2011 ny investor conference v8 - commercebank.com

TRANSCRIPT

INVESTOR OVERVIEWFebruary 2011February 2011

Charles KimExecutive Vice President and Chief Financial Officer

Jeffery AberdeenController

Nicole RoseManager Mergers and Acquisitions

CAUTIONARY STATEMENT

A b f t t t ill b ki i t ti dA number of statements we will be making in our presentation andin the accompanying slides are “forward-looking statements”within the meaning of the Private Securities Litigation Reform Actof 1995, such as statements of the Corporation’s plans, goals,

bj i i j i i d i iobjectives, expectations, projections, estimates and intentions.These forward-looking statements involve significant risks anduncertainties and are subject to change based on various factors(some of which are beyond the Corporation’s control). Factorsthat could cause the Corporation’s actual results to differmaterially from such forward-looking statements made herein orby management of the Corporation are set forth in theCorporation’s Third Quarter Report on Form 10-Q and theCorporation’s Current Reports on Form 8-K.

1

S C it B k 145 i th i d t $18 billi i t

ABOUT COMMERCE BANCSHARES

Lower Midwest Footprint – over 370 banking locations and 4,979 employees• 71% of 2010 pre-tax profits from five key markets

Super-Community Bank – over 145 years in the industry – $18 billion in assets

p p y• Denver and Tulsa markets added in 2007• Lending presence in Nashville and Cincinnati • Commercial Payment Services offered in 48 states

Major Markets- Kansas City- St. Louis- Wichita

S i fi ld

Performance – CAGR

20102010 1010

St. Louis & Kansas CityDeposit Market Share**

2010

- Springfield- Peoria/Bloomington

20102010 10yr10yr

EPS*EPS* 28%28% 4%4%

Cash Div*Cash Div* 3%3% 9%9%

Stock PriceStock Price 8%8% 4%4%

2010US Bancorp 12% BoA 11% Commerce 8% UMB 5%

Total ReturnTotal Return 10%10% 6%6%UMB 5%Others 64%

*Per share figures have been restated for 5% stock dividend distributed on 12/20/10**Source: FDIC 2010 Deposit Data 2

ABOUT OUR MARKETS

KKansas City St. Louis Denver Tulsa Outstate1

2010 Population (000’s) 2,031 2,835 2,582 930 1,759

5-Year Projected Growth 4.0% 1.7% 7.2% 3.5% 3.9%

CBI M kCBI Market Penetration2 23.8% 19.3% 0.4% 0.5% 15.5%

Median Household $57 $54 $62 $47 N/AIncome (000’s)$57 $54 $62 $47 N/A

Unemployment rate3 9.1% 9.5% 8.7% 7.5% 8.2%

2009 FDIC CBI Deposits (000’s)

$4,508 $4,308 $80 $109 $2,501

Deposit Share 11.7% 6.9% 2.8% 0.7% 6.6%1.Outstate includes Wichita, Springfield, Columbia, Peoria and Bloomington2. 2010 households in county with CBI branch3. U.S. Bureau of Labor Statistics as of November 2010Source: Nielsen and U.S. Bureau of Labor Statistics 3

SUPER-COMMUNITY BANK PLATFORM

Super-Regional Back End

A More Nimble Format … With Higher Service Focus

Community Bank Front End Super-Regional Back End • Sophisticated payment processing systems• Broad consumer product offerings• Private banking; trust; capital markets

Community Bank Front End• Flat organization – quick decisions• Employees embrace strong culture• Award winning customer service

K l d f t d k t • Competitive on unit costs• Knowledge of customers and markets reduces risk

A Strategy that Builds Results for Tomorrow• Sales across business lines

Focus on people/talent development• Focus on people/talent development• Investment in technology• Top quartile credit quality metrics• Disciplined approach to acquisitionsp pp q

