2012-06-29 cord.si (s&p capital i) cordlife initiation

DESCRIPTION

2012-06-29 CORD.SI (S&P Capital I) Cordlife initiation.pdfTRANSCRIPT

This report is for information purposes and should not be considered a solicitation to buy or sell any security. Neither Standard & Poor’s nor any other

party guarantees its accuracy or makes warranties regarding results from its usage. Redistribution is prohibited without written permission. Copyright ©

2012. All required disclosures and analyst certification appears on the last 3 pages of this report. Additional information is available on request.

June 29, 2012

Cordlife Group Initiation Banking for the future

Strong market position in Singapore and Hong Kong. Cordlife is the

market leader in private cord blood banking in Singapore and is

among the top three players in Hong Kong. The group’s strong market

position and reputation will enable it to benefit from growing demand

for cord blood banking services.

Expanding prospects. Cordlife plans to leverage on its established

brand and market leadership to grow its position further in existing

markets. To this end, it will intensify marketing activities to promote

awareness towards the benefits of cord blood banking and will

increase its capacity through new proposed headquarters and

facilities at Yishun A’Posh Bizhub. The company also intends to

diversify into complementary services such as offering umbilical cord

tissue banking in Singapore and will grow through accretive

acquisitions in selected markets.

Higher penetration rate to drive industry growth. While the number

of resident births in Singapore and Hong Kong are expected to remain

stable over the next few years, the deepening of penetration rates in

both the markets will drive demand for cord blood banking.

Higher revenue for 9MFY12 (Jun.), margin under pressure.

Cordlife’s 9MFY12 net profit declined to SGD4.6 mln (-25.4%YoY)

mainly a result of: (i) lower gross margin attributed to higher cost of

testing brought by a change in the AABB standards; and (ii) higher

administration costs from IPO and director fees. The group announced

an interim net DPS of SG1.8 cents and a special DPS of SG0.2 cents.

Key Fundamentals

FYE Jun. 30 Jun-09 Jun-10 Jun-11Revenue 22.6 28.2 25.7 EBIT 7.1 8.4 7.2 EBITDA Margin % 32.6 31.3 30.3 Net Income 6.2 8.3 8.5 Basic EPS (SG cents)* 2.66 3.55 3.64 Price/Earnings (x) 19.4 14.5 14.1 EPS Growth % N.A. 33.7 2.47 DPS (SG cents) N.A. N.A. N.A.Dividend yield % N.A. N.A. N.A.Price/Book value (x)* 4.45 3.63 2.95 Return on equity % N.A. 27.6 23.0 Return on assets % N.A. 16.3 14.8 Total Debt:Equity % 3.8 2.7 2.1 Source: Company data, S&P Capital IQ *Based on 232.7 mln post IPO shares in issue

GICS: Healthcare/Healthcare Equipment and Services

Business Summary: Cordlife Group Ltd, an investment holding company, provides cord

blood banking and umbilical cord tissue banking services.

Country of Incorporation: Singapore

Head Office Location: 61 Science Park Road, No. 05-16/17/18, The Galen Singapore

Science Park II, Singapore 117525.

Place of Operation: Singapore, Hong Kong and Shenzhen

Website: www.cordlife.com

IR Contact: Ms. Dolores Phua | [email protected]

| +65-6534 5122

CURRENT PRICE:

SGD0.515

Lau Seu Yee/Lee Wee Sieng

Equity Analyst

65 6239 6391

Key statistics

52-week Price Range 0.80 / 0.43Avg Vol - 12 months ('000 shares) 2,232.5Price performance (%) - 1 month 15.7

- 3 month N.A.- 12 month N.A.

No. of Outstanding shares (mln) 232.7Free Float (%) 61.6

Market Cap (SGD mln) 119.8Enterprise value (SGD mln) 88.2

Major shareholders (%)China Stem Cells (East) Co Ltd 10.5

City Challenge Global Ltd 9.4Coop International Pte Ltd 8.8

Source: Company data, S&P Capital IQ

2

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Share Price Performance

Cordlife Group Share Price Chart

Source: S&P Capital IQ

There is limited share price history since Cordlife was recently listed (on Mar. 29,

2012). As such, we can only compare its one-month share price performance with

the STI and its peers.

Comparative Performance

Cordlife GroupFTSE Straits Times Index

China Cord Blood Corp. Stemlife Bhd Bionet Corp.

1 Month 15.73% 2.14% -1.14% 5.95% 26.91%3 Month N.A. -5.61% -6.81% 56.14% 13.29%6 Month N.A. 6.77% 20.37% 56.14% 22.24%Source: S&P Capital IQ

Share Price Performance Details

Current Price 0.515 52-week Hi/Low 0.80/0.43 10-day Avg Volume (mln) 4.10427 Price 1 Month Ago 0.445 1 Month Price Performance 15.73% Price 3 Months Ago N.A. 3 Month Price Performance N.A. Price 6 Months Ago N.A. 6 Month Price Performance N.A. Price 12 Months Ago N.A. 12 Month Price Performance N.A. Market Capitalization (SGD mln) 119.8 Beta N.A.

Source: S&P Capital IQ

0.40

0.50

0.60

0.70

0.80

Price 30 Day Moving Average

0306090120150180

29‐Mar 8‐Apr 18‐Apr 28‐Apr 8‐May 18‐May 28‐May 7‐Jun 17‐Jun 27‐Jun

Volume Vol ('mln)

Price (SGD)

3

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Financial Performance

Recent interim performance: Cordlife’s 9MFY12 (Jun.) net profit dropped 25.4%

YoY to SGD4.6 mln in spite of 14.2% YoY increase in total revenue. The higher

revenue was attributed to: (i) an increase in the provision of cord blood banking

services driven by a rise in the number of client deliveries, from about 4,900 in

9MFY11 to 5,300 in 9MFY12; and (ii) provision of new cord tissue banking services

in Hong Kong which commenced in March 2011.

The group’s profitability was however, weakened by a lower gross margin of

68.8% (-2.1%-pts) as a result of increase in cost of testing brought about by a

change in the AABB standards. In addition, margins were affected by higher

administrative expenses (+76.8% YoY) due to IPO expenses and increase in

headcount and director fees. This was partially offset by higher associate’s

income of SGD1.4 mln (+32.3% YoY) due to the growth of Guangzhou Tianhe

Nuoya’s business as new customers signed up each year.

Cordlife’s balance sheet remains healthy as at 9MFY12 with minimal total debt to

equity ratio of about 3%. As at end-9MFY12, total borrowings increased to about

SGD2.0 mln (from SGD0.8 mln end-FY11). Given this is matched by a healthy cash

& cash equivalents of SGD33.6 mln (an increase of 742% from FY11 level), the

group remains in net cash position in 9MFY12. Operating cash flow remains

positive while listing proceeds help add to the overall increase in cash and

equivalents. The additional loan drawn down is to finance the A’Posh Bizhub

property which is presently under construction.

