20 june 2013 prism cement limited - iias: india's leading ... · voting advisory june 2013...

TRANSCRIPT

Voting Advisory

June 2013 Prism Cement Limited 1|P a g e

20 June 2013 Prism Cement Limited Company Profile BSE: 500338 | NSE: PRISMCEM ISIN: INE010A01011 Industry: Cement Index: S&P BSE 500/ CNX 500 Face Value: Rs. 10.0 Mkt Price: Rs. 36.0 Fiscal Year End: March

Promoter Rajan Raheja, family and group companies

Financials Particulars FY13 (Rs. bn)

Total Income 47.7

Net Worth 10.9

Equity Capital 5.0

Market Cap. 19.5

Overview

52 week H/L(Rs.) 60.0-35.8

Current P/E(x) [s] Negative

Current P/B(x) [s] 1.8

Source: IiAS Research, Market sources [s]Standalone;

Write to us Institutional Investor Advisory Services 15th Floor, West Wing, PJ Tower Dalal Street, Mumbai -400 001 Email: [email protected] www.iias.in

Annual General Meeting (AGM) Meeting date : 25 June 2013, 11.30 am

Proxy deadline : 23 June 2013, 11.30 am

Notice date : 9 May 2013

Meeting venue : Taj Mahal Hotel, 4-1-999, Abids Road, Hyderabad – 500001.

Company overview Prism Cement Ltd (PCL), part of Rajan Raheja Group, is an integrated building material company. The company has three divisions’ viz., Prism Cement, H & R Johnson (India), and RMC Readymix (India). The cement division operates two units, both in Satna, Madhya Pradesh (MP) with a combined installed capacity of 5.6 million tons per annum (mtpa). The H & R Johnson (India) division manufactures tiles, bath fittings and kitchens under brands Johnson, Marbonite and Endura. The RMC Readymix (India) division manufactures and markets ready-to-mix concrete.

Agenda Items

# Type* Description of resolution IiAS

Recommendation Indicators See Legend

1 O To adopt FY13 financial statements See Analysis

2 O To reappoint Rajesh G Kapadia as director AGAINST G M R S T V

3 O To reappoint Akshay R Raheja as director FOR

4 O To reappoint Ms. Ameeta A Parpia as director FOR

5 O To reappoint N M Raiji & Co. as statutory auditors and fix their remuneration

AGAINST G M R S T V

6 S To reappoint Vijay Aggarwal as a Managing Director (MD) and fix his remuneration

AGAINST G M R S T V

7 S To reappoint Ganesh Kaskar as an Whole-time Director (WTD) and fix his remuneration

AGAINST G M R S T V

8 S To approve payment of commission to non-executive independent directors (IDs)

AGAINST G M R S T V

*O/S: Ordinary/Special Executive Summary (click on respective link for detailed analysis)

Accounts For FY13, although PCL’s total income increased by nearly 6% to Rs 47.7 bn, Its EBIDTA was flat at Rs 2.7 bn though its margins declined by 0.3% to 5.7%. PCL’s loss before tax increased to Rs 0.8 bn from loss of Rs 0.5 bn and net loss to Rs 0.6 bn from Rs 0.3 bn in FY12 respectively.

Board Appointments

PCL’s board comprises nine directors, of which, three are executive and the remaining six are non-executive directors. Of the six non-executive directors, PCL classifies three as independent viz. Akshay R Raheja, Ms. Ameeta A Parpia and Rajesh G Kapadia. IiAS classifies Rajesh G Kapadia, Chairman, as non-independent given his association with four group companies. Given Rajesh Kapadia’s reclassification as non-independent, the company is not in compliance with the ratio of independent and non-independent directors specified in clause 49.

We recommend voting FOR the reappointment of Akshay R Raheja and Ms. Ameeta A Parpia and AGAINST Rajesh G Kapadia.

Remuneration PCL seeks shareholders’ approval to reappoint Vijay Aggarwal as the MD and Ganesh Kaskar as a WTD and fix their remuneration. The company has stated that all executive directors, in aggregate, will be paid upto 10% of net profits as remuneration. No detailed breakup of the salary components have been provided for either director, which makes the structure open ended. We recommend voting against the resolution and advise shareholders to seek further clarifications from the management regarding the proposed compensation structure for Vijay Aggarwal and Ganesh Kaskar i.e. fixed, perquisite value, incentive linked pay and retirals.

Auditor N M Raiji & Co. have been the statutory auditors of the company over 19 years. We recommend voting AGAINST their reappointment given their extended association with the company.

