2009 sabor housing forecast

DESCRIPTION

2009 SABOR Housing Forecast. “The Recession is bad enough. A relentless new cycle is making it worse.”. -Washington Post December 28, 2008. If the FDA regulated the media, it would require all stories about the economy to carry this warning: - PowerPoint PPT PresentationTRANSCRIPT

2009 SABOR Housing Forecast

2009 SABOR Housing Forecast

-Washington PostDecember 28,

2008

“The Recession is bad enough. A relentless new cycle is making it worse.”

• If the FDA regulated the media, it would require all stories about the economy to carry this warning:

“Dizziness and pangs of existential angst may result. Do not read if you suffer from gloominess or are prone to bouts of anxiety. If you are near retirement age, consult with a physician before reading.”

CHANGING TRENDS

• 1947-1974: Era of the Broker– “Civic Generation of Giants”

• 1974 - 2001: Era of the Agent– “All Commissions and credit were the

results of the agents”

• 2001 - Present: Era of the Consumer

ECONOMIC OUTLOOK: TOP CONCERNS

1. Being able to afford the cost of living2. Having enough money to retire3. Uncertainty about things that could affect

the family budget4. Healthcare 5. Long-term care

Source: Harris Interactive

TEXAS HOME PRICES AT LEAST RISK

• According to PMI Group’s Winter 2009 Risk Index:

“Dallas, Houston and San Antonio – least likely large MSA’s in the country to experience lower home prices in the next two years.”- Austin ranked 12th

OTHER TOP RANKING TEXAS CITIES

• Sherman/Denison• Victoria• Odessa• Bryan/College Station

TEXAS IS TOP RELOCATION DESTINATION

• Texas Tops list – 4th year in a row– Number of inbound relocations in Texas exceeded– Number of outbound moves net of 1,903

Allied Van Lines annual survey of Top Relocation Destinations

• #2: North Carolina• #3: Virginia• Largest Net Losses:

• Michigan, Pennsylvania, New Jersey, Illinois

16,844

19,217

22,40524,562

22,824

18,661

0

5000

10000

15000

20000

25000

2003 2004 2005 2006 2007 2008

2003

2004

2005

2006

2007

2008

ANNUAL SALES TRENDS (JAN – DEC)

Number of Sales

Source: MLS

• Number of sales is down 18% year to date compared to 2007

• Down 23% from their peak in 2006

NUMBER OF SALES BY PRICE RANGE

(NOVEMBER)

0

200

400

600

800

1000

1200

1400

<$199,999 $200,000-$499,999

NOV. 05

NOV. 06

NOV. 07

NOV. 08

Price Range

# of Sales

11621210

1072

762

310 328362

231

Source: MLS

• Number of homes that sold at or below $199,999 has market share of 74%

• Number of houses that sold at or between $200,000 - $499,999 has market share of 22%

NUMBER OF SALES $500,000 AND ABOVE (NOVEMBER)

0

10

20

30

40

50

NOV. 05NOV. 06NOV. 07NOV. 08

# of Sales

27

46

4038

> $500,000 Price Range Source: MLS

Nov. ‘05

Nov. ‘06 Nov.

‘07 Nov. ‘08

• Number of houses that sold at or above $500,000 is down 5% from 2007

• Down 17% from November 2006

• Market share in November of 2008 – 4%

NUMBER OF MONTHLY ACTIVE LISTINGS BY YEAR

0

2000

4000

6000

8000

10000

12000

14000

16000

200620072008

Month

# of Active

Listings

Source: MLS

MONTHS OF INVENTORY BY YEAR

(Includes Single-Family & Condos/Townhomes)

0.01.02.03.04.05.06.07.08.09.0

200620072008

Month

Months of

Inventory

Source: Texas A&M Real Estate Research Center

MONTHS OF INVENTORY

• Months of supply are up because the number of sales is falling

• Months of supply will vary by price range– $1,000,000+ = 48 months of supply (Nov ‘08)– $500,000-$999,999 = 23 months of supply (Nov ‘08)– $250,000 - $499,999 = 14 months of supply (Nov ‘08)– $250,000 and below = 7 months of supply (Nov ‘08)

DAYS ON MARKET(November)

Source: MLS

0

10

20

30

40

50

60

70

80

90

Nov. 05 Nov. 06 Nov. 07 Nov. 08

Days onMarket

6861

78

87

DAYS ON MARKET ANALYSIS

• Days on market are up 12% from 2007

• Days on market increase as you move north of Loop-1604

FORECLOSURE INFORMATION

UP23%

2008 COMPARED

TO 2007

www.FLSonline.com

Foreclosure postings have climbed 41% over the past 5 years, since 2003.

Foreclosure Listing Service, Inc.

