2012 north bridge future of open source study

TRANSCRIPT

OPENThe Open Source Leadership

Panel at OSBC May 21, 2012

SOURCE

THE FUTURE OF

2012

FUTURE OF OPEN SOURCE 2012

THE LEADERSHIP PANEL

Gil YehudaDir. of Open Source

and Open Standards

@gyehuda

Michael SkokGeneral Partner

@mjskok

Tim YeatonCEO

@black_duck_sw

Tom EricksonCEO

@tom_eric

Ryan GarnerVP, Dir.-to-Consumer

Services

@ryanTgarner

2

FUTURE OF OPEN SOURCE 2012

AGENDA

Markets

Community

Investment & Innovation

3

LOOK FOR LIVE VOTING!

FUTURE OF OPEN SOURCE 2012

OPEN SOURCE COLLABORATORS

4

FUTURE OF OPEN SOURCE 2012

SURVEY RESPONSES

5

FUTURE OF OPEN SOURCE 2012

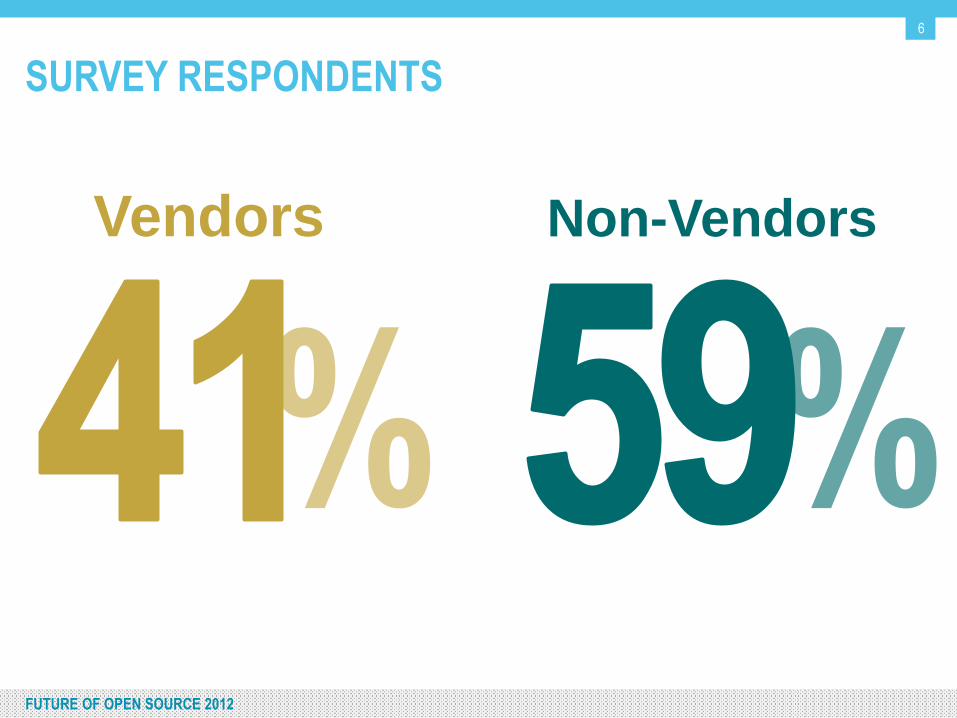

SURVEY RESPONDENTS

Vendors Non-Vendors

6

FUTURE OF OPEN SOURCE 2012

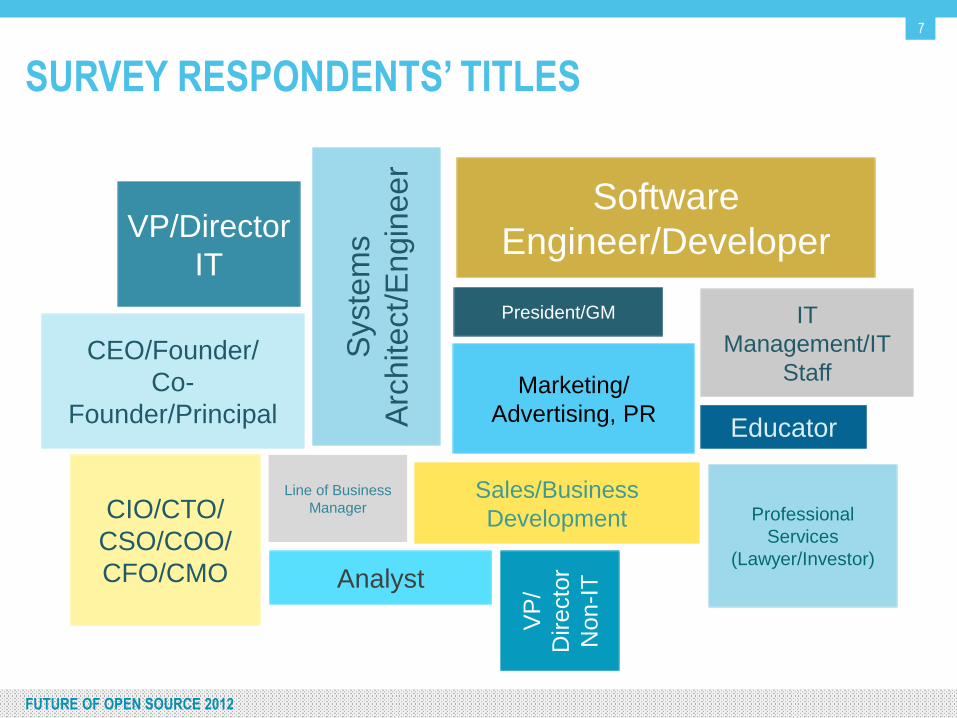

SURVEY RESPONDENTS’ TITLES

7

Marketing/

Advertising, PR

VP/Director

IT

IT

Management/IT

StaffS

yste

ms

Arc

hitect/E

ngin

eer

Professional

Services

(Lawyer/Investor)

