions 68 55Payments for goods and services - 493 - 378Receipts from members 140 513 124 050Receipts from the Territory 81 323 68 652Payments to members - 218 505 - 169 653Taxes paid - 8 865 - 9 489NET CASH FLOWS FROM OPERATING ACTIVITIES 10(a

)- 5 790 13 494

Proceeds from investments 24 885 2 798Purchase of investments - 23 300 - 17 000NET CASH FLOWS FROM INVESTING ACTIVITIES 1 585 - 14 202

Net increase in cash - 4 205 - 708

Cash at bank at beginning of period 5 736 6 444

CASH AT BANK AT END OF PERIOD 10(b)

1 531 5 736

The statement of cash flows should be read in conjunction with the notes to the financial statements.

42

Notes to the Financial Statements for the year ended 30 June 20141. Reporting Entity

The Northern Territory Government and Public Authorities Employees’ Superannuation Fund (the fund) (ABN 67 738 128 022) is established under the Superannuation Act (as amended). The fund incorporates a member accumulation and a defined benefit component and operates for the purpose of providing benefits for or in relation to members under the Northern Territory Government and Public Authorities’ Superannuation Scheme Rules (as amended). Administration of the scheme is conducted by the Northern Territory Superannuation Office on behalf of the Trustee.

2. Basis of Preparation(a) Statement of complianceThe financial report is a general purpose report that is prepared in accordance with AAS, including AAS25, other applicable accounting standards, the requirements of the Superannuation Industry (Supervision) Act 1993 and Regulations and the provisions of the Superannuation Act as amended.International Financial Reporting Standards (IFRS) form the basis of AAS issued by the AASB. Certain requirements of AAS25 however differ from the equivalent requirements that would be applied under IFRS.The financial statements were approved by the Trustee on 26 September 2014.(b) Basis of measurementThe financial statements are prepared on a net market value basis.(c) Functional and presentation currencyThe financial statements are presented in Australian dollars, which is the functional currency of the scheme.Amounts have been rounded to the nearest thousand dollars except where otherwise noted.(d) Use of estimates and judgementsThe preparation of financial statements requires the Trustee to make judgements, estimates and assumptions that affect the application of accounting policies and reported amounts of assets and liabilities, income and expenses. Actual results may differ from these estimates.Estimates and underlying assumptions are viewed on an ongoing basis. Revisions to accounting estimates are recognised during the period in which the estimate is revised and in any future periods affected.There are no critical accounting estimates and judgments contained in these financial statements other than those used to determine the liability for accrued benefits, which are not brought to account but disclosed by way of note. The following significant accounting policies have been adopted in the preparation and presentation of the financial report.

3. Significant Accounting PoliciesThe accounting policies set out below have been applied consistently in these financial statements.(a) Assets

43