1.general course questions & final group project, due thursday 2.review quiz #4 chapter 18 &...

TRANSCRIPT

1. General Course Questions & Final Group Project, due Thursday

2. Review Quiz #4 Chapter 18 & 8:

A. Chapter 18 - Long-term Construction Contracts(Questions 7, 9, 10, 11 , & 12 BE 2, 3, 4, Ex 5, Prob 1, 3 & 6 add’l practice ex 7 & Pr 4)

B. Chapter 8 - Inventory Pricing Methods (?12,13,16 BE 5,6,7, P 6)

3. Finish Chapter 9: Inventory – Additional Valuation Issues

A. Lower of Cost or Market (LCM) (Brief ex 2, ?2,3,7, Ex 5 Prob 1 & 3)

B. Relative Sales Value (Question 8, Brief Ex 4 & 7)

C. Estimating Inventory – using Gross profit (?11, Brief Ex 7 Prob 4)

Retail Inventory Method (?14, BE 8)

D. Purchase Commitments & Disclosures (Brief Ex 5 & 6, ?17, Ex 10)

• Follow-up Questions to prep Final: Ch 7, 18 and 8 (Cash, Receivables, Revenue Recognition and Dollar Value LIFO, in addition to last quiz)

• Self, Peer and Course Evaluations

Intermediate AccountingIntermediate AccountingDecember 1December 1stst, 2010, 2010

Intermediate AccountingIntermediate AccountingDecember 1December 1stst, 2010, 2010

GAAP requires inventory to be stated at the lower of cost or market, abandoning the historical cost principle when the future utility (revenue producing ability) of the asset drops below it original cost.

Market = Replacement Cost (the cost to replace by purchase or reproduction, not sales price)

Thus, LCM is Lower of Cost or Replacement Cost and determined using “Designated Market”

Loss should be recorded when loss occurs, not in the period of sale

Restate asset at “designated” market to replace cost.

Inventory: Lower of Cost or Inventory: Lower of Cost or Market (LCM)Market (LCM)

2

Why use Replacement Cost (RC) for Market?

Decline in the RC usually results in a decline in selling price.

RC allows a consistent rate of gross profit.

A reduction in RC may fail to indicate a reduction in utility, thus two additional valuation limitations are used to determine the Designated Market which is then compared to Cost to determine if a LCM write-down is needed.

The Designated Market is the middle of the three: Replacement Cost (cost to replace or reproduce) Ceiling - net realizable value (NRV= selling price less disposal cost) and

Floor - net realizable value less a normal profit margin.

Determining Designated Determining Designated Market for use in Market for use in

assessing LCMassessing LCM

3

Item Historical Replacement Ceiling Floor Final Cost Cost (NRV) (NRV – profit) Inventory $

A $80,000 $88,000 $120,000 $104,000 $

B $90,000 $88,000 $100,000 $70,000 $

C $90,000 $88,000 $100,000 $90,000 $

D $90,000 $88,000 $87,000 $70,000 $

Finding the Designated Finding the Designated Market to Determine Lower Market to Determine Lower

of Cost or Marketof Cost or Market

4

NotNot

<<

CostCost MarketMarket

Ceiling = NRVCeiling = NRV

Replacement CostReplacement Cost

Floor =

NRV less Normal

Profit Margin

Floor =

NRV less Normal

Profit MarginGAAP

LCM

GAAP

LCM

NotNot

>>

Rational for Designated Rational for Designated Market Market

Ceiling and Floor LimitationsCeiling and Floor Limitations•Ceiling – prevents overstatement of the value of obsolete, damaged, or shopworn inventories.

•Floor – deters understatement of inventory and overstatement of the loss in the current period.

5

•Illustration 9-5Illustration 9-5

Lower of Cost or Market - Lower of Cost or Market - Individual ItemsIndividual Items

6

•Illustration 9-5Illustration 9-5

Lower of Cost or Market - Lower of Cost or Market - Individual ItemsIndividual Items

$415,000

7

Ending inventory (cost) $ 415,000

Ending inventory (LCM) 350,000

Adjustment to LCM $ 65,000

Allowance to reduce inventory to market (contra inventory account)

Loss on inventory 65,000

Inventory

65,000

Cost of goods sold 65,000

Allowance

Method

Allowance

Method

Direct

Method

Direct

Method

Recording Decline in Market Recording Decline in Market Value (LCM) Individual ItemsValue (LCM) Individual Items

65,000

8

Allowance Direct

Current assets:

Cash 100,000$ 100,000$

Accounts receivable 350,000 350,000

I nventory 770,000 705,000

Less: inventory allowance (65,000)

