©1998-20031 foreign currency options ii. ©1998-2003 1. using options for hedging

TRANSCRIPT

©1998-2003 1

Foreign Currency Options II

©1998-2003

1. Using Options for Hedging

©1998-2003

The set up (Using calls)

• A U.S. importer must pay CHF250,000

• The payment will occur in late September

• The importer is concerned that CHF may appreciate against the dollar so that its dollar-denominated payment may increase.

©1998-2003

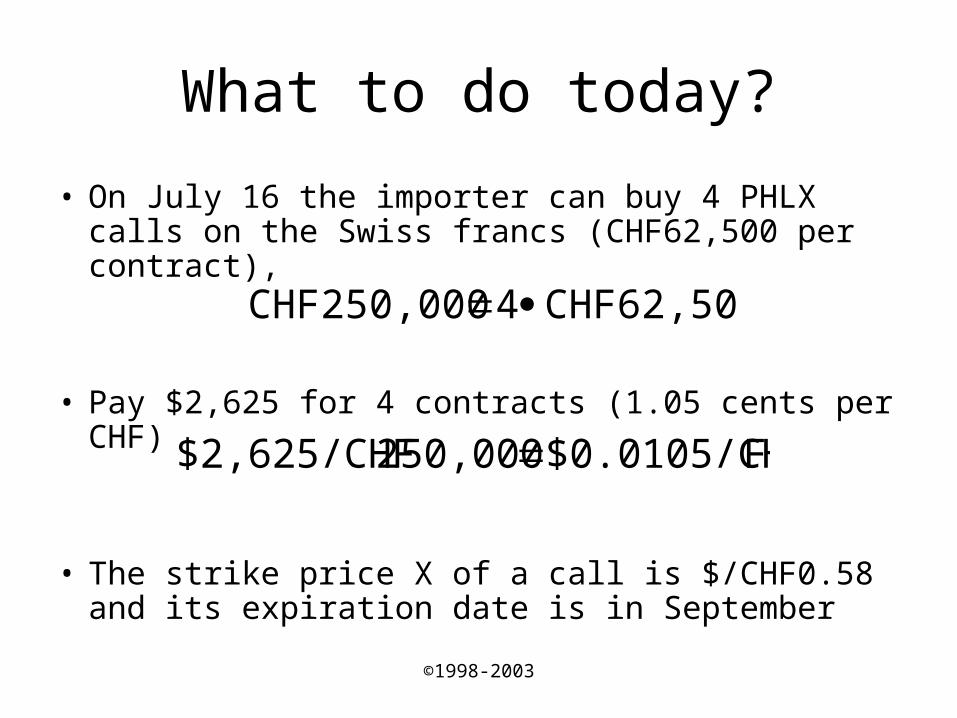

What to do today?

• On July 16 the importer can buy 4 PHLX calls on the Swiss francs (CHF62,500 per contract),

• Pay $2,625 for 4 contracts (1.05 cents per CHF)

• The strike price X of a call is $/CHF0.58 and its expiration date is in September

CHF62,5004CHF250,000

F$0.0105/CH250,000$2,625/CHF

©1998-2003

Expiration: scenario 1

• The spot price of CHF at expiration is $0.5790• Since S < X, Max{(S - X), 0} = 0, the intrinsic

(and total) value is 0• The option will not be exercised, i.e. it expires

worthless• The importer incurs a total loss (or more

precisely a hedging cost) of $2,625 which was paid initially for 4 call options

• The profit for the underwriter (the counterparty of the option contract) is $2,625

©1998-2003

Expiration: scenario 2

• The spot price of CHF at expiration is $0.5820• Since S > X, Max{(S - X), 0} = $0.0020, the

intrinsic value is 0.20 cents per Swiss franc• The U.S. importer exercises the option and gets

• The importer incurs a total net loss (hedging cost) of $2,125:

• The underwriter’s profit is $2,125

CHF250,000$0.0020CHF$500

$500$2,620$2,125

©1998-2003

Expiration: scenario 3

• The spot price of CHF at expiration is $0.5920• Since S > X, Max{(S - X), 0} = $0.0120, the

intrinsic value is 1.20 cents per Swiss franc• The U.S. importer exercises the option and gets

• The importer has a total net gain of $375:

• The underwriter’s loss is $375

CHF250,000F0.0120$/CH$3,000

$2,625$3,000$375

©1998-2003

Call option on a diagram

$/CHF spot rate

0.58

Option profitcents/CHF

Long call

Short call

Strike price

Profit

Loss

Limited loss

Limited Profit0

“At the money”

©1998-2003

The Set up (Using puts)

• An American exporter will receive CHF250,000

• The receipt will occur in late September

• The exporter is concerned that CHF may depreciate against the dollar so that its dollar-denominated cash inflow may be reduced.

