2003 anz annual report strong differ ent successful ... · $400m $0m return on equity maintained...

TRANSCRIPT

2003 ANZAnnual Report Strong

DifferentSuccessfulSustainable

The bank with a human face, easy to do business with, building enduring customer relationships

For our customers

A great company, with great people, great values, great opportunities

For our people

One of the most efficient, best managed, and most successful banks in the world

For our shareholders

Trusted. Making a sustainable contribution to society For our

community

Breakout. Bold, different, investing, partnering, growing For our

future

The ANZAgenda

1

Investor Snapshot

Chairman’s Report

Chief Executive Officer’s Report

Chief Financial Officer’s Review

Risk Management

A View from the CEO on Creating Sustainable Businesses

The National Bank of New Zealand

People

Personal and Rural Customers

Business Banking

Systems

Community and Environment

Leadership

Business Profiles

Board of Directors

Corporate Governance and the Board

Compensation

Guide to Concise Financial Report

Concise Financial Report

Directors’ Report

Directors’ Declaration

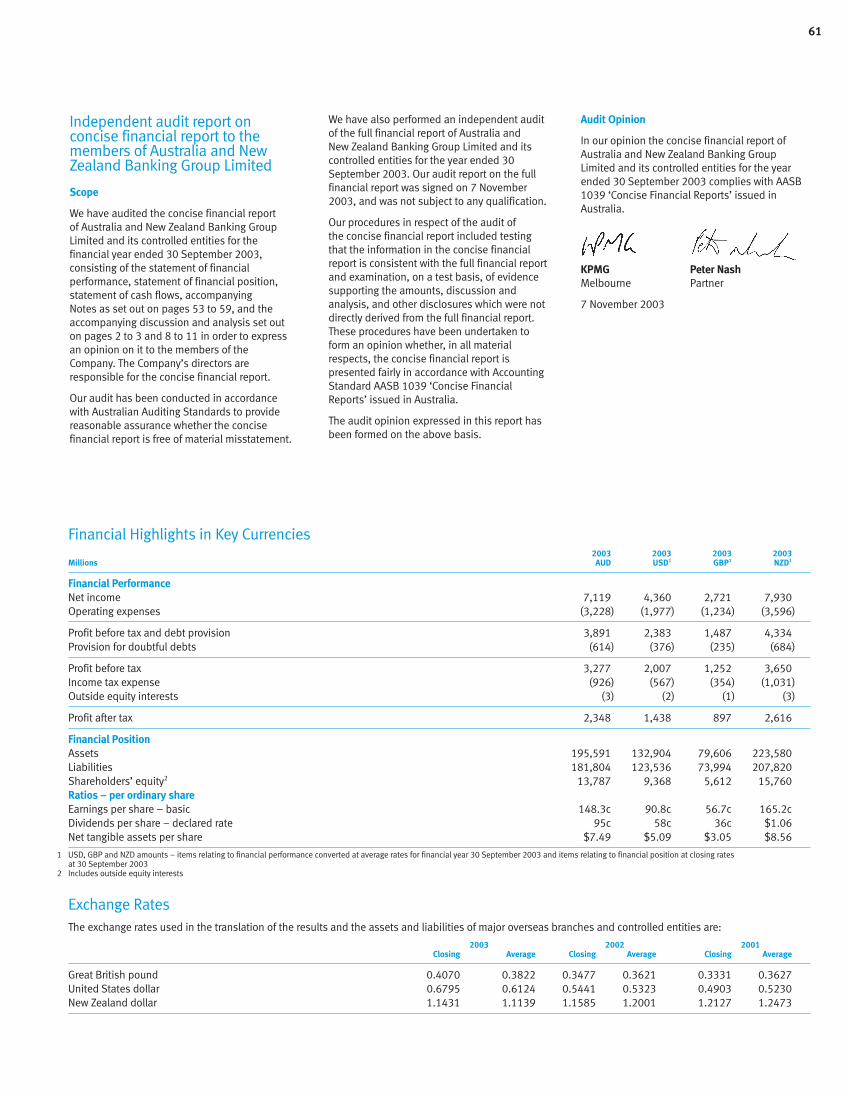

Auditors’ Report

Shareholder Information

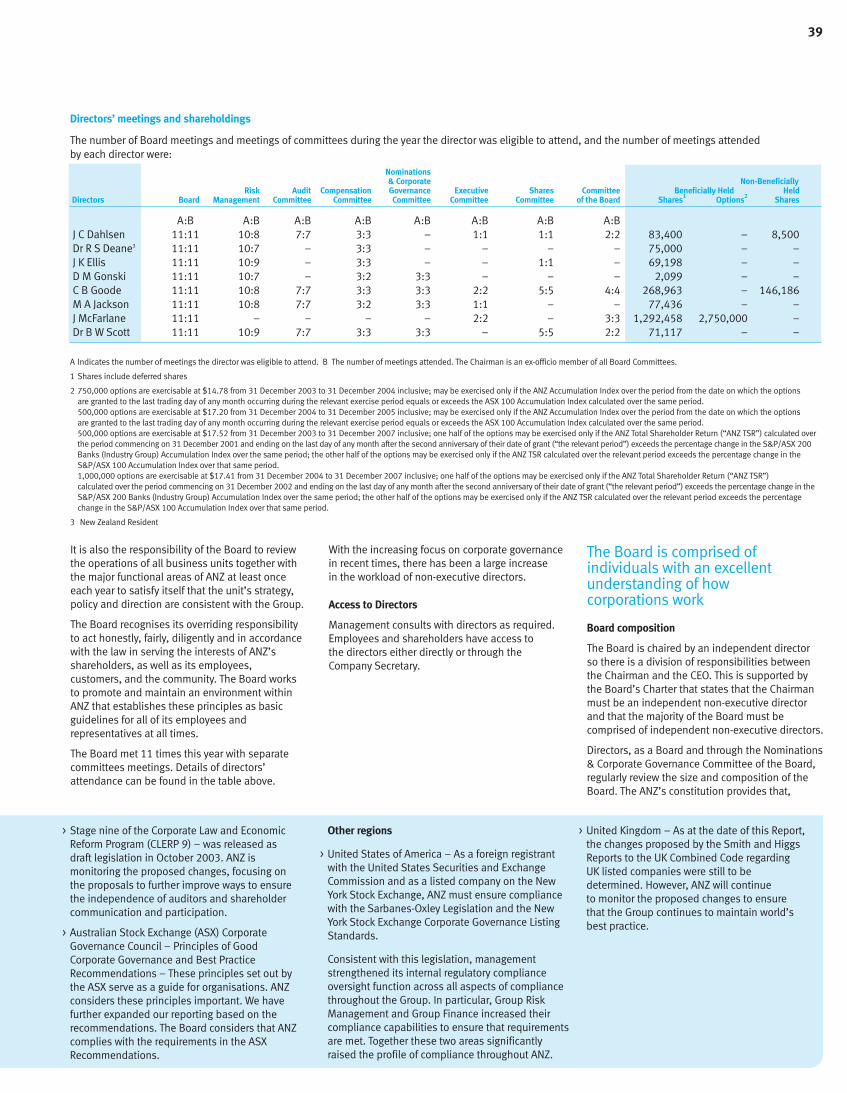

Shareholder Feedback Form

Information for Shareholders

0204060812141618202224262830343843484951606162

Last PageInside Back Cover

Contents

Key terms

Cost to income ratio (CTI)A business efficiency measure. It is the ratio ofour expenses (excluding goodwill amortisation)to our income.

Credit ratingA measurement of the credit worthiness of abusiness. AAA is the top credit rating accorded by ratings agencies such as Moody’s InvestorServices and Standard & Poor’s. The better ourcredit rating, the cheaper we can borrow moneyfrom capital markets. ANZ’s long-term creditrating is AA-.

Dividend per share (DPS)The amount of the Company’s after tax earningsdeclared and paid to ordinary shareholders. It is usually expressed as a number of cents pershare, or as a dividend per share.

Earnings per share (EPS)The amount, in dollars, of earnings divided by the average number of ordinary shares. For example, if the earnings are $2 million and 1 million shares are outstanding, the earningsper share would be $2.00 ($2 million ÷ 1 millionshares = $2.00). The earnings figure is based onprofit after tax less preference share dividends.

Economic value added (EVATM)

A measure of risk-adjusted accounting profit. It is based on operating profit after tax, adjustedfor one-off items, the cost of capital, imputationcredits and economic credit costs.

Net profit after tax (NPAT)The Group’s net profit after all taxes, expensesand provisions have been deducted from theoperating income.

Return on equity (ROE)A calculation which shows the return the Company has made on the money ordinaryshareholders haveinvestedin ANZ. It isexpressed as a percentage.

Investor Snapshot 2003.The year at a glance

2

Movement in our share price has been in line with most of our major competitors in 2003.

In 2003, we continued to deliver improved returnsto our shareholders with a record interim dividendof 44 cents and a final dividend of 51 cents both100% franked.

Earnings per share growth was above 8%.

A record dividend per share together with a relatively stable share price has again delivered returns to our shareholders.

We continued to deliver realgrowth to our shareholders

ANZ share price

$23

$21

$19

$17

$15

$13

$11

$9

$7

$5

Sep

98

Mar

99

Sep

99

Mar

00

Sep

00

Mar

01

Sep

01

Mar

02

Sep

02

Mar

03

Sep

03

$300

$250

$200

$150

$100

$50

Value of $100 investment in ANZ shares invested for five years(A)

$0

Sep

98

May

99

Jan

99

Sep

99

Jan

00M

ay 0

0S

ep 0

0Ja

n 01

May

01

Sep

01

Jan

02M

ay 0

2S

ep 0

2Ja

n 03

May

03

Sep

03

2002 200320012000

Dividend per share

100c

0c

80c

60c

40c

20c

2002 2003200120001999

0c

150c

120c

90c

60c

30c

Earnings per share(B)

Our share price has remainedrelatively steady over 2003

Healthy dividend growth Profitability growth remained solid

For further information on financial terms, please refer to the Guide to Concise Financial Report on page 48

3

EVATM growth was moderately dampenedby relatively higher cost of capital. EVATM

nonetheless continued to increase inabsolute terms.