Commission to non-executive directors

PCL proposes to pay commission of upto 1% of its net profits, in aggregate, to all its non-executive independent directors for a period of five years commencing 1 April 2013. Investors should note that the commission paid to ID’s is open ended and without an overall cap. Further, the company may seek approval once it starts earning profits. We recommend voting AGAINST the resolution.

75.0% 3.0%

1.0%

21.0%

Promoter DII FII Others

Voting Advisory

June 2013 Prism Cement Limited 2|P a g e

Financial Performance (standalone) Segment Revenue (consolidated)

Particulars (Rs. bn)

FY11 FY12 FY13

Total income 33.9 45.1 47.7

EBIDTA 3.3 2.7 2.7

EBIDTA margin (%) 9.7 6.0 5.7

PBT 1.3 (0.5) (0.8)

PBT margin (%) 3.8 Negative Negative

PAT 0.9 (0.3) (0.8)

PAT margin (%) 2.7 Negative Negative

EPS (Rs.) 1.8 Negative Negative

ROANW (%) 7.6 Negative Negative

ROACE (%) 6.1 3.8 3.4

Debt/EBIDTA (x) 1.0 0.9 1.2

Source: Company filings

Outer ring represents FY13 data: Total op. income Rs 48.4 bn Inner ring represents FY12 data: Total op. income Rs 45.7 bn

Public Shareholding > 1% holding Sr. No.

Name of shareholder

Shares held (million)

Holding as %age of total

1 Prism Trust 12.3 2.45

2 HDFC Standard Life Insurance Company Ltd 8.6 1.70

3 Regal Investment & Trading Co Pvt Ltd M/s Zash Investment and Trading Co Pvt Ltd

6.1 1.21

4 ICICI Prudential Discovery Fund 6.0 1.19

5 Reema Business Services Pvt Ltd 5.6 1.11

6 Napean Trading & Investment Co Ltd Tarish Investment And Trading Co Pvt Ltd

5.5 1.10

Total 44.1 8.77

Source: BSE filings

Change in Shareholding Pattern (%)

Year Promoter FII DII Others

Mar-13 74.9 1.0 3.0 21.1

Dec-12 74.9 1.0 3.3 20.8

Sep-12 74.9 1.4 3.1 20.6

Jun-12 74.9 1.3 3.1 20.7

Mar-12 74.9 1.3 3.2 20.6

Mar-11 74.9 6.3 1.1 17.7

Mar-10 74.9 4.4 0.8 19.9

Mar-09 61.7 4.3 0.1 33.9

Mar-08 61.7 5.3 0.6 32.4

Source: BSE

Price Performance

3 Yrs: 13 June 2010 to 13June 2013 5 Yrs: 13 June 2008 to 13 June 2013 Source: BSE

3 Yrs 5 Yrs -31%

4% 12%

18% 13%

21%

3 YR 5 YR

PCL S&P BSE 500 CNX 500

37%

38%

25% 39%

38%

23% Cement

Tiles, Bath andKitchen fittings(TBK)

Ready-MixedConcrete (RMC)

Voting Advisory

June 2013 Prism Cement Limited 3|P a g e

Category: Accounts

Financial Performance:

Business Risk Indicators Parameter FY11 FY12 FY13

Cash Flow from Operations/EBIDTA 0.8 0.9 0.9

Contingent liabilities as % of net worth

13.3 19.1 31.1

Secured loans as % of net block 76.2 73.7 105.2

Leverage Profile

Related Party Transactions (RPT) Annual transactions (Rs. bn) FY12 FY13 Comment

Investment 0.2 0.1 Rs 0.1 bn invested in Silica Ceramica Private Ltd. – wholly owned subsidiary of the company

Income from related entities 1.4 2.0 Expenses towards related entities

5.4 6.8

Loan given 0.1 - Outstanding balance (Rs. bn) FY12 FY13 Parameter Assessment

Receivable 0.2 0.3 Outstanding RPT exposure 5.0% of net worth Receivable towards loan and interest

0.4 0.4 Exposure to promoter entities Negligible

Payable 1.1 1.2 Transactions with promoter controlled entities Negligible

Liquidity Position

Parameter Rs. bn

Marketable securities

0.2

Operating cash 2.3

Cash balance 0.3

Audit Integrity Parameter Result

Head of audit committee Independent

Independent directors in audit committee

67%

Tenure of auditor (Yrs) >19

Tenure of audit partner (Yrs) >19

Performance relative to Industry Average

Parameter PCL Peers[1] RONW (%) Negative 6.3 Debt/Equity(x) 1.5 0.9 Interest cover (x)

