2004 annual report more blue - À propos de … · pierre despars vice president, finance and...

TRANSCRIPT

more blue2004 ANNUAL REPORT

GA

ZM

ÉTR

OLIM

ITED

PAR

TNE

RS

HIP

2004A

NN

UA

LR

EP

OR

T

G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

HIGHLIGHTS

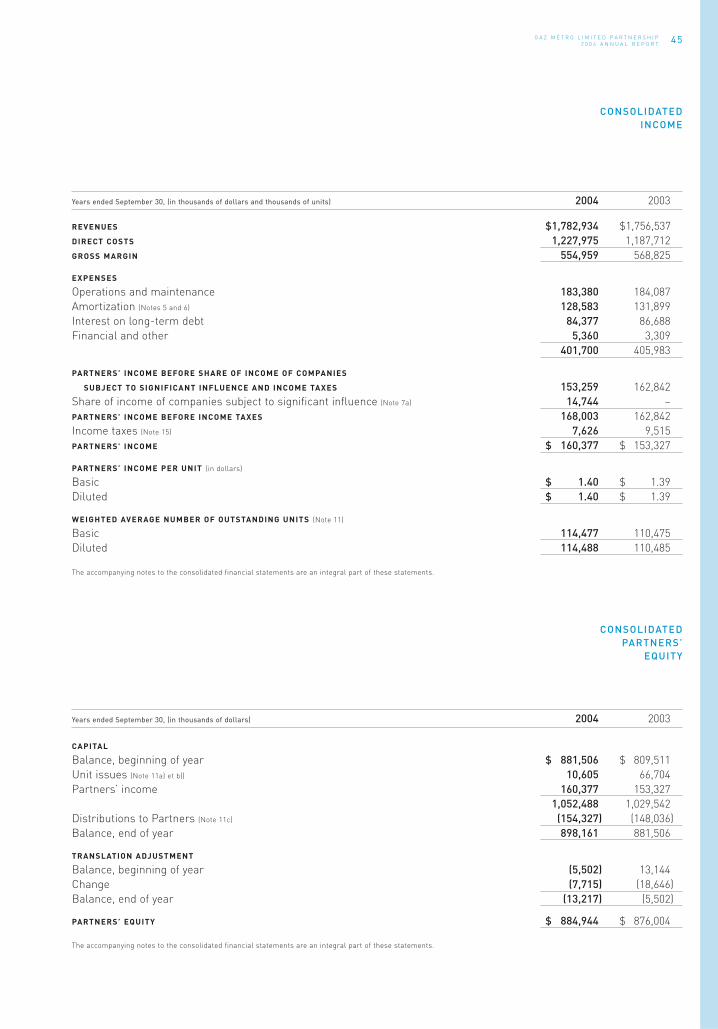

Years ended September 30, (in millions of dollars, except for unit data which is in dollars) 2004 2003

CONSOLIDATED INCOME AND CASH FLOWS

Revenues $1,783 $1,757

Gross margin $ 555 $ 569

Income before interest, taxes and amortization $ 386 $ 385

Partners’ income $ 160 $ 153

Cash flows related to operating activities (before working capital) $ 351 $ 356

Capital expenditures and deferred charges $ 190 $ 235

Partners’ income per unit

Basic $ 1.40 $ 1.39

Diluted $ 1.40 $ 1.39

Distributions paid per unit $ 1.36 $ 1.34

Weighted average number of outstanding units (in millions) 114.5 110.5

Interest coverage on long-term debt over a period of 12 months (times) 2.99 2.88

CONSOLIDATED NORMALIZED VOLUMES (1) (in millions of cubic metres)

MARKETS

Industrial 3,120 3,071

Commercial 1,917 1,905

Residential 752 741

Total 5,789 5,717

OTHER INFORMATION

Authorized rate of return on deemed common equity (Quebec distribution activity) 10.96% 10.34%

Credit ratings

Long-term bonds(2) (S&P/DBRS) A/A A/A

Commercial paper(2) (S&P/DBRS) A-1(low)/R-1(low) A-1(low)/R-1(low)

Stability of distributions (S&P/DBRS) SR-1/STA-1(low) SR-1/STA-1(low)

Market prices on Toronto Stock Exchange (in dollars):

High $22.73 $20.86

Low $19.40 $17.50

Close $21.04 $20.28

Public ownership in Partnership 25.3% 24.9%

CONSOLIDATED BALANCE SHEETS

Total assets $2,361 $2,431

Long-term debt, including current portions $1,209 $1,289

Partners’ equity $ 885 $ 876

Partners’ equity per unit $ 7.73 $ 7.69

Net tangible asset coverage on total long-term debt,

including current portion (times) 1.71 1.66

(1) Estimated volumes at normal temperatures in Quebec only.

(2) Through its General Partner, Gaz Métro, inc.

2,26

3

00

2,35

0

01

2,33

7

02

CAPITAL EXPENDITURES AND DEFERRED CHARGES (in millions of dollars)

139

00

253

01

107

02

CASH FLOWS RELATED TO OPERATING ACTIVITIES(in millions of dollars)

190

00

323

01

299

02

PARTNERS’INCOME(in millions of dollars)

144

00

141

01

155

02

2,43

1

03

235

03

299

03

153

03

2,36

1

04

190

04

341

04

160

04

TOTAL ASSETS (in millions of dollars)

08 transportation and supply systems

10 management committee

12 report to partners

15 mission, objective and the partnership

16 corporate structure

17 the year in review

24 social and environmental report

29 management’s discussion and analysis

43 consolidated financial statements

70 board of directors

75 directors and officers

76 offices

77 information for partners

Just like the large companies that use natural gas for their industrial processes, a growing number of institutions,businesses and homeowners are choosing the “blue solution”to heat air and water. In doing so, these men and women are using the right energy in the right place.

Through the contribution of “blue” to the energy portfolio,Gaz Métro is helping Quebec make even more headway.

more headway

ROBERT TESSIERPresident and Chief Executive Officer

more customers

7,759new customers

opted for the comfort and efficiency of natural gas, a record exceeding

even last year’s performance.The love affair with natural gas

has only just begun.

a more efficient energy

1,310employees

who, every single day, put all their energy into serving our customers well.

Their efficiency can be measured.89%: customer satisfaction rate.

534: points obtained on the Qualimètre, the diagnostic tool of the Mouvement québécois

de la qualité. Exceptional progress. At Gaz Métro, more efficient energy

is also a question of human resources.

more growth

15% annualized total return of a

Gaz Métro unit for 11 years, which is 5% higher than the average return on the S&P/TSX index.

08 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

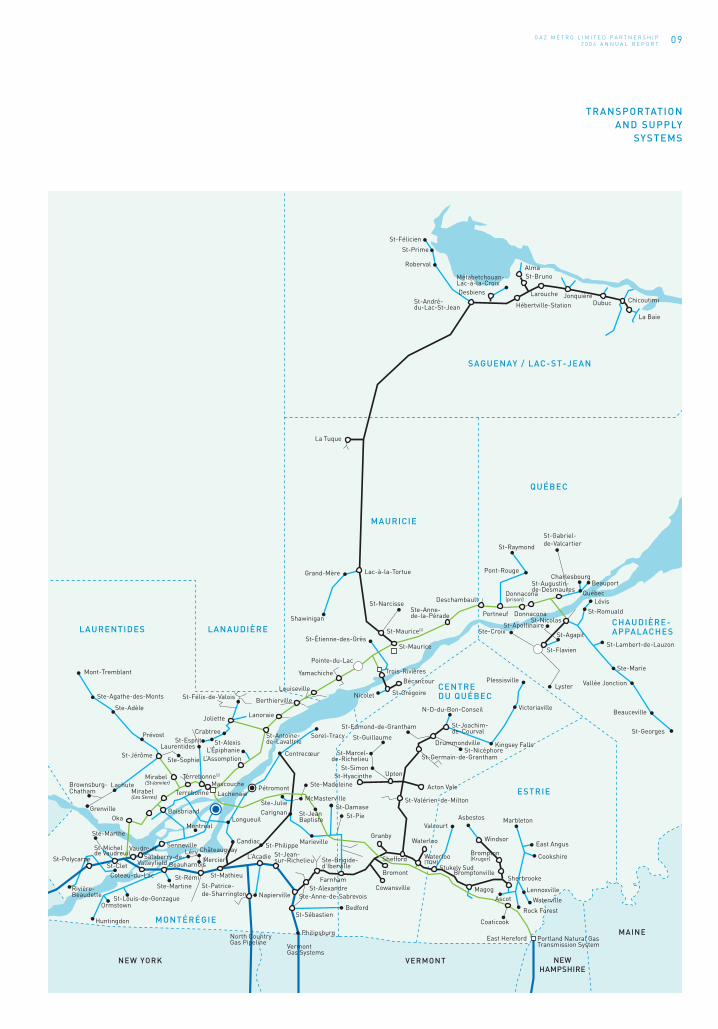

TRANSPORTATION AND SUPPLY SYSTEMS

Ottawa

CornwallIroquois

Gatineau

ONTARIO

ABITIBI-TÉMISCAMINGUE

Thorne

Témiscaming

Earlton

Rouyn-Noranda

Malartic

Amos

Val-d’OrLouvicourt

Map of the territory (not to scale) November 2004

Main distribution lines

Transportation system (TQM)

Transportation system (TCPL)

Distribution system (partial representation)

