· auditor-general’s report on the public accounts of ghana, mdas – 31 december 2006 1 part i...

TRANSCRIPT

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 1

PART I

REPORT OF THE AUDITOR-GENERAL ON THE PUBLIC ACCOUNTS OF GHANA-MINISTRIES, DEPARTMENTS AND

OTHER AGENCIES (MDAs) FOR THE FINANCIAL YEARENDED 31 DECEMBER 2006

Introduction

I have audited the accounts of MDAs for the financial year ended 31 December 2006 in accordance with Article 187 (2) of the 1992 Constitution of the Republic of Ghana. This report presents the results of financial and compliance audit of MDAs and special audits and contains matters of significance that I believe should be brought to the attention of the House.

Audit objectives

2. Section 13 of the Audit Service Act, 2000 (Act 584) enjoins the Auditor-General to examine in such manner as he thinks necessary, the financial operations of MDAs and ascertain, among other things, whether in his opinion:

monies have been expended for the purposes for which they were appropriated and the expenditures have been made as authorised; and

essential records have been maintained and the rules and procedures applied were sufficient to safeguard and control public property; and

all public monies have been fully accounted for and rules and procedures applicable are sufficient to secure an effective check on the assessment, collection and proper allocation of the revenue.

3. My Officers were guided by the above objectives to ensure andencourage proper and prudent management of public funds. They also reviewed the continuing adequacy of key areas of MDAs internal control systems and risk management. Matters raised in this report including recommendations intended to further deepen financial

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 2

management and controls as detailed in the succeeding paragraphs were discussed with MDAs.

Summary of findings and recommendations

4. We again found major breakdown of controls over tax administration, cash management, procurement and payroll. These common and recurring problems which run in my report from year to year are disturbing. Table I, as usual, depicts the global financial impact of the lapses while Table 2 is an illustration of the impact on each MDA.

5. Table 2 also presents the status of high-risk areas facing MDAs identified in 2006 warranting attention. Lasting solutions to high-risk problems offer the potential to save billions of cedis, dramatically improve service to taxpayers, strengthen public confidence and trust in the performance and accountability of our public sector and impacts positively on Government’s developmental agenda.

6. Accordingly, this report contains my views on what remains to be done for each high-risk area to address the problem. Perseverance by MDAs in implementing recommended panacea and continued parliamentary oversight and action are both essential.

7. Table 1 shows that the financial impact of these irregularities was ¢279.77 billion (including US$2,020,026 converted at the prevailing rate of ¢9,211.45 to the United States dollar as at 31 December 2006) compared with 2005 figure of ¢257.40 billion (including US$217,414 converted at the prevailing rate of ¢9,076.20 as at 31 December 2005), an increase of ¢22.37 billion or 8.7%.

Trend of financial irregularities

8. We again evaluated the above trend against the Gross Domestic Product (GDP), actual revenue and expenditure. Matching financial irregularities against these criteria is generally accepted as appropriate indicators of trends in financial performance.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 3

9. The financial impact of ¢257.40 billion for 2005 and ¢279.77 billion for 2006 as a percentage of GDP, actual revenue and expenditure is shown in the table below:

Item 2005(¢Billion)

% 2006(¢Billion)

%

GDP 97,018.00 0.3 112,320.30 0.3Actual revenue 30,325.70 0.8 30,841.90 0.9Actual expenditure 25,158.70 1.0 34,908.41 0.8

10. As can be seen from the above table, the irregularities compared with the above criteria showed no real improvement. There is still room for improvement and I urge MDAs to continue to review their financial internal control systems and also enforce rigidly applicable financial rules and regulations to ensure sound financial management of their entities.

11. My comments on the financial shortcomings and recommendations to address them are provided in the succeeding paragraphs.

Table1: Summary of financial irregularities for 2006 and 2005 financial years

Irregularities %2005

%2006

¢Million2005

¢Million2006

US$2005

US$2006

Total (¢M)2005

Total (¢M)2006

1VAT/IRS/CEPS uncollected taxes, others 71.4 61.5 183,428.0 171,748.4 42,366 29,475 183,812.9 172,019.9

2 Cash irregularities 10.4 14.8 25,824.3 34,057.1 114,848 799,486 26,866.7 41,421.5

3Outstanding loans/debts 9.4 12.9 23,731.8 35,450.1 47,100 62,556 24,159.3 36,026.3

4 Stores/ procurement irregularities

3.4 4.4 8,918.5 12,298.1 12,601 8,918.5 12,414.2

5 Payroll overpayments

1.3 4.2 3,336.8 1,480.3 13,100 1,115,948 3,455.7 11,759.8

Contract irregularities 4.0 2.0 10,126.0 5,539.7 10,126.0 5,539.7

7Staff rent arrears 0.1 0.2 45.8 590.4 45.8 590.4Total 100 100 255,426.4 261,164.1 217,414 2,020,066 257,400.1 279,771.8

VAT/IRS/CEPS, uncollected taxes, others-¢172.02 billion

12. Tax irregularities consist of:

misappropriation of tax revenue;

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 4

outstanding rent tax;

non-payment of corporate tax;

non-payment of National Reconstruction Levy;

issuance of dishonoured cheques in settlement of taxes;

failure to levy penalties on late fillers of returns;

outstanding debts from traders; and

petroleum tax arrears.

13. The 2006 irregularities aggregate of ¢172.02 billion compared with ¢183.81 billion for 2005 reveals a decrease of ¢ 11.79 billion or 6.4% and a marginal improvement on the performance of the revenue agencies. The lapses arose from ineffective supervision over schedule officers, lack of effective monitoring and recovery of outstanding taxes and weak internal control over tax collection. Since revenue collection plays a pivotal role in Government’s development agenda, I call on the Revenue Agencies Governing Board to review the tax collection machinery and strategies and initiate measures to aggressively recover all overdue taxes. I also renew the following recommendations to further boost tax collection and Government cashflow:

delinquent debts should be subjected to regular review ;

revenue collecting agencies should identify potential sources of revenue by widening the tax net to include small and medium scale self-employed;

tough sanctions should be invoked against tax defaulters;

internal control systems and risk management in IRS,VAT and CEPS, strengthened, including better supervision to ensure that staff perform their duties efficiently and in accordance with the tax laws;

IRS should launch effective public education campaign to create adequate public awareness of the withholding tax regime. All providers of goods and services must be sensitised to demand their tax credit certificates from

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 5

withholding agencies even if they do not intend to use them to claim their tax credits; and

the Minister for Finance and Economic Planning should ensure that government stores are procured from only Value-Added Tax-registered persons in line with section 30 (2) of the FAA,2003.

Cash irregularities - ¢41.42 billion

14. Cash irregularities include:

unacquitted payments;

unpresented payment vouchers;

misappropriation of revenue and other receipts;

misapplication of funds;

bank balances not promptly transferred into the Consolidated Fund; and

payment vouchers not returned to Treasuries.

15. Cash irregularities increased from ¢26.87 billion in 2005 to ¢41.42 billion in 2006, a rise of ¢14.55 billion or 54.2%, indicating very weak control exercised by MDAs over cash resources. The escalation was due to the intransigence of imprest holders to promptly account for imprests, lack of effective supervisory control over revenue collection and blatant failure on the part officers entrusted with the disbursement of funds to obtain supporting document forfunds disbursed. I therefore urge MDAs to continue to review and strengthen their internal control systems. They should also rigidly enforce the provisions of the FAA, 2003 and FAR, 2004 and apply the necessary sanctions against compliance violators to ensure sound financial management of their entities.

Outstanding loans/debts - ¢36.03 billion

16. The above figure of ¢36.03 billion for 2006 represents an upsurge of ¢11.87 billion or 49.1% over last year’s figure of ¢24.16 billion. The rise was due mainly to amounts owed to the Ministry of

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 6

Energy (¢26.20 billion) by Oil Marketing Companies in respect of petroleum taxes. While urging the Ministry to put in place proper monitoring and prompt collection procedures over petroleum taxes, I call on all other MDAs to regularly monitor their accounts receibables to ensure their prompt collection to prevent them from metamorphosing into bad debts.

Payroll irregularities - ¢11.76 billion

17. Due to overpayment of salaries at Foreign Missions (¢10.32 billion) and locally (¢1.44 billion), payroll irregularities escalated from ¢3.46 billion in 2005 to ¢11.76 billion in 2006, an increase of ¢8.30 billion or 239.9%. The Foreign Missions’ overpayment was the result of the use of incorrect exchange rates in the conversion of home-based staff salaries into local currencies while the overpayments locally was due, to ineffective co-ordination between MDAs, CAGD and the Banks. I recommend that MOFEP, MFA and CAGD should effectively control exchange rate usage at Foreign Missions. I also recommend improved co-ordination among MDAs, CAGD and the Banks to ensure prompt deletion of ghost names from the payroll and the return of unearned salaries to chest.

