2010 currency hedging in world index equity fund

TRANSCRIPT

EQUITIES | CAPABILITIES

Currency Hedging in SSgA’s World Index Equity Fund

With its broad geographical coverage, the MSCI World

Index is generally considered to be a good approximation

of the equity market portfolio, as defi ned by the Capital

Asset Pricing Model (CAPM)1. In theory, since the MSCI

World Index approximates CAPM, the index is effi cient

and should theoretically offer the highest return for a

given level of risk. However, the actual returns investors

receive from portfolios that track the index will vary

depending on the base currency of the investor.

This note outlines the impact of currency fl uctuations

on the returns of the MSCI World Index and explains

how currency risk is limited in SSgA’s World Index

Equity Fund.

SSgA’s World Index Equity Fund

SSgA’s World Index Equity Fund seeks to track the

MSCI World Index. The recently created new share

class in the fund - euro hedged - enables European

investors to benefi t from tracking a globally diversifi ed

index while hedging their non-euro exposure to mitigate

the impact of currency risk.

Broad geographical diversifi cation

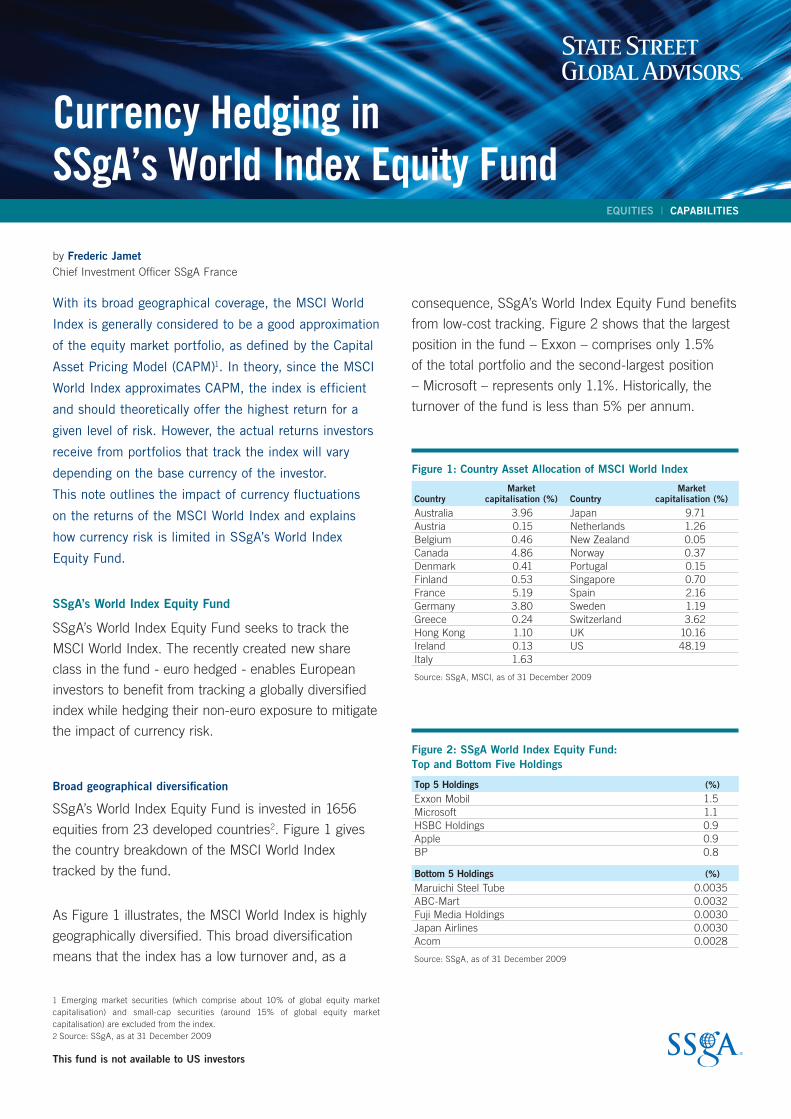

SSgA’s World Index Equity Fund is invested in 1656

equities from 23 developed countries2. Figure 1 gives

the country breakdown of the MSCI World Index

tracked by the fund.