4

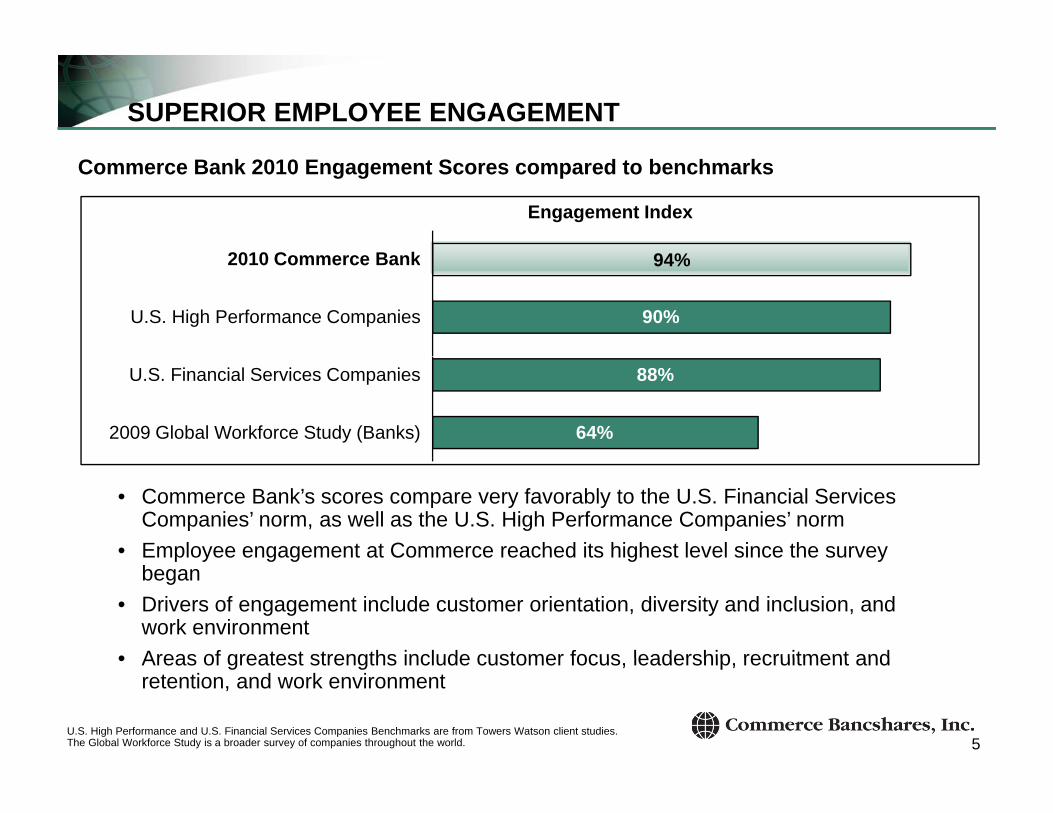

SUPERIOR EMPLOYEE ENGAGEMENT

94%2010 Commerce Bank

Engagement Index

Commerce Bank 2010 Engagement Scores compared to benchmarks

94%

U.S. High Performance Companies 90%

2010 Commerce Bank

2009 Global Workforce Study (Banks) 64%

U.S. Financial Services Companies 88%

• Commerce Bank’s scores compare very favorably to the U.S. Financial Services Companies’ norm, as well as the U.S. High Performance Companies’ norm

• Employee engagement at Commerce reached its highest level since the survey p y g g g ybegan

• Drivers of engagement include customer orientation, diversity and inclusion, and work environment

• Areas of greatest strengths include customer focus leadership recruitment and

U.S. High Performance and U.S. Financial Services Companies Benchmarks are from Towers Watson client studies. The Global Workforce Study is a broader survey of companies throughout the world.

• Areas of greatest strengths include customer focus, leadership, recruitment and retention, and work environment

5

INDUSTRY RECOGNITION AND CUSTOMER SATISFACTION

Commerce Bank Ranked Highest Customer Satisfaction

America’s Best Banks by Forbes Magazine 2010 J.D. Power Retail Banking Results

Commerce ranked in the top ten on the list of America's Best Banks by Highest Customer Satisfaction

with Retail Banking in the Midwest Region Three Years in a Row*

the list of America s Best Banks by Forbes Magazine

Commerce Score = 809 Co e ce Sco e 809Midwest Bank Average = 746 Competitors of note: UMB = 765, Nat City/PNC = 761, US Bank = 748, BOA = 723, Regions = 717

Recognized as one of the best regional banks in America for overall

2010 Greenwich Excellence Award

regional banks in America for overall customer satisfaction.

*Commerce Bank received the highest numerical score among retail banks in the Midwest region in the proprietary J.D. Power and Associates 2008-2010 Retail Banking Satisfaction StudiesSM, tied in 2009. 2010 study based on a total of 47,673 total responses measuring 18 providers in the Midwest region(IA, IL, KS, MO, MN, WI) and measures opinions of consumers with their primary banking provider. Proprietary study results are based on experiences and perceptions of consumers surveyed in January 2010. Your experiences may vary. Visit jdpower.com. 6

DIVERSE REVENUE SOURCES

• Balanced mix of interest and non-interest income• Meaningful contribution from wealth management and card businesses

Commerce Bank Peer Banks*

14%

Commerce Bank

4%

7%

Peer Banks

10% 61%

7%

8% 68%

6%

9%1%

10%

3%1%

Card incomeWealth management

OtherService charges

Fees & commissionNet interest income

Note: Excludes Gains and Losses on SecuritiesSource: Financial Information Systems; Data as of 9/30/10