©1998-2003

What to do today?

• On July 16 the exporter can buy 4 PHLX puts on the Swiss Frank (CHF62,500 per contract),

• Pay $2,225 for 4 contracts (0.89 cents per CHF)

• The strike price of a put is $0.58 and its expiration date is in September

62,5004CHF250,000

$0.0089250,000$2,225/CHF

©1998-2003

Expiration: scenario 1

• The spot price of CHF at expiration is $0.5810• Since S > X, Max{(X - S), 0} = 0, the intrinsic

(and total) value is 0• The option will not be exercised

• The exporter incurs a total loss of $2,225 which was paid initially for 4 put options

• The underwriter’s profit is $2,225

©1998-2003

Expiration: scenario 2

• The spot price of CHF at expiration is $0.5780• Since S < X, Max{(X - S), 0} = $0.0020, the

intrinsic value is 0.20 cents per Swiss franc.• The U.S. exporter exercises the option and gets

• The exporter incurs a total net loss of $1,725:

• The underwriter’s profit is $1,725

CHF250,000F0.0020$/CH$500

$500$2,225$1,725

©1998-2003

Expiration: scenario 3

• The spot price of CHF at expiration is $0.5680• Since S < X, Max{(S - X), 0} = $0.0120, the

intrinsic value is 1.20 cents per Swiss franc• The U.S. exporter exercises the option and gets

• The exporter has a total net gain of $775:

• The underwriter’s loss is $775

CHF250,000F0.0120$/CH$3,000

$2,225$3,000$775

©1998-2003

Put option on a diagram

$/CHF spot rate

0.58

Option profitcents/CHF

Long put

Short put

Strike price

Limited loss

Limited Profit

Profit

Loss

“At the money”

©1998-2003

Alternative strategies: Forwards and futures

• Forwards and futures offer a protection against exchange rate risk exposure at the lowest cost.

• Options offer a protection at a premium.

• Forwards and futures eliminate any upside (positive) impact of the exchange rate risk.

• Options do not eliminate the upside (positive) impact of the exchange rate risk.

©1998-2003

The set up(Using options or futures)

• On July 1, an American company makes a sale for which is will receive CHF125,000 on September 1.

• The spot price of CHF is $0.6922.• The firm wants to protect itself against a

declining Swiss franc by selling its expected CHF receipts forward (using a futures contract) or by buying (long) a CHF put option.