Champion Pipe Line

Compressor station

City gate station

Underground storage

Liquified natural gas plant

Intrafranchise gas supplier

Transportation system

Gazifère

09G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

TRANSPORTATION AND SUPPLY

SYSTEMS

St-Félicien

St-Prime

Roberval

St-André-du-Lac-St-Jean

La Tuque

Grand-Mère

Shawinigan

Lac-à-la-Tortue

St-Raymond

Pont-Rouge

Deschambault

Portneuf Donnacona

CharlesbourgBeauport

QuébecLévis

St-Romuald

St-Lambert-de-Lauzon

Ste-Marie

Vallée Jonction

Beauceville

St-Georges

St-Nicolas

St-Flavien

St-ApollinaireSte-Croix St-Agapit

LysterPlessisville

VictoriavilleN-D-du-Bon-Conseil

St-Joachim-de-Courval

St-GuillaumeSorel-Tracy

Contrecœur

Upton

Acton Vale

Valcourt

WaterlooGranby

CarignanLongueuil

Candiac

L’Acadie

St-Mathieu

St-PhilippeLéry

Beauharnois

Châteauguay

Mercier Salaberry-de- ValleyfieldSt-Clet

Ste-Marthe

St-Polycarpe

VaudreuilSt-Michel de Vaudreuil

Coteau-du-Lac

Ormstown

Huntingdon

St-Louis-de-GonzagueRivière-Beaudette

Senneville

St-RémiSte-Martine

NapiervilleSt-Patrice-de-Sharrington

St-Sébastien

Philipsburg

VermontGas Systems

North CountryGas Pipeline

Ste-Brigide-d’Iberville

St-Jean-sur-Richelieu

Marieville

McMasterville

Ste-Madeleine

St-DamaseSt-PieSt-Jean

Baptiste

Ste-Julie

Pétromont

Shefford

Bromont

CowansvilleSt-AlexandreFarnham

Bedford

Ste-Anne-de-Sabrevois

Waterloo(TQM)

Windsor

Brompton(Kruger)

Marbleton

Stukely Sud

Asbestos

East Angus

Cookshire

Lennoxville

Waterville

Rock Forest

Coaticook

AscotMagog

BromptonvilleSherbrooke

East Hereford Portland Natural GasTransmission System

St-Valérien-de-Milton

St-SimonSt-Hyacinthe

St-Marcel-de-Richelieu

St-Edmond-de-Grantham

Drummondville

St-Germain-de-Grantham

Kingsey FallsSt-Nicéphore

St-Augustin-de-Desmaures

Donnacona(prison)

Ste-Anne-de-la-Pérade

St-Narcisse

St-Maurice

St-Maurice(2)

St-Étienne-des-Grès

Pointe-du-Lac

Yamachiche Trois-RivièresBécancour

St-GrégoireNicoletLouiseville

Berthierville

St-Alexis

L’Assomption

Lachenaie

Joliette

CrabtreeSt-Esprit

Ste-Adèle

Ste-Agathe-des-Monts

Mont-Tremblant

Prévost

St-Jérôme

GrenvilleOka

Boisbriand

Montréal

Laurentides

Ste-Sophie

Mirabel(St-Janvier)

TerrebonneMascouche

Terrebonne(2)

St-Félix-de-Valois

Métabetchouan-Lac-à-la-CroixDesbiens

Hébertville-Station

AlmaSt-Bruno

Larouche JonquièreDubuc

La Baie

Chicoutimi

SAGUENAY / LAC-ST-JEAN

QUÉBEC

St-Gabriel-de-Valcartier

CHAUDIÈRE-APPALACHES

CENTRE DU QUÉBEC

MAINE

VERMONTNEW YORK

MAURICIE

LAURENTIDES LANAUDIÈRE

MONTÉRÉGIE

ESTRIE

Lanoraie

L’Épiphanie

St-Antoine-de-Lavaltrie

LachuteMirabel(Les Serres)

Brownsburg-Chatham

NEWHAMPSHIRE

10 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

MANAGEMENTCOMMITTEE

RENÉ BÉDARDVice President, Legal Affairs

and Corporate Secretary

LUC SICOTTEVice President, Planning

Gaz Métro and President

and Chief Executive Officer,

Gaz Métropolitain Plus

JEAN SIMARDVice President, Public

and Governmental Affairs

SERGE RÉGNIERVice President, Human

Resources, Quality and

Internal Communications

PIERRE DESPARSVice President, Finance

and Corporate Affairs

JACQUES CHARRONVice President, Operations

SOPHIE BROCHUVice President, Customer

and Gas Supply

ROBERT TESSIERPresident and

Chief Executive Officer

Second row

First row

11G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

MANAGEMENTCOMMITTEE

RENÉ BÉDARDA graduate in law from the Université de Sherbrooke and a member of theBarreau du Québec since1964, René Bédard first worked as a litigation lawyerfor a Montreal firm before joining the Expo ‘67 Legal Department. Later, he acted as Legal Counsel for Wabush Mines, then for SOQUIP, where hebecame Vice President, Legal Affairs in 1982. In 1987, he joined Noverco asVice President, Legal Affairs and Secretary. With Gaz Métro since 1990, initiallyas Corporate Secretary, he was appointed Vice President, Legal Affairs andCorporate Secretary in 2003.

PIERRE DESPARSPierre Despars has a degree in Business Administration from HEC Montréaland an MBA from Concordia University. He is a Chartered Accountant and aCertified Management Accountant. After starting work at KPMG in 1985, hebecame Plant Controller and Accounting Manager at Imprimeries Quebecor.He joined Gaz Métro in 1991 as an advisor and held various positions beforebeing named Vice President, Administration and Regulatory Affairs in 1996,then Vice President, Finance and Corporate Affairs in August 2003. He sits onthe boards of Gaz Métropolitain Plus, TQM Pipeline, Northern New EnglandGas (NNEG), Vermont Gas and NordTech Aerospace. He is also a member of theAudit Committees at NNEG, Vermont Gas and NordTech Aerospace. In additionhe is a director of the Maison des greffés and the Amis de Jean de la Mennais.

LUC SICOTTEA graduate in business administration, Luc Sicotte obtained his MBA (Finance)in 1980. Since then, he has worked for large management consulting firms,was Treasurer for Groupe La Laurentienne from 1987 to 1994 and Vice President,Finance for Groupe Transcontinental (1994-1998), before becoming Vice Presidentand Chief Financial Officer at Gaz Métro. In August 2003 he was appointed Vice President, Planning and President and Chief Executive Officer, Gaz Métropolitain Plus. Mr. Sicotte is responsible for the unregulated activities of Gaz Métro. He is Chairman of the Board of Directors of Aqua Data andAqua-Rehab, represents Gaz Métro on the board of InfraMetrix of Boston, and is a director of VDN Cable.

JACQUES CHARRONJacques Charron obtained a B.Sc. from Université de Montréal and held management positions at Scotiabank, Pratt & Whitney Canada and GEC Alstombefore joining Gaz Métro in 1997. First appointed Vice President, HumanResources, Technological Development and Customer Services, he was named Vice President, Operations in November 2001. He chairs the Board of Directors of the Natural Gas Technologies Center and sits on the boards of Gaz Métropolitain Plus, Consulgaz, Aqua-Rehab, Le Boulot vers..., Champion Pipe Line Corporation, and Hôpital Maisonneuve-Rosemont.

JEAN SIMARDA lawyer, Jean Simard has specialized in public affairs for more than 20 years,mainly in crisis management, government relations, environmental commu-nications and strategic counsel. Initially a political advisor, he developed aconsulting practise in environment and energy-related public affairs. He wasVice President, Energy and Environment at HKDP prior to becoming VicePresident, Public and Governmental Affairs at Gaz Métro in May 2004. He isDeputy Chair of the Nature Conservancy of Canada, Quebec Region. He is amember of the Barreau du Québec, the John Molson School of BusinessConsultative Committee, the Canadian Gas Association, the Canadian EnergyCouncil and the Association de l’industrie électrique du Québec.

SOPHIE BROCHUA graduate in Economics from Université Laval, Sophie Brochu is an energyspecialist. She began her career with SOQUIP in 1987 as a financial analyst,became Assistant to the President in 1991, then Vice President, Development,until 1997, when she joined Gaz Métro as Vice President, Business Development.She later took over the responsibility for strategic planning and natural gassupply. In January 2003, she also became Vice President, Sales, Marketing andCustomer Services.

SERGE RÉGNIERFollowing a B.A. from Université de Sherbrooke, Serge Régnier studied manage-ment at Concordia University and industrial relations at Université de Montréal.He joined Culinar in 1984, before holding management positions in personnel andindustrial relations at Agropur, Fine Cheese Division, and at Natrel. He joinedGaz Métro in1998 as Director, Human Resources, Advisory Services and wasnamed Vice President, Human Resources, Quality and Internal Communicationsin November 2001. He sits on the Board of Directors of the Mouvement québécoisde la qualité, Association québécoise des allergies alimentaires, Aqua Dataand Gaz Métropolitain Plus.

ROBERT TESSIERRobert Tessier has been President and Chief Executive Officer of Gaz Métrosince 1997. He started his career in the public sector where, among others,he was Vice Rector of the Université du Québec, Secretary of the Conseil duTrésor du Québec, Deputy Minister in the Ministère de l’Énergie et desRessources, and Executive Vice President of Société générale de financement.From 1991 to 1992, he was President and Chief Executive Officer of MIL Groupand, from 1992 to 1996, of Alstom Canada. Mr. Tessier is a director of AXACanada, Investors Group Corporate Class Inc, CGI Group and the CanadianGas Association. He also chairs the board of the Montreal Heart Institute.

