2 - otc.nfmf.nootc.nfmf.no/public/news/11437_2.pdf · intermediate financing to ensure that...

TRANSCRIPT

Marine Accurate Well ASA

STRICTLY PRIVATE AND CONFIDENTIAL

Company Update

2 June 2010

Solely for review in connection with the proposed restructuring – not for reproduction or distribution. The information contained herein may be subject to change without prior notice. Please note that this is not an offering document.

in Connection with the Proposed Restructuring

THIS PRESENTATION AND ITS ENCLOSURES AND APPENDICES (HEREINAFTER JOINTLY REFERRED TO AS THE “PRESENTATION”) HAS BEEN PREPARED BY MARACC – MARINE ACCURATE WELL ASA (”MARACC” OR THE ”COMPANY”) EXCLUSIVELY FOR INFORMATION PURPOSES. THIS PRESENTATION HAS NOT BEEN REVIEWED OR REGISTERED WITH ANY PUBLIC AUTHORITY OR STOCK EXCHANGE. RECIPIENTS OF THIS PRESENTATION MAY NOT REPRODUCE, REDISTRIBUTE OR PASS ON, IN WHOLE OR IN PART, THE PRESENTATION TO ANY OTHER PERSON.

THIS PRESENTATION CONTAINS INFORMATION OBTAINED FROM THIRD PARTIES. SUCH INFORMATION HAS BEEN ACCURATELY REPRODUCED AND, AS FAR AS THE COMPANY IS AWARE AND ABLE TO ASCERTAIN FROM THE INFORMATION PUBLISHED BY THAT THIRD PARTY, NO FACTS HAVE BEEN OMITTED THAT WOULD RENDER THE REPRODUCED INFORMATION TO BE INACCURATE OR MISLEADING.

THE DISTRIBUTION OF THIS PRESENTATION AND THE OFFERING, SUBSCRIPTION, PURCHASE OR SALE OF SECURITIES ISSUED BY THE COMPANY IN CERTAIN JURISDICTIONS IS RESTRICTED BY LAW. PERSONS INTO WHOSE POSSESSION THIS PRESENTATION MAY COME ARE REQUIRED BY THE COMPANY TO INFORM THEMSELVES ABOUT AND TO COMPLY WITH ALL APPLICABLE LAWS AND REGULATIONS IN FORCE IN ANY JURISDICTION IN OR FROM WHICH IT INVESTS OR RECEIVES OR POSSESSES THIS PRESENTATION AND MUST OBTAIN ANY CONSENT, APPROVAL OR PERMISSION REQUIRED UNDER THE LAWS AND REGULATIONS IN FORCE IN SUCH JURISDICTION, AND THE COMPANY SHALL NOT HAVE ANY RESPONSIBILITY OR LIABILITY FOR THESE OBLIGATIONS. IN PARTICULAR, NEITHER THIS PRESENTATION NOR ANY COPY OF IT MAY BE TAKEN OR TRANSMITTED OR DISTRIBUTED, DIRECTLY OR INDIRECTLY, INTO CANADA OR JAPAN.

THIS PRESENTATION DOES NOT CONSTITUTE AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY ANY SECURITIES IN ANY JURISDICTION TO ANY PERSON TO WHOM IT IS UNLAWFUL TO MAKE SUCH AN OFFER OR SOLICITATION IN SUCH JURISDICTION.

THIS PRESENTATION AND THE INFORMATION CONTAINED HEREIN DO NOT CONSTITUTE AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES AND ARE NOT FOR PUBLICATION OR DISTRIBUTION TO U.S. PERSONS (WITHIN THE MEANING OF REGULATION S UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE “U.S. SECURITIES ACT”)). THE SECURITIES PROPOSED TO BE OFFERED IN THE COMPANY HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE SECURITIES ACT AND MAY NOT BE OFFERED OR SOLD IN THE UNITED STATES OR TO U.S. PERSONS EXCEPT PURSUANT TO AN EXEMPTION FROM THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT.

IN RELATION TO THE UNITED STATES AND U.S. PERSONS, THIS PRESENTATION IS STRICTLY CONFIDENTIAL AND IS BEING FURNISHED SOLELY IN RELIANCE ON APPLICABLE EXEMPTIONS FROM THE REGISTRATION REQIUREMENTS UNDER THE U.S. SECURITIES ACT, AS AMENDED. THE SECURITIES OF MARACC HAVE NOT AND WILL NOT BE REGISTERED UNDER THE U.S. SECURITIES ACT OR ANY STATE SECURITIES LAWS, AND MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES, OR TO OR FOR THE ACCOUNT OR BENEFIT OF U.S. PERSONS, UNLESS AN EXEMPTION FROM THE REGISTRATION REQUIREMENTS OF THE U.S. SECURITIES ACT IS AVAILABLE. ACCORDINGLY, ANY SECURITIES OF MARACC WILL ONLY BE OFFERED OR SOLD (I) WITHIN THE UNITED STATES, OR TO OR FOR THE ACCOUNT OR BENEFIT OF U.S. PERSONS, ONLY TO QUALIFIED INSTITUTIONAL BUYERS (”QIBs”) IN PRIVATE PLACEMENT TRANSACTIONS NOT INVOLVING A PUBLIC OFFERING AND (II) OUTSIDE THE UNITED STATES IN OFFSHORE TRANSACTIONS IN ACCORDANCE WITH REGULATION S. ANY PURCHASER OF SECURITIES OF MARACC IN THE UNITED STATES, OR TO OR FOR THE ACCOUNT OF U.S. PERSONS, WILL BE DEEMED TO HAVE MADE CERTAIN REPRESENTATIONS AND ACKNOWLEDGEMENTS, INCLUDING WITHOUT LIMITATION THAT THE PURCHASER IS A QIB.

NONE OF THE COMPANY’S SECURITIES HAS BEEN OR WILL BE QUALIFIED FOR SALE UNDER THE SECURITIES LAWS OF ANY PROVINCE OR TERRITORY OF CANADA. THE COMPANY’S SECURITIES ARE NOT BEING OFFERED AND MAY NOT BE OFFERED OR SOLD, DIRECTLY OR INDIRECTLY, IN CANADA OR TO OR FOR THE ACCOUNT OF ANY RESIDENT OF CANADA IN CONTRAVENTION OF THE SECURITIES LAWS OF ANY PROVINCE OR TERRITORY THEREOF.

Important information

2

THIS PRESENTATION AND ITS CONTENTS ARE CONFIDENTIAL AND ITS DISTRIBUTION (WHICH TERM SHALL INCLUDE ANY FORM OF COMMUNICATION) IS RESTRICTED UNDER ENGLISH LAW PURSUANT TO SECTION 21 (RESTRICTIONS ON FINANCIAL PROMOTION) OF THE FINANCIAL SERVICES AND MARKETS ACT 2000 (AS AMENDED). IN RELATION TO THE UNITED KINGDOM, THIS PRESENTATION IS ONLY DIRECTED AT, AND MAY ONLY BE DISTRIBUTED TO, PERSONS WHO FALL WITHIN THE MEANING OF ARTICLE 19 (INVESTMENT PROFESSIONALS) AND 49 (HIGH NET WORTH COMPANIES, UNINCORPORATED ASSOCIATIONS, ETC.) OF THE FINANCIAL SERVICES AND MARKETS ACT 2000 (FINANCIAL PROMOTION) ORDER 2001 (AS AMENDED) OR WHO ARE PERSONS TO WHOM THE DOCUMENT MAY OTHERWISE LAWFULLY BE DISTRIBUTED. THIS PRESENTATION MAY ONLY BE DISTRIBUTED IN CIRCUMSTANCES WHICH DO NOT RESULT IN AN OFFER TO THE PUBLIC IN THE UNITED KINGDOM WITHIN THE MEANING OF THE PUBLIC OFFERS OF SECURITIES REGULATIONS 1995 (AS AMENDED).

THE CONTENTS OF THIS PRESENTATION ARE NOT TO BE CONSTRUED AS LEGAL, BUSINESS, INVESTMENT OR TAX ADVICE. EACH RECIPIENT SHOULD CONSULT WITH ITS OWN LEGAL, BUSINESS, INVESTMENT AND TAX ADVISER AS TO LEGAL, BUSINESS, INVESTMENT AND TAX ADVICE.

THERE MAY HAVE BEEN CHANGES IN MATTERS WICH AFFECT THE COMPANY SUBSEQUENT TO THE DATE OF THIS PRESENTATION. NEITHER THE ISSUE NOR DELIVERY OF THIS PRESENTATION SHALL UNDER ANY CIRCUMSTANCE CREATE ANY IMPLICATION THAT THE INFORMATION CONTAINED HEREIN IS CORRECT AS OF ANY TIME SUBSEQUENT TO THE DATE HEREOF OR THAT THE AFFAIRS OF THE COMPANY HAVE NOT SINCE CHANGED, AND THE COMPANY DOES NOT INTEND, AND DOES NOT ASSUME ANY OBLIGATION, TO UPDATE OR CORRECT ANY INFORMATION INCLUDED IN THIS PRESENTATION.

THIS PRESENTATION INCLUDES AND IS BASED ON, AMONG OTHER THINGS, FORWARD LOOKING INFORMATION AND STATEMENTS. SUCH FORWARD LOOKING INFORMATION AND STATEMENTS ARE BASED ON THE CURRENT EXPECTATIONS, ESTIMATES AND PROJECTIONS OF MARACC OR ASSUMPTIONS BASED ON INFORMATION AVAILABLE TO THE COMPANY. SUCH FORWARD LOOKING INFORMATION AND STATEMENTS REFLECT CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE SUBJECT TO RISKS, UNCERTAINTIES AND ASSUMPTIONS THAT COULD CAUSE THE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS OF THE COMPANY TO BE MATERIALLY DIFFERENT FROM ANY FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS THAT MAY BE EXPRESSED OR IMPLIED BY STATEMENTS AND INFORMATION IN THIS PRESENTATION, INCLUDING, AMONG OTHERS, RISKS OR UNCERTAINTIES ASSOCIATED WITH THE COMPANY’S PRODUCTS, SEGMENTS, DEVELOPMENT, GROWTH MANAGEMENT, FINANCING, MARKET ACCEPTANCE AND RELATIONS WITH CUSTOMERS, AND, MORE GENERALLY, GENERAL ECONOMIC AND BUSINESS CONDITIONS, CHANGES IN DOMESTIC AND FOREIGN LAWS AND REGULATIONS (INCLUDING WITHOUT LIMITATION THE US COASTWISE LAWS), TAXES, CHANGES IN COMPETITION AND PRICING ENVIRONMENTS, FLUCTUATIONS IN CURRENCY EXCHANGE RATES AND INTEREST RATES AND OTHER FACTORS. SHOULD ONE OR MORE OF THESE RISKS OR UNCERTAINTIES MATERIALISE, OR SHOULD UNDERLYING ASSUMPTIONS PROVE INCORRECT, ACTUAL RESULTS MAY VARY MATERIALLY FROM THOSE DESCRIBED IN THIS DOCUMENT. THE COMPANY DOES NOT INTEND, AND DOES NOT ASSUME ANY OBLIGATION, TO UPDATE OR CORRECT THE INFORMATION INCLUDED IN THIS PRESENTATION.