Detailed Profit & Loss

SGD mln Fiscal Nine Months Ending Mar-12 Mar-11 YoY (%) Revenue 21.3 18.7 14.2 Cost of sales (6.6) (5.4) 22.5 Gross profit 14.7 13.2 10.8 Gross profit margin 68.8% 70.9% Other operating income 0.1 0.3 (72.0) Selling and marketing expenses (4.9) (4.2) 16.6 Administrative expenses (6.9) (3.9) 76.8 Profit from operations/EBIT 2.9 5.4 (45.8) EBIT margin 13.7% 28.8% Share of results in associate 1.4 1.1 32.3 Finance income 1.0 0.8 29.5 Finance costs (0.0) (0.0) (97.5) Profit before tax 5.4 7.2 (25.4) PBT Margin 25.3% 38.7% Income tax (0.8) (1.0) (25.1) Effective tax rate 14.3% 14.3% Net profit attributable to equity holders 4.6 6.2 (25.4) As reported EPS (SG cents) 1.98 2.66 (25.4) Share capital (mln) 232.7 232.7 Weighted share capital (mln) 232.7 232.7 Source: Company data, S&P Capital IQ Research

4

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Income Statement (SGD mln)

FYE June 30 2009 2010 2011 Total Revenue 22.6 28.2 25.7 Growth Over Prior Year N.A. 24.7% -8.8% Gross Profit 16.4 20.5 18.3 Margin % 72.6% 72.8% 71.1% EBITDA 7.4 8.8 7.8 Margin % 32.6% 31.3% 30.3% EBIT 7.1 8.4 7.2 Margin % 31.4% 29.9% 28.1% Earnings from Cont. Ops. 6.5 8.4 8.5 Margin % 29.0% 29.9% 33.0% Net Income 6.2 8.3 8.5 Margin % 27.4% 29.4% 33.0% Basic EPS* 2.7 3.6 3.6

Key Growth and Fundamental Ratios

FYE June 30 2009 2010 2011 EPS Growth (%) N.A. 33.7 2.6 Sales Growth (%) N.A. 24.7 -8.8 Asset Turnover (x) N.A. 0.6 0.5 Inventory Turnover (x) N.A. 32.9 31.1 Receivables Turnover (x) N.A. 3.4 3.6 Effective Tax Rate (%) 15.2 15.4 14.7 Total Debt to Equity (%) 3.8 2.7 2.1 Interest Coverage (x) 283.5 183.0 167.7 Quick Ratio (x) 1.8 0.9 1.4 Current Ratio (x) 2.1 1.0 1.6 Payout Ratio (%) 0.0 0.0 0.0 Debt to Capital (%) 3.7 2.6 2.0

Balance Sheet (SGD mln)

FYE June 30 2009 2010 2011 Current Assets 24.5 21.0 12.9 Fixed Assets 0.8 2.0 4.3 Other LT Assets 17.5 35.8 38.2 Total Assets 42.7 58.8 55.4 Current Liabilities 11.8 21.2 8.0 Total Liabilities 14.5 25.8 14.8 Share capital 25.7 25.7 25.7 Shareholder's Equity 28.3 33.0 40.6 Cash and Cash Equivalents 7.0 8.2 4.0 Total Debt 1.1 0.9 0.8 Net Cash/(Debt) 5.9 7.3 3.2

Cash Flow (SGD mln)

FYE June 30 2009 2010 2011 Cash from Operations 3.8 8.3 8.0 Capital Expenditure (0.4) (1.6) (3.1) Cash from Investing (3.2) (16.2) (4.4) Total Debt Issued 1.9 9.5 5.4 Total Debt Repaid (0.6) (0.0) (12.6) Cash from Financing 1.3 9.5 (7.3) Change in Cash 2.0 1.4 (3.3) Cash flow per share (SG cents)* 1.6 3.6 3.5 Source: Company data, S&P Equity Research estimates * Based on 232.7 mln post IPO shares in issue

5

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Industry Characteristics and Outlook

Summary: Cord blood banking is a consolidated industry in Singapore and Hong

Kong (Cordlife’s two key markets) dominated by a few key players and has

relatively high entry barriers. Demand for cord blood banking is dependent on: (i)

number of births and (ii) public acceptance of cord blood banking. The number of

births for Singapore and Hong Kong residents has been relatively stable in the

past five years and will likely remain flat in the next few years. The key

uncertainty in the Hong Kong market lies with a potential ban in mainland PRC

expectant mothers giving birth in Hong Kong. Nevertheless, the growth in cord

blood banking is expected to be driven by an increase in penetration rate in the

respective markets helped by increasing public acceptance of cord blood banking.

Brief description of cord blood banking: Cord blood banking involves the

processing, testing, cryopreservation and storage of umbilical cord blood which

is collected at birth. Stem cells from cord blood can be used to treat diseases

such as leukaemia, cerebral palsy, blood and immune system disorders.

Key revenue drivers: Cordlife’s revenue is mainly driven by its storage volume of

cord blood banking which is determined by: (i) number of births; (ii) penetration

rate of cord blood banking; and (iii) its market share.

The number of new births in a country will directly dictate the overall market size

of cord blood banking industry in the country. In Singapore, the number of births

was relatively stable in the past five years averaging 39,301 (CAGR of 0.7% during

2006-2011). Going forward, Deloitte & Touche Financial Advisory Services

(DTFAS) expect the Singapore births growth to remain fairly flat. In Hong Kong,

the number of births has been increasing at a steady rate (CAGR of 7.8%) during

2006-2011, growing to 95,400 in 2011 from 65,600 in 2006. The growth in births

was driven by an influx of mainland PRC expectant mothers which increased to

43,982 in 2011 from 26,132 in 2006. In recent news, the chief executive-elect

proposed a ban on mainland women giving birth in Hong Kong from 2013 which

may adversely affect the potential market for cord blood banking in Hong Kong.

In contrast, the annual birth numbers among Hong Kong residents have been

relatively stable, ranging from 43,000 to 49,000 in the past few years and is

expected to remain stable over the next few years.

Singapore and Hong Kong total live births and YoY growth (2006-2011)

Source: Singapore Department of Statistics, Census and Statistics Department – Hong Kong SAR

Singapore

05,000

10,00015,00020,00025,00030,00035,00040,00045,00050,000

2006 2007 2008 2009 2010 2011-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Total Births

Total Births YoY

Hong Kong

010,00020,00030,00040,00050,00060,00070,00080,00090,000

100,000

2006 2007 2008 2009 2010 2011-12.0%

-9.0%

-6.0%

-3.0%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

Total Births

Total Births YoY

6

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Penetration rate of private cord blood banking is measured as annual incremental

units of cord blood stored in private banks divided by annual number of new

births. Factors influencing the penetration rate in a particular market include: (i)

public awareness and acceptance; (ii) favorable regulatory environment and

Government subsidies; and (iii) cord blood applications and potential uses.

According to DTFAS, Singapore is a relatively mature cord blood banking market

with a penetration rate of 24% in 2010 and a CAGR of 16% during 2007-2010. The

strong CAGR was partly due to a government subsidy of 50% of the collection fee

through “child development co-saving” scheme. Looking forward, DTFAS expects

penetration rate of private cord blood banking market in Singapore to grow to

38% in 2015 with a CAGR of around 9% for 2011-2015.

In Hong Kong, the penetration rate was estimated to be 11.5% in 2010 and a

CAGR of 15% during 2007-2010. DTFAS projected penetration rate to increase to

20.6% in 2015 with a CAGR of 10% for 2011-2015, helped by higher visibility of

cord blood banking.

Singapore and Hong Kong Penetration Rate and Incremental Storage Volume in

Private Sector (2007-2015F)

Source: DTFAS Market Research

While total new births combined with penetration rate will determine the size of

cord blood banking industry in the respective country, Cordlife’s market share

will determine the firm’s storage volume which directly drives its revenue stream.

Cordlife had an estimated market share of around 62% and 28% of the Singapore

and Hong Kong private cord blood banking market respectively in 2010.

Competitive Landscape and Pressure

The cord blood banking industry in Singapore and Hong Kong is consolidated and

has relatively high entry barriers such as cord blood banking licensing, reputation

and networking with hospitals. In Singapore, there are only three cord blood

banks: one public (Singapore Cord Blood Bank) and two private (Cordlife and

StemCord). Both the private blood banks began operations in Singapore in the

early 2000s. Cordlife is the larger player with market share of 62% and storage

capacity of 60,000 units. StemCord has market share of 38% and storage capacity

of 40,000 units.