©1998-2003

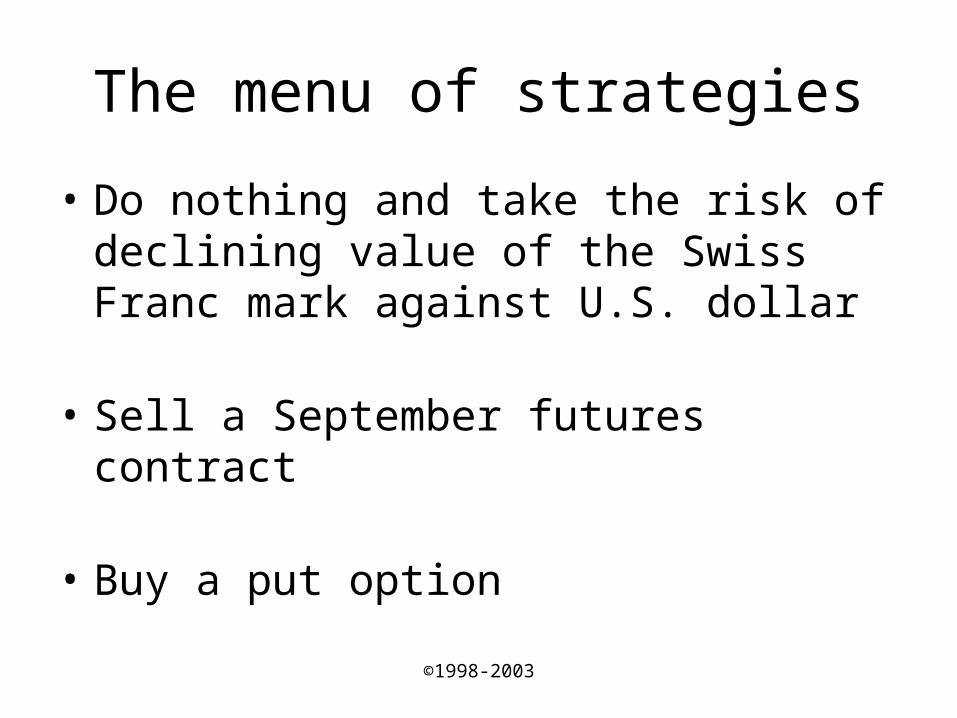

The menu of strategies

• Do nothing and take the risk of declining value of the Swiss Franc mark against U.S. dollar

• Sell a September futures contract

• Buy a put option

©1998-2003

Scenario 1: depreciating CHF

July 1 September 1

Spot $0.6922 $0.6542

September futures $0.6956 $0.6558

September 68 long put $0.0059 $0.0250

September 70 long put $0.0144 $0.0447

©1998-2003

Scenario 1: Strategies 1 & 2

• With do nothing strategy, the company will incur a loss of $4,750

• With selling short a futures contract, the company will– loose $4,750 in the spot market– gain $4,975 in the futures market

– net profit $225

CHF125,000HF0.6542)$/C(0.6922$4,750

CHF125,000HF0.6558)$/C(0.6956$4,975

©1998-2003

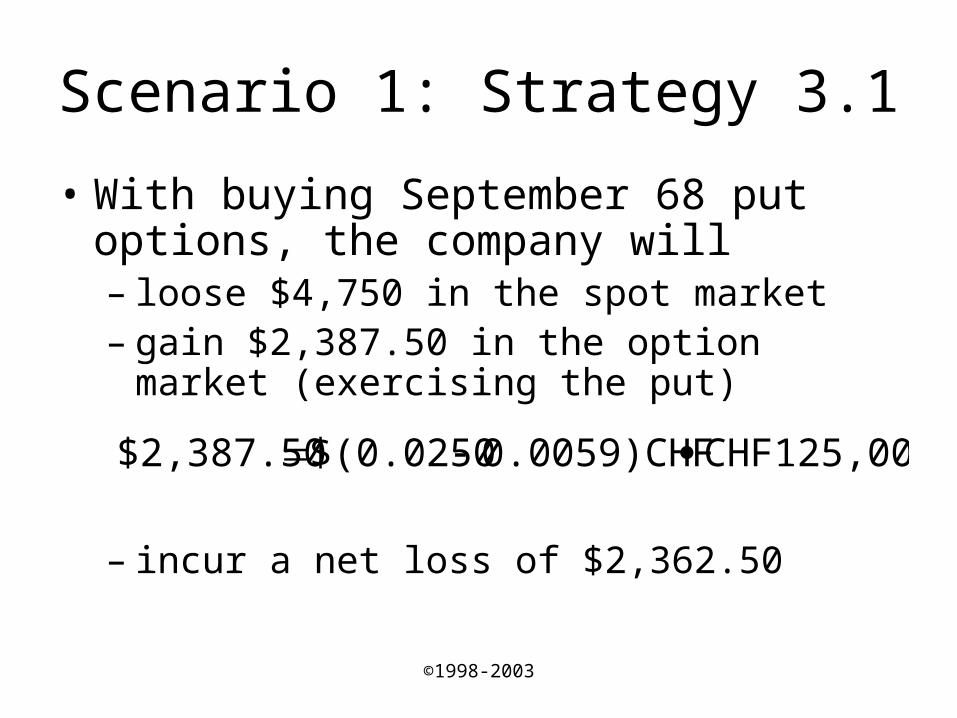

Scenario 1: Strategy 3.1

• With buying September 68 put options, the company will – loose $4,750 in the spot market – gain $2,387.50 in the option market

(exercising the put)