BY ATTENDING OR RECEIVING THIS PRESENTATION YOU ACKNOWLEDGE THAT YOU WILL BE SOLELY RESPONSIBLE FOR YOUR OWN ASSESSMENT OF THE MARKET AND MARKET POSITION OF THE COMPANY AND THAT YOU WILL CONDUCT YOUR OWN ANALYSIS AND BE SOLELY RESPONSIBLE FOR FORMING YOUR OWN VIEW OF THE POTENTIAL FUTURE PERFORMANCE OF THE COMPANY’S BUSINESS.

THIS PRESENTATION IS SUBJECT TO NORWEGIAN LAW, AND ANY DISPUTE ARISING IN RESPECT OF THIS PRESENTATION IS SUBJECT TO THE EXCLUSIVE JURISDICTION OF THE NORWEGIAN COURTS.

Important information (cont’d)

3

Table of contents

1. Executive summary

2. Market opportunity

3. Project overview

4. Proposed restructuring

5. Financial overview

Appendix

A. Supporting slides

B. Risk factors

Background

MARACC is building the Island Innovator – a purpose built heavy well intervention and drilling unit targeted for North Sea operations

- Contract with COSCO for a fully equipped semi-submersible vessel- Well intervention and drilling equipment from National, Cameron, VetcoGray and Wison- Newly revised delivery schedule implies delivery during 3Q 2011 and fully operational start-up during 2Q 2012

Rig upgraded with full-scale drilling capabilities to further enhance operational flexibility and strengthen the potential for long-term contracts at improved dayrates

Island Offshore to market and manage the vessel, and to provide project management and supervision during construction

~USD 290 mill raised in capital to date- NOK 385 mill equity issue (Feb-07)

- USD 120 mill secured bond issue (Feb-07)

- USD 80 mill subordinated convertible bond issue (Jul-07)

- USD 30 mill subordinated convertible bond issue (Oct-08)

OTC registered in Norway (ticker: MARA)

Confidential

5

Situation assessment

MARACC has for the last year worked along several tracks to fully finance the remaining unfunded capex requirement of ~USDm 260, however, efforts have proven unsuccessful mainly due to prevailing market conditions and lack of contract

In response to the challenging situation, MARACC is proposing a solution of an intermediate financing of NOKm 213-360 through a directed equity issue, of which NOKm 213 is fully underwritten

- Underwriting conditional upon acceptance of the restructuring proposal and shareholders’ approval- Proposed structure has also been welcomed by key suppliers which have agreed to revised payment schedules

conditional on a successful completion of the proposed restructuring and directed equity issue- Intermediate financing to ensure that construction can continue uninterrupted until 4Q 2010

Subject to new equity capital being raised, MARACC has been able to obtain amended payment schedules from certain key suppliers

Possibility of entering into a turn-key contract with COSCO for delivery of a complete well intervention and drilling unit currently being explored

- Parallel activities of mechanical completion, commissioning and top-side installation to safeguard schedule- Defer payment of last installment to COSCO- Maintain turn-key responsibility with the yard – considered to be more efficient and reducing integration risks- COSCO has gained experience from top-side installation on Sevan Driller

Debt restructuring by equitisation of all existing debt required to secure new equity capital

MARACC to continue its effort to fully finance the project by end of 2010- Restructuring believed to further enhance the possibility of addressing the remaining financing requirement through bank

debt and / or bond issue

6

Table of contents

1. Executive summary

2. Market opportunity

3. Project overview

4. Proposed restructuring

5. Financial overview

Appendix

A. Supporting slides

B. Risk factors

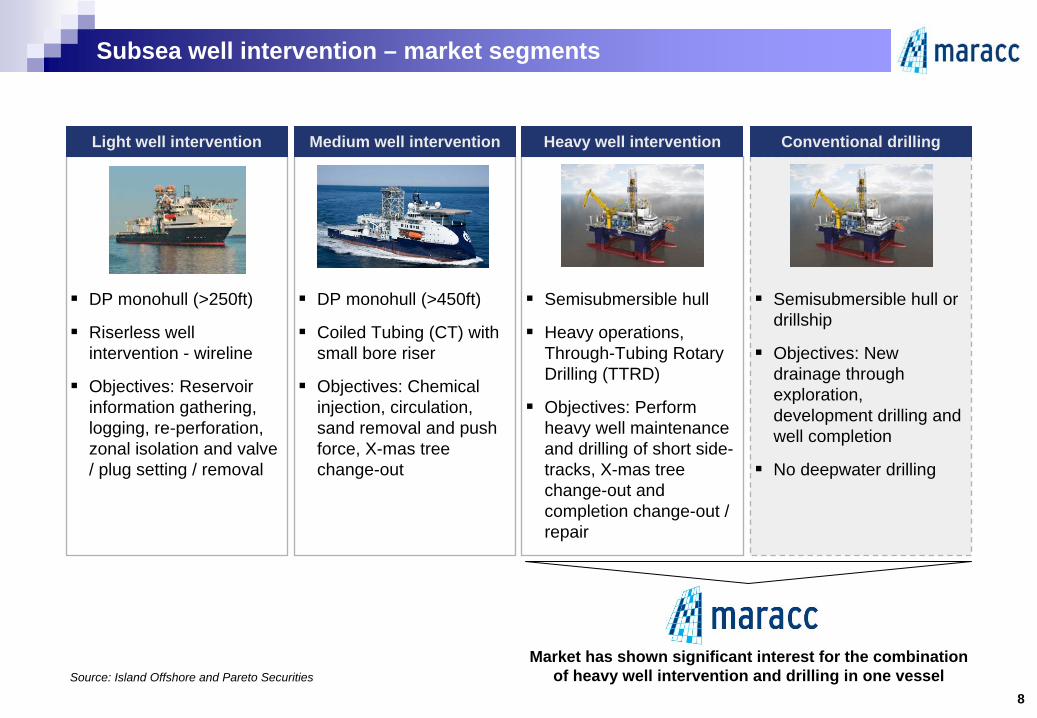

Subsea well intervention – market segments

Confidential

DP monohull (>250ft)

Riserless well intervention - wireline

Objectives: Reservoir information gathering, logging, re-perforation, zonal isolation and valve / plug setting / removal

Light well intervention Medium well intervention

DP monohull (>450ft)

Coiled Tubing (CT) with small bore riser

Objectives: Chemical injection, circulation, sand removal and push force, X-mas tree change-out

8

Heavy well intervention

Semisubmersible hull

Heavy operations, Through-Tubing Rotary Drilling (TTRD)

Objectives: Perform heavy well maintenance and drilling of short side-tracks, X-mas tree change-out and completion change-out / repair

Conventional drilling

Semisubmersible hull or drillship

Objectives: New drainage through exploration, development drilling and well completion

No deepwater drilling

Source: Island Offshore and Pareto SecuritiesMarket has shown significant interest for the combination

of heavy well intervention and drilling in one vessel

9

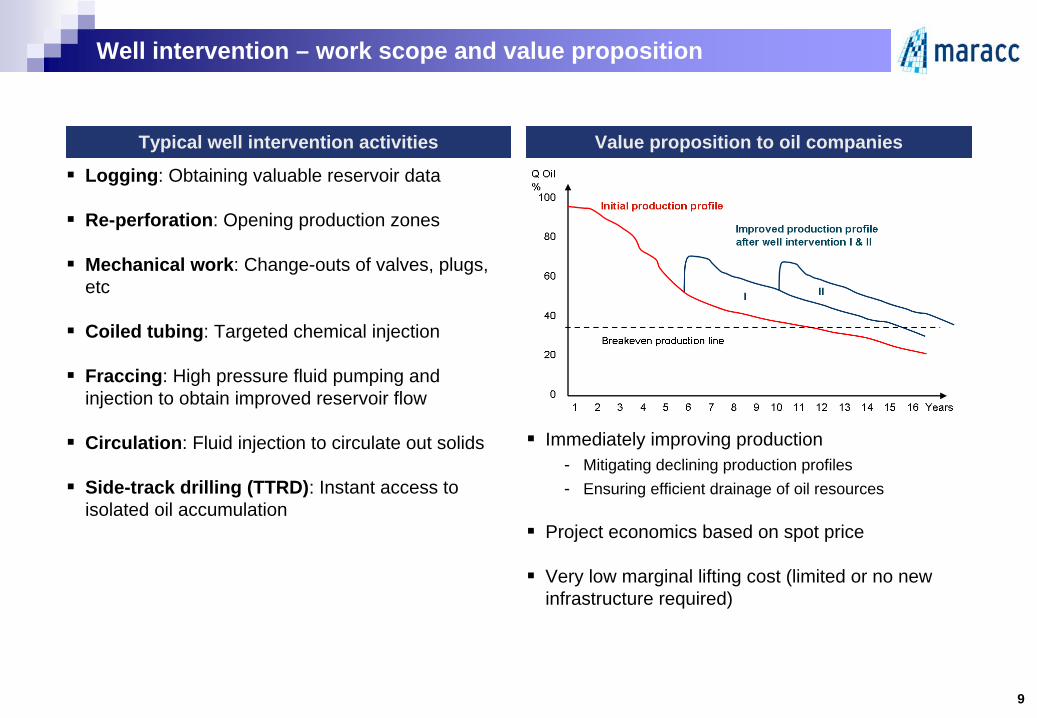

Well intervention – work scope and value proposition

Logging: Obtaining valuable reservoir data

Re-perforation: Opening production zones

Mechanical work: Change-outs of valves, plugs, etc

Coiled tubing: Targeted chemical injection

Fraccing: High pressure fluid pumping and injection to obtain improved reservoir flow

Circulation: Fluid injection to circulate out solids

Side-track drilling (TTRD): Instant access to isolated oil accumulation

Typical well intervention activities Value proposition to oil companies

Immediately improving production- Mitigating declining production profiles- Ensuring efficient drainage of oil resources