* Peer Banks include: ASBC, BOKF, Central Bancompany, CYN, CFR, FMER, MBFI, PVTB, TCB, UMBF, WTFC, ZION

7

IMPROVED EARNINGS RESULT FROM LOWER PROVISION AND GOOD EXPENSE CONTROL

($ in millions) 2008 2009 201009 vs. 10 % change

Net Interest Income $593 $636 $646 2%Non-Interest Income 376 396 405 2%

Total Revenue $968 $1,032 $1,051 2%Securities Gains/(Losses) 30 (7) (2) (75%)Non-Interest Expense (615) (621) (631) 2%Provision for Loan Losses (109) (161) (100) (38%)Pre-Tax Income 274 243 318 31%

Income Taxes (85) (74) (96) 30%

Net Income $189 $169 $222 31%

Dil t d EPS* $2 24 $1 97 $2 52 28%Diluted EPS* $2.24 $1.97 $2.52 28%

ROA 1.15% 0.96% 1.22%

ROE 11.8% 9.8% 11.2%

Efficiency Ratio 63.1% 59.9% 59.7%

*Restated for 5% stock dividend on 12/20/2010 8

GROWTH IN CARD AND COMMERCE TRUST COMPANY DRIVE TOP LINE GROWTH

($ in millions) 2008 2009 201009 vs. 10% change

Interest Income $850 $790 $729 (8%)( )Interest Expense $257 $154 $83 (46%)

Net Interest Income $593 $636 $646 2%

Contribution fromContribution from …Deposit fees 110 106 93 (12%)Cards 114 122 149 22%T t 80 77 81 5%Trust 80 77 81 5%

Bond Trading & Brokerage 28 33 30 (9%)

Other 44 58 52 (10%)

Non-Interest Income $376 $396 $405 2%

Total Revenue $969 $1,032 $1,051 2%

9

CONTINUED FOCUS ON EXPENSE MANAGEMENT

($ in millions) 2008 2009 201009 vs. 10% change

Salaries & Benefits $334 $346 $347 0%$ $ $ 0%

Occupancy 46 46 47 2%

Equipment 25 26 23 (9%)

Supplies & Communications 35 32 27 (16%)

Data Processing 56 62 68 10%

Other 93 85 93 8%Other 93 85 93 8%

Subtotal: Controllable Expense $589 $597 $604 1%

Deposit Insurance 2 27 19 (30%)

Non-recurring* 24 (2) 7

Total Non-Interest Expense $615 $622 $631 1%

* Excludes partial reversal of VISA litigation expenses in all three years and loss on auction rate securities of $33 million in 2008

10

INVESTMENT PORTFOLIO: HIGH QUALITY, DIVERSE, SHORT DURATION

ARCsAsset Backed

12/31/2009 PORTFOLIO

Unrealized Gain $72 million12/31/2010 PORTFOLIO

Agency2.8%

Treasury6.1%

2.3%33.4%

Unrealized Gain $72 millionInvestment Grade 96.9%

Duration2007 2 07 yrs

Total investments $7.4 billionUnrealized gain $130 million12 mo maturities $2.1 billionCorporate 2.4%

2007 2.07 yrs2008 2.39 yrs2009 2.09 yrs

DurationDec 2010 2.08 yrsDec 2009 2.09 yrsDec 2008 2.39 yrs

8.7%8 7%

Municipal13.2%

Agency MBS

31.0%

8.7%8.7%

Non-Agency MBS

Source: InTrader 11

SLIGHT INCREASE IN C&I LOANS WHILE UTILIZATION RATES REMAIN LOW

Loan Trends$ in thousands

Bal

ance

s

50.00%

60.00%

3,500,000

4,000,000

zatio

n R

ate

sine

ss L

oan

30.00%

40.00%

2,500,000

3,000,000

Util

iz

uart

erly

Bus

0 00%

10.00%

20.00%

1 500 000

2,000,000

,500,000

Qu 0.00%1,500,000

4Q103Q102Q101Q104Q093Q092Q091Q094Q083Q082Q081Q08

Business Loan BalancesUtilization Rate

12

EARNINGS PERFORMANCE SIGNIFICANTLY ABOVE PEERS AND LARGE BANKS

Return on Assets Return on Equity

Financial Returns

CBSH 2010

CBSH 2010 ROE

1.19%

0.96%

1.15%

1.00%1.10%1.20%

10.98%

9.76%

11.81%

10.00%11.00%12.00%

Return on Assets Return on Equity

8 57%

ROA1.22%

ROE11.15%

0 49%

0.69%

0.60%0.70%0.80%0.90%

6.75%6.95%

6.00%7.00%8.00%9.00%0.86% 8.57%

7.17%0.65%

0.49%0.42%

0.27%

0.20%0.30%0.40%0.50%

4.11%3.24%

2.00%3.00%4.00%5.00%

0.00%0.10%

Sept YTD 2010

200920080.00%1.00%

Sept YTD 2010

20092008

*Peer Banks include: ASBC, BOKF, CYN, CFR, FMER, MBFI, PVTB, TCB, UMBF, WTFC, ZION **Large banks include: JP Morgan, Citigroup, BoA, Wells Fargo, US Bancorp, Regions, Fifth Third, M&I, PNC, State StreetSource: SNL Financial