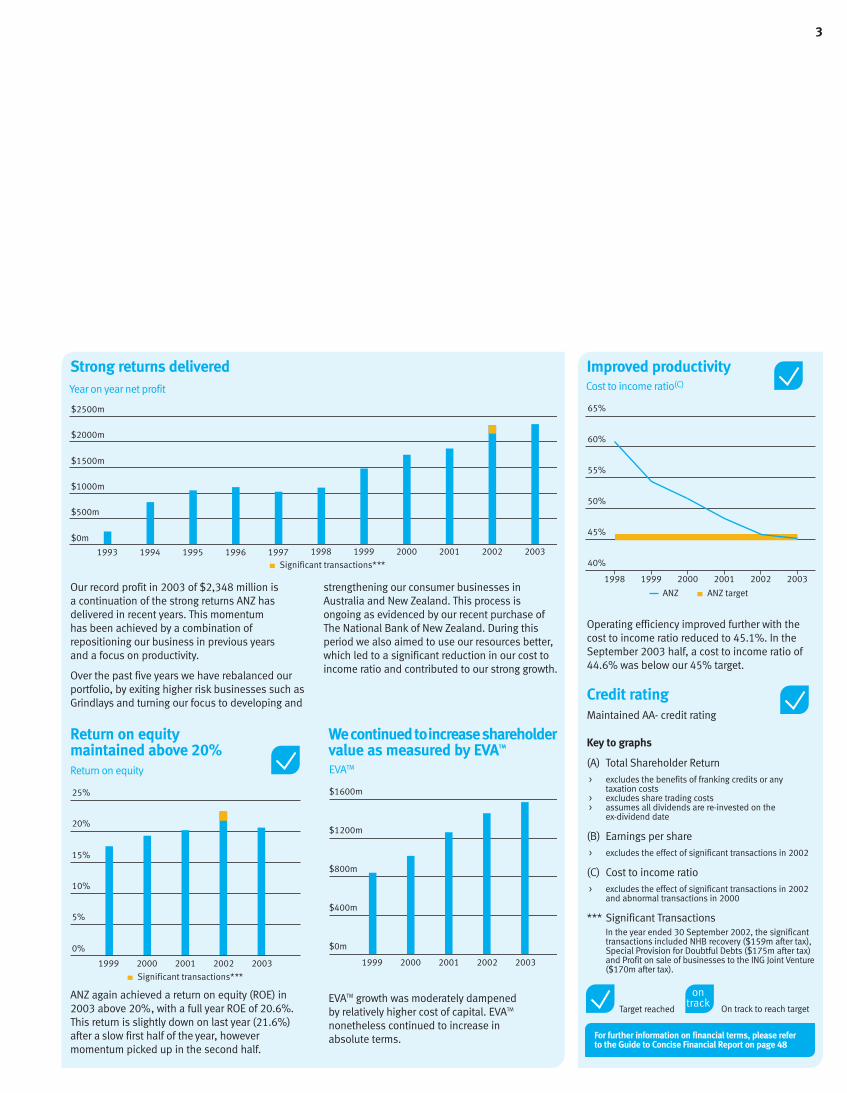

ANZ again achieved a return on equity (ROE) in2003 above 20%, with a full year ROE of 20.6%.This return is slightly down on last year (21.6%)after a slow first half of the year, howevermomentum picked up in the second half.

Operating efficiency improved further with thecost to income ratio reduced to 45.1%. In theSeptember 2003 half, a cost to income ratio of44.6% was below our 45% target.

Year on year net profit

$0m

$2500m

$2000m

$1500m

$1000m

$500m

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Significant transactions***

2002 2003200120001999

Return on equity

0%

25%

20%

15%

10%

5%

Significant transactions***

Cost to income ratio(C)

60%

65%

55%

50%

45%

40%

2002 20032001200019991998

ANZ ANZ target

2002 2003200120001999

EVATM

$1600m

$1200m

$800m

$400m

$0m

Return on equitymaintained above 20%

Wecontinuedtoincreaseshareholdervalue as measured by EVATM

Target reached On track to reach target

Improved productivity

Credit ratingMaintained AA- credit rating

Strong returns delivered

Our record profit in 2003 of $2,348 million isa continuation of the strong returns ANZ hasdelivered in recent years. This momentum has been achieved by a combination ofrepositioning our business in previous yearsand a focus on productivity.

Over the past five years we have rebalanced ourportfolio, by exiting higher risk businesses such asGrindlays and turning our focus to developing and

strengthening our consumer businesses inAustralia and New Zealand. This process isongoing as evidenced by our recent purchase ofThe National Bank of New Zealand. During thisperiod we also aimed to use our resources better,which led to a significant reduction in our cost toincome ratio and contributed to our strong growth.

Key to graphs

(A) Total Shareholder Return> excludes the benefits of franking credits or any

taxation costs> excludes share trading costs> assumes all dividends are re-invested on the

ex-dividend date

(B) Earnings per share> excludes the effect of significant transactions in 2002

(C) Cost to income ratio> excludes the effect of significant transactions in 2002

and abnormal transactions in 2000

*** Significant TransactionsIn the year ended 30 September 2002, the significanttransactions included NHB recovery ($159m after tax),Special Provision for Doubtful Debts ($175m after tax)and Profit on sale of businesses to the ING Joint Venture($170m after tax).

ANZ performed well in 2003. Profit after tax,excluding significant transactions in 2002,was up 8.3% this year, demonstrating theeffectiveness of our specialist business modelin delivering returns to shareholders. Thedirectors were pleased to increase the dividendper share by 11.8% to 95 cents fully franked.

Most of our businesses recorded solid growthwith some recording double-digit growth in earnings. These were partially offset by a one-off charge in our credit card business. We delivered solid financial performance byfocusing on organic growth, effective costcontrol and the management of risk.

The return on ordinary shareholders’ equitywas slightly down at 20.6%, although above our target of 20%. Our cost to income ratio of45.1% is the lowest of the major Australianbanks and places ANZ among the most efficientbanks in the world relative to business mix. Riskscontinue to be well managed. Specific provisionswere down by 28% to $527 million. Our capitalposition is strong, with the Group’s adjustedcommon equity ratio at 5.7%, which was at theupper end of our target range for 2003.

Significantly, we settled a long-running taxdispute with the Australian Taxation Office thisyear relating to equity product transactionsundertaken predominantly in the 1990s. Thesettlement of $262 million was met from ANZ’sexisting tax provisions.

Growth through specialisationANZ is focused on creating sustainable valuefor shareholders –now and in the longer term.

Much of this work involves building on thecompetitive advantages that exist in our specialistbusinesses. This year’s results reinforce thequality of each of these businesses. In manycases such as credit cards, corporate bankingand automobile and equipment leasing, ourbusiness is the market leader.

We believe our specialist business strategyis fundamental to sustaining and buildingleadership positions that help us to deliversuperior returns to shareholders and make adifference to our customers, community and staff.

Chairman’s Report A solidplatform forfuture growth

4

Charles GoodeChairman

5

Strategic expansionWe continually evaluate opportunities to expandin Australia, New Zealand and elsewhere in Asiaand the Pacific.

On 24 October 2003, we agreed to acquireThe National Bank of New Zealand from LloydsTSB for $4.915 billion at exchange rates on23 October 2003. The acquisition will makeus the largest bank in New Zealand and isconsistent with our strategic goal to havesustainable top three positions in each ofour core businesses and markets.

We have also taken steps to develop a smallportfolio of growth options in East Asia over the medium to long-term. This has involvedtwo relatively modest initiatives: signing amemorandum of understanding with theShanghai Rural Credit Cooperative Union – expected to become the Shanghai CooperativeBank – and a joint venture credit card businesswith Metrobank in the Philippines.

Our role in the communityWe continue to give high priority to creating a distinctive culture within ANZ as part of theGroup’s long-term competitive advantage.This involves reinforcing a performance cultureamong staff while unleashing their talents andenergy to expand the business for the benefitof shareholders, our customers and thecommunity we serve.

While we have a wide range of formal communityprograms in place in countries in which weoperate, being part of a community meansbeing able to respond quickly to urgent needs.

All of us at ANZ feel proud of the way our staff responded to the terrible bushfires thatdestroyed over 530 homes in Australia’s capital,Canberra in January. ANZ provided immediatecash assistance for its mortgage customerswhose primary residence had been affected bythe bushfires. The grants of $5,000 to $10,000were gifts and did not have to be repaid. Wealso offered a range of other measures and ourlocal staff worked hard to help customers andothers affected by the tragedy.

As part of the process to strengthen therelationships we have with our staff and thebroader community, we have been examiningour response to concerns about environmentaland social issues. This process has provided uswith the opportunity to re-examine our role asa bank and the contribution we make to societyas “the bank with a human face”.

Importance of our staffThe continuing strong performance of ANZ, its growth in returns to shareholders andincreasing responsiveness to customers and the community is the result of the hard workand commitment of our 23,137 staff. On behalfof the Board and shareholders, I thank them fortheir contribution.

Governance strengthenedThis year we have taken further steps tostrengthen our corporate governance anddisclosure standards. It has been a yearwhen regulatory emphasis has increasedsubstantially, both in Australia and overseas.While this interest on the part of regulators iswelcomed, so long as it focuses upon goodprocess and good governance, ANZ is itselfproactive in this area. Our belief is that goodcorporate governance is not only an ethical andstewardship responsibility; it can also give ANZa strong advantage.

We believe a strong focus on corporategovernance and transparency, combined withdelivering on our promises, makes ANZ bothmore attractive to investors and a moresustainable business.

This starts with regulatory compliance butsignificantly involves fostering an environmentin which open, well-informed and constructivediscussion is encouraged. This provides thebasis for actively monitoring the company’sactivities and creates an environment in whichintegrity is able to prevail at every level.

It also means a commitment to transparentreporting, timely and accurate disclosuresand management accountability. For some years ANZ has been recognised for its levelof transparency and disclosure to investors, not only in Australia, but globally.

The Board’s focus in 2003ANZ’s Board met 11 times during 2003, withadditional specific activities carried out by theBoard’s committees. This year some of the keyissues to engage the Board included strategicgrowth opportunities and their role in ANZ’sfuture success; strengthening operating riskmanagement including improved governanceassociated with technology changes; theimpending changes to international financialreporting standards and their impact on ANZ;and our approach to sustainability and how theGroup balances its obligations to shareholders,customers, staff and the community.

OutlookIn the year ahead, we expect the Australian and New Zealand economies to continue toperform relatively well and for overseas marketsto strengthen from their low base. Somechallenges are, however, posed by variousfactors including low interest rates andassociated margin pressure and the risingAustralian dollar.

Overall, ANZ is making good progress towardachieving its business priorities. We haveproduced a solid, consistent financialperformance and we are creating growthopportunities for the future. I am confidentthis will enable us to continue to deliver valuefor you, our shareholders.

Charles GoodeChairman

ANZ’s agenda is based on a strategy ofspecialisation that is well executed andconsistently delivers superior performance for our shareholders, staff, customers and the community we serve.

Overall, the 2003 financial result has beenreasonable in an environment that is beginning to be difficult for banks around the world. It’sthe power of our specialisation strategy and the quality of the teams that run our specialistbusinesses that has allowed us to reinvent ANZover the past five years as a low risk,well-managedcompany that consistently produces sound results.