Project economics based on spot price

Very low marginal lifting cost (limited or no new infrastructure required)

10

Through-Tubing Rotary Drilling (TTRD)

Drilling of short side-tracks in existing wells (up to 2,000 metres)

- Instant access to isolated oil accumulation of 1–10 mmboe in the proximity of existing fields

Low cost drainage solution for smaller reservoir pockets

Required to maintain plateau production and achieve drainage goals on several fields

Prospects already identified in Norwegian waters estimated to require >2,000 rig days

Pay-back time for oil companies in weeks / months

Exclusive agreement with Halliburton to offer integrated heavy well intervention services

Existing production tubing

Production packer

Through Tubing Sidetrack

Whipstock

Strong underlying market fundamentals

Number of subsea wells growing rapidly as oil companies move to deeper waters

Complexity of reservoirs increasing

Recovery rates significantly lower for subsea wells compared to platform wells

Increased oil recovery (IOR) through well intervention yielding attractive economics for oil companies

11

Subsea well intervention Conventional drilling (NCS)

Oil price support economics for oil companies and activity expected to remain high

Tight market balance for quality assets in the mid-water segment supported by ageing fleet and few newbuilds entering the market

Rates currently at attractive levels and outlook remains strong, recent fixtures in the range of USD 375k-400k/day

Increased subsea activity and IOR initiatives support strong outlook for heavy well intervention services going forward. NCS mid-water drilling market remains attractive supported by recent strong fixtures

Division of subsea tender activity into regions

0

10

20

30

40

50

60

70

80

90

100

W2

W7

W12

W17

W22

W27

W32

W37

W42

W47

W52

w05

w10

w15

w20

# te

nder

s ou

t

Asia Pacific Europe&West Africa Latin America M iddle EastNorth America Northwest Europe Other

Source: Carnegie Research, ODS Petrodata

20102009

Dayrates and utilisation (marketed)

0

100 000

200 000

300 000

400 000

500 000

600 000

Jan0

5

May

0

Sep0

5

Jan0

6

May

0

Sep0

6

Jan0

7

May

0

Sep0

7

Jan0

8

May

0

Sep0

8

Jan0

9

May

0

Sep0

9

jan.

10

50 %

60 %

70 %

80 %

90 %

100 %

110 %

Dayrates Utilisation (marketed)

Source: Carnegie Research, ODS-Petrodata

12

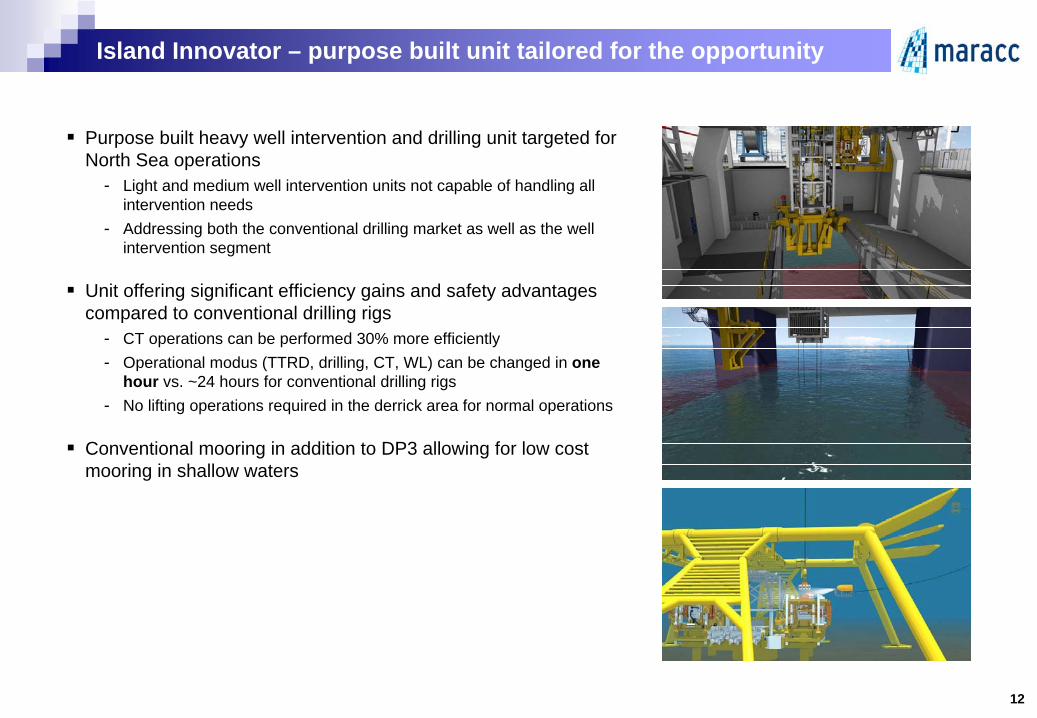

Island Innovator – purpose built unit tailored for the opportunity

Purpose built heavy well intervention and drilling unit targeted for North Sea operations

- Light and medium well intervention units not capable of handling all intervention needs

- Addressing both the conventional drilling market as well as the well intervention segment

Unit offering significant efficiency gains and safety advantagescompared to conventional drilling rigs

- CT operations can be performed 30% more efficiently- Operational modus (TTRD, drilling, CT, WL) can be changed in one

hour vs. ~24 hours for conventional drilling rigs- No lifting operations required in the derrick area for normal operations

Conventional mooring in addition to DP3 allowing for low cost mooring in shallow waters

Table of contents

1. Executive summary

2. Market opportunity

3. Project overview

4. Proposed restructuring

5. Financial overview

Appendix

A. Supporting slides

B. Risk factors

14

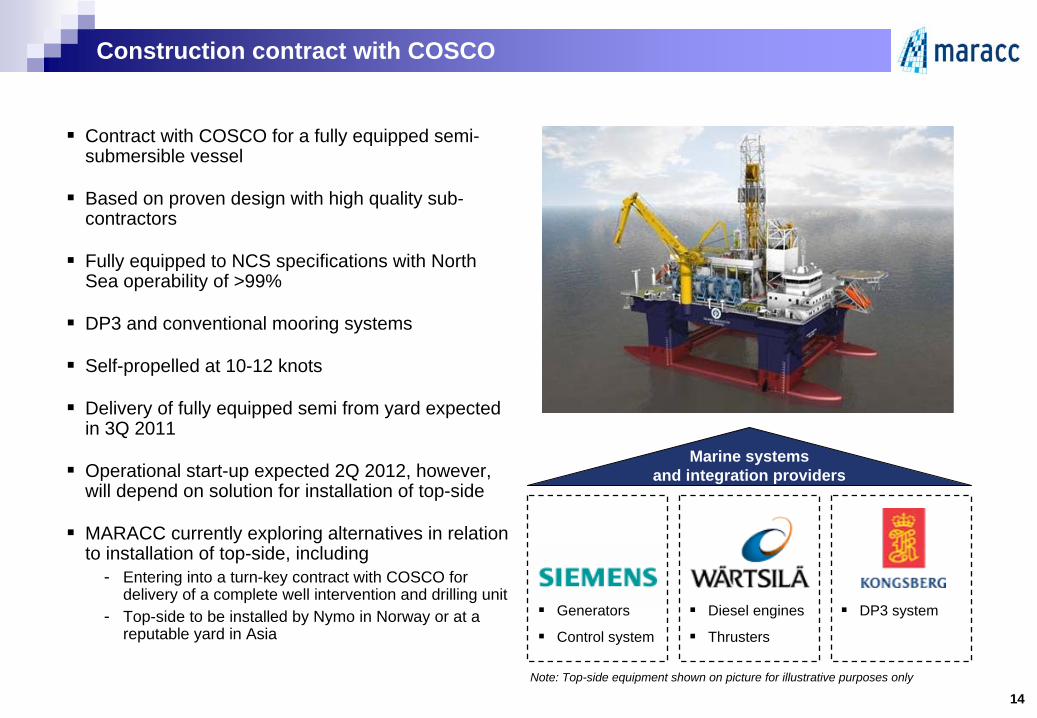

Construction contract with COSCO

Contract with COSCO for a fully equipped semi-submersible vessel

Based on proven design with high quality sub-contractors

Fully equipped to NCS specifications with North Sea operability of >99%

DP3 and conventional mooring systems

Self-propelled at 10-12 knots

Delivery of fully equipped semi from yard expected in 3Q 2011

Operational start-up expected 2Q 2012, however, will depend on solution for installation of top-side

MARACC currently exploring alternatives in relation to installation of top-side, including

- Entering into a turn-key contract with COSCO for delivery of a complete well intervention and drilling unit

