2011 seacoast church employee benefits guide

DESCRIPTION

A quick reference for Seacoast employees to check their employee benefits information.TRANSCRIPT

EMPLOYEE BEnEfits GuidEA quick reference guidebook

for seacoast Church employees detailing their benefits, plan

costs and coverages.

PLAn YEAR | 2011

table of contents

Medical plan blue choice www.bluechoicesc.com customer service: 800-868-2528

dental plan delta dental www.deltadental.com customer service: (800) 529-3268

vision plan eyeMed vision care www.eyemedvisioncare.com customer service: 866-9eYeMed

short terM disabilitY plan aflac - bryce Kinney www.aflac.com customer service: 803-629-4601 [email protected]

long terM disabilitY plan prudential (group# 54004ltd) www.prudential.com customer service: 800-842-1718

basic terM life insurance plan prudential www.prudential.com customer service: 800-778-2255

flexible spending account (fsa) blue Water administratorscustomer service: 800-377-7749

health reiMburseMent account (hra)blue Water administratorscustomer service: 800-377-7749

403b retireMent planameriprise richard c. Young, Jr. phone:843-971-0982 x201 email: [email protected]

benefit contacts

eligibility .........................................................................................................................................................................................................3

Medical plan.................................................................................................................................................................................................4

health & Wellness .....................................................................................................................................................................................6

dental insurance .......................................................................................................................................................................................7

vision insurance ........................................................................................................................................................................................8

glossary of terms .....................................................................................................................................................................................9

short-term disability insurance ....................................................................................................................................................10

long-term disability insurance.....................................................................................................................................................12

voluntary term life insurance .......................................................................................................................................................13

flexible spending account (fsa) ................................................................................................................................................14

health reimbursement account (hra)...................................................................................................................................15

employee assistance program (eap) ........................................................................................................................................18

403b plan ....................................................................................................................................................................................................18

important notices about your plan ...........................................................................................................................................19

seacoast church employee benefits guide 20112

Welc

ome

seacoast church eMploYee benefits hotline :

seacoast church employees have access to a dedicated employee benefit hotline to answer questions about enrollment, coverage, claims and all other concerns regarding their employee benefit package. our call center is staffed with trained professionals who understand your benefits plan and are dedicated to providing solutions to your problems. its easy and its free, just call or email:

1-800-377-7749 (toll-free) Monday - Friday 9am - 5pm ESTemail: [email protected]

are You el igible for benefits?

to determine the benefits for which you may be eligible, please refer to the chart below . You are eligible to participate in these plans upon meeting each plan’s eligibility requirements. You also have the option to enroll your eligible dependents in some of these plans. eligible dependents may include:

• Your spouse or your children (dependent age limit to 26*)

individuals whose coverage ended, or who were denied coverage (or were not eligible for coverage), because the availability of dependent coverage of children ended before attainment of age 26 are eligible to enroll in the healthplan. employees requesting to enroll eligible dependents will have the opportunity during this open enrollment period. enrollment will be effective January 1, 2011.

*certain limitations apply. please call the employee benefits hotline for additional information, 800-377-7749

Plan Eligibility New Hire Eligibility Waiting Period

Medical/prescription 30+ hours per week 1st of month following date of hire

dental 30+ hours per week 1st of month following date of hire

vision 30+ hours per week 1st of month following date of hire

basic life and ad&d 30+ hours per week 1st of month following date of hire

long-term disability 30+ hours per week 1st of month following date of hire

403b plan all employees no waiting period, eligible date of hire

eligibility .........................................................................................................................................................................................................3

Medical plan.................................................................................................................................................................................................4

health & Wellness .....................................................................................................................................................................................6

dental insurance .......................................................................................................................................................................................7

vision insurance ........................................................................................................................................................................................8

glossary of terms .....................................................................................................................................................................................9

short-term disability insurance ....................................................................................................................................................10

long-term disability insurance.....................................................................................................................................................12

voluntary term life insurance .......................................................................................................................................................13

flexible spending account (fsa) ................................................................................................................................................14

health reimbursement account (hra)...................................................................................................................................15

employee assistance program (eap) ........................................................................................................................................18

403b plan ....................................................................................................................................................................................................18

important notices about your plan ...........................................................................................................................................19

Questions? call the employee benefits hotline: 1-800-377-7749 3

Seacoast ChurchWe are committed to providing employees with a benefits program that is both comprehensive and competitive. Our program offers a broad range of plan options to meet the needs of our diverse workforce. This program is designed to assist you in providing for the health, well–being and financial security of you and covered dependents.

Medical plan ADMINISTERED BY BluE cHOIcE

Benefits In-NetworkMEMBER PAYS

Out-of-NetworkMEMBER PAYS

Deductible per Benefit Period per Member per family (All family Members can contribute with no one Membercontributing more than the individual deductible amount.)

$3,750 $7,500

$4,250 $8,500

Maximum Coinsurance per Benefit Period per Member per family

n/a n/a

$5,750 $11,500

Physician Care (Routine/preventive care covered) office services (all other) Mandated preventive care

deductible, then 0% $0

deductible, then 40% not covered

Other Routine Care (not subject to deductible or copayment)gYn exam routine screening Mammogram routine screening colonoscopy

$0 $0 $0

not covered not covered not covered

Hospital/Facility Services (Authorization required, In & Out of Network)inpatient admission (including maternity) skilled nursing facility long-term acute care facility Mri, cat scan, pet scan

deductible, then 0% deductible, then 0%deductible, then 0% deductible, then 0%

deductible, then 40% deductible, then 40% deductible, then 40%

Outpatient/Ambulatory Care Facilities (Authorization required, In & Out of Network)all services (including maternity) emergency room services urgent care

deductible, then 0% deductible, then 0%deductible, then 0%

deductible, then 40% deductible, then 0%

deductible, then 40%

Prescription Medicinecertain prescription Medicine may require prior authorization or have dosage limits

deductible, then 0% not covered

Specialty Pharmaceuticals deductible, then 0% not covered

Other Services ambulancebehavioral therapy (aba) for autism spectrum disorderdental services due to accidental injurydurable Medical equipment (dMe) (Authorization required)home healthhospiceinitial prosthetic appliancesMedical suppliesoccupational therapyop private duty nursingphysical therapyspeech therapy chiropractic services

deductible, then 0% deductible, then 0%deductible, then 0%deductible, then 0%deductible, then 0%deductible, then 0%deductible, then 0%deductible, then 0%deductible, then 0%deductible, then 0%deductible, then 0%deductible, then 0% deductible, then 0%

deductible, then 40% not covered

deductible, then 40% deductible, then 40% deductible, then 40% deductible, then 40% deductible, then 40% deductible, then 40% deductible, then 40% deductible, then 40% deductible, then 40% deductible, then 40%

not covered

covered transplants will be treated the same as any other medical condition. services must be provided at abluechoice healthplan participating facility or a blues distinction for transplant designated facility.

seacoast church employee benefits guide 20114

ADMINISTERED BY BluE cHOIcEMedical plan & contributions

To assist employees with the cost of the medical plan, Seacoast church gives you a Health Reimbursement

Account (HRA) visa card. Seacoast church is contributing the following amounts to your HRA for the 2011 plan year. Additional HRA monies can be earned through participation in Seacoast Wellness (see next

page for details).