0.6 2.0

PAT margin (%) Negative 2.0 Current Ratio(x) 0.8 1.2

[1]FY12 data

Accounting Policies Accounting Policy Method adopted 3-yr pattern and impact on P&L

Depreciation Straight Line Method No change

Inventory Weighted Average Method No Change

0.00

2.00

4.00

6.00

5

10

15

FY11 FY12 FY13

Borrowings (Rs.bn) Debt/EBIDTA

Debt/Networth Interest coverage

Resolution 1: To adopt FY13 financial statements

For the year ended March 2013, the total income of the company increased by 6% to Rs 47.7 bn (Rs 45.1 bn). On a consolidated basis, revenue from cement, TBK and RMC increased by 6% to Rs 48.2 bn (Rs 45.5 bn).

During FY13, despite increase in topline, the company’s EBIDTA remained constant to Rs 2.7 bn compared to that of FY12 on account of increased manufacturing expenses and freight charges. In FY13, finance expenses increased to Rs 1.9 bn from Rs 1.6 bn in FY12. PCL’s loss before tax increased to Rs 0.8 bn from Rs 0.5 bn in FY12. Net loss during the year was Rs 0.6 bn (Rs 0.3 bn).

Ratio

s

Rs. bn

Voting Advisory

June 2013 Prism Cement Limited 4|P a g e

Category: Board Composition

IiAS Evaluation Parameters for Board Appointments

Parameter Analysis Risk Level Details

Is the chairman of the board an independent director? No[1] Low Refer Table 1 Is there a separation in the roles between the Chairman and CEO/MD?

Yes - Refer Table 1

Proportion of independent directors on the board 22%[2] Moderate Refer Table 1

Proportion of non-executive directors on the board 67% Moderate Refer Table 1 Does the company have a policy on the retirement age of directors? No Low

Does the company have a policy on the tenure of independent directors?

No Moderate

Do all the board committees have at least one independent director? Yes -

Is there any whistleblower policy for the independent directors? No -

Proportion of promoter representatives on board 33% - Refer Table 1

Overall Moderate [1] Independent as per the company classification [2] 33% as per company classification

Table 1: Board composition

Sl. No

Name of director

Occupation Age

(yrs.) Tenure

(yrs.)

Attendance at board

meetings

Other Directorships

Compensation (Rs.mn)

Executive

1 Manoj Chabra Managing Director 61 9 100% 1 36.2

2 Vijay Agarwal Managing Director 44 3 80% 4 41.8

3 Ganesh Kaskar Whole-time Director 53 3 100% - 18.5

Non-Executive Non-independent

4 Rajan B Raheja [P] Promoter, Rajan Raheja Group 58 19 80% 7 -

5 Satish B Raheja[P] Former Director, Supreme Petrochem Ltd.

49 19 - 3 -

6 Akshay R Raheja [P]

Director, Hathway Cable & Datacom Ltd.

30 7 40% 3 -

7 Rajesh G Kapadia

(Chairman)[1] Chartered Accountant 56 4 100% 7 -

Non-Executive Independent -

8 James Brooks Overseas Development Executive, RMC Group

64 3 80% - -

9 Ms. Ameeta A Parpia

L.L.B Advocate & Solicitor 47 3 80% 2 -

Source: Company filings and IiAS research [P] –Promoter

[1] Classified as independent by the company. Due to his association with four other group companies, IiAS considers him non-independent. For the year ended 31 March 2013, the non-executive directors were paid in aggregate, an amount of Rs 4.5 lakhs as sitting fees.

Resolution 2: To reappoint Rajesh G Kapadia as director

Resolution 3: To reappoint Akshay R Raheja as director

Resolution 4: To reappoint Ms. Ameeta A Parpia as director

IiAS Recommendation: AGAINST

IiAS Recommendation: FOR

IiAS Recommendation: FOR

Seeking reappointment

Voting Advisory

June 2013 Prism Cement Limited 5|P a g e

Table 2: Proposed Appointments – IiAS Checklist

IiAS Director Checklist Rajesh G Kapadia Akshay R Raheja Ms. Ameeta A Parpia

Executive/Non-executive Non-executive Non-executive Non-executive

Category of Appointment Independent Non-Independent Independent

IiAS Director Classification Non-Independent Non-Independent Independent

Independence X N.A.