- Top-side to be installed by Nymo in Norway or at a reputable yard in Asia

Generators

Control system

Diesel engines

Thrusters

DP3 system

Marine systemsand integration providers

Note: Top-side equipment shown on picture for illustrative purposes only

15

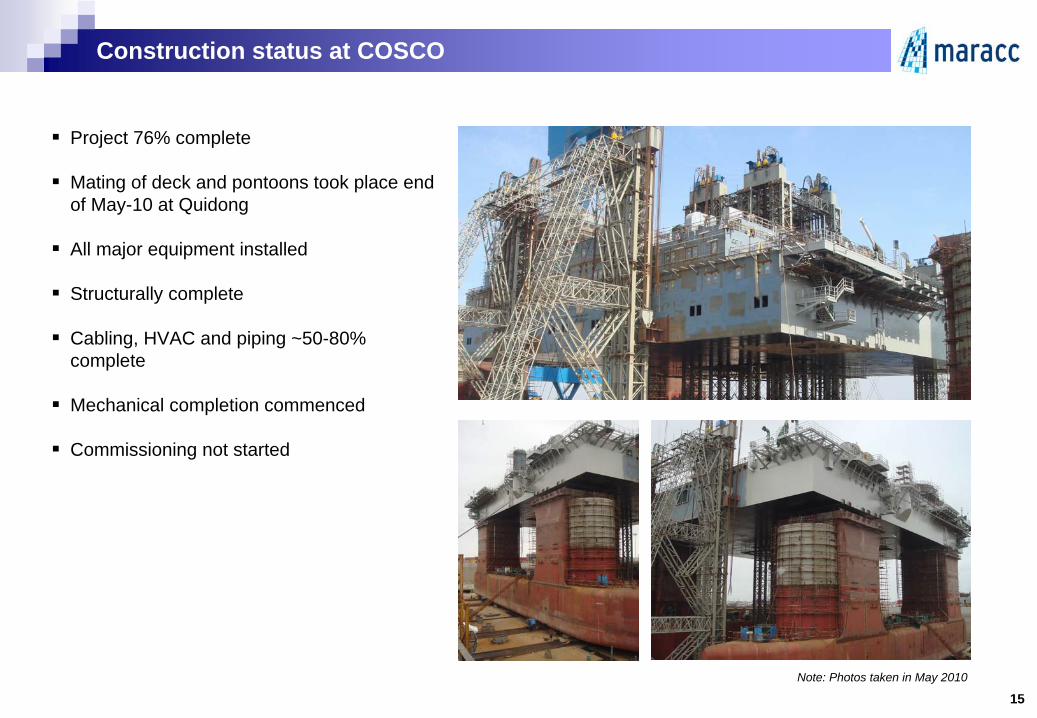

Construction status at COSCO

Project 76% complete

Mating of deck and pontoons took place end of May-10 at Quidong

All major equipment installed

Structurally complete

Cabling, HVAC and piping ~50-80% complete

Mechanical completion commenced

Commissioning not started

Note: Photos taken in May 2010

16

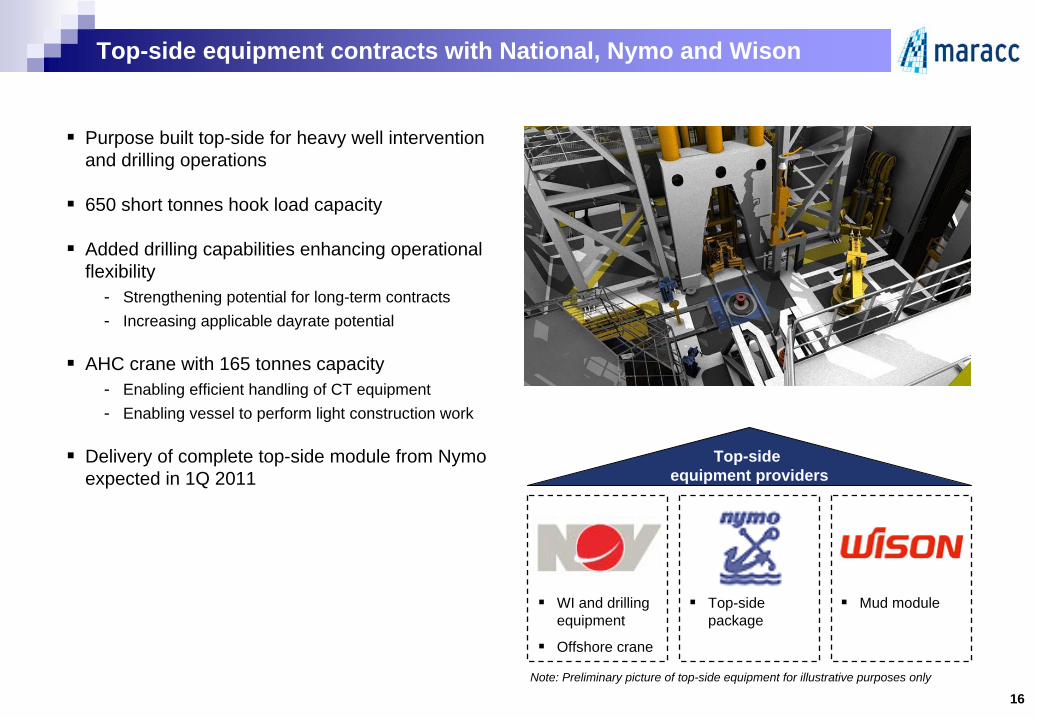

Top-side equipment contracts with National, Nymo and Wison

Purpose built top-side for heavy well intervention and drilling operations

650 short tonnes hook load capacity

Added drilling capabilities enhancing operational flexibility

- Strengthening potential for long-term contracts- Increasing applicable dayrate potential

AHC crane with 165 tonnes capacity- Enabling efficient handling of CT equipment- Enabling vessel to perform light construction work

Delivery of complete top-side module from Nymo expected in 1Q 2011

Top-side equipment providers

Note: Preliminary picture of top-side equipment for illustrative purposes only

WI and drilling equipment

Offshore crane

Top-side package

Mud module

17

BOP and riser contracts with Cameron and VetcoGray

Cameron to deliver full-size BOP stack and control system

- 18-3/4” 15K 5 cavity BOP stack- Conventional direct hydraulic control system for 750m

water depth

VetcoGray to deliver riser system- Standard MR6 marine drilling riser

Contracts with Cameron and VetcoGray are temporarily suspended pending contract outcome

- Depending on contract, BOP and riser could be provided by client

- Cancellation to be decided upon by year end 2010- Although certain penalties will apply, a potential

cancellation would reduce estimated remaining capex by ~USDm 40

BOP stack

BOP control system

Marine riser system

Diverter system

Drilling equipment providers

Note: Picture of drilling equipment for illustrative purposes only

VetcoGraya GE Oil & Gas business

18

Marketing status

Potential for long-term contract confirmed through marketing to date, especially for unit offering full scale drilling capabilities in addition to flexible heavy well intervention services

- North Sea: TTRD / side-track drilling and Coiled Tubing- Gulf of Mexico: Coiled Tubing and well completion

In discussions with Statoil for long-term contract for Category B services (well intervention)

Tendered to Total for the Laggan and Tormore project (3 years drilling)

Several other oil companies have showed interest for heavy well intervention services, including Shell

Project management

Technicaloperations MarketingMarine crew

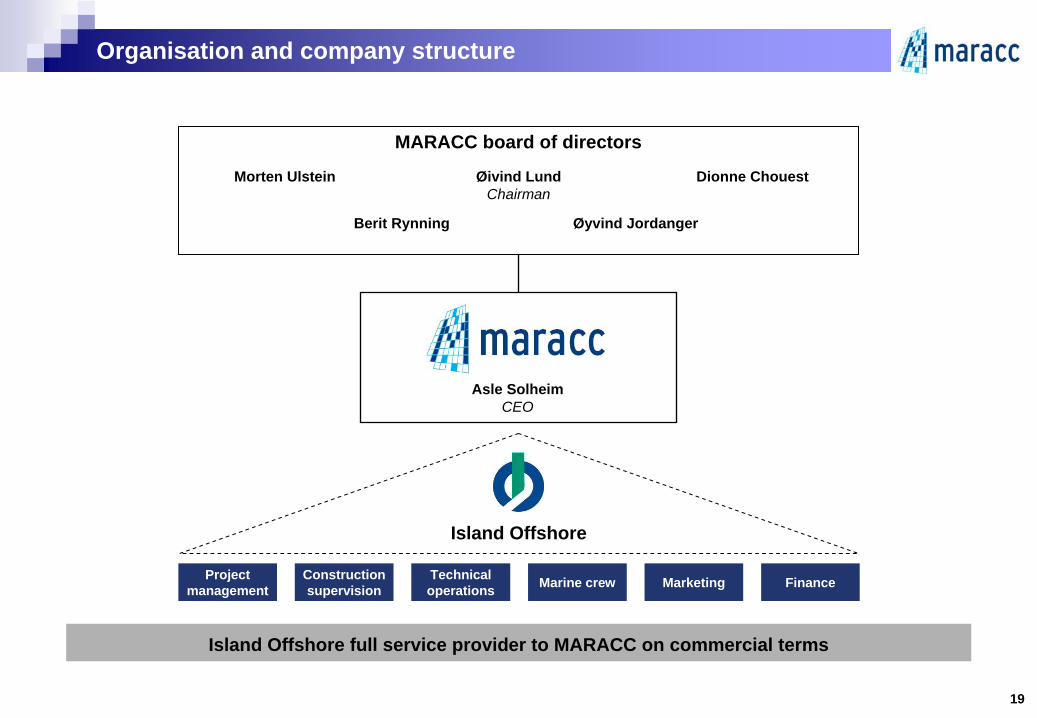

MARACC board of directors

Dionne ChouestØivind LundChairman

19

Organisation and company structure

Island Offshore

Morten Ulstein

Berit Rynning

Finance

Øyvind Jordanger

Asle SolheimCEO

Island Offshore full service provider to MARACC on commercial terms

Construction supervision

Has held various senior positions with ABB including CEO of ABB in Norway and President & Country Manager in TurkeyChairman of the board of directors of YaraHolds an MSc and a PhD in electrical engineering and a degree in industrial economy

Øivind LundChairman of the board

Dionne ChouestBoard member

Owner and officer of several of the Edison Chouest Offshore group companiesHas held the position as general counsel of the Edison Chouest Offshore group since 1993Holds a bachelor of science degree in accounting from Nicholls State University and a law degree from Tulane Law School

More than 25 years experience from the offshore and marine sectors both as investor and through various CEO positions (Rolls Royce Marine, Vickers Ulstein Marine Systems, Ulstein Industrier)Founder and chairman of Island Offshore, the leading well intervention company globally, and responsible for managing the Ulstein family’s investment companiesHolds an MSc in naval engineering from the Norwegian University of Science and Technology

Morten UlsteinBoard member

Experienced management and board of directors

Some 30 years experience from the oil & gas industry, mainly within drilling and operations, including MD of Dolphin for 6 years and thereafter President of Navion Inc (Navion ASA acquired by Teekay in January 2003)Currently holds the position as director of business development & offshore projects at TeekayHolds an MSc in petroleum engineering from the Norwegian University of Science and Technology

Øyvind JordangerBoard member

Manager for industry relations at the International Research Institute of Stavanger (IRIS)More than 35 years of experience from the oil & gas industry having held several senior positions within Statoil including country manager in Mexico, government relations manager in Venezuela and project manager in AlgeriaJournalist from the Oslo University College and London School of Journalism

Berit RynningBoard member

20

More than 20 years of relevant experience including MD of ABB Offshore Systems UKSince 2005, involved in developing subsea riserless well intervention solutions with FMC and Island OffshoreHolds a BSc in mechanical engineering from the University of Wisconsin at Madison

Asle SolheimCEO

Table of contents

1. Executive summary

2. Market opportunity

3. Project overview

4. Proposed restructuring

5. Financial overview

Appendix

A. Supporting slides

B. Risk factors

Background and considerations

During the last year, MARACC has been working along several tracks to address the remaining financing requirement, including conventional bank and / or bond financing, as well as export credit agencies both in China and Norway

However, none of these efforts have proven successful in light of the prevailing market conditions, perceived construction risk and lack of contract

In MARACC’s opinion, the only viable alternative is to raise short-term financing enabling MARACC to continue the construction process, and simultaneously continue its efforts to secure a contract and a financing solution for the remaining capex

In the absence of any short-term financing, the board of directors will be compelled to pursue formal insolvency proceedings