Prepaids 20,000 20,000

Total current assets 1,175,000 1,175,000

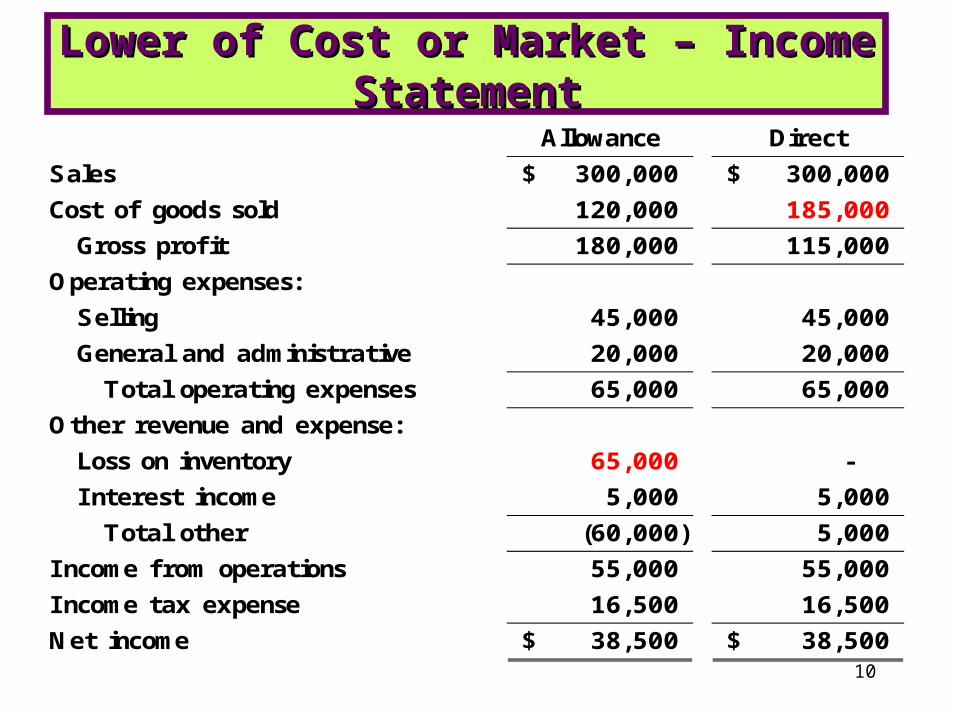

Lower of Cost or Market – Lower of Cost or Market – Balance SheetBalance Sheet

9

Allowance Direct

Sales 300,000$ 300,000$

Cost of goods sold 120,000 185,000

Gross profit 180,000 115,000

Operating expenses:

Selling 45,000 45,000

General and administrative 20,000 20,000

Total operating expenses 65,000 65,000

Other revenue and expense:

Loss on inventory 65,000 -

I nterest income 5,000 5,000

Total other (60,000) 5,000

I ncome from operations 55,000 55,000

I ncome tax expense 16,500 16,500

Net income 38,500$ 38,500$

Lower of Cost or Market – Income Lower of Cost or Market – Income StatementStatement

