2009 pension decisions – navigating the storm€¦ · january 2009 corporate update 2009 pension...

TRANSCRIPT

January 2009

Corporate Update

www.lcp.uk.com

2009 Pension decisions – navigating the storm All indications are that we are entering another challenging year. Whilst we hope that 2009 will not see anything like the financial convulsions of 2008, clear decision making will be critical for companies in the months ahead. Pension liabilities will be a key area in which tough decisions will need to be taken to protect company balance sheets, P&L account and to control cash contributions.

In this corporate update we highlight the key issues and assumptions for year end accounting for companies with Defined Benefit (or Final Salary) pension plans, and identify a number of areas in which decisions made in 2009 will help a company to control costs and manage cash outlay. Understandably the new economic environment will compel many companies to review their pension strategy, with implications that will define the situation for many years to come. The long-term nature of pensions decisions make it essential that appropriate consideration is given to align pension policy with long-term corporate strategy, in addition to helping stakeholders to get through the remainder of the current financial crisis.

Accounting for pensions – too much choice?

Companies that sponsor Defined Benefit pension plans with a significant allocation to equity investments know that their pension assets have taken a hit, and so it has been somewhat surprising that for much of 2008 there has not been a significant increase in the pension deficit for accounting purposes. The reason for this is that pension liabilities (for accounting purposes) are measured using bond yields on AA-rated bonds. This has pushed down the value placed on liabilities as corporate bond yields rose on the back of historically high spreads between AA-rated corporate bonds and government bonds. In effect, the credit crunch has “cushioned” the impact on the deficit of falling asset values.

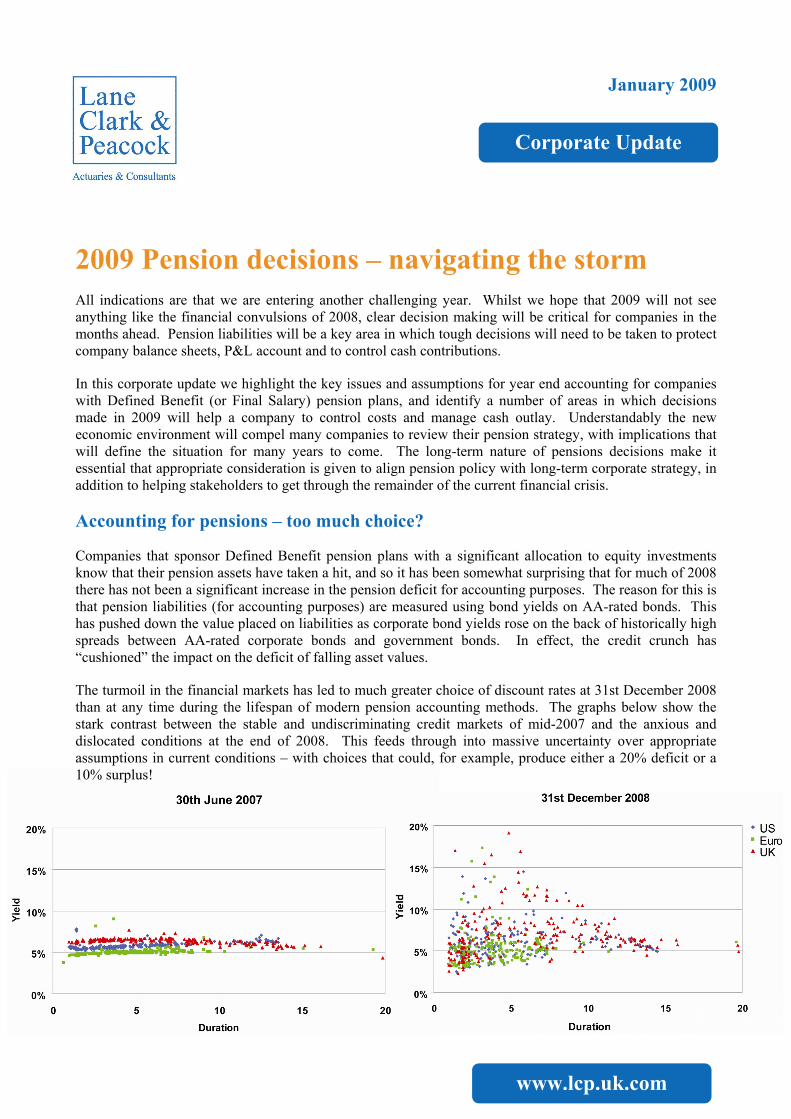

The turmoil in the financial markets has led to much greater choice of discount rates at 31st December 2008 than at any time during the lifespan of modern pension accounting methods. The graphs below show the stark contrast between the stable and undiscriminating credit markets of mid-2007 and the anxious and dislocated conditions at the end of 2008. This feeds through into massive uncertainty over appropriate assumptions in current conditions – with choices that could, for example, produce either a 20% deficit or a 10% surplus!