A potential sale of the project, especially in an insolvency situation, is believed to provide very limited recovery for stakeholders, including the secured bondholders

- Unit still ~2 years away from expected operation start-up- Significant construction work to be completed and financed

MARACC firmly believes that the prospects for the highest recovery for all stakeholders is obtained through the proposed restructuring and contemplated directed equity issue, and for MARACC to continue working to obtain a contract and fully finance the project

Noble Denton retained in February 2010 to provide a technical report assessing the status of the construction process and evaluating the completion date

- Noble Denton provided their report in April 2010; please see appendix for a brief summary of their key findings

22

23

Brief overview of the restructuring proposal*

Restructuring proposal involves a full conversion of all outstanding bonds (including accrued interest) into equity in order to secure new equity financing

- Senior secured bonds; 4.00 new shares issued in exchange for each $1.00 held (incl. accrued interest as per 31-May-10)- Convertible bonds; 1.20 new shares issued in exchange for each $1.00 held (incl. accrued interest as per 31-May-10)- no fractional shares to be issued (rounded down to the nearest whole new share)

Restructuring proposal subject to certain conditions, including (i) minimum NOKm 213 being raised in new equity capital (gross proceeds) at an issue price of NOK 0.45 per share, (ii) approval of the proposed restructuring by all outstanding bond issues, and (iii) approval by existing shareholders

Furthermore, provisions relating to mandatory offer obligations (40% ownership threshold) in MARACC’s articles of association shall be deleted as part of the proposed restructuring

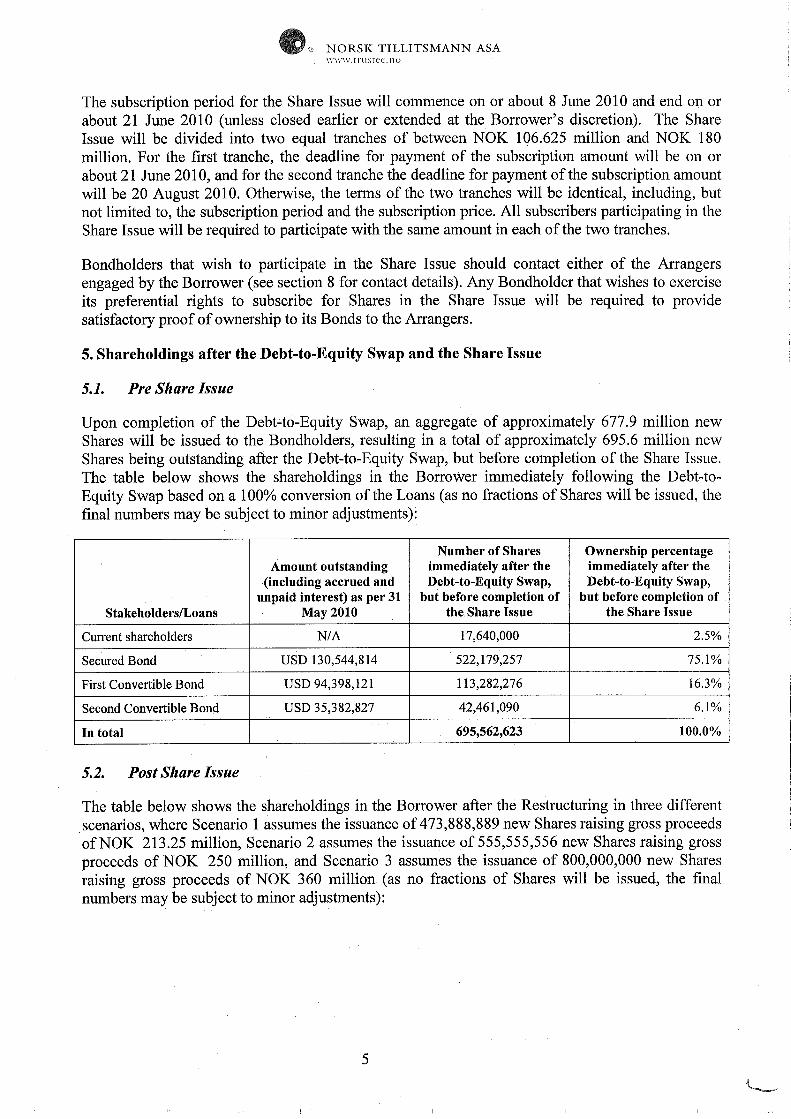

All existing stakeholders will be invited to subscribe for their pro rata share of the directed equity issue (based on equity interest post restructuring), avoiding further dilution by such participation

Senior secured bondholders to have an ownership of ~75% post restructuring (but before the directed equity issue), implying a recovery on nominal amount of ~31% based on the issue price of NOK 0.45 per share

NOTE: Amount outstanding including interest accrued as per 31 May 2010 but excluding USDm 1.0 of principal amount held by MARACC in the senior secured bond. Analysis based on NOK / USD exchange rate of 6.45

* PLEASE REFER TO THE SUMMONS DATED 2 JUNE 2010 FOR FURTHER DETAILS (AVAILABLE ON WWW.STAMDATA.NO)

Amount Proforma Proforma Implied conversion price Implied recoveryStakeholders o/s (USDm) shares (m) ownership NOK USD Nom. amount Amount o/s

Current equity owners - 17.6 2.5% - - - -Senior secured bond 130.5 522.2 75.1% 1.61 0.2500 31% 28%$80m convertible bond 94.4 113.3 16.3% 5.37 0.8333 10% 8%$30m convertible bond 35.4 42.5 6.1% 5.37 0.8333 10% 8%Total 695.6 100.0%

Proforma ownership post restructuring and directed equity issue

NOKm 213-360 to be raised in new equity capital through a contemplated private placement of shares- Conditional upon acceptance of the restructuring proposal and shareholders’ approval- Proceeds to be raised, and shares to be issued, in two equal tranches (1st tranche end June; 2nd tranche mid August)

Issue price of NOK 0.45 per share implying a pre-money equity value NOKm 313 (~USDm 49)

Minimum issue amount of NOKm 213 (~USDm 33) fully underwritten by key stakeholders- 2% underwriting fee payable-in-kind through issuance of 36 million warrants (ie. no cash cost to MARACC)- Warrants exercisable within 3 years at a subscription price of NOK 0.45 per share- Underwriting conditional upon acceptance of the restructuring proposal and shareholders’ approval

All existing stakeholders will be invited to subscribe for their pro rata share of the directed equity issue (based on equity interest post restructuring), avoiding further dilution by such participation

- Bondholders that wish to exercise their preferential rights to subscribe in the directed equity issue will be required to provide satisfactory proof of ownership to their bonds

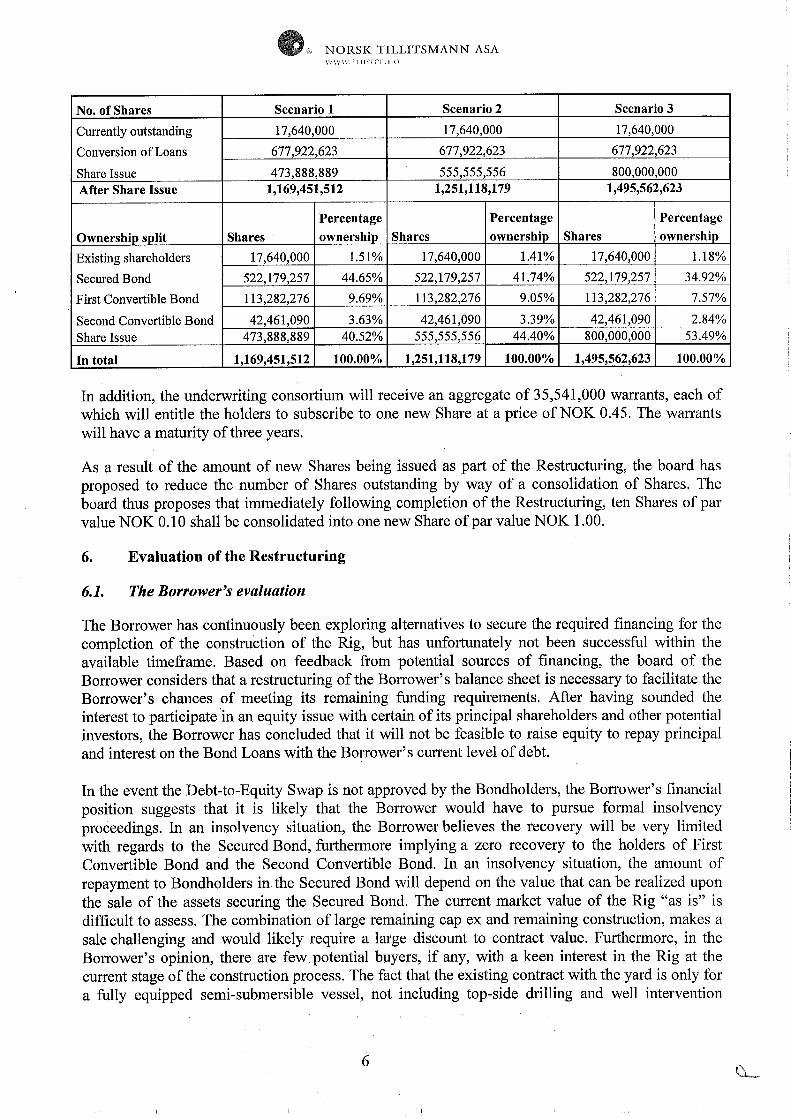

In the event of no participation, present stakeholders will be diluted, according to the proforma ownership table below- Not adjusted for the proposed 10:1 reverse share split following completion of the proposed restructuring and directed equity issue

24

Directed equity issue - gross proceeds raisedNOKm 213 NOKm 250 NOKm 360

Stakeholders Shares (m) Ownership Shares (m) Ownership Shares (m) Ownership

Current equity owners 17.6 1.5% 17.6 1.4% 17.6 1.2%Senior secured bond 522.2 44.7% 522.2 41.7% 522.2 34.9%$80m convertible bond 113.3 9.7% 113.3 9.1% 113.3 7.6%$30m convertible bond 42.5 3.6% 42.5 3.4% 42.5 2.8%New equity owners 473.9 40.5% 555.6 44.4% 800.0 53.5%Total 1,169.5 100.0% 1,251.1 100.0% 1,495.6 100.0%

NOTE: Analysis excluding 36 million warrants to be issued to underwriters upon completion of the directed equity issue (representing ~3% of shares o/s post issue)