Singapore

0

2000

4000

6000

8000

10000

12000

14000

16000

2007 2010 2015F0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Incremental storage vol. (private) Penetration rate (private)

Hong Kong

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2007 2010 2015F0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Incremental storage vol. (private) Penetration rate (private)

7

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

In Hong Kong, the top three players (Cordlife, Cryolife and Healthbaby) accounted

for more than 90% in terms of incremental and cumulative storage volume in the

private sector. Cyrolife had the most cumulative storage units, but less

incremental storage units than Healthbaby and Cordlife in 2010. Healthbaby had

the highest annual incremental storage units, followed by Cordlife. Healthybaby,

Cordlife and Cyrolife are estimated to have 45%, 28% and 23% of market share (in

terms of incremental storage), respectively in 2010.

Pricing structure

The following two tables highlight the pricing structure of key private cord blood

banks in Singapore and Hong Kong.

Pricing structure of key private cord blood banks in Singapore and Hong Kong

Private cord blood banks - Singapore Private cord blood banks - Hong Kong

Collection fee or

one-time fee Annual storage fee Storage period

Collection fee or

one-time fee Annual storage fee Storage period

Cordlife Option (i) SGD1,950 SGD250 21 years Cordlife Option (i) HKD19,000 HKD1,500 18 years

Option (ii) SGD4,200 SGD250 (from year 11 ) 21 years Option (ii) HKD23,500 HKD1,500 (from year 5 ) 18 years

Option (iii) SGD6,200 No annual fees 21 years Option (iii) HKD29,500 HKD1,500 (from year 10 ) 18 years

Option (iv) HKD36,000 No annual fees 18 years

Stemcord SGD1,580 SGD275 5 years or more

Usually 21 years Cyrolife Option (i) HKD37,400 No annual fees 18 years

Option (ii) HKD41,500 No annual fees 23 years

Option (iii) HKD45,380 No annual fees 28 years

Healthbaby HKD38,000 No annual fees 18 years

Source: DTFAS Market Research, Company website

Key Operating Costs

Cordlife’s key operating costs are: (i) cost of sales, (ii) selling & marketing

expenses and (iii) administrative expenses. The cost of sales relates to expenses

incurred in processing and storage of cord blood and includes costs of various

tests carried out, direct labour & material costs and overheads such as laboratory

and storage rental expenses. Cost of sales accounted for 27.2%, 28.9% and 31.2%

of revenue for FY10, FY11 and 9MFY12, respectively. The increase in cost of sales

in 9MFY12 was partly due to higher cost of additional blood testing required to

meet a change in AABB standards.

Selling & marketing expenses include advertising and promotion expenses,

marketing staff salaries and commission expenses. It accounted for 20.1%, 22.9%

and 23.1% of revenue for FY10, FY11 and 9MFY12, respectively. Administrative

expenses include salaries of administrative and finance staff, rental expenses,

consultancy expenses and depreciation of office equipment. It accounted for

23.3%, 21.6% and 32.3% of revenue for FY10, FY11 and 9MFY12, respectively. The

higher administrative expenses in 9MFY12 were mainly due to the one-off IPO

expenses of SGD1.3 mln incurred in 3QFY12.

8

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Breakdown of key operating costs and margin for FY10, FY11 and 9MFY12

FY10

27.20%

20.10%

23.30%

29.40%

FY11

28.90%

22.90%21.60%

26.60%

Cost of sales Selling & marketing expenses Administrative expenses Operating margin

9MFY12

31.20%

23.10%

13.40%

32.30%

Source: Company data

Key Risks

Regulatory risks: Cord blood banking industry is regulated by the respective

countries’ health authorities and global accreditation bodies. Any adverse

changes in regulatory policies, guidelines or requirements may impact the

industry. For example, a change in blood testing requirements by AABB resulted

in a cost increase of SGD120 per cord blood unit. In addition, a ban or significant

reduction in quota for mainland PRC mothers giving birth in Hong Kong will

reduce its potential market in Hong Kong.

Technology and alternative medical treatment risks: Future medical or

technological advances may render cord blood banking irrelevant. Although it is

currently possible to collect stem cells from other bodily sources such as bone

marrow, it involves surgical procedures and may potentially cause side effects. If

medical advances enable cheaper or more effective ways to collect and store

stem cells, cord blood banking may be made redundant. New medical treatments

superior to the use of cord blood in medical treatment may also eliminate the

need for cord blood banking.

Reputation risks: Any inadequacies or problems with Cordlife’s cord blood

banking services or the cord blood banking industry in general resulting in bad

publicity or tarnishing of reputation will decrease the demand for its cord blood

banking services.

Credit risks associated with instalment customers: Cordlife is exposed to delay

or default on payments by its customers who are on annual payment options. Its

annual payment customers accounted for 40.3% and 39.2% of its total customers

in FY10 and FY11, respectively. Nevertheless, the default rates had been low at

0.1% and 0.2% of its total customers in FY10 and FY11, respectively.

Foreign exchange risks: As Cordlife has significant operations in Hong Kong, it

is exposed to foreign exchange translation risk as its reporting currency is in

SGD. 28.0% and 25.2% of its total revenue in FY10 and FY11, respectively were

denominated in HKD.

9

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Cordlife’s Growth Strategy

Cordlife will continue to leverage on its established brand, expertise and market

leadership to grow its core business in Singapore and Hong Kong. To this end, it

intends to intensify certain marketing activities which are aimed at promoting

awareness towards the benefits of cord blood banking in these markets. It will

also be increasing its current capacity and the recently acquired 22,000 sq.ft.

space in A’Posh Bizhub in Yishun will enable storage of up to about 650,000 cord

blood units when completed by year-end. Cordlife’s key growth plans include the

following:

Capitalise on strategic investment in the PRC for growth in Hong Kong

For growth in Hong Kong, Cordlife will continue to capitalise on its co-marketing

arrangement with China Cord Blood which gives it access to PRC expectant

mothers in Beijing, Guangdong and Zhejiang provinces who intend to deliver in

Hong Kong. For 2012, the Hong Kong government has set a quota of 31,000

places in maternity wards for mainland women in private hospitals and 3,400 in

public hospitals in response to public pressure. The management believes that in

the event if the government bars mainland Chinese women from giving birth in

Hong Kong, the company’s strong brand, track record and rising public

awareness of cord blood banking should help weather this potential change in

government regulations. In addition, the ban - if imposed - will not apply to

mainland Chinese women married to Hong Kong residents.

Leverage on expanded clinical use

As medical development expands the therapeutic utility of cord blood banking,

the perceived value of cord blood banking will be enhanced. The company

actively keeps abreast of research in the area of clinical utility of cord blood and

seeks to update it customers on these developments on a periodic basis.

Diversify into secondary and complementary services

The company was the first to introduce the automated processing system in

Singapore and Hong Kong. It is currently exploring the possibility of offering

umbilical cord tissue banking services in Singapore and has begun discussions

with MOH in relation to the licensing requirements for the provision of such a

service. The company also intends to grow its services through collaborations, in-

licensing and strategic alliances as opposed to in-house research and

development programme, and considers Singapore an ideal place for such

activities, given the depth of public biomedical research and pro-collaboration

attitudes of research institutions.

Growth through accretive acquisitions in selected markets

Cordlife is actively seeking opportunities to broaden its service offering and

expand its geographical coverage in Asia through accretive acquisitions in

selected markets around the region. In connection with its demerger from CBB

(listed on the Australian Stock Exchange and previously known as Cygenics

Limited), the company has entered into the ROFR agreement in which it was

granted right of first refusal (“ROFR”) to acquire CBB’s business in Indonesia,

India and Philippines.