CIO/CTO/

CSO/COO/

CFO/CMO Analyst

Educator

CEO/Founder/

Co-

Founder/Principal

President/GM

Software

Engineer/Developer

Sales/Business

DevelopmentV

P/

Directo

r

Non-I

T

Line of Business

Manager

FUTURE OF OPEN SOURCE 2012

AGENDA

Markets

Community

Innovation & Investment

8

FUTURE OF OPEN SOURCE 2012

OSS DEPLOYED IN YOUR ORGANIZATION

9

Open Source deployment is reaching a

tipping point

Open source deployment

has reached >75%

Open source will make up

51%–75% of deployment

FUTURE OF OPEN SOURCE 2012

VENDORS VS. NON-VENDOR COMPANIES

OSS DEPLOYMENT IN 5 YEARS

OSS as a % of Deployed Code

0%

10%

20%

30%

40%

50%

Over 75% 51%-75% 26%-50% Up to 25%

% o

f R

esp

on

ses

Vendor

Non Vendor23%

45%

31%29%

14%

30%

18%

10%

10

FUTURE OF OPEN SOURCE 2012

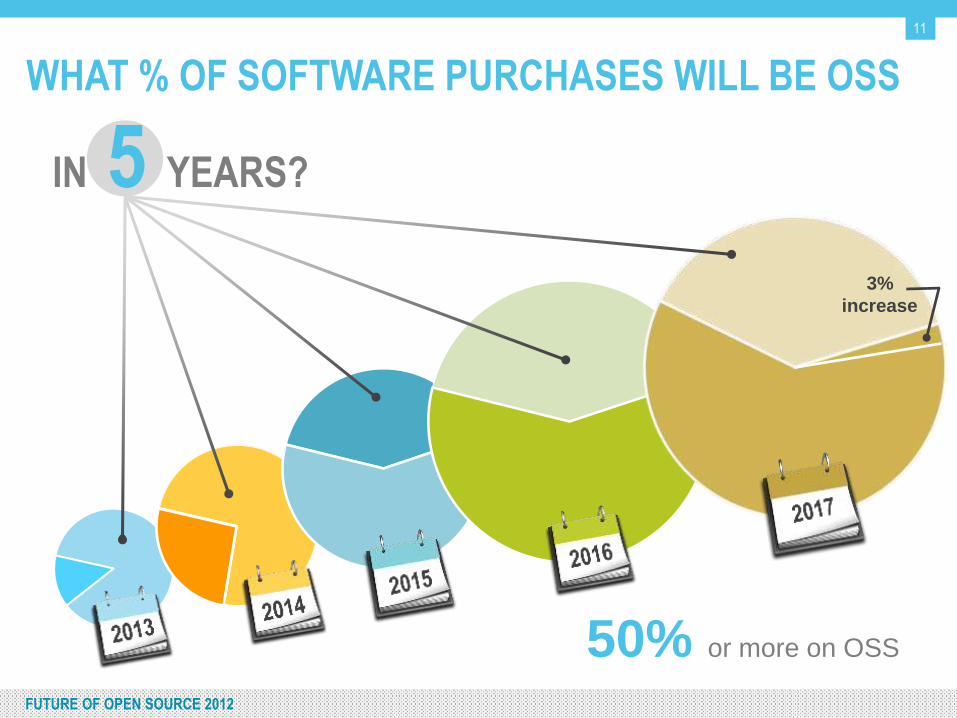

3%

increase

WHAT % OF SOFTWARE PURCHASES WILL BE OSS

50% or more on OSS

IN 5 YEARS?