12 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

NEW CORPORATE FAMILY

The past year saw major changes in the shareholdings of Noverco,the sole shareholder of Gaz Métro inc., which owns 74.7% of the unitsof Gaz Métro Limited Partnership for which it is the General Partner.Capital Infragaz s.e.c. (now Trencap s.e.c.), a newly formed limitedpartnership, became a shareholder of Noverco, joining Enbridgeand Gaz de France, whose ownership interests remain unchanged.

Through Trencap and Noverco, Gaz Métro acquired new soliddiverse investors, namely: Caisse de dépôt et placement du

Québec, SNC-Lavalin, the Fonds de solidarité FTQ, British ColumbiaInvestment Management Corporation, the Régime des rentes du

mouvement Desjardins and, just recently, the Régime de retraite

de l’Université du Québec. We would like to welcome theseorganizations to our corporate family, as well as the new membersof the Board of Directors. Furthermore, with the purchase of$10,5 million of units on October 21, 2003 by the underwriters of the successful September 30, 2003 $70,0 million unit issue, thepublic increased its interest in the Partnership to 25.3%. Theseinvestments by professional investors and the general publicspeak to the confidence investors have in our organization andprovide us with an incentive to excel.

The second phase of the advertising campaign to promoteGaz Métro’s new corporate image, which is a reflection of a newcorporate vision, was again enthusiastically received by the generalpublic. This year, the Partnership is continuing its transformationby focusing on the functional aspects of gas appliances. Thecampaign bolsters the ongoing efforts of the organization and itsbusiness partners to develop and retain its clientele.

The new corporate image is more than just an image. It reflectsprofound changes in the organization’s culture. All of our personnelhave had to adapt their approaches in order to achieve the ambi-tious objectives set in an energy context that will not stand still.

We are proud that this cultural change, which focuses on qualityand aims to ensure customers, investors and employees are satisfied,is well underway, if not already a fait accompli. The Partnershipexpresses its sincere thanks to its employees and business partnersfor their open-mindedness, efforts and accomplishments.

RESULTS

In spite of adverse factors that reduced income by $6.3 million,Partners’ income in 2004 is up by 4.6% to $160.4 million. Partnersreceived distributions of $154.3 million, i.e. $1.36 per unit. Partners’income per unit of $1.40 is up by $0.01 over the 2003 fiscal year.

The adverse factors that had to be offset in order to achieve thisgrowth are the impact of a further reduction in the corporate taxrate, which, among other things, reduces the income tax expenserecovered from Gaz Métro’s customers in Quebec, and the impactof a stronger Canadian dollar in relation to its U.S. counterpart onthe results for Vermont Gas Systems and Portland Natural GasTransmission System. Income per unit was also affected by the factthere were 3.6% more weighted average number of outstandingunits in 2004 than in 2003.

The Partnership also invested $2.8 million in a proposed LNGterminal (“Rabaska”) and, in accordance with our developmentexpense policy, charged this amount to income.

The increase in Partners’ income is attributable to a largerownership interest in PNGTS and improved profitability in theEnergy Services and Other sector. Income from the distributionactivity is virtually the same as last year. Details of the results forthese three sectors are described further on.

PERFORMANCE OF UNIT

As mentioned above, distributions totalled $1.36 per unit, an increase of $0.02 over the 2003 fiscal year. The price of the

report to partners

13G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

REPORT TO

PARTNERS

unit was up by 3.7% from $20.28 as at September 30, 2003to $21.04 as at September 30, 2004. As the return on distri-butions ($1.36/$20.28) is 6.7%, the total return on the unit was 10.4% in 2004.

For the 11 years since the initial public offering of the Partnership’sunits, the total annualized return on the unit is 14.8%.

DISTRIBUTION

The distribution of natural gas generated 85.9% of the Partners’income for its 2004 fiscal year. Income from this sector was$137.7 million for the year, i.e. $0.3 million lower than in 2003. A weaker U.S. dollar in relation to the Canadian dollar reducedincome reported for Vermont Gas Systems. In addition, as indicatedin last year’s Report, income was hit by a further reduction in thefederal corporate tax rate, which had a negative impact on Partners’income from the Quebec distribution activity, which is beforeincome taxes.

Furthermore, the base rate of return authorized by the Régie de

l’énergie was lower than the previous year. Nevertheless, a totalreturn of 11.47% was realized, compared to 11.05% in 2003, dueto the sharing of productivity gains and overearnings with customers.

Normalized volumes (for temperatures, in Quebec) sold were 5,789 million cubic metres, 1.3% more than the previous year. All of the markets contributed to this increase. Even more impor-tantly, a record 7,759 new contracts were signed in Quebec in 2004,and penetration of the new construction market continues to grow.

Gaz Métro’s customers are being well taken care of as tightly controlled costs, orderly development and higher volumes madeit possible to reduce distribution rates by an average of 3% for the2005 year. Distribution is the only service that is fully controlledby Gaz Métro.

For the 2005 fiscal year, the Régie de l’énergie approved a rate ofreturn, after deemed income taxes, of 11.64% on Partners’ equityallocated to the Quebec distribution activity. This includes an incen-tive return of 1.95% due to realized and anticipated productivitygains under a regulatory framework that has enabled customers,environmental groups and Partners to all come out winners sinceit was introduced in 2001.

TRANSPORTATION

Except for the two pipelines owned by Champion Pipe Line, awholly-owned subsidiary that supplies Gaz Métro’s system in Abitibiand Témiscamingue, Gaz Métro’s investments in the transpor-tation sector are limited to ownership interests in two pipelines inwhich TransCanada PipeLines is a co-owner. The sector contributed$22.5 million, or 14.0%, to consolidated income. The most noteworthy events in 2004 were the increase in the ownershipinterest in Portland Natural Gas Transmission System from 26.9%to 38.3% on November 17, 2003 and the restructuring of themanagement of PNGTS, with the positive impacts to be feltespecially starting in 2006.

TQM Pipeline continues to perform well and is getting readyto respond to greater demand from Gaz Métro, among others, tosupply cogeneration plants like the TransCanada Energy plantin Bécancour.

ENERGY SERVICES AND OTHER

A turnaround in this sector generated income of $2.8 million, i.e.1.7% of consolidated income, compared to a loss of $0.2 millionin 2003, primarily on account of restructuring costs. Aqua Data andAqua-Rehab Group, in which the Partnership owned 50% interestsfor a number of years, are now wholly-owned subsidiaries. Thisexplains in large part why total revenues for the sector were up by12.0% in 2004 to $68.2 million.

14 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

REPORT TO PARTNERS

CURRENT PROJECT

The proposed Rabaska LNG terminal, in which Gaz Métro isworking with strategic partners, i.e. Gaz de France and Enbridge,continues to evolve. Gaz Métro spent $2.8 million to develop thisproject in 2004. While there were a number of setbacks before theconsultation process had been completed, the Partnership and itspartners continue to evaluate the project’s feasibility. The LNGterminal, which could receive annual volumes equivalent toQuebec’s current consumption, would provide Gaz Métro andEnbridge, and their customers, with a welcome diversification oftheir gas supply. International LNG trade has an enviablereputation in terms of safety and reliability.

BUSINESS OPPORTUNITIES AND OUTLOOK

In August 2004, the Régie de l’énergie authorized the repeal ofHydro-Québec’s commercial dual energy rate as of April 2006.The Partnership plans to seize the business opportunities thatwill arise as a result of this decision and is proposing efficientnatural gas solutions to businesses that have to make the tran-sition. At the end of the 2004 fiscal year, we had already startedto take advantage of this new potential.

Hydro-Québec Distribution issued a new call for tenders for elec-tricity produced by cogeneration plants. This should provide oppor-tunities for Gaz Métro either as a distributor, a developer or both.

Following its ratification by Russia in October 2004, the KyotoProtocol will come into force next year. In this context, naturalgas is more than ever an effective environmental solution for

industries to reduce their greenhouse gas emissions (GGEs). It is worth mentioning that, in February 2004, the Government of Quebec recognized the Partnership’s performance in terms ofprocesses and results in reducing GGEs.

There was a great deal of discussion during the first half of 2004about Quebec’s energy needs and what should be done to meetthem. This discussion should continue unabated over the nextfew months with a parliamentary commission hearing on Quebec’senergy future. Gaz Métro intends to capitalize on this opportunity,which should see the formulation of a new energy policy, to pro-mote a vision of responsible sustainable energy development inwhich natural gas should assume its rightful place because of the advantages it has over other forms of energy.

At the Board of Directors meeting today, the Board announcedthat the Partnership’s quarterly income distribution has beenmaintained at $0.34 per unit.

CHANGES TO THE BOARD OF DIRECTORS

There have been a number of changes to the Board of Directorssince last year’s Report to Partners, in particular, following the changein the shareholdings of Noverco. Pierre Anctil, Ghislain Gauthier andPierre Michaud replaced Hélène de Kovachich and Yvon Lamontagne(who had in turn replaced Jacques Laurent and Thierry Vandal), andGaston LongVal. In addition, Jean Abiteboul and Mel F. Belich replacedDidier Holleaux and J. Richard Bird respectively. The Board would liketo express its appreciation for the contribution of the Directors whosemandates have ended.

