2. real business cycle - uni- · pdf file2 real business cycle theory introduction (1)...

TRANSCRIPT

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

Introduction

Simplistic RBC Model

Simple stochastic growth model

Baseline RBC model

2. Real Business Cycle Theory(June 25, 2013)

Prof. Dr. Thomas StegerAdvanced Macroeconomics II | Lecture| SS 13

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

2

Real Business Cycle Theory

Introduction (1)

Business cycle research studies the causes and consequences of the recurrent expansions and contractions in aggregate economic activity that occur in most industrialized countries.

Kydland and Prescott (1982) and Long and Plosser (1983) have shown that one could build a successful business cycle model that involved market clearing, no monetary factors and no rational for macroeconomic policy.

Simple equilibrium models, driven by shifts in TFP, could generate time series with the same complex patterns of persistence, comovement and volatility as those of actual economies.

The models of the RBC research program are now widely applied in monetary economics, international economics, public finance, labor economics, and asset pricing. Many of these model economies, in contrast to early RBC studies, involve substantial market failures,

so that government intervention is desirable. In others, the business cycle is driven by monetary shocks or by exogenous shocks in beliefs. DSGE models are by now the laboratory in which modern macroeconomic analysis is conducted.

There has been increasing concern about the mechanisms at the core of the standard RBC models: business cycles are driven mainly by large and cyclically volatile shocks to productivity, which are well represented by Solow residuals.

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

3

Real Business Cycle Theory

Introduction (2) Cyclical components of US expenditures. Sample period is 1947:1-1996:4. All variables are detrended using the Hodrick-Prescott filter.

Economists have long been interested in understanding the economic mechanisms that underlie the different volatilities of key macroeconomic aggregates. (King / Rebelo, 1999, p. 938)

cf. to investment demand

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

4

Real Business Cycle Theory

Introduction (3)

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

5

Real Business Cycle Theory

Introduction (4)

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

6

Real Business Cycle Theory

Introduction (5)

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

7

Real Business Cycle Theory

Introduction (6)

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

8

Real Business Cycle Theory

Introduction (7)

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

9

Real Business Cycle Theory

Introduction (8)

Sorce: King and Rebelo(1999, p. 938)

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

10

Real Business Cycle Theory

Introduction (9)

Volatility. The facts on volatility are as follows (King / Rebelo, 1999, pp. 938-39)

Consumption of non-durables is less volatile than output;

Consumer durables purchases are more volatile than output;

Investment is three times more volatile than output;

Government expenditures are less volatile than output;

Total hours worked has about the same volatility as output;

Capital is much less volatile than output, but capital utilization in manufacturing is more volatile than output;

Employment is as volatile as output, while hours per worker are much less volatile than output, so that most of the cyclical variation in total hours worked stems from changes in employment;

The real wage rate is much less volatile than output.

Comovement. Most macroeconomic series are procyclical, that is, they exhibit a positive contemporaneous correlation with output. The high degree of comovement between total hours worked and aggregate output, displayed above, is particularly striking. Three series are essentially acyclical - wages, government expenditures, and the capital stock - in the sense that their correlation with output is close to zero.

Persistence. All macroeconomic aggregates display substantial persistence; the first-order serial correlation for most detrended quarterly variables is on the order of 0.9. This high serial correlation is the reason why there is some predictability to the business cycle.

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

11

Real Business Cycle Theory

Introduction (10)

Some of the facts just described have been influential in shaping the views of economists about of how the economy operates (King / Rebelo, 1999, pp. 941-42):

The high volatility of investment supports Keynes' famous assertion that investors have "animal spirits“ (→ formalized by common beliefs through Tobin’s q).

The low cyclical volatility of capital (K) is often taken to imply that one can safely abstract from movements in capital in constructing a theory of economic fluctuations.

The high correlation between hours worked (hL) and aggregate output indicates that the labor market is key to understanding business fluctuations.

The Kaldor facts suggest the importance of building models that feature a common trend in most real aggregates.