Large Banks**Peer Banks*Commerce Bank

13

STRONG AND QUALITY CAPITAL POSITION

14 3%16.0%

18.0%

13 8%14.3%

17.7%1.6%

Rat

io

3.0%

11.5%12.3%

13.2%14.3%

3 1%3.5%3.1%

3.8% 0.4%0.4%

10.0%

12.0%

14.0%

0.2%

13.8%

2.9%

12.8%

1.4%

0.8%12.1%0.9%

14.0%

1.1%

1.3%2.3%

10.0%0.9%

10.3%0.8%

13.4%1.1%

10.8%

djus

ted

Ass

ets

3.9%3.3%3.1%

4.0%

6.0%

8.0%

6.7%7.2%7.5%7.7%8.6%8.6%9.1%9.6%

12.2%12.2%

Cap

ital /

Ris

k A

d

0.0%

2.0%

6.7%

FITBHBANRFZIONKEYCMATCBFMER MIASBC CFRBOKFUMBFCBSH

Tier

1 C

Among bank holding companies over $10 billion, CBSH is Moody’s highest rated (B+) for financial strength*

Tier 1 CommonTARP PreferredTruPSOther

*Moody’s as of 12/13/2010; Tied with two other banksSource: SNL Financial; Data as of 9/30/2010