Five years of achievementLast year I reported on the achievements we had made since 1997 making ANZ a very differentbank. These included:

> lowering risk

> balancing our business portfolio by growing our consumer businesses while maintaining our strong business banking franchise

> radically transforming our cost structure andbecoming one of the most efficient banksin the world

> reinvigorating our culture by tapping into the energy and passion of our staff.

In thinking about that transition – and what ANZis today – it is being the “bank with the humanface” which is the core of who we are and whatwe do at ANZ. Our objectives, strategy, tacticsand organisational structure are aligned totranslate the “bank with a human face” from a set of words into everyday actions.

Customer driven businessesAll businesses now operate in a customer-driveneconomy. This is particularly true in financialservices where there are more competitorspursuing a stable number of more sophisticated,better informed buyers. The Internet, consumeradvocate organisations and a critical mediaenable customers to find and analyse competingproducts and to make informed choices.

Many financial services offerings have becomecommodities where differentiation lies in theprovider’s service and reputation rather thanthe product itself. We believe that to competeand survive in the customer economy takesmore than simply improving customerrelationships. It is about the whole organisationevolving to put the customer at the centre.

Specialisation works forshareholders and customersWe set out on this path in 2000 recognising that over time specialist businesses, whichhave real capabilities, produce more sustainablevalue than generalists. Importantly, theyare better able to get close to customers,understand their real needs and delivermore valuable services and products. We have seen that through our Local CEOs andbranch staff, we are now much closer to thecommunities we serve. It reflects a reality thatour customers and our staff find it easier toidentify with a more agile, less bureaucraticorganisation. Customers identify with “their”branch or “their” relationship manager. Staffidentify with “their” team or “their” business.

At the same time, we began to show our staffand the rest of the community that ANZ was adifferent bank. We announced a moratorium onrural bank closures, offered to buy the branchesbeing closed by one of our major competitors,gave immediate “no strings attached” grants tocustomers whose houses had been destroyedby bushfires and started trialing a matchedsavings program for low income earners.

We also recognised that winning companiesare companies that can offer value to customersat lower cost. We radically changed our costbase which is now flowing through topropositions such as our low-cost personaltransaction accounts and the associatedgrowth in customer numbers that is part ofour “best deal with a human face” strategy forpersonal banking.

Winning through specialisationThrough specialisation, each of our businessesis now:

> more transparent

> more flexible and more responsive to itsstaff and customers

> easier to do business with

> offering more satisfying jobs with moreautonomy

> developing a culture of innovation, teamworkand shared responsibility

> making implementation easier

> able to grow faster.

All of this is a very different approach to anyother bank. Through it, we seek to deliver moreconsistent, sustainable returns to shareholders.

Focusing on sustainedperformance and growthWhile all we have achieved so far remainscentral to ANZ’s agenda, another measure ofour progress will be the management actionswe take in other areas to deliver continuedsuperior performance and growth over the comingyears. The reality is that there is more to ANZthan producing consistent short-term results.

We have reached agreement on acquiring TheNational Bank of New Zealand which givesus a leading position in New Zealand. It is a very different acquisition, one based onimproving customer service, satisfaction and growth by leveraging the strengths ofboth companies.

It demonstrates that we are in a transitionalphase, which means we will focus increasinglyon three strategic priorities in the years ahead:

> delivering sustainable performance and valuethrough a rich portfolio of strongly positionedbusinesses with best-practice cost andprocess leadership that allow us to achieveabove sector revenue and share growth.

Chief Executive Officer’s Report The ANZ

Agenda:achievingvalue throughspecialisation

6

7

> earning the respect of our stakeholders byconsistently producing superior financialresults through knowing the business andcustomers best, and creating a strong salesand service culture while developing realengagement with the community.

> creating a new future by leveraging specialisationas a distinctive approach and by beingdynamic, innovative and willing to experiment.

Creating more valueOur future is about delivering the best value forcustomers, performing and growing to createvalue for our shareholders, leading and inspiringeach other, earning the trust of the community,and being bold and having the courage to bedifferent. It’s why people come to work for ANZ– to be part of a company that is continuallyraising its energy levels to make a lasting impact and create something that matters forshareholders, customers and the communitywe serve.

By really being the “bank with a human face” to our customers, staff and community, andfocusing on these priorities, ANZ is stronger,more sustainable, more successful andvery different.

John McFarlaneChief Executive Officer

John McFarlaneChief Executive Officer

Chief FinancialOfficer’s Review Growth,

returnsand profit

8

Sep 02 excluding significant transactions(A)

$2500m

$2300m

$2100m

$1900m

$1700m

$1500m

Sep 02

2322

Sep 03

2348(154)

Sign

ifica

nt tr

ansa

ctio

ns

293

Net

Inte

rest

Inco

me

12

Non

Inco

me

Inte

rest

(75)

Expe

nses

(4)

Prov

isio

ning

(46)

Tax

& O

EI2168

NPAT increase NPAT decrease Prior period NPAT$0m

8%Institutional Financial ServicesChange

5%Personal Banking & Wealth Mgmt

9%Mortgages

12%Corporate

-4%Consumer Finance

8%New Zealand Banking

34%Asia Pacific

23%Esanda/UDC

-24%Treasury

$100m $200m $300m $400m $500m $600m $700m $800m

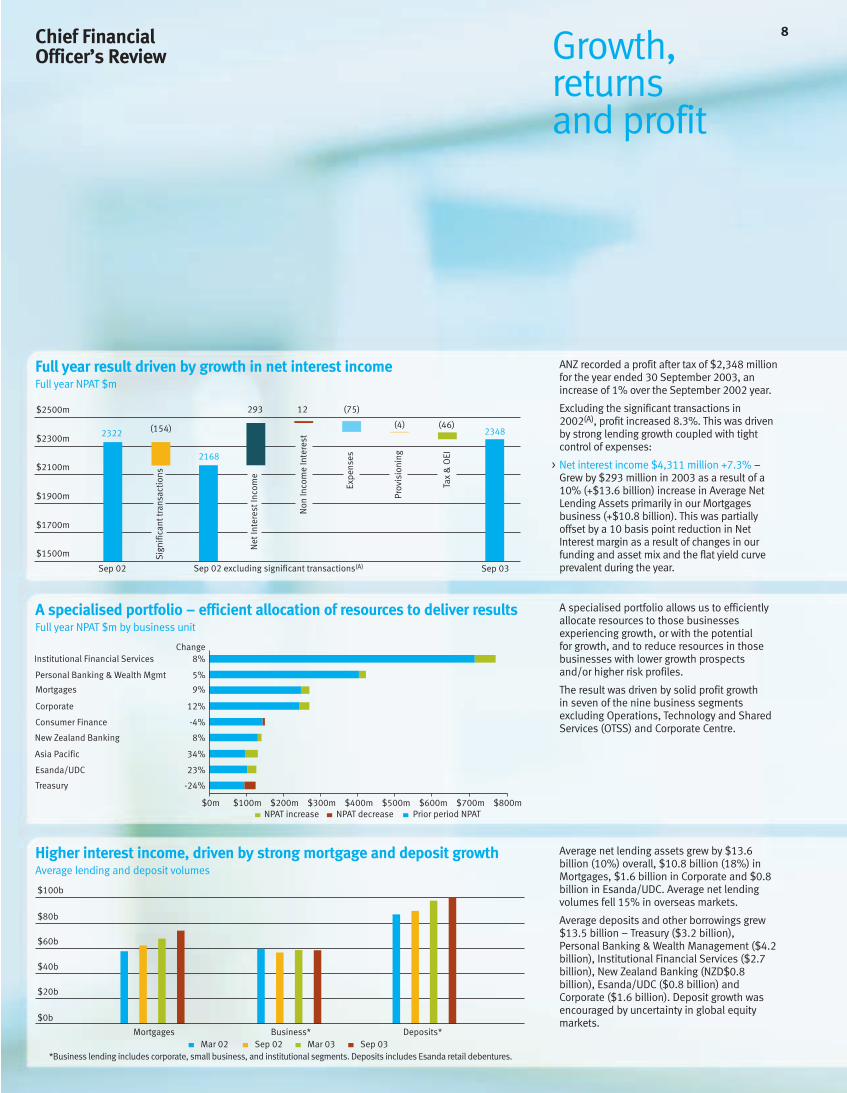

ANZ recorded a profit after tax of $2,348 millionfor the year ended 30 September 2003, anincrease of 1% over the September 2002 year.

Excluding the significant transactions in2002(A), profit increased 8.3%. This was drivenby strong lending growth coupled with tightcontrol of expenses:

> Net interest income $4,311 million +7.3% –Grew by $293 million in 2003 as a result of a10% (+$13.6 billion) increase in Average NetLending Assets primarily in our Mortgagesbusiness (+$10.8 billion). This was partiallyoffset by a 10 basis point reduction in NetInterest margin as a result of changes in ourfunding and asset mix and the flat yield curveprevalent during the year.

A specialised portfolio allows us to efficientlyallocate resources to those businessesexperiencing growth, or with the potentialfor growth, and to reduce resources in thosebusinesses with lower growth prospectsand/or higher risk profiles.

The result was driven by solid profit growth in seven of the nine business segmentsexcluding Operations, Technology and SharedServices (OTSS) and Corporate Centre.

Average net lending assets grew by $13.6billion (10%) overall, $10.8 billion (18%) inMortgages, $1.6 billion in Corporate and $0.8billion in Esanda/UDC. Average net lendingvolumes fell 15% in overseas markets.

Average deposits and other borrowings grew$13.5 billion – Treasury ($3.2 billion),Personal Banking & Wealth Management ($4.2billion), Institutional Financial Services ($2.7billion), New Zealand Banking (NZD$0.8billion), Esanda/UDC ($0.8 billion) andCorporate ($1.6 billion). Deposit growth wasencouraged by uncertainty in global equitymarkets.

Full year result driven by growth in net interest incomeFull year NPAT $m

A specialised portfolio – efficient allocation of resources to deliver resultsFull year NPAT $m by business unit

Deposits*Business*Mortgages

$0b

$100b

Mar 02 Sep 02 Sep 03Mar 03*Business lending includes corporate, small business, and institutional segments. Deposits includes Esanda retail debentures.

$80b

$60b

$40b

$20b

Higher interest income, driven by strong mortgage and deposit growthAverage lending and deposit volumes

9

> Non-Interest Income $2,808 million +0.4% –Reported growth was flat for the year. Afteradjusting for the sale of ANZ Funds Managementbusinesses to the ING Joint Venture and underaccrual of loyalty points cost on credit cards inprior periods, underlying growth was 5.2% drivenby higher lending fees in our Corporate Banking,Asset Finance and Institutional Bankingbusinesses, higher equity accounted profit fromour investment in PT Panin Bank and developmentproperty sales in Institutional Banking.