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

12

Real Business Cycle Theory

A simplistic RBC model (1)

Consider as perfectly competitive economy. There is mass one of identical households (HH). Every HH is endowed with L>0 units of labor, which are supplied inelastically to the labor market. HH rent their capital stock to firms. The saving rate, 0<s<1, is fixed.

There is mass one of identical firms. Each firm has access to a standard Cobb‐Douglas technology.

The simplistic RBC model is described by

Assume ρ=0 and α=0, can this simplistic RBC model explain persistent output fluctuations? Given 0<ρ<1, how does the potential of explaining persistent output fluctuations change with α?

The stochastic variable εt is characterized by E(εt)=0, V(εt)=const., COV(εt,εt‐i)=0 for all t and i.

To simplify, we assume that the depreciation rate is 100% (δ=1) such that capital at time t is Kt=sYt‐1.

One plausible example for real shocks, apart from natural disasters or technological innovations, would be fluctuations of the oil price in a small open economy. How can this be modeled?

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

13

Real Business Cycle Theory

A simplistic RBC model (1a)

One plausible example for real shocks, apart from natural disasters or technological innovations, would be fluctuations of the oil price in a small open economy. How can this be modeled?

Assume the following production structure (Mt: input of crude oil; ptM: price of crude oil)

In competitive equilibrium, the amount of crude oil employed in Y-production is determined by (to simplify notation we set L=1)

Solving for Mt and plugging into the original Y-technology gives the indirect technology to read

In this simple RBC model, oil price fluctuations represent the impulses that induce business cycle movements.

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

14

Real Business Cycle Theory

A simplistic RBC model (2)

Letting lower case letters denote natural logarithms, one may write

Moreover, notice that

Substituting at‐1 in equ. (*) by the RHS of the preceding equation gives

The pseudo steady state is characterized by εt=0 for all t and yt=yt‐1 for all t.

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

15

Real Business Cycle Theory

Simplistic RBC model (3)

Basic propagation mechanism: A positive technology shock (εt>0)

increases contemporary output and, via saving and investment, the stock of capital next period.

For α=0.1 capital is comparably unimportant in the production process, Y=AKαL1‐α. Hence, a positive technology shock has only short lasting consequences (low persistency).

The opposite applies for α=0.9.

α=0.1

α=0.9

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

16

Real Business Cycle Theory

Stochastic growth model: model setup

Timing of events within every period: The shock materializes, then the agent decides on consumption.

This problem differs from the deterministic model in two respects:Output at each period t depends not only on Kt but also on the realization of a stochastic variable Bt. The timing of

events then implies that, in every period t, the agent decides upon Ct knowing the realization of Bt.

As a result of uncertainty about the future, the agent decides only upon C₀ at t=0 and postpones the decision on {C₁,C₂,...}. At t=1 the agent then decides upon C₁ knowing K₁ and B₁ and so on.

Consider the following stochastic Ramsey model (Heer and Maussner, 2005, p. 35)

t∈ time index; "period t" describes the time interval [t,t+1)

E₀ expectations conditional on information in period t=0

0<β<1 subjective discount factor

Ct consumption in period t

Kt stock of capital in period t

Bt stochastic technology parameter

εt i.i.d. random variable with E(εt)=ε and V(εt)=σε

0<γ<1 parameter that captures the degree of persistency of technology shocks

At captures (exogenous) technological progress (approximately) at rate λ≥0

Lt labor input (considered exogenous here)

δ>0 depreciation rate

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

17

Real Business Cycle Theory

Stochastic growth model: dynamic problem (1)

The first‐order conditions ∂ /∂C₀=0 and ∂ /∂K₁=0 can now be expressed as follows

Since C₀, K₁ and, hence, the multiplier μ₀ are non-stochastic we may write

At period t=0, K₀ and B₀ are given and the agent decides on C₀. To solve the above problem we employ the method of Lagrangian multipliers which requires to set up the following Lagrangian function (e.g., Chow, 1997, Chapter 2)

The associated first-order conditions involve ∂LA/∂C₀=0 and ∂LA/∂K₁=0 (together with the dynamic budget constraint). To form these partials, let us write the relevant parts of the Lagrangian explicitly as follows

The value of capital in t=1, given by μ1 , depends on TFP in period 1, given by B1, which is not known in t=0.