Coverage Tier HRA Amount

employee only $1,100

family $2,200

Benefits In-NetworkMEMBER PAYS

Out-of-NetworkMEMBER PAYS

Mental Health & Substance Use Disorders (The following services must be authorized in advance by Companion Benefit Alternatives at 1-800-868-1032) inpatient hospital facility servicesinpatient physician servicesoutpatient facility institutional servicesoutpatient facility professional servicesoffice professional services

deductible, then 0% deductible, then 0%deductible, then 0%deductible, then 0%

0%

deductible, then 40% deductible, then 40%deductible, then 40%deductible, then 40%deductible, then 40%

Maximums

Annual Benefit MaximumBehavioral Therapy (ABA) Occupational TherapyOP Private Duty NursingPhysical TherapySkilled Nursing FacilitySpeech Therapy Chiropractic Care

$2,000,000$50,000 per benefit period20 visits per benefit period60 visits per benefit period20 visits per benefit period120 days per benefit period20 visits per benefit period $1,000 per benefit period

Benefit Period 1/1/2011 to 12/31/2011

In order to receive In-Network benefits, all services must be provided by a BlueChoice HealthPlan Participating Provider. This applies to each individual service unless otherwise noted. All admissions must be authorized by BlueChoice HealthPlan in order to be covered. Benefits are subject to all terms, conditions, limitations, and exclusions outlined in the Contract.

*HRA monies are used for medical deductible only, which does include prescriptions.

hra

Medical Plan coverage Tier Biweekly Employee Pay Deductions

Biweekly Seacoast church cost

employee only $22.56 $100.44

employee + spouse $133.20 $87.89

employee + child(ren) $104.90 $164.30

family $217.59 $163.18 Med

ical

Questions? call the employee benefits hotline: 1-800-377-7749 5

HEAlTH & WEllNESS AT SEAcOAST cHuRcH

seacoast church cares about the health and happiness of each employee. the program seeks to provide each employee with access to competent medical care, cultivate a lifestyle that includes proper exercise and diet, and cultivate a positive mental outlook. Wellness incentives help to minimize tensions in the workplace, create more of a team spirit among employees and also enhance productivity while reducing absenteeism.

below are highlights of activities that you may complete for wellness rewards. Wellness rewards is money deposited into your health reimbursement account that may be used for the purchase or reimbursement of eligible medical expenses. You have been issued a debit card tied to your hra.

GROWING HEAlTHY cHAllENGE

our goal is to encourage a healthy lifestyle so that our employees are happier, healthier and more productive. We will be offering a wellness challenge from May 1-31 for all employees & spouses covered under the medical plan. this challenge will reward employees for pursuing healthy habits such as:

• consuming fruits & vegetable • routine exercise • adequate sleep • stress Management • drinking recommended amounts of water

during these time, employees will be provided a weekly tracking form so you can keep track of your progress and be successful in this challenge.

WAlkING WORkS

the goal of this program is to positively impact employee health and productivity: • incorporate physical activity into one’s daily routine • track personal progress

Wellness Activity Date covered Employee & Spouse Wellness Reward

Walking Works april 1-30, 2011 $200 toward hra

growing healthy challenge May 1-31, 2011 $200 toward hra

physical exam complete by June 30, 2011 $300 each toward hra

ADMINISTERED BY BluE WATER BENEfITShealth & Wellness

seacoast church employee benefits guide 20116

ANNuAl PHYSIcAl

please take the form with you to be completed at your annual physical and ask your physician to sign the form and fill out the required information. all full-time eligible employees and spouses covered under the plan who complete an annual physical prior to June 30, 2011 will be eligible for $300 toward your hra. employees must fax this completed form to blue Water benefits at 843-884-3338. employees that have obtained a physical later than october 1, 2010, do not need to complete another physical to receive reimbursement, but must still complete the required form.

“They have no struggles; their bodies are healthy and strong.” - psalM 73:4

Questions? call the employee benefits hotline: 1-800-377-7749 7

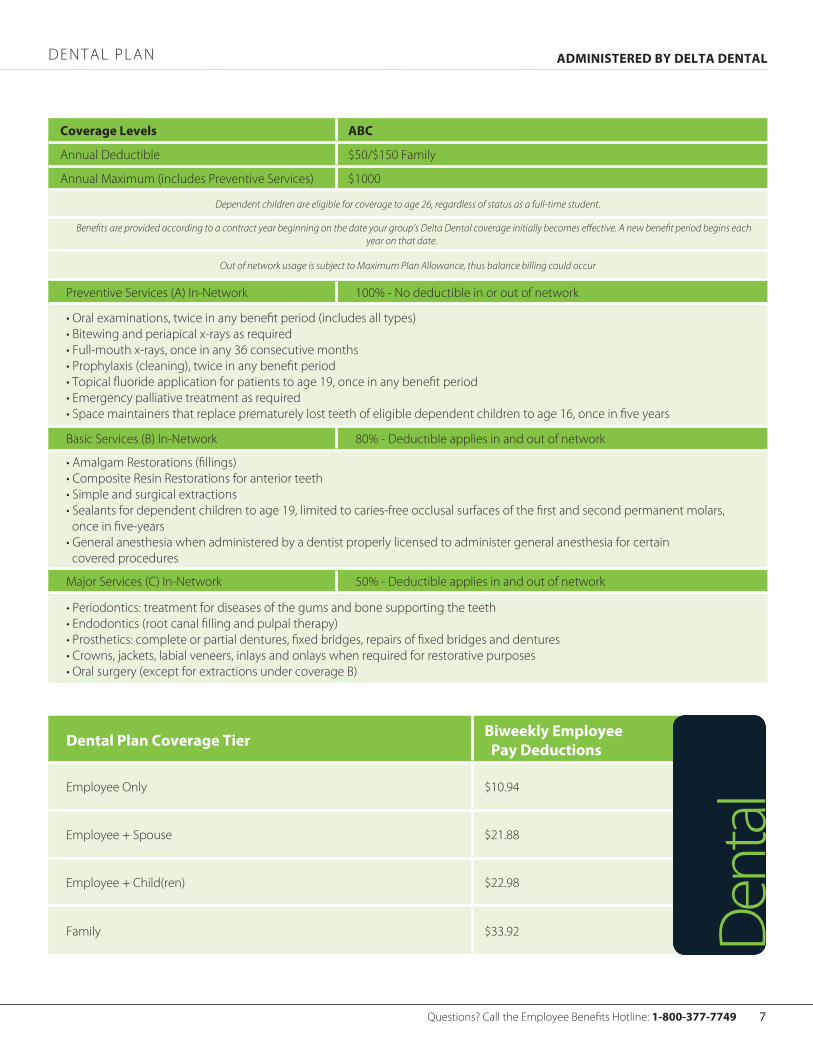

dental plan ADMINISTERED BY DElTA DENTAl

coverage levels ABc

annual deductible $50/$150 family

annual Maximum (includes preventive services) $1000

Dependent children are eligible for coverage to age 26, regardless of status as a full-time student.

Benefits are provided according to a contract year beginning on the date your group’s Delta Dental coverage initially becomes effective. A new benefit period begins each year on that date.