> Expenses $3,228 million +2.4% – Once again,tightly controlled across the Group. Higher stafflevels required to service increased lendingvolumes and an increase in software amortisationon system upgrades, were the main contributors

to the 2.4% increase in costs. Discretionarycosts were contained as the control ofexpenses remains a key aspect of our financialmanagement.

> Provisioning $614 million +0.7% – Asset qualityimproved with the Economic Loss Provision (ELP)rate down primarily due to a higher proportion ofmortgages. This lower rate offset the impactof increased lending volumes.

> Tax & Outside Equity Interests (OEI)$929 million +5.2% – Increase in profits causedthe higher tax expense in 2003, however, ahigher amount of equity accounted earningshas meant that the growth in tax expense wasbelow profit growth.

Strong results in Corporate (12%) andEsanda/UDC (23%) were driven by strongdomestic growth, while the 34% improvementin Asia Pacific resulted largely from higher equityaccounted earnings from PT Panin Bank, higherforeign exchange earnings and lending growth.

Profit in Mortgages grew 9% reflecting continuedgrowth in the Australian housing market whilethe 5% improvement in Personal Banking andWealth Management resulted largely fromincreased deposit volumes and increasedcommissions on mortgage sales. This waspartially offset by lower earnings from our INGJoint Venture.

TheInstitutional FinancialServices result increased8% with strong contributions from Capital Marketsand the Australasian operations of InstitutionalBanking. Contributions from Structured FinanceInternational and the offshore operations ofInstitutional Banking reduced following thedecision to reduce exposure to the US and UK markets.

New Zealand Banking results were flat afteradjusting for the impact of the appreciation in the exchange rate.

Consumer Finance was impacted by the underaccrual of loyalty expense, and mismatch earnings in Treasury reduced as high yieldinginvestments matured.

Peter MarriottChief Financial Officer

Sustained underlying profit growth in our coredomestic markets has been supported bystrong growth in Asia and Pacific. The Group’sstrategy to reduce exposure to higher riskoffshore sectors saw reduced profit in the UKand US.

Australia

UK/US & other

Pacific

New Zealand

Asia

72%

15%

5% 3% 5%

Profits continued to be derivedfrom our core domestic markets2003 NPAT by geography – %

(A) Significant TransactionsIn the year ended 30 September 2002, thesignificant transactions included NHB recovery($159m after tax), Special Provision for Doubtful Debts($175m after tax) and Profit on sale of businesses tothe ING Joint Venture ($170m after tax).

For further information on financial terms, please refer to the Guide to Concise Financial Report on page 48and the Investor Snapshot on page 2

10Chief FinancialOfficer’s Review

* Sep 02 excludes significant transactions** excludes volume impact and benefits from repricing

Und

erly

ing

grow

th

Cash

flow

impa

cton

trad

ing

secu

riti

es in

com

e

Pani

n bo

nd s

ales

$2900m

$2800m

$2700m

$2600m

$2500m

(71)

(20)

(37)(33)

Sep

03

Sep

02*

20

45

JV im

pact

Und

erst

atem

ent o

flo

yalt

y ex

pens

e in

200

2

Card

s un

der-a

ccru

al

Hig

her l

oyal

ty c

osts

**

Low

er S

FI in

com

e

(38)

28081462796

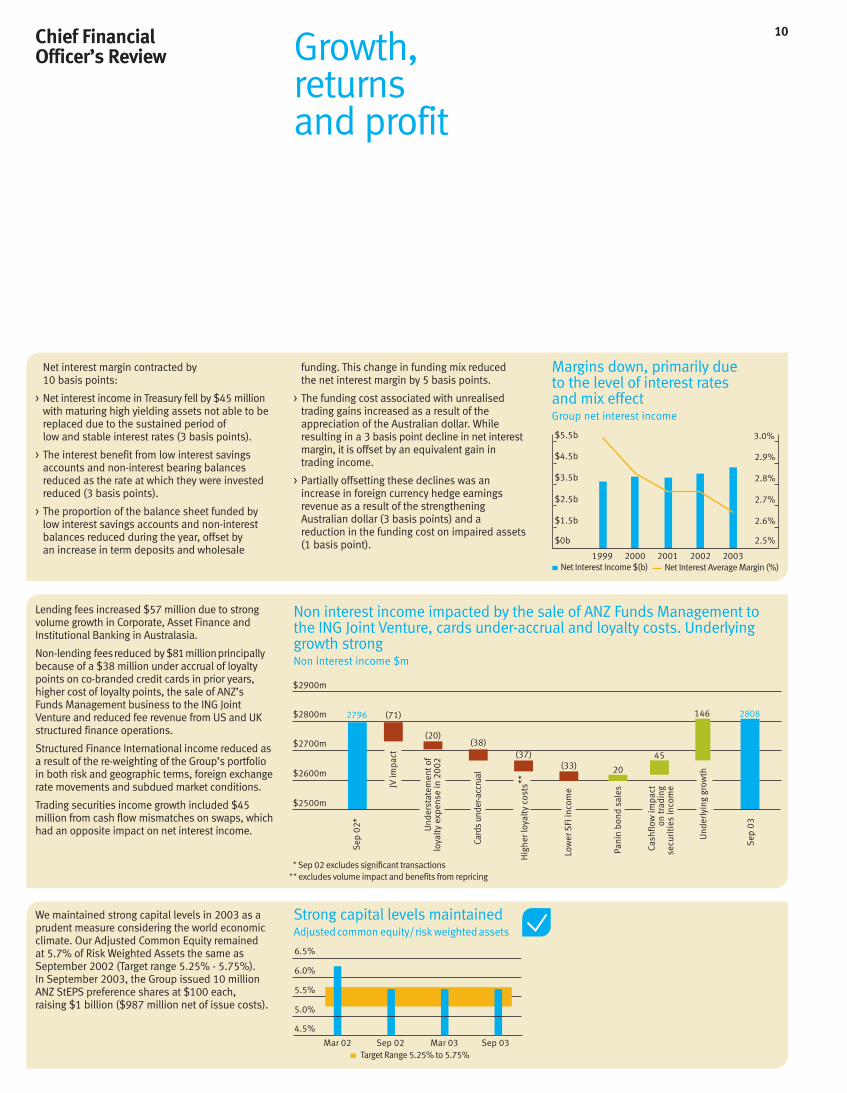

Lending fees increased $57 million due to strongvolume growth in Corporate, Asset Finance andInstitutional Banking in Australasia.

Non-lending feesreduced by $81millionprincipallybecause of a $38 million under accrual of loyaltypoints on co-branded credit cards in prior years,higher cost of loyalty points, the sale of ANZ’sFunds Management business to the ING JointVenture and reduced fee revenue from US and UKstructured finance operations.

Structured Finance International income reduced asa result of the re-weighting of the Group’s portfolioin both risk and geographic terms, foreign exchangerate movements and subdued market conditions.

Trading securities income growth included $45million from cash flow mismatches on swaps, whichhad an opposite impact on net interest income.

Non interest income impacted by the sale of ANZ Funds Management tothe ING Joint Venture, cards under-accrual and loyalty costs. Underlyinggrowth strongNon interest income $m

Net interest margin contracted by10 basis points:

> Net interest income in Treasury fell by $45 millionwith maturing high yielding assets not able to bereplaced due to the sustained period oflow and stable interest rates (3 basis points).

> The interest benefit from low interest savingsaccounts and non-interest bearing balancesreduced as the rate at which they were investedreduced (3 basis points).

> The proportion of the balance sheet funded bylow interest savings accounts and non-interestbalances reduced during the year, offset byan increase in term deposits and wholesale

$2.5b

$0b

$5.5b

$3.5b

$4.5b

$1.5b

2.5%

2.6%

2.7%

2.8%

2.9%

3.0%

Net Interest Income $(b) Net Interest Average Margin (%)2001 20021999 2000 2003

Margins down, primarily due to the level of interest ratesand mix effectGroup net interest income

Growth,returnsand profit

Mar 03 Sep 03Sep 02Mar 02

4.5%

5.0%

6.5%

6.0%

5.5%

Target Range 5.25% to 5.75%

funding. This change in funding mix reduced the net interest margin by 5 basis points.

> The funding cost associated with unrealisedtrading gains increased as a result of theappreciation of the Australian dollar. Whileresulting in a 3 basis point decline in net interestmargin, it is offset by an equivalent gain intrading income.

> Partially offsetting these declines was anincrease in foreign currency hedge earningsrevenue as a result of the strengtheningAustralian dollar (3 basis points) and areduction in the funding cost on impaired assets(1 basis point).

We maintained strong capital levels in 2003 as aprudent measure considering the world economicclimate. Our Adjusted Common Equity remainedat 5.7% of Risk Weighted Assets the same asSeptember 2002 (Target range 5.25% - 5.75%).In September 2003, the Group issued 10 millionANZ StEPS preference shares at $100 each,raising $1 billion ($987 million net of issue costs).

Strong capital levels maintained Adjusted common equity/risk weighted assets

11

2002 200320011998 1999 2000

$300m

$0m

$700m

$400m

$500m

$600m

$200m

$100m

Headline ELP (bps)

0 bps

80 bps

ELP charge*excludes the $250 million special provision in 2002

ELP adjustment

70 bps

60 bps

50 bps

40 bps

30 bps

20 bps

10 bps

2002 200320011999 2000

$900m

$0m

$1500m

$1200m

$600m

$300m

Aust/NZ UK/US Asia Other International

New non-accruals have reduced significantlyover the last year, particularly in the offshoreportfolios where in 2002 two large single nameexposures in the offshore Telecommunicationsand Energy portfolios accounted for 35% of newnon-accruals.

End of period gross lending asset volumesreduced 24% in overseas markets as a resultof the strategy to reduce higher risk exposuresin the UK and US and the exchange rate impactof a strengthening Australian dollar.

The Group economic loss provision charge(ELP) was $614 million, compared with $610million (excluding the $250 million specialprovision) in the year to September 2002. Thestandard ELP charge to operating segments at$514 million reduced from September 2002.An additional charge of $100 million (7 basispoints) was taken to recognise continueduncertainty and expected levels of default inthe offshore lending portfolios.