Page 2

Unfortunately, the “cushion” has eased, with a crash in bond yields over December 2008. Yields on UK government bonds fell by around 0.5% pa over the month and this was further exacerbated by a number of high-yielding bonds leaving the main AA-rated corporate indices at the end of December after having been downgraded from AA status. The impact of this rebalancing was to reduce the spread on AA-rated corporate bond yields over government bond yields by around 0.2% pa on the main UK indices and around 0.7% pa on Eurozone indices.

So what is the impact of the recent fall in AA-rated bond yields? Whilst partly offset by a slight reduction in long-term inflation expectations, this fall will typically increase the value placed on pension liabilities by around 10% and will substantially increase deficits, or push companies that had a pension surplus into deficit at the year end.

With most UK pension liabilities being linked to inflation in some way, another issue for companies to grapple with is the way to calculate long-term inflation projections, and how to allow for the short-term negative inflation anticipated by the market for the next couple of years – the market is predicting a period of deflation. The sting here is that pensions do not generally decrease when inflation is negative, so pensioners effectively receive increases ahead of inflation during a deflationary period.

If reporting under International GAAP, there is the additional question of whether (or perhaps at what level) a new accounting rule called IFRIC14 causes measures based on cash funding requirements to “trump” the normal calculation of the liability values under accounting standards. This is also an important consideration for companies who currently report under US GAAP but are moving towards International GAAP.

More detailed consideration of the important accounting issues for year end discussion are covered in greater depth in our recently published “European Pensions Briefing” report, which is available as a download from the LCP website or from your normal contact at LCP.

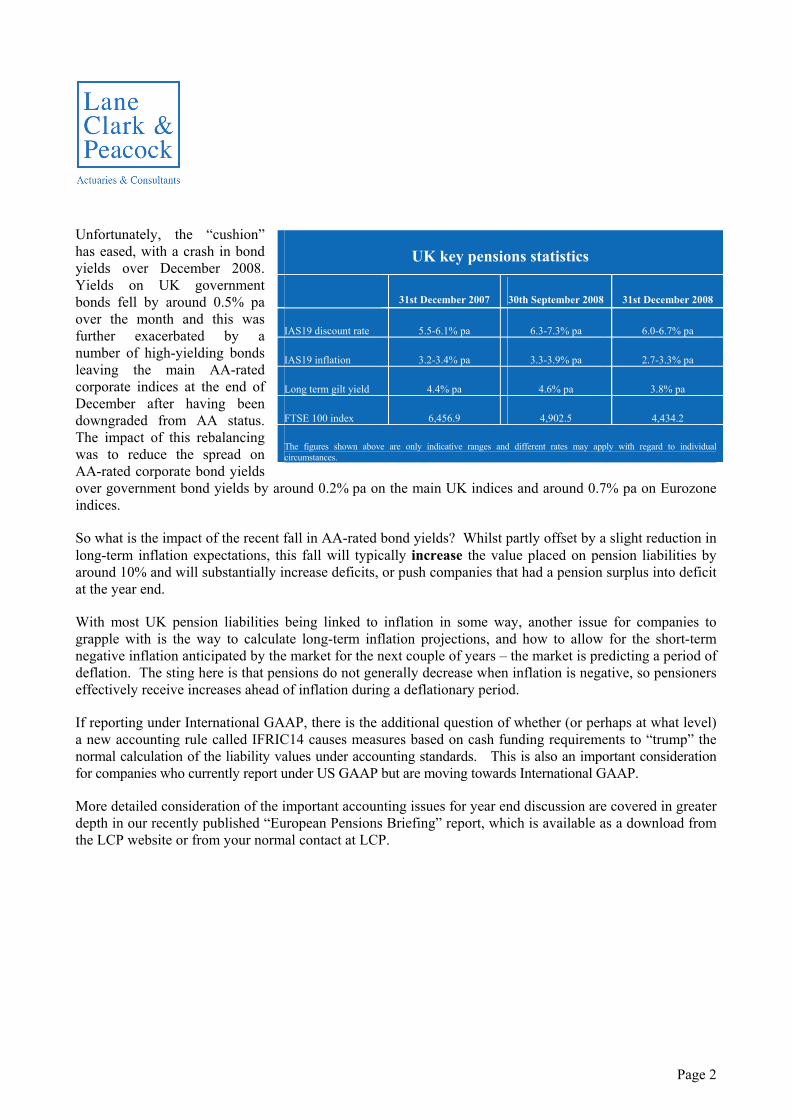

UK key pensions statistics

31st December 2007 30th September 2008 31st December 2008

IAS19 discount rate 5.5-6.1% pa 6.3-7.3% pa 6.0-6.7% pa

IAS19 inflation 3.2-3.4% pa 3.3-3.9% pa 2.7-3.3% pa

Long term gilt yield 4.4% pa 4.6% pa 3.8% pa

FTSE 100 index 6,456.9 4,902.5 4,434.2

The figures shown above are only indicative ranges and different rates may apply with regard to individual circumstances.