ROBERT PARIZEAUChairman of the Board

ROBERT TESSIERPresident and Chief Executive Officer

Gaz Métro inc.

in its capacity as General Partner

November 18, 2004

15G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

MISSION, OBJECTIVE AND

THE PARTNERSHIP

MISSION

Gaz Métro transports and distributes natural gas in Quebec and inthe northeastern portion of North America. It also sells goods andservices ancillary to its main activity. It makes use of its know-howto pursue activities that are related or similar to its core business.

OBJECTIVE

Gaz Métro’s financial objective is to provide its Partners with a stable,predictable return, accompanied by growth in value over the years.From a business perspective, the Partnership intends to provide itscustomers with high-quality energy services at the lowest possiblecost, through policies and programs aimed at motivating its employ-ees and business partners.

THE PARTNERSHIP

Gaz Métro’s core business is the distribution of natural gas. The Partnership delivers approximately 97% of the natural gasconsumed in Quebec. Vermont Gas Systems, Inc., a wholly-ownedsubsidiary, is the sole gas distributor in Vermont.

Gaz Métro also owns significant financial interests in two natural gastransportation companies, including a 50% interest in TQM Pipelineand Company, Limited Partnership, which operates a gas pipeline thatconnects upstream with that of TransCanada PipeLines and down-stream with that of Portland Natural Gas Transmission System. Thepipeline owned by PNGTS, in which Gaz Métro holds a 38.3% interest,originates at the Quebec border and extends to the suburbs ofBoston. In addition, a wholly-owned subsidiary of the Partnershipoperates two gas pipelines that cross the Ontario border to supplyGaz Métro’s distribution system in northwestern Quebec.

In addition to these activities and major ownership interests, thePartnership sells goods and services, through subsidiaries and affiliates, in the energy related business, and in water, wastewater and fibre optics networks.

16 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

CORPORATE STRUCTURE(NOVEMBER 18, 2004)

CAISSE(General Partner)

50.99%

RÉGIMEDES RENTESDU MOUVEMENTDESJARDINS

8.33%

RÉGIME DERETRAITE DEL’UNIVERSITÉ DU QUÉBEC

1.79 %

BC INVESTMENTMANAGEMENTCORPORATION

11.11%

SNC-LAVALIN INC.

11.11%

SOLIDARITYFUND QFL

16.67%

TRENCAP S.E.C.

50.38%

GAZ DE FRANCE

17.56%

ENBRIDGE

32.06%

NOVERCO INC.

100%

GMi(General Partner)

74.7%

PUBLIC(Limited Partners)

25.3%

GMLP GMiGaz Métro inc.

GMLPGaz Métro Limited Partnership

CAISSECaisse de dépôt et placement du Québec andCapital d’Amérique CDPQ Inc. (General Partner)

BC INVESTMENT MANAGEMENT CORPORATIONTwo trust members of the group owning respectively 9.44% (bcIMC (PPSAF) Investment Trust No.1) and 1.67% (bcIMC (WCBAF-PPSAF)Investment Trust No.1) of the ownership interest

DISTRIBUTIONOF NATURAL GAS

ENERGY SERVICESGaz Métropolitain PlusCCUM Servitech

OTHER ACTIVITIESVDN Cable Aqua DataAqua-RehabTeldig

TRANSPORTATIONOF NATURAL GAS

17G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

the yearin review

RECORD NEW SALES BREAKTHROUGH IN QUEBEC CITY AWARDS FOR “LIFE IN BLUE” CAMPAIGN OPENING OF NEW BUSINESS

OFFICES CONTINUES OPERATION SHIELD MEETINGS –A SUCCESS TO BE REPEATED FIXED-PRICE GAS FOR COMMERCIAL

AND INSTITUTIONAL CUSTOMERS GAZ MÉTRO –FINALIST IN THE COMMERCE KORN/FERRY CONTEST INFRASTRUCTURE

REHABILITATION –A PROMISING FUTURE FIBRE OPTICS –RACING AHEAD!

18 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

THE YEAR IN REVIEW

BREAKTHROUGH IN QUEBEC CITY

Gaz Métro made a significant breakthrough in the residential market in Quebec City.Until quite recently, it connected no more than 30 new houses a year; however, by theend of 2004, 205 new homes will be supplied with natural gas, exceeding the objectiveset. Natural gas is now available in 14 residential subdivisions as well as in apartmentbuildings in Quebec City. In addition, most of the new condos in the region are nowequipped with natural gas fireplaces and other appliances. This breakthrough augurswell for the future in this developing market.

OPERATION SHIELD MEETINGS – A SUCCESS TO BE REPEATED

Operation Shield is a major initiative aimed at retaining commercial and industrialcustomers who consume 75,000 m3 or more of natural gas per year. To get closer tothese customers, 14 meetings were organized in five regions and involved discussionswith almost 400 people from more than 265 companies about trends in energy, hownatural gas prices are set, and energy efficiency. Gaz Métro specialists were able tospot business opportunities as well as promote high energy-efficient equipment.

GEOMARKETING SYSTEM – TO BETTER TARGET THE MARKET

To better focus its sales efforts, Gaz Métro introduced an efficient geomarketingsystem that helps it track the evolution of activities in geographic, demographic andsocioeconomic terms, as well as access to needed information in a timely fashion. Thisinnovative solution helps target potential business customers in order to develop appro-priate commercial strategies and better plan the extension of its distribution system.

ZOOM CLIENT – A CONTINUING SUCCESS

For the third year, the Zoom Client program has enabled Gaz Métro to increase its contactswith small and medium-sized commercial and industrial customers. Most of the partici-pants received a “health bulletin” to help them compare their energy consumption withother businesses in the same field of activity. More than 200 had their installationsinspected by a technician, who made recommendations on energy efficiency. Membersof the Zoom Client program were also invited to three information sessions this yearwhere they were able to talk about energy with various specialists in the field.

Last year, the Energy Planning Network in the United States awarded Gaz Métro its“Best CRM Solutions for C&I” award for its Zoom Client program.

TRANSCANADA ENERGY : GAZ METRO’S LARGEST CUSTOMER EVER

The environmental assessment process for the proposed construction of a natural gaspipeline to supply the TransCanada Energy cogeneration plant at Bécancour has beensuccessfully completed. This included two series of consultations with the Bureau

d’audiences publiques sur l’environnement (BAPE). Gaz Métro was able to satisfactorily

7,759NEW CUSTOMERS

RECORD NEW SALES

7,759 businesses and homeowners chose

Gaz Métro in 2004, beating the previous

year’s record for the number of new customers

and volumes. The residential sector posted

exceptional results, with agreements to

connect 981 existing homes (782 in 2003),

and 4,362 newly built houses (3,467 a year

earlier), to the natural gas system.

19G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

THE YEAR IN REVIEW

respond to questions from the public about the environment and public safety sincethe BAPE report, made public in September 2004, concluded that the project wasjustified. With an expected cost in the order of $54 million, the pipeline, which will passunder the river to link the two shores of the St. Lawrence, will be one of the largestsystem extensions in the history of Gaz Métro. The cogeneration plant will have a capacity of 507 MW and consume 926 cubic metres (33 Bcf ) of natural gas. Thisrepresents approximately one third of the present volumes delivered to the Quebecindustrial market.

LIFE – AFTER BLUE!

In 2003, Gaz Métro began to change its image by shortening its name, adopting a newlogo and creating a new signature. An advertising campaign aimed at the generalpublic marked the transformation. The small flames and “life in blue” quickly went onto become the recognized trademark of Gaz Métro.

The campaign results surpassed all expectations–surveys show that it exceeded allindustry standards for brand awareness, appreciation, comprehension and attribution.

Last year, the focus was on the word BLUE from “life in blue” to really imprint the newimage in the mind of the public. This year, the advertising campaign focused on LIFE, by explaining the product and its advantages in everyday life. The small blue flames,brighter than ever, are at work in environments that demonstrate natural gasapplications. This second year speaks more to potential customers about the product,its applications and advantages.

NEW COLLECTIVE AGREEMENT FOR SALES REPRESENTATIVES

Gaz Métro signed a new collective agreement with its 46 Sales Representatives,affiliated with the Fédération des travailleurs et travailleuses du Québec. This groupof employees will now benefit from an improved incentive package when salesobjectives are surpassed. The renewed agreement also includes a well-definedcustomer retention plan which will help strengthen ties to customers and build loyalty.

ENHANCED PARTNERING ARRANGEMENT WITH PLUMBING AND HEATING CONTRACTORS

Gaz Métro has restructured the partnering arrangement that was introduced in the early1990s with about 250 plumbing and heating companies. The program, whichencourages contractors to sign up a certain number of installations of natural gasequipment and to respect Quebec Building Code standards, is now based on a sharedsales structure. Five Sales Representatives have thus been assigned to oversee, coachand motivate contractors with the goal of promoting greater use of natural gas. Contractorscan now also benefit from a designated territory. This business approach hasadvantages for everyone–contractors, Gaz Métro and customers alike.

AWARDS FOR “LIFE IN BLUE” CAMPAIGN

INFOPRESSE MEDIA AWARDS

Two awards for media strategies, including

the Media Grand Prize of the Year.