Geographic new non-accrual loans

20032002

$150m

$0m

$350m

$300m

$200m

$250m

$100m

$50m

Energy Domestic Corporate Asset FinanceConsumer Finance Other Offshore Other

New non-accrual loans by source

ANZ Group

Australia & NZ

International

-25% -20% -15% -10%

15%

11%

-5% 0% 5% 10% 15%

-24% -9%

Local currencyAustralian dollars

24% reduction in gross lending assets in offshore portfolioLending asset growth for the year to Sept 2003

Doubtful Debts Provision reflectsimproved underlying portfolio*

New non-accruals reduced 23% on 2002

In recent years, ANZ has been repositioningitself away from higher risk offshoreinstitutional lending, towards lower riskdomestic lending as reflected in our 2003growth in Mortgages and reduction in US andUK lending. This has resulted in a reduction inour ELP rate over time, which fell from 43 basispoints in September 2002 to 39 basis points inSeptember 2003.

For further information on financial terms, please refer to the Guide to Concise Financial Report on page 48and the Investor Snapshot on page 2

12Risk Management

Key TermsArrears – a contractually due and payable sum which remains overdue/unpaid.

Credit risk – the potential for loss arising from the failure of a customer or counter-party tomeet its contractual obligations.

Market risk – the potential loss the Group mayincur from changes in interest rates, foreignexchange rates or the prices of equity sharesand indices, commodities, debt securities andother financial contracts, including derivatives.It also includes the risk that the Group willincur increased interest expense arising fromfunding requirements during periods of poormarket liquidity.

Operational risk – the direct or indirect lossresulting from inadequate or failed internalprocesses, systems, or from external events.

Over the year, ANZ has remained vigilant inmonitoring and managing the Group’s global risksincluding:

> Credit risk – Overall credit quality remains sound;reduced level of defaults in the corporateportfolio; offshore credit exposures reduced to6% of our loan portfolio.

> Market risk – Levels remain low.

> Operational risk – Strengthened businesscontinuity and crisis management capabilities towithstand the emergence of new threats,including increased threats of terrorism and theSARS virus; enhanced technology riskmanagement processes with specific focus onnew software releases.

> Other risk – Increased focus on strategic andemerging risks; substantial progress made onBasel II (see page 38).

Offshore exposuresWe have reduced our offshore credit exposures,including to the power and telecommunicationsindustries.

> Telecommunications – Active portfoliomanagement of exposures to this sector resultedin a reduction in credit limits for offshoretelecommunications operators of 46%.

> Power –As expected, some further deteriorationin the Group’s US power portfolio over the lastyear was experienced, however, our US powerexposures have been managed down by 28% to $1.3 billion and any further losses which might result from this portfolio are expected to be manageable.

Australia and New Zealand marketThe Australian and New Zealand portfolio riskprofile has continued to improve over the yearwith strong mortgage growth and reduced highrisk exposures.

> Consumer portfolio – Arrears and loss rates arenow at or near historically low levels; low-riskpersonal business exposures now comprisetwo thirds of the Group’s loan portfolio.

> Residential property market – Adherence toconservative lending criteria, including allowingfor the likelihood of interest rate increases in

the assessment of borrowers’ capacity to makemortgage payments has ensured a robustmortgages portfolio; we also have conservativelending policies in place to ensure our riskexposure to inner-city apartment marketsacross Australia is minimised.

> Recent APRA stress-testing of our mortgagesportfolio confirms that we are well-placed towithstand a severe downturn in the Australianhousing market.

Large Individual Credit ExposuresOver the year to September 2003, ANZ hasmanaged down its large exposure risks andsignificantly reduced portfolio concentrations. To further reduce risk in the Group’s creditportfolio, our maximum limits applicable toexposures to individual customers have alsobeen reduced.

12

>BB-

B+ to CCCNon Accrual

5.7%1.5%

2.3%0.6%

BB-

BB+ to BB

BBB-

AAA toBBB 14.8% 12.8%

55.3%

15.3%

13.7%

41.5%

19.2%

17.3%

7.2% 2.9%

Sep 98 Sep 03

The Group’s credit risk profile, representing therisk of our customer lending portfolio, hasimproved over the last 5 years. This is evidentwith growth in our lower risk domestic portfolios(particularly mortgages in the BBB- category)and reductions in our high risk exposures.

*Internal credit ratings have been mapped to externalcredit grades

ANZ Group’s credit risk profile hasimproved over the last 5 years*

1313

Mark LawrenceChief Risk Officer

ANZ haslowered riskacross itsglobal portfolio

excludes non-recourse and uncommitted facilities

60%

90%

120%

150%

30%

0%

Sep 03Sep 02Sep 01

Australia Americas Asia NZ International

100%

0%

Sep 03Sep 96

15%

15%13%

6%

70% 81%

Pacific Europe

24%

35%

9%

32%

Personal business Corporate business

100%

0%

Sep 03Sep 97

54%66%

46%34%

In line with strategy, lower risk personalbusinesses now comprise two thirds of thecredit loan portfolio. This has been underpinnedby strong growth in the mortgages portfolio.

In line with ANZ’s lower risk strategies, offshorelending exposures have decreased as aproportion of total lending assets.

One measure of the concentration of largeexposures in the Group’s portfolio is theaggregate of the 10 largest committed corporateexposures as a percentage of adjusted commonequity (ACE). This is used as a measure of risk,hence the lower the ratio the lower theconcentration risk. This ratio has declinedsignificantly over the past 24 months.

Lower risk portfolio due to increasedproportion of personal businessesTop 10 exposures further reduced

ANZ portfolio moving toward lower risk domestic exposures

Based on the Group’s lending assets

For further information on financial terms, please refer to the Guide to Concise Financial Report on page 48and the Investor Snapshot on page 2

14

This year I discovered a surprising andinteresting statistic, which I have reflected onfrom an ANZ perpective.

Of the Top 20 companies by marketcapitalisation in Australia in 1980, only eightremained on the 1990 list, and five on the2000 list.

ANZ, I’m pleased to say, is one of those whichhas survived and thrived, albeit with some upsand downs, so that it is one of the five on boththe 1980 and 2000 Top 20 lists.

Our responsibility to deliverThe challenge for ANZ is to continue to createvalue by delivering strong and sustainableperformance and value to shareholders – notonly this year and next year, but over the longterm. While this is the responsibility of anymanagement team, it is particularly true of abank. That’s precisely why there is so muchmention of “sustainability” in this report.

The key to delivering sustainable performanceand value starts with the fundamentals – havinga genuine competitive advantage, ensuringflawless execution of strategy, no-surprisesmanagement and delivering on promises toshareholders.

In financial terms, value represents the capitalinvested in ANZ, plus a premium representingfuture earnings and value that the marketascribes to our expected future economic valueadded. In fact, this explains around 60% ofour share price. It takes into account ourunique specialisation strategy and growthopportunities, the talent of our staff, ourculture, the market positions and customerfranchises held by our specialist businesses,the strength of our brand and our reputationin the community.

While the value of investment represented bytangible net assets per share has risen byaround 9% a year since 1998, the valuerepresented by future economic value addedhas risen by about 21% a year. It’s a compellingstatistic that forces me, as Chief ExecutiveOfficer, to think about business differently.

Focus on long-term valueIt highlights that enduring success means morethan short-term performance. Sustainable valuetakes us beyond the traditional notion ofshareholder value as it has been conceivedand implemented over the past decade. It recognises that delivering sustainable valuein the long-term is, in essence, about restoringcustomer faith and building community trust byunderstanding that we do not serveshareholders exclusively, but others as well.

It is why being the “bank with the human face”has to be at the core of who we are and whatwe do at ANZ. It means we integrate economic,environmental and social factors, andbalance our obligations to different groupsof stakeholders and create value for allof them – shareholders, customers, staff andthe community.

It requires us to continually factor the long-terminto our decision-making.

Our societal purposeThis year we have developed a corporateresponse to environmental and social concernsexpressed by our key stakeholders. Many of ourstaff have been involved in an assessment ofour impact on society, contributing to definingANZ’s “Societal Purpose” and in developing a number of new initiatives to improve ourenvironmental and social performance. Ourparticular approach to sustainability is based on seeing our people, customers andcommunity as an integrated business system.It means embedding society’s environmentaland social concerns into our core businesspractices, products and services to ensure we stay aligned with the society in which we operate.

It formally acknowledges that we exist to meet the needs of shareholders and to do sosuccessfully in the long-term we must recognisethat society’s values and aspirations are marketforces, where people act on their beliefs asvoters, investors, employees and customers.

Building broader relationshipsBecoming a fully engaged, respectedparticipant in society is about building abroader, deeper set of relationships based on respect, trust and integrity. It’s clearlyunderstanding our purpose in society so thatwe have a framework for making decisions.

We believe a focus on sustainability will giveus a competitive advantage. While investorsand customers, governments and otherstakeholders are increasingly favouring thosecompanies whom they see as truly sustainable,we also believe sustainability has the potentialto create new value for shareholders through:

> increasing staff engagement and satisfactionleading to higher productivity and commitmentto ANZ’s success

> growing market share as a result of improvedbrand strength and customer satisfaction

> gains in productivity and lower costs throughimproved environmental, health and safety performance

> improving our lending risk profile throughsuperior understanding of social andenvironmental risks

> enhancing corporate governance by ensuringsystematic transparency and accountabilityin all aspects of our business.

A View from the CEO on Creating SustainableBusinesses

Deliveringsustainableperformanceand value

15

It is not a radical concept. It is why we take timeeach year in our Annual Report to explain not onlyour annual financial results but to report on whatwe are doing for staff, customers and thecommunity we serve.

Integrating sustainabilityThis more formal approach to sustainability,however, involves integrating the concept ofdelivering value to a broad range of stakeholdersinto our business strategies and the way weoperate, and to begin creating greater alignmentbetween the interests of shareholders and thoseof society, and to report transparently on ourprogress. It will mean seeking help from andcreating new relationships with groups from awide cross-section of society.

It is the focus on these themes that will allow usto continue to create value and to ensure ANZ isa leading company today and in 20 years time.

John McFarlaneChief Executive Officer

Sep 98

0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

$22

Market expectations of future performance determine our current share price

$17.95

$9.02

Tangible net assets per share

$4.98

Expected future economic value added

$4.04

$7.49

$10.46

Compound growth 9%

Tangible net assets per share

Expected future economic value added

> Unique strategy> Sustainable leadership> Growth opportunities

> Strong brand> Talented people> Vibrant culture

Compound growth 21%

Sep 03

Serving different stakeholders

Shareholders own ANZ and appoint directors, therefore the directors’ focus is on shareholders

Directors have a duty to act in the best interests of ANZ

Sustainable performance…Growing acknowledgement that to protect the long-term value of ANZ, the needs of our customers, people, shareholders and community must be addressed

On 24 October 2003, ANZ announced it hadreached agreement with Lloyds TSB to acquireTheNational Bank ofNew Zealand for $4.915billion at exchange rates on 23 October 2003.