Stores/procurement irregularities - ¢12.41 billion

18. The above irregularities comprise items paid for but not supplied, fuel not taken on ledger charge and overstocking of store items. The irregularities totalled ¢12.41 billion and compared to the previous year’s figure of ¢8.92 billion, showed an increase of ¢3.49 billion or 39.1%. In this connection, I wish to advise MDAs to put in place proper stores accounting procedures which will ensure proper accountability for all store purchases, particularly, proper maintenance of vehicle log books

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 7

Table 2: Summary of cash irregularities, payroll overpayments, stores/procurement and other irregularities classified according to MDAs

No.

Ministry TaxIrregularities

CashIrregularities

Outstanding loans/debts

Payroll overpmts

Stores/procurement irregularities

ContractIrregulari.

Staff rentarrears Total

(¢M) (¢M) (¢M) (¢M) (¢M) (¢M) (¢M) (¢M)1 Finance & Economic Planning 169,525.1 7,598.4 22.0 109.4 177,254.92 Energy 104.8 3,780.0 26,200.0 460.4 30,545.23 Foreign Affairs, Reg.Co-opera. & NEPAD 2,554.1 400.6 10,317.7 116.1 13,388.54 Health 577.7 5,167.9 1,920.9 353.0 2,796.4 352.7 11,168.65 Education, Sports and Science 229.0 5,798.6 2,078.1 371.0 516.5 37.5 18.9 9,049.66 Lands, Forestry and Mines 4,164.2 2,660.2 17.2 6,841.67 The Interior 357.6 4,640.7 93.2 168.4 1,185.5 166.4 6,611.88 Water Resources, Wks & Hous. 9.2 173.1 54.1 63.4 83.1 4,544.1 14.6 4.941/69 Office of Government Machinery 102.5 2,036.4 175.6 105.7 1,159.1 36.5 3.615/8

10 Food and Agriculture 3.0 51.1 2,815.8 201.7 289.0 24.0 4.4 3,389.011 Defence 3,110.0 3,110.012 Transportation 80.1 1,287.5 1,347.7 33.5 307.3 50.3 3,106.413 Tourism & Diasporan Relations 937.5 1,831.1 2,768.614 Trade, Ind. PSD and PSI 86.7 1,286.3 367.8 107.9 95.8 1,944.515 Other Agencies 774.2 40.6 40.2 855.016 Information and Natational Orientation 6.7 572.5 222.2 801.417 Justice & Attorney-General 272.8 272.818 Manpower, Youth and Employment 50.8 18.6 69.419 Local Govt Rural Dev. & Environment 5.1 32.0 37.1

TOTAL 172,019.9 41,421.5 36,026.3 12,414.2 11,759.8 5,539.7 590.4 279,771.8

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 8

Contract irregularities - ¢5.54 billion

19. Contract lapses include outstanding refund of mobilisation amounts, non-tendering of contracts, items paid for but not supplied and unexecuted projects. This figure decreased from ¢10.13 billion in 2005 to ¢5.54 billion in 2006. Failure on the part of MDAs to award contracts to competent contractors and to comply strictly with the Public Procurement Act, 2003 (Act 663) caused the anomaly. I therefore recommend strict adherence to the provisions of the Public Procurement Act, 2003 (Act 663) to ensure value for money in contract management.

Staff rent arrears - ¢590.4 million

20. Due to managements’ failure to deduct rent at source, non-deduction/arrears of rent escalated from ¢45.8 million in 2005 to ¢590.4 million, an increase of ¢544.6 million or 1,189%. I call on MDAs and the CAGD to intensify efforts at deducting rent at source in a timely manner and improving verification of rent payments to eliminate the incidence of rent arrears completely.

Conclusion

21. I am not satisfied with improvement in efforts to address shortcomings in internal controls and governance frameworks against the backdrop of fresh financial rules and regulations and the litany of financial irregularities exhibited by MDAs.

22. While a strong expenditure management is essential to good financial management, good systems in themselves are not enough. They must be applied correctly and ethically. I therefore strongly recommend that MOFEP develops Values and Ethics Code for the Public Service to ensure proper, effective and efficient use of public funds.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 9

PART II

SUMMARY OF FINDINGS AND RECOMMENDATIONS BY MDAS

MINISTRY OF FINANCE AND ECONOMIC PLANNING

23. Internal control weaknesses including weak supervision over Accounting officers and Cashiers as well as non-adherence to rules and regulations governing cash management resulted in the misappropriation of revenue totalling ¢2.01 billion by some officials of the VAT Service and the Controller and Accountant-General’s Department. We recommended recovery of the misappropriated revenue and strengthening of supervisory controls over accounting staff and other internal controls to minimise the incidence of misappropriations.

24. The Headquarters of MOFEP and two other departments under the Ministry failed to obtain expenditure supporting documents to substantiate purchases and other expenditures totalling ¢5.09 billion due to ineffective supervision over the operations of Procurement officers and other operatives as well as laxity on the part of management. To ensure transparency and full accountability, we recommended that the respective managements should provide the relevant expenditure documents to substantiate the expenditures and justify the payments.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 10

25. The operations of some VAT offices within the Greater Accra Region were characterised by cash irregularities such as loss of revenue through the receipt of dud cheques by traders, lodgement of revenue into unknown accounts and uncredited cash and cheque lodgements totalling ¢463.0 million. The failure of the respective VAT offices to regularly prepare bank reconciliation statements resulted in the lapses. We recommended that management should ensure that bank reconciliation statements are prepared monthly and all unreconcilled items investigated.

26. Funds totalling ¢399.4 million were not promptly transferred from various commercial banks into the Consolidated Fund at Bank of Ghana due to the failure of District Finance officers to monitor the operations of such accounts. In order to enhance the Government cashflow position, we recommended prompt transfer of these and subsequent funds into the Consolidated Fund.

27. Various MDAs within the Volta Region failed to return to their treasury offices, receipted duplicate copies of payment vouchers as evidence of disbursement of the amounts involved. As a result, we could not ascertain the total payments of ¢918.3 million made on these vouchers. We recommended to the DFOs to retrieve the outstanding vouchers to confirm the disbursements.

28. The debt stock of the Tema Large VAT Office (LVO) was ¢8.24 billion as at 31 December 2006 due to the failure of the Tax office to strictly apply the tax collection enforcement regulations regarding monitoring progress and collection of debts. We recommended that management should pursue pragmatic recovery policies, including legal action to recover the debts.

29. Traders under the jurisdiction of the Kaneshie Industrial Area and the Osu Local Office were indebted to the VAT Service in the sum of ¢46,018.9 million in respect of penalty for failing to file tax returns, assessments raised during control verifications and unredeemed returned cheques. We recommended to the Local offices to employ all institutional and legal measures to recover the debts.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 11

30. Forty-two VAT registered traders under the Kumasi VAT office issued dud cheques amounting to ¢454.0 million for the settlement of their tax liabilities between January 2004 and June 2006. The action of the traders deprived the Service of timely use of the tax revenue. We recommended to management to recover the amount and strengthen its tax collection enforcement procedures to forestall such acts by traders.

31. Tax irregularities such as failure to deduct tax, failure to establish debts in taxpayers account, failure to charge interest and levy penalty and failure to obtain VAT invoices totalling ¢7.24 billion were recorded by MOFEP and some of its departments during the year under review. The inaction of the Ministry and the affected departments to apply and enfore relevant tax laws accounted for the lapses. We recommended prompt payment of all unremitted taxes and strict compliance with the tax laws.

32. Post Clearance and Warehousing Unit audits carried out by CEPS management during the year disclosed underpayment of duties and penalties totalling ¢28.39 billion. Factors such as poor record–keeping by warehouse keepers and manipulation of customs values by some importers to reduce liabilities accounted for the lapses. We recommended prompt recovery of the duties from the importers and improvement in record-keeping as well as applying stringent measures to deal with tax defaulters.

33. Four companies who were allowed to clear goods by paying part of the duties and the balance later abused the facility, resulting in an outstanding amount of ¢2.08 billion. We recommended recovery of the amount and the exercise of circumspection by management in granting credit facilities.

34. The Internal Revenue Service failed to collect National Reconstruction Levy totalling ¢759.7 million due to its inability to notify taxpayers of their obligation. We recommended to the Service to collect the outstanding amount and ensure that tax payers are notified of their obligations promptly.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 12

35. The indebtedness of IRS in respect of PAYE stood at ¢5.48 billion as at 31 December 2005. Management explained that the late receipt of its 2.8% retention accounted for its inability to promptly pay its PAYE taxes. We recommended that the Service should settle its outstanding tax from its retention and also liquidate the penalty for late payment.