for financial strength

14

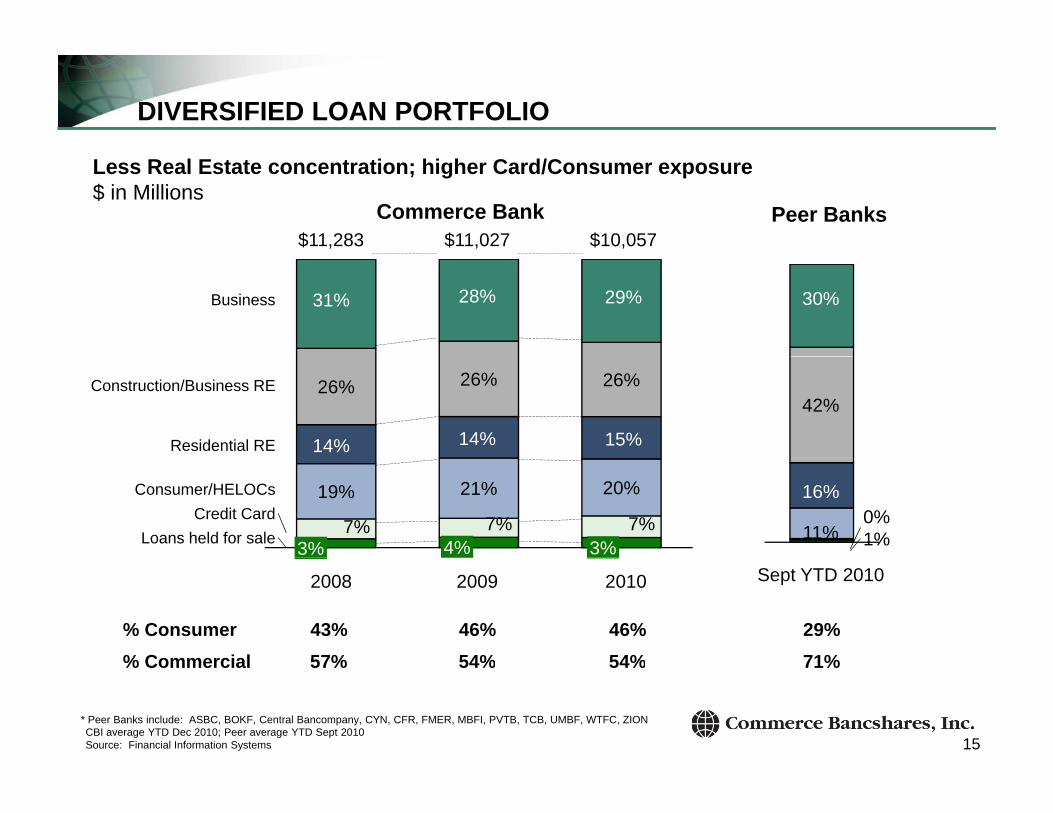

DIVERSIFIED LOAN PORTFOLIO

Commerce Bank Peer Banks$11,027 $10,057$11,283

Less Real Estate concentration; higher Card/Consumer exposure$ in Millions

30%Business 29%28%31%

42%26% 26% 26%

Residential RE

Construction/Business RE

15%14%14%

1%0%

11%

16%

7% 7% 7%

19% 21% 20%

Loans held for saleCredit Card

Consumer/HELOCs

4% 3%3%Sept YTD 20102009 20102008

% Consumer 43% 46% 46% 29%% Commercial 57% 54% 54% 71%% Commercial 57% 54% 54% 71%

CBI average YTD Dec 2010; Peer average YTD Sept 2010 Source: Financial Information Systems

* Peer Banks include: ASBC, BOKF, Central Bancompany, CYN, CFR, FMER, MBFI, PVTB, TCB, UMBF, WTFC, ZION

15

RESERVES REMAIN STRONG; WHILE NPAs CONTINUE DOWNWARD TREND

Reser e co erage among ind str 's best

1 2%1.4%

$200

$240

Reserve coverage among industry's best

0.6%0.8%1.0%1.2%

$120

$160

$200

s to

Loa

ns

Mill

ions

0.0%0.2%0.4%

$0

$40

$80

NPA

's

$ in

'05 '06 '07 '08 09 1Q10 2Q10 3Q10 4Q10

$ Allow for Loan Loss $ Non-Perform Assets

% NPA to Total Loans

• NPAs at 6/30/10 decreased by $19 million in 2010; now 1% of total loans• Reserve coverage of 203% of NPAs at 12/31/10• Reserve coverage of 203% of NPAs at 12/31/10

16

Largest 100CBINet Charge-Off Rates for CBI vs. Other Banks

CHARGE-OFFS CONSISTENTLY BETTER THAN INDUSTRY

3.00%

3.50%

Largest 100CBI

3.00%

3.50%

Business C&I Net C/OsNet Charge Off Rates for CBI vs. Other Banks

2.59%2.65% 2.51%

3.42%

2.78% 2.72% 2.80%

Commercial R/E Net C/Os

1.00%

1.50%

2.00%

2.50%

1.00%

1.50%

2.00%

2.50%1.97% 1.78% 1.65%

2.51%

0 44%0.74%

0 39%0.80%

1.58% 1.70%

0.00%

0.50%

Sep‐10Jun‐10Mar‐10Dec‐09Sep‐090.00%

0.50%

Sep‐10Jun‐10Mar‐10Dec‐09Sep‐09

Credit Card Net C/Os

0.11%0.44%

Consumer Net C/Os Credit Card Net C/Os

0.29%0.05%

0.39% 0.23%

3.00%

3.50%

4.00%

9 00%

10.00%

11.00%

12.00%

3.33%3.15%

2 63%

10.32%9.42%

10.16%10.98%

8.53%

Consumer Net C/Os Credit Card Net C/Os

1.50%

2.00%

2.50%

5.00%

6.00%

7.00%

8.00%

9.00%2.63%

2.18%6.55%

1.59%1.90%1.86%

2.24%

1.72%1.50%

6.85% 6.50% 6.94% 6.70%

17

1.00%

Sep‐10Jun‐10Mar‐10Dec‐09Sep‐094.00%

Sep‐10Jun‐10Mar‐10Dec‐09Sep‐09

Source: Federal Reserve

Description

OUR AREAS OF FOCUS REFLECT THE CHALLENGES AND OPPORTUNITIES THAT WE SEE IN THE MARKETPLACE

• Add high quality loans across lending categories, at appropriate spreads

Description

Build new customer

Grow quality loans

A i d i d i h l l i hirelationships Build relationship deposits

• Acquire and retain deposits that are truly relationship-based

Manage and develop • Invest in developing talent

Maintain our distinctive

Enhance operating productivity

• Continuously improve cost discipline• Emphasize sales force effectiveness

Manage and develop talent • Manage productivity

advantagesproductivity

Reinvigorate fee income

• Replace lost fee income from changes in regulation and customer behavior

• Align fees with value to customers

Invest in high return business

Expand payments systems business

• Continue emphasis on commercial card, merchant, and treasury businesses

• Develop and pilot new products

G • Capitalize on market disruption to acquire new customersbusiness Grow money management