New Zealand’s best bankThe National Bank of New Zealand is one ofNew Zealand’s leading banks with net loansand advances of NZ$35 billion representingaround 23% of industry lending. It has strongmarket share in personal, rural, and smallbusiness banking including a national networkof 160 retail branches and 260 ATMs.

The National Bank of New Zealand alsoenjoys consistently high customer and staffsatisfaction levels. In the year to September2003, The National Bank of New Zealandmaintained its top position in the ACNielsenConsumer Finance Monitor with 71% of personalcustomers rating its service as excellent or verygood. This is coupled with leading levels of staffsatisfaction (85%).

The National Bank of New Zealand’s trackrecord of value creation is based on anefficient operating model, strong revenuegrowth with sound credit quality and high levelsof staff and customer satisfaction driven by astrong and experienced management team.

A strong existing businessANZ of course already has a strong business inNew Zealand that dates back to 1840. Today,ANZ has established its position among the topfive banks in New Zealand with over one millionpersonal customers and a leading position incorporate banking.

We have also taken a number of steps toinvigorate our existing business in New Zealandincluding more autonomy for New Zealandmanagement and a series of initiatives to improvecustomer satisfaction including introducing newproducts, opening branches and re-organisingour approach to personal banking.

Strategic milestoneThe acquisition is a significant strategicmilestone for ANZ. It is part of ANZ’s strategy todevelop leading positions in growth businessesin its home markets and clearly establishes ANZas New Zealand’s largest bank. It also reflectsour long-term confidence in New Zealand’seconomic prospects.

A different acquisitionFollowing completion of the acquisition of TheNational Bank of New Zealand in December2003, our combined business in New Zealandwill contribute as much as 30% of earnings in future years. Naturally, the significance of ourbusiness and of our presence in New Zealandwill necessitate a very different approach tothinking about our business in New Zealand, ourcustomers, staff and our role in New Zealand asthe largest provider of banking services.

We have already stated the acquisition willbe very different – one based on improvingcustomer service, satisfaction and growth.ANZ intends that both the ANZ and TheNational Bank of New Zealand brands, namesand branch networks will be retained for theforseeable future. By working together withThe National Bank of New Zealand andfocusing on the interests of our customers,staff and the community we can create a betterorganisation in the future for New Zealand andfor shareholders.

The National Bankof New Zealand

16

17

An acquisitionbased oncustomersatisfactionand growth

Sally Morgan enjoysthe flexibility ofworking part of herweek from home.This is another wayANZ is committed to life balance for its people

.

People 18

19

Better organisational leadership, talent and avibrant culture results in better performance forshareholders. It’s a big statement, but globallycompanies rated as being leaders in theirpeople practices produce, on average,significantly higher returns to shareholders thanindustry peers. It is easy then to understandwhy we have consistently placed so muchemphasis on creating a unique ANZ culture thatengages and involves everyone in the company.

Real progressWe survey all of our staff twice yearly to measureour progress. In 2000, when we started theprocess of systematically developing our cultureas a unique and competitive asset as part of ourspecialisation strategy, only 52% of staff weresatisfied working for ANZ. The top 10 values ofmanagement included bureaucracy, hierarchy,control and short-term focus.

Through the programs we have put in place,staff satisfaction now stands at more than 80%,and the values of the past have been replacedby customer focus, achievement, accountabilityand continuous improvement.

These programs involve our people at all levels.They help foster diversity, create opportunities,encourage ongoing learning through trainingand education, promote a healthy life balanceand build a distinctive culture. They aredesigned not only to nurture individual talentbut also to develop ANZ as an organisationbest able to meet the needs of customers,shareholders, staff and the community.

Cultural transformationSince 2000, over 13,000 of our peoplehave participated in a cultural transformationprogram called Breakout. Breakout emphasisesleadership, diversity, coaching and development.This program reflects today’s reality thateveryone in the organisation has to be a leader,whether it is at the moment of contact with thecustomer or at the moment of a decision in theirday-to-day role.

Creating opportunitiesTo support this transformation, we havedeveloped opportunities for our people toenrich their careers at ANZ and provide thenecessary skills required to meet businessneeds. For example, the Opportunities@ANZinitiative provides information and resourcesfor staff to develop their careers through shortand long-term job placements and professionaldevelopment programs.

We have made significant progress instrengthening our talent identification and this has profoundly improved the quality ofleadership succession, creating opportunitiesfor our talented people as well as bringing infresh talent from the market.

We are fostering diversity within ANZ through the establishment of diversity forums within our specialist businesses. Representation of females in ANZ management roles is aboveaverage for the banking and finance industry andwe are incrementally increasing representation– over 31% of middle management rolesare currently held by women. In executivemanagement, almost 17% are women and by 2005 our expectation is that women willfill 20% of executive roles.

Health and safetyANZ has a strong commitment to the health,safety and well-being of our people. We arecontinuously improving our managementsystem aligned with regulatory standards andannual external audit review. All reportedinjuries continue to trend downwards with a28% reduction in the incidence rate per 1000staff since 2000 in Australia and New Zealand.Recognising the importance of personalwellness we are actively looking at innovativeways to improve the overall well-being ofour people.

ANZ is a people and values orientedorganisation with a shared vision of becoming quite a different companyand realising the ability for each person tocontribute their very best. By doing this wecreate sustainable value for our shareholders,staff and the community we serve.

A more vibrantculture createsvalue forshareholders

2003200220012000

Staff satisfaction continues to rise ANZ overall satisfaction

20%

0%

50%

75%

100%

Australia and New Zealand staff

30

20

40

50

60

10

0

2003200220012000

28% reduction in reported injuries since 2000 All reported injury incidence rate per 1000 staff

managerssenior managersexecutives

ANZ expects to have 20% of executive positions held by women by 2005

15%

0%

20%

35%

25%

30%

10%

5%

2000 2001 2002 2003

The first step towards change is knowing thatyou need to change.

During the 1990s, ANZ followed most other banksin Australia. We introduced electronic transactionchannels and reduced the size of our branchnetwork. We improved our pricing disciplines andworked hard to reduce our processing costs. At thesame time, we invested in the development ofleading retail products. Our growth in creditcards and mortgages is evidence of our successin building strong specialist product businesses.

In financial terms, this strategy was verysuccessful for shareholders. But it was notsustainable for customers or the community. By closing branches we damaged our reputationwith the community and reduced our ability totalk to our customers about their needs and howwe could help meet them. Ultimately, a declinein staff and customer satisfaction will translateinto lower returns for shareholders.

We knew we had to change.

Re-energising our businessThe first decision we took, in 2000, was to stopclosing branches in rural Australia. This decisionremains in place and, in the past 12 months, wehave started to open new branches and add moreATMs. Being present where our customers wantus to be is a core part of our strategy – it is partof putting “retailing” back into retail banking.

Last year, we went one step further andestablished a program to reconnect with local communities. We did this by devolving our personal banking business into small,community-based businesses, each with a Local CEO in charge. Our local teams treat theirbusiness and the customers as their own. Theyhave their own profit and loss statement andincreasingly share in the local results they create.

In our Rural Banking business, the local businessmodel is best established. Here, our localteams look after all customers that live in thecommunity, including personal customers, smallbusinesses and agribusinesses. By giving ourpeople and customers the confidence that ANZwill be there for them come rain or shine, we arebeing rewarded with higher productivity andmore business.

Investing in branchesTo deliver a professional retailing environmentwe need to invest in our branch network. Duringthe year, we have refurbished more than 100branches and increased the focus on salestraining and merchandising. We have developeda new telling platform, which will be rolled outto all branches in the 2004 financial year.

This strategy of investment and growth hasre-energised our network and our people.Things have started to change.

The market is recognising our progress. In 2003,Personal Investor magazine named us BankingInstitution of the Year, Savings Institution of theYear and Agri Lender of the Year in Australia.

Winning new customersWe are confident the investments we are making in our product businesses and indistribution will translate into higher customersatisfaction and market share. We continue to grow our credit card and mortgagebusinesses, and in the last 18 months, wehave made good progress in building ourposition in transaction banking and deposits.In 2002, we introduced two new, lower costtransaction accounts and, since then, wehave added approximately 100,000 newcustomers to ANZ.

We have also improved access to bankingservices for those on low incomes andpensions. Our Access Basic Account provideseffectively fee-free banking for customerswith a health care card.

Personal and Rural Customers Getting on

with a newapproach

20

Acting to fix problemsMeanwhile, we know that things don’t alwaysgo the way we plan. And when they do gowrong, we sometimes take too long to fix theissues for our customers. Addressing this hasbecome a top priority.

We have started by setting ourselves targetsaround problem and complaint resolution, andmade these part of our Customer Charter.We have appointed a Customer Advocate toensure that more protracted complaints areresolved fairly, and that we report each year onour progress.

We are also trying to improve the understandingof financial services in Australia. We have taken the lead by commissioning Australia’sfirst comprehensive study on financial literacy,supported by a range of initiatives to assistcustomers with their financial literacy needs(see page 26).

Anyone who has stood in a queue, waited forsomeone to answer the phone or thought aboutapproaching a competitor after a poor experienceknows we still have much to do. We mustmake the transition if we are going to create a sustainable business for our shareholders,customers and the community we serve.

The strategy for our Personal Banking businessis simple. Our aim is to provide our customerswith market leading products, reliable serviceand someone local to turn to. It’s about beingthe “bank with the human face” and being easyto do business with; part of our journey towardshaving the customer at the centre of everythingwe do.

21

Dairy farmer, Mark Disisto,finds ANZ’s flexiblefinancial solutionsmeet his personaland business needs

We aim to answer all customer calls quickly – percentage of calls answered within 1 minute100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Oct

02

Nov

02

Dec

02

Jan

03

Feb

03

Mar

03

Apr

03

May

03

Jun

03

Jul 0

3

Aug

03

Sep

03

13 13 14 Enquiries 13 22 73 Credit Card Enquiries

We are aiming to serve customers in our branches within five minutes – average queue wait times are low*

0.00

Sep 03

Aug 03Jul 03

Jun 03

May 03Apr 03Mar 03Feb 03Jan 03

Dec 02Nov 02Oct 02

0.50 1.00 1.50 2.00 2.50

Minutes*Based on mystery shopping survey

2000 2001 2002 2003

ATMs 1,045 1,074 1,127 1,192

We’re improving access by adding ATMs

Points of ATM access

Ray’s Outdoors hasgrown from a smallGeelong-based retailstore to a 17-locationoperation. Ray Frost,Managing Director, has made his dream a reality – ANZ hasbeen there to assist

Business Banking 22

23

ANZ has a traditional strength in providingbanking services to businesses and largeinstitutions. We measure that by market share,by the depth of our relationships and thefinancial performance of our businesses. In 2003, ANZ was the leading bank to 26% of large corporations in Australia and in themiddle corporate market we are the primarybanker to 29% of businesses.