Tenure N.A.

Attendance X

Other Affiliations

Shares Held NIL 5,576,784 76,000

Qualification

IiAS Recommendation AGAINST FOR FOR

N.A.: Not applicable

Director Profiles Rajesh G Kapadia

Qualification Chartered Accountant

Work experience Long experience in the field of finance and accounts

Committee memberships

Chairman, Audit Committee Remuneration Committee Shareholders Grievance Committee Share Transfer Committee

Other directorships

1. Asianet Satellite Communications Ltd. * 2. Exide Industries Ltd. (L) * 3. EIH Associated Hotels Ltd.(L) * 4. Goldiam International Ltd. (L) 5. Goldiam Jewellery Ltd. 6. ING Vysya Life Insurance Company Ltd. * 7. Raheja QBE General Insurance Company Ltd. *

Akshay R Raheja

Qualification MBA from Columbia Business School, New York

Work experience 10+ years of experience in business management

Committee memberships Audit Committee

Other directorships 1. Asianet Satellite Communications Ltd. 2. Hathway Cable & Datacom Ltd. (L) 3. Raheja QBE General Insurance Company Ltd.

Ms. Ameeta A Parpia

Qualification LL.B Advocate & Solicitor

Work experience Partner of A H Parpia & Company Practicing as a lawyer for last 22 years

Committee memberships

Chairman, Shareholders Grievance Committee Remuneration Committee Audit Committee Share Transfer Committee

Other directorship 1. Raheja QBE General Insurance Company Ltd. 2. Supreme Petrochem Ltd. (L)

(L): Listed companies * Part of Rajan Raheja group Source: Company filings and IiAS research

Voting Advisory

June 2013 Prism Cement Limited 6|P a g e

Discussion

The board of PCL comprises nine directors. Of these, three are executives and six are non-executives. Of the six non-executive directors, the company classifies three directors as independent. We do not consider Rajesh G Kapadia, non-executive chairman of the company, as independent given his association with four group companies. Given his reclassification, the company is not in compliance with Clause 49 of the Listing Agreement, SEBI and the pending Companies Bill, 2012 – hereinafter referred to as ‘Companies Bill’ (refer Box 1) regarding mix of independent and non-independent directors. Box 1: IiAS policy snapshot – minimum number of independent directors Akshay Raheja has attendance of 40% in the board for FY13. In FY11 and FY12 his attendance has been 83%. His average attendance in the board meetings for the last three years is 69% which is less than our recommended threshold of 75%. IiAS does not generally vote against promoter directors on account of attendance in any one year. Given that he is a promoter director we recommend voting FOR his reappointment but expect he will be regular in future. IiAS recommends voting FOR the reappointment of Akshay R Raheja and Ms Ameeta A Parpia. IiAS recommends voting AGAINST the reappointment of Rajesh G Kapadia.

Clause 49 of the listing agreement states that for a company with an executive chairman; at least 50% of the board should comprise independent directors. In the case of a company with a non-executive chairman, at least one-third of the board should be independent. However, if non-executive chairman is a promoter, 50% of the directors have to be independent. Clause 149 (3), Companies Bill, 2012 - Every listed public company shall have at least one-third of the total number of directors as independent directors and the Central Government may prescribe the minimum number of independent directors in case of any class or classes of public companies.

Voting Advisory

June 2013 Prism Cement Limited 7|P a g e

Category: Auditors

IiAS Evaluation Parameters for Auditor Appointment

Parameter Analysis Risk Level

Details

Is the tenure of the auditor firm more than 10 consecutive years? Yes High

Has the audit partner been rotated in the last five years? No High

Does the company have an auditor rotation policy in place? No Low

Is the non-audit to total fees within acceptable limits? Yes - Refer Table 3

Have the audit fees increased consistently? Yes - Refer Table 3

Is there a significant increase in auditor remuneration from the previous auditor?

No - Refer Table 3

IiAS Recommendation AGAINST Source: Company Filings, IiAS Research

Discussion In FY13, N M Raiji & Co. was the statutory auditor of the company with J M Gandhi as the signing partner. The auditor and the audit partner both have been associated with PCL at least for 19 years (since 1995). IiAS believes that to maintain independence, auditors should be rotated every 10 years and the signing partner every five years (refer box 2). For the year ended 31 March 2013. N M Raiji & Co. was paid a remuneration of Rs 7.0 mn, an increase from Rs 6.8 mn paid in the previous year.