Page 3

Defined Benefit accrual – time to call it a day?

Given the economic slowdown, many companies sponsoring a defined benefit pension plan, in which benefit accrual is still continuing, will be asking themselves whether this can still continue beyond 2009? A growing number of companies have taken the step to freeze their plan and many other companies are looking at their options. Although the question may have been asked before, the answer under current circumstances may have changed.

Our experience suggests that initially companies enter into the question of ceasing accrual by weighing up the potentially positive financial implications against the perceived adverse HR implications. However, the true picture typically has more subtle elements, some of which can be counterintuitive, for example:

• We expect to see more cases where closure to future accrual is positive from an HR point of view because of the harmonisation benefits. This can happen, for example, where a pension plan has been closed to new members for some years, and there are growing difficulties with a “two tier workforce”. Freezing the plan removes the continuing distinction between defined benefit “haves”, and the defined contribution “have-nots”.

• Financial implications can also be misunderstood. If active members accruing benefits are only a small proportion of the plan membership, then closure to future accrual is likely to deliver limited cost savings. The more noticeable impact may be to bring employer commitment to the pension plan into question in the eyes of members and trustees. In these situations, financial considerations may be better addressed by focusing on areas such as investment strategy, a pensioner “buy-in” and other ways of managing the accrued liabilities.

• We expect the government’s planned introduction of Defined Contribution Personal Accounts from 2012 to act as a further catalyst to close Defined Benefit plans to future accrual from the point they are implemented, if not before.

Deciding whether to freeze the plan and close to future accrual requires careful consideration. Ensuring that any such exercise yields the desired results requires precise planning, given the many potential pitfalls. This process should include:

• making a balanced assessment of the costs and benefits of closing to accrual, in comparison with other cost-reduction options, and alternative de-risking strategies such as securing liabilities for current pensioners with an insurer to eliminate longevity risk;

• asking your lawyers the right questions, focusing on areas such as trustee powers, employment terms and consultation requirements;

• appropriate design of replacement defined contribution arrangements, and any associated life insurance and disability benefits, together with consideration of financially material “non-headline” areas such as contracting out; and

• communication – in our experience an honest, open and courteous message on why a plan is being closed has yielded much greater acceptance among employees than could ever be achieved by a slick but disingenuous exercise in “spin”.

Page 4

Valuations in 2009 - negotiating with Trustees

Many pension plans will have funding valuations due in 2009 – which is the key point at which the financial health of the plan is reassessed and the employer’s contributions to the plan are fixed for the next three years. The current extreme economic conditions will mean that negotiations with the trustees have never been so important, and early warning and planning will greatly assist the company in managing these negotiations.