10

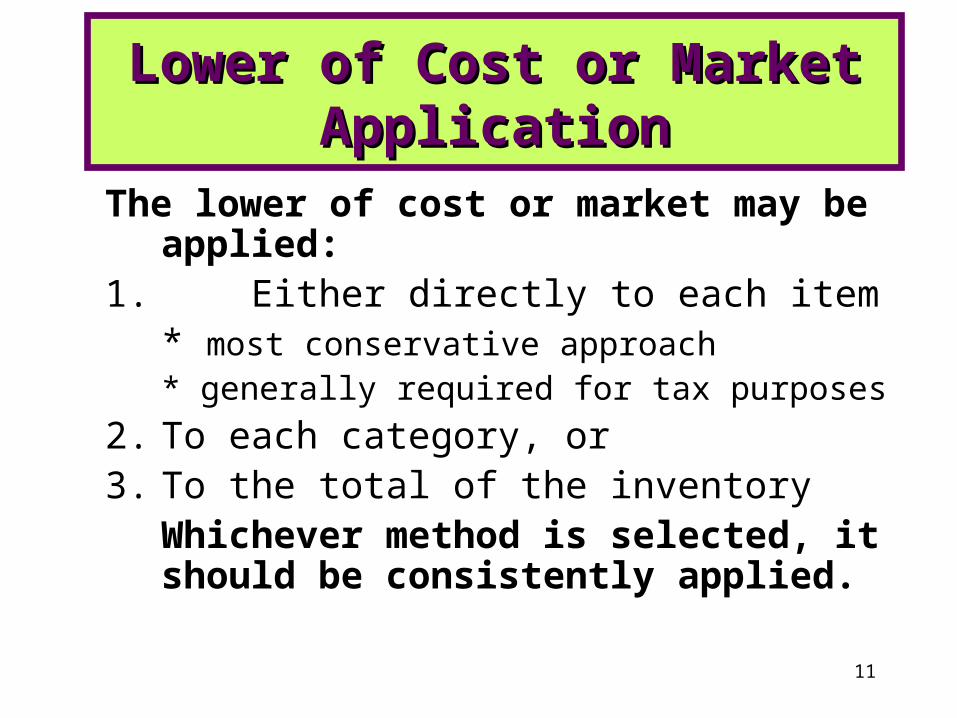

The lower of cost or market may be applied:1. Either directly to each item

* most conservative approach* generally required for tax

purposes

2. To each category, or3. To the total of the inventory

Whichever method is selected, it should be consistently applied.

Lower of Cost or Market Lower of Cost or Market ApplicationApplication

11

Lower of Cost or Market - Lower of Cost or Market - Individual Items, Major Categories Individual Items, Major Categories

or Total Inventoryor Total Inventory

12

Lower of Cost or Market - Lower of Cost or Market - Individual Items, Major Categories Individual Items, Major Categories

or Total Inventoryor Total Inventory

13

LCM ExampleLCM Example

Assume in each case that the selling expenses are $8 per unit and that the normal profit is $5 per unit. Calculate the limits for each case (ceiling and floor). Then enter the amount that should be used for the lower of cost or market.

Designated Market -chose the middle one

Selling Price

Ceiling (NRV)

Replace-ment $

Floor (NRV less profit)

Cost Lower of

cost/mkt

a $ 54 $ 38 43

b $ 47 $ 36 40

c $ 56 $ 39 40

d $ 47 $ 42 40

1. Compute the Designated Market Ceiling for each item which is its Net Realizable Value (NRV)

(NRV = Selling price less costs to complete sale).

2. Compute the Designated Market Floor for each item which is its NRV less any normal profit.

3. Identify each item's Designated Market, which is the middle dollar amount, by circling it.

4. Compare cost to designated market and use Lower of Cost or Designated market.

Also Homework today: Brief Ex 214

Expense are recorded when the loss in utility occurs. Profit on sale only recognized at the point of sale.

Inventory may be valued at cost in one year and at market the next year.

Net income in the year of loss is lower. Net income in subsequent period may be higher than normal if expected reductions in sales price do not materialize.

LCM uses a “normal profit” in determining inventory values, which is a subjective measure.

Some Deficiencies:

Evaluation of LCM Rule

15

Recording the Decline in Recording the Decline in Market ValueMarket Value

For subsequent increases in inventory value:

o US GAAP prohibits the reversal of writedowns

o IFRS requires the reversal of writedowns

What if the Market Value What if the Market Value Recovers?Recovers?

16

• Valuation at Net Realizable Value Permitted by GAAP under the following conditions:

(1) there is a controlled market with a quoted price for all quantities, and

(2) there are no significant costs of disposal (rare metals and agricultural products) or

(3) it is too difficult to obtain cost figures (meatpacking)

• Relative Sales Value – “Basket Purchase”

• Purchase Commitments

Other Valuation IssuesOther Valuation Issues

17

• Appropriate basis when basket purchases are made.

• Basket purchases involve a group of varying units.

• The purchase price is paid as a lump sum amount.

• The lump sum price is allocated to units on the basis

of their relative sales values.• Quickest approach – determine the percentage total cost to total

revenue and use it to allocate cost or gross profit

Valuation Basis: Valuation Basis: Relative Sales ValuesRelative Sales Values

Also Homework today: question 8 and Brief Ex 418

Kirby Company buys three different lots (A, B and C) in a basket purchase, paying $297,500 for all three.The lots were sold as follows:

Sales Price Cost Gross ProfitA $75,000 _______ _________

B $150,000 _______ _________C $200,000 _______ _________

Total $425,000 _______ _________What is the cost of A, B and C and the gross profit for each lot?(Suggestion: determine the percentage total cost to total revenue and use it

to allocate cost and/or gross profit)

Relative Sales Values: Relative Sales Values: ExampleExample

19

Kirby Company buys three different lots (A, B and C) in a basket purchase, paying $297,500 for all three.The lots were sold as follows:

% Cost to Sales = $297.5k/$425K = 70%Sales Price Cost Gross Profit

A $75,000 x 70% $ 52,500 $22,500 B $150,000 x 70% $105,000 $45,000

C $200,000 x 70% $140,000 $60,000Total $425,000 $ 297,500 $127,500

What is the cost of A, B and C and the gross profit for each lot?