We regularly check what our clients think of usthrough market research and this year, of themajor Australian banks, ANZ has again ratednumber one in overall client satisfaction amongthe corporate and institutional market.

This isn’t something we take for granted.Businesses are demanding in the service theyexpect. Maintaining our leadership positionrequires continuous focus on understanding ourclients’ business, providing them with creativeideas and solutions, and delivering specialistproducts and services to meet their needs.

Specialist clients focusDuring the 1990s, we lost sight of the fact thatthe small to medium enterprise (SME) sectoralso valued this focus rather than a one-size-fits-all approach. As a result, we lost valuableclients and market share. Our specialisationstrategy helped us remember and since 2000we have established a new strategy with newgoals for SME banking. We focused on creatinga new proposition for clients based ondeveloping our people, creating a sales andservice focus and giving greater autonomy toour account managers to listen to and workwith clients to meet their needs.

Three years later, the results are plain to see.Client satisfaction has improved and we arenow equal with the best of the major banks. We plan to do better. Staff satisfaction hasrisen from just 30% in 2000 to 80% in 2003.Importantly, we have grown our market sharesignificantly above system growth whilecarefully managing risk. We have turned a business in decline into one of ANZ’sfastest growing businesses. It’s the power of specialisation and creating a specialistfocus on customers.

New specialist productsSpecialisation in our investment bankingproduct businesses of Trade and TransactionServices, Capital Markets, Foreign Exchange,Structured Finance and Corporate Financing and Advisory has also enabled us to extend our range of investment banking solutions. Forexample, ANZ’s Corporate Portal provides clientswith a range of online services including foreignexchange, capital markets and trade financetogether with financial decision-making tools.

We have continued to extend the product rangeavailable to medium-sized corporates throughour “Wall Street to Main Street” proposition. We are also using this experience to developnew and innovative products for our small tomedium enterprise clients.

Building on the strength of our businessbanking franchise through specialisationcreates a powerful force that continues to allow us to explore opportunities to reshape the business around client needs and createnew growth opportunities.

ANZ is ratednumber one in clientsatisfaction

ANZ leads Corporate Banking customer satisfaction*8

7.5

6.5

7

2002 2003200120001999199819971996

*Source – Roberts Research 1996-2003

Total customers Significant r’ships Lead r’ships

80%

0%

20032001 2002

Institutional customer relationships –we have the largest market share in Australia*

70%

30%

69%

61%59%

42%

71%

64%

37%

70%

60%

50%

40%

30%

20%

10%

*Source – Greenwich and Associates 2003

DepositsNet loans & advances

We are growing from an underweight position in Small to Medium Enterprises – Funds under Management growth$8b

27% 12%$6b

$4b

$2b

$0b

Sep 02 Sep 03

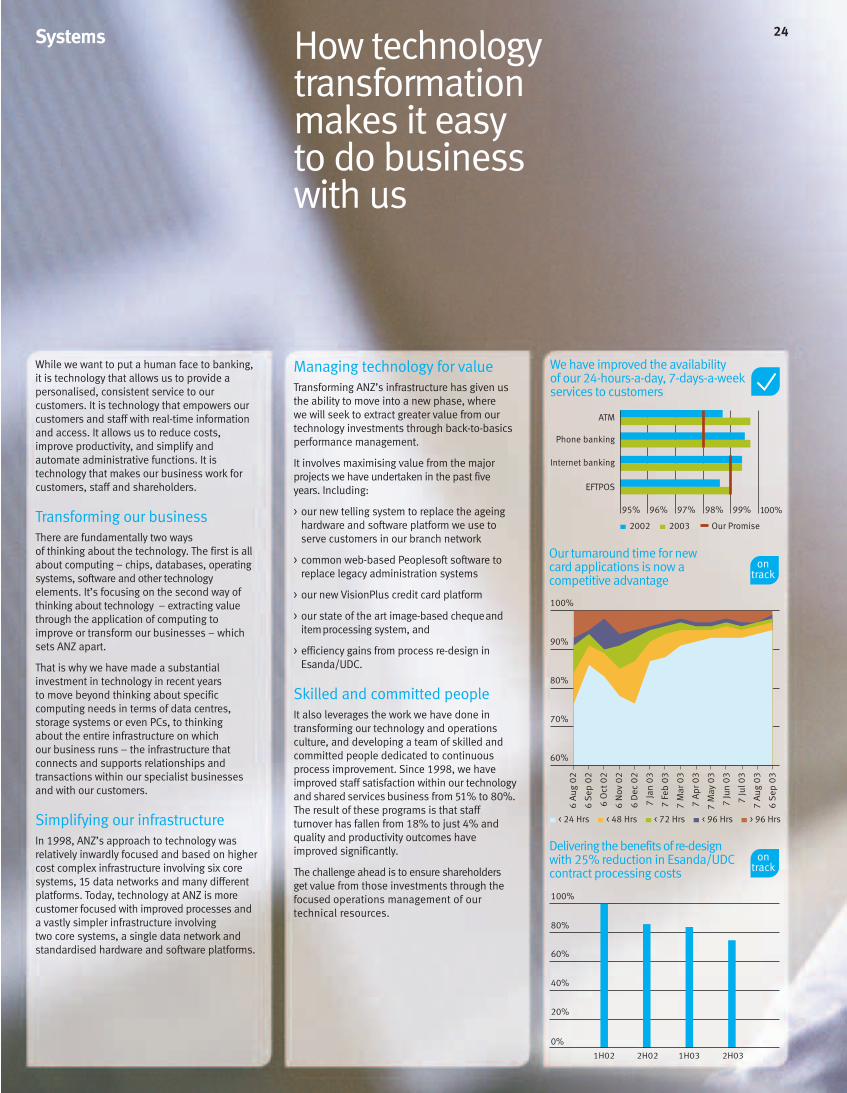

While we want to put a human face to banking,it is technology that allows us to provide apersonalised, consistent service to ourcustomers. It is technology that empowers ourcustomers and staff with real-time informationand access. It allows us to reduce costs,improve productivity, and simplify andautomate administrative functions. It istechnology that makes our business work forcustomers, staff and shareholders.

Transforming our businessThere are fundamentally two waysof thinking about the technology. The first is allabout computing – chips, databases, operatingsystems, software and other technologyelements. It’s focusing on the second way ofthinking about technology – extracting valuethrough the application of computing toimprove or transform our businesses – whichsets ANZ apart.

That is why we have made a substantialinvestment in technology in recent yearsto move beyond thinking about specificcomputing needs in terms of data centres,storage systems or even PCs, to thinking about the entire infrastructure on which our business runs – the infrastructure thatconnects and supports relationships andtransactions within our specialist businessesand with our customers.

Simplifying our infrastructureIn 1998, ANZ’s approach to technology wasrelatively inwardly focused and based on highercost complex infrastructure involving six coresystems, 15 data networks and many differentplatforms. Today, technology at ANZ is morecustomer focused with improved processes anda vastly simpler infrastructure involving two core systems, a single data network andstandardised hardware and software platforms.

Managing technology for valueTransforming ANZ’s infrastructure has given usthe ability to move into a new phase, where we will seek to extract greater value from ourtechnology investments through back-to-basicsperformance management.

It involves maximising value from the majorprojects we have undertaken in the past fiveyears. Including:

> our new telling system to replace the ageinghardware and software platform we use toserve customers in our branch network

> common web-based Peoplesoft software toreplace legacy administration systems

> our new VisionPlus credit card platform

> our state of the art image-based chequeanditemprocessing system, and

> efficiency gains from process re-design inEsanda/UDC.

Skilled and committed peopleIt also leverages the work we have done intransforming our technology and operationsculture, and developing a team of skilled andcommitted people dedicated to continuousprocess improvement. Since 1998, we haveimproved staff satisfaction within our technologyand shared services business from 51% to 80%.The result of these programs is that staffturnover has fallen from 18% to just 4% andquality and productivity outcomes haveimproved significantly.

The challenge ahead is to ensure shareholdersget value from those investments through thefocused operations management of ourtechnical resources.

Systems How technologytransformation makes it easyto do businesswith us

24

60%

70%

80%

90%

100%

6 A

ug 0

2

6 S

ep 0

2

6 O

ct 0

2

6 N

ov 0

2

6 D

ec 0

2

7 Ja

n 0

3

7 F

eb 0

3

7 M

ar 0

3

7 A

pr 0

3

7 M

ay 0

3

7 Ju

n 0

3

7 Ju

l 03

7 A

ug 0

3

6 S

ep 0

3

< 24 Hrs < 48 Hrs < 72 Hrs < 96 Hrs > 96 Hrs

Our turnaround time for new card applications is now a competitive advantage

1H03 2H032H021H02

Delivering the benefits of re-designwith 25% reduction in Esanda/UDC contract processing costs

0%

100%

80%

60%

40%

20%

We have improved the availability of our 24-hours-a-day, 7-days-a-week services to customers

2002 2003 Our Promise

Phone banking

Internet banking

EFTPOS

ATM

100%99%98%97%96%95%

25

Anastasia Bakolias –a Customer ServiceConsultant at ANZ’sCall Centre – deliversdistinctive customerservice every day

Partnering on financial issuesWe have also developed responses to some ofthe major social issues that involve the financialservices industry. These issues include financialliteracy and the low level of national savings.

During the year, ANZ commissioned and publishedthe results of the first national survey of adultfinancial literacy. For the first time, the researchprovides benchmarks for the measurement offinancial literacy across the Australian population.It also identifies aspects of financial productsand services that are causing the greatest problemsfor consumers and those segments of thepopulation that are struggling with financial skills.

ANZ has committed to improve financialliteracy in Australia, particularly among itsown customers. We are integrating the learningsfrom the survey into our business operations,training our people so they can identify andassist customers facing financial difficulty andestablishing a community partnership to developan adult education program.

This year, we have trained over 3,500 serviceconsultants in branches throughout Australiaand introduced a booklet titled “Kick-start yourfinancial fitness” to help people who want to useand manage their money more effectively. OurConsumer Finance business has also developeda website and series of brochures to assistcustomers and the community to betterunderstand how credit works.

In partnership with the Brotherhood of StLaurence, we have also introduced Saver Plus –Australia’s first matched savings program. It encourages families on lower incomes toregularly and consistently save for costs associatedwith their child’s secondary schooling.Participants will also receive financial educationtraining. The Saver Plus pilot aims to help 300Australian families on lower incomes reach asavings target and encourage or establish asavings habit.

Thefirst Saver Pluspilot commenced in Frankston,Victoria. ANZ and the Brotherhood are nowworking with Berry Street Victoria and TheBenevolent Society to conduct further programsin Shepparton, Victoria, and Campbelltown, New South Wales.