11

FUTURE OF OPEN SOURCE 2012

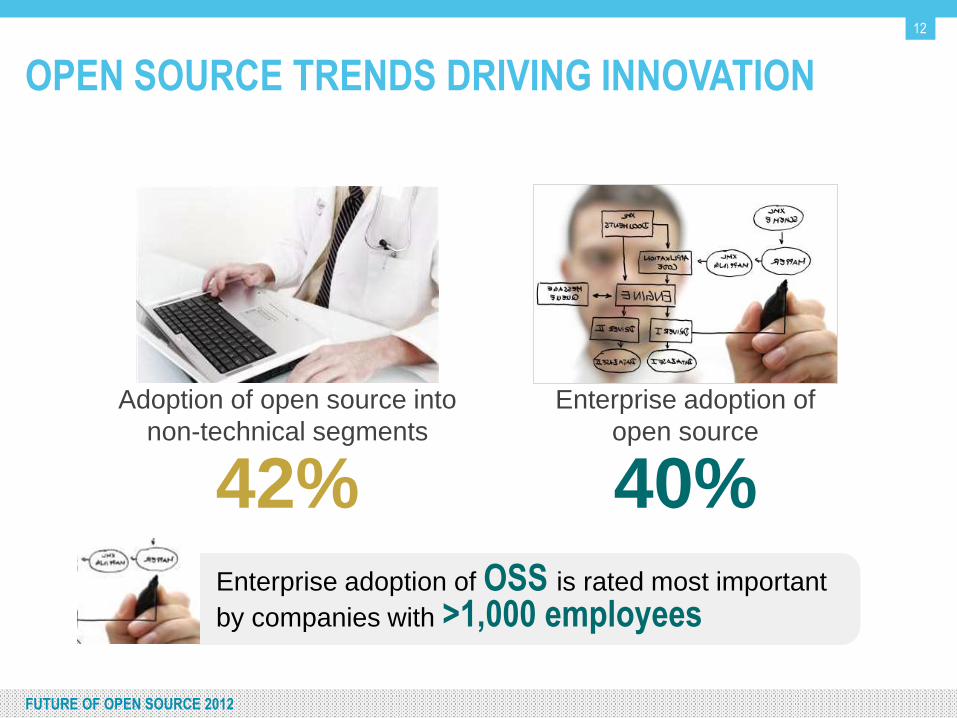

OPEN SOURCE TRENDS DRIVING INNOVATION

Enterprise adoption of OSS is rated most important

by companies with >1,000 employees

Adoption of open source into

non-technical segments

42%

Enterprise adoption of

open source

40%

12

FUTURE OF OPEN SOURCE 2012

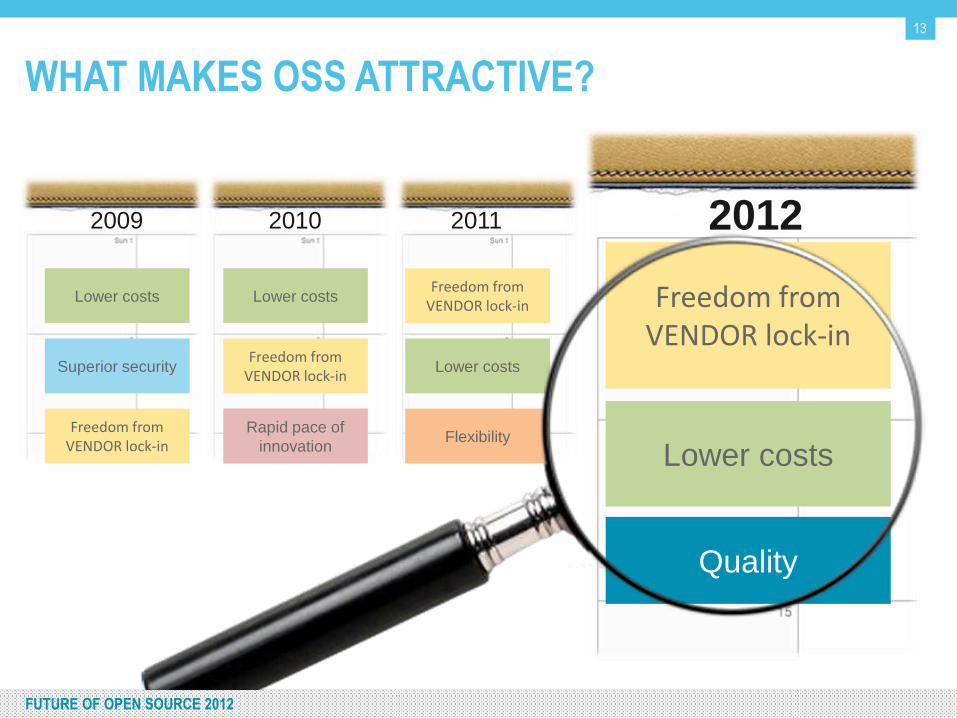

WHAT MAKES OSS ATTRACTIVE?