10

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Strengths

Market Leadership. According to the Market Research Report conducted by

DTFAS, the market share held by Cordlife in Singapore and Hong Kong in

2010 is approximately 62% and 28%, respectively.

Clinical Leadership. It is believed that Cordlife is one of the first private cord

blood banks in Singapore and amongst the first in Hong Kong to have issued

cord blood units stored with the company for transplants and other

therapeutic use.

Quality Leadership. Cordlife was one of the first in Singapore and amongst

the first in Asia to be accredited by AABB and have remained accredited

since 2005. Its Hong Kong facility has been certified ISO:9001 since August

2007 and was accredited by AABB in October 2011.

Technology Leadership. Cordlife was one of the first to adopt the automated

processing system in Singapore and Hong Kong and is constantly seeking to

improve services through the use of technology which will improve the utility

of the cord blood units.

Experienced Management Team. The management, led by its Executive

Director and CEO, Mr Yee Pinh Jeremy, is supported by a team of key

executives who are experienced and competent in their respective functions.

Established brand and distribution networks. Cordlife maintains

collaborative relationships or arrangements with major private hospitals and

several clinics in Singapore and Hong Kong. It also has a collaborative

agreement with China Cord Blood Corporation to market Cordlife Hong

Kong’s cord blood banking services to Chinese expectant mothers planning

to deliver their babies in Hong Kong.

Weaknesses

Dependence on the two key markets, Singapore and Hong Kong exposes

Cordlife to concentrated geographical risks markets such as adverse

economic conditions, weaker consumer confidence/spending and

unfavorable regulatory changes.

Growth of the business is dependent on the fertility level as well as

population base in its key markets, Singapore and Hong Kong. Whilst

Singapore is facing stagnating and low birth rates, Hong Kong’s birth rates

have been supported by an influx of mainland mothers. In 2011, nearly 47%

of over 95,000 newborns in Hong Kong, or about 44,000 were born to

mainland women. Of the estimated 44,000 mainland women who gave birth

in Hong Kong, 33,000 went to private hospitals. The possible ban by the Hong

Kong authorities to prevent mainland Chinese women from giving birth in

Hong Kong may affect the potential market for cord blood banking in the

country.

Industry is competitive with a few established cord blood banking service

providers already operating in the same region and there is potential influx

of new entrants. In addition, there is the choice of selecting public cord blood

banking. This leaves limited flexibility in enhancing profit margins and

passing through rising costs.

11

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Significant capital investment to keep pace with technological advances.

The evolving cord blood banking industry coupled with increasing

competition requires key capital investment to continuously enhance existing

infrastructure and keep pace with technological developments.

Management Guidance

Management remains cautiously optimistic on the forward demand for its cord

blood banking services. Despite worries on the debt crisis in Europe and

uncertainties in the economic environment, Cordlife’s management is confident

of sustaining its profitability with its strong market position and brand equity

coupled with favourable industry factors. The positive industry factors include the

following:

Singapore’s private cord blood banking is expected to keep growing. As the

larger of only two private cord blood banking service providers in Singapore,

it is in a good position to benefit from deepening penetration rates of cord

blood banking in the country. As provided in the industry section earlier, the

penetration level of private cord blood banking is expected to rise 38% by

2015 from 24% in 2010 (Source: DTFAS). With Cordlife’s larger space at its

new headquarters and facility at Yishun, A’ Posh Bizhub, this should further

entrench its leadership position in Singapore.

Similarly, Cordlife is expected to benefit from deepening penetration rates in

Hong Kong, which are expected to rise from 11.5% in 2010 to 20.6% in 2015

(Source: DTFAS). Leading players, of which Cordlife is one of the top three in

terms of market share, are driving this growth by raising the visibility of cord

blood banking. Cordlife launch of the umbilical cord tissue banking in March

2011 offers an additional service to potential customers.

The group has also benefited from its indirect 10% shareholding in

Guangzhou Tianhe Nuoya. The nationwide penetration rate for private cord

blood banks in China is expected to increase from 0.5% in 2010 to 1.4% in

2015 (Source: DTFAS).

As for the possible ban by authorities to prevent pregnant women from mainland

China from giving birth in Hong Kong, management believes that its strong

brand, solid track record and leadership position should provide it with a firm

footing to weather this potential regulatory change. Furthermore, the ban, if

imposed, will not apply to mainland Chinese women married to Hong Kong

residents. With the relatively stable annual birth numbers among Hong Kong

residents ranging from 43,000 to 49,000, this should provide a substantial pool of

potential customers.

12

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Peer Comparison

The following charts show Cordlife’s fundamental performance and valuation

ratios relative to its listed peers with similar business activities in the region.

China Cord Blood Corp is a NYSE-listed company that owns stakes in cord blood

banks in Beijing, Guangdong, Zhejiang and Shandong. Bionet Corp, a Taiwan-

listed company is engaged in cell tissue banking and cell therapy which operates

primarily in Taiwan. Stemlife, listed in Bursa Malaysia is involved in stem cell

banking and therapeutics. Cryo-Save Group listed on the NYSE Euronext

Amsterdam operates as a family stem cell bank in Europe, Asia and Africa. While

Cordlife’s listing history is short, its profitability and capital efficiency ratios

compare favourably with its peers.

Cordlife’s annual sales growth declined in FY11 due to decrease in client

deliveries caused by the leading-on effects arising from the deteriorating global

economic condition. In spite of lower revenues, Cordlife managed to register a

small growth in its EPS due to efficient cost management and higher contribution

from associate’s income. The EPS growth rates for Bionet and Stemlife were not

meaningful as the two companies swung between profits and losses in the past

few years. Cordlife has managed its costs relatively well over the past years

showing healthy profit margins compared to its listed peers. Cordlife’s balance

sheet also appears healthy with a minimal debt/equity ratio of 2.1% in FY11.

Annual Sales Growth (%) Annual EPS Growth (%)

(50)

(30)

(10)

10

30

50

2009 2010 2011

(120)

(80)

(40)

-

40

80

120

160

200

2009 2010 2011

Source: S&P Capital IQ

PER (X) Gearing (%)

On the PER valuation parameter, Cordlife has relatively short history as it was listed only in March 2012. Meanwhile, the company has a healthy balance sheet with minimal debt/equity ratio.

-

5

10

15

20

25

30

35

40

45

2009 2010 2011

Debt/Equity

-

2

4

6

8

10

2009 2010 2011

Source: S&P Capital IQ

Cordlife Group Limited(SGX:P8A)

China Cord BloodCorporation (NYSE:CO)

Bionet Corp (GTSM:1784)

Stemlife Berhad(KLSE:STEMLFE)

Cryo-Save Group N.V.(ENXTAM:CRYO)

13

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

EBITDA Margin (%) Net Profit Margin (%)

Cordlife has managed its cost relatively well, showing healthy EBITDA and net profit margins as compared to its listed peers.

(30)

(20)

(10)

-

10

20

30

40

50

2009 2010 2011

(25)

(10)

5

20

35

2009 2010 2011

Source: S&P Capital IQ

Note: For the charts above, all the companies are based on their latest FY11 results except China Cord Blood Corporation which is based on the recently released FY12 results (year-end March).

P/B vs. ROE comparisons shows that Cordlife is priced relatively attractively based on its 9MFY12 annualised results. It is trading at a reasonable P/B of 1.6x supported by an above average ROE.

P/B (x) vs. ROE (%)

2.4x, 10.1Stemlife

2.1x, 2.0Bionet

1.6x, 10.6Cordlife

1.0x, 12.2China Cord

Blood

0.7x, 4.9Cryo-Save

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

0.0x 0.5x 1.0x 1.5x 2.0x 2.5x

P/B

ROE

Source: S&P Capital IQ

Note: Given that Cordlife’s share base has increased following its recent listing, for peer comparison, we have used Cordlife’s annualised 9MFY12 results to compute P/B and ROE ratios based on the post-listing share capital and shareholders’ equity.