Hence, we keep the expectations operator on the RHS of the 2nd FOC.

K0 is treated as given, whereas C0 and K₁are treated as unknowns!

Hence, we need two FOCs to determine C0 and K₁.

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

18

Real Business Cycle Theory

Stochastic growth model: dynamic problem (2)

At period t=1, K₁ and B₁ are given and the agent decides on C₁. The associated Lagrangian function reads

The first-order conditions involve ∂LA/∂C₁=0 and ∂LA/∂K₂=0 (together with the dynamic budget constraint). To form these partials, let us write the relevant parts of the Lagrangian explicitly as follows

The first‐order conditions ∂ A/∂C1=0 and ∂ /∂K2=0 can now be expressed as follows

Since C₁, K₂ and, hence, the multiplier μ₁ are non-stochastic we may write

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

19

Real Business Cycle Theory

Stochastic growth model: dynamic problem (3)

Continuing this way, one finds that, since Kt must be optimal at every t, the plan for choosing {C₀,C₁,..} and {K₀,K₁,..} must solve the system

Eliminating the shadow price μt yields

Reduced form dynamic system: the evolution of the economy is governed by

This is the stochastic Euler equation! It can be viewed as an intertemporal

utility no-arbitrage condition: LHS: Increase in welfare if one unit of

output is being consumed today. RHS: Increase in welfare if this unit is being

invested today. The increase in consumption possibilities then is 1+FK‐δ. This increase is valued according to u’(c); since future outcome is risky we apply E(.); and discount by ß to be able to compare the result to the RHS.

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

20

Real Business Cycle Theory

Stochastic growth model: general remark on FOC

The set of first-order conditions can be readily developed by setting up the Lagrangian function (where we assume that labor is endogenous) and forming the associated first-order conditions, i.e.