$132,900

$142,600

$149,800 $149,900

$120,000

$125,000

$130,000

$135,000

$140,000

$145,000

$150,000

2005 2006 2007 2008

MedianSalesPrice

YTD MEDIAN SALES PRICE PER YEAR

(JAN - DEC)

Source: MLS

• Prices are stable and are expected to continue this trend in 2009

• Price stability will vary by price range and location

Subdivision $/Sq.Ft.20

06

$/Sq.Ft. 2007

Percentage Change ’06 to ‘07

$/Sq.Ft. Jan-Nov

2008

Percentage Change ’07 to ‘08

The Dominion $157 $181 15% $188 4%Alamo Heights

$181 $195 8% $199 2%

Terrell Hills $149 $172 15% $182 6%Olmos Park $170 $185 9% $180 -3%Monte Vista $149 $156 5% $159 2%Cordillera Ranch

$190 $185 -3% $195 5%

Elm Creek $131 $133 1% $130 -2%

PRICE/SQ. FT. PER SUBDIVISION

Subdivision $/Sq.Ft. 2006

$/Sq.Ft. 2007

Percentage Change ’06 to ‘07

$/Sq.Ft. Jan-Nov

2008

Percentage Change ’07 to ‘08

Bluffview $116 $133 15% $131 -1%

Deerfield $101 $104 3% $105 1%Hunters Creek

$101 $102 1% $99 -3%

Castle Hills $94 $105 12% $98 -7%Inwood $116 $133 15% $124 -7%Rogers Ranch

$108 $107 -1% $112 13%

Shavano Park

$129 $137 6% $140 2%

Fair Oaks $132 $131 -1% $133 2%

PRICE/SQ. FT. PER SUBDIVISION

Subdivision $/Sq.Ft. 2006

$/Sq.Ft. 2007

Percentage Change ’06 to ‘07

$/Sq.Ft. Jan-Nov

2008

Percentage Change ’07 to ‘08

Churchill Estates

$91 $87 -4% $87 0%

San Pedro Hills

$79 $85 3% $84 -1%

Braun Station

$80 $77 -4% $64 -17%

Colonies North

$79 $85 7% $89 5%

PRICE/SQ. FT. PER SUBDIVISION

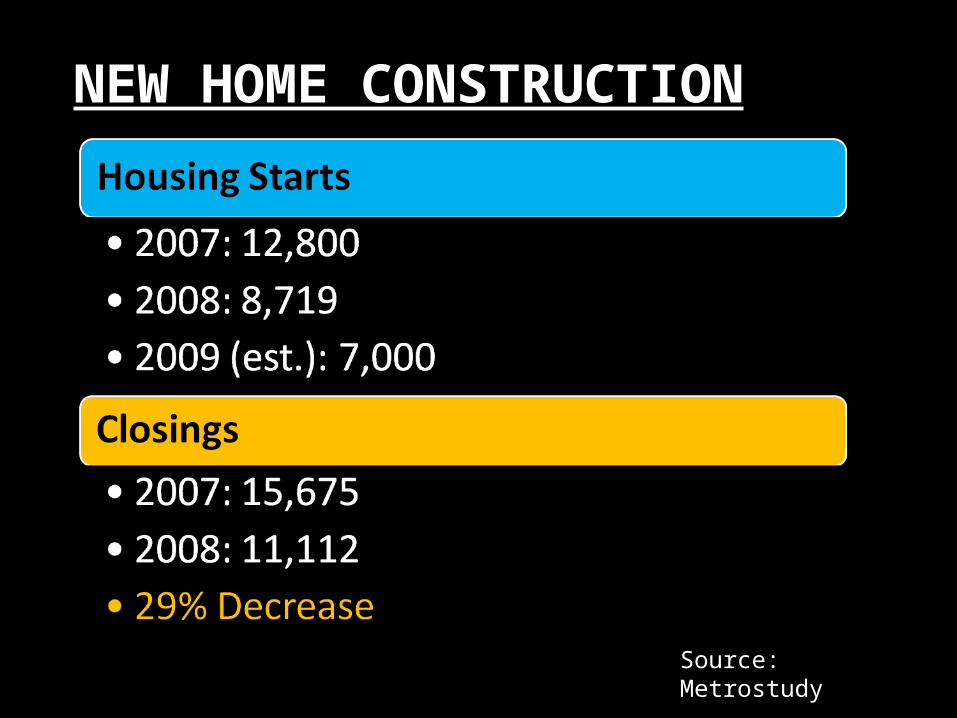

NEW HOME CONSTRUCTION

Source: Metrostudy

NEW HOME CONSTRUCTION (CONT.)