Out of network usage is subject to Maximum Plan Allowance, thus balance billing could occur

preventive services (a) in-network 100% - no deductible in or out of network

• oral examinations, twice in any benefit period (includes all types)• bitewing and periapical x-rays as required• full-mouth x-rays, once in any 36 consecutive months• prophylaxis (cleaning), twice in any benefit period• topical fluoride application for patients to age 19, once in any benefit period• emergency palliative treatment as required• space maintainers that replace prematurely lost teeth of eligible dependent children to age 16, once in five years

basic services (b) in-network 80% - deductible applies in and out of network

• amalgam restorations (fillings)• composite resin restorations for anterior teeth• simple and surgical extractions• sealants for dependent children to age 19, limited to caries-free occlusal surfaces of the first and second permanent molars, once in five-years• general anesthesia when administered by a dentist properly licensed to administer general anesthesia for certain covered procedures

Major services (c) in-network 50% - deductible applies in and out of network

• periodontics: treatment for diseases of the gums and bone supporting the teeth• endodontics (root canal filling and pulpal therapy)• prosthetics: complete or partial dentures, fixed bridges, repairs of fixed bridges and dentures• crowns, jackets, labial veneers, inlays and onlays when required for restorative purposes• oral surgery (except for extractions under coverage b)

Dental Plan coverage Tier Biweekly Employee Pay Deductions

employee only $10.94

employee + spouse $21.88

employee + child(ren) $22.98

family $33.92 dent

al

Vision care Services Member cost Out-of-Network

exam with dilation as necessary $10 copay $30

standard contact lens fit and follow-up exam up to $40 n/a

premium contact lens fit and follow-up exam 10% off retail n/a

frames: any available frame at provider location$0 copay; $130 allowance, 20% off balance over $130

$65

standard plastic lenses

single vision $25 copay $25

bifocal $25 copay $40

trifocal $25 copay $60

standard progressive lens** $90 $40

premium progressive lens** $90, 80% of charge less $120 allowance $40

lens options

uv treatment, tint (solid and gradient), standard plastic scratch coating

$15 n/a

standard polycarbonate $40 n/a

standard anti-reflective coating $45 n/a

polarized and other add-ons 20% off retail price n/a

contact lenses (contact lens allowance includes materials only)

conventional$0 copay; $115 allowance, 15% off balance over $115

$92

disposable$0 copay; $115 allowance, plus balance over $115

$92

Medically necessary $0 copay, paid-in-full $200

laser vision correction

lasik or prK from u.s. laser network 15% off retail price or 5% off promotional price n/a

additional pairs benefit:

Members also receive a 40% discount off complete pair eyeglass purchases and a 15% discount off conventional contact lenses once the funded benefit has been used.

n/a

frequency

examination, lenses or contact lenses once every 12 months

frame once every 24 months

v is ion plan ADMINISTERED BY EYEMED

** standard/premium progressive lenses not covered - fund as a bifocal lens

seacoast church employee benefits guide 20118

ADMINISTERED BY EYEMEDvis ion plan contributions

glossarY of terMs

Questions? call the employee benefits hotline: 1-800-377-7749 9

Vision Plan coverage Tier Biweekly Employee Pay Deductions

employee only $2.69

employee + spouse $5.10

employee + child(ren) $5.38

family $7.90 visio

n

coinsurance - a percentage of an eligible expense that you are required to pay for a covered service.

Deductible - the amount you must pay before the plan begins to pay benefits.

Explanation of Benefits (EOB) - after you or your provider submit a claim, an explanation will be sent to you that will give you claims payment information, including the amount paid to the provider and any amount you may owe. if a deductible and/or coinsurance applies, the amount applied to your deductible and out-of-pocket maximum will also be shown.

Network - the providers and facilities contracted with to render health care to members. Members receiving in-network care generally obtain a higher level of benefits.

Out-of-Pocket Expense - the annual maximum limit you may pay for covered expenses. after your share of eligible expenses (deductible and coinsurance) reaches a certain limit, the plan will pay 100 percent (unless balance billing applies) of most covered medical expenses for a covered plan member for the remainder of the calendar year.

Out-of-pocket maximum - the most you pay in coinsurance during a benefit plan year. after you reach your out-of-pocket maximum, your medical plan option pays 100% of eligible expenses for the remainder of the benefit plan year.

Primary care physician (PcP) - a family practitioner, general practitioner, internist or pediatrician who provides care and coordinates your medical treatment. network pcps meet qualification standards and are subject to periodic review.

In-network Provider - a physician, hospital or other health care provider that joins a managed care plan and provides services based on negotiated fees. generally, using an in-network provider will save you money in the form of copayments, lower deductibles and a higher reimbursement level, and the provider will file claims for you.

Out-of-network Provider - an out-of-network provider does not participate in the plan and therefore charges a non-discounted fee. payments for out-of-network services are based on your benefit plan and maximum allowable charges. also your portion of the coinsurance and your deductible will be higher when you go out of network for services. When you visit an out-of-network provider, in most cases, you may need to file a claim for reimbursement. Many providers who are not members of the network will file claims for you, but not all out-of-network providers perform this service. if you use an out-of-network provider, be sure to talk with the provider’s staff about whether you or the provider will file your claim.

THE NEED

becoMing disabled is often an unexpected and burdensoMe experience, and it can happen to anYone. What if a disabilitY interrupted Your Job,Your incoMe, and Your financial securitY? hoW Would You MaKe Your house or rent paYMent, or cover daY-to-daY expenses? it’s iMportant to consider these Questions because a disabilitY could adverselY affect Your Well-being and Your finances at a tiMe When You should be concentrating on recoverY.

cONSIDER THESE fAcTS:

• about 62 million people in the united states have some disability that affects daily activity.1

• approximately two-thirds of those with disabilities are younger than 65.1

• around 3-in-10 people entering the workforce today will become disabled before retiring.2

When disabled, you may not only lose the ability to earn a living, but you may also lose savings, retirement funds, or even your home. the financial obligations can be overwhelming. disability insurance plays an integral and important role in your financial planning.

HOW AflAc cAN HElP

aflac’s disability income protection advantage benefits provide a source of income while you concentrate on getting better. Knowing that your disability coverage is backed by a market leader with more than 50 years in the insurance industry may help provide you with peace of mind.

aflac’s short-term disability insurance policy provides you with options to help meet your income and financial needs.

• Your aflac plan stays with you even when you change or leave your job.

• We pay you a cash benefit for each day you are disabled.

• aflac does not coordinate benefits. regardless of any other disability insurance benefits you may have, including social security, we will pay you directly (unless you assign the benefits).

Peace of mind. Cash benefits. Knowing that you’ll have help in the event of disability. All are good reasons to strongly consider the benefits of Aflac.1 “disability and health in the united states, 2001–2005,” national center for health statistics, 2008. 2 social security administration fact sheet 2007.

cHOOSE THE POlIcY YOu NEED

policy a57500sc choose the coverage You need

• Monthly benefit: $500–$5,000 (subject to income requirements)

• benefit periods: 6 months

• elimination periods (injury/sickness): 0/7, 0/14, 7/14, 14/14, 0/30, 30/30, 60/60, 90/90

or

limited benefit health policy a57500lbsc* choose the coverage You need

• Monthly benefit: $500–$5,000 (subject to income requirements)

• benefit period: 3 months

• elimination periods (injury/sickness): 0/7, 0/14, 7/14, 14/14*this is limited benefit health insurance.

limited benefit health policy a57500lbsc provides limited benefits only, which are less than the minimum standard for benefits for disability income protection coverage as prescribed by the insurance regulatory authority of your state.

short terM disabil itY ADMINISTERED BY AflAc

seacoast church employee benefits guide 201110

WHAT WE WIll PAY

Total Disability Benefit: if you have a full-time Job and your coverage is in force at the time of your sickness or off-the-Job injury, we will insure you as follows: if your covered sickness or covered off-the-Job injury causes your total disability within 90 days of your last treatment for your covered sickness or covered off-the-Job injury, we will pay you the daily disability benefit for each day of your disability or your successive periods of disability. You will no longer be qualified to receive this benefit upon the earlier of your: (1) being released by your physician to perform the material and substantial duties of your full-time Job or (2) working at any job.