GRAFIKA AWARD FOR GRAPHIC DESIGN

Two awards for graphic design

PUBLICITÉ-CLUB DE MONTRÉAL –

CREATIVE ADVERTISING CONTEST

Coq de bronze – Direct marketing,

consumer acquisition category

Four people who worked on the campaign

were honoured.

20 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

THE YEAR IN REVIEW

TEGA PROJECT – NEW TECHNOLOGY TAKES MARKET BY STORM

Gaz Métro struck a good deal when it collaborated with TEGA to develop new natural gas duct heaters for the industrial, commercial and institutional sectors. This partnership, which includes the Natural Gas Technologies Center–Gaz Métro is oneof the Center’s sponsors–developed a patented device that adapts to all sizes of existingair ducts and improves energy efficiency. The new duct heaters were a commercial andtechnical success right from day one.

SUCCESSION PLANNING – PREPARING FOR THE FUTURE

Gaz Métro has set up a succession program to fill management positions in theOperations sector, where about 60% of all employees work. Under this ongoingprogram, employees can follow a personalized development plan that opens the doorto an eventual career in management. The program’s integrated approach links acandidate’s potential in terms of abilities, development of managerial skills, as wellas operating knowledge and abilities, with Gaz Métro’s future needs.

OPENING OF NEW BUSINESS OFFICES CONTINUES

The construction boom in the Laurentians, along with Gaz Métro’s marketing initiatives,have led to a growth in demand for natural gas, with the result that approximately 50 employees in this regional business office have now moved into new, more suitablepremises to better serve their growing clientele.

The Quebec City business office and the Eastern Quebec regional division office alsohave a new address. The new building in the Quebec City industrial park now housesabout 50 employees. Besides space for Administration and Sales, the building also has a showroom for natural gas technologies and a very modern videocon-ference room, which one user in particular, the École de technologie gazière, will usefor training students in the region. Gaz Métro manages this training center, which is basedin Boucherville.

SATISFYING CUSTOMERS

Gaz Métro very much wants to satisfy its customers and the community at large.However, just like any other enterprise, it makes occasional mistakes and so itsometimes receives complaints and comments. To handle them better, it has introduceda customer satisfaction management policy, along with an information system that centralizes the management of problem cases and instantly transmits the variouscommunications to the appropriate person in the organization. This has helped reduce handling time by more than 60%. The new procedure also permits a moredetailed analysis of complaints and comments received in less time and, to the extentpossible, to take the necessary steps to correct the cause of the dissatisfaction.

INNOVATIVE TOOL LENDS A HAND

Gaz Métro has increased its efficiency by

automating how it manages the inspection

of new installations of gas equipment.

The Partnership has designed a computerized

tool, the size of a hand-held computer, which

eliminates paper forms. The Mobilité project

has several other advantages: work orders

are now sent to technicians over cellular

bandwidth, data collection is faster, and

the data are transmitted directly to the SAP

information system, considerably reducing

the risk of errors. The device also speeds

up communication with the installer and

follow up if an installation is non-compliant.

The small device has made a big difference in

improving efficiency and customer satisfaction.

21G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

THE YEAR IN REVIEW

IMPROVED PROCESSES

With the growing number of residential and commercial customers, the Groupe

d’amélioration des processus et des pratiques d’affaires (GAPP) turned its attentionto simplifying and streamlining the steps between signing a contract and billing a newcustomer. GAPP also modified certain business practices, for example, by modifyingthe procedure for collecting overdue accounts during the winter. Now, besides writingletters, we communicate in person or by telephone with residential customers to agree,if possible, on ways of paying the amount owing. More businesslike and more flexible,this approach has also turned out to be advantageous for customers and Gaz Métro.

PUBLIC INFORMATION SESSION ON MAJOR INDUSTRIAL RISKS –

A NEW WAY OF PLANNING INDUSTRIAL DEVELOPMENT ON THE TERRITORY

In February 2004, Gaz Métro took part in a public information day organized by theComité mixte municipal industriel (CMMI) in Montreal East. The objective was toinform the residents of this district about the risks presented by the industriesconcentrated there and the measures to be taken to mitigate their risks in the eventof a serious incident. Gaz Métro prepared a leaflet for the occasion on the LNG Plant,where natural gas is stored in liquefied form to meet peak-period demand. The morethan 500 people who attended greatly appreciated this communication operation, a first in Quebec. Gaz Métro’s participation attests to the company’s responsible andtransparent management and its willingness to work together with the community.

VERMONT GAS SYSTEMS

Vermont Gas Systems connected 1,373 new customers to its system in 2004, hittinga new five-year peak. Compared with the previous fiscal year, new sales in terms ofanticipated volumes increased by 38%, including a 126% increase in the commercialmarket. To serve its customers better, Vermont Gas added 4 km to its distributionsystem and 53 km to its main gas lines.

Vermont Gas energy efficiency programs were recognized by two national organi-zations: the American Council for an Energy–Efficient Economy and Energy Star Homes.

FOR SMALL BUSINESS OWNERS – A SIMPLE AND QUICK FINANCING PROGRAM

In partnership with Scotiabank, Gaz Métro has introduced a new financing programfor small business owners. With its very competitive rates and simplified applicationprocess, the program facilitates the purchase of new natural gas equipment. Thecustomer just has to complete a one-page form and submit it to Scotiabank, along withan estimate from an installer. The bank’s response is given within 48 hours followingreceipt of the application.

INNOVATIVE PROGRAM TO STABILIZE SYSTEM GAS COSTS

Gaz Métro’s financial derivatives program, approved by the Régie de l’énergie, has notonly reduced fluctuations in natural gas prices by more than 60%, it also reducedthe cost of system gas supply by 1.2%. When prices were climbing and customers couldhave expected a higher bill, instead they saw a reduction that represents about$7 million. The kind of “insurance policy” the organization has put in place is one ofthe most avant-garde of all financial derivatives programs to be found among naturalgas utilities in North America.

FIXED-PRICE GAS FOR COMMERCIAL

AND INSTITUTIONAL CUSTOMERS

On October 1, 2003, with the approval of

the Régie de l’énergie, Gaz Métro launched

a new fixed-price gas service for small

businesses and institutions, i.e., customers

who consume between 7,500 m3 and

1,168,000 m3 of natural gas per year.

Since then, suppliers and brokers have

shown increased interest in this new supply

program and a growing number of customers

have opted for the service.

22 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

THE YEAR IN REVIEW

LEAP FORWARD IN QUALITY

Gaz Métro exceeded the objective it had set itself before the external audit thatassessed its quality performance in September 2004. In 2001, it obtained 379 pointson the Qualimètre–the diagnostic tool developed by the Mouvement québécois de la

qualité. This year, Gaz Métro was awarded 534 points! According to the auditor, thisis an exceptional result in both progress and score achieved. The auditor also remarkedon the cooperation received from all the employees–more than 300 from all levels ofthe organization–who took part in the very rigorous evaluation process.

RESCHEDULING WORKING HOURS – AN IDEA WHOSE TIME HAS COME

After the introduction of a four-day workweek for unionized employees, the Partnershipdecided to look at the work schedule for managers and specialized personnel. Theseemployees have been offered a proposal that includes formulae and criteria to help themachieve a better work-family balance, so long as the needs of the organization are met.

VERSATILITY PROGRAM A HIT

The versatility program, which stemmed from the introduction of a shorter workweekfor Gaz Métro’s blue-collar employees, led about 200 of them to the doors of theÉcole de technologie gazière in the past year for training to develop their multi-skillknowledge. Versatility is essential to the smooth running of the new work schedule,which came into effect in January 2004, and all the Operations’ technicians are now multi-skilled.

A CULTURE OF HEALTH AND SAFETY IN THE WORKPLACE

In order to instill a genuine culture of prevention, Gaz Métro has drawn up an actionplan that will lead to establishing a new policy on workplace health and safety. By getting not only the Joint Committees but all personnel involved in the plan, Gaz Métro is clearly demonstrating that it wants prevention to be a daily concernthroughout the organization.

GAZ MÉTRO – FINALIST IN THE COMMERCE KORN/FERRY CONTEST

In January 2004, Gaz Métro was among the four finalists in the Grandes entreprises

category for the Commerce Korn/Ferry Grand Prize in the second edition of this contestthat recognizes excellence in corporate governance. Gaz Métro was in competition with National Bank, Industrial Alliance and SNC-Lavalin. In the end, SNC-Lavalin tookfirst prize.

The contest criteria include: having a head office in Quebec, being listed on the stockexchange for five years or more, and posting annual performance above the TSX index.

MEASURING BUSINESS SKILLS

To ensure the development of a business

culture, Gaz Métro has introduced a new

performance-appraisal process for its

approximately 400 managers and specialized

personnel. The process evaluates individual

performance by measuring five skills:

collaboration, rigour, business sense,

flexibility and action-orientation.

23G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

THE YEAR IN REVIEW

SUBSIDIARIES OF ENERGY SERVICES AND OTHER SECTOR PERFORMED WELL

Net income from Energy Servicesand Other Sector is $2.8 million in 2004, compared to a net loss of $0.2 million in 2003.

FLEXIBILITY AND QUALITY OF SERVICE – KEY FACTORS IN BUILDING LOYALTY

In the energy services area, GMP has renewed several large contracts, including onewith the Office municipal de l’habitation de Montréal (OMHM). Over the next three years, GMP will continue to take care of boiler room maintenance in 400 buildingsthat house more than 10,000 apartments. This renewal is evidence of OMHM’ssatisfaction with the only company in Quebec that can offer 24/7 service, for which80 hours a week are at regular rates.