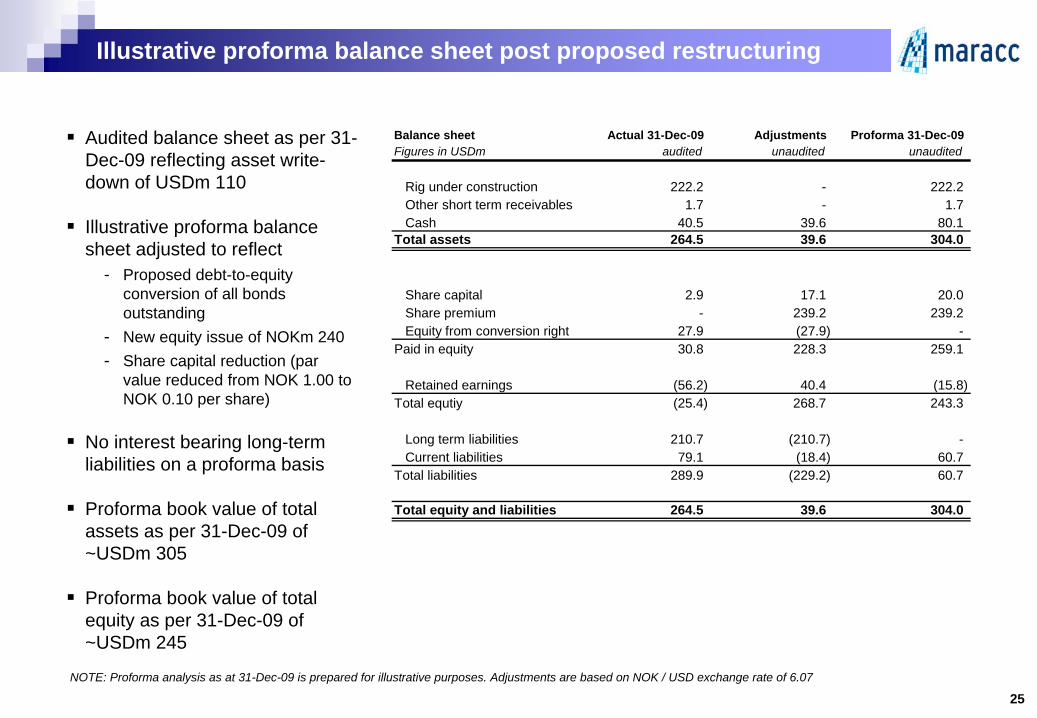

Illustrative proforma balance sheet post proposed restructuring

Audited balance sheet as per 31-Dec-09 reflecting asset write-down of USDm 110

Illustrative proforma balance sheet adjusted to reflect

- Proposed debt-to-equity conversion of all bonds outstanding

- New equity issue of NOKm 240- Share capital reduction (par

value reduced from NOK 1.00 to NOK 0.10 per share)

No interest bearing long-term liabilities on a proforma basis

Proforma book value of total assets as per 31-Dec-09 of ~USDm 305

Proforma book value of total equity as per 31-Dec-09 of ~USDm 245

25

Balance sheet Actual 31-Dec-09 Adjustments Proforma 31-Dec-09Figures in USDm audited unaudited unaudited

Rig under construction 222.2 - 222.2Other short term receivables 1.7 - 1.7Cash 40.5 39.6 80.1

Total assets 264.5 39.6 304.0

Share capital 2.9 17.1 20.0Share premium - 239.2 239.2Equity from conversion right 27.9 (27.9) -

Paid in equity 30.8 228.3 259.1

Retained earnings (56.2) 40.4 (15.8)Total equtiy (25.4) 268.7 243.3

Long term liabilities 210.7 (210.7) -Current liabilities 79.1 (18.4) 60.7

Total liabilities 289.9 (229.2) 60.7

Total equity and liabilities 264.5 39.6 304.0

NOTE: Proforma analysis as at 31-Dec-09 is prepared for illustrative purposes. Adjustments are based on NOK / USD exchange rate of 6.07

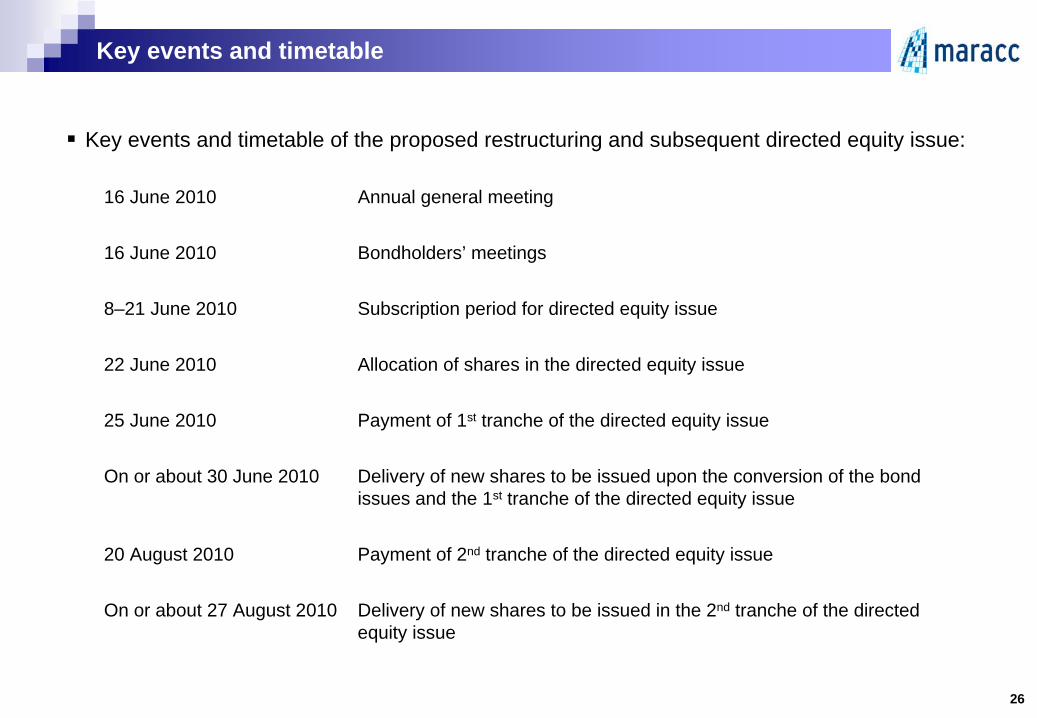

Key events and timetable

Key events and timetable of the proposed restructuring and subsequent directed equity issue:

16 June 2010 Annual general meeting

16 June 2010 Bondholders’ meetings

8–21 June 2010 Subscription period for directed equity issue

22 June 2010 Allocation of shares in the directed equity issue

25 June 2010 Payment of 1st tranche of the directed equity issue

On or about 30 June 2010 Delivery of new shares to be issued upon the conversion of the bond issues and the 1st tranche of the directed equity issue

20 August 2010 Payment of 2nd tranche of the directed equity issue

On or about 27 August 2010 Delivery of new shares to be issued in the 2nd tranche of the directed equity issue

26

Table of contents

1. Executive summary

2. Market opportunity

3. Project overview

4. Proposed restructuring

5. Financial overview

Appendix

A. Supporting slides

B. Risk factors

28

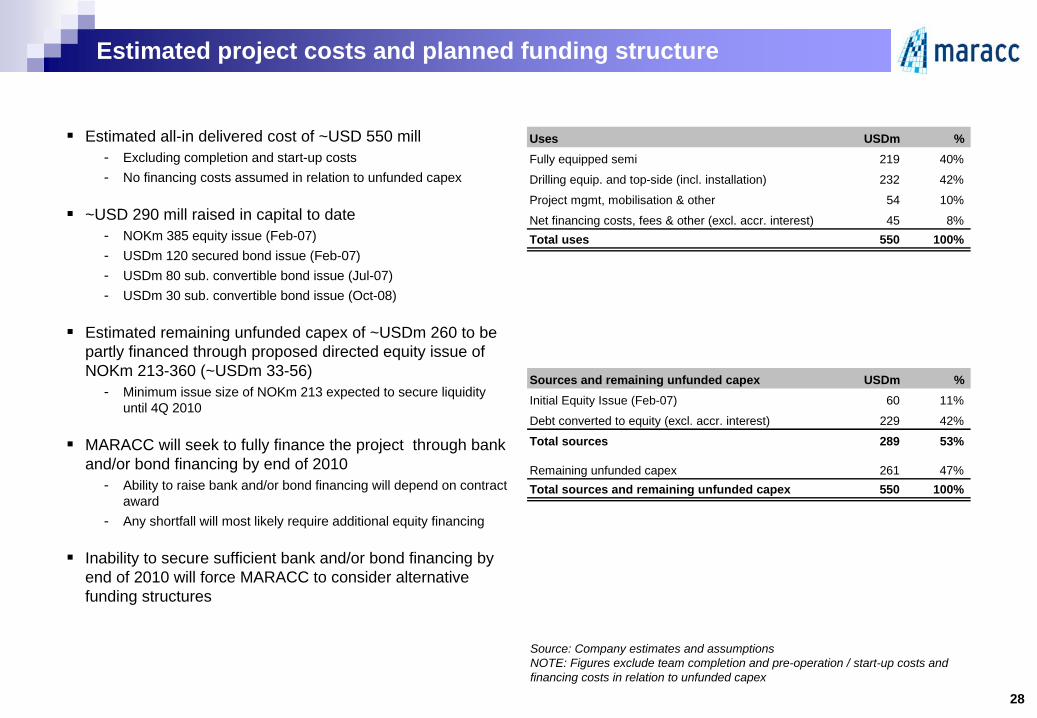

Estimated project costs and planned funding structure

Estimated all-in delivered cost of ~USD 550 mill- Excluding completion and start-up costs- No financing costs assumed in relation to unfunded capex

~USD 290 mill raised in capital to date- NOKm 385 equity issue (Feb-07)- USDm 120 secured bond issue (Feb-07)- USDm 80 sub. convertible bond issue (Jul-07)- USDm 30 sub. convertible bond issue (Oct-08)

Estimated remaining unfunded capex of ~USDm 260 to be partly financed through proposed directed equity issue of NOKm 213-360 (~USDm 33-56)

- Minimum issue size of NOKm 213 expected to secure liquidity until 4Q 2010

MARACC will seek to fully finance the project through bank and/or bond financing by end of 2010

- Ability to raise bank and/or bond financing will depend on contract award

- Any shortfall will most likely require additional equity financing

Inability to secure sufficient bank and/or bond financing by end of 2010 will force MARACC to consider alternative funding structures