Partial Disability Benefit: if you have a full-time Job and your coverage is in force at the time of your sickness or off-the-Job injury, we will insure you as follows: if your covered sickness or covered off-the-Job injury causes your partial disability within 90 days of your last treatment for your covered sickness or covered off-the-Job injury, we will pay you the daily disability benefit for each day of your disability or your successive periods of disability.

You will no longer be qualified to receive this benefit upon the earlier of your: (1) being released by your physician to perform the material and substantial duties of your full-time Job or (2) working at any job earning 80 percent or more of your pre-disability base pay earnings.

Transitional Disability Benefit: if you do not have a full-time Job and your coverage is in force at the time of your sickness or off-the-Job injury, we will insure you as follows: if your covered sickness or covered off-the-Job injury causes your transitional disability within 15 days of your last treatment for your covered sickness or covered off-the-Job injury, we will pay you one-half of the daily disability benefit for each day you remain unable to work at any job. this benefit is payable for a maximum period of three months of disability or successive periods of disability and is subject to the elimination period shown in the policy schedule.

You will no longer be qualified to receive this benefit upon the earlier of your: (1) being released by your physician to perform the material and substantial duties of any job or (2) working at any job. this benefit is limited to a lifetime maximum period of a total of three months, regardless of the number of disabilities or the duration of any disability.

the daily disability benefit is one-thirtieth of the applicable monthly disability benefit shown in the policy schedule.

the total and partial disability benefits are payable up to the benefit period selected and are subject to the elimination period shown in the policy schedule.

• Mental or emotional disorders, including but not limited to the following: bipolar affective disorder (manic-depressive syndrome), delusional (paranoid) disorders, psychotic disorders, somatoform disorders (psychosomatic illness), eating disorders, schizophrenia, anxiety disorders, depression, stress, or postpartum depression. the policy will pay, however, for covered disabilities resulting from alzheimer’s disease, or similar forms of senility or senile dementia, first manifested while coverage is in force. a physician does not include you or a member of your immediate family.

benefits will be paid for only one disability at a time even if the disability is caused by more than one sickness, more than one injury, or a sickness and

an injury. the term complications of pregnancy does not include premature delivery without incidence, multiple gestation pregnancy, false labor, occasional spotting, prescribed rest during pregnancy, morning sickness, and similar conditions associated with the management of a difficult pregnancy but not constituting a classifiably distinct pregnancy complication. cesarean deliveries are not considered complications of pregnancy.

pre-existing condition limitations: a pre-existing condition is a condition misrepresented or not revealed in the application and for which symptoms existed prior to the effective date of coverage that would cause an ordinarily prudent person to seek diagnosis, care, or treatment or for which medical advice or treatment was recommended by or received from a physician. disability caused by a pre-existing condition, including deliveries for children conceived prior to the effective date of coverage, or reinjuries to a pre-existing condition will not be covered unless it begins more than 12 months after the effective date of coverage.

the policy does not cover losses caused by or resulting from donating an organ within the first 12 months of the effective date of the policy.

ADDITIONAl INfORMATION

Fully Portable: When you own aflac’s disability income protection advantage, you may choose to keep your policy regardless of job changes by continuing to pay premiums. the payroll rate may be retained after one month’s premium payment on payroll deduction.

Guaranteed-Renewable to Age 70: You are guaranteed the right to renew the policy until the policy anniversary date following your 70th birthday by the timely payment of premiums at the rate in effect at the beginning of each term. You can never be singled out for a rate increase. rates can be changed only if the rate is changed for all policies of this class. While the policy is in force, no change will be made in your class because of your age, sex, or physical condition.

Provisions of Coverage: aflac reserves the right to meet with you during the pendency of a claim or to use an independent consultant and a physician’s statement to determine whether you are qualified to receive disability benefits. You must be under the care and attendance of a physician for benefits to be payable. benefits will cease on the date of your death.

if you have any other disability benefit in force with aflac, only one disability benefit is payable.

the policy to which this sales material pertains is written only in english; the policy prevails if interpretation of this material varies.

ADMINISTERED BY AflAcshort terM disabil itY

Questions? call the employee benefits hotline: 1-800-377-7749 11

Aflac - Bryce kinney www.aflac.com

customer Service: 803-629-4601 [email protected]

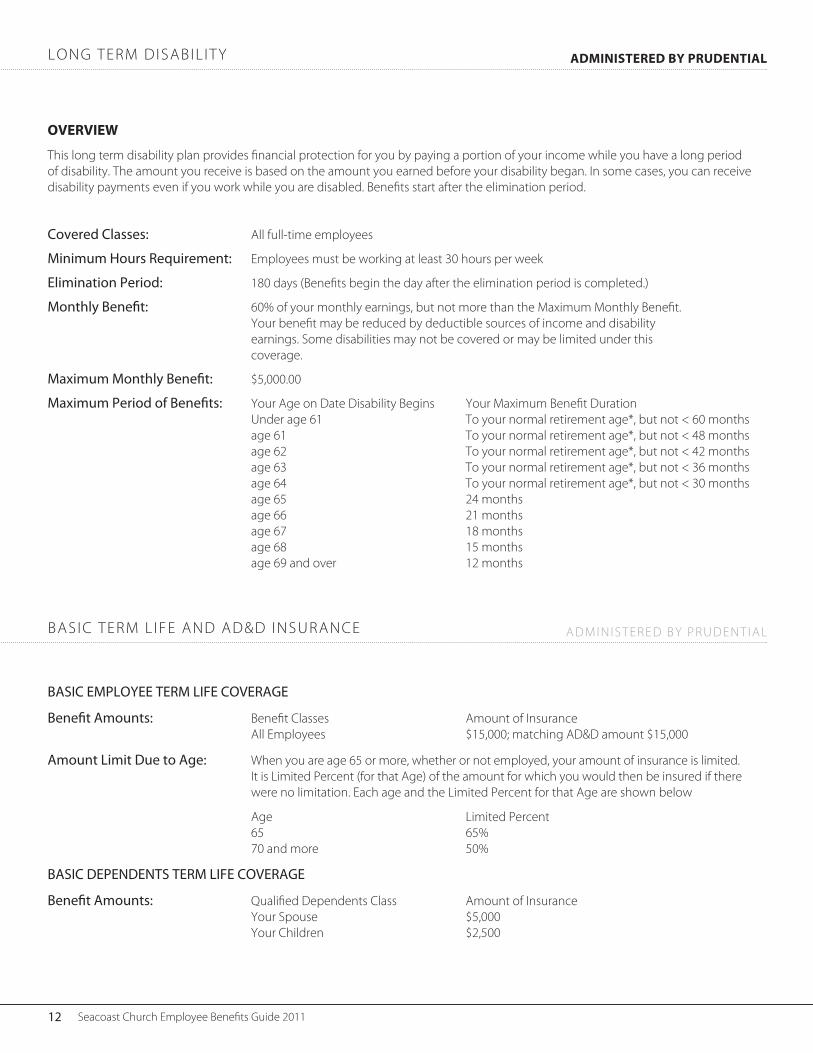

OVERVIEW

this long term disability plan provides financial protection for you by paying a portion of your income while you have a long period of disability. the amount you receive is based on the amount you earned before your disability began. in some cases, you can receive disability payments even if you work while you are disabled. benefits start after the elimination period.