2009

Lower costs

Superior security

Freedom from VENDOR lock-in

2010

Lower costs

Rapid pace of

innovation

Freedom from VENDOR lock-in

2011

Lower costs

Flexibility

Freedom from VENDOR lock-in

2012

Lower costs

Quality

Freedom from VENDOR lock-in

13

FUTURE OF OPEN SOURCE 2012

TOP BARRIERS TO OPEN SOURCE SELECTION

48%

47%

35%

14

FUTURE OF OPEN SOURCE 2012

12%Financial Services

23%Health/Medical/Life

Sciences

INDUSTRIES MOST IMPACTED BY OSS IN 2012

15

44%Data

Management

FUTURE OF OPEN SOURCE 2012

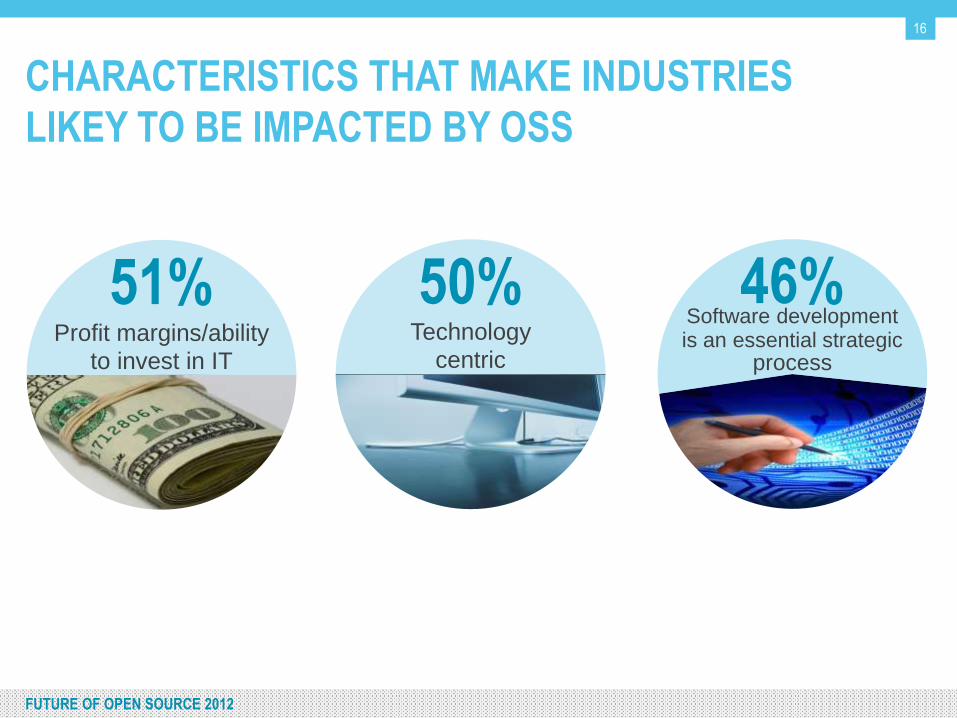

CHARACTERISTICS THAT MAKE INDUSTRIES

LIKEY TO BE IMPACTED BY OSS

16

Profit margins/ability

to invest in IT

51% 50%Technology

centric

46%Software development is an essential strategic

process

FUTURE OF OPEN SOURCE 2012

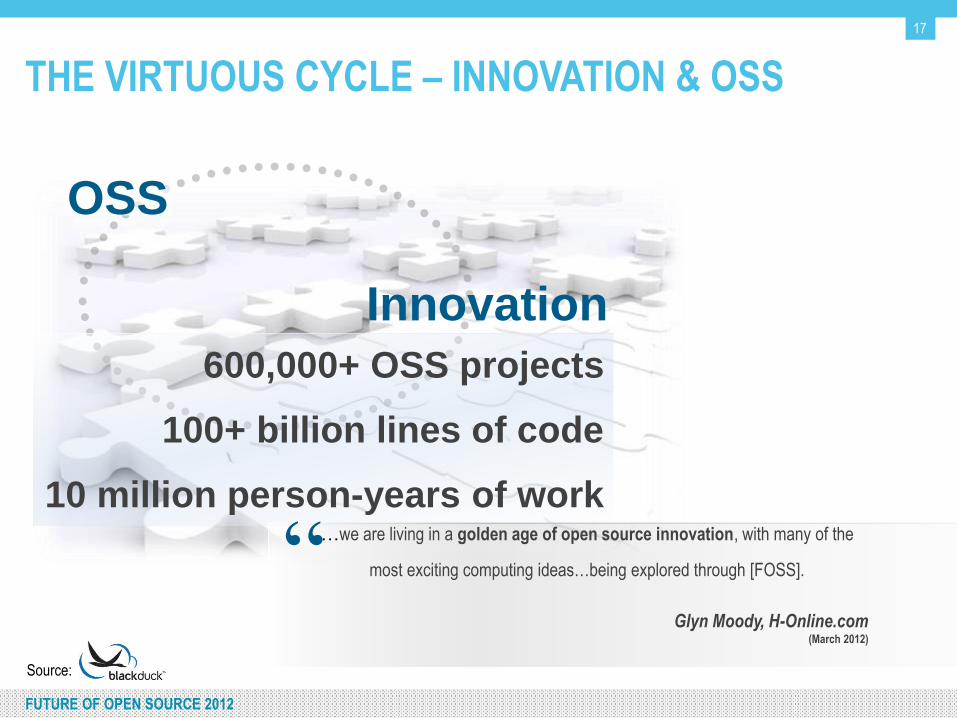

THE VIRTUOUS CYCLE – INNOVATION & OSS

OSS

Innovation

600,000+ OSS projects

100+ billion lines of code

10 million person-years of work…we are living in a golden age of open source innovation, with many of the

most exciting computing ideas…being explored through [FOSS].