36. Stores and procurement irregularities such as failure to route stores and fuel purchases through store recods and vehicle log books and the excess printing of certificates totalled ¢109.4 million for the year. Non-compliance with procurement rules and procedures and store regulation and lack of efficient and qualified staff to manage the procurement and store-keeping transactions in the Ministry mainly accounted for the identified irregularities. We recommended compliance with existing store and procurement regulations and the strengthening of supervisory controls to enhance transparency and accountability in procurement and store keeping function of the Ministry.

37. Failure of the Akatsi District Finance Office to promptly delete the names of five deceased pensioners from the payroll resulted in the payment of unearned salaries totalling ¢22.0 million into their bank accounts. We recommended recovery of the illegal payments and the prompt deletion of the names of the separated staff from the payroll.

38. An Accountant of the PWD Regional Office, Accra forged the signature of the Regional Engineer on payment vouchers and fraudulently withdrew a total of ¢539.0 million from the Treasury’s Account at the Bank of Ghana between March and May 2005. Even though he is currently on interdiction, we recommended that the matter be reported to the Police and appropriate measure instituted to prevent a recurrence.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 13

MINISTRY OF ENERGY

39. Non-adherence to the provisions of Section 87 of the Internal Revenue Act, 2000 (Act 592) by management of the Ministry led to the retention of 5% withholding tax of ¢104.8 million deducted between April and November 2004. We requested management to remit the amount to IRS and ensure compliance with the tax law.

40. Due to improper monitoring, Oil Marketing Companies (OMC) defaulted in the payment of Bulk Oil Storage Transportation (BOST) margin amounting to ¢3.78 billion between 2004 and 2005. To prevent loss of revenue to Government, we advised management to liaise with the BOST Secretariat to recover the amount and also introduce ledger accounts to facilitate monitoring of the debts.

41. Management’s inaction to enforce the provisions of the Criminal Code Amendment Decree, 1973 (NRCD 160) led to the issuance of dud cheques totalling ¢26.20 billion by its clients. We

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 14

advised management to redeem the cheques and enforce the provisions of the Decree.

MINISTRY OF FOREIGN AFFAIRS

42. Due to inadequate supervision and improper segregation of duties, Foreign Missions’ operations were characterised by substantial cash irregularities involving US$229,619 (¢2.12 billion) and Є36,257 (¢440,146.9 million). The irregularities included misappropriation, imprests not accounted for and wasteful expenditure. To minimise these irregularities, we recommended strengthening of supervisory controls over finances of the Missions and strict adherence to the Foreign Service Accounting Instructions, the FAA, 2003 and the FAR, 2004.

43. We noted overpayment of salaries to Home-based staff totalling US$1,115,948 (¢10.28 billion) due mainly to the use of wrong exchange rates in salary conversions. We recommended that adequate controls should be exercised by MOFEP, MFA and CAGD over the use of exchange rates at the Missions.

44. The incidence of failure on the part of foreign-based staff to refund utility bills paid by the Missions on their behalf and also retire imprests at due dates was high. In this connection, Є30,909 (¢375.2 million) and US$2,862 (¢26.4 million) respectively were outstanding against some home-based staff as at the end of 2006. Lack of effective monitoring of these transactions led to the anomaly. We recommended close monitoring of these transactions by Heads of Chancery and strict adherence to the Foreign Service Accounting Instructions, the FAA, 2003 and the FAR, 2004.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 15

MINISTRY OF HEALTH

45. Due to management’s failure to effectively monitor imprests, provide proper custody for payment vouchers and ensure proper acquittance of payments, cash irregularities totalling ¢5.17 billion were noted during the year. We recommended strict enforcement of the relevant provisions of the FAA, 2003 and FAR, 2004 by managements to curb the anomalies.

46. Non-adherence to the provisions of the Public Procurement Act, 2003 (Act 663) and Stores Regulations, 1984 led to stores/procurement irregularities totalling ¢2.80 billion. We recommended to managements of the various institutions under the Ministry to ensure strict compliance with the afore-mentioned regulations to ensure value for money in procurement transactions.

47. Owing to delays in the deletion of names of separated staff of Health Institutions from the payroll, a total amount of ¢353.0 million was paid as unearned salaries into the bank accounts of a number of

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 16

separated staff. We advised Heads of the various Institutions to recover the amounts to chest, ensure prompt deletion of the names and regular monitoring of the payroll to prevent a recurrence of the anomaly.

48. Our review disclosed that outstanding staff advances and indebtedness of some National Health Insurance Schemes to some Health Institutions amounted to ¢1.92 billion. We urged managements of the Institutions concerned to closely monitor these debts and recover the amounts involved.

49. Tax irregularities which comprised unremitted tax to the IRS and purchases from non- VAT registered suppliers, totalled ¢577.7 million. We recommended prompt payment of the unremitted amounts and strict compliance with Section 30 of the FAA, 2003 to boost tax revenue.

50. Failure by management to ensure the deduction of rent at source led to staff occupying Government bungalow/flats and quarters owing rent totaling ¢352.7 million. We urged management to collect the arrears, maintain a rent register and ensure deduction of rent at source.

MINISTRY OF EDUCATION, SPORTS AND SCIENCE

51. The Ministry’s failure to exercise due diligence led to the excess printing of National Best Teacher Award certificates worth ¢197.8 million. We recommended to management to institute measures to prevent recurrence in future.

52. Non-enforcement and non-compliance with Regulations 2(c) and 39(c) of FAR, 2004 resulted in cash irregularities involving ¢2.60 billion. The lapses

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 17

included, misappropriation of revenue, losses and misapplication of funds. We recommended strict adherence to the above Regulations and relevant provisions of the FAA, 2003 to curb the lapses.

53. Advances recoverable from staff and institutions by the GES management stood at ¢2.07 billion as at the end of 2006. We advised management to intensify its efforts at collecting the over-due amounts. We also recommended regular review and follow-up of advances granted.

54. Due to inadequate co-ordination among management, CAGD and the commercial banks, unearned salaries totaling ¢371.0 million were paid to a number of separated staff. We recommended recovery of the amount and effective co-ordination among these institutions to curb this payroll irregularity.

55. Stores/procurement irregularities which included items not taken on ledger charge and fuel not recorded in log books, totalled ¢516.5 million due to non-enforcement of the relevant provisions of the Store Regulations. We advised management to ensure strict compliance with Stores Regulations 0522 and 0529.

56. Non-compliance with Sections 87 and 88 of the Internal Revenue Act, 2000 (Act 592) resulted in tax irregularities amounting

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 18

to ¢229.0 million. We advised management to recover the amount for payment to the Internal Revenue Service and also ensure strict adherence to the tax laws.

MINISTRY OF LANDS, FORESTRY AND MINES

57. An officer of the Land Title Registry, Tema misappropriated revenue amounting to ¢126.0 million. Additionally, a revenue inspector of the Administrator of Stool Lands, Techiman and two revenue collectors of Lands Department, Bekwai failed to account for revenue totalling ¢14.7 million. We advised their respective managements to intensify supervision over the revenue collectors and ensure that the amounts are recovered from them. We also advised that disciplinary action should be taken against the culprits in line with Regulation 8(1) of L.I. 1802.

58. The Accounts Section of Lands Commission Secretariat failed to produce for audit, 144 payment vouchers amounting to ¢2.40 billion covering January 2004 to December 2005. We urged management to trace the payment vouchers and submit them for audit, failing which the amount involved should be recovered from the schedule officer.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 19

59. The Lands Commission Secretariat used ¢1.10 billion out of revenue collected to meet its recurrent expenditure pending receipt of funds from MOFEP. We reminded management that its action contravened Regulation 22(1) of the L.I. 1802 and advised compliance with the regulation.

60. Out of ¢95.5 million loans granted to Disaster Volunteer Groups (DVGs) in five NADMO District offices in 2004 and 2005 for the purchase of seeds and fertilizers and for okro and peper farming, ¢85.5 million remained unpaid as a result of lack of criteria for recovery of the loans. We recommended that management should intensify its efforts to recover the loans and define appropriate criteria for the disbursement and recovery of loans.

MINISTRY OF THE INTERIOR

61. Owing to delayed release of funds from MOFEP, management of Ghana Immigration Service (GIS) failed to pay into the Special Collections Account an amount of US$15,770 being part of a total collection of US$380,125. The amount was used to finance staff foreign travels. As of now, US$2,400 has been refunded, leaving US$13,370. We urged management to pay the balance into the Special Collections Account and ensure compliance with Regulation 22(1) of the L.I. 1802.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 20

62. Between May and September 2006, the Tema office of GIS paid collections totalling ¢1.12 billion to GIS Head office in Accra instead of Bank of Ghana, in contravention of Head office directive issued on 12 May 2006. We recommended strict adherence to the financial directives and Regulation 22(1) of L.I. 1802.