Table 3: Auditor’s remuneration Particulars (Rs. in mn) FY11 FY12 FY13

Statutory audit 5.1 5.2 5.5

Tax audits 0.6 0.6 0.5

Total audit fees 5.7 5.8 6.0

Non-audit fees

Certifications/other services

0.3 1.0 1.0

Total non-audit fees 0.3 1.0 1.0

Total fees[1] 6.0 6.8 7.0

Non-audit to total fees (%)

5.0 14.7 14.3

[1]Excludes out of pocket expense

Box 2: Guidelines on auditor appointment

According to clause 139 of the new Companies Bill 2012, an auditor will be permitted to hold office for a five year term and can then be reappointed for another five year term. After two consecutive five-year terms, there needs to be a cooling-off period of five years before subsequent reappointments. When the new Companies Bill is passed into law, audit firms would be allowed to hold office for ten consecutive years. According to IiAS policy, to maintain the independence of auditors – tenure of audit partner should not exceed five years and audit firm should be rotated every 10 years. A cooling period of five years should elapse before the re-appointment of the same audit firm or the audit partner.

IiAS recommends voting AGAINST the resolution.

Resolution 5: To reappoint N M Raiji & Co. as statutory auditors and fix their remuneration IiAS Recommendation: AGAINST

0.3 1 1

5.7 5.8 6

0%

20%

40%

60%

80%

100%

2011 2012 2013

Non-Audit fees (Rs. mn) Audit fees (Rs. mn)

Threshold

Voting Advisory

June 2013 Prism Cement Limited 8|P a g e

Category: Remuneration

IiAS Evaluation Parameters for Managerial Remuneration

Parameter Analysis Risk Level Details

Is the proposed remuneration for a promoter? No -

What is the percentage hike in remuneration from previous term/year?

N.A. -

Is the remuneration commensurate with the growth in profits/operations?

No -

Is the proposed resolution open-ended? Yes Medium

Is there a component of performance-linked pay in the proposed salary?

Yes -

Is the remuneration in line with industry peers? - - Refer Table 4 & 5

Does the person have the requisite qualifications? Yes -

Has the company disclosed a clear remuneration policy to the shareholders?

No -

IiAS recommendation AGAINST N.A. - Not Applicable Source: Company Filings, IiAS Research

Discussion Vijay Aggarwal, 44, is the MD of PCL. He was appointed as the MD on the board of PCL on 3 March 2010 for a period of three years, prior to which he was an alternate director to Satish B Raheja. Since 1998 he was the MD and CEO of the erstwhile H & R Johnson (India) Ltd. before it was merged with PCL. He does not hold any shares in the company. He is a qualified electrical engineer from IIT, Delhi and a post graduate from IIM-A with a long experience in the manufacturing sector. Ganesh Kaskar, 53, is the whole-time director of PCL since 3 March 2010. Prior to his appointment in PCL, he was the CEO of the erstwhile RMC Readymix (India) Private Limited (RMC) since 2001, now merged with PCL. He does not hold any shares in PCL. He has a degree in engineering from IIT, Mumbai. He has almost three decades of experience in civil construction field, of which nearly two decades are in the ready-mixed concrete and building material industry. PCL seeks shareholders’ approval to reappoint Vijay Aggarwal as Managing Director and Ganesh Kaskar as the Whole-time Director for a period of three years commencing from 3 March 2013 and fix their remuneration. Remuneration Policy

The criterion for remuneration remains unchanged for Vijay Aggarwal and Ganesh Kaskar, wherein the annual salary and perquisites shall not exceed 5% of PCL’s net profit in case of one executive director and 10% in case of all the executives together. The directors are also eligible for provident fund, superannuation fund or annuity fund.

If in a given year the company makes inadequate or nil profits the company will pay remuneration by way of salary, perquisites and allowances, not exceeding the limits specified in schedule XIII to the Companies Act, 1956.

Resolution 6: To reappoint Vijay Aggarwal as the Managing Director of the company and fix his remuneration

Resolution 7: To reappoint Ganesh Kaskar as the Whole-time Director of the company and fix his remuneration

IiAS Recommendation: AGAINST IiAS Recommendation: AGAINST

Voting Advisory

June 2013 Prism Cement Limited 9|P a g e

Box 3: Regulation snapshot section 309 (3) of the Companies Act, 1956

A director who is either in the whole-time employment of the company or a managing director may be paid remuneration either by way of a monthly payment or at a specified percentage of the net profits of the company or partly by one way and partly by the other: Provided that except with the approval of the Central Government such remuneration shall not exceed five per cent of the net profits for one such director, and if there is more than one such director, ten percent for all of them together.