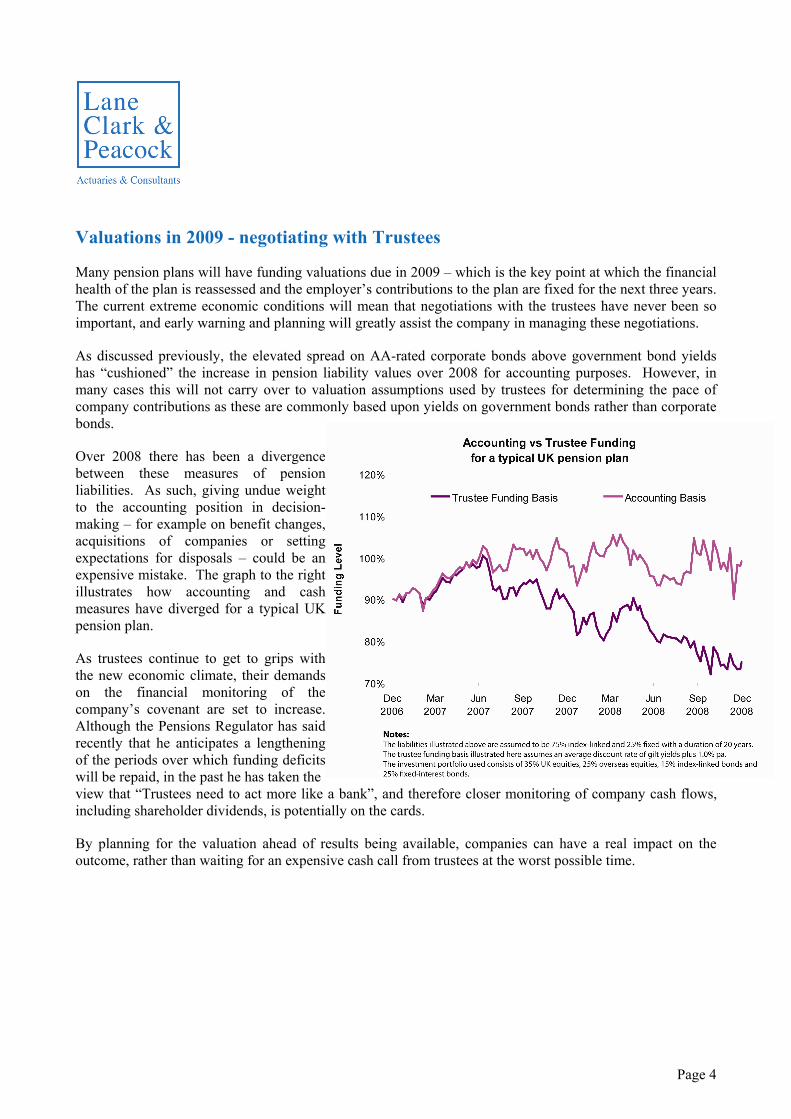

As discussed previously, the elevated spread on AA-rated corporate bonds above government bond yields has “cushioned” the increase in pension liability values over 2008 for accounting purposes. However, in many cases this will not carry over to valuation assumptions used by trustees for determining the pace of company contributions as these are commonly based upon yields on government bonds rather than corporate bonds.

Over 2008 there has been a divergence between these measures of pension liabilities. As such, giving undue weight to the accounting position in decision-making – for example on benefit changes, acquisitions of companies or setting expectations for disposals – could be an expensive mistake. The graph to the right illustrates how accounting and cash measures have diverged for a typical UK pension plan.

As trustees continue to get to grips with the new economic climate, their demands on the financial monitoring of the company’s covenant are set to increase. Although the Pensions Regulator has said recently that he anticipates a lengthening of the periods over which funding deficits will be repaid, in the past he has taken the view that “Trustees need to act more like a bank”, and therefore closer monitoring of company cash flows, including shareholder dividends, is potentially on the cards.

By planning for the valuation ahead of results being available, companies can have a real impact on the outcome, rather than waiting for an expensive cash call from trustees at the worst possible time.

Page 5

Pension Protection Fund levies are set to rise – act now

With rising corporate insolvency rates, the number of claims on the PPF is likely to increase dramatically, and the levies required to fund it are inevitably going to increase. Companies, and trustees, have an opportunity in the first quarter of 2009 to act to minimise their levy for 2009/10, and prepare for the 2010/11 levy year.

Key actions with a deadline at the end of quarter one 2009 are as follows:

The PPF have proposed significant changes for future levy years, and so these last two years under the current rules might offer one of the last opportunities for a substantial “easy win”.

Impacting the 2009/10 levy

Certify deficit contributions

If deficit contributions have been paid since the last PPF “section 179” valuation, certifying these to the PPF can reduce your levy

Contingent asset certificates

Consider putting a “type A” intra-group guarantee in place, which can result in a lower insolvency probability for the purposes of setting the PPF levy

Impacting the 2010/11 levy

PPF funding level Consider whether to submit a new PPF “section 179” valuation to the Pensions Regulator in order for the PPF to reflect the updated position when calculating your levy

Insolvency probabilities

Review the Dun and Bradstreet failure scores for your sponsoring employers or guarantors, and take action to improve their standing

Scheme return information

Review the information held on “Exchange” (the Pension Regulator’s online scheme return system), as this will be used to calculate the levy

Page 6

This Corporate Update is based on our current understanding of the subject matter and relevant legislation which may change in the future. Such changes cannot be foreseen. This document is prepared as a general guide only and should not be taken as an authoritative statement of the subject matter. No responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this Corporate Update can be accepted by LCP.

If you would like any assistance or further information on the contents of this Corporate Update, please contact Alex Waite or Michael Berg or the partner who normally advises you at LCP. You can contact us by telephone on +44 (0)20 7439 2266, by email to [email protected], or through LCP’s website at www.lcp.uk.com.

Specific contacts: Accounting issues: Alex Waite or Shaun Southern European Pensions Briefing: Phil Cuddeford or Colin Haines Benefit reviews: Michael Berg or Richard Murphy Pension buyouts: Charlie Finch or Clive Wellsteed PPF levy: Mark Alexander