63. Due to inadequate procurement planning, 7,094.21 metres of camouflage materials and 1,040 pieces of uniforms purchased at the cost of ¢976.2 million for use by Police officers on United Nations assignment had remained in stock for 18 months. We advised management to adequately plan its procurements in line with the Public Procurement Act, 2003 (Act 663).

64. Uncompleted projects amounting to ¢17.02 billion initiated between 1999 and 2005 were abandoned for new projects costing ¢18.56 billion which had not been budgeted for by the Police Administration. We urged management to ensure judicious use of government resources by ensuring continuity in project execution.

65. The Police Hospital used IGF amounting to ¢4.07 billion to purchase drugs and other consumables without parliamentary approval. We advised that management should seek retroactive parliamentary approval for the retention of the amount through MOFEP.

66. Between January 2004 and December 2005, the Ghana National Fire Service (GNFS) procured goods worth ¢2.13 billion from eight non-VAT registered companies, resulting in the loss of ¢319.9 million in revenue. We recommended that management should comply with the provisions of Public Procurement Act and also reprimand the officers responsible for the purchases.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 21

MINISTRY OF WATER RESOURCES, WORKS AND HOUSING

67. An official of the PWD office, Tamale misappropriated revenue of ¢6.6 million as a result of lack of supervision on the part of his management. We urged management to recover the amount from him and disciplinary action taken against him in accordance with Regulation 8(1) of L.I. 1802.

68. A contractor who was paid 30% mobilisation advance of ¢4.50 billion in October 2005 for hydrological works valued at ¢15.0 billion which he was to complete within five months, delivered only 6% of the work and vacated the project site, nine months after the scheduled completion date. The matter has been referred to the Attorney General’s office for advice.

69. Due to poor supervision and lax control over accounting documentation, a former Accountant and revenue collectors of the Water and Sanitation Development Board (WSDB) in Bibiani and Donkorkrom misappropriated revenue totalling ¢38.5 million and ¢36.8 million respectively. We urged the Board to step up its supervisory role and ensure recovery of the amount. We also advised

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 22

management to take disciplinary action against the culprits in line with Regulation 8(1) of L.I. 1802.

70. Cash shortages of ¢30 million and ¢48.4 million were noted against the Accountant and Stand Pipe Agents (SPAs) of the Donkorkrom office respectively. We advised the Board to recover the amounts from them and also ensure that disciplinary actions are taken against them in compliance with Regulation 8(1) of L.I. 1802.

OFFICE OF GOVERNMENT MACHINERY

71. Rush purchases of items led to management’s inability to ensure the recording of store items worth ¢255.2 million in the store ledger. We requested management to prepare an annual procurement plan which will help address the problem of unrecorded stores in accordance with the Public Procurement Act, 2003 (Act 663).

72. Management’s failure to conduct quality assurance tests led to the loss of US$121,336.50 (¢1.12 billion) on garment exports to the USA. Also, lack of good credit control policy resulted in an outstanding debt of US$19,064 (¢175.6 million). We recommended

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 23

to management to investigate the loss and appropriate disciplinary action taken against those responsible. We also advised management to conduct quality assurance on maiden garment exports to ensure success of the PSI. Meanwile, credit control system should be put in place to ensure recovery of the debt of US$19,064.

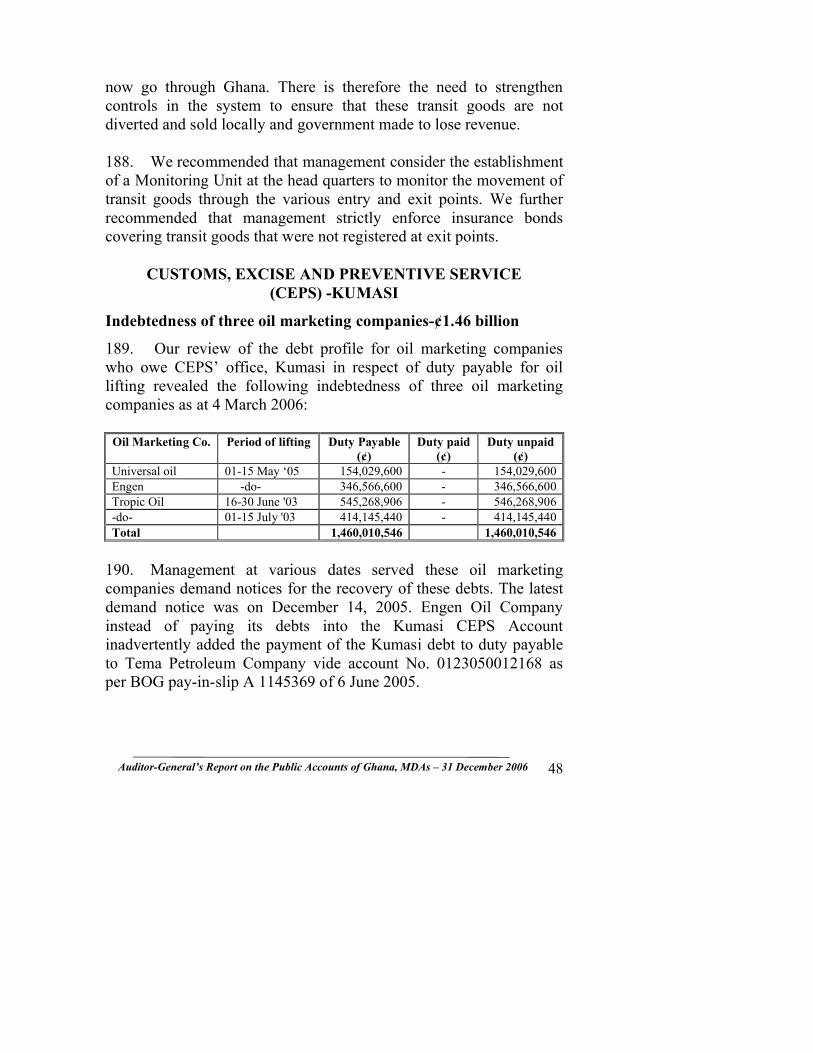

MINISTRY OF FOOD AND AGRICULTURE

73. Store items valued at ¢242.0 million were not taken on ledger charge to provide audit trail and also ensure accountability. The lapse occurred as a result of non-segregation of duties and lax supervision. We urged management to comply with the relevant Stores Regulations, ensure segregation of duties and intensify its supervisory role.

74. The Apam District Office single-sourced the purchase of items worth ¢24.0 million and thus negated the gains of competitive tendering. This resulted from poor management of stock to determine the re-order levels. We recommended prudent management of stock to avoid panic buying.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 24

75. As a result of management’s failure to ensure prompt deletion of names of separated staff from the payroll, ¢190.0 million was paid as unearned salaries to 12 former staff members. We advised managements of the MDAs involved to recover the unearned salaries and improve payroll monitoring.

76. Management neglected to comply with applicable financial regulations resulting in cash irregularities totalling ¢51.1million. Included in the lapses were direct disbursement from revenue of ¢21.1million and wasteful expenditure of ¢19.5 million. We recommended strict adherence to the relevant provision of FAR, 2004 and FAA, 2003.

MINISTRY OF DEFENCE

77. Management of 37 Military Hospital purchased items worth ¢3.11 billion between July 2005 and September 2006 without ensuring that they were taken on ledger charge before usage. We advised management to ensure that all purchases are routed through stores to ensure accountability.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 25

MINISTRY OF TRANSPORTATION

78. The inability of management of the Ministry of Transportation, Headquarters to properly monitor payments resulted in an over-payment of ¢106.2 million to a consultant. We recommended recovery of the amount and proper monitoring of contract payments through contract registers.

79. Thirty General Counterfoil Receipt (GCR) books were not accounted for by the Tema office of the Driver and Vehicle Licensing Authority (DVLA). We advised management to investigate the matter.

80. Audit investigation into alleged revenue misappropriation revealed that an Accounts Officer of the Akim Oda office of DVLA short paid revenue to chest by an amount of ¢634.0 million as a result of ineffective supervision over his duties. The officer also failed to account for 189 GCR books. Management informed us that the culprit had been arrested and arraigned before court. We urged management to pursue the matter with the Police.

81. The Department of Urban Roads, Sekondi made unauthorised variation payments totalling ¢39.1 million which ranged between 32% and 46% over the original contract sums. We advised management to obtain approval for the variations and also desist from the practice of paying for contract variations without approval.