As Figure 1 illustrates, the MSCI World Index is highly

geographically diversifi ed. This broad diversifi cation

means that the index has a low turnover and, as a

1 Emerging market securities (which comprise about 10% of global equity market

capitalisation) and small-cap securities (around 15% of global equity market

capitalisation) are excluded from the index.

2 Source: SSgA, as at 31 December 2009

consequence, SSgA’s World Index Equity Fund benefi ts

from low-cost tracking. Figure 2 shows that the largest

position in the fund – Exxon – comprises only 1.5%

of the total portfolio and the second-largest position

– Microsoft – represents only 1.1%. Historically, the

turnover of the fund is less than 5% per annum.

Figure 1: Country Asset Allocation of MSCI World Index

Market Market Country capitalisation (%) Country capitalisation (%)

Australia 3.96 Japan 9.71

Austria 0.15 Netherlands 1.26

Belgium 0.46 New Zealand 0.05

Canada 4.86 Norway 0.37

Denmark 0.41 Portugal 0.15

Finland 0.53 Singapore 0.70

France 5.19 Spain 2.16

Germany 3.80 Sweden 1.19

Greece 0.24 Switzerland 3.62

Hong Kong 1.10 UK 10.16

Ireland 0.13 US 48.19

Italy 1.63

Source: SSgA, MSCI, as of 31 December 2009

Figure 2: SSgA World Index Equity Fund: Top and Bottom Five Holdings

Top 5 Holdings (%)

Exxon Mobil 1.5

Microsoft 1.1

HSBC Holdings 0.9

Apple 0.9

BP 0.8

Bottom 5 Holdings (%)

Maruichi Steel Tube 0.0035

ABC-Mart 0.0032

Fuji Media Holdings 0.0030

Japan Airlines 0.0030

Acom 0.0028

Source: SSgA, as of 31 December 2009

by Frederic JametChief Investment Offi cer SSgA France

This fund is not available to US investors

2

CURRENCY HEDGING IN SSgA’S WORLD INDEX EQUITY FUND

Currency hedging to help mitigate currency risk

In contrast, the currency exposure of the fund is far

less diversifi ed than the equity allocation because of

the signifi cant exposure of the MSCI World Index to the

US dollar (48.19%), Japanese yen (9.71%) and British

pound (10.16%) as of 31 December 2009.

Given this concentrated currency exposure, the

performance of the fund is directly affected by

exchange rate movements and, for European investors,

by the euro / US dollar exchange rate in particular.

To reduce this currency risk, CAPM theory

recommends partial currency hedging against the

domestic currency of the investor. A non-hedged

MSCI World Index portfolio would be sub-optimal for

a non-US investor, for example, since as Figure 1

shows, a signifi cant part of the US dollar currency risk

(48.19%) would not be hedged.

In general, the volatility of returns from world equity

portfolios lies between 15-20%; at 24.56%3, Barra’s

measure of volatility for the MSCI World Index is

currently higher as a result of the spike in volatility

over the last two years. For a European investor,

approximately 30% of this volatility stems exclusively

from currency risk. Given its signifi cant contribution to

total risk, currency risk should clearly be managed.

The euro share class in SSgA’s World Index Equity

Fund implements systematic currency hedging

against every currency exposure except the euro.

Our hedging methodology replicates MSCI’s by

adjusting the currency hedging for every currency

on a monthly basis. For example, US dollar exposure

is sold at the end of every month against the euro

until the following month end. The profi t/loss is then

received/paid and the new US dollar exposure is

sold again. This process is undertaken for all currencies

to which the index is exposed, with the exception of

the euro.

3 Source: Barra, SSgA as at 31 December 2009

The hedging strategy we have developed is designed

to enable investors to receive pure “local” returns and

substantially reduces most of the currency risk linked to

exchange rate movements involving the euro.

What Is The Optimal Hedge Ratio?

Figure 3 shows the volatility of a range of different

combinations of hedged and unhedged MSCI World

Index portfolios. In this example, the fully hedged

portfolio actually has higher volatility than the fully

unhedged portfolio. The optimal hedge ratio in terms of

producing minimal volatility is achieved with a portfolio

comprising 40% MSCI World Hedged and 60% MSCI

World Unhedged, which has a currency-related volatility

of 4.74% and a total volatility of 24.35%. Although

leaving 60% of the portfolio unhedged results in

currency risk of 4.74%, some exposure to currency risk

is deemed advantageous for diversifi cation.

