1st view - welcome to willis re · sidecar capacity works well for reinsurers in writing the more...

TRANSCRIPT

Page 1

1ST VIEW1 July 2012

Page 2

RENEWALS – 1 July 2012

Introduction 3Property Territory and Comments 4 Rates 5 Pricing Trend Graphs 6Casualty Territory and Comments 7 Rates 7Specialties Line of Business and Comments 8 Rates 9Capital Markets Comments 9Workers’ Compensation Comments 9 Rates 9

1st ViewThis thrice yearly publication delivers the very first view on current market conditions to our readers. In addition to real-time Event Reports, our clients receive our news brief, The Daily Willis ReView, periodic newsletters, white papers and other reports.

Willis ReGlobal resources, local delivery For over 100 years, Willis Re has proudly served its clients, helping them obtain better value solutions and make better reinsurance decisions. As one of the world’s premier global reinsurance brokers, with 40 locations worldwide, Willis Re provides local service with the full backing of an integrated global reinsurance broker.

© Copyright 2012 Willis Limited / Willis Re Inc. All rights reserved: No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, whether electronic, mechanical, photocopying, recording, or otherwise, without the permission of Willis Limited / Willis Re Inc. Some information contained in this report may be compiled from third party sources we consider to be reliable; however, we do not guarantee and are not responsible for the accuracy of such. This report is for general guidance only, is not intended to be relied upon, and action based on or in connection with anything contained herein should not be taken without first obtaining specific advice. The views expressed in this report are not necessarily those of the Willis Group. Willis Limited / Willis Re Inc. accepts no responsibility for the content or quality of any third party websites to which we refer. Willis Limited, a Lloyd’s broker is authorized and regulated by the Financial Services Authority.

TABLE OF CONTENTS

Page 3

Peter C. HearnChairman, Willis Re1 July 2012

Looks can be deceiving

After another quarter of modest loss activity across both the International and North American markets, June 1 and July 1 reinsurance renewals produced a continuation of the highly segmented approach which had emerged over the last 12 months. Headline figures forecasting reasonable rate increases have been largely driven by loss activity. The impact of model change and macro-economic factors have played an increasingly muted role. As presented in this report, some buyers with loss-free programs, even in areas of peak exposure, have managed to obtain risk-adjusted rate reductions.

The targeted underwriting approach taken by most reinsurers has been welcomed by cedents. They have seen their efforts to manage, analyze and, in some cases, de-risk their portfolio(s) rewarded in differential pricing. This approach does not support a generalized market hardening to the frustration of some reinsurers.

Major changes in some vendor catastrophe models over the past 12 months, along with regulatory pressures, have driven a continued move towards more customized catastrophe modeling, including the use of multiple models and client-specific applications. While this has assisted primary reinsurance buyers with good quality original data, this trend is not so apparent in the retrocession market where reinsurers are facing less flexibility from their retrocessionaires in terms of differentiated catastrophe modeling.

While the pace of mergers and acquisitions among traditional reinsurers continues, there has been a marked increase in the flow of capital into non-traditional vehicles. Hedge fund investors are increasingly being joined by longer term investors, in particular pension funds, who are attracted to the non-correlated returns available in reinsurance risk.

The increase in capital and capacity is flowing not only into catastrophe bonds, as witnessed by the issue of the first Workers’ Compensation catastrophe bond, the recent completion of a US $750M bond offering by Florida Citizens and the projected full year new catastrophe bond issuance of US $5.5B to $6B, but also into sidecar capacity for existing reinsurers. Access to third party sidecar capacity works well for reinsurers in writing the more capital-intensive areas of property reinsurance such as Florida and retrocessional.

While the influx of capital is clearly welcomed by buyers and has helped stabilize rate increases, underlying concerns remain over the durability of highly fungible capital. Much of it is untested and conditioned by investor reaction to a major catastrophe event(s). Potential volatility is heightened by single source investors versus funds or sidecars comprised of multiple investors.

Unfortunately, with many of the existing reinsurers trading below book value, the attractiveness of investing in more traditional, permanent capital structures is not readily apparent. It is clear that the damping impact on rates due to the influx of new capital is frustrating for existing reinsurers who are battling concerns over falling investment income and dwindling reserve releases.