82. Owing to the failure of management of the Wa office of the Department of Feeder Roads to maintain proper monitoring records we could not ascertain the indebtedness of contractors who had been supplied equipment valued at ¢1.35 billion on credit and who were to repay through deductions from contract payments to them. We advised management to open and maintain records on the debts to ensure effective monitoring.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 26

MINISTRY OF TOURISM AND DIASPORAN RELATIONS (MTDR)

83. Lack of proper co-ordination among MOFEP, CAGD and MTDR resulted in the non-deduction of 5% withholding tax of US$29,475 from contract payment of US$589,500 made to Messrs CTK-Network Aviation Ltd. We recommended recovery and remittance of the tax to the IRS and effective co-ordination among the three institutions.

84. Payment voucher with face value of ¢1.08 billion were not presented for audit due to the Ministry’s inadequate control over disbursements. We recommended strict control over disbursements in accordance with Regulation 39 of the FAR, 2004.

85. Management failed to adhere strictly to the provisions of Section 81(1) of the Internal

Revenue Act, 2000 (Act 592), resulting in the non-deduction of withholding tax amounting to ¢666.0 million. We recommended recovery of the amount and strict adherence to the tax law.

86. Due to the intransigence of imprest holders, imprests totalling US$25,000 remained unaccounted for as at 31 December 2006. We advised

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 27

management to use stringent measures to compel the defaulting officers to account for the amounts.

87. The Ministry single-sourced and awarded a contract valued at ¢2.00 billion without seeking approval from the Public Procurement Board (PPB). We recommended that management should seek retrospective approval from the PPB for the award.

MINISTRY OF TRADE, INDUSTRY, PRIVATE SECTOR DEVELOPMENT & PSI

88. We noted cash irregularities involving ¢1.29 billion which included ¢1.22 billion, representing payments to trainees which were not supported by the relevant documentation. The lapse was caused by the non-enforcement of Regulation 39 of the FAR, 2004. We recommended that management should provide the relevant documentation to acquit the payments and ensure compliance with the Regulation.

89. We observed deficiencies in the management of the erstwhile Ghana National Trading Corporation’s (GNTC) properties for which the Ministry has oversight responsibility. In this regard, we noted non-payment of rent and illegal occupation of some of the properties by tenants as some of the anomalies in the administration of the estates. We recommended that the Regional Trade Officers should be given the responsibility to monitor all former GNTC properties in the Regions and collect the rents on them. Also, the Oversight Committee of the Ministry in consultation with the Diverstiture Implementation Committee (DIC) should determine rent payable by the occupants of some of these properties to ensure regular collection of rents from them.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 28

OTHER AGENCIES

90. Five persons from two Agencies were paid unearned salaries totalling ¢40.6 million. We urged management to recover the amounts from the separated staff and also ensure that their names are promptly deleted from the payroll.

91. Fuel worth ¢40.2 million bought by CHRAJ, Bolgatanga and Judicial Service, Sekondi was not recorded in the vehicle log books due to ineffective supervision. We recommended that future fuel purchases should be recorded in vehicle log books.

92. Total payments of ¢230.8 million made by the Judicial Service and the High Court, both of Sekondi were not supported with official receipts from the payees. We requested management to obtain official receipts to authenticate the payments.

93. Deposits and revenue of ¢357.0 million and US$16,140 were misappropriated by the Accountant, Kweku Mensah and his assistant, Doreen Love Akwettey respectively due to break- down in the internal control system. The culprits have been arrested by the Police. We recommended recovery of the amounts and strengthening of the internal control system.

94. Failure on the part of the former Accounts officer to record grants totalling ¢39.7 in a cash book resulted in the amount remaining unaccounted for. We advised that the officer should be made to account for the amount.

MINISTRY OF INFORMATION AND NATIONAL ORIENTATION

95. An Accounts officer at the Volta Star radio station of the Ghana Broadcasting Corporation misappropriated ¢581.9 million revenue collected between 2000 and December 2006 because the

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 29

Regional Accounts officer failed to supervise his work over the period. We recommended that management should recover the amount and also institute disciplinary action against him in accordance with Regulation 8(1) of L.I. 1802. Management should also strengthen internal controls to forestall recurrence.

MINISTRY OF JUSTICE AND ATTORNEY GENERAL

96. Failure by the Accountant of the Registrar-General’s Department, Accra to ensure regular preparation of bank reconciliation statements, resulted in fake bank lodgements of revenue totalling ¢272.8 million in 2004. We recommended that management should conduct further investigation into the matter and ensure recovery of the amount to chest. We also advised management to ensure regular preparation of bank reconciliation statements to prevent a recurrence of the anomaly.

MINISTRY OF MANPOWER, YOUTH AND EMPLOYMENT

97. Due to management’s inability to promptly delete the names of separated staff from the payroll, unearned salaries totalling ¢50.8 million were paid into the bank accounts of five retired or deceased staff of Tema and Takoradi offices of the Labour Department. We urged management to pursue recovery and have the name deleted from the payroll.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 30

98. Non-compliance with Financial Administration Regulation by the Department of Social Welfare, Wa resulted in fuel purchases amounting to ¢18.6 million not entered in the vehicle log books. We advised management to immediately procure and maintain vehicle log books and ensure that all fuel purchases are taken on ledger charge.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 31

PART III

DETAILS OF FINDINGS AND RECOMMENDATIONS

MINISTRY OF FINANCE AND ECONOMIC PLANNING EADQUARTERS

Unacquitted payment vouchers-¢5.01 billion

99. Our audit disclosed that 34 payment vouchers with a face value of ¢5,014,252,900 which were raised for a variety of activities, were not supported with relevant expenditure documents such as receipts, invoices and duly signed statements of claim to authenticate the payments.

100. According to the Chief Accountant, the officers concerned have failed to comply with her persistent requests that payees submit the appropriate expenditure statements, receipts, and invoices to support payment vouchers raised by her.

101. To ensure transparency and accountability, we recommended that management should pressurize the payees concerned to provide the relevant expenditure statements and supporting details for our examination, failing which the amounts involved should be recovered from them. We also urged management to ensure that the relevant supporting documents are attached to all future payment vouchers.

102. Management indicated that the clerks of the appropriate committees of Parliament, from where a significant number of the payment vouchers emanated, would be contacted to produce the relevant supporting documents to authenticate the transactions.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 32

Failure to deduct withholding tax - ¢700.3 million

103. Section 84 (1) (a-d) of the Internal Revenue Act, 2000 (Act 592) requires a person or an employer making payment of fees, commission or emoluments etc, to a resident person to withhold tax on the gross amount of the payment at the rate of 15 per cent as prescribed in part IV (a) of the first schedule of the Act.

104. Our review disclosed that, on the contrary, various allowances paid to both staff and non-staff covering the period 1 January 2004 to 31 December 2005 totalling ¢4,668,374,220 were not subjected to the 15 percent withholding tax deductions amounting to ¢700,256,133.

105. Management could not offer any tangible explanation for its failure to implement the provisions of the tax law.

106. We recommended that management should recover the outstanding taxes and remit them to the IRS. Management should also ensure prompt deductions of appropriate taxes on all future allowances for payment to the IRS in compliance with the tax law.

Unpresented value books and absence of stock register of value books

107. Our audit disclosed that the Chief Accountant failed to maintain a stock register on value books. Consequently, management could not ensure effective control over the acquisition, custody and movement of all value books.

108. The irregularity resulted in the failure of management to present three GCR books for audit check. Details were provided to management.

109. Though the three GCR books were alleged to have been used in collecting revenue involving the sale of budget statements and the amounts recorded in the cashbook, we were unable to confirm the amounts without reference to the duplicate copies of the receipts.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 33

110. We recommended to management to trace the apparently missing three GCRs for audit and also introduce a stock register for value books. Management promised to contact its former Head of the Accounts section who was not available at the time of our audit.

Failure to utilise car loans for intended purpose - ¢604.7 million

111. We noted that 74 members of staff applied for and were granted loans amounting to ¢520,200,000 and ¢84,500,000 in November 2004 and December 2005 respectively by the Ministry of Finance and Economic Planning (MOFEP) to purchase means of transport for the efficient and effective discharge of their official duties.

112. We noted however that the beneficiaries failed to utilise the loans for the intended purpose on the grounds that they were sourcing for more funds elsewhere to add up to the loans granted. They claimed that the loans granted them were not sufficient enough to enable them purchase the required vehicles.

113. We recommended that management should prevail on the appropriate authorities to make vehicle advances realistic enough to enable officers purchase means of transport in future. Management should also ensure that the loans are utilized for the intended purpose or the amount involved should be recovered to chest.