– incur a net loss of $2,362.50

CHF125,0000.0059)CHF$(0.0250$2,387.50

©1998-2003

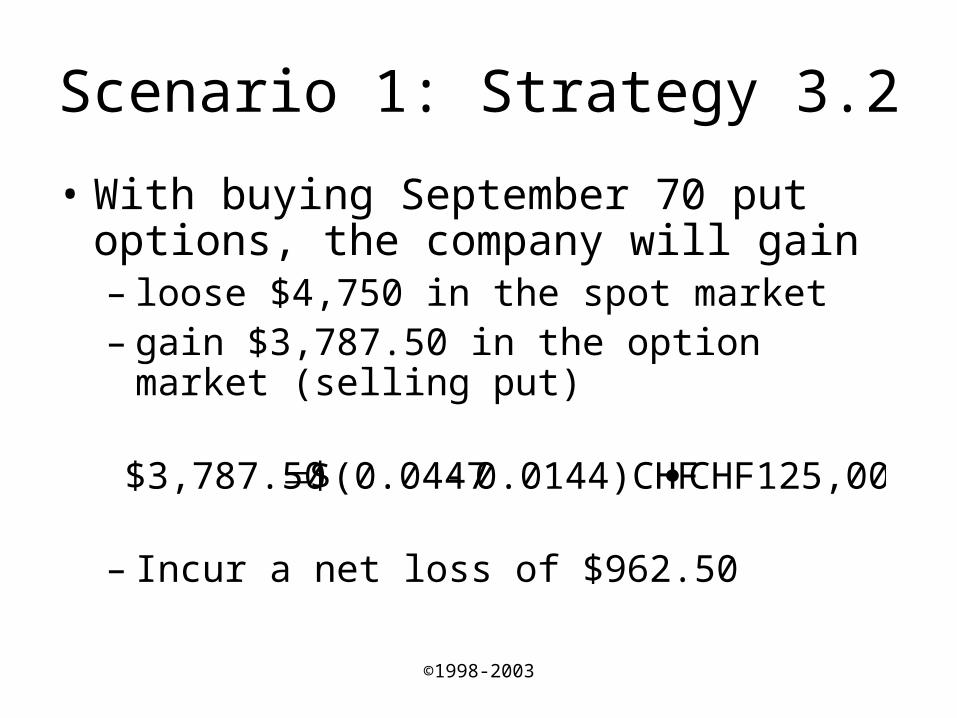

Scenario 1: Strategy 3.2

• With buying September 70 put options, the company will gain– loose $4,750 in the spot market – gain $3,787.50 in the option market (selling

put)

– Incur a net loss of $962.50

CHF125,0000.0144)CHF$(0.0447$3,787.50

©1998-2003

Scenario 2: appreciating CHF

July 1 September 1

Spot $0.6922 $0.7338

September futures $0.6956 $0.7374

September 68 put $0.0059 $0.0001

September 70 put $0.0144 $0.0001

©1998-2003

Scenario 2: Strategies 1 & 2

• With do nothing strategy, the company will have a gain of $5,200

• With selling short a futures contract, the company will– gain $5,200 in the spot market– loose $5,225 in the futures market

– net loss $25

CHF125,000HF0.6922)$/C(0.7338$5200

CHF125,000HF0.6956)$/C(0.7374$5,225

©1998-2003

Scenario 2: Strategy 3.1

• With buying September 68 put options, the company will– gain $5,200 in the spot market – loose $725 in the option market (selling put)

– net gain $4,475

CHF125,0000.0001)CHF$(0.0059$725

©1998-2003

Scenario 2: Strategy 3.2

• With buying September 70 put options, the company will – gain $5,200 in the spot market – loose $1,787.50 in the option market (selling

put)