Capitalize on market disruption to acquire new customers• Deepen relationships with existing CTC and bank

customers

18

RETAIL - 2011 PLAN HIGHLIGHTS

CORE RETAIL STRATEGIESCORE RETAIL STRATEGIESCORE RETAIL STRATEGIESCORE RETAIL STRATEGIES

Create new revenue streams from

Refine marketing strategy and

Drive for improved productivity

Accelerate Channel Innovation

Align spending with new revenue

Manage Critical Issues for Customer /streams from

product lines and/or services

strategy and customer experience to drive more business

productivity, empowerment and accountability of our frontline

Innovation new revenue paradigm

for Customer / Support / Service / Infrastructure

business of our frontline staff

2011 Key Initiatives2011 Key Initiatives

• Re-energize direct lending model• New products / “apps” to expand revenue streams (electronic stmt. histories)

I t d d b h l t l t t t l lt t l

2011 Key Initiatives2011 Key Initiatives

• Introduced new branch sales tools to generate greater cross sales results; new customer sales• Generate more revenue through online channel• Address branch costs – right number branch locations; refine branch operating costs• Proactively address regulatory issues (overdraft debit)Proactively address regulatory issues (overdraft, debit)

19

LEVERAGE ONLINE CHANNEL: OVER 60% OF RETAIL CUSTOMERS ACTIVELY USE ONLINE BANKING

We expect to drive revenue with various approaches:We expect to drive revenue with various approaches:

• Open and fund Deposit accounts

• Apply for loans

Open accounts • Apply for loans

• Apply for credit cards

Example:

Online check shopping• Shop for new and re-order existing

• Increases spend per order

Sell add-on services

p p25%

• Incremental $200k+ per year

• e-Statement and Reg E• Existing marketing

campaigns

Cross-sell with targeted marketing

• Create custom messages and offers

20

RETAIL - ALIGN SPENDING WITH CURRENT REVENUE MODEL

G l R d t hil

Core Retail2010 Expenses = $235 million

Goal: Reduce costs while maintaining sales/service/risk management expectations

F l j t d t$67 million

$64 million

• Formal projects underway to re-engineer operating models

• Examples:St ffi d l i l l–Staffing model – universal employee

–Self-service delivery options at branches

• Reduced 2010 expenses $18 million (6%)

$104 million

(6%)

Direct expenseProcessing costsAdminstrative costs

21

COMMERCIAL - OPPORTUNITIES FOR LOAN GROWTH

Working capital tili ation %• Working capital utilization %

• Industry opportunities Healthcare

25%

2007-2010 Loan Growth Trend

Agribusiness Beverage Distribution

• New markets16%

21%20%

25%

Denver Tulsa Cincinnati9%

16%

10%

15%

Nashville

• Refinancing CMBS transactions

• Asset purchases0%

5%

• Asset purchases

• Tax advantage loan programs

• Government programs

0%Beverage AgribusinessHealthcare

SBA/USDA/MO Link

YTD Average Balance 22

COMMERCIAL – OPPORTUNITIES FOR LOAN GROWTH

23

COMMERCIAL - DEPOSITS & THE PAYMENT SYSTEM

• Focus on payments processing$3 500

Deposit Growth Trend

Wholesale lockbox processing

Remote deposit volume up 13%

Enhancing online banking platform

$3,500

3,000

2,500

+32%

Enhancing online banking platform

• Transition from paper to electronic

Procurement card

2,000

1,500

ACH

Check conversion

• Evaluating Reg Q impact

500

1,000

0 • Evaluating Reg Q impact

• Focused calling for Merchant Bankcard2008

020102009

Non-InterestInterest

24

COMMERCE TRUST COMPANY – OVERVIEW

• $25 billion in assets under administration

As one of the largest trust companies in the US, The Commerce Trust Company excels at providing objective financial advice, exceptional personal service and comprehensive wealth management solutions.

$25 billion in assets under administration• Ranked #27 based on assets under management*• A team of over 470 and the average officer has 15 years of experience• 100+ years in the business

A growth opportunity for Commerce Bank• Third consecutive year of record asset management sales ($8.1 million)• Achieved all time highs in account retention and client satisfaction scores• Achieved all time highs in account retention and client satisfaction scores• Private banking deposits growth of 20% in 2010 for a total of $1.3 billion in deposits;

loans total $671 million• Strong investment performance from both proprietary & open architecture portfolios

C B d F d k d t 5 b t i k dj t d b d t l f d– Commerce Bond Fund ranked among top 5 best risk adjusted bond mutual funds by Smart Money Magazine (Oct. 2010)

• Fee waivers of $6 million per year continue on short-term client assets due to low interest rates

• Ultra high net worth (Family Office) trust business expanding; assets now total $5.9 billion