Ten missing vehicles

114. Our review of the stock sheet of MOFEP fleet of vehicles obtained from the Transport Officer covering the period 2002 to 2004 disclosed that ten vehicles could not be accounted for, as they could not be traced during a physical inspection. The Transport Officer maintained that he had no idea of the whereabouts of those vehicles.

115. Our enquiry at the Driver and Vehicle Licensing Authority (DVLA), however, revealed that the vehicles were registered in the

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 34

name of individuals and institutions. We could therefore not confirm whether those vehicles in the names of individuals were sold to them and under what circumstances, and whether they had been paid for or not.

116. Interviews we had with the Security Officers at the gate disclosed that vehicle movements to workshops for repairs and maintenance were scarcely recorded at the gate, except on weekends. In our opinion, the failure by management to promptly detect the disappearance of the ten vehicles is attributed to the absence of an Assets Register, which would have enabled the monitoring of the movements of MOFEP vehicles. We urged management to conduct adequate investigation into the missing vehicles to determine the whereabouts of the vehicles and their current ownership status.

117. Management assured that investigations were underway to locate the missing vehicles. Also, a plant inventory register had been introduced for the Ministry’s vehicles for effective monitoring.

Vehicles not covered by documents of ownership

118. Section 6 of Road Traffic Regulations, 1974, requires that any registered vehicle bought or which change hands should be transferred to the new owner with all the necessary documents.

119. Our examination of the Ministry's vehicle files, however, disclosed non-compliance with this requirement. Out of 70 vehicles purchased between 1995 and 2004, 24 were still in the name of the vendors. 120. We further noted that 15 vehicles, received as donation from Project Coordinators, were not covered by DVLA certificates of ownership.

121. Upon inquiry, the Transport Officer informed us that the vehicles were registered by the vendor companies from whom the purchases were made. He further explained that he had written to the

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 35

vendor, Toyota Ghana Ltd. for transfer of ownership on seven vehicles but the company had not taken the requested action. He could, however, not provide us with receiving reports indicating the source and conditions of the donated vehicles.

122. In the absence of proper documentation of ownership, these vehicles, most of which have private registration numbers, could easily lose their ownership identity.

123. We recommended that management should take steps to effect the necessary transfers into the Ministry’s name, to pre-empt any avoidable loss. Management responded that the Transport Officer had been requested to get in touch with the DVLA to effect immediate transfer of ownership to MOFEP.

Assets register

124. Our review of inventory records disclosed that assets made up of office equipment and furniture acquired by the Ministry since 1997 had not been recorded in any Fixed Assets Register to safequard them. Besides, we observed that there were no inventory list displayed in any of the offices in the main building and the annexes. We also noted that 98 percent of the assets at the various divisions and units were not labelled with MOFEP’s identification logo to confirm ownership. This is in breach of Regulation 2(n) of FAR, 2004 (L.I. 1802) which enjoins heads of departments to compile and maintain assets registers of their departments.

125. Upon inquiry, the Estates Manager explained that there was no handing over notes and no assets register when he took over the office, but he took the initiative to compile a list of some of the assets.

126. We recommended that management should up-date the existing assets register, display inventory lists in all offices and label all assets with the Ministry’s logo. Management responded that steps were being taken to address the lapses.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 36

Lack of action on obsolete and unserviceable assets

127. We observed that unserviceable items made up of computers, printers, photocopier machines and fax machines have been kept in many offices for 2-12years. We also noted that obsolete items made up of plant, equipment and furniture were dumped in rooms at the ends of various floors of the main Ministry block, Redco Warehouse, Redco Guest House and Dansoman Estate Staff Flats.

128. According to the officer in charge of the Maintenance Unit, the items were dumped at these locations after the last public auction of obsolete items held in June 1999 and that no further auction has taken place since then.

129. To prevent further deterioration of these assets and subsequent loss in value, we recommended that early action should be taken to dispose of them. We also suggested that equipment breakdown should be reported promptly for repairs whilst the Ministry introduces asset management policies for its future guidance.

130. Management intimated that arrangements had been made to sort out all assets that have outlived their useful lifespan for auction.

VALUE ADDED TAX (VAT) SERVICE

TEMA LARGE VAT OFFICE (LVO)

Misappropriation of revenue - ¢383.8 million

131. An audit disclosed that between August 2004 and September 2005, Mr. J.M.K. Abedu, an Accounts Clerk of the Tema LVO through fraudulent means short paid to chest revenue he received from VAT registered traders to the tune of ¢383,846,950. He succeeded in perpetrating the fraud due to lack of effective supervision over his work. Mr. Abedu has vacated his post whilst management has retrieved only ¢30,800,000 from him, leaving a balance of ¢353,046,950 unrecovered.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 37

132. We recommended to management to recover the outstanding amount and take appropriate disciplinary action against Mr. Abedu. Management should also strengthen supervisory control over revenue collection to avoid a recurrence of the fraud.

Poor debt management and huge debt stock - ¢8.24 billion

133. The debt stock which represents amounts owed by taxpayers to the Office, stood at ¢8,240,000,000 as at 31 December 2006. Our review disclosed that ¢2,718,406,568.77 representing 33% of the total debt stock as at May 2006 was declared uncollectible. We were however not provided with any authority/express permission endorsing the uncollectability of the debt. Also, 38% of the debt stock amounting to ¢3,128,278,157.73 was described as 'others' for which no breakdown was provided.

134. We noted that the Enforcement and Debt Management Unit (EDM) of the office failed to maintain accurate enforcement progress sheets, (VAT 46) to record and monitor progress of action to be taken on debtors.

135. We advised management to adhere strictly to section 3(3) of the Value Added Tax Service operational manual which spells out action to be taken on debtors to minimise the debt stock.

Outstanding rescheduled debt - ¢883.0 million

136. We observed that Legon Fishing Co. Ltd's debt of ¢1,529,179,386.54 was rescheduled as per Head Office letter referenced OPS-EDM-051206 of 6 December 2005. In the said letter the company should have finished paying by May 2006.

137. On the contrary, we noted that as at 14 July 2006 the company had paid ¢735.0 million, leaving a balance of ¢883,074,908.79. The Local offfice however failed to inform Head office for the next line of action to be taken to retrieve the outstanding amount.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 38

138. We recommended that interest should be charged on the outstanding amount and steps taken to retrieve the remaining amount. Management responsed that distress procedures had already been initiated.

KANESHIE INDUSTRIAL AREA (KIA) LVO

Failure to levy penalty on late fillers - ¢1.09 billion

139. The VAT law imposes on every VAT registered person an obligation to file VAT return for each prescribed accounting period of one month. The return must be submitted to the VAT office not later than the last working day of the month immediately following the one to which the return is related as stated in section 28(4) of Act 546. Specific penalty of ¢1,000,000 is imposed under section 28(8) of Act 546 on a taxable person who without justification fails to submit his tax returns on the due date and a further penalty of ¢5,000 for each day that the return is not submitted.

140. Our review of the computer generated report on late filers (ISSU) for the period October 2005 to June 2006 disclosed that there were 1125 late filers for which no notices of penalty charges were served. We however noted from the daily cash register covering the same period that 34 traders were charged penalties totalling ¢39,662,827 during the period for late filing.

141. The net effect is that 1,091 traders who filed their returns late were not charged ¢1,000,000 penalty each and a further ¢5,000 for each day that the return was delayed. As a result, ¢1,090,000,000 billion was lost to the LVO through non-compliance with Section 28(8) of Act 546.

142. We recommended that the LVO should apply Section 28(8) on recalcitrant traders to discourage them from late filing and also increase revenue to the Government.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 39

Issuance of dud cheques-¢138.8 million

143. Our review of the LVO’s bank statements and the returned cheques register revealed that 12 cheques totalling ¢138,785,832 which were dishonoured between December 2005 and July 2006 were still outstanding as at 13 September 2006. The situation contravened Section 31(1) of the VAT Act 546 which requires that “any tax due, penalty and interest which remain unpaid after the due dates may be recovered by the Commissioner".

144. We also did not see any records (VAT 87) raised to reverse the credits and re-establish the debts in the respective traders’ ledgers. Furthermore, there was no evidence that interest was charged on the amounts involved as required under Section 32(1) of the VAT Act.

145. We recommended to the LVO to pursue the traders who issued the dud cheques and retrieve the amount involved to chest. Also, traders whose cheques are consistently dishonoured should be made to pay by cash or bankers draft. Furthermore, an interest register should be opened to record interest charged on dishonoured cheques for subsequent recovery from the affected traders.

146. In response, management indicated that amounts totalling ¢9,949,951 had been recovered from some of the traders as at 2006 and the relevant accounting records (VAT 87) raised to reverse the required credits. Also, out of the list, nine traders had been blacklisted. Additionally, interests had been charged on the amounts and entered in the interest register.

