17th annual meeting of the association of japanese business studies paper session 2: case studies...

Post on 19-Dec-2015

215 views

TRANSCRIPT

17th Annual Meeting of The Association of Japanese Business Studies

Paper Session 2: Case Studies

JAPANESE ‘MINI BANKS’Retail Banking Services through Convenience Stores

byWilliam V. Rapp

The New Jersey Insititute of Technology, USA&

Mazhar ul IslamThe International University, Bruchsal, Germany

©William Rapp & Mazhar Islam 20042

Outline

Introduction

Post War Japanese Financial System

Japanese Convenience Stores (CVS)

Information Technology in CVS

Evolution of CVS Mini-banks

Conclusions

©William Rapp & Mazhar Islam 20043

Introduction Mini-banks - retail banking services

provided by convenience stores (CVS) in Japan

Typical Retail Banking and Financial Services

Loan repayment Utility bill collection Online purchase payments (e & m Commerce) Fund transfers (other payments, e.g. insurance) Credit cards (including credit lines) ATM and Multimedia Kiosks Brokerage and Insurance

©William Rapp & Mazhar Islam 20044

Introduction Main Drivers

Financial Sector Reforms Strategic Application of IT by the leading

CVS 24x7 opening hour of CVS Increase in store traffic Economies of Scope Strategic Alliances (Banks, Financial

Services)

©William Rapp & Mazhar Islam 20045

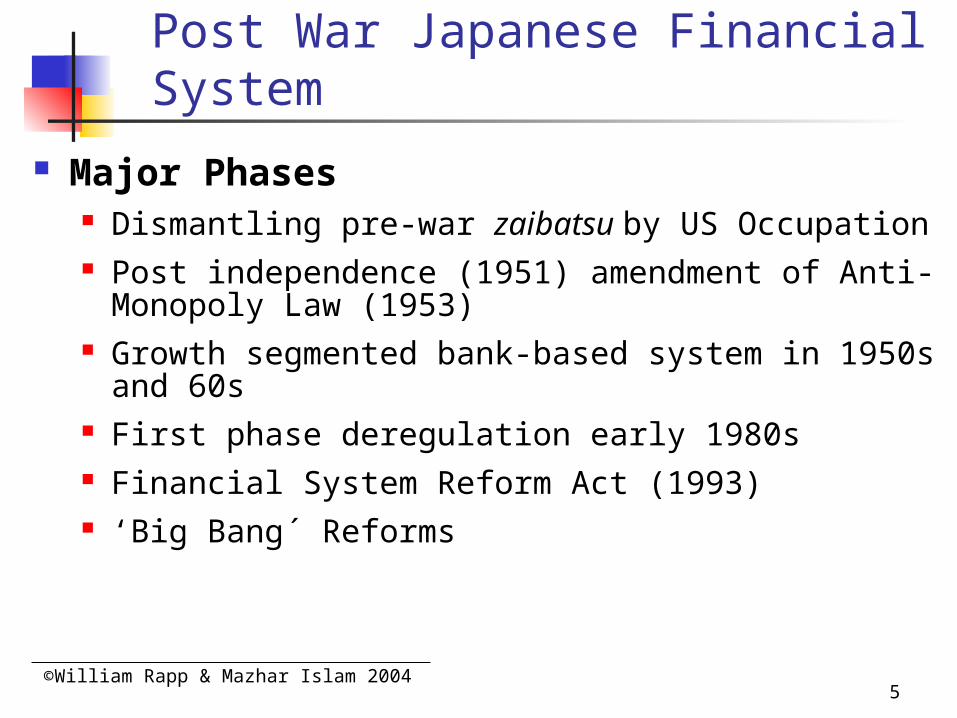

Post War Japanese Financial System

Major Phases

Dismantling pre-war zaibatsu by US Occupation Post independence (1951) amendment of Anti-

Monopoly Law (1953) Growth segmented bank-based system in 1950s

and 60s First phase deregulation early 1980s Financial System Reform Act (1993) ‘Big Bang´ Reforms