However we find that the remuneration paid for FY12 has breached this limit and the company has sought shareholders’ approval for waiver of recovery of remuneration. The company has taken central government’s approval for the excess remuneration of Rs 65.4 mn to be paid to both the managing directors and executive director of the company in the circumstance of non-availability of profits for FY12.

For FY13, remuneration paid to Vijay Aggarwal is Rs 41.8 mn (Rs 33.0 mn) and Ganesh Kaskar is Rs 18.5 mn (Rs 16.9 mn).

Table 4: Remuneration levels across peer companies – Managing Director (MD), Vijay Aggarwal

Sr. No. Company Name Name of director Designation

Total

Remuneration

(Rs. mn)

Total

income

(Rs. bn)

PAT

(Rs. bn)

PAT

margin

(%)

Mkt Cap

(Rs. bn)

Peers based on size

1 Birla Corporation Ltd.

B R Nahar MD 23.7 27.3 2.7 9.9 18.6

2 Prism Cements Ltd.

Vijay Aggarwal MD 41.3 47.7 -0.6 (1.3) 20.1

Others Peers (FY12)

3 Ambuja Cements Ltd.

Onne van der Weijde CEO & MD 37.0 100.8 12.9 12.8 270.9

4 ACC Ltd. Kuldip Kaura CEO & MD 52.8 112.3 10.6 9.4 228.5

Table 5: Remuneration levels across peer companies –Whole-time Director (WTD), Ganesh Kaskar

Sr. No. Company Name Name of director Designation

Total

Remuneration

(Rs. mn)

Total

income

(Rs. bn)

PAT

(Rs.

bn)

PAT

margin

(%)

Mkt

Cap (Rs.

bn)

1 Century Textiles & Industries Ltd.

B L Jain WTD 19.4 48.9 0.2 0.41 26.4

2 Shree Cements Ltd. Mahendra Shingi WTD 55.7 59.9 6.2 10.35 163.4

3 Prism Cements Ltd. Ganesh Kaskar WTD 18.5 47.7 -0.6 (1.3) 20.1

From the above table, we observe that the remuneration paid to MD, Vijay Aggarwal is higher in comparison with the peers in the same industry, whereas the remuneration paid to Ganesh Kaskar is in line with his peers in the industry, and commensurate with the size of the company. However it does not reflect the falling profits of the company. Investors may also note that the while the salary is compared to CEO’s in the cement business, we understand that Vijay Agarwal has day to day responsibility of the H&R Johnson business.

Voting Advisory

June 2013 Prism Cement Limited 10|P a g e

Chart1: Performance v/s Pay

Remuneration paid to directors – Rs mn Net profit and Market cap – Rs bn Source: IiAS research

From the above chart, it is observed that over the period of four years (2010-2013) an increase in the pay to Vijay Aggarwal and Ganesh Kaskar has been inversely related to the growth in market cap and PAT of the company. Remuneration to Vijay Aggarwal has increased at a CAGR of 18% and remuneration to Ganesh Kaskar has increased at a CAGR of 15% over the period of four years whereas PAT has declined at a CAGR of 162% over the same period. Investors should also note that Vijay Aggarwal’s remuneration is substantially higher than the average MD’s remuneration of Rs 36 mn across the BSE 500 companies. The company is in the process of expanding its cement producing capacity from the current 5.6 mtpa to 10 mtpa by 2016 (source ICRA). This may have led to increase in the role and responsibilities of the directors. However as mentioned we understand that Vijay Agarwal has day to day responsibility of the H&R Johnson business. Further given that the company has been loss making for the last two years, IiAS expects the remuneration to remain unchanged. IiAS Analysis Although Vijay Aggarwal and Ganesh Kaskar possess appropriate qualifications and expertise for the positions they are being reappointed to, the remuneration proposed is open ended and without any overall cap. The details on allowances, perquisites bonus commission has not been mentioned by PCL. The relevant excerpt from the notice is given below: ‘Remuneration, by way of salary, dearness allowance, perquisites and other allowances payable monthly, and commission, which together shall not, in any financial year, exceed five per cent of its net profits for one such managerial person and if there is more than one such managerial person, ten per cent for all of them together, as may be decided from time to time by the Board.’ Although we favour the reappointment of Vijay Aggarwal as MD of the company, we find that his proposed remuneration is not just substantially higher than his industry peers but open ended and without an overall cap. Given that this is a combined resolution for his reappointment and remuneration, we recommend voting AGAINST this resolution. And although Ganesh Kaskar salary is in line with his peers, the resolution is open ended and without a cieling. Again, as it is a combined resolution for his appointment and remuneration, IiAS recommends voting AGAINST his appointment.