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

21

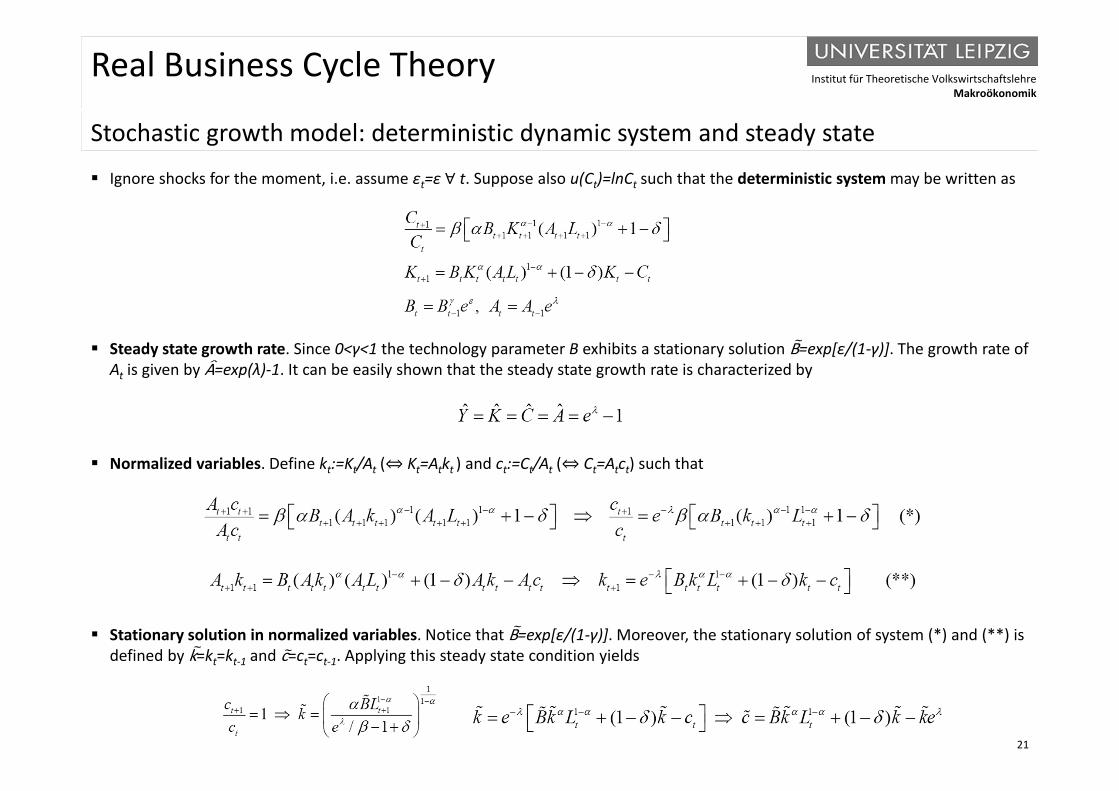

Real Business Cycle Theory

Stochastic growth model: deterministic dynamic system and steady state

Ignore shocks for the moment, i.e. assume εt=ε ∀ t. Suppose also u(Ct)=lnCt such that the deterministic system may be written as

Steady state growth rate. Since 0<γ<1 the technology parameter B exhibits a stationary solution B=exp[ε/(1‐γ)]. The growth rate of At is given by A=exp(λ)‐1. It can be easily shown that the steady state growth rate is characterized by

Normalized variables. Define kt:=Kt/At (⇔ Kt=Atkt ) and ct:=Ct/At (⇔ Ct=Atct) such that

Stationary solution in normalized variables. Notice that B=exp[ε/(1‐γ)]. Moreover, the stationary solution of system (*) and (**) is defined by k=kt=kt‐1 and c=ct=ct‐1. Applying this steady state condition yields

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

22

Real Business Cycle Theory

Stochastic growth model: impulse-response functions

Impulse‐response functions (theory‐based). The dynamic evolution of the model economy in response to a shock is investigated. This is based on the following steps: I. Normalize the variables such that the transformed system does not exhibit growth.II. Compute the (pseudo) steady state (i.e. steady state assuming that no shocks occur) in normalized variables.III. Simulate this deterministic dynamic system.

The impulse is a temporary technology shock by 1%.

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

23

Real Business Cycle Theory

Basic RBC model: model setup

Consider the following basic RBC model (cf. Brunner and Strulik, 2004, p. 82)

To solve this dynamic optimization problem we set up the following Lagrangian function

The FOCs must now be complemented by a static efficiency condition ∂u(Ct,Lt)/∂Lt+μt∂F(Kt,Lt)/∂Lt=0 or

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

24

Real Business Cycle Theory

Basic RBC model: dynamic system

The complete set of first‐order conditions then reads as follows

Eliminating the shadow price one gets Stochastic Euler equationLHS: marginal utility (cost of a C

reduction by one unit)RHS: The discounted expected

benefit of postponing consumption by one unit in terms of utility

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

25

Real Business Cycle Theory

Basic RBC model: deterministic dynamic system and steady state

Let us ignore shocks for the moment, i.e. εt=ε ∀ t. The corresponding deterministic system may be expressed as

As before, the steady state growth rate is given by Y=K=C=A=exp(λ)‐1. Defining normalized variables kt:=Kt/At (⇔ Kt=Atkt ) and ct:=Ct/At (⇔ Ct=Atct), the first-order condition -∂u(Ct,Lt)/∂Lt=μt∂F(Kt,Lt)/∂Lt reads

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

26

Real Business Cycle Theory

Basic RBC model: dynamic system and steady state

Complete dynamic system. The complete dynamic system in terms of normalized variables then reads

Observe that this is the same as before complemented by a static efficiency condition for Lt.