©William Rapp & Mazhar Islam 20046

Post War Japanese Financial System

Legacy 1950s to 1970s Bank-based funding system (indirect

finance) Underdeveloped stock and bond markets Structure of banking very stable – no new

entry, virtually no bank failures/mergers Banks segmented by function and size of

customers Consumer banking limited No credit cards

©William Rapp & Mazhar Islam 20047

Post War Japanese Financial System

First Phase Deregulation After first Oil Crisis in early 1970s due to

competitive pressures and bankruptcies 1980 amendment to Financial Exchange

and Foreign Trade Control Law 1984 – US- Japan Yen-Dollar Accord Slow growth decrease loan demand Increased interest real estate and retail

loans “Bubble”

©William Rapp & Mazhar Islam 20048

Post War Japanese Financial System

1980s Japanese economy expanded globally

(FDI) - expansion lending lead “bubble economy”

Excellent nominal performance by Financial Institutions (e.g. Nomura)

Ministry of Finance (MOF) did not initiate key structural reforms while BoJ provided liquidity (effects Yen appreciation)

©William Rapp & Mazhar Islam 20049

The Financial System Reform Act (1993)

Deregulated financial system allowed financial firms to offer multiple services

Phased Formation Of Universal Banking

Intensified competition Among Leading Firms (Banks, Securities, Insurance)

Post War Japanese Financial System

©William Rapp & Mazhar Islam 200410

“Big Bang” Reform November 1996 Prime Minister

Hashimoto announced the “Big Bang” financial sector reform

Main goal: progressive financial sector reform to bring Japan’s financial markets to par with those of New York and London by 2001

To make a “free, fair and global” market

Post War Japanese Financial System

©William Rapp & Mazhar Islam 200411

Consequences of the “Big Bang”

Consolidation in the Domestic Markets (many forced but some were voluntary)

Entry Foreign and Non-financial Firms (e.g. Ripplewood, Sony, Ito-Yokado)

New Types of Banks and Financial Services

Post War Japanese Financial System

©William Rapp & Mazhar Islam 200412

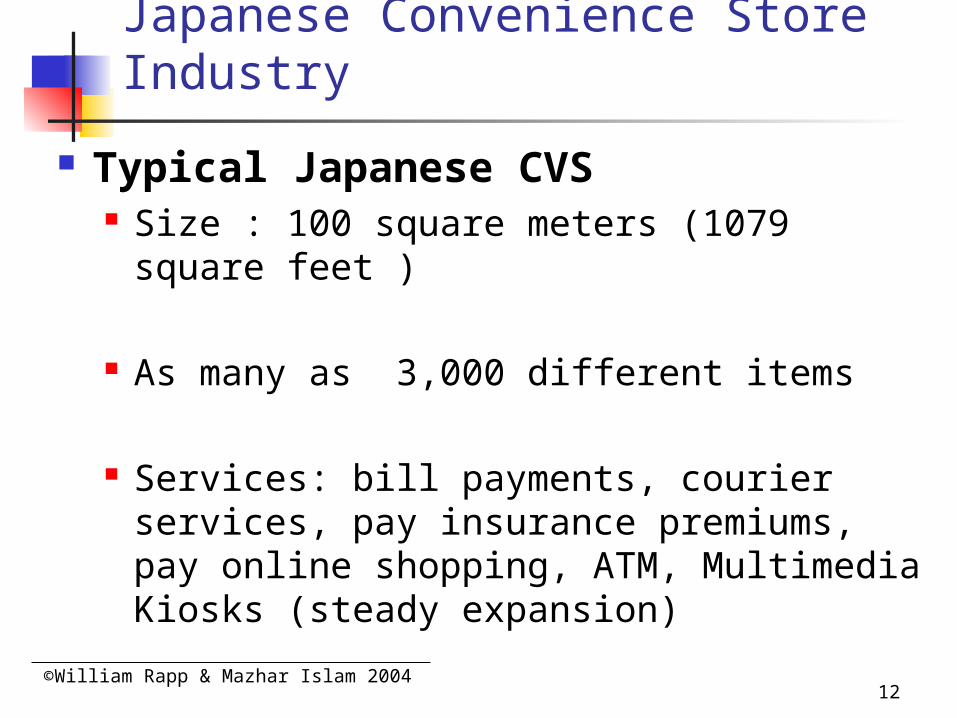

Japanese Convenience Store Industry

Typical Japanese CVS Size : 100 square meters (1079 square

feet )