Glyn Moody, H-Online.com(March 2012)

“Source:

17

FUTURE OF OPEN SOURCE 2012

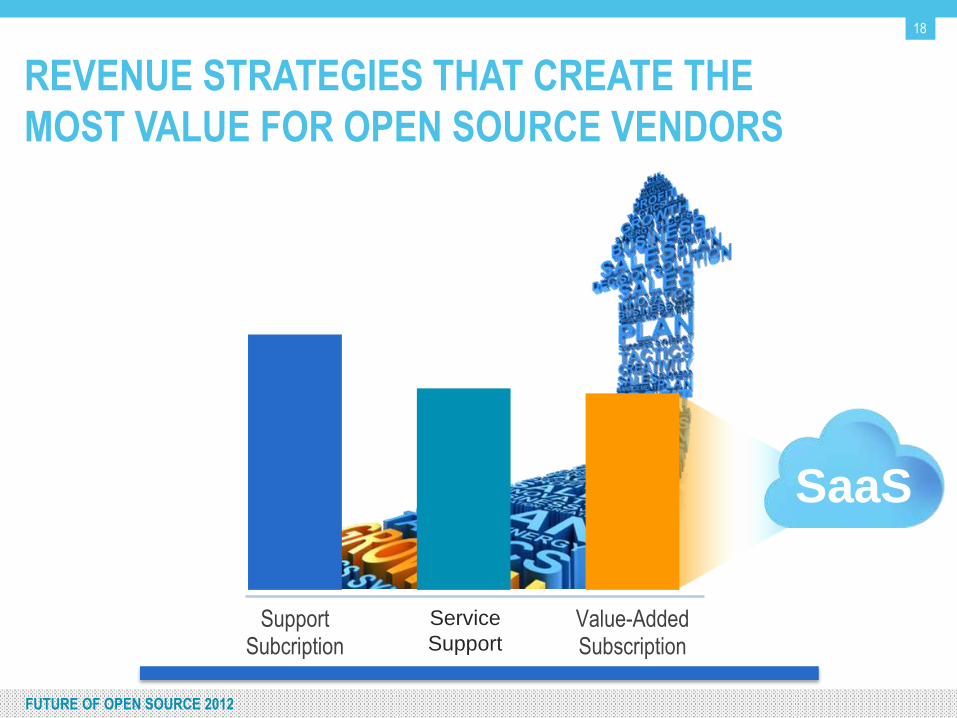

REVENUE STRATEGIES THAT CREATE THE

MOST VALUE FOR OPEN SOURCE VENDORS

18

SaaS

52%

41% 40%

SupportSubcription

Service Supprt Value-AddedSubscription

Service

Support

FUTURE OF OPEN SOURCE 2012

AGENDA

Markets

Community

Innovation & Investment

19

FUTURE OF OPEN SOURCE 2012

OSS PROJECTS

20

Project maturity 43%

Availability of

commercial support 23%

Size of

community 19%

FACTORS INFLUENCING CHOICE OF OSS PROJECTS

FUTURE OF OPEN SOURCE 2012

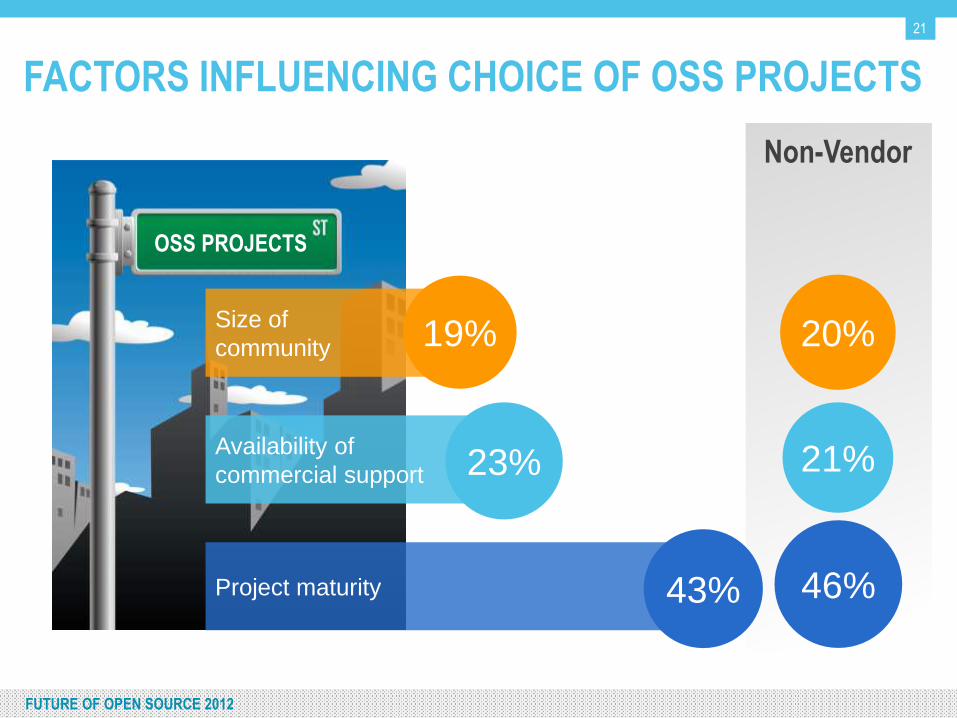

Non-Vendor

OSS PROJECTS

21

Project maturity 43%

Availability of

commercial support 23%

Size of

community 19%