Relative Sales Values: Relative Sales Values: ExampleExample

20

Relative Sales Values: Relative Sales Values: Example 2Example 2

Crawford Furniture Company purchased a carload of wicker chairs. The manufacturer sold the chairs to Crawford for a lump sum of $60,000, because they want to discontinue these items. The three types of chairs and their estimated selling prices are listed below. Given the 2011 sales below, determine how much gross profit Crawford should recognize in 2011 and what amount they should report as unsold chair inventory.

EstimatedUnit

Sales in 2011

2011 Gross Profit

Realized

Inventory December 31, 2011# of Chairs

Unit Sales Price

Total Selling Price

Lounge Chairs 400 90 $ 36,000 200

Arm Chairs 300 80 $ 24,000 100

Straight Chairs 800 50 $ 40,000 120

220 $ 100,000

(Suggestion: determine the percentage total cost to total revenue and use it to allocate cost and gross profit) 21

Relative Sales Values: Relative Sales Values: Example 2Example 2

Crawford Furniture Company purchased a carload of wicker chairs. The manufacturer sold the chairs to Crawford for a lump sum of $60,000, because they want to discontinue these items. The three types of chairs and their estimated selling prices are listed below. Given the 2011 sales below, determine how much gross profit Crawford should recognize in 2011 and what amount they should report as unsold chair inventory.

EstimatedUnit

Sales in 2011

2011 Gross Profit

Realized

Inventory December 31, 2011# of Chairs

Unit Sales Price

Total Selling Price

Lounge Chairs 400 90 $ 36,000 60% 200 $ 7,200 $ 10,800

Arm Chairs 300 80 $ 24,000 60% 100 $ 3,200 $ 9,600

Straight Chairs 800 50 $ 40,000 60% 120 $ 2,400 $ 20,400

220 $ 100,000 $ 12,800 $ 40,800

22

• Cancellable contracts– No entry or disclosure required

• Formal, non-cancelable contracts – Seller retains title, buyer recognizes no asset but should

disclose contract details in footnote – If execution of the contract is expected to result in a loss,

buyer must record the loss in the period the market prices decreased:

DR Unrealized Holding Loss

CR Est liability on purchase commitment

Purchase CommitmentsPurchase Commitments

Homework today: Brief Ex 5 & 623

• Inventory estimation used when:– a fire or other catastrophe destroys either

inventory or inventory records– taking a physical inventory is impractical– auditors only need an estimate of the

company’s inventory

• Gross Profit Method

• Retail Sales Method

Inventory Estimation Inventory Estimation TechniquesTechniques

24

25

Estimate Inventory Using Estimate Inventory Using Gross ProfitGross Profit

1. Calculate Cost of Goods Available for Sale (CGA)

2. Estimate Cost of Goods Sold (CGS) using Sales and estimate of Gross Profit

3. Deduct Estimate of CGS from CGA to get Estimate of Ending Inventory

26

Estimate Inventory Using Estimate Inventory Using Gross ProfitGross Profit

1. Calculate Cost of Goods Available for Sale (CGA)

2. Estimate Cost of Goods Sold (CGS) using Sales and estimate of Gross Profit

3. Deduct Estimate of CGS from CGA to get Estimate of Ending Inventory

Whitsunday Company’s warehouse burned and its inventory was completely destroyed. The accounting records were kept in the office building and escaped harm. The following information was available: Net sales $426,000 Beginning inventory 80,000 Net purchases 300,000Average gross profit on sales 20%

Use the above information to estimate the ending inventory lost in the fire using the gross profit method.

27

Estimate Inventory Using Estimate Inventory Using Gross ProfitGross Profit

1. Calculate Cost of Goods Available for Sale (CGA) $380,000

2. Estimate Cost of Goods Sold (CGS) using Sales and estimate of Gross Profit: (CGS 80% if Gross Profit is 20%)

Sales x CGS % = CGS: $426,000 x 80% = $340,800

3. Deduct Estimate of CGS from CGA to get Estimate of Ending Inventory $380,000 – 340,800 = $39,200

Whitsunday Company’s warehouse burned and its inventory was completely destroyed. The accounting records were kept in the office building and escaped harm. The following information was available: Net sales $426,000 Beginning inventory 80,000 Net purchases 300,000Average gross profit on sales 20%

Use the above information to estimate the ending inventory lost in the fire using the gross profit method.