Covered Classes: all full-time employees

Minimum Hours Requirement: employees must be working at least 30 hours per week

Elimination Period: 180 days (benefits begin the day after the elimination period is completed.)

Monthly Benefit: 60% of your monthly earnings, but not more than the Maximum Monthly benefit. Your benefit may be reduced by deductible sources of income and disability earnings. some disabilities may not be covered or may be limited under this coverage.

Maximum Monthly Benefit: $5,000.00

Maximum Period of Benefits: Your age on date disability begins Your Maximum benefit duration under age 61 to your normal retirement age*, but not < 60 months age 61 to your normal retirement age*, but not < 48 months age 62 to your normal retirement age*, but not < 42 months age 63 to your normal retirement age*, but not < 36 months age 64 to your normal retirement age*, but not < 30 months age 65 24 months age 66 21 months age 67 18 months age 68 15 months age 69 and over 12 months

BasiC EMPloyEE tERM lifE CovERagE

Benefit amounts: benefit classes amount of insurance all employees $15,000; matching ad&d amount $15,000

amount limit Due to age: When you are age 65 or more, whether or not employed, your amount of insurance is limited. it is limited percent (for that age) of the amount for which you would then be insured if there were no limitation. each age and the limited percent for that age are shown below

age limited percent 65 65% 70 and more 50%

BasiC DEPEnDEnts tERM lifE CovERagE

Benefit amounts: Qualified dependents class amount of insurance Your spouse $5,000 Your children $2,500

long terM disabil itY

basic terM l ife and ad&d insurance

ADMINISTERED BY PRuDENTIAl

adMinistered bY prudential

seacoast church employee benefits guide 201112

OVERVIEW

an important part of a sound financial plan, life insurance from the prudential insurance company of america and its affiliates provides a valuable death benefit to your beneficiaries upon your death. Your beneficiaries can then use this money to replace some of the income you would have earned or to help pay off debts or other expenses.

Employees electing voluntary life insurance on themselves may also elect coverage on their children up to $10,000.

coverage $2,000 $4,000 $6,000 $8,000 $10,000 deduction $0.09 $0.19 $0.28 $0.38 $0.47

Age Brackets $5,000 $25,000 $50,000 $75,000 $100,000 $125,000 $150,00015 - 19 $0.16 $0.82 $1.64 $2.46 $3.28 $4.10 $4.9220 - 24 $0.20 $0.99 $1.98 $2.98 $3.97 $4.96 $5.9525 - 29 $0.24 $1.18 $2.35 $3.53 $4.71 $5.88 $7.0630 - 34 $0.25 $1.26 $2.52 $3.77 $5.03 $6.29 $7.5535 - 39 $0.32 $1.58 $3.16 $4.74 $6.32 $7.90 $9.4840 - 44 $0.42 $2.10 $4.20 $6.30 $8.40 $10.50 $12.6045 - 49 $0.63 $3.14 $6.28 $9.42 $12.55 $15.69 $18.8350 - 54 $1.02 $5.11 $10.22 $15.33 $20.45 $25.56 $30.6755 - 59 $1.73 $8.67 $17.33 $26.00 $34.66 $43.33 $51.9960 - 64 $2.73 $13.67 $27.35 $41.02 $54.69 $68.37 $82.0465 - 69 $4.52 $22.59 $45.18 $67.78 $90.37 $112.96 $135.5570 - 74 $7.86 $39.31 $78.62 $117.93 $157.25 $196.56 $235.8775 - 79 $13.13 $65.65 $131.31 $196.96 $262.62 $328.27 $393.9280 - 84 $22.63 $113.16 $226.32 $339.47 $452.63 $565.79 $678.95

BI-WEEklY EMPlOYEE DEDucTIONS (SPOuSE cOVERAGE) - GuARANTEE ISSuE=$20,000

BI-WEEklY EMPlOYEE DEDucTIONS - GuARANTEE ISSuE=$100,000

Age Brackets $10,000 $50,000 $100,000 $150,000 $200,000 $250,000 $300,00015 - 19 $0.33 $1.64 $3.28 $4.92 $6.55 $8.19 $9.8320 - 24 $0.40 $1.98 $3.97 $5.95 $7.94 $9.92 $11.9125 - 29 $0.47 $2.35 $4.71 $7.06 $9.42 $11.77 $14.1230 - 34 $0.50 $2.52 $5.03 $7.55 $10.06 $12.58 $15.0935 - 39 $0.63 $3.16 $6.32 $9.48 $12.65 $15.81 $18.9740 - 44 $0.84 $4.20 $8.40 $12.60 $16.80 $21.00 $25.2045 - 49 $1.26 $6.28 $12.55 $18.83 $25.11 $31.38 $37.6650 - 54 $2.04 $10.22 $20.45 $30.67 $40.89 $51.12 $61.3455 - 59 $3.47 $17.33 $34.66 $51.99 $69.32 $86.65 $103.9860 - 64 $5.47 $27.35 $54.69 $82.04 $109.38 $136.73 $164.0865 - 69 $9.04 $45.18 $90.37 $135.55 $180.74 $225.92 $271.1170 - 74 $15.72 $78.62 $157.25 $235.87 $314.49 $393.12 $471.7475 - 79 $26.26 $131.31 $262.62 $393.92 $525.23 $656.54 $787.8580 - 84 $45.26 $226.32 $452.63 $678.95 $905.26 $1,131.58 $1,357.89

ADMINISTERED BY PRuDENTIAlvoluntarY l ife insurance

Questions? call the employee benefits hotline: 1-800-377-7749 13

Your Flexible Spending Account (FSA)

What is a FSA?

there are two types of flexible spending accounts:

Health Care and Dependent Care

flexible spending accounts (fsa) help you save money by providing a way to pay for certain types of health care and dependent care on a pre-tax basis.

How a FSA works

during open enrollment you decide how much money you want to contribute for the year (up to $4,000). You have only one opportunity a year to enroll, unless you have a qualified “life change”. the amount you designate for the year is taken out of your paycheck in equal installments each pay period and placed in a fsa account. as you incur medical expenses that are not fully covered by your insurance, you may submit your expenses for claims transactions using one of the following options:

1) explanation of benefits form from your insurance carrier after a claim has been paid;

2) detail claim from the provider of services (ex: physician/dentist) on the provider of services form with all information related to the service and expenses;

3) a prescription form that you receive from the pharmacy with the information on each prescription you are submitting;

4) a computer form from a pharmacy for prescriptions filled at that pharmacy with all detail information related to the prescriptions/date/costs You may submit any one of the above to evidence claim payment to blue Water administrators.