Source: Company estimates and assumptionsNOTE: Figures exclude team completion and pre-operation / start-up costs and financing costs in relation to unfunded capex

Uses USDm % Fully equipped semi 219 40%

Drilling equip. and top-side (incl. installation) 232 42%

Project mgmt, mobilisation & other 54 10%

Net financing costs, fees & other (excl. accr. interest) 45 8%Total uses 550 100%

Sources and remaining unfunded capex USDm % Initial Equity Issue (Feb-07) 60 11%

Debt converted to equity (excl. accr. interest) 229 42%

Total sources 289 53%

Remaining unfunded capex 261 47%Total sources and remaining unfunded capex 550 100%

29

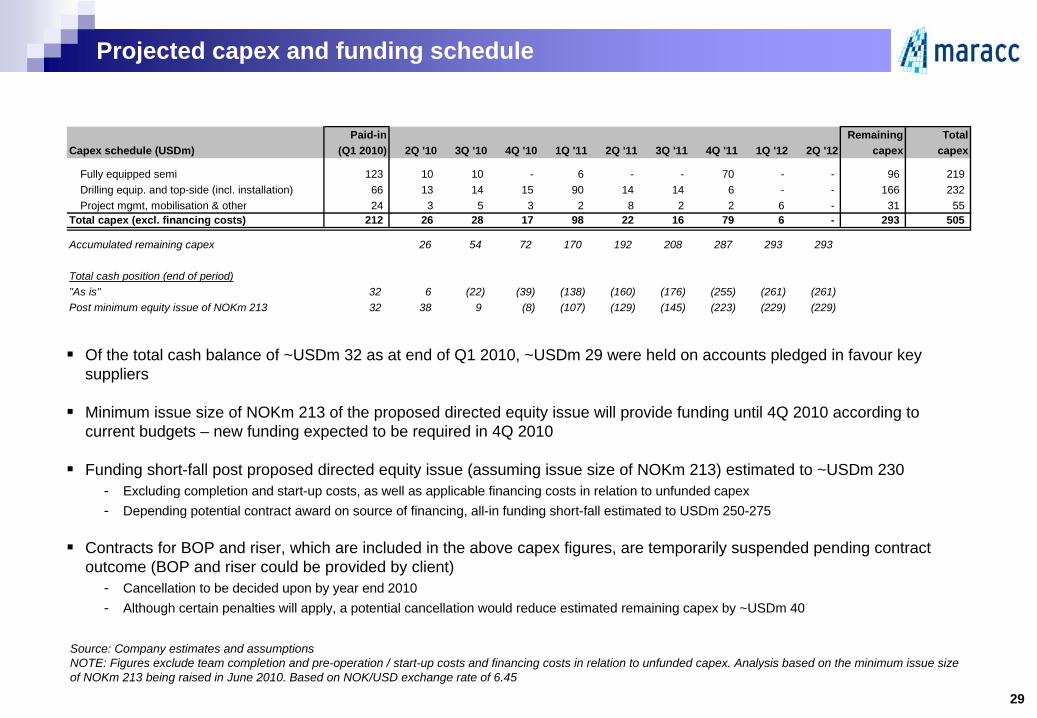

Projected capex and funding schedule

Of the total cash balance of ~USDm 32 as at end of Q1 2010, ~USDm 29 were held on accounts pledged in favour key suppliers

Minimum issue size of NOKm 213 of the proposed directed equity issue will provide funding until 4Q 2010 according to current budgets – new funding expected to be required in 4Q 2010

Funding short-fall post proposed directed equity issue (assuming issue size of NOKm 213) estimated to ~USDm 230- Excluding completion and start-up costs, as well as applicable financing costs in relation to unfunded capex- Depending potential contract award on source of financing, all-in funding short-fall estimated to USDm 250-275

Contracts for BOP and riser, which are included in the above capex figures, are temporarily suspended pending contract outcome (BOP and riser could be provided by client)

- Cancellation to be decided upon by year end 2010- Although certain penalties will apply, a potential cancellation would reduce estimated remaining capex by ~USDm 40

Source: Company estimates and assumptionsNOTE: Figures exclude team completion and pre-operation / start-up costs and financing costs in relation to unfunded capex. Analysis based on the minimum issue size of NOKm 213 being raised in June 2010. Based on NOK/USD exchange rate of 6.45

Paid-in Remaining TotalCapex schedule (USDm) (Q1 2010) 2Q '10 3Q '10 4Q '10 1Q '11 2Q '11 3Q '11 4Q '11 1Q '12 2Q '12 capex capex

Fully equipped semi 123 10 10 - 6 - - 70 - - 96 219Drilling equip. and top-side (incl. installation) 66 13 14 15 90 14 14 6 - - 166 232Project mgmt, mobilisation & other 24 3 5 3 2 8 2 2 6 - 31 55

Total capex (excl. financing costs) 212 26 28 17 98 22 16 79 6 - 293 505

Accumulated remaining capex 26 54 72 170 192 208 287 293 293

Total cash position (end of period)"As is" 32 6 (22) (39) (138) (160) (176) (255) (261) (261)Post minimum equity issue of NOKm 213 32 38 9 (8) (107) (129) (145) (223) (229) (229)

30

Illustrative financials and valuation metrics (fully invested)

Base case illustrative financials assume long-term contract at USD 375’ / day, opex of USD 165’ / day and successful completion of proposed restructuring and directed equity issue

Illustrative financials assume completion of the proposed restructuring and directed equity issue (minimum issue size of NOKm 213)

Project assumed fully financed through new debt financing of USDm 270

- No additional equity capital assumed other than the minimum issue size of the proposed directed equity issue

- Working cap requirement and start-up costs at delivery of USDm 25 assumed

Assumed capital structure yielding a fully invested mid-year EV of ~USDm 325

Assumed asset value at delivery of USDm 450-500 providing significant valuation upside

- Corresponding to 100-150% equity upside potential

Base case illustrative financials underpins solid cash flow generation and attractive valuation on a fully invested basis

- EV / EBITDA of 4.8x- P / E of 3.0x- Equity pay-back time of ~2 years

Source: Company estimates and assumptionsNOTE: Net interest expense based on opening balance figures. Analysis based on NOK / USD exchange rate of 6.45 and excluding 36 million warrants to be issued to underwriters upon completion of directed equity issue

Low Base UpperKey Assumptions Case Case CaseAve Daily Rate USD / day 350,000 375,000 400,000Ave Daily Opex USD / day 165,000 165,000 165,000Impl. EBITDA day rate USD / day 185,000 210,000 235,000Utilisation Rate 95% 95% 95%Effective Cash Tax Rate 10% 10% 10%

Summary P&LSales USDm 121 130 139

Opex " (59) (59) (59)Mgmt Incentive Fee " (2) (3) (3)

EBITDA " 59 68 76Depreciation " (18) (18) (18)

EBIT " 41 50 58Net Interest Expense " (20) (20) (20)Tax Expense " (2) (3) (4)

Net Profit " 20 27 35

Capitalisation and ValuationCurrent shares o/s m 1,169.5 1,169.5 1,169.5Share Price NOK 0.45 0.45 0.45Share Price USD 0.07 0.07 0.07

= Market Value of Equity USDm 82 82 82- Cash (mid-year) " 25 29 33+ Bank Debt " 270 270 270= EV (fully invested) " 326 323 319

EV / EBITDA 5.5x 4.8x 4.2xP / E 4.2x 3.0x 2.4xROE (at market) 24% 33% 42%ROCE (EBIT / cap empl at market) 13% 15% 18%

Table of contents

1. Executive summary

2. Market opportunity

3. Project overview

4. Proposed restructuring

5. Financial overview

Appendix

A. Supporting slides

B. Risk factors

32

Island Innovator – technical specifications

Fully equipped semi-submersible vessel

Loa 106.00m

Bm 65.00m

Dm 35.85m

D 8.50m – 17.75m

Displacement 21,100 – 34,000 tons

Deck load capacity 4,000 tons

Safety certificate 120 persons

Cabins Single cabins: Fixed 120, according to NMD / NORSOK req.

Helideck Sikorsky S61-N, S-92, Super Puma, Sikorsky S92

DP system Kongsberg Maritime SDP-22 + SDP-12 back-up

Engines 6 x 5,600 kW diesel generator,

1 x 1,138 kVA emergency generator

Thrusters 6 x 3.8 MW (68 tons) fixed pitch, controllable speed

Ballast pumps 4 off, combined capacity 3,000 m3 / h

Deck cranes 1 x 15T / 30T SWL @ 42m radius offshore

1 x 15T / 30T SWL @ 50m radius offshore

1 x 75T port crane

Offshore crane 1 x 165T AHC heavy lift, 50m reach

Winches 4 double winches for wire 750 tons

Well intervention and drilling equipment

Dynamic hook load 650 short tons

Max drilling depth 8,000m

Max water depth Drilling: 1,250m / Intervention: 3,000m

Key findings from Noble Denton report

Noble Denton’s key findings MARACC’s response

33

Delivery from COSCO and final deliveryDelivery from COSCO estimated Oct-11Implies final delivery late May-12 in Norway

Integration risksDrilling Equipment System interface is a critical componentIntegration contract should be entered as soon as possible, to reduce / avoid interface issuesInterface issues could cause schedule and cost impacts

Rig capacity with regards to 1,300m drilling riserQuestioning rig capacity with regards to riser loads for 1,300m drilling riserTwo mud pumps installed, three required for conventional drilling

Completion reportingReports show 75% and 0.65% weekly progressNoble Denton assessment is 60% complete and 0.6% weekly progress

WeldingVery low findings of weld defectsNoble Denton recommends a third party to verify numbers

Top-side installation at COSCO will move out delivery date but secure ready-for-operation date in 2Q 2012 as a full completion at COSCO will improve overall efficiencyExpects final delivery 2Q 2012, inline with Noble Denton’s estimates

Interfaces are tightly monitored and controlled to reduce risks Contract of integration is now being considered with COSCO to address integration concerns and obtain higher efficiencyCOSCO has now gained top-side installation experience on Sevan Driller and is therefore considered a good alternative to NYMO

The rig is preferably used for drilling to 750mRiser above 1,000m will have to be supplied from separate supplyvesselHalliburton to provide third mud pump (combined cement and mud pump)

COSCO reports 76% complete (10-May-10), however, the weighting of the commissioning activities are regarded too low and is expected to take time which is now allowed for

Close to 21 km inspected and results have been acceptableBoth DnV and an independent Norwegian survey company has been used to verify welds