14

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Company Background

Cordlife is primarily involved in cord blood banking which comprises collection at

birth, processing, testing, cryopreservation and storage of umbilical cord blood

units. It also provides umbilical cord tissue banking (currently only in Hong

Kong). The group is one of the first private cord blood banks in Asia. Currently,

the group provides cord blood banking services in Singapore and Hong Kong but

has also catered to clients from Indonesia, Macau and Philippines via cooperation

agreements. In addition it has a marketing collaboration agreement with China

Cord Blood to gain access to mainland PRC expectant mothers planning to deliver

in Hong Kong. It also owns an indirect 10% stake in Guangzhou Tianhe Nuoya

which has the sole license to operate cord blood banking in Guangdong, PRC.

Cordlife was incorporated in Singapore on May 2, 2001 and received license from

Ministry of Health to operate in June 2002. The group entered Hong Kong and the

PRC markets through Cordlife Hong Kong in March 2005. Cordlife was demerged

from its holding company, CBB on Jun. 30, 2011. Subsequently it listed on the

Singapore Exchange on Mar. 29, 2012.

Currently, Cordlife has stored in excess of 35,000 cord blood units in its

processing facilities located in Singapore and Hong Kong. The group is the larger

of only two private cord blood banks in Singapore and is amongst the three

market leaders for private cord banks in Hong Kong. It is estimated to have a 62%

and 28% market share in private cord blood banking market in 2010 in Singapore

and Hong Kong respectively.

Over the years, Cordlife has received a number of awards and accreditations such

as: (i) American Association of Blood Banks (AABB) accreditation for its

Singapore and Hong Kong facilities since September 2005 and October 2011

respectively; (ii) ISO9001 certification for its Hong Kong facility since August

2007; and (iii) Top Pregnant/Baby Products Award 2011 by Pregnancy Magazine.

Cordlife’s management is led by its chief executive officer & executive director,

Mr Yee Pinh Jeremy, who has been instrumental in the development and

management of the group over the past ten years. The other executive officers in

the group are Ms Gwendolene Yeo (general manager of Singapore operations),

Ms Emily Cheung (general manager of Cordlife Hong Kong) and Ms Thet Hnin Yi

(financial controller). Ms Yeo and Ms Cheung have been with the group for more

than seven years.

15

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Shareholding Structure

Public

62%

Substantial

Shareholders

38%

Source: S&P Capital IQ

Significant Shareholders

Common Shares

Equivalent Held

% of Common Shares

Outstanding

Market Value (SGD mln)

China Stem Cells (East) Company Limited 24,366,666 10.47 12.55 City Challenge Global Limited 21,800,000 9.37 11.23 Coop International Pte. Ltd. 20,450,000 8.79 10.53

Source: Company data, S&P Capital IQ

Corporate Governance and Board of Directors

The board comprises six members, of which three are independent directors.

There is a separation of the non-executive chairman and CEO roles. Independent

directors chair key committees: audit, nominating and remuneration, and form a

majority in the audit committee (three out of three), nominating committee (two

out of three) and remuneration committee (two out of three).

Board of Directors

Name Title Date Joined

Dr Ho Choon Hou Chairman and non-executive director June 2011 Mr Yee Pinh Jeremy Executive director and chief executive officer June 2011 Ms Jin Lu Non-executive director July 2011 Mr Ho Sheng Lead independent director July 2011 Dr Goh Jin Hian Independent director July 2011 Mr Ng Tiak Soon Independent director November 2011

Source: Company data, S&P Capital IQ

16

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

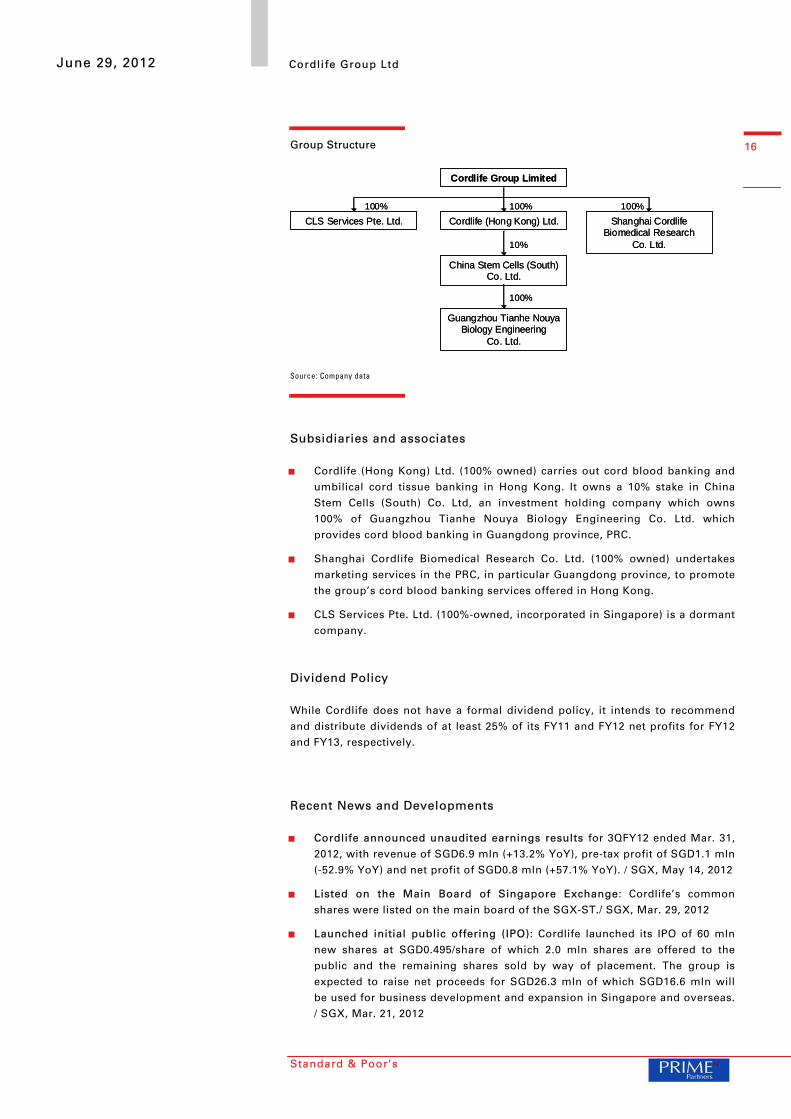

Group Structure

Source: Company data

Subsidiaries and associates

Cordlife (Hong Kong) Ltd. (100% owned) carries out cord blood banking and

umbilical cord tissue banking in Hong Kong. It owns a 10% stake in China

Stem Cells (South) Co. Ltd, an investment holding company which owns

100% of Guangzhou Tianhe Nouya Biology Engineering Co. Ltd. which

provides cord blood banking in Guangdong province, PRC.

Shanghai Cordlife Biomedical Research Co. Ltd. (100% owned) undertakes

marketing services in the PRC, in particular Guangdong province, to promote

the group’s cord blood banking services offered in Hong Kong.

CLS Services Pte. Ltd. (100%-owned, incorporated in Singapore) is a dormant

company.

Dividend Policy

While Cordlife does not have a formal dividend policy, it intends to recommend

and distribute dividends of at least 25% of its FY11 and FY12 net profits for FY12

and FY13, respectively.