As many as 3,000 different items

Services: bill payments, courier services, pay insurance premiums, pay online shopping, ATM, Multimedia Kiosks (steady expansion)

©William Rapp & Mazhar Islam 200413

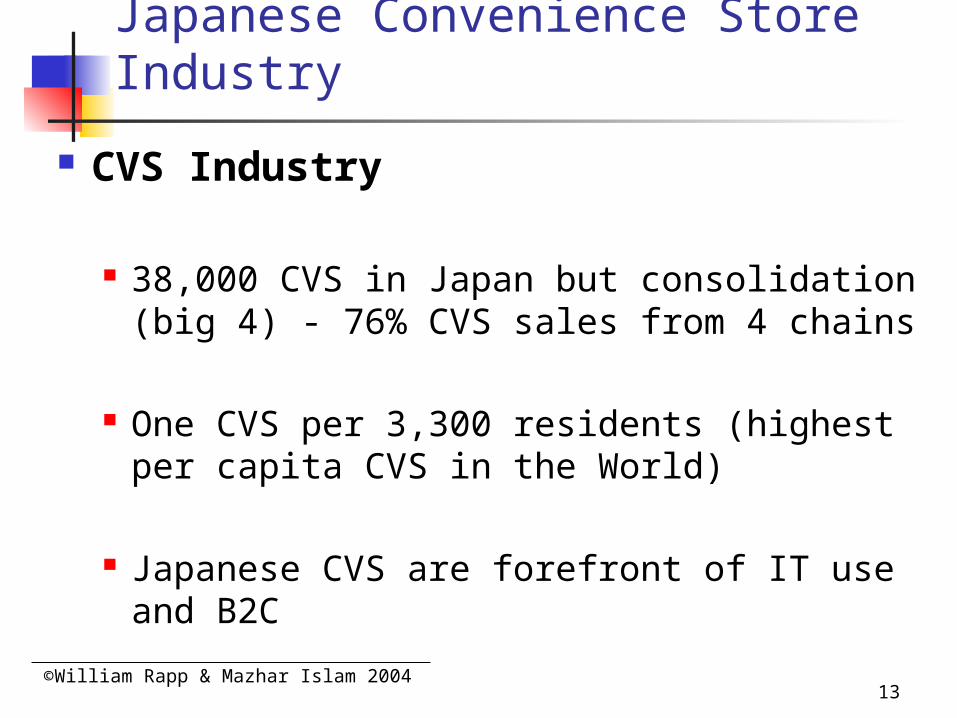

CVS Industry

38,000 CVS in Japan but consolidation (big 4) - 76% CVS sales from 4 chains

One CVS per 3,300 residents (highest per capita CVS in the World)

Japanese CVS are forefront of IT use and B2C

Japanese Convenience Store Industry

©William Rapp & Mazhar Islam 200414

Leading Japanese CVS Seven Eleven Japan

Industry leader in terms of # stores and sales Concentrates in greater Tokyo Per store and per square meter sales at least

50% higher that any major competitors Lawson (Mitsubishi Lead)

Second in terms of # stores and sales Operates in every ken (province); Leader in implementing multimedia kiosks

(Loppi)

Japanese Convenience Store Industry

©William Rapp & Mazhar Islam 200415

Leading Japanese CVS FamilyMart (C. Itoh Lead)

3rd largest chain; Toyota connection Primarily in greater Tokyo and Nagoya Caters exclusive high end products

C&S Formed in 2001 by the merger of CIRCLE K

and SUNKUS & ASSOCIATES Became a key player in the industry Undertaking key structural reforms

Japanese Convenience Store Industry

©William Rapp & Mazhar Islam 200416

Information Technology in CVS

Seven Eleven Japan(SEJ) is industry leader

Ishiwaka and Nejo (1998) report that information system of SEJ is the world’s largest network in retail industry

Other leading CVS in Japan are typically followers in IT implementation and new services

