16 - alabama power · environmental management (“adem”). while sips were due september 6, 2016,...

TRANSCRIPT

2016

Integrat

ed Resource

Plan Su

mmary Report

i

2016 Integrated Resource Plan

EXECUTIVE SUMMARY…………….....…………………………………………………………. 1

I. INTRODUCTION..…………………………….………………………….…………………. 7

II. ENVIRONMENTAL STATUTES AND REGULATIONS…..………………...………….. 10II.A. General..…………………………………………..………………….…………….…… 10II.B. Air Quality..…………………..………………...…….………………..……………..… 11II.C. Water Quality..…………………………………………………………….…..…….…. 15II.D. Coal Combustion Residuals..………………………...…………………….…….……. 16II.E. Global Climate Issues..……………………………………………………….….….…. 17

III. INTEGRATED RESOURCE PLAN..……………………………………………....……….. 19III.A. Process Overview..……………………………………………………………..…...…. 19III.B. Load Forecast..………………………………………………………………….…...… 24III.C. Fuel Forecast..…………………………………………………………………….…… 25III.D. Reserve Margin..………………………………………………………………..….…. 26III.E. Resource Options..………………………………………………………………..…… 29III.F. Summary of Results..………………………………………………………….…….… 39

IV. CONCLUSION..………………….…………………………………………………………… 42

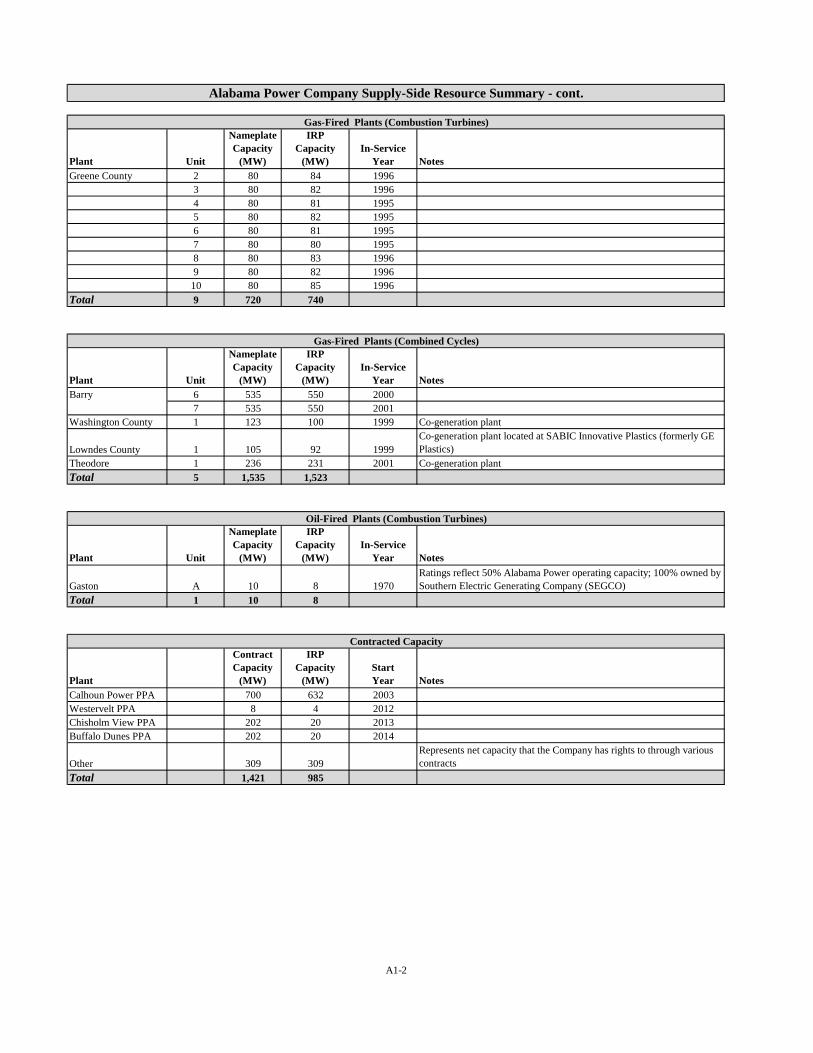

APPENDIX 1 - 2016 Integrated Resource Plan - Existing Supply-Side Resources Figure A1-1: Alabama Power Existing Generating Resources…………….…… A1-1

Alabama Power Company

Summary Report

Alabama Power Company 2016 IRP

1

EXECUTIVE SUMMARY

The Alabama Power Company (“Alabama Power” or “Company”) 2016 Integrated Resource

Plan (“2016 IRP”) serves as the foundation for certain decisions affecting the Company’s

portfolio of supply-side and demand-side resources. Like prior IRPs, the 2016 IRP is a

management tool that facilitates the Company’s ability to provide reliable and cost-effective

electric service to customers, while accounting for the risks and uncertainties inherent in

planning for resources sufficient to meet expected customer demand. The 2016 IRP was

developed and finalized at the end of 2015.

In this 2016 IRP Summary Report (which overviews the complex and data intensive IRP

process), the Company continues to recognize evolving market and regulatory conditions, so as

to position the Company to respond to future developments, all for the benefit of customers. As a

product of the Company’s exhaustive planning process, the 2016 IRP represents a

comprehensive plan and serves as the basis on which the Company can confidently manage its

reliable and diverse portfolio of supply-side and demand-side resources and offer electricity

service at rates below the national average.

In this respect, the 2016 IRP continues the Company’s commitment to providing customers a

diverse supply-side generating portfolio. Resource diversity, which for Alabama Power includes

nuclear, natural gas, coal, oil, hydroelectric, wind, and biomass resources, provides significant

benefit to customers as it enables the Company to adapt more readily to changing economic and

regulatory conditions. In fact, the Company considers it vital to maintain a diverse supply-side

generating portfolio, given the inherent uncertainty of the future and the potential for rapid

changes in the economic and regulatory landscape impacting energy supply. The 2016 IRP

provides flexibility for the benefit of customers.

As the Alabama Public Service Commission (“APSC” or “Commission”) is well aware, one of

the key issues facing the Company at this time is the U.S. Environmental Protection Agency’s

(“EPA”) Clean Power Plan (“CPP”), which was published in final form on