2010 2011 2012 2013

Net Profit

Vijay Aggarwal

Ganesh Kaskar

Market Cap.

Voting Advisory

June 2013 Prism Cement Limited 11|P a g e

Category: Commission to IDs

Resolution 8: To approve payment of commission to the Non-Executive Independent Directors (ID’s)

IiAS Recommendation: AGAINST

Discussion PCL shareholders, in FY12, had approved remuneration by way of commission not exceeding one percent of net profit of the company with a cap of Rs 5 mn in any financial year to be paid to James Brook for five years ending 31 March 2017.

Pursuant to Section 309 of the Companies Act, 1956, PCL seeks shareholder’s approval to pay commission within the maximum limit of one percent of the net profits of the company to all its ID’s viz. Rajesh G Kapadia, James A Brooks and Ms. Ameeta A Parpia for a period of five years commencing from 1 April 2013. Box 4: Regulation Snapshot – section 309 of Companies Act 1956

The provisions contained in section 309 (4) of the Companies Act 1956 stipulate that a director who is neither in the whole- time employment of the company nor a managing director may be paid remuneration by way of commission if the company by special resolution authorizes such payment; provided that the remuneration paid to such director, or where there is more than one such director, to all of them together, shall not exceed one per cent of the net profits of the company, if the company has a managing or whole- time director.

In FY11, PCL paid commission of Rs 2.5 mn to James Brook which was 0.2% of the net profit (Rs 1460 mn), as computed under Section 349 of the Companies Act and under stipulated limits. During FY12 and FY13, the company did not pay any commission to James Brook as the company did not earn profits. Investors should note that the commission paid to ID’s is open ended, IiAS would advise shareholders to ask for a remuneration cap as was in the earlier case. Further, the company may seek approval once they start earning profits.

IiAS recommends voting AGAINST the resolution.