Outstanding debts from traders -¢29.84 billion

147. Section 31 of the VAT Act 546 stipulates that "any tax due, penalty and interest which remain unpaid after the due dates may be recovered by the Commissioner". We noted from the records of the Enforcement and Debt Management (EDM) Unit that a total amount of ¢29,839,937,880.68 was owed by 510 traders of the LVO as at 31

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 40

August 2006. The debt stock figure had come from assessments raised during control verification exercises conducted in 2005 and 2006.

148. We recommended that the LVO should employ all institutional and legal measures to recover the debts. Also, control verification exercises should be done in time to avoid possible huge assessments raised on traders.

149. Management assured us that it had drawn up a debt collection exercise programme to retrieve the debts on monthly basis till December 2006.

LARGE TAX PAYERS UNIT (LTU)

Wrong transfer of revenue - ¢7.90 billion

150. Tax revenue is lodged into LTU/VAT transit account and periodic transfers are made by BOG into VAT main consolidated account. However, we noted that BOG on 24 November 2005 wrongly transferred revenue of ¢7,900,000,000 into the Government Main Treasury Cash Account (GMTC) instead of VAT main consolidated account.

151. Since requisite portions of VAT revenue are credited to the GET fund and the National Health Insurance Scheme, we recommended that the LTU Head should ensure that the transaction is reversed and the amount transferred to VAT main consolidated account. This will enable appropriate disbursements to be made into the various stakeholders’ accounts.

Failure to establish debts in tax-payers account - ¢12.02 billion

152. In order to determine whether additional assessments raised during tax audits are imputed on the LTIPS and established as a debt in the tax payer’s accounts statements, we reviewed 28 comprehensive tax audit reports issued during the year 2005.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 41

153. We observed that additional tax assessments raised in 22 of the 28 audit reports totalling ¢12,020,449,397 had not been debited to the respective traders’ accounts statements.

154. This contravened Section 10.8.3 of the LTU’s procedure manual which requires that findings from tax audits shall be imputed on the LTIPS not more than fifteen days after the completion of an audit. These additional assessments have remained unimputed for periods ranging from 5 to 13 months.

155. We recommended that taxpayers’accounts be updated within fifteen days after issuance of tax audit reports in accordance with the LTU’s procedure manual.

156. The Head of Audit explained that audit officers responsible for the imputing of additional assessment on the LTIPS were initially not conversant with the use of the LTIPS. They had however been trained on it to enable them imput the additional assessment.

Lodgement of revenue in unknown account -¢18.7 million

157. We noted that proceeds from the sale of value books received from the IRS for the period May 2004 to July 2005 which amounted to ¢18,667,000 were paid into the LTU operations account No. 01256-600480-53 and later remitted to the IRS. However, the IRS’ account into which the amount was transferred was not identified to us for our verification.

158. We requested management to provide us with the account number into which the amount was paid to confirm its receipt by the IRS.

159. Management promised to investigate and communicate the outcome to us.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 42

ADABRAKA LVO

Failure to charge interest and levy penalty - ¢5.92 billion

160. We reviewed the report on late filers at the Adabraka LVO for August to November 2005. For the four months sampled and with a materiality limit of one million cedis and above, we noted that a total of 108 traders in payment position failed to file their returns on the due dates and penalties were imposed on them, as well as interest on outstanding tax due from them. These totalled ¢5,092,000,000. We however observed that the Office did not properly monitor these transactions as stipulated under section 28 of the VAT Act 546 and Operational directive No. 035/HQ on imposition of interest on outstanding amounts of VAT.

161. We recommended that the Office should recover the ¢5,092,000,000 and all other penalties and interest due on outstanding VAT amounts. We also advised management to properly monitor these transactions by introducing the appropriate registers as required under the above-mentioned VAT law and operational directive.

OSU LVO

Uncredited cheque lodgements - ¢259.2 million

162. We observed that a total amount of ¢259,238,497.51 paid into the LVO's account at the Bank of Ghana between April 2005 and June 2006 had not been credited to the account. This anomaly was not promptly detected because the office failed to prepare monthly bank reconciliation statements.

163. We recommended that management should write to BOG to credit its account with those lodgements and also ensure regular monthly preparation of bank reconciliation statements. Management assured that it had written to the Bank of Ghana (BOG) to have the account credited with the amount.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 43

Unredeemed returned cheques-¢464.9 million

164. Our examination of the returned cheques register disclosed that 51 traders issued cheques totalling ¢464,859,551 to the LVO which were subsequently dishonoured by their banks. We also noted that as at the close of our audit in December 2006 these traders had not repaid the amounts involved.

165. Though issuance of dud cheques is a criminal offence no action has been taken against the traders contrary to administrative guideline No. FIN.002/HQ of 1 November 2002 which quotes in part that “steps be taken by head of VAT outstations to prosecute offenders to serve as deterrent to others”.

166. Management's failure to institute necessary action against these traders has resulted in this situation which increased the debt stock of the LVO.

167. We recommended that management should write to the traders involved reminding them of the seriousness of their offence, demand payment of the amounts involved or take punitive action against them.

Uncredited amount-¢56.2 million

168. Our verification of revenue transfers by GCB, Osu Branch to BOG VAT accounts revealed that an amount of ¢56,163,700 alleged to have been transferred by GCB to the VAT revenue account No. 01230500120 at the Bank of Ghana on 31/05/05 had not been credited to the account.

169. We further noted that management failed to liaise with either the BOG or the GCB or both why the anomaly occurred. Management's failure to monitor transfers from GCB to BOG revenue account resulted in this irregularity.

170. We recommended and management responded that it had taken steps to ensure the account is credited with the amount.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 44

Indebtedness of traders-¢41.48 billion

171. We noted that 610 traders owe the LVO a total amount of ¢41,477,152,616. This debt resulted from traders filing returns without paying the tax, dishonoured cheques and assessments raised against them.

172. We however noted that management had initiated measures such as distress actions against some of the traders to recover the unpaid debts.

173. This, notwithstanding, we recommended that management should intensify its tax collection efforts to recover the taxes owed by the traders.

VAT SERVICE – KUMASI

Misappropriation of revenue - ¢1.61 billion

174. Our review of a VAT Internal Audit Report issued in December 2005, disclosed that as a result of poor supervision and weak internal control, VAT revenue totalling ¢1,610,473,187 collected during the period 2000 to August 2005 was misappropriated by the underlisted Officers:

No. Name of officer Amount ¢

a. Michael Osei Agyeman/Atakorahb. Amaniampong & Appiah Kubi 1,081,993,839c. Richard Kelly Afeku and Nixon

Toppar 254,678,520

d. Eric Bosompem Twum 27,128,000e. Unidentified signatories 193,526,829.62f. Kennedy Attakora Amaniampong 50,945,000g. Richard Kelly Afeku (IOU) 2,201,000

Total 1,610,473,188.62

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 45

175. In the first four (a-d) the Internal Audit Report which was corroborated by us noted that Mr. Appiah Kubi of the (ISSU) Information Support System Unit) aided the whole process by imputting data (VAT 20, 23 and 30) in the VAT Input Processing System (VIP) ignoring material changes that had been made on the documents by either post dating or back dating the transactions. In the last three (e-g) miscellaneous revenue was misappropriated without lodging it at the bank.

176. We recommended to management to furnish this office with the outcome of the VAT Internal Audit Report submitted to VAT Head Office. This will enable us ascertain the necessary corrective action taken by management to retrieve the embezzled revenue from the officers involved.

Dud cheques - ¢454.0 million

177. Our review of the Returned Cheques schedule as at 30 June 2006 revealed that for the period 18 January 2004 to 30 June 2006, 42 VAT registered traders issued dud cheques totalling ¢453,954,385 for the settlement of their tax liabilities. By this action, coupled with inaction on the part of VAT officials, the 42 traders deprived the Service and consequently the State the timely use of the amount for development purposes.

178. We recommended prompt recovery of this amount from the affected traders. Management responded that revenue totalling ¢274,845,031 had been recovered leaving a balance of ¢179,109,354 against 25 traders and companies.