A way to save taxes

enrolling in a fsa can save you money by reducing your taxable income. Your total savings will depend upon your family income, tax status, and expected amount of health and dependent care costs. the contributions you make to a flexible spending account are deducted from your pay before your federal, state, or social security taxes are calculated and are never reported to the irs. the end result is that you decrease your taxable income and increase your spendable income. You can save hundreds or even thousands of dollars a year.

Estimate expenses carefully

to receive the greatest savings, you must carefully estimate the amount of eligible out-of-pocket expenses you will have for the year. once you have estimated the total annual amount, divide it by 26. that amount is what you may want to have deducted from your gross pay (before taxes) each pay period to be used to fund your flexible spending account. if you terminate before the end of the plan year and have an account balance you may be eligible to elect cobra for this benefit. if you do not elect cobra, any unclaimed contributions will be forfeited. You have 60 days from date of termination to file claims for expenses incurred prior to termination. please see spd for complete plan details.

Do not over estimate

be conservative in your calculations. if you do not incur eligible expenses for the full amount you elected to put in your fsa, the remaining balance in your account will be forfeited according to irs regulations. use it or lose it!

A closer look at Health Care FSA’s

health care flexible spending accounts allow employees to set aside pre-tax dollars taken through a payroll deduction to pay for expenses not covered by any medical or dental plan in which you may be enrolled. these pre-tax dollars are set aside in a personal flexible spending account until needed. the most you may set aside for this account is $4,000 per year.

Eligible expenses

according to irs regulations, the expenses listed on page 16 are eligible to be claimed against a health care fsa. these expenses must be incurred during the plan year and must not be eligible for reimbursement from insurance policies or any other source. also, expenses can only be incurred by you, your spouse, or any dependent (if you furnished over one half of the dependent’s support during the plan year). please use the list on page 16 to estimate the amount you wish to put in your health care fsa. We encourage you to refer to this list during the year to be sure you are taking full advantage of your fsa.

Changes to the Over the Counter Eligibility for Reimbursement - January 1, 2011

healthcare reform has changed the allowable fsa over the counter drugs. the list on pages 16-17 of this guide has been provided in categories of items that will be removed from the *iias list. this list may assist you in determining the amount that you allow for your flexible spending account election, and if you have a health reimbursement account that allows all irs 213 expenses.

A closer look at Dependent Care FSA’s

dependent care flexible spending accounts may be used to pay for work-related child care and adult dependent care expenses you incur for the care of dependent children under age 13 or any disabled dependent who lives with you and who you claim on your taxes. if you use dependent care services for a child, you know how much you need to budget for this expense every month. With an fsa, you set aside money to pay this expense with pre-tax dollars.

What’s best for you?

Your total savings will depend upon your family income, tax status, and total expenses. if you have dependent care expenses, you may choose to claim a tax credit when you file your federal taxes rather than contribute to a dependent care fsa. Your own circumstances will determine whether using a dependent care fsa or the federal income tax credit will be better for you.

Contributions limits

the dependent care fsa allows employees to set aside pre-tax dollars taken through a payroll deduction to pay for work-related child care expenses (daycare must have a valid tax id) or adult dependent care. up to $5,000 can be set aside for this purpose.

flexible spending account ADMINISTERED BY BluE WATER ADMINISTRATORS

seacoast church employee benefits guide 201114

Your Health Reimbursement Account (HRA)

in conjunction with the new health plan, each employee will be provided with a health reimbursement account (hra) to assist in covering deductible costs. seacoast will contribute the following amounts this year.

ElIGIBlE EMPlOYEES: INITIAl cONTRIBuTION ...... $1,100fAMIlY cOVERAGE: INITIAl cONTRIBuTION .......... $2,200

EligiblE EMployEES: WEllNESS PROGRAM cONTRIBuTION ............ uP TO $700

EligiblE SpouSE: WEllNESS PROGRAM cONTRIBuTION ............ uP TO $700

the hra provides first dollar coverage for medical expenses. You may use this money toward your medical deductible. for example, if you have employee only coverage, your annual medical deductible is $3,750 (in-network). Your hra will cover the first $1,100 of expenses. the remaining $2,650 will then be your responsibility unless you have earned additional wellness program contributions.

HRA funds will not roll forward from year to year. Account balances will start over each January 1.

HRA Benefits Card

You will be provided with a benefits card which will assist you in using your hra. this card is to be used only for qualified medical expenses and can be swiped at the time of payment just like a debit card. the money will automatically deduct from your hra. please keep all of your detailed eob’s and/or receipts for charges. You may be asked to submit these to blue Water benefits for verification.

Checking your HRA balance

to check your balance on the hra you will visit the website:

https://employeebwa.lh1ondemand.com

the first time you log onto this site you will use the following username and password:

username: First initial of your first name and then full last name (all lower case) Example: John Smith = jsmith password: changeme1

once you have logged on for the first time you will be prompted to create a new unique password for future login. upon login you will be able to check your hra account balance. click on the My account button and choose to view your account balance.

You may also check your hra account balance by contacting blue Water benefits at 800-377-7749.

How to use your HRA Benefits Card

present your hra benefits card for purchase of medical expenses. please be sure to keep your receipt and you may submit your expenses for claims or benefits card transactions.

FSA Benefits Card

You will be provided with a benefits card which will assist you in using your fsa. this card is to be used only for qualified medical expenses and can be swiped at the time of payment just like a debit card. the money will automatically deduct from your fsa. please keep all of your detailed eob’s and/or receipts for charges. You may be asked to submit these to blue Water benefits for verification.

Checking your FSA balance

to check your balance on the fsa visit the website:

https://employeebwa.lh1ondemand.com

the first time you log onto this site use these credentials:

username: your social security # no dashes Example: 123456789 password: changeme1

once you have logged on for the first time you will be prompted to create a new unique password for future login. upon login you will be able to check your fsa account balance. click on the My account button and choose to view your account balance. You may also check your fsa account balance by contacting the employee benefits hotline at 1-800-377-7749.

File your claims by logging onto the website:

https://employeebwa.lh1ondemand.com

click on the file claiMs link and select the file claim button next to the appropriate account. fill out the form and click submit. print your confirmation page and send a copy of it along with your claim (detail claim from provider, explanation of benefits form from insurance carrier or copy of prescription) to:

blue Water administrators fax#: 843-375-0157

How to file a paper claim

file your paper claims by logging onto the website

https://employeebwa.lh1ondemand.com

click on the forMs link and print. fill out the form and send a copy of it along with your claim (detail claim from provider, explanation of benefits form from insurance carrier or copy of prescription) to:

blue Water administrators | attn: flex 1024 eWall street, ste 101 | Mt. pleasant, sc 29464 fax: 843.375.0157 [email protected]

ADMINISTERED BY BluE WATER ADMINISTRATORShealth reiMburseMent account

Questions? call the employee benefits hotline: 1-800-377-7749 15

Important Change Regarding Over-the Counter (OTC) MedicationsStarting January 1, 2011, OTC medications will require a doctor’s prescription to be eligible for FSA/HSA reimbursement.

As a result, OTC medications cannot be purchased using the mySourceCard® after 12/31/10 unless dispensed by a pharmacy the same as a standard prescription. If a manual claim is submitted for purchase of an OTC medication after 12/31/10, a prescription receipt must be included with the claim in order to receive reimbursement.Non-medicated OTC products (gauze pads, diabetes test strips, saline solution, etc.) are not affected by this change in the law. You can continue to receive FSA/HSA reimbursement for such items after 12/31/10 in the same manner you do now.