FACTORS INFLUENCING CHOICE OF OSS PROJECTS

46%

21%

20%

FUTURE OF OPEN SOURCE 2012

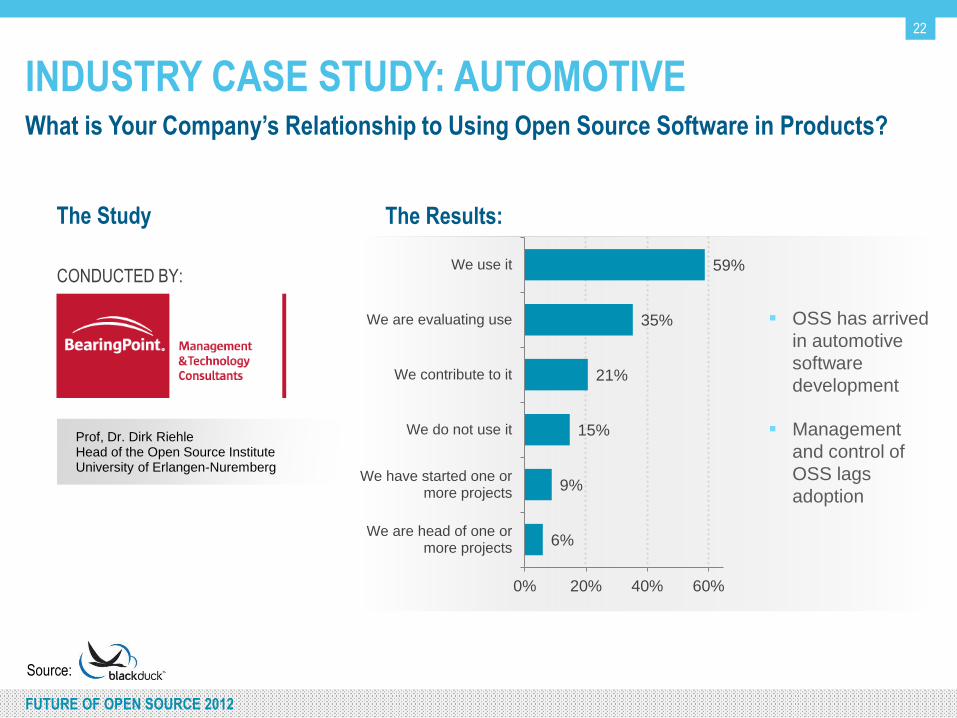

INDUSTRY CASE STUDY: AUTOMOTIVEWhat is Your Company’s Relationship to Using Open Source Software in Products?

22

Source:

Prof, Dr. Dirk RiehleHead of the Open Source InstituteUniversity of Erlangen-Nuremberg

CONDUCTED BY:

6%

9%

15%

21%

35%

59%

0% 20% 40% 60%

We are head of one ormore projects

We have started one ormore projects

We do not use it

We contribute to it

We are evaluating use

We use it

The Results:

OSS has arrived

in automotive

software

development

Management

and control of

OSS lags

adoption

The Study

FUTURE OF OPEN SOURCE 2012

HIRING: WHAT ASPECT OF OSS EXPERIENCE IS

MOST IMPORTANT?