GMP sold the assets of Option Gaz, a subsidiary that specialized in equipment distri-bution, in order to concentrate on the maintenance and servicing of heating equipment.

INFRASTRUCTURE REHABILITATION – A PROMISING FUTURE

Requiring no street or sidewalk excavation, the interior structural casing procedure isa novel solution that helps prolong the useful life of water and wastewater pipes by40 years at a cost that is as much as 50% less than traditional replacement techniques.The procedure also minimizes inconvenience for traffic, since no trenches are required,and so helps eliminate the social costs of conventional infrastructure-replacementwork. The future looks promising, especially given the infrastructure work municipal-ities will be undertaking in the next few years.

75SCHOOLS

FIBRE OPTICS – RACING AHEAD!

VDN Cable has the wind in its sails.

Revenues were up in 2004, positively

affecting the company’s bottom line. The

subsidiary recently won a call for tender

by the Pointe-de-l’Île school board to link

75 schools through its high-speed bandwidth

service. The Grande Bibliothèque de Montréal

will also be connected to this metropolitan

network. With the convergence of telecom-

munications and IT, it’s full speed ahead

in the fibre optics sector!

24 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

social and environmentalreport

EVEN MORE COMMITTED

At Gaz Métro, achieving excellence also means improving the quality of life of the community

and safeguarding the environment. Every day, the men and women who work for Gaz Métro take

concrete steps to assure the future for tomorrow’s generation. By choosing business practices

inspired by sustainable development, supporting almost 300 non-profit organizations every year,

and by showing leadership on environmental matters, the Partnership and its employees are

keeping this promise to our children.

25G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

SOCIAL AND ENVIRONMENTAL

REPORT

LENDING A HELPING HAND TO PROMISING ARTISTS

Gaz Métro is helping up-and-coming artists by contributing to the successof a few selected events. For the last five years, Gaz Métro has been apartner of the Festiblues international de Montréal and in 2004 supportedthe Relève en blues concert for the third consecutive year. About 100,000people saw the Festiblues, a musical festival with considerable social andcommunity benefits.

FIRE DANCING ON WATER

Gaz Métro was involved in the development of Place Jean-Paul-Riopelle,inaugurated in June 2004 in Montreal’s International District. The focalpoint of this magnificent public square is La Joute, a sculpture-fountainby the celebrated artist. Surrounded by a circle of natural gas flamesdancing on a pool of water, the installation fulfills the wishes of Riopelle.Gaz Métro contributed to several facets of the project, including the designof the development by the Natural Gas Technologies Center, the realizationof the project, and the creation of a fund to ensure the integrity of the work.

LIFE IN BLUE–SYMBOL OF SUSTAINABLE DEVELOPMENT

“Life in blue,” the new corporate signature, calls to mind the Blue Planetby promoting natural gas as a source of energy that fosters environmentalprotection. This stance is in line with the Policy Statement by the Montreal

Community regarding Sustainable Development that Gaz Métro signed,along with the Ville de Montréal and 70 other signatories. This actionplan is aimed at consolidating achievements, changing old habits andrevising practices from a sustainable development perspective throughoutthe Ville de Montréal territory.

HELPING PEOPLE WHO HELP PEOPLE

This year, Gaz Métro and its employees contributed some $180,000to the annual Centraide campaign.

OVERVIEW

The Partnership has operations in nine regions of Quebec and redistributes

a portion of its revenues in grants to organizations in the territory served by

its system. In line with the policy that governs the selection and management

of its contributions, the Partnership concentrates its philanthropic efforts in the

following areas: health, education (university level), culture and socio-community

development. In 2004, the Partnership contributed more than $1,200,000 to

these causes.

Gaz Métro is also committed to demonstrating leadership, rigour and

determination in pursuing its environmental activities, both as a natural gas

distributor and with its customers. The ISO 14001 certificate it has held since

October 2000 was re-registered in 2004, reflecting the quality of the work of

its personnel and Gaz Métro’s determination to continue to improve its ways

of doing business in order to meet the “green challenge” every single day.

26 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

SOCIAL AND ENVIRONMENTAL REPORT

HIGH VISIBILITY IN THE COMMUNITY

For several years now, Gaz Métro and its employees have joinedtogether to play fairy godmother to children in a primary school nearits head office. A visit from Santa and his helpers with gifts for theyoungest, career days for the oldest, and timely help for all, areexamples of how this initiative works. A volunteer committee of about a dozen employees maintains a liaison between the schooland Gaz Métro.

The benefit evening on behalf of Projet 80 helped raise $19,000. Themoney goes exclusively toward reducing school dropouts amongyouth in the Hochelaga-Maisonneuve district.

Gaz Métro and its employees contributed $45,000 toward Christmasbaskets for families who live near its head office.

The Partnership has been supporting the Petit cirque Gaz Métro since2000. This is a community project for kids aged 5-12 in the Hochelaga-Maisonneuve district, with activities related to the fascinating worldof the circus and theatre.

FOCUS ON CHILDREN

Future generations are central to the concerns of the Partnership, andseveral activities are aimed at improving the health and well-being of our children.

Employees participated in ski competitions in support of children:the Grand Prix 24h de Tremblant for the Fondation Charles-Bruneauand the Telus Mobility Ski Challenge for the Ronald McDonaldChildren’s Charities.

Gaz Métro is also involved with Sun Youth and with the FondationMaurice-Tanguay in the draw for Sun Youth and Expo Québec homesfor the benefit of sick and handicapped children.

About 15 employees mounted a giant bike in the “Pedal for Kids”event for the Montreal Children’s Hospital.

Gaz Métro is a member of the donors circle for the Hôpital Sainte-Justine’shuge fundraising campaign.

SUPPORTING EDUCATION

Gaz Métro plays an active part in the university community practically everywhere in Quebec; in particular, it contributes to the Réseau des universités

du Québec foundations, as well as to specialized and higher learning institutions.

27G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

SOCIAL AND ENVIRONMENTAL

REPORT

RECONCILING THE ENVIRONMENT, PROFITABILITY AND SOCIAL

CONCERNS–THE RESULTS SPEAK FOR THEMSELVES

The agreement on the regulatory framework setting rates has enabledGaz Métro and its customers to benefit from the productivity gainsachieved. The results speak for themselves: as of October 1, 2004,customers saw a 3% reduction in distribution rates, and a better rate ofreturn was authorized for Gaz Métro as a result of sharing these produc-tivity gains.

Gaz Métro functions within a regulatory framework that is unique inCanada, the result of a unanimous agreement with representatives of its customers and environmental groups. The agreement negotiated in 2003 and approved by the Régie de l’énergie will be in effect for five years from October 1, 2004, replacing the agreement in effect sinceOctober 1, 2000. It reconciles respect for the environment with the socialand economic interests of customers and Partners. For example, theagreement stipulates that the productivity gains achieved will be used,in certain proportions, to reduce natural gas rates, finance the EnergyEfficiency Fund and improve the rate of return for the Partners.

The Energy Efficiency Fund, managed by a committee made up of represen-tatives of customers and environmental groups, will give priority to projectswith low-income residential customers or with a social or communityobjective. The fact that the agreement was accepted by all interested partiesand approved by the Régie is also a reflection of the quality of the relationsthat prevail between Gaz Métro and its business Partners.

PRESERVING OUR NATURAL ENVIRONMENT

About 30 employees climbed Mount Royal on snowshoes for the “Climbof the blue tuques.” The event raised $200,000 to help protect themountain that sits squarely in the middle of Montreal. Other employeesparticipated in Les îles à la rame on Lac Saint-Pierre, a UNESCO WorldBiosphere Reserve.

MARKING ENVIRONMENT WEEK TOGETHER

Gaz Métro employees enthusiastically participated in Environment Weekfor a third year. Program activities included: Opération vélo-boulot,encouraging people to bike to work, Les bons coups des employésexhibit, highlighting initiatives taken to protect the environment, and a tasting of organic products.

ÉCOGESTE AWARD FOR EFFORTS THAT BENEFIT THE ENVIRONMENT

On November 13, 2003, Gaz Métro received a special award from the jury for the Québec ÉcoGESte program. The recognition honours anorganization that stands out for its dynamism and success in its field ofactivity. The jury selected Gaz Métro for the changes made to its systemand its operations, which have considerably reduced its greenhousegas emissions, and also for its energy-efficiency programs aimed at its customers.

28 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

SOCIAL AND ENVIRONMENTAL REPORT

DEVELOPING BIOGAS OPENS UP NEW AVENUES

Intersan has developed a process to capture the gas produced by thebiological decomposition of non-recyclable waste at its landfill site inSainte-Sophie. Gaz Métro ships this gas via a 13-kilometer pipeline tothe Cascades fine paper plant in Saint-Jérôme. This innovative initiative,approved by the Régie de l’énergie, will meet a large part of Cascades’energy needs for the next 10 years. The decomposition of waste in anairless environment generates biogas, which is high in methane, theprincipal component of natural gas. The development of biogas hasattractive commercial potential, as well as being an important steptoward sustainable development. With unique expertise in this field inQuebec, Gaz Métro is actively working on other projects of this kind thatopen up new avenues for energy and the environment.