Analysis of recent investment returns clearly shows that most reinsurers’ ‘satisfactory’ investment returns in 2011 were derived from capital gains arising from falling interest rates and tightening bond spreads on ‘safe haven’ bonds. There may however be payback for these surpluses; these gains, when reinvested in a low rate environment, yield a series of lower cashflows and - once interest rates start to rise or sentiment changes on safe haven bonds - reinsurers face potential capital loss on falling values in their bond portfolios, particularly in the long-dated portions. Curiously, despite the fact this scenario is well known in industry circles, pricing on longer tail classes remains soft despite these warning signs to reinsurer’s balance sheets. The eventual increase in interest rates, coupled with a likely increase in inflation, could potentially trigger a hard market ahead of significant loss events.

Against this demanding background, traditional reinsurers face the challenge of earning an acceptable return on their capital. However, despite their own difficulties, most reinsurers remain focused on providing their clients with differentiated support.

Page 4

Property – territory and comments

Australia• Several catastrophe excess of loss programs now include coverage of flood event losses for the

first time• Catastrophe excess of loss market at renewal was relatively “bespoke,” depending on loss

activity of individual client, extent of flood coverage and portfolio differentiability• Per risk excess of loss pricing was dependent on individual clients’ claims activity and portfolio

differentiability• Some adverse loss development on Brisbane flood and Cyclone Yasi claims, impacting pricing

on some programs

Caribbean• Continued pressure from reinsurers on original rates in the islands, particularly Barbados and

Jamaica • Pricing remains market-driven and not unduly affected by model change

China• Renewal pricing is relatively stable for risk cover • Slightly increased pricing for non-earthquake cover, even for loss free programs (0% to +5%) • Increased pricing for earthquake cover, especially on higher layers with big capacity, even for

loss free programs (0% to +15%) • Retrocession pricing is significantly increased, even for loss free programs (0% to +40%) • Capacity for risk cover and catastrophe cover is adequate

Latin America• The period of July, 2011 through today has remained free of any notable catastrophe events• Catastrophe prices are relatively stable with small increases applicable largely related to

increased capacity demand on some programs• Proportional treaty renewals have no clear trend across the region with variations on

individual treaties, terms and conditions• There has been an increase in frequency and size of per risk losses across the region over the

past 3 years• Appetite for risk excess of loss business in general is being tempered with price movements

strictly following results

Middle East• Retrocession capacity for the Middle East based reinsurers has shown an increase• Event limits and cession limits are now being imposed on markets which did not include them

historically• Political Violence limitations are being implemented• Tightening of territorial scope of insurers and reinsurers operating within the region• Increase in automatic capacity being given to some of the larger players within the region• Increased retention being imposed by leaders

Page 5

South Africa• Commision on pro rata treaties remain as expiring or are moving downwards dependent on result • Catastrophe pricing is increasing on a risk-adjusted basis • Risk excess of loss pricing is moving up based on risk-adjusted pricing and loss experience

U.S. – Nationwide• International catastrophe losses have reduced reinsurer appetite for national accounts with worldwide exposures • Capacity remains adequate although the impact of the collateralized markets is not as noticable on commercial accounts • Non-modeled perils being analyzed more closely following 2011 activity • Pricing below the double digit rate increases that were targeted by reinsurers leading into June and July renewals

U.S. – Regional• Capacity remains adequate supplemented by additional capacity from collateralized markets • Pricing mostly down with increases limited to loss impacted programs or where buyers seeking significant new limit due to

growth in new regions • Greater reinsurer appetite for single state placements than for super regional accounts • Some reinsurers cut back on top layers with minimum rates on line

Rates

Property rates

TerritoryPro rata

commissionRisk loss free

% changeRisk loss hit %

change

Catastrophe loss free %

change

Catastrophe loss hit %

changeAustralia 0% 0% to +10% various 0% to +10% +5% to +25%

Caribbean 0% 0% various +5% to +10% N/A China N/A 0% to -5% +10% to +25% 0% to +15% N/A

Latin America +1% to -5% -5% to +5% +5% to +25% 0% to +5% N/A Middle East 0% +5% to +10% +10% to +15% +10% +20% to +35% South Africa 0% +5% +10% +5% +10%

U.S. – National 0% 0% +2.5% to +7.5% 0% to +5% +2.5% to +7.5%U.S. – Regional N/A 0% +2.5% to +7.5% -10% to +5% +5%

Page 6

Australia

U.S. – Nationwide

The charts on these pages display estimated year-to-year Property catastrophe rate movement, using 100 in 1990 as a baseline.