Conclusion

The euro hedged share class available in SSgA’s World

Index Equity Fund enables investors to mitigate the impact

of currency risk that derives from investing in a diversifi ed

portfolio of international investments. It also provides the

fl exibility to create portfolios with variable hedge ratios

through the combination of hedged and unhedged

portfolios to achieve a minimum volatility portfolio.

Figure 3: Volatility of the Hedged and Unhedged MSCI World Index

CountryFully

Unhedged30%

Hedge

Optimal (40%

Hedge)50%

Hedge60%

Hedge Fully

Hedged

% volatility

Risk Indices 0.87 0.87 0.87 0.87 0.87 0.87

Industry 1.07 1.07 1.07 1.07 1.07 1.07

Country 2.68 2.68 2.68 2.68 2.68 2.68

Currency 7.91 5.53 4.74 3.95 3.16 0

World Equity 24.89 24.89 24.89 24.89 24.89 24.89

Asset Selection 1.16 1.16 1.16 1.16 1.16 1.16

Total Volatility 24.56 24.36 24.35 24.36 24.39 24.79

Source: Barra, as at 31 December 2009

This fund is not available to US investors

www.ssga.com

State Street Global Advisors is the investment management business

of State Street Corporation (NYSE: STT), one of the world’s leading

providers of fi nancial services to institutional investors.

©2010 STATE STREET CORPORATION INTR-0105 3228-01.10

CURRENCY HEDGING IN SSgA’S WORLD INDEX EQUITY FUND

State Street Global Advisors Limited. Authorised and regulated by the Financial Services Authority. Registered in England. Registered No. 2509928. VAT No. 5776591 81. Registered offi ce: 20

Churchill Place, Canary Wharf, London E14 5HJ. Telephone: +44 (0)20 3395 6000. Facsimile: +44 (0)20 3395 6350. Web: www.ssga.com

This material is for your private information. The information we provide does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy

or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. We encourage you to consult your tax or fi nancial

advisor. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy of, nor liability for,

decisions based on such information. Past performance is no guarantee of future results.

This document should be read in conjunction with its prospectus. All transactions should be based on the latest available prospectus which contains more information regarding the charges, expenses

and risks involved in your investment.

This communication is directed at professional clients (this includes eligible counterparties as defi ned by the Financial Services Authority) who are deemed both knowledgeable and experienced

in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients)

should not rely on this communication.

SSgA may have or may seek investment management or other business relationships with companies discussed in this material or affi liates of those companies, such as their offi cers, directors and

pension plans.

THIS FINANCIAL PRODUCT IS NOT SPONSORED, ENDORSED, SOLD OR PROMOTED BY MSCI INC. (“MSCI”), ANY OF ITS AFFILIATES, ANY OF ITS INFORMATION PROVIDERS OR ANY OTHER THIRD PARTY

INVOLVED IN, OR RELATED TO, COMPILING, COMPUTING OR CREATING ANY MSCI INDEX (COLLECTIVELY, THE “MSCI PARTIES”). THE MSCI INDEXES ARE THE EXCLUSIVE PROPERTY OF MSCI. MSCI AND

THE MSCI INDEX NAMES ARE SERVICE MARK(S) OF MSCI OR ITS AFFILIATES AND HAVE BEEN LICENSED FOR USE FOR CERTAIN PURPOSES BY [LICENSEE]. NONE OF THE MSCI PARTIES MAKES ANY

REPRESENTATION OR WARRANTY, EXPRESS OR IMPLIED, TO THE ISSUER OR OWNERS OF THIS FINANCIAL PRODUCT OR ANY OTHER PERSON OR ENTITY REGARDING THE ADVISABILITY OF INVESTING

IN FINANCIAL PRODUCTS GENERALLY OR IN THIS FINANCIAL PRODUCT PARTICULARLY OR THE ABILITY OF ANY MSCI INDEX TO TRACK CORRESPONDING STOCK MARKET PERFORMANCE. MSCI OR ITS