Recent News and Developments

Cordlife announced unaudited earnings results for 3QFY12 ended Mar. 31,

2012, with revenue of SGD6.9 mln (+13.2% YoY), pre-tax profit of SGD1.1 mln

(-52.9% YoY) and net profit of SGD0.8 mln (+57.1% YoY). / SGX, May 14, 2012

Listed on the Main Board of Singapore Exchange: Cordlife’s common

shares were listed on the main board of the SGX-ST./ SGX, Mar. 29, 2012

Launched initial public offering (IPO): Cordlife launched its IPO of 60 mln

new shares at SGD0.495/share of which 2.0 mln shares are offered to the

public and the remaining shares sold by way of placement. The group is

expected to raise net proceeds for SGD26.3 mln of which SGD16.6 mln will

be used for business development and expansion in Singapore and overseas.

/ SGX, Mar. 21, 2012

Cordlife Group Limited

CLS Services Pte. Ltd. Cordlife (Hong Kong) Ltd. Shanghai CordlifeBiomedical Research

Co. Ltd.

China Stem Cells (South) Co. Ltd.

Guangzhou Tianhe NouyaBiology Engineering

Co. Ltd.

100% 100% 100%

100%

10%

Cordlife Group Limited

CLS Services Pte. Ltd. Cordlife (Hong Kong) Ltd. Shanghai CordlifeBiomedical Research

Co. Ltd.

China Stem Cells (South) Co. Ltd.

Guangzhou Tianhe NouyaBiology Engineering

Co. Ltd.

100% 100% 100%

100%

10%

17

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

Glossary

S&P STARS - Since January 1, 1987, S&P Capital IQ Equity Research has ranked a

universe of U.S. common stocks, ADRs (American Depositary Receipts), and ADSs

(American Depositary Shares) based on a given equity’s potential for future

performance. Similarly, S&P Capital IQ Equity Research has used STARS®

methodology to rank Asian and European equities since June 30, 2002. Under

proprietary STARS (STock Appreciation Ranking System), S&P equity analysts rank

equities according to their individual forecast of an equity’s future total return

potential versus the expected total return of a relevant benchmark (e.g., a regional

index (S&P Asia 50 Index, S&P Europe 350® Index or S&P 500® Index)), based on a

12-month time horizon. STARS was designed to meet the needs of investors looking

to put their investment decisions in perspective. Data used to assist in determining

the STARS ranking may be the result of the analyst’s own models as well as internal

proprietary models resulting from dynamic data inputs.

S&P Quality Rankings (also known as S&P Earnings & Dividend Rankings)-

Growth and stability of earnings and dividends are deemed key elements in

establishing S&P’s earnings and dividend rankings for common stocks, which are

designed to capsulize the nature of this record in a single symbol. It should be noted,

however, that the process also takes into consideration certain adjustments and

modifications deemed desirable in establishing such rankings. The final score for

each stock is measured against a scoring matrix determined by analysis of the scores

of a large and representative sample of stocks. The range of scores in the array of

this sample has been aligned with the following ladder of rankings:

A+ Highest B+ Average C Lowest

A High B Below Average D In Reorganization

A- Above Average B- Lower NR Not Ranked

S&P Issuer Credit Rating - A Standard & Poor’s Issuer Credit Rating is a current

opinion of an obligor’s overall financial capacity (its creditworthiness) to pay its

financial obligations. This opinion focuses on the obligor’s capacity and willingness

to meet its financial commitments as they come due. It does not apply to any specific

financial obligation, as it does not take into account the nature of and provisions of

the obligation, its standing in bankruptcy or liquidation, statutory preferences, or the

legality and enforceability of the obligation. In addition, it does not take into account

the creditworthiness of the guarantors, insurers, or other forms of credit

enhancement on the obligation.

S&P Capital IQ EPS Estimates – S&P Capital IQ earnings per share (EPS) estimates

reflect analyst projections of future EPS from continuing operations, and generally

exclude various items that are viewed as special, non-recurring, or extraordinary.

Also, S&P Capital IQ EPS estimates reflect either forecasts of S&P Capital IQ equity

analysts; or, the consensus (average) EPS estimate, which are independently

compiled by Capital IQ, a data provider to S&P Capital IQ Equity Research. Among

the items typically excluded from EPS estimates are asset sale gains; impairment,

restructuring or merger-related charges; legal and insurance settlements; in process

research and development expenses; gains or losses on the extinguishment of debt;

the cumulative effect of accounting changes; and earnings related to operations that

have been classified by the company as discontinued. The inclusion of some items,

such as stock option expense and recurring types of other charges, may vary, and

depend on such factors as industry practice, analyst judgment, and the extent to

which some types of data is disclosed by companies.

S&P Core Earnings – S&P Capital IQ Core Earnings is a uniform methodology for

adjusting operating earnings by focusing on a company's after-tax earnings

generated from its principal businesses. Included in the S&P Capital IQ definition are

employee stock option grant expenses, pension costs, restructuring charges from

ongoing operations, write-downs of depreciable or amortizable operating assets,

purchased research and development, M&A related expenses and unrealized

gains/losses from hedging activities. Excluded from the definition are pension gains,

impairment of goodwill charges, gains or losses from asset sales, reversal of prior-

year charges and provision from litigation or insurance settlements.

S&P 12 Month Target Price – The S&P Capital IQ equity analyst’s projection of the

market price a given security will command 12 months hence, based on a

combination of intrinsic, relative, and private market valuation metrics, including

S&P Fair Value.

S&P Capital IQ Equity Research – S&P Capital IQ Equity Research U.S. includes

Standard & Poor’s Investment Advisory Services LLC; Standard & Poor’s Equity

Research Services Europe includes McGraw-Hill Financial Research Europe Limited

trading as Standard & Poor’s; Standard & Poor’s Equity Research Services Asia

includes McGraw-Hill Financial Singapore Pte. Limited’s offices in Singapore,

Standard & Poor’s Investment Advisory Services (HK) Limited in Hong Kong,

Standard & Poor’s Malaysia Sdn Bhd, and Standard & Poor’s Information Services

(Australia) Pty Ltd.

Abbreviations Used in S&P Capital IQ Equity Research Reports

CAGR- Compound Annual Growth Rate

CAPEX- Capital Expenditures

CY- Calendar Year

DCF- Discounted Cash Flow

EBIT- Earnings Before Interest and Taxes

EBITDA- Earnings Before Interest, Taxes, Depreciation and Amortization

EPS- Earnings Per Share

EV- Enterprise Value

FCF- Free Cash Flow

FFO- Funds From Operations

FY- Fiscal Year

P/E- Price/Earnings

PEG Ratio- P/E-to-Growth Ratio

PV- Present Value

R&D- Research & Development

ROE- Return on Equity

ROI- Return on Investment

ROIC- Return on Invested Capital

ROA- Return on Assets

SG&A- Selling, General & Administrative Expenses

WACC- Weighted Average Cost of Capital

Dividends on American Depository Receipts (ADRs) and American Depository

Shares (ADSs) are net of taxes (paid in the country of origin).

Disclosures/Disclaimers

Required Disclosures In contrast to the qualitative STARS recommendations covered in this report, which

are determined and assigned by S&P Capital IQ equity analysts, S&P’s quantitative

evaluations are derived from S&P’s proprietary Fair Value quantitative model. In

particular, the Fair Value Ranking methodology is a relative ranking methodology,

whereas the STARS methodology is not. Because the Fair Value model and the

STARS methodology reflect different criteria, assumptions and analytical methods,

quantitative evaluations may at times differ from (or even contradict) an equity

analyst’s STARS recommendations. As a quantitative model, Fair Value relies on

history and consensus estimates and does not introduce an element of subjectivity

as can be the case with equity analysts in assigning STARS recommendations.

S&P Global STARS Distribution In North America

As of March 31, 2012, research analysts at S&P Capital IQ Equity Research North

America recommended 34.5% of issuers with buy recommendations, 57.9% with

hold recommendations and 7.6% with sell recommendations.