Beginning inventory $80,000

Net purchases 300,000

Cost of goods available for sale 380,000

Estimated cost of goods sold:

Net sales 426,000

Less: Est gross profit (85,200)(340,800)

Estimated ending inventory $39,200

Gross Profit Method to Gross Profit Method to Determine EIDetermine EI

28

29

Example 2: Estimate Example 2: Estimate InventoryInventory

Using Gross Profit Using Gross Profit

1.

2.

3.

On December 31, 2010 Carr Company's inventory burned. Sales and purchases for the year had been $1,400,000 and $980,000, respectively. The beginning inventory (Jan. 1, 2010) was $170,000; in the past Carr's gross profit has averaged 40% of selling price. Compute the estimated cost of inventory burned.

30

Example 2: Estimate Example 2: Estimate InventoryInventory

Using Gross Profit Using Gross Profit

1. Calculate Cost of Goods Available for Sale (CGA) $1,150,000

2. Estimate Cost of Goods Sold (CGS) using Sales and estimate of Gross Profit: (CGS 60% if Gross Profit is 40%)

Sales x CGS % = CGS: $1,400,000 x 60% = $840,000

3. Deduct Estimate of CGS from CGA to get Estimate of Ending Inventory $1,150,000 – 840,000 = $310,000

On December 31, 2010 Carr Company's inventory burned. Sales and purchases for the year had been $1,400,000 and $980,000, respectively. The beginning inventory (Jan. 1, 2010) was $170,000; in the past Carr's gross profit has averaged 40% of selling price. Compute the estimated cost of inventory burned.

On December 31, 2010 Carr Company's inventory burned. Sales and purchases for the year had been $1,400,000 and $980,000, respectively. The beginning inventory (Jan. 1, 2010) was $170,000; in the past Carr's gross profit has averaged 40% of selling price. Compute the estimated cost of inventory burned.

BI+ Net Purchases= COGA -Estimated COGS: Net Sales less estimated gross profitEstimated Ending inventory

Gross Profit Method Gross Profit Method Example 2Example 2

31

This inventory estimation technique is used when:– a fire or other catastrophe destroys either inventory or inventory records

– taking a physical inventory is impractical– auditors only need an estimate of the company’s inventory

Appropriate for retail concerns with:• high volume sales and• different types of merchandise

• Assumes an observable pattern between cost and prices.

Retail Inventory MethodRetail Inventory Method

32

Steps:1. Determine ending inventory at retail price

2. Convert this amount to a cost basis using a cost-to-retail ratio

BI (at retail) + Net Purchases (at retail) – Net sales = EI (at retail)

EI (at retail) X Cost-to-Retail ratio = estimated “EI” (at cost)

Retail Inventory MethodRetail Inventory Method

33

Given for the year 2002: at cost at retail Beginning inventory $2,000 $3,000 Purchases (Net) $10,000 $15,000 Sales (Net) $12,000What is ending inventory, at retail and at cost?

Retail Inventory Method: Retail Inventory Method: ExampleExample

34

at cost at retail

Beginning inventory $ 2,000 $ 3,000 Purchases (Net) $10,000 $15,000 Goods available for sale $12,000 $18,000 less: Sales (Net) ($12,000) Ending inventory (at retail) $6,000 Times: cost to retail ratio x

Ending inventory at costCOGS

Retail Inventory Method: Retail Inventory Method: ExampleExample

35

1. General Course Questions & Final Group Project, due Thursday

2. Questions before final 30 minute Quiz:

A. Chapter 18 - Long-term Construction Contracts(Questions 7, 9, 10, 11 , & 12 BE 2, 3, 4, Ex 5, Prob 1, 3 & 6 add’l practice ex 7 & Pr 4)

B. Chapter 8 - Inventory Pricing Methods (?12,13,16 BE 5,6,7, P 6)

4. Chapter 8 Dollar Value LIFO (homework: ?14, 17-20, BE 9, Ex 26, Prob 11 &

Case 9)

5. Chapter 9: Inventory – Additional Valuation Issues

A. Lower of Cost or Market (LCM) (Brief ex 2)

B. Relative Sales Value (Question 8, Brief Ex 4)

C. Estimating Inventory – using Gross profit (question 11, Brief Ex 7)

D. Purchase Commitments (Brief Ex 5 & 6)

6. Extra Credit Session - Columbia Sportswear Annual Report Project

Intermediate AccountingIntermediate AccountingNovember 30November 30thth, 2010, 2010

Intermediate AccountingIntermediate AccountingNovember 30November 30thth, 2010, 2010

36