25*Source: FDIC - Fiduciary related assets as of Sept 30, 2010

COMMERCE TRUST COMPANY – 2011 INITIATIVES

Target Markets for Enhanced Institutional Trust Services

• Retirement Plan Services/401(k)– $5 - $50 million in assets

• Fixed Income Management– Hospitals, insurance, colleges and

– Complex plan designs– Poor advisor support

• Investment ConsultingFoundations corporations insurance

universities– $10 million and up

• Specialized Nonprofit ServicesBack office support– Foundations, corporations, insurance

– $10 - $100 million– Underserved by consulting

community

– Back office support– Charitable gift administration– Needs that go beyond money

management

• Target Emerging Wealth Segment ($100 to $500k)

Restructure of Commerce Brokerage/Integration with CTC

• Synergies will allow for new product development for brokerage customers• Greater financial planning & investment tools to serve clients• Improved technology for back office will lower costs while offering more competitive

products

26

CARD PRODUCTS – A LEADER IN THE PAYMENTS INDUSTRY

Among US Banks, Nilson Ranks Commerce Bank:

Debit / PrepaidDebit / Prepaid Card#33 Debit Card Issuer

Consumer Card

Merchant

#25 Consumer Card Issuer

Merchant Services#13 Bank Acquirer*

Commercial Card

#9 Purchasing Card Issuer

* Excludes non-bank acquirers 27

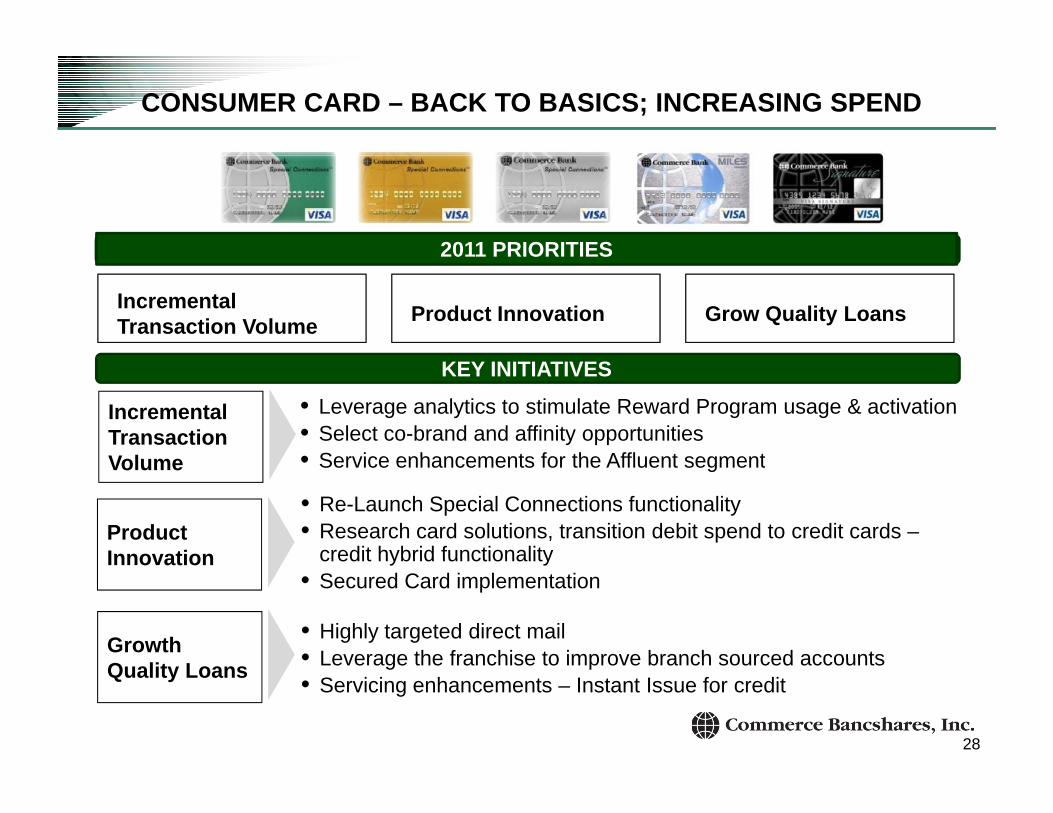

CONSUMER CARD – BACK TO BASICS; INCREASING SPEND

2011 PRIORITIES

Incremental Transaction Volume Product Innovation Grow Quality Loans

2011 PRIORITIES

KEY INITIATIVES

Incremental Transaction V l

• Leverage analytics to stimulate Reward Program usage & activation• Select co-brand and affinity opportunities• Service enhancements for the Affluent segmentVolume • Service enhancements for the Affluent segment

Product Innovation

• Re-Launch Special Connections functionality• Research card solutions, transition debit spend to credit cards –

credit hybrid functionalityInnovation credit hybrid functionality• Secured Card implementation