In Europe

As of March 31, 2012, research analysts at S&P Capital IQ Equity Research Europe

recommended 30.1% of issuers with buy recommendations, 49.4% with hold

recommendations and 20.5% with sell recommendations.

18

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

In Asia

As of March 31, 2012, research analysts at S&P Capital IQ Equity Research Asia

recommended 35.9% of issuers with buy recommendations, 54.3% with hold

recommendations and 9.8% with sell recommendations.

Globally

As of March 31, 2012, research analysts at S&P Capital IQ Equity Research globally

recommended 34.0% of issuers with buy recommendations, 56.3% with hold

recommendations and 9.7% with sell recommendations.

Additional information is available upon request.

Other Disclosures This report has been prepared and issued by S&P Capital IQ and/or one of its

affiliates. In the United States, research reports are prepared by Standard & Poor’s

Investment Advisory Services LLC (“SPIAS”). In the United States, research reports

are issued by Standard & Poor’s (“S&P”); in the United Kingdom by McGraw-Hill

Financial Research Europe Limited, which is authorized and regulated by the

Financial Services Authority and trades as Standard & Poor’s; in Hong Kong by

Standard & Poor’s Investment Advisory Services (HK) Limited, which is regulated by

the Hong Kong Securities Futures Commission; in Singapore by McGraw-Hill

Financial Singapore Pte. Limited (MHFSPL), which is regulated by the Monetary

Authority of Singapore; in Malaysia by Standard & Poor’s Malaysia Sdn Bhd

(“S&PM”), which is regulated by the Securities Commission; in Australia by Standard

& Poor’s Information Services (Australia) Pty Ltd (“SPIS”), which is regulated by the

Australian Securities & Investments Commission; and in Korea by SPIAS, which is

also registered in Korea as a cross-border investment advisory company.

The research and analytical services performed by SPIAS, McGraw-Hill Financial

Research Europe Limited, MHFSPL, S&PM, and SPIS are each conducted separately

from any other analytical activity of S&P Capital IQ.

S&P Capital IQ or an affiliate may license certain intellectual property or provide

pricing or other services to, or otherwise have a financial interest in, certain issuers

of securities, including exchange-traded investments whose investment objective is

to substantially replicate the returns of a proprietary Standard & Poor's index, such

as the S&P 500. In cases where S&P Capital IQ or an affiliate is paid fees that are tied

to the amount of assets that are invested in the fund or the volume of trading activity

in the fund, investment in the fund will generally result in S&P Capital IQ or an

affiliate earning compensation in addition to the subscription fees or other

compensation for services rendered by S&P Capital IQ. A reference to a particular

investment or security by S&P Capital IQ and/or one of its affiliates is not a

recommendation to buy, sell, or hold such investment or security, nor is it

considered to be investment advice.

Indexes are unmanaged, statistical composites and their returns do not include

payment of any sales charges or fees an investor would pay to purchase the

securities they represent. Such costs would lower performance. It is not possible to

invest directly in an index.

S&P Capital IQ and its affiliates provide a wide range of services to, or relating to,

many organizations, including issuers of securities, investment advisers, broker-

dealers, investment banks, other financial institutions and financial intermediaries,

and accordingly may receive fees or other economic benefits from those

organizations, including organizations whose securities or services they may

recommend, rate, include in model portfolios, evaluate or otherwise address.

For details on the S&P Capital IQ research objectivity and conflict-of-interest policies,

please visit:

http://www.standardandpoors.com/products-services/equity-research-main/en/us/

For a list of companies mentioned in this report with whom S&P Capital IQ and/or

one of its affiliates has had business relationships within the past year, please go to:

http://www.standardandpoors.com/products-

services/articles/en/us/?assetID=1245187982940

Standard & Poor's and its affiliates provide a wide range of services to, or relating to,

many organizations, including issuers of securities, investment advisers, broker-

dealers, investment banks, other financial institutions and financial intermediaries,

and accordingly may receive fees or other economic benefits from those

organizations, including organizations whose securities or services they may

recommend, rate, include in model portfolios, evaluate or otherwise address.

S&P has received compensation from one or more institutions, each in the range of

SGD 16,000 to SGD 25,000, for the right to distribute and co-brand S&P’s research

on this company.

Disclaimers With respect to reports issued to clients in a language other than English and in the

case of inconsistencies between the English and translated versions of a report, the

English version prevails. Neither S&P Capital IQ nor its affiliates guarantee the

accuracy of the translation. Assumptions, opinions and estimates constitute our

judgment as of the date of this material and are subject to change without notice.

Past performance is not necessarily indicative of future results.

S&P Capital IQ, its affiliates, and any third-party providers, as well as their

directors, officers, shareholders, employees or agents (collectively S&P Parties) do

not guarantee the accuracy, completeness or adequacy of this material, and S&P

Parties shall have no liability for any errors, omissions, or interruptions therein,

regardless of the cause, or for the results obtained from the use of the information

provided by the S&P Parties. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR

IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF

MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR

USE. In no event shall S&P Parties be liable to any party for any direct, indirect,

incidental, exemplary, compensatory, punitive, special or consequential damages,

costs, expenses, legal fees, or losses (including, without limitation, lost income or

lost profits and opportunity costs) in connection with any use of the information

contained in this document even if advised of the possibility of such damages.

Capital IQ is a business of S&P Capital IQ.

Ratings from Standard & Poor’s Ratings Services are statements of opinion as of

the date they are expressed and not statements of fact or recommendations to

purchase, hold, or sell any securities or to make any investment decisions.

Standard & Poor’s assumes no obligation to update its opinions following

publication in any form or format. Standard & Poor’s ratings should not be relied

on and are not substitutes for the skill, judgment and experience of the user, its

management, employees, advisors and/or clients when making investment and

other business decisions. Standard & Poor’s rating opinions do not address the

suitability of any security. Standard & Poor’s does not act as a fiduciary. While

Standard & Poor’s has obtained information from sources it believes to be reliable,

Standard & Poor’s does not perform an audit and undertakes no duty of due

diligence or independent verification of any information it receives.

S&P Capital IQ keeps certain activities of its business units separate from each

other in order to preserve the independence and objectivity of their respective

activities. As a result, certain business units of S&P Capital IQ may have

information that is not available to other S&P Capital IQ business units. S&P Capital

IQ has established policies and procedures to maintain the confidentiality of certain

non-public information received in connection with each analytical process.

Standard & Poor’s Ratings Services did not participate in the development of this

report. Standard & Poor’s may receive compensation for its ratings and certain

credit-related analyses, normally from issuers or underwriters of securities or from

obligors. Standard & Poor’s reserves the right to disseminate its opinions and

analyses. Standard & Poor’s public ratings and analyses are made available on its

Web sites, www.standardandpoors.com (free of charge), and

www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may

be distributed through other means, including via Standard & Poor’s publications

and third-party redistributors. Additional information about our ratings fees is

available at www.standardandpoors.com/usratingsfees .

This material is not intended as an offer or solicitation for the purchase or sale of

any security or other financial instrument. Securities, financial instruments or

strategies mentioned herein may not be suitable for all investors. Any opinions

expressed herein are given in good faith, are subject to change without notice, and

are only current as of the stated date of their issue. Prices, values, or income from

any securities or investments mentioned in this report may fall against the interests

19

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

of the investor and the investor may get back less than the amount invested. Where

an investment is described as being likely to yield income, please note that the

amount of income that the investor will receive from such an investment may

fluctuate. Where an investment or security is denominated in a different currency to

the investor’s currency of reference, changes in rates of exchange may have an

adverse effect on the value, price or income of or from that investment to the

investor. The information contained in this report does not constitute advice on the

tax consequences of making any particular investment decision. This material is not

intended for any specific investor and does not take into account your particular

investment objectives, financial situations or needs and is not intended as a

recommendation of particular securities, financial instruments or strategies to you.