Steady state. The steady state in terms of normalized variables (satisfying xt+1=xt for all t) is determined by

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

27

Real Business Cycle Theory

Basic RBC model: impulse-response functions (1)

Impulse‐response functions (theory‐based). The dynamic evolution of the model economy in response to a shock is investigated. This is based on the following steps: I. Normalize the variables such that the transformed system does not exhibit growth.II. Compute the (pseudo) steady state (i.e. steady state assuming that no shocks occur) in normalized variables.III. Simulate this deterministic dynamic system.

The impulse is a temporary technology shock by 1%.

Notice the comovement between yand L.

It would be nice to plot also w(t)!

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

28

Real Business Cycle Theory

Basic RBC model: impulse-response functions (2)

Impulse‐response functions. Below are typical impulse-response functions, which describe the dynamic behavior of the economy under study. The shock considered is a one-time shock in technology amounting to 1 percent increase in At.

These plots are taken from Romer (2006; Chapter 4.7).

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

29

Real Business Cycle Theory

Basic RBC model: replicating actual business cycles (1)

Source: King / Rebelo (1999, p. 959)

“With a series of productivity shocks in hand, we simulated our model economy's response to these shocks… Figure 13 displays the results, which we think are dramatic. Panel 1 shows the model and actual paths for output, which are virtually identical. In part, this is an artifact of our procedure for constructing the technology shock, which is a weighted average of output and capital as we just discussed.” King and Rebelo (1993, p. 986)

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

30

Real Business Cycle Theory

Basic RBC model: replicating actual business cycles (2)Source: King / Rebelo (1999, p. 959)

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

31

Real Business Cycle Theory

Comparison of theoretical and empirical moments

Given a sequence of shocks {εt}, which may be determined as shocks to TFP (Solow residual), the time paths of the endogenous variables (consumption, labor, capital etc.) are computed.

This is repeated x-times (with x being "sufficiently large"). Subsequently, one can determine the volatility, auto‐correlations and comovements of the endogenous variables.

These theoretical moments are then compared to empirical moments.

As an illustration, consider the simplistic RBC model, which allows for a closed-form solution. In this case, simulating the model is trivial since the closed-form solution is available.

Based on this sample of time paths one can calculate the standard deviation.

Comment: Given a stochastic process of the form xt+a₁xt‐1+a₂xt‐2=εt (with σε=const.) the variance of xt is given (e.g., Arnold, 2002, p. 8).

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

32

Real Business Cycle Theory

Summary and conclusion

The RBC model represents a neoclassical economy where real shocks drive output and employment movements.

The underlying model economy is perfect and, hence, the movements are optimal responses to shocks. Put differently, observed aggregate output and employment movements are interpreted to represent time‐varying Pareto‐optimal equilibria.

Thus, contrary to conventional wisdom, macroeconomic fluctuations do not reflect any market failures, and government interventions to mitigate them can only reduce welfare.

The notion that adverse downward movements in total technology cause recessions is just plain silly. This is the theory according to which the 1930s should be known not as the Great Depression but as the Great Vacation. (Mussa, 1998, p. 384)

The RBC research program has initiated the DSGE methodology. This set of techniques has been applied extensively within the context of other macroeconomic theories, most prominently the New Keynesian Theories.

Institut für Theoretische VolkswirtschaftslehreMakroökonomik

33

Real Business Cycle Theory

Notation

At exogenous technological progress Bt stochastic technology parameterCt consumption ct:=Ct/At normalized consumptionEt expectations in period tKt stock of capitalkt:=Kt/At normalized capitalLA Lagrangian functionLt labor input 0<s<1 saving rate u(.) instantaneous utilityYt final output at time tỹ pseudo steady state

0<α<1 technology parameter 0<β<1 subjective discount factor0<γ<1 parameter indicating persistency of technology shocksδ≥0 capital depreciation rate εt i.i.d. random variable with E(εt)=ε≥0 and V(εt)=σε

η>0 preference parameterλ≥0 rate of technological progressμt Lagrangian multiplier

ρ>0 time preference rate σ standard deviation