CUSTOMS, EXCISE AND PREVENTIVE SERVICE

Short collections and penalty imposed - ¢28.39 billion

179. This year’s Post Clearance and Warehousing Unit audits uncovered total short collections of ¢20,023,545,551 made up of ¢19,739,155,704 from post clearance and ¢284,389,847 from

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 46

warehousing. A total penalty of ¢8,369,355,501 was imposed on the enterprises involved. Below is a table showing the short collections and penalty imposed on the enterprises:

Short collection Penalty Total duePost Clearance 19,739,155,704 7,703,278,534 27,442,434,238Warehousing 284,389,847 666,076,967 950,466,814Total 20,023,545,551 8,369,355,501 28,392,901,052

180. Following audit recommendations, an amount of ¢8,774,078,636 representing 43.8% was recovered as compared to 9.3% in 2005. Recovery of short collections has been greatly enhanced by the introduction of the GCNET/GCMS which makes it impossible for an indebted importer to transact any business with CEPS unless the outstanding debt is paid. The reasons for the short collections were:

poor record-keeping by warehouse keepers deliberate manipulation of custom values by some

importers to reduce tax liabilities removal of exempt goods for consumption in Ghana

without payment of the appropriate duties and taxes suppression of actual freight charges paid or payable to

reduce tax liabilities

181. We noted management’s action to overcome these anomalies such as the on-going establishment of a price database system. We also recommended the establishment of Tax Courts to deal swiftly with tax defaulters.

Outstanding re-scheduled duties-¢2.07 billion

182. Four companies were allowed to clear their goods by paying part of the duties and taxes and the balance later. These entities have defaulted and are yet to settle their accounts totalling ¢2,077,243,113 with the Service.

183. We urged management to intensify efforts to retrieve the outstanding tax from the defaulters.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 47

Transit goods

184. Our objective for the audit of goods in transit was to ensure that such goods were not diverted for consumption in Ghana because Government then loses duties and taxes that should have been paid on them.

185. Our review of reports on transit transactions showed that some of the weaknesses identified in our previous reports continued to exist. The following table explains findings at three exit points:

Akanu Elubo PagaTotal transit transactions 401 666 100Transit items registered 322 428 64Re-exportation registered 16 40Transactions not registered 58 198 36

186. We were therefore, unable to satisfy ourselves that vehicles/transactions not registered by the CGNET/GCMS system exited the country. Weaknesses that still exist in the transit scheme include:

Exit stations not given advance information on transit goods and scheduled dates of arrival at exit points.

Non existent communication link between transit officers, departure and exit points.

Ineffective tracking of transit vehicle and goods. Failure to seal transit goods on board vehicles to avoid

being tampered with in the course of the journey. Poor record keeping at departure and exit points. The

problem was now brought to the fore with the introduction of the GCNET/GCMS system.

The GCNET/GCMS system itself fails to capture names of escort officers for easy identification.

187. We noted that the volume of transit transactions has increased tremendously since the Ivorian crises started in 2003. Goods that used to transit through Cote 'D' Ivoire to Burkina Faso, Niger and Mali

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 48

now go through Ghana. There is therefore the need to strengthen controls in the system to ensure that these transit goods are not diverted and sold locally and government made to lose revenue.

188. We recommended that management consider the establishment of a Monitoring Unit at the head quarters to monitor the movement of transit goods through the various entry and exit points. We further recommended that management strictly enforce insurance bonds covering transit goods that were not registered at exit points.

CUSTOMS, EXCISE AND PREVENTIVE SERVICE (CEPS) -KUMASI

Indebtedness of three oil marketing companies-¢1.46 billion

189. Our review of the debt profile for oil marketing companies who owe CEPS’ office, Kumasi in respect of duty payable for oil lifting revealed the following indebtedness of three oil marketing companies as at 4 March 2006:

Oil Marketing Co. Period of lifting Duty Payable (¢)

Duty paid (¢)

Duty unpaid (¢)

Universal oil 01-15 May ‘05 154,029,600 - 154,029,600Engen -do- 346,566,600 - 346,566,600Tropic Oil 16-30 June '03 545,268,906 - 546,268,906-do- 01-15 July '03 414,145,440 - 414,145,440Total 1,460,010,546 1,460,010,546

190. Management at various dates served these oil marketing companies demand notices for the recovery of these debts. The latest demand notice was on December 14, 2005. Engen Oil Company instead of paying its debts into the Kumasi CEPS Account inadvertently added the payment of the Kumasi debt to duty payable to Tema Petroleum Company vide account No. 0123050012168 as per BOG pay-in-slip A 1145369 of 6 June 2005.

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 49

191. As at the time of writing this report in March 2007, the reversal entry by Bank of Ghana, Tema in favour of Kumasi Collection Account in the sum of ¢346,566,600 had not been effected.

192. We recommended to management to pursue the retrieval of the amounts from the defaulting oil companies while action is taken to ensure the reversal of the entry by Bank of Ghana, Tema.

CUSTOM EXCISE AND PREVENTIVE SERVICE-TAMALE

Petroleum tax arrears-¢5.92 billion

193. Our examination of the accounting records and schedules in respect of tax payments for the period under review, disclosed that nine Oil Marketing Companies owed the Service ¢5,920,002,836 in tax arrears. The details were provided to management.

194. The situation was as a result of the lack of vigilance on the part of CEPS to ensure that taxes are paid promptly as and when they fall due.

195. We urged management to pursue recovery of the tax arrears of ¢5,920,002,836 from the Oil Companies and pay same to chest.

Purchases not recorded in store records before disposal- ¢18.8 million

196. Section 30(i) of Financial Administration Act, 2003 (Act 654) enjoins all departments and organisations to maintain adequate records for stores. Our audit of the accounts and related records of the Tamale office of the Service disclosed on the contrary that store purchases worth ¢18,795,000 made during the period under review were not recorded in store records before alleged disposal. In further violation of the Act, issues of stores were made without authorised requisitions.

197. Management’s failure to enforce the laid down regulations resulted in the situation. In the absence of the required records, we

Auditor-General’s Report on the Public Accounts of Ghana, MDAs – 31 December 2006 50

could not confirm the receipt and issues of the items. The lapse could also end up in non-supply of the items and loss of funds to Government.

198. We urged management to ensure that all future purchases together with supplies from CEPS Headquarters in Accra are taken on ledger charge before being issued out.

INTERNAL REVENUE SERVICE - HEADOFFICE

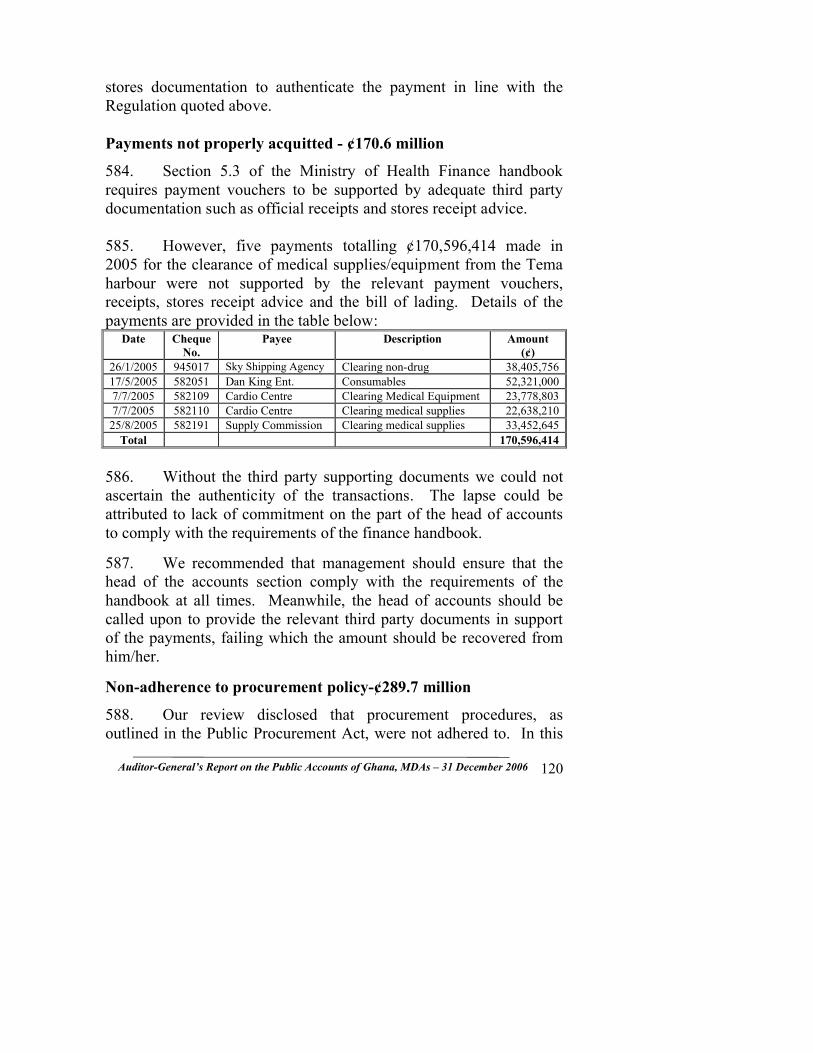

Outstanding corporate tax - ¢18.27 billion