Rebuilding community trust begins withrecognising that our standing in the communityis as important to our future as ourrelationships with customers and staff.

We know that many in our society believe bankshave become increasingly detached from thecommunity. Many of the actions which fosteredthat view arose out of a focus on short-termshareholder value. This undermined customerfaith and public trust and diminished the pridestaff felt in working for us.

Strengthening local communitiesRebuilding community trust is about acting with fairness and integrity. Contributing to the health of local communities can also play a role.

Recognising this, the ANZ Community Fund pilot was developed to offer our frontline staffthe means to work with their communities toidentify local issues and provide local solutions.With over 120 projects supported aroundAustralia in the past financial year, the ANZCommunity Fund will be extended to all brancheswith an annual commitment of $1.6 million.

ANZ Community Fund – supportinga variety of local projects

Tamara Lovering fromANZ Kingscote, SouthAustralia, and JimGorman from KangarooIsland Food Group,support an ANZCommunity Fund activity– packing food parcelsfor people in need

Communityand Environment Why broadening

our thinkingabout thecommunityis important to all our futures

26

Youth Education Community development

20%

18%

10%

30%11%

4%7%

DroughtMedical OtherIndigenous

27

Changing environmental impactsANZ also believes that it has an obligation to shareholders and society to operate as efficiently as possible to reduce itsenvironmental impacts. It is part of being a well-managed business. This includes ourdirect impacts – the resources we use incarrying out our operations such as energy,paper and travel, and our indirect impacts –such as the impacts of our customers towhom we lend and invest in.

In 2003, ANZ undertook a thoroughassessment of its environmental impacts andexamined its performance in managing thoseimpacts against some of its internationalpeers. We also consulted and engagedour staff and community groups on howimprovements can be made to reduce bothour direct and indirect impacts.

Improving our performanceBuilding on ANZ’s existing programs we haveundertaken a number of new initiatives toassist in managing our direct impacts. These include:

> appointing a full-time environmental managerto coordinate activities and develop oursystems

> examining our supply chain and assessingways to integrate environmental criteria intoour purchasing decisions

> developing a set of corporate improvementtargets and specific initiatives to meet these

> continuing to work on achieving ourcommitments to the Federal Government’sGreenhouse Challenge program

> becoming a signatory to the United NationsEnvironment Programme Finance Initiatives andengaging a range of external stakeholders

> reviewing our existing environmental lendingpolicy and procedures

> engaging ANZ’s external auditor to review ourdata measurement systems and verify theenvironmental baseline we established.

Further details on ANZ’s environmentalprogram and performance can be found at www.anz.com/sustainability.

New lending opportunitiesSustainability also creates new lending andinvestment opportunities. During the past year,a number of business units have been exploringthe demand for new “green” lending products.ANZ’s Infrastructure Services business has beenactive in the renewable energy area and hasrecently partnered with Spain’s EHN to pursuenew wind power opportunities in Australia. Our International Structured Finance businessis also pursuing new lending opportunities inthe growing renewable energy market in Europe.

28Leadership Transformingour financialperformanceand culture

When we created ANZ’s specialisation strategyin 2000, we knew that it would only work if wecreated a very different approach to leadershipand culture.

We recognised that the one-dimensional conceptof leadership – the person at the top whom others follow – disappeared 20 years ago. AtANZ, everyone in the organisation has to be aleader. We have brought this about by creating an environment where leadership can be fosteredacross all levels in the Group.

Business leaders within ANZ shape the destinyand nature of their business. They build itscapability to grow, they improve its effectivenessand they ensure the delivery of results. Our newleaders are at all levels of the organisation: thepeople at the moment of contact with ourcustomers or those at the moment of decisionwho are accountable for that decision.

Our approach to leadership is to foster anenvironment where people have the freedomand responsibility to achieve more than theythought they could. This is turning our culture into a unique competitive asset.

Bob EdgarChief Operating Officer

John McFarlaneChief Executive Officer

Peter MarriottChief Financial Officer

Peter HawkinsGroup Managing Director, Group Strategic Development

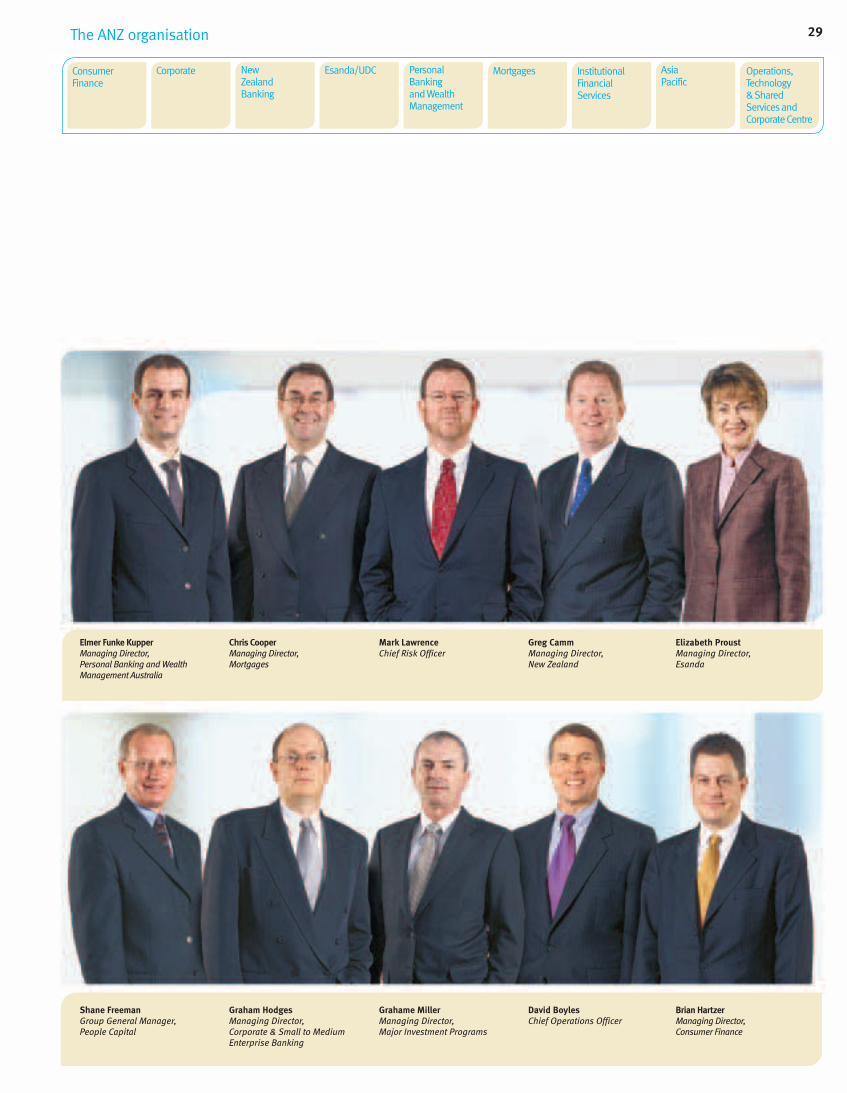

29

ConsumerFinance

Corporate NewZealand Banking

Esanda/UDC MortgagesPersonal Banking and Wealth Management

Institutional Financial Services

Asia Pacific

Operations, Technology & Shared Services and Corporate Centre

The ANZ organisation

Shane FreemanGroup General Manager, People Capital

Graham HodgesManaging Director, Corporate & Small to MediumEnterprise Banking

Grahame MillerManaging Director, Major Investment Programs

David BoylesChief Operations Officer

Brian HartzerManaging Director, Consumer Finance

Elizabeth ProustManaging Director,Esanda

Greg CammManaging Director, New Zealand

Mark LawrenceChief Risk Officer

Elmer Funke KupperManaging Director,Personal Banking and WealthManagement Australia

Chris CooperManaging Director,Mortgages

30

New Zealand BankingGreg Camm, Managing Director New Zealand Banking

NZ Banking provides banking services, includingwealth management, for personal, small businessand corporate customers in New Zealand throughbranches, call centres, relationship managers andonline banking.

Staff satisfaction 88% (up from 83% in 2002)

$m 2003 2002 %

Operating income 538 490 10

Operating expenses -314 -281 12

Provisions -13 -13 0

Profit before tax 211 196 8

Income tax expense(A) -70 -65 8

Net profit 141 131 8

Cost to income ratio (CTI) 58.4% 57.3% 2

Staff (FTE) 2535 2371 7

Performance

Profit – Increased 8% driven by an appreciation inthe New Zealand dollar. Excluding the exchange rateimpact, profit was flat. This was due to flat feegrowth as we improved the competitiveness of ourproduct ranges; and increased frontline branch staffnumbers to improve customer service.

CTI – Increased by 2%, reflecting the investment infrontline staffing as part of the Restoring CustomerFaith program in Personal, and increasing capacityin Business and Rural.

Risk Management – Credit quality remains soundwith provision for doubtful debts charge falling 5%(in local currency terms) despite solid lending

Business Profiles

CorporateGraham Hodges, Managing DirectorCorporate and Small to MediumEnterprise Banking

Corporate comprises two businesses: Small toMedium Enterprises Australia (SME), whichprovides banking services for businesses withturnover up to $10 million; and Corporate BankingAustralia, which manages customer relationshipsand develops financial solutions for businesseswith turnover $10 million to $100 million.

Staff satisfaction 85% (7% improvement on 2002)

$m 2003 2002 %

Operating income 653 604 8

Operating expenses -219 -212 3

Provisions -48 -46 4

Profit before tax 386 346 12

Income tax expense(A) -116 -104 12

Net profit 270 242 12

Cost to income ratio (CTI) 33.5% 35.1% -5

Staff (FTE) 1597 1487 7

Performance

Profit – Increased by 12% with net interest incomegrowth of 9% due to strong volumes in bothdeposits and lending. Business growth resultedfrom an increased geographical presence, a focuson industry specialisation and stronger salesdisciplines.

CTI – Decreased as efficiency of the businesscontinues to improve.

Risk Management – Overall portfolio risk profileremains strong. Provision for doubtful debtsincreased 4% against a 19% growth in lendingvolumes. However, net specific provisions rose16% in 2003 largely reflecting problems with two

Esanda/UDCElizabeth Proust, Managing DirectorEsanda

Esanda/UDC delivers motor vehicle andequipment finance; equipment operating leasesand management services; fleet managementservices; and investment products through Esanda(Australia), Esanda FleetPartners (Australia & NewZealand) and UDC (New Zealand) and SpecialisedAsset Finance (Australia).

Staff satisfaction 79% (up from 77% 2002)