©William Rapp & Mazhar Islam 200417

SEJ’s First Generation Integrated Information System (IIS) In 1978 linked all stores - Electronic Ordering System

allowed store managers to place orders directly to HQ Government regulations did not allow different

businesses to connect at that time In 1982 SEJ introduced 2d generation Point of Sales

based System (POS) using Bar Codes – first CVS Started collecting sales related information which was

sent directly to HQ for analysis - “item-by-item control”

Linked suppliers with the system placing orders directly

Information Technology in CVS

©William Rapp & Mazhar Islam 200418

3d Generation of IIS Implemented in mid 80s Installed PCs with graphical display in stores Installed improved Point of Sales (POS)

terminals capable of collecting more information about customers

New POS could access the server at the HQ – 2-way communication

4th Generation of IIS implemented early 1990s - use high-speed integrated services digital network (ISDN) for data communications.

Information Technology in CVS

©William Rapp & Mazhar Islam 200419

Evolution of IIS ISDN was based on client-server technology 4th phase introduced Graphic Order Terminals and

Scanner Terminals Next (5th) Generation Implemented in 1999 -

Capable handling vast multimedia data at higher speeds, cutting data communication costs by 20%

Developed jointly with 12 companies (e.g. Nomura Research Institute (NRI), NEC and Microsoft; Uses satellite telecommunications and proprietary network

Invested 60 billion yen Solicit field rep and store manager inputs - Sensors

installed in stores collect information about customers

Information Technology CVS

©William Rapp & Mazhar Islam 200420

Source: Seven Eleven Japan

©William Rapp & Mazhar Islam 200421

Evolution of CVS Mini-Banks

Key Drivers Financial Sector Reforms Strategic Application of IT by leading CVS 24x7 open hours of CVS (convenience) Development payment services Customer have cash payment preference Increased store traffic Economies of Scope

©William Rapp & Mazhar Islam 200422

Three levels of mini-bank sophistication Level – I : Begin late 1980s with bill

collection Level – II: Start late 1990s after “Big

Bang” reform Level – III: Start beginning 2000/2001

Evolution of CVS Mini-Banks

©William Rapp & Mazhar Islam 200423

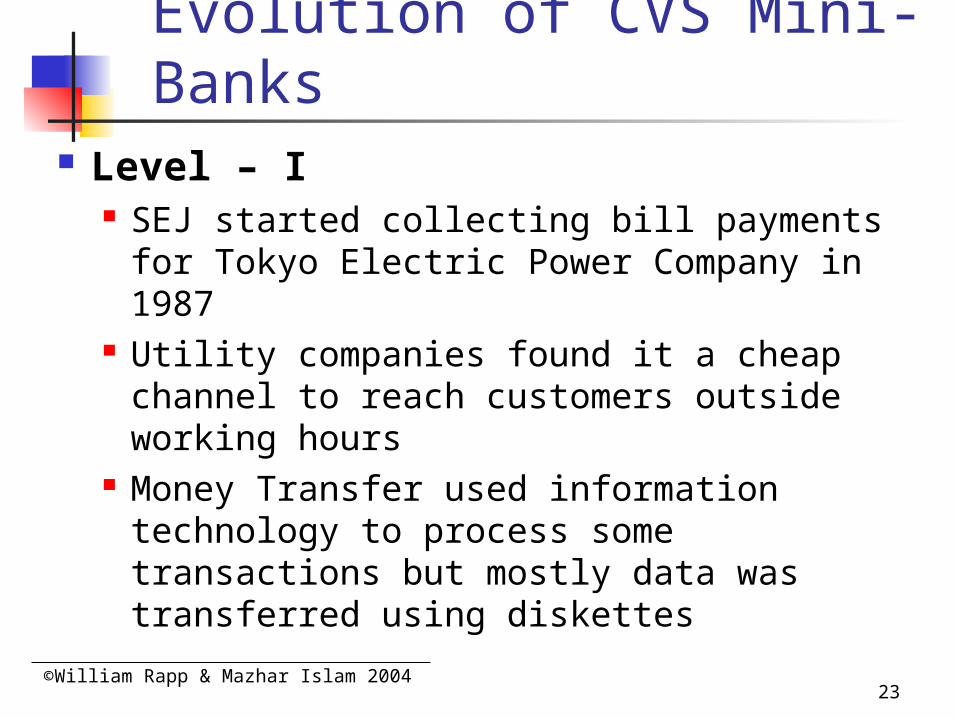

Level – I SEJ started collecting bill payments for

Tokyo Electric Power Company in 1987 Utility companies found it a cheap

channel to reach customers outside working hours

Money Transfer used information technology to process some transactions but mostly data was transferred using diskettes