– net gain of $3412.50

CHF125,0000.0001)CHF$(0.0144$1,787.50

©1998-2003

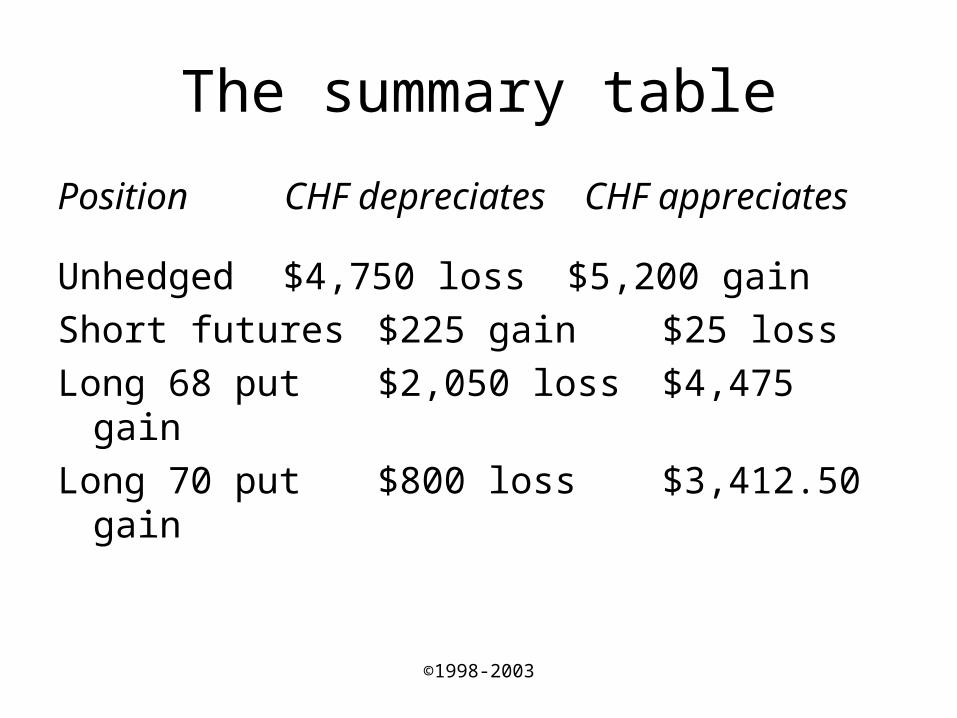

The summary table

Position CHF depreciates CHF appreciates

Unhedged $4,750 loss $5,200 gain

Short futures $225 gain $25 loss

Long 68 put $2,050 loss $4,475 gain

Long 70 put $800 loss $3,412.50 gain

©1998-2003

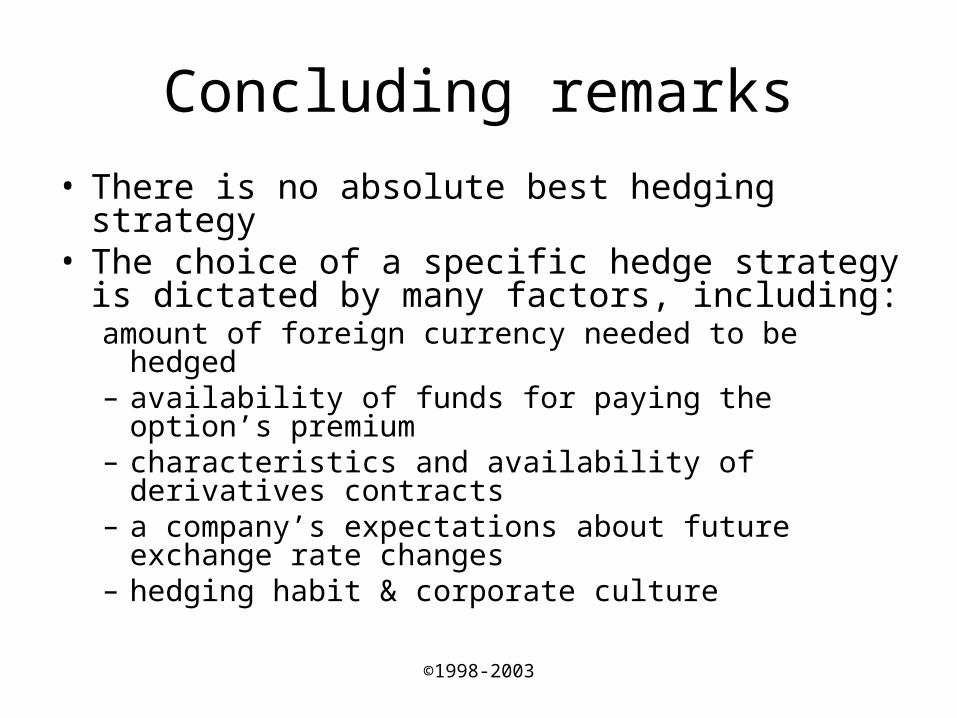

Concluding remarks

• There is no absolute best hedging strategy• The choice of a specific hedge strategy is

dictated by many factors, including:amount of foreign currency needed to be hedged– availability of funds for paying the option’s premium– characteristics and availability of derivatives contracts– a company’s expectations about future exchange rate

changes– hedging habit & corporate culture