Voting Advisory

June 2013 Prism Cement Limited 12|P a g e

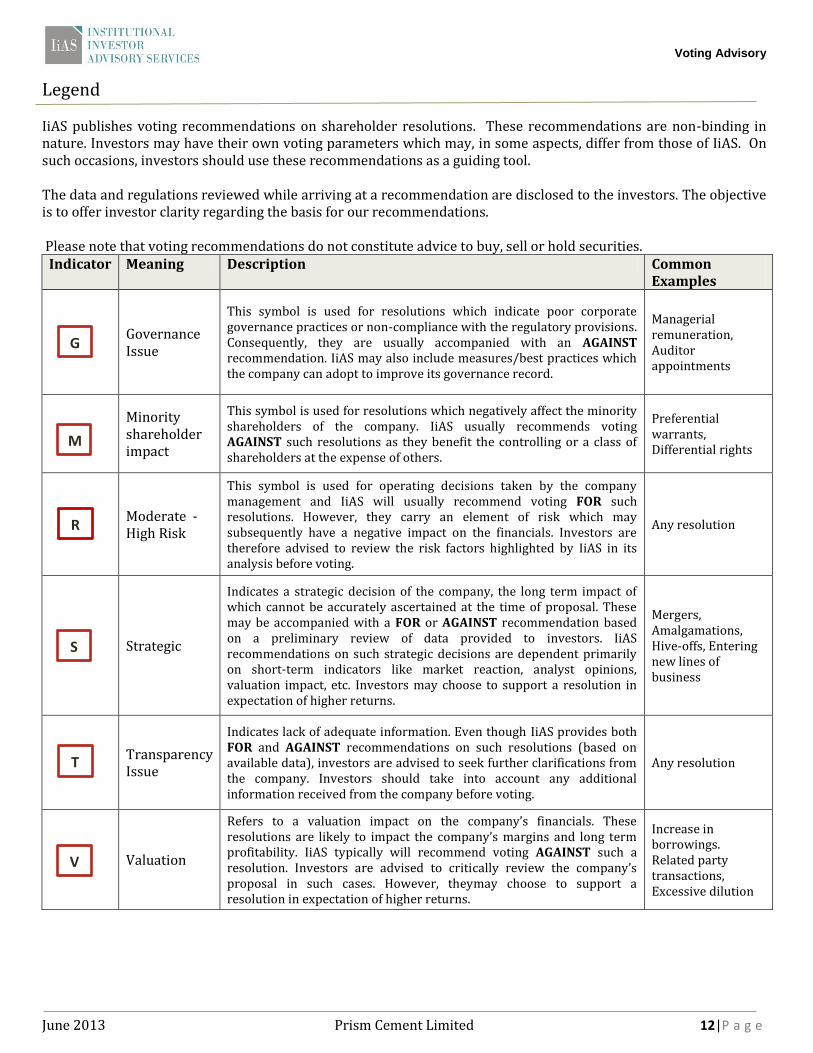

Legend IiAS publishes voting recommendations on shareholder resolutions. These recommendations are non-binding in nature. Investors may have their own voting parameters which may, in some aspects, differ from those of IiAS. On such occasions, investors should use these recommendations as a guiding tool. The data and regulations reviewed while arriving at a recommendation are disclosed to the investors. The objective is to offer investor clarity regarding the basis for our recommendations. Please note that voting recommendations do not constitute advice to buy, sell or hold securities.

Indicator Meaning Description Common Examples

Governance Issue

This symbol is used for resolutions which indicate poor corporate governance practices or non-compliance with the regulatory provisions. Consequently, they are usually accompanied with an AGAINST recommendation. IiAS may also include measures/best practices which the company can adopt to improve its governance record.

Managerial remuneration, Auditor appointments

Minority shareholder impact

This symbol is used for resolutions which negatively affect the minority shareholders of the company. IiAS usually recommends voting AGAINST such resolutions as they benefit the controlling or a class of shareholders at the expense of others.

Preferential warrants, Differential rights

Moderate -High Risk

This symbol is used for operating decisions taken by the company management and IiAS will usually recommend voting FOR such resolutions. However, they carry an element of risk which may subsequently have a negative impact on the financials. Investors are therefore advised to review the risk factors highlighted by IiAS in its analysis before voting.

Any resolution

Strategic

Indicates a strategic decision of the company, the long term impact of which cannot be accurately ascertained at the time of proposal. These may be accompanied with a FOR or AGAINST recommendation based on a preliminary review of data provided to investors. IiAS recommendations on such strategic decisions are dependent primarily on short-term indicators like market reaction, analyst opinions, valuation impact, etc. Investors may choose to support a resolution in expectation of higher returns.

Mergers, Amalgamations, Hive-offs, Entering new lines of business

Transparency Issue

Indicates lack of adequate information. Even though IiAS provides both FOR and AGAINST recommendations on such resolutions (based on available data), investors are advised to seek further clarifications from the company. Investors should take into account any additional information received from the company before voting.

Any resolution

Valuation

Refers to a valuation impact on the company’s financials. These resolutions are likely to impact the company’s margins and long term profitability. IiAS typically will recommend voting AGAINST such a resolution. Investors are advised to critically review the company’s proposal in such cases. However, theymay choose to support a resolution in expectation of higher returns.

Increase in borrowings. Related party transactions, Excessive dilution

G

M

S

V

T

R

Voting Advisory

June 2013 Prism Cement Limited 13|P a g e

Disclaimer

This document has been prepared by Institutional Investor Advisory Services India Limited (IiAS). The information contained herein is from publicly available data or other sources believed to be reliable, but we do not represent that it is accurate or complete and it should not be relied on as such. IiAS shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for any Voting or investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigation as it deems necessary to arrive at an independent evaluation of the individual resolutions which may affect their investment in the securities of companies referred to in this document (including the merits and risks involved). The discussions or views expressed may not be suitable for all investors. This information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject IiAS to any registration or licensing requirements within such jurisdiction. The distribution of this document in certain jurisdictions may be restricted by law, and persons in whose possession this document comes, should inform themselves about and observe, any such restrictions. The information given in this document is as of the date of this report and there can be no assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice. IiAS reserves the right to make modifications and alterations to this statement as may be required from time to time. However, IiAS is under no obligation to update or keep the information current. Nevertheless, IiAS is committed to providing independent and transparent recommendation to its client and would be happy to provide any information in response to specific client queries. Neither IiAS nor any of its affiliates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. . The disclosures of interest statements incorporated in this document are provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report. The information provided in these reports remains, unless otherwise stated, the copyright of IiAS. All layout, design, original artwork, concepts and other Intellectual Properties, remains the property and copyright of IiAS and may not be used in any form or for any purpose whatsoever by any party without the express written permission of the copyright holders.