Evolution of CVS Mini-Banks

©William Rapp & Mazhar Islam 200424

Level – II “Big Bang” reform allowed non-financial firms to

participate in financial services business Began Foreign Exchange Services using ISDN

lines (real time data transfer) Automated Teller Machines (ATM is a bank

branch) Opened “bank accounts” Multimedia Kiosks (MMK) Credit Cards

Evolution of CVS Mini-Banks

©William Rapp & Mazhar Islam 200425

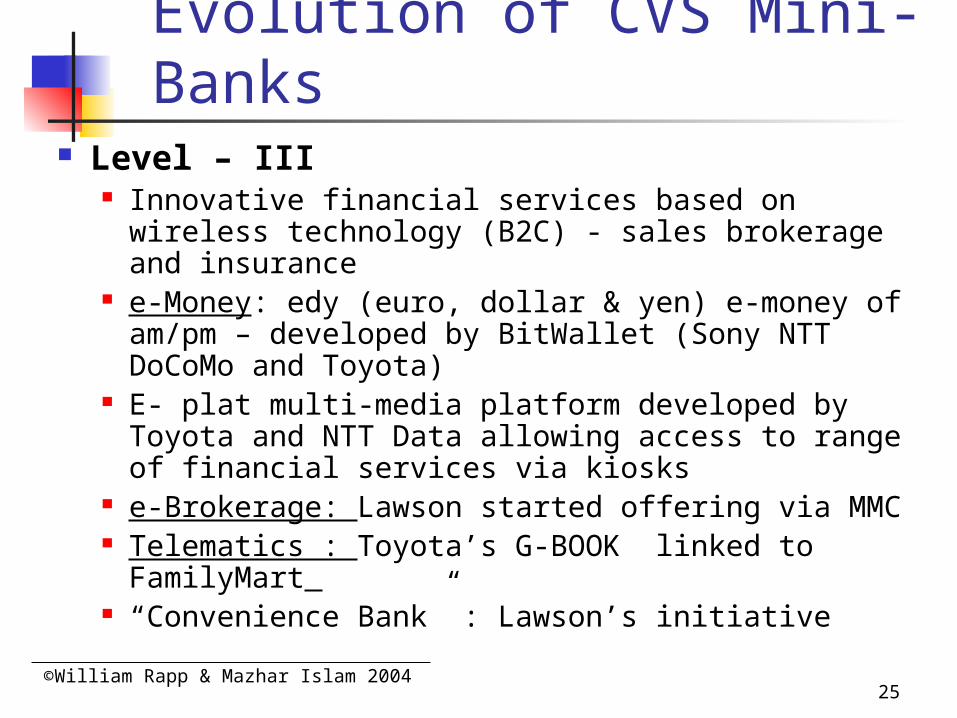

Level – III Innovative financial services based on wireless

technology (B2C) - sales brokerage and insurance e-Money: edy (euro, dollar & yen) e-money of

am/pm – developed by BitWallet (Sony NTT DoCoMo and Toyota)

E- plat multi-media platform developed by Toyota and NTT Data allowing access to range of financial services via kiosks

e-Brokerage: Lawson started offering via MMC Telematics : Toyota’s G-BOOK linked to

FamilyMart “Convenience Bank” : Lawson’s initiative

Evolution of CVS Mini-Banks

©William Rapp & Mazhar Islam 200426

Conclusions Why should the “mini-banks” be

successful in future? Cheaper ubiquitous way to reach customers Strategic use of customer information in

developing financial products and services. i.e. Citigroup’s “customer life cycle model”

In line with the overall strategy of the CVS to increase store traffic

IY-Bank extend superstores and restaurants Connections To Large Japanese and Foreign

Financial Firms WalMart connection