ENERGY EFFICIENCY–REDUCTIONS EQUAL TO CONSUMPTION

BY 7,000 HOMES

Gaz Métro’s Energy Efficiency Plan has enabled its customers to achievesavings of 20,435,328 m3 of natural gas and to reduce their emissionsby about 37,000 tonnes of carbon dioxide, which is more than what7,000 single-family homes would have consumed or produced.

Energy efficiency has been part of the corporate culture at Gaz Métro formany years. In 1999, it tabled its first Energy Efficiency Plan with the Régie

de l’énergie. The Plan includes a total of 15 programs for residentialand business markets, including large companies.

RECOGNITION FOR GAZ MÉTRO’S ENERGY EFFICIENCY PLAN

Two residential programs under Gaz Métro’s Energy Efficiency Plan (EEP) won a Best Practice Award from the American Council for an Energy-EfficientEconomy. This recognition honours the best energy-efficiency program offered by North American natural gas distributors. Gaz Métro is the onlydistributor in Canada to have won this prize to date.

Gaz Métro was also a Natural Resources Canada 2004 ENERGY STAR Market Transformation Award Winner for raising its standards for the certification of residential appliances eligible for its EEP programs.

29G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

management’sdiscussionand analysisManagement’s Discussion & Analysis (“MD&A”) should be read in conjunction with theconsolidated financial statements of Gaz Métro Limited Partnership (“Gaz Métro” or the“Partnership”) included in the 2004 Annual Report. Those consolidated financial statementshave been prepared in accordance with Canadian generally accepted accounting principles.All amounts in that Report are in millions of Canadian dollars, unless otherwise indicated.

FORWARD-LOOKING STATEMENTS

To enable investors to better understand the Partnership’s outlook for the future and make more informed investment decisions, the matters discussed

herein may contain forward-looking information about Gaz Métro’s objectives, strategies, financial condition, operating results and activities. Such infor-

mation expresses, as of the date hereof, the estimates, forecasts, projections, expectations or opinions of the Partnership concerning future events or

results. Actual results may differ materially from the results anticipated herein and, consequently, we cannot guarantee that any forward-looking state-

ment will materialize. Forward-looking information does not take account of the impact transactions or non-recurring matters announced or arising after

the statements have been made might have on the Partnership’s results.

The risks and uncertainties that could cause actual results and future events to differ materially from current expectations are described herein,

in particular under Risks.

Gaz Métro does not propose nor does it commit to update forward-looking information, even if new information becomes available as a result of future

events, or for any other reason.

30 mission, objectives and activities

31 performance summary

33 financial results analysis

35 liquidity and capital structure

39 risks

40 recent accounting changes

40 additional information

30 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

MISSION, OBJECTIVES AND ACTIVITIESMISSION

Gaz Métro transports and distributes natural gas in Quebec and the northeastern portion of the continent. It also sells goods and servicesancillary to its main activity. It makes use of its know-how to pursue activities that are related or similar to its core business.

OBJECTIVES

Gaz Métro’s financial objective is to provide its Partners with a stable predictable return accompanied by growth in value over the years.From a business perspective, the Partnership intends to provide its customers with high-quality energy services at the lowest possiblecost, through policies and programs aimed at motivating its employees and business partners.

DISTRIBUTION

Gaz Métro’s core business is the distribution of natural gas. The Partnership delivers approximately 97% of the natural gas consumed in Quebec while Vermont Gas Systems (“VGS”), a wholly-owned subsidiary, is the sole gas distributor in Vermont.

The Quebec distribution activities are regulated by the Régie de l’énergie (“Régie”), which sets distribution rates and supervises andmonitors operating activities and development of the gas system. VGS is regulated by the Vermont Public Service Board in the United States.

In the Partnership’s view, the combined effect of its marketing efforts, higher electricity and fuel oil prices, and the increased acceptanceof “the right energy in the right place” concept should generate larger market shares for natural gas in years to come. In addition, the construction of certain gas-fired power plants, in particular cogeneration plants, should increase deliveries and therefore have a positive impact on future results.

TRANSPORTATION

Gaz Métro owns significant financial interests in two natural gas transportation enterprises. The first is a 50% interest in TQM Pipelineand Company, Limited Partnership (“TQM”), which operates a gas pipeline in Quebec that connects upstream with that of TransCanadaPipeLines and downstream with those of Portland Natural Gas Transmission System (“PNGTS”) and Gaz Métro. The pipeline owned byPNGTS, in which Gaz Métro owns a 38.3% interest, originates at the Quebec border and extends to the suburbs of Boston. In addition,a wholly-owned subsidiary of the Partnership operates two gas pipelines that cross the Ontario border to supply Gaz Métro’s distributionsystem in northwestern Quebec. In Canada, transportation activities are regulated by the National Energy Board (“NEB”). In the UnitedStates they are regulated by the Federal Energy Regulatory Commission (“FERC”).

No major investments have been made in the TQM and PNGTS systems for a few years. This erodes the rate base used to calculate theauthorized return, which in turn reduces earnings. TQM and PNGTS have therefore to remain on the lookout for potential additionalinvestments in these two systems, and, particularly in the case of PNGTS, to control operating costs in order to maximize income.

In 2004, PNGTS undertook a major rationalization of its operating costs which should have a positive impact on results starting in 2006.

ENERGY SERVICES AND OTHER

The Partnership sells goods and services, through subsidiaries, joint ventures and companies subject to significant influence, in the energybusiness and in water, wastewater and fibre optics networks.

The past two years have seen a refocusing of activities, downsizing of operations and restructuring of management. The energy-relatedactivities are now focused on the maintenance and repair of residential, commercial and industrial equipment, and on the heating andcooling of large buildings in the vicinity of the Climatisation et Chauffage Urbain de Montréal plant.

Growth of the water and wastewater activities will likely accelerate in the future as integrated water distribution and wastewater collectionsystems master plans become mandatory in Quebec. At the same time, Aqua Data Inc., a wholly-owned subsidiary of Gaz Métro, is makingan effort to penetrate the U.S. market through a joint venture with a large U.S. environmental engineering firm.

MANAGEMENT’S DISCUSSION AND ANALYSIS

31G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

The investment in shares and convertible debentures of Cable VDN is performing as expected. Cable VDN’s higher sales, combined withtight control over operating costs, should allow it to become profitable starting in 2005.

DEVELOPMENT PROJECTS AND POTENTIAL ACQUISITIONS

In 2004, the Partnership and its partners, Enbridge Inc. (“Enbridge”) and Gaz de France, devoted considerable time and effort to an LNG terminal project called Rabaska. In light of the anticipated evolution of gas production in North America, the project’s partners believethat Lévis on the St. Lawrence River is an excellent port of entry for natural gas from overseas. As distributors, Enbridge and Gaz Métrowould get part of their supply from Rabaska.

However, local municipal authorities have opposed the project from the start of consultations, which were conducted in accordance withthe process established by the NEB. Other local and regional stakeholders have since expressed interest in pursuing the review of theproject. Rabaska’s developers are therefore now considering the alternatives available to them under the circumstances.

In terms of potential acquisitions, Gaz Métro is keeping its eyes open for opportunities that are in line with the Partnership’s missionand that would immediately create value so as not to have to reduce Partner distributions.

PERFORMANCE INDICATORS

Gaz Métro’s core business is the distribution of natural gas in Quebec, with its some 1,300 employees and all of the challenges that involves.In the pursuit of excellence with its suppliers and business partners, the Partnership developed indicators for measuring the organization’sperformance in relation to objectives set at the beginning of the year.

The indicators include:profitability;customer satisfaction;sales growth and new customers;budget versus actual;work atmosphere and performance;occupational health and safety;etc.

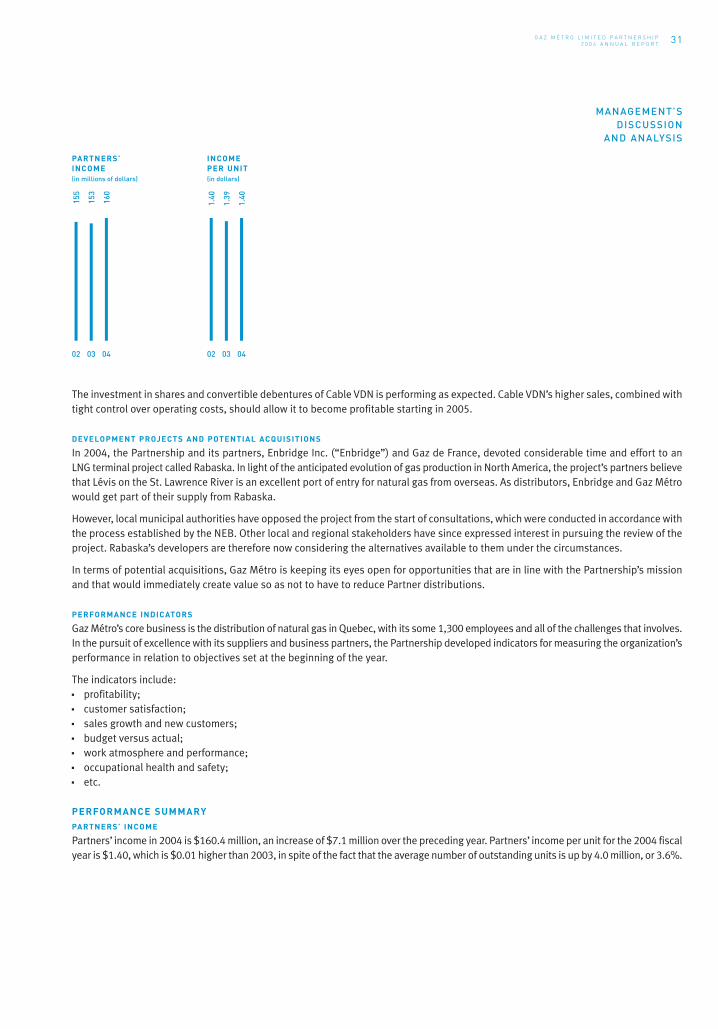

PERFORMANCE SUMMARYPARTNERS’ INCOME

Partners’ income in 2004 is $160.4 million, an increase of $7.1 million over the preceding year. Partners’ income per unit for the 2004 fiscalyear is $1.40, which is $0.01 higher than 2003, in spite of the fact that the average number of outstanding units is up by 4.0 million, or 3.6%.