Management agreement with Island Offshore – key terms

Construction supervision- Oversee the builder’s performance of the construction contract- Responsible for developing the top-side specifications- Oversee the progress and performance of the Owner Furnished Equipment (OFE)- Represent MARACC at commissioning, tests and trials

Business management services- General administrative and advisory services in connection with the management of the vessel- Post-delivery technical management (including crewing and insurance) of the vessel- Marketing of the vessel for employment and / or sale

Management fees- Construction period: ~USD 2 mill in construction management fee per quarter (incl. project management team, yard

supervision and company G&A)- After completion: Fixed daily management fee of USD 5,000 and incentive fee of 4% of EBITDA

Termination- Island Offshore Management may terminate in the event of a change of control occurring in MARACC- MARACC may terminate in the event of a change of control occurring in Island Offshore Management or Island

Offshore, or in case of Island Offshore reducing its ownership in MARACC to below 10% of the share capital- In the event of a sale of vessel or MARACC change of control event occurring, Island Offshore Management is entitled

to a termination fee of 2% of MARACC’s enterprise value

Confidential

34

A leading provider of vessels and services to the offshore oil industry in the North Sea

- Some 20 vessels under management including 4 well intervention units

Strategic co-operation with US based Edison Chouest Offshore in the Gulf of Mexico and South America, the World’s second largest offshore supply company (privately held)

Riser Less Well Intervention (RLWI) alliance with FMC and Aker Solutions established in 2004

- RLWI operations successfully performed for Statoil (~90 wells), BP (4 wells) Chevron (1 well) and Nexen (2 wells)

Island FrontierMay 2004 Statoil

Fixed contract: 2010–2013

Built / Delivery Comments

Island WellserverMay 2008 Statoil

Fixed contract: 2008–2011+ 3 year option

Island ConstructorJul 2008 BP

Fixed contract: 2008 – 2010+ 2 x 1 year option

Island InnovatorQ2 2012 (exp.) Currently being marketed in key

markets (North Sea and GoM)

Island Offshore – company overview

35

Well intervention fleet

Vessel

Table of contents

1. Executive summary

2. Market opportunity

3. Project overview

4. Proposed restructuring

5. Financial overview

Appendix

A. Supporting slides

B. Risk factors

GENERALInvesting in MARACC involves inherent risks. Prospective investors should consider, among other things, the risk factors set out below before making an investment decision. Any of the risks described below could have a material adverse impact on MARACC’s business, financial condition and results of operations and could therefore have a negative effect on the trading price of any securities issued by MARACC and affect a prospective investor's investment. The information below does not purport to be exhaustive. Additional risks and uncertainties not presently known to MARACC or that MARACC currently deems immaterial may also have a material adverse effect on MARACC’s business, financial condition and operating results.An investment in MARACC is suitable only for investors who understand the risk factors associated with this type of investment and who can afford a loss of all or part of the investment. Such information is presented as of the date hereof and is subject to change, completion or amendment without notice.

OPERATIONAL AND CONSTRUCTION RISKConstruction risksMARACC’s only rig is under construction. The construction process is complex and the yard constructing the fully equipped semi-submersible vessel to be used for the rig has limited experience in constructing offshore vessels. The process has already suffered some delays and cost overruns and this is not uncommon for new builds in the industry. Although MARACC is of the opinion that the construction process is under control and should be completed according to the revised schedule without any further increased costs, there can be no assurances that further delays and cost overruns will not occur.MARACC has entered into fixed priced contracts on a pre-agreed scope in connection with the production of the rig. Should further change orders prove necessary, this may lead to increased costs and/or delays.Several suppliers will deliver equipment and/or services in connection with the production of the rig. In addition the project will be dependent on a successful integration of different equipment packages and modules. MARACC itself is also responsible for certain parts of the production and utilises sub- contractors in this regard. Should MARACC, its suppliers or any other involved party not be able to satisfactory perform their duties under the construction agreements, this may lead to delays or increased costs, which again could have a negative affect on the value of the securities issued by MARACC.Outsourced managementMARACC relies on Island Offshore Management’s ability to provide project management and management services to MARACC. Any failure in the provision of these services may have a material adverse impact on MARACC’s business and MARACC’s financial results and operations. As a consequence of the management agreement, the holders of securities issued by MARACC generally have limited possibilities to participate in and influence the management of MARACC.Political and regulatory risksChanges in the legislative and fiscal framework governing the activities of the oil companies could have a material impact on exploration and development activity in general and could also affect MARACC’s operations directly. In particular, changes in political regimes will constitute a material risk factor for MARACC’s operations in foreign countries. Risk of war, other armed conflicts and terrorist attacks War, military tension and terrorist attacks have caused instability in the world’s financial and commercial markets. This has in turn significantly increased political and economic instability in some of the geographic markets in which MARACC operates (or may operate in the future) and has contributed to high levels of volatility in prices for among other things oil and gas. Continuing instability may contribute to even higher level of volatility in prices. In addition, acts of terrorism and threats of armed conflicts in or around various areas in which MARACC operates (or may operate in the future) could limit or disrupt MARACC’s markets and operations, including disruptions from evacuation of personnel, cancellation of contracts or the loss of personnel or assets.

Risk factors

37

MARACC may assume substantial liabilitiesIt should be emphasised that contracts in the offshore sector require high standards of safety, and it is important to note that all offshore contracts are associated with considerable risks and responsibilities. These include technical, operational, commercial, financial and political risks. MARACC will obtain insurances deemed adequate for its business, but it is impossible to insure against all applicable risks and liabilities. For instance, under some contracts MARACC may have unlimited liability for losses caused by its own gross negligence, whereas such liability in general will not be covered by insurance policies. MARACC may also incur liability for pollution and other environmental damage without being able to recover said liabilities through insurances.Service life and technical risksThe service life of a new rig is generally assumed to be more than 30 years, but will ultimately depend on its capability. There can be no assurance that MARACC’s rigs will be successfully deployed for such period of time. There will always be some exposure to technical risks, with unforeseen operational problems leading to unexpectedly high operating costs and/or lost earnings, which may have a material adverse effect on the financial position of MARACC.

COMMERCIAL RISKDrilling contracts and employment of rigsEven if MARACC will utilise its current resources in its endeavours to ensure that charter agreements with customers are secured for the rig, no such charter agreement has yet been secured and no assurances can be given that MARACC will be sufficiently successful in deploying its rig. A delay or failure in obtaining a contract for the rig may have a material adverse impact on the financial position of MARACC.There is often considerable uncertainty as to the duration of offshore drilling contracts because the agreements may give the operator both extension and early cancellation options. There can also be off-hire periods between contracts. The cancellation or postponement of one or more contracts can have a material adverse impact on the earnings of drilling companies, including MARACC.Oil prices Historically, demand for offshore exploration, development and production has been volatile and closely linked to the price of hydrocarbons. Low oil prices typically lead to a reduction in exploration drilling as the oil companies scale down their investment budgets. The sharp reduction in production costs on new oil fields and the increase in the use of drilling rigs for production drilling will probably to some extent reduce the strong historical correlation between rig rates and oil prices. Nevertheless, a decrease in the oil and gas prices may have a material adverse impact on the financial position of MARACC.Limited operating historyMARACC is a relatively recently formed entity and has limited operating history and only financial information for a limited period of time upon which prospective investors can evaluate MARACC’s future performance. Concentration MARACC has no restrictions relating to the diversification or concentration of its assets. However, as MARACC’s assets are concentrated in a single industry, MARACC may be more vulnerable to particular economic, political, regulatory, environmental or other developments than a company holding a more diversified portfolio of assets, and the aggregate return of MARACC will be substantially adversely affected by unfavourable performance of its assets.Intellectual property rightsMARACC must observe third parties’ patent rights and intellectual rights. There is always an inherent risk of third parties claiming that the technology being utilised in the construction of MARACC’s rigs or in its operations infringes third parties’ patents or intellectual property rights, and any such claim, if successful, could have a material adverse effect on MARACC’s results of operation.

Risk factors (cont’d)

38

FINANCIAL RISKFunding of MARACC’s rigMARACC has not yet obtained all the funding required for MARACC’s investments in the rig and further substantial financing will be necessary in the future. Should MARACC not succeed in obtaining financing on satisfactory terms, this may adversely affect the value of an investor’s investments.Interest rate and currency fluctuationsMARACC will be exposed to risks due to fluctuations in interest and exchange rates. MARACC may attempt to minimise these risks by implementing hedging arrangements as appropriate, but will not be able to avoid these risks.Since MARACC’s financial reporting is in NOK, while the income and expenses of MARACC are primarily in USD, currency fluctuations may influence the value of any securities issued by MARACC. The value of non-NOK currency denominated charter contracts and indebtedness will be affected by changes in currency exchange rates or exchange control regulations. Currency exchange rates are determined by forces of supply and demand in the currency exchange markets. These forces are affected by the international balance of payments, economic and financial conditions, government intervention, speculation and other factors. Changes in currency exchange rates relative to NOK may affect the NOK value of MARACC’s assets and thereby impact upon MARACC’s total return on such assets. Currency fluctuations relative to NOK of an investor’s currency of reference may adversely affect the value of an investor’s investments. Borrowing and leverageBorrowings create leverage. To the extent income derived from assets obtained with borrowed funds exceeds the interest and other expenses that MARACC will have to pay, MARACC’s net income will be greater than if borrowings were not made. Conversely, if the income from the assets obtained with borrowed funds is not sufficient to cover the cost of such borrowings, the net income of MARACC will be less than if borrowings were not made. MARACC will borrow only when it believes that such borrowings will benefit MARACC after taking into account considerations such as the costs of the borrowings and the likely returns on the assets purchased with the borrowed monies, but no assurances can be given that MARACC will be successful in this respect.

RISK FACTORS RELATING TO THE SECURITIES ISSUED BY MARACCInvestment and trading risks in generalAny investment in securities issued by MARACC is associated with an element of risk. MARACC operates in a market featuring open and fierce competition, and a number of factors outside MARACC’s control may affect its performance. The price of the securities will also be subject to fluctuations in line with general movements in the capital markets and the liquidity in the secondary market. Historically, the earnings of offshore service companies and the value of the equipment used have seen major fluctuations.Price volatility of publicly traded securitiesThe shares issued by MARACC are not listed on any stock exchange or similar market, and no plans currently exist to apply for any such listing. Although the shares have been registered on the Norwegian OTC market, there is no assurance that investors can realize any part of the value of their investments. In addition, the liquidity and the market price of the shares may be adversely affected by changes in the overall market for similar securities, MARACC’s financial performance or prospects or in the prospects for companies in its industry generally.

Risk factors (cont’d)

39