Property Catastrophe pricing trends

Caribbean

Australia

0

100

200

300

400

500

600

Caribbean

0

100

200

300

400

500

600

U.S.A.

0

100

200

300

400

500

600

Page 7

Casualty – territory and comments

Australia – General Liability / Employers’ Liability / Professional Liability• There is abundant capacity across all classes of liability business• No major changes to exclusionary language• Pricing has been influenced by reinsurers’ return requirements• Specific loss experience has become more of an issue

South Africa• Pricing moving upwards on a risk-adjusted basis

U.S. – General Liability• Appetite for general liability is steady to softening• Primary companies continue to increase retention

U.S. – Motor• The market is stable

U.S. – Professional Liability• Stable market, both insurance and reinsurance• Reinsurers generally supportive of long term buyers• Rates generally flat, with some small decreases for quality accounts and some increases being seen for the first time in 9 years

for more difficult accounts

Rates

Casualty rates

Territory Pro rata commissionXL – No loss emergence

% changeXL – With loss emergence

% changeAustralia N/A 0% to +2.5% +2.5% to +5%

Caribbean – Motor 0% 0% +5% to +10%South Africa N/A +5% +10%

U.S. – General Liability +1% to +1.5% 0% to -3% 0% to +3%U.S. – Motor 0% to +1.5% 0% 0% to +3%

U.S. – Professional Liability 0% 0% to -5% 0% to +5%

Page 8

Specialties – line of business and comments

Healthcare – U.S.• Reinsurance market conditions for Medical Professional Liability business remain favorable• Reinsurance pricing has been flat-to-falling, reflective of moderated loss trends and stable underlying rates• Reinsurance markets generally receptive to supporting required limit capacity• High quality reinsurance capacity is plentiful

Marine• Pricing levels generally flat other than upwards pressure on Energy-related business • Continuing capacity shortages for Energy and International Group of Protection & Indemnity Clubs reinsurance program-

exposed business • Capacity plentiful for straightforward Hull and Cargo portfolios • Although little affected business renews at 1st July, the market impact of “Costa Concordia” will depend on the ultimate

quantum of the liability loss

Medical Excess – U.S.• Per person excess of loss medical reinsurance capacity continues to be stable and competitive• There is growing trend and interest toward aggregate only medical reinsurance, where capacity is limited

Non-Marine Retrocession• Sufficient traditional capacity and ample collateralized capacity with new / renewed sidecars and a number of new funds• Continued pressure from reinsurers to limit scope to named territories and named perils• A benign first half of the year – especially in comparison with 2011 – is allowing buyers to consider their appetite for retaining

more risk• In general, retrocession price increases mostly held to a similar level as the start of the year, although programs with Thai flood

claims (whose scale is still uncertain) experienced much larger price increases in line with exposure• The Industry Loss Warranty market was sluggish in late May / early June, however plentiful capacity (following the over-

subscribed Florida renewals) has led to sizeable price reductions and activity increasing again entering the U.S. wind season

Political Risk• As expected, the credit crunch and resultant global recession has continued to have an impact on the political risks market• The ever changing Euro zone crisis continues to be of concern to both clients and reinsurers• Egypt had begun to show signs of stability, but in light of very recent events, the market remains cautious, while monitoring

developments• Insurers / reinsurers also watching Argentina, given the recent posturing of the President • Overall, the market is generally stable; in spite of the France’s banking sector problems, enquiry level remained high for the

second quarter• Political Risk / Contract Frustration pricing continues to be competitive, with Credit rates often more attractive; reinsurance

capacity available from both new and existing reinsurers, but leading capacity still relatively limited