23

Experience

with a variety

of projects

35%

Code

contributions

28%

FUTURE OF OPEN SOURCE 2012

AGENDA

Markets

Community

Innovation & Investment

24

FUTURE OF OPEN SOURCE 2012

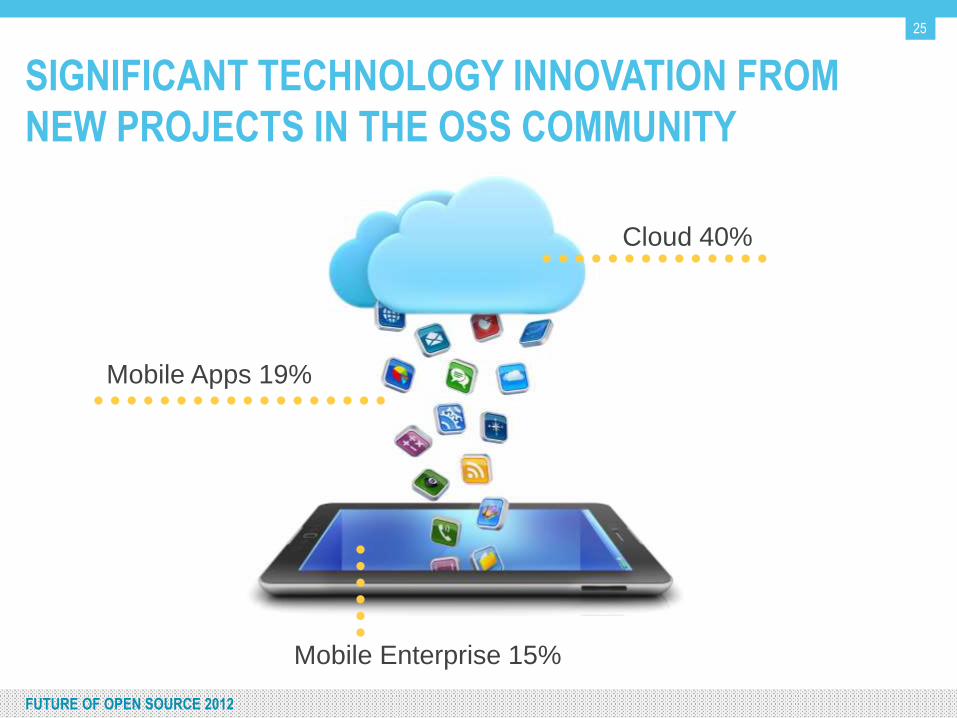

SIGNIFICANT TECHNOLOGY INNOVATION FROM

NEW PROJECTS IN THE OSS COMMUNITY

25

Cloud 40%

Mobile Apps 19%

Mobile Enterprise 15%

FUTURE OF OPEN SOURCE 2012

Android gaining momentum,

share > 70%

iOS share declined, but number

of projects increased

OPEN SOURCE DRIVES MOBILE INNOVATION

26

Source:

New Mobile OSS Projects

>18,000 cumulative

projects

10,000 new in 2011

alone!

Share of Projects*

* Based on OSS projects that specify a mobile platform

FUTURE OF OPEN SOURCE 2012

48.5% 63.3%

1.4%

49%

OSS INVESTMENTS BY THE NUMBERS

Dollars

Invested

Deals

Completed

Avg. Deal

Size

Seed,

Series A

$452.8M 73 $6.8M $118.7M

$674.9m

72

$10.1M $192.7M

2010

2011

27

FUTURE OF OPEN SOURCE 2012

201220112010

HOT OSS COMPANIES

28

FUTURE OF OPEN SOURCE 2012

= Growth

Quality Innovation

29

FUTURE OF OPEN SOURCE 2012

WITH GROWTH COMES…

30

Revenue

Super-

Communities

Enterprise

Adoption

FUTURE OF OPEN SOURCE 2012

THANK YOU! OPEN SOURCE COLLABORATORS

31

FUTURE OF OPEN SOURCE 2012

FIND OUT MORE

32

http://www.northbridge.com/open-source http://www.opensourcedelivers.com/