Eligible FSA/HSA Healthcare Expenses

Eligible FSA/HSA OTC Medications and Products

*if prescribed for a particular ailment or medical condition; provider letter required

Acupuncture •Alcoholism treatment •Allergy shots and testing•Ambulance (ground or air)•Artificial limbs•Blind services and equipment•Car controls for handicapped*•Chiropractor services •Coinsurance and deductibles•Contact lenses •Crutches, wheelchairs, walkers•Deaf services -- hearing aid/batteries, •hearing aid animal & care, lip reading expenses, modified telephone, etc.Dental treatment•Dentures •Diagnostic tests•Doctor’s fees •Drug addiction treatment & facilities•Drugs (prescription) •

Eye examinations and eyeglasses •Home health and/or hospice care•Hospital services•Insulin •Laboratory fees •LASIK eye surgery•Medical alert (bracelet, necklace)•Medical monitoring and testing •devices*Nursing services •Obstetrical expenses •Occlusal guards •Operations and surgeries (legal)•Optometrists •Orthodontia •Orthopedic services•Osteopaths •Oxygen/oxygen equipment •Physical exams (except for employ-•ment-related physicals)

Physical therapy •Psychiatric care, psychologists, psy-•chotherapists Radial keratotomy •Schools (special, relief, or handi-•capped) Sexual dysfunction treatment •Smoking cessation •Surgical fees •Television or telephone for the hear-•ing impaired Therapy treatments* •Transportation (essentially and pri-•marily for medical care; limits apply)Vaccinations•Vitamins (prescription only)*•Weight loss programs* •X-rays•

Please note that this list is not intended to be comprehensive tax advice. For more detailed information, please consult IRS Publication 501 or see your tax advisor.

Baby care (diaper rash ointments, •teething gel, rehydration fluids, etc.)Contraceptives (condoms, gels, •foams, suppositories, etc.) Eczema & psoriasis remedies•Eye drops, ear drops, nasal sprays•First aid kits •Hemorrhoidal preparations•Hydrogen peroxide, rubbing alcohol•Laxatives•Medicated bandaids & dressings•Motion sickness remedies•Nicotine medications (smoking ces-•sation aids)Pain relievers (aspirin, ibuprofen, •acetaminophen, naproxen, etc.)Sleep aids & sedatives•Wart removal remedies, corn patch• es

ELIGIBLE NOW AND WILL REMAIN ELIGIBLE AFTER 12/31/10 WITH NO PRESCRIPTION REQUIRED:

Braces & supports•Contact lens solution•Diabetic testing supplies & equip-•ment Durable medical equipment (power •chairs, walkers, wheelchairs, CPAP equipment & supplies, etc.)Home diagnostic (pregnancy tests, •ovulation kits, thermometers, blood pressure monitors, etc.)Non-medicated bandaids, rolled •bandages & dressingsReading glasses•

All OTC items listed are examples.

ELIGIBLE NOW, BUT WILL REQUIRE PRESCRIPTION TO REMAIN ELIGIBLE AFTER 12/31/10:

Acne medications & treatments•Allergy & sinus, cold, flu & cough •remedies (antihistimines, deconges-tants, cough syrups, cough drops, nasal sprays, medicated rubs, etc.)Antacids & acid controllers (tablets, •liquids, capsules)Antibiotic & antiseptic sprays, creams •& ointmentsAnti-diarrheals•Anti-fungals•Anti-gas & stomach remedies•Anti-itch & insect bite remedies•Anti-parasitics•Digestive aids•

Eligible FSA/HSA Expenses and OTC Products

healthcare expenses ADMINISTERED BY BluE WATER ADMINISTRATORS

seacoast church employee benefits guide 201116

NON-ELIGIBLE FSA/HSA Healthcare Expenses

NON-ELIGIBLE FSA/HSA Over-the-Counter ProductsThe following are examples of OTC medications & products which are NOT eligible for FSA/HSA reimbursement.

Additional items will join this list effective January 1, 2011, due to changes in the law brought about by the Patient Protection and Affordable Care Act (PPACA) of 2010. See reverse side for additional information.

Advance payment for services to be rendered •Automobile insurance premium allocable to medical •coverageBoarding school fees•Body piercing•Bottled water•Chauffeur services•Controlled substances•Cosmetic surgery and procedures•Cosmetic dental procedures•Dancing lessons•Diapers for Infants•Diaper service•Ear piercing•Electrolysis•Fees written off by provider•Food supplements•Funeral, cremation, or burial expenses•Hair transplant•Herbs & herbal supplements•Household & domestic help•

Health programs, health clubs, and gyms•Illegal operations and treatments•Illegally procured drugs•Insurance premiums (not reimburseable under FSA… •only PRA)Long-term care services•Maternity clothes•Medical savings sccounts•Premiums for life insurance, income protection, dis-•ability, loss of limbs, sight or similar benefitsPersonal items•Preferred provider discounts•Social activities•Special foods and beverages•Swimming lessons•Tattoos/tattoo removal•Teeth whitening•Transportation expenses to & from work•Travel for general health improvement•Uniforms•Vitamins & supplements without prescription •

Aromatherapy•Baby bottles & cups•Baby oil•Baby wipes•Breast enhancement system•Cosmetics (including face cream & moisturizer)•Cotton swabs•Dental floss•Deodorants & anti-perspirants•Dietary supplements•Feminine care items•Fiber supplements•Food•Fragrances•

Hair regrowth preparations•Herbs & herbal supplements•Hygiene products & similar items•Low-carb & low-fat foods•Low calorie foods•Lip balm•Medicated shampoos & soaps•Petroleum jelly•Shampoo & conditioner•Spa salts•Suntan lotion•Toiletries (including toothpaste)•Vitamins & supplements without prescription•Weight loss drugs for general well-being•

NON-ELIGIBLE FSA/HSA Expenses and OTC Products

ADMINISTERED BY BluE WATER ADMINISTRATORShealthcare expenses

Questions? call the employee benefits hotline: 1-800-377-7749 17

eMploYee assistance prograM (eap)

seacoast 403b plan

first sun counselors are available to assist you and all family members who are eligible for company health care benefit issues, addiction, family issues, or life transition issues, assistance is just a phone call away. in addition to these services, each eligible person may also use up to five (5) of the following life management services.

• telephonic legal consultation • family financial counseling • adult care consultation • childcare services • school assistance • college assistance • adoption assistance

first sun eap offers web-based information, articles, self-assessments, and streaming videos that focus on a wide range of behavioral health topics. information about financial planning and financial calculators are also available online.

If you have any questions or need additional materials. first Sun EAP staff are available 24 hours a day, 7 days a week.

Please call: 1-800-968-8143

www.firstsuneap.com

Benefits Member Pays

Individual & family counselingvisits 1-5

$0

Individual & family counselingvisits 6-10

$25 per visit

life Management Services5 visits

$0

ADMINISTERED BY fIRST SuN EAP

seacoast teaches the 10-10-80 principle for the resources god has given us. that means to tithe 10%, save 10% and live off of the remaining 80%. as you think about your 10% savings, your retirement plays an important role. one of the best ways to save for your retirement is through your 403(b) plan at seacoast.

are you saving for your retirement? the responsibility for retirement savings belongs to the employee. employees have choices to make proactive decisions resulting in achieving a secure, healthy and comfortable retirement. this includes the decision to save, how much to invest and how to make their savings last through retirement.

the seacoast 403(b) plan is designed to help you save for your retirement and provide tax advantages.