AFFILIATES ARE THE LICENSORS OF CERTAIN TRADEMARKS, SERVICE MARKS AND TRADE NAMES AND OF THE MSCI INDEXES WHICH ARE DETERMINED, COMPOSED AND CALCULATED BY MSCI WITH-

OUT REGARD TO THIS FINANCIAL PRODUCT OR THE ISSUER OR OWNERS OF THIS FINANCIAL PRODUCT OR ANY OTHER PERSON OR ENTITY. NONE OF THE MSCI PARTIES HAS ANY OBLIGATION TO TAKE

THE NEEDS OF THE ISSUER OR OWNERS OF THIS FINANCIAL PRODUCT OR ANY OTHER PERSON OR ENTITY INTO CONSIDERATION IN DETERMINING, COMPOSING OR CALCULATING THE MSCI INDEXES.

NONE OF THE MSCI PARTIES IS RESPONSIBLE FOR OR HAS PARTICIPATED IN THE DETERMINATION OF THE TIMING OF, PRICES AT, OR QUANTITIES OF THIS FINANCIAL PRODUCT TO BE ISSUED OR

IN THE DETERMINATION OR CALCULATION OF THE EQUATION BY OR THE CONSIDERATION INTO WHICH THIS FINANCIAL PRODUCT IS REDEEMABLE. FURTHER, NONE OF THE MSCI PARTIES HAS ANY

OBLIGATION OR LIABILITY TO THE ISSUER OR OWNERS OF THIS FINANCIAL PRODUCT OR ANY OTHER PERSON OR ENTITY IN CONNECTION WITH THE ADMINISTRATION, MARKETING OR OFFERING OF

THIS FINANCIAL PRODUCT. ALTHOUGH MSCI SHALL OBTAIN INFORMATION FOR INCLUSION IN OR FOR USE IN THE CALCULATION OF THE MSCI INDEXES FROM SOURCES THAT MSCI CONSIDERS RELI-

ABLE, NONE OF THE MSCI PARTIES WARRANTS OR GUARANTEES THE ORIGINALITY, ACCURACY AND/OR THE COMPLETENESS OF ANY MSCI INDEX OR ANY DATA INCLUDED THEREIN. NONE OF THE MSCI

PARTIES MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO RESULTS TO BE OBTAINED BY THE ISSUER OF THE FINANCIAL PRODUCT, OWNERS OF THE FINANCIAL PRODUCT, OR ANY OTHER PERSON

OR ENTITY, FROM THE USE OF ANY MSCI INDEX OR ANY DATA INCLUDED THEREIN. NONE OF THE MSCI PARTIES SHALL HAVE ANY LIABILITY FOR ANY ERRORS, OMISSIONS OR INTERRUPTIONS OF

OR IN CONNECTION WITH ANY MSCI INDEX OR ANY DATA INCLUDED THEREIN. FURTHER, NONE OF THE MSCI PARTIES MAKES ANY EXPRESS OR IMPLIED WARRANTIES OF ANY KIND, AND THE MSCI

PARITES HEREBY EXPRESSLY DISCLAIM ALL WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE, WITH RESPECT TO EACH MSCI INDEX AND ANY DATA INCLUDED THEREIN.

WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL ANY OF THE MSCI PARTIES HAVE ANY LIABILITY FOR ANY DIRECT, INDIRECT, SPECIAL, PUNITIVE, CONSEQUENTIAL OR ANY OTHER

DAMAGES (INCLUDING LOST PROFITS) EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

This fund is not available to US investors.

ContactFor further information, please contact Frederic Jamet, Chief Investment

Officer, SSgA France. Telephone: +33(0) 1 44 45 40 85.

Email: [email protected].

Alternatively, please contact your local office. The national flags below

indicate the countries served by each office.

SSgA Belgium

+32 (0) 2 663 2036

SSgA France +33 (0) 1 44 45 40 00

SSgA Germany +49 (0) 89 558 78 422/+49 (0) 69 66 77 45 016

SSgA Italy +39 02 32066 100

SSgA Middle East & North Africa +971 (0) 4 437 2800

SSgA Switzerland +41 (0) 44 245 70 00

SSgA United Kingdom

+44 (0) 20 3395 6254