Source: Metrostudy

TEXAS JOB GROWTH IN 2008Leads the Nation from Oct07 to

Oct08

MAJOR METROS JOB GROWTH( Oct07 to Oct08 )

JOB GROWTH PAST 12 MONTHS

Ending October, 2008

Source: Texas Workforce Commission

JOB GROWTH PAST 12 MONTHS

Ending October, 2008

Source: Texas Workforce Commission

JOB GROWTH PAST 12 MONTHS

Ending October, 2008

Source: Texas Workforce Commission

SINGLE-FAMILY BUILDING PERMITS

Nov07 to Nov08

5,856 Permits issued in San Antoniofrom Nov07 to Nov08

HOME PRICE APPRECIATION

Best States Worst StatesN. Dakota 4.0% Nevada -20.9%S. Dakota 3.9% California -20.8%Texas 3.2% Florida -16.0%Alabama 2.8% Arizona -13.5%Oklahoma 2.8% Rhode Island - 8.0%

Source: OFHEO

3Q07 to 3Q08

BUYING A HOUSE FOR THE LONG TERM(Even in the roughest markets)

Source: OFHEO

City Price Change (Last 12 Months)

Price Change (Last 5 Years)

Orlando, FL -15.40% + 48.66%

Naples, FL -25.25% + 29.78%

Las Vegas, NV -26.78% + 25.82%

Fresno, CA -23.52% + 26.08%

Los Angeles, CA -26.78% + 45.55%

ISSUES TO WATCH: 2009

• May be the lowest mortgage rates in our lifetime

• Can the government get Fannie Mae & Freddie Mac working again?

• Housing starts bottom at lowest level since WWII• Home sales volume could decline 5-10% again in

2009 due to high level of uncertainty

• Oil and Gas prices • The economy is likely to hit bottom before the

end of the year; a rising stock market will be the signal

• Thousands of families will buy homes in 2009• Government intervention is quickly becoming

a problem and not a solution

ISSUES TO WATCH: 2009 (CONT.)

81ST TEXAS LEGISLATURE

• Appraisal Reform– Mandatory Sales Price Disclosure vs. Appraisal

Reform– Reliance on Property taxes to fund public

schools

• REALTOR Position: • Support a Constitutional amendment to give state

entity authority to enforce uniform standards among ALL appraisal districts in Texas

• Support legislation that changes how an effective tax rate is calculated to ensure no new revenue is realized by local taxing jurisdictions when local property values increase

• ABR hearings: uniformity, consistency, and transparency

• Bexar County: Consumer report and media campaign

81ST TEXAS LEGISLATURE

Source: Mark Nash, Chicago-based residential real estate author, broker and columnist

SIDELINED HOMEBUYERSSIDELINED HOMEBUYERS

• Fence-sitters• “It’s time for our family to

buy the new home that suits our needs.”

COLLABORATIVE HOME PRICING

• Seller with agent look at closed comparables, set a price, and the buyer and his agent agree/disagree

• In the end, a mortgage lender and their appraiser will set the price

HOUSE THERAPISTS

• Independent third-party (house therapist or coach)– Brings household relationships to common ground

on prickly issues such as to stay or move, how much to spend on remodeling or decorating, etc.

– Outline benefits and pitfalls of overspending

LOVESEATS

• Consumers appreciate ease at which they can be arranged

DINING CHAIRS THAT DON’T MATCH

OLDER WAR-HORSE APPLIANCES

• 1940’s – 1980’s – Harvest gold double ovens (1970’s)– Cold spot refrigerators (1950’s)– Dryers (1960’s)

MASTER BED AS THRONE

• At-home luxury hotel experience• Posh linens, pillows and mattresses• Dual master suites

• Parchment Whites• Cashmere Yellows• Bright Optimistic Blues• Radiant Golds• Grassy Greens

OBAMA ERA PAINT COLORS

SPECIAL HOME COMPONENTS

• Open Floor Plans (minimizing walls in common areas)

• Eco-friendly/green building components• Larger garages

– Garage floors & doors

FIXER-UPPER HOMES

• Buyers want to inherit new kitchens & bathrooms

INDOOR-OUTDOOR CARPET

• Often masks flaws in homes

TRACK LIGHTING

• “Don’t really have any interesting artwork or architectural features to spotlight”

• “Bring undue attention to nothing.”

FORECLOSURE “FLUFF”

• National Foreclosure rate in 2008 was just under 3%

• In the Great Depression, it was just over 40%

HOME STAGING

• 4 Groups:– Civics: 62 years and older– Baby Boomers: 43 years to 61 years– Gen X’ers: 31 years to 42 years– Millennials: 13 years to 30 years

Source: John Ansbach with Generational Consulting Group

GENERATIONAL DIVERSITY

CIVICS; MATURES, GI’S, GREATEST GENERATION

Values & Preferences:

58 million people

Source: John Ansbach with Generational Consulting Group

BABY BOOMERS – “ME” GENERATION78 million people

Values & Preferences:

Source: John Ansbach with Generational Consulting Group

GENERATION X: X’ERS, BABY BUSTERS

48 million; the original “latchkey” kids

Values & Preferences:

Source: John Ansbach with Generational Consulting Group

MILLENNIALS: GEN Y, ECHO BOOMERS

73 million people

Values & Preferences:

Source: John Ansbach with Generational Consulting Group

SUGGESTED READING