MANAGEMENT’S DISCUSSION

AND ANALYSIS

155

02

PARTNERS’ INCOME(in millions of dollars)

153

03

160

04

INCOME PER UNIT(in dollars)

1.40

02

1.39

03

1.40

04

32 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

This growth can be explained primarily by additional income from the Partnership’s investment in PNGTS, following the increase of itsownership interest from 20.7% to 26.9% on September 30, 2003, and to 38.3% on November 17, 2003, as well as improved profitabilityof the Energy Services and Other Sector in 2004.

Partners’ income is up in spite of the negative impacts of:the 2% reduction in the federal tax rate applicable to the calculation of the Partnership’s deemed income tax cost included in its Quebecdistribution rates (negative impact of approximately $4.1 million);a stronger Canadian dollar in relation to the U.S. dollar (negative impact of $2.2 million); anddevelopment costs of $2.8 million on the Rabaska project.

REVENUES AND GROSS MARGIN

Consolidated revenues for the year ended September 30, 2004 are up by $26.4 million, or 1.5%, to $1,782.9 million compared to$1,756.5 million the preceding year. This increase can be explained primarily by an increase in the average selling price of natural gasand higher transportation, load-balancing and distribution rates. In Quebec, natural gas supply, transportation and load-balancing servicesare billed to customers at their cost to the Partnership and, therefore, have no impact on gross margin or Partners’ income.

Normalized deliveries (for temperatures in Quebec) during the 2004 year are 5,789 million cubic metres of natural gas, an increase of1.3% over 2003. All of the markets contributed to the increase.

Consolidated gross margin is down by 2.4%, or $13.9 million, from the preceding year to $555.0 million. The decrease is mainlyattributable to the fact that the Partnership’s share of PNGTS’ gross margin has not been recorded since November 17, 2003, as a resultof the change in the method of accounting for Gaz Métro’s investment in this enterprise. If the new method had been adopted at the samedate the previous year, gross margin for 2003 would have been $16.5 million lower and gross margin for 2004 would therefore have been$2.6 million higher than the previous year.

LIQUIDITY

Cash flows from operating activities, before changes in non-cash working capital items in 2004, are down $5.6 million to $350.7 million,compared to $356.3 million the preceding year.

The debt/invested capital ratio is 58.3% as at September 30, 2004, compared to 60.1% at the same date the previous year. The decreasecan be explained primarily by a lower debt load attributable to the fact that, as the Partnership has not had joint control of PNGTS since November 17, 2003, it no longer records its share of the items in PNGTS’ balance sheet. This change in accounting methodremoved long-term debt of $97.8 million from Gaz Métro’s balance sheet.

MANAGEMENT’S DISCUSSION AND ANALYSIS

1,60

8

02

1,75

7

03

1,78

3

04

NORMALIZED VOLUMES (millions of cubic metres)

5,92

1

025,

717

035,

789

04

GROSS MARGIN(in millions of dollars)

556

02

569

03

555

04

TOTALASSETS(in millions of dollars)

2,33

7

02

2,43

1

03

2,36

1

04

REVENUES(in millions of dollars)

33G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

OTHER HIGHLIGHTS

On June 30, 2004, there were changes in the shareholdings of Noverco Inc., the sole shareholder of GMi (parent company of Gaz Métro).Capital Infragaz s.e.c. (now Trencap s.e.c.) acquired the shares owned by Hydro-Québec, National Bank Financial and the Caisse de dépôt et placement du Québec. These shares represented 50.38% of the total issued shares. The interests of Enbridge and Gaz de Franceremained the same.

A noteworthy event in 2004 was the renewal until 2009 of the performance incentive mechanism whereby productivity gains generatedby the Quebec distribution activity are shared by the Partnership and its customers. Introduced in 2001, following an agreement withthe intervenors before the Régie and ratified by it, this regulatory framework is considered a model by the industry. This incentivemechanism provides an effective stimulus for penetrating new markets and increasing profitability through the sharing of productivitygains by the Partnership and its customers.

A total of 7,759 new customers chose Gaz Métro in 2004, a record. The penetration rate in the new residential construction sector hasbeen growing steadily for the past few years and, with 14.7% new dwellings in the Montreal area, 2004 was no exception. A major invest-ment in an advertising campaign promoting a new corporate image was no doubt partially responsible for this success.

In spite of the pressures the significant number of new customers placed on the organization in 2004, the new customer satisfactionrate of 91% this year is in line with previous years.

The results of the organizational performance survey based on an external audit in 2004 show that the Partnership is making substantialprogress in its pursuit of excellence, an initiative that involves employees and their unions. The impact is being felt of the investmentsmade in work organization, management, training and the enterprise resource planning (ERP) system.

FINANCIAL RESULTS ANALYSISDISTRIBUTION SECTOR

The Partnership benefits from a revenue normalization mechanism that is a function of normal temperatures for the distribution of naturalgas in Quebec. Gaz Métro normalizes deliveries (for temperatures) and reflects the adjustment in its revenues through rate stabilizationaccounts. During the 2003 and 2004 fiscal years, temperatures were colder than normal, which resulted in changes of $11.7 million in2003 and $2.3 million in 2004 in the stabilization accounts in Quebec. The regulatory mechanism provides that the Partnership will adjustits annual rates to return these amounts to customers over a period of five years, starting in the second subsequent year.

As already explained, because the Partnership’s revenues reflect its cost of purchasing the natural gas sold by the Distribution Sector, thishas no impact on Gaz Métro’s results in Quebec and analyzing revenues does not provide a clear picture of the evolution of the Sector’s activities.

MANAGEMENT’S DISCUSSION

AND ANALYSISLONG-TERMDEBT(in millions of dollars)

1,24

1

02

1,28

9

03

1,20

9

04

DISTRIBUTIONS PAID PER UNIT(in dollars)

1.28

02

1.34

03

1.36

04

OPERATING CASH FLOWS BEFORE WORKING CAPITAL

(in millions of dollars)

286

0235

603

351

04

IND

US

TRIA

L

CONSOLIDATED NORMALIZED VOLUMES(millions of cubic metres)

3,07

1

03

3,12

0

04

CO

MM

ER

CIA

L

1,90

5

03

1,91

7

04

RE

SID

EN

TIA

L

741

03

752

04

TOTA

L V

OL

UM

E

5,71

7

03

5,78

9

04

34 G A Z M É T R O L I M I T E D P A R T N E R S H I P

2 0 0 4 A N N U A L R E P O R T

Gross margin provides a clearer picture of how the Sector is doing. It is up by $2.2 million, or 0.4%, to $487.9 million in 2004 from $485.7 million the preceding year. Apart from the 1.3% increase in normalized volumes, this can be explained primarily by the increasein the rate of return authorized by the Régie on Partners’ equity allocated to the Quebec distribution activity from 10.34% in 2003to 10.96% in 2004, partially offset by the 2% decrease in the federal income tax rate, which had a negative impact of approximately $4.1 million.

In 2004, the Quebec distribution activity earned $14.0 million ($13.2 million in 2003) more than the return authorized by the Régie. Underthe terms of the performance incentive sharing mechanism, the Partnership therefore included in revenues for the year its $4.7 million($4.4 million in 2003) share as an incentive return and will return the balance to customers in the 2006 fiscal year, primarily in the form of rate reductions.

Operations and maintenance expenses for the Distribution Sector increased by $4.5 million, or 2.9%, to $158.9 million. This can beexplained primarily by amounts spent on the advertising campaign launched in the fall of 2003 as well as a larger contribution to oneof Gaz Métro’s employee pension plans.

Amortization related to fixed assets and deferred charges is down by $4.2 million in 2004, compared to 2003, to $114.8 million. The decreaseis due to the mechanism for returning to customers their share of the excess returns earned by the Partnership in prior years. Gaz Métropresents the amount it has to return to customers in a particular year as a reduction of amortization expense. The amount to be returnedin 2004 is higher than in 2003.

Interest expense is up by $5.2 million, primarily due to an increase in the average debt load of the Quebec distribution activity in 2004,as well as an increase in the weighted average cost of this debt over the preceding year.

Partners’ income from the Distribution Sector’s activities is $137.7 million, which is slightly less than the $138.0 million for the precedingyear. The stronger Canadian dollar in relation to its U.S. counterpart in 2004 had a negative effect on the Sector’s income as part of thedistribution activities are in U.S. dollars. Had it not been for the foreign exchange impact, income would have been $0.9 million higher in 2004.

TRANSPORTATION SECTOR