Growth • Highly targeted direct mail• Leverage the franchise to improve branch sourced accountsQuality Loans • Leverage the franchise to improve branch sourced accounts• Servicing enhancements – Instant Issue for credit

28

STRONG RESULTS IN COMMERCIAL CARD & OPPORTUNITIES IN MERCHANT PROCESSING WARRANT CONTINUED INVESTMENT

Commercial C d

• 40 sales reps covering territories across 48 states• CCX Volume grew to over $1 6 billion with a 148%

2011 PLAN HIGHLIGHTS

Card expansion

• CCX Volume grew to over $1.6 billion with a 148% growth rate and now comprises ½ of entire portfolio

Medical • Sold 93 hospitals in 2010, representing over $1.1 billion

in potential spenderci

al

rd

KEY INIIATIVESverticalp p

• Goal to add over 100 new hospital clients in2011

S d

• B2B Electronic Invoice Presentment and Payment Product• Natural extension to AP product offering

Com

me

Car

Syncada by VisaNatural extension to AP product offering– Implement and Launch Product – Select current clients for pilot and sign 10 total clients

Referral • Leverage internal referral networks (Commercial bank Referral network

g (and Retail Bank) to drive Merchant sales

Industry and t dM

erch

ant

roce

ssin

g

• Cost effectively provide access to hundreds of leads– Signed three associations in 2010 representing over

trade associations

M Pr 700 hospitals and more than 100 self-storage companies

29

PRODUCT OPPORTUNITIES IN THE PAYMENTS SYSTEM

• Reduces costs• Combines payment processes for all

suppliers

Payment

suppliers• Provides automated expense allocation• Enhances supplier relationships with

standard data processes and on-time payments

Commerce Bank Advantagespayments

• Easy access to data through a single online system

Processing• Expands payment product offering

• Creates tighter paymentonline system• Removes manual processes allowing for

efficient enforcement of compliance and controls

• Ensures on time payments eliminating

• Creates tighter payment integration with our customers

• Generates additional• Ensures on time payments eliminating late payment penalties

O ti i t t f b d

Financing

• Generates additional revenue income

• Optimizes payment terms for buyers and suppliers while maximizing working capital

30

M&A POSTURE

• We are strategic buyers

• Focus on opportunities to round out our existing core footprint

• Augment expansion markets if strategic fits become available

• FDIC deals increasingly less attractive

• Healthy bank sales may present opportunities in future

• Targeted loan purchases; management lift outs could be

CAPITALIZING ON OUR POSITION OF STRENGTH:

• Targeted loan purchases; management lift-outs could be attractive

CAPITALIZING ON OUR POSITION OF STRENGTH: ORGANIC GROWTH IS PRIORITY ONE

31

RECAP OF THEMES…

• 2011: Credit picture much improved, but still a h ll i i t f b kchallenging revenue environment for banks

• Commerce well positioned; emphasis on revenue and operating modelsand operating models

• Areas of focus:–Creating new customer relationships–Creating new customer relationships–Building on our strengths People, operations, products

– Investing in high return businessesInvesting in high return businesses

32

EARNINGS RECOVER IN 2010, THOUGH REVENUES MAY BE CHALLENGED

$3.00

$12 00

$13.00 Revenue Per Share Earnings Per Share

$2.20

$2.60

$10 00

$11.00

$12.00

r Sha

re

r Sha

re

$1.80

$

$8 00

$9.00

$10.00

arni

ngs

Per

even

ue P

er

$1 00

$1.40

$6 00

$7.00

$8.00 EaR

$1.00 $6.00 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Dividends per share* $0.39 $0.42 $0.53 $0.65 $0.72 $0.77 $0.82 $0.86 $0.87 $0.90

*Restated for 5% stock dividend distributed in December 2010

per share*

33

CONTINUING COMMITMENT TO SHAREHOLDER RETURN

T t l h h ld t *Total shareholder returns*Indexed, 12/31/1999 = 100

180200 COMMERCE

BANK

120140160180

S&P 500INDEX

BANK

6080

100INDEXNASDAQBANKS

402000 2002 2004 2006 2008 2010

Annualized returns*Percent

3 yr3 yr 5 yr5 yr 10 yr10 yrCBSHCBSH 3.3%3.3% 1.7%1.7% 6.4%6.4%S&P 500S&P 500 (2.9%)(2.9%) 2.3%2.3% 1.4%1.4%

*Assumes reinvested dividendsSource: NASDAQ & S&P

NASDAQ BanksNASDAQ Banks (10.3%)(10.3%) (8.5%)(8.5%) 0.2%0.2%

34