Page 9

Rates

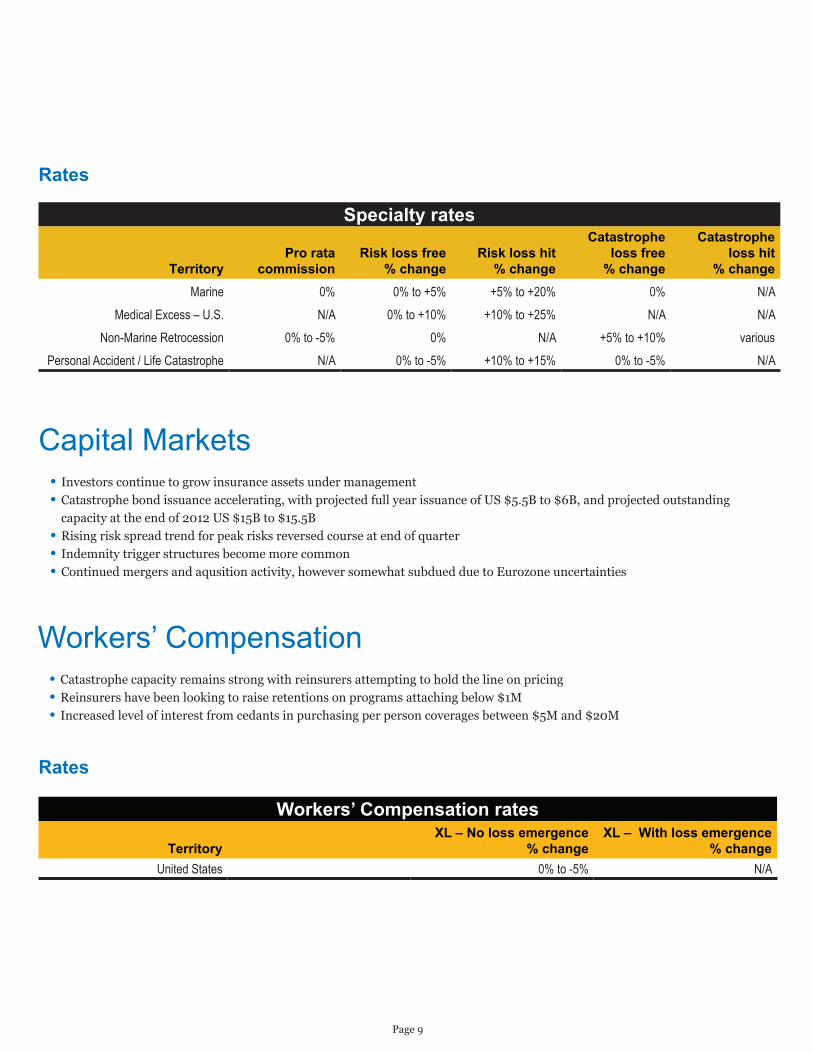

Specialty rates

TerritoryPro rata

commissionRisk loss free

% changeRisk loss hit

% change

Catastrophe loss free

% change

Catastrophe loss hit

% changeMarine 0% 0% to +5% +5% to +20% 0% N/A

Medical Excess – U.S. N/A 0% to +10% +10% to +25% N/A N/ANon-Marine Retrocession 0% to -5% 0% N/A +5% to +10% various

Personal Accident / Life Catastrophe N/A 0% to -5% +10% to +15% 0% to -5% N/A

Capital Markets• Investors continue to grow insurance assets under management • Catastrophe bond issuance accelerating, with projected full year issuance of US $5.5B to $6B, and projected outstanding

capacity at the end of 2012 US $15B to $15.5B• Rising risk spread trend for peak risks reversed course at end of quarter • Indemnity trigger structures become more common • Continued mergers and aqusition activity, however somewhat subdued due to Eurozone uncertainties

Workers’ Compensation• Catastrophe capacity remains strong with reinsurers attempting to hold the line on pricing • Reinsurers have been looking to raise retentions on programs attaching below $1M • Increased level of interest from cedants in purchasing per person coverages between $5M and $20M

Rates

Workers’ Compensation rates

TerritoryXL – No loss emergence

% changeXL – With loss emergence

% changeUnited States 0% to -5% N/A

Page 10

Global and local reinsurance Willis Re employs reinsurance experts worldwide. Drawing on this highly professional resource, and backed by all the expertise of the wider Willis Group, we offer you every solution you look for in a top tier reinsurance advisor, one that has comprehensive capabilities, with on-the-ground presence and local understanding.

Whether your operations are global, national or local, Willis Re can help you make better reinsurance decisions, access worldwide markets, negotiate optimum terms and boost your business performance.

How can we help?To find out how we can offer you an extra depth of service combined with extra flexibility, simply contact us.

Begin by visiting our website at www.willisre.comor calling your local office.

Media InquiriesClare KerriganCommunications and Marketing Director Willis ReThe Willis Building51 Lime StreetLondon EC3M 7DQTel: +44 (0) 20 3124 [email protected]

Willis LimitedThe Willis Building51 Lime StreetLondon EC3M 7DQTel: +44 (0) 20 3124 6000Fax: +44 (0) 20 3124 8223

Willis Re Inc.One World Financial Center200 Liberty Street3rd FloorNew York, NY 10281Tel: +1 (212) 915 7600