• seacoast church is currently matching contributions $.50 for every $1 you contribute up to 5% of your income.

• Minimum contribution is $25 per pay period.

What are you waiting for? call your local ameriprise agent to make an appointment and get started saving for your future.

Rich Young Senior Financial Advisor843.971.0982 ext. 201

seacoast church employee benefits guide 201118

DEPENDENT cHIlDREN cOVERAGE NOTIcE

Individuals whose coverage ended, or who were denied coverage (or were not eligible for coverage), because the availability of dependent coverage of children ended before attainment of age 26 are eligible to enroll in Seacoast Church health plan. Individuals may request enrollment for such children during open enrollment. Enrollment will be effective January 1, 2011. For more information contact the Benefits Hotline at 1-800-377-7749.

Your adult children can join or remain on your plan whether or not they are:

• Married; • Living with you; • In school; • Financially dependent on you;

if you are eligible for health coverage from your employer, but are unable to afford the premiums, some states have premium assistance programs that can help pay for coverage. these states use funds from their Medicaid or chip programs to help people who are eligible for employer-sponsored health coverage, but need assistance in paying their health premiums.

if you or your dependents are already enrolled in Medicaid or chip, you can contact your state Medicaid or chip office to find out if premium assistance is available.

if you or your dependents are not currently enrolled in Medicaid or chip, and you think you or any of your dependents might be eligible for either of these programs, you can contact your state

Medicaid or chip office or dial 1-877-Kids noW or www.insurekidsnow.gov to find out how to apply. if you qualify, you can ask the state if it has a program that might help you pay the premiums for an employer-sponsored plan.

once it is determined that you or your dependents are eligible for premium assistance under Medicaid or chip, your employer’s health plan is required to permit you and your dependents to enroll in the plan – as long as you and your dependents are eligible, but not already enrolled in the employer’s plan. this is called a “special enrollment” opportunity, and you must request coverage within 60 days of being determined eligible for premium assistance.

u.s. department of labor u.s. employee benefits security administration www.dol.gov/ebsa 1-866-444-ebsa (3272)

department of health and human services centers for Medicare & Medicaid services www.cms.hhs.gov 1-877-267-2323, ext. 61565

Medicaid and the Children’s Health insurance Program (CHiP) offer free or low-Cost Health Coverage to Children and families

for more information on special enrollment rights, you can contact either:

You should contact your state for further information on eligibilitysouth carolina – Medicaid

Website: http://www.scdhhs.govphone: 1-888-549-0820

iMportant notices regarding Your benefits plan

Questions? call the employee benefits hotline: 1-800-377-7749 19

MEDIcARE PART D cREDIBlE cOVERAGE NOTIcE

prior to november 15, 2007, all employers who offer a medical plan that provides pharmacy coverage are required to send a notice to all plan participants who are eligible for Medicare. because we do not track which of our employees are eligible for Medicare, we are meeting this obligation by providing this notice to all employees who are eligible for our benefits program. this notice does not apply to you if you or your dependents are not Medicare eligible. if you or a covered dependent are Medicare eligible or will become Medicare eligible in 2010 or 2011, this notice is important to you and contains important, time sensitive information. please read it carefully and act accordingly to protect your interests.

please read this notice carefully and keep it where you can find it. this notice has information about your current prescription drug coverage with seacoast church, and prescription drug coverage available for people with Medicare. it also tells you where to find more information to help you make decisions about your prescription drug coverage.

• Medicare prescription drug coverage became available in 2006 to everyone with Medicare through Medicare prescription drug plans and Medicare advantage plans that offer prescription drug coverage. all Medicare prescription drug plans provide at least a standard of coverage set by Medicare. some plans may also offer more coverage for a higher monthly premium.

• seacoast church has determined that the prescription drug benefit offered through seacoast church medical plan is, on average for all plan participants, expected to pay as much as the standard Medicare prescription drug coverage and is considered creditable coverage.

individuals can enroll in a Medicare prescription drug plan when they first become eligible for Medicare and each year from november 15th through december 31st. however, because you have existing prescription drug coverage that, on average, is as good as Medicare coverage, you can choose to join a Medicare prescription drug plan later. each year after that, you will have the opportunity to enroll in a Medicare prescription drug plan between november 15th through december 31st. if you do decide to enroll in a Medicare prescription drug plan and want to drop your seacoast church prescription drug coverage you will have to drop all of your healthcare coverage with seacoast church since prescription drug coverage is a part of your seacoast church healthcare plan. please be aware that you may not be able to get this coverage back should you decide to drop it.

You should compare your current coverage, including which drugs are covered, with the coverage and cost of the plans offering Medicare prescription drug coverage in your area. Your current coverage pays for other health expenses in addition to prescription drugs. You will be eligible to receive all of your current health and prescription drug benefits even if you choose to enroll in a Medicare prescription drug plan.

You should also know that if you drop or lose your coverage with seacoast church and don’t enroll in Medicare prescription drug coverage after your current coverage ends, you may pay more to enroll in Medicare prescription drug coverage later. if you go 63 days

or longer without prescription drug coverage that’s at least as good as Medicare’s prescription drug coverage, your monthly premium will go up at least 1% per month for every month that you did not have that coverage. for example, if you go nineteen months without coverage, your premium will always be at least 19% higher than what most other people pay. You’ll have to pay this higher premium as long as you have Medicare coverage. in addition, you may have to wait until the following november to enroll.

for more information about this notice or your current prescription drug coverage, contact our customer service team for further information at 1-800-370-1578. note: You may receive this notice at other times in the future such as before the next period you can enroll in Medicare prescription drug coverage, and if this coverage changes. You also may request a copy at any time.

More detailed information about Medicare plans that offer prescription drug coverage is available in the ’Medicare & You’ handbook. You will get a copy of the handbook in the mail every year from Medicare. You may also be contacted directly by Medicare prescription drug plans. You can also get more information about Medicare prescription drug plans from these places:

• visit www.medicare.gov.

• call your state health insurance assistance program (see your copy of the Medicare & You handbook for their telephone number) for personalized help.

• call 1–800–Medicare (1–800–633–4227).

ttY users should call 1–877–486–2048

for people with limited income and resources, extra help paying for a Medicare prescription drug plan is available. information about this extra help is available from the social security administration (ssa). for more information about this extra help, visit ssa online at www.ssa.gov, or call them at 1–800–772–1213 (ttY1–800–325–0778).

remember: Keep this notice. if you enroll in one of the Medicare approved plans offering prescription drug coverage, you may need to provide a copy of this notice when applying for the coverage to show that you are not required to pay a higher premium amount.

lIfETIME lIMIT cHANGE NOTIcE

The lifetime limit on the dollar value of benefits under Seacoast church no longer applies. Individuals whose coverage ended by reason of reaching a lifetime limit under the plan are eligible to enroll in the plan. for more information contact Blue Water Benefits at 1-800-377-7749.

iMportant notices regarding Your benefits plan