Before acting on any recommendation in this material, you should consider whether

it is suitable for your particular circumstances and, if necessary, seek professional

advice.

This document does not constitute an offer of services in jurisdictions where S&P

Capital IQ or its affiliates do not have the necessary licenses.

For residents of the U.K. - This report is only directed at and should only be relied on

by persons outside of the United Kingdom or persons who are inside the United

Kingdom and who have professional experience in matters relating to investments or

who are high net worth persons, as defined in Article 19(5) or Article 49(2) (a) to (d) of

the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005,

respectively.

For residents of Singapore - Anything herein that may be construed as a

recommendation is intended for general circulation and does not take into account

the specific investment objectives, financial situation or particular needs of any

particular person. Advice should be sought from a financial adviser regarding the

suitability of an investment, taking into account the specific investment objectives,

financial situation or particular needs of any person in receipt of the

recommendation, before the person makes a commitment to purchase the

investment product.

For residents of Malaysia - All queries in relation to this report should be referred to

Ching Wah Tam and Ahmad Halim.

For residents of Indonesia - This research report does not constitute an offering

document and it should not be construed as an offer of securities in Indonesia, and

that any such securities will only be offered or sold through a financial institution.

For residents of the Philippines - The securities being offered or sold have not been

registered with the Securities and Exchange Commission under the Securities

Regulation Code of the Philippines. Any future offer or sale thereof is subject to

registration requirements under the Code unless such offer or sale qualifies as an

exempt transaction.

Canadian investors should be aware that any specific securities discussed in this

research report can only be purchased in Canada through a Canadian registered

dealer and, if such securities are not available in the secondary market, they can only

be purchased by eligible private placement purchasers on a basis that is exempt

from the prospectus requirements of Canadian securities law and will be subject to

resale restrictions.

For residents of Australia – This report is distributed by Standard & Poor’s

Information Services (Australia) Pty Ltd (“SPIS”) in Australia.

Any express or implied opinion contained in this report is limited to "General Advice"

and based solely on consideration of the investment merits of the financial product(s)

alone. The information in this report has not been prepared for use by retail investors

and has been prepared without taking account of any particular person's financial or

investment objectives, financial situation or needs. Before acting on any advice, any

person using the advice should consider its appropriateness having regard to their

own or their clients' objectives, financial situation and needs. You should obtain a

Product Disclosure Statement relating to the product and consider the statement

before making any decision or recommendation about whether to acquire the

product. Each opinion must be weighed solely as one factor in any investment

decision made by or on behalf of any adviser and any such adviser must accordingly

make their own assessment taking into account an individual's particular

circumstances.

SPIS holds an Australian Financial Services Licence Number 258896. Please refer to

the SPIS Financial Services Guide for more information at

www.fundsinsights.com.au.

STANDARD & POOR’S, S&P, S&P 500, S&P Europe 350 and STARS

are registered trademarks of Standard & Poor’s Financial Services

LLC.

PrimePartners Disclaimer

Without prejudice to and without limiting the generality of the foregoing

disclosures and disclaimers:

PrimePartners Corporate Finance Pte Ltd (“PPCF”) is licensed for the provision of

corporate finance advisory services and dealing in securities in Singapore and has

been appointed as the sponsor of this company.

In connection with the foregoing, PPCF has the right to distribute and co-brand

S&P’s research on this company, and PPCF has been named and included in this

report solely on such basis.

No publication, dissemination, provision, delivery or circulation of this report (or

any information or material herein) by PCPF and/or any of its affiliates, employees,

directors, shareholders, officers, agents or representatives (collectively the “PPCF

Entities”) shall in any way be deemed or construed as the provision of any advice

and/or recommendation on this company and/or any of its securities or as the issue

or promulgation of any research analyses or research reports on this company

and/or any of its securities by the PPCF Entities, and the PPCF Entities expressly

disclaims any responsibility or liability for the same.

The PPCF Entities do not warrant or represent or guarantee the accuracy,

completeness or adequacy of this report (or any information or material herein),

and the PPCF Entities shall have no liability for any errors, omissions or

interruptions therein, regardless of the cause, or for the results obtained from the

use of this report (or any information or material herein). PPCF Entities disclaims

all express or implied warranties, including but not limited to, any warranties of

merchantability, suitability or fitness for a particular purpose or use. In no event

shall PPCF Entities be liable to any party for any direct or indirect, incidental,

exemplary, compensatory, punitive, special or consequential damages, costs and

expenses, legal fees, or losses (including without limitation, lost income or lost

profits and opportunity costs) in connection with any use or reliance on this report

(or any information or material herein) even if advised of the possibility of such

damages.

Where this report is in relation to a company that is to be listed:

(i) No publication or dissemination of this report to any person shall be made

during the period commencing on the Blackout Commencement Date (as defined

below) and concluding on a date on which its shares are listed on the relevant stock

exchange in Singapore, and/or any other applicable blackout period(s) specified in

the relevant laws and regulations (including orders, notifications, notices,

guidelines, codes and practice notes of the Monetary Authority of Singapore).

“Blackout Commencement Date” means the date falling no later than fourteen (14)

days prior to the date a prospectus or offer document in respect of the initial public

offering of shares of the issuer is to be lodged with the relevant authority in

Singapore under the SFA.

No publication or dissemination of this report shall be made to any person unless

such person falls within the definition of institutional investors under the Securities

and Futures Act of Singapore (Chapter 289) (“SFA”) for purposes of investing in the

issuer and has requested for this report.

No publication or dissemination of this report (or any information or material

herein) in any country or countries outside Singapore shall be made unless the

publication and dissemination of this report (or any information or material herein)

does not infringe upon any law, code or other requirement of that country or

countries.

20

Standard & Poor’s

June 29, 2012 Cordlife Group Ltd

No reproduction, publication or dissemination of this report (or any information or

material herein) shall be made by any person to whom this report is provided or any

person who otherwise comes into receipt or possession of such report.

This report (and the information and material herein) is not intended as an offer or

solicitation for the purchase or sale of any security or other financial instrument.

Securities, financial instruments or strategies mentioned herein may not be suitable

for all investors. Any opinions expressed herein are given in good faith, are subject

to change without notice, and are only current s of the stated date of their issue.

Prices, values, or income from any securities or investments mentioned in this report

may fall against the interests of the investor and the investor may get back less than

the amount invested. Where an investment is described as being likely to yield

income, please note that the amount of income that the investor will receive from

such an investment may fluctuate. Where an investment or security is denominated

in a different currency to the investor’s currency of reference, changes in rates of

exchange may have an adverse effect on the value, price or income of or from that

investment to the investor. The information contained in this report does not

constitute advice on tax consequences of making any particular investment decision.

This report (and the information and material herein) is not intended for any specific

investor and does not take into account your particular investment objectives,

financial situations or needs and is not intended as recommendation or particular

securities, financial instruments or strategies to you. Before acting on any

recommendation in this material, you should consider whether it is suitable for your

particular circumstances and, if necessary, seek professional advice.

This document does not constitute an offer of services in jurisdictions where PPCF or

its affiliates do not have the necessary licences.

For residents of Singapore- Anything herein that may be construed as a

recommendation is intended for general circulation and does not take into account

the specific investment objectives, financial situation or particular needs of particular

needs of any particular person. Advice should be sought from a financial adviser

regarding the suitability of an investment, taking into account the specific investment

objectives, financial situation or particular needs of any person in receipt of the

recommendation, before the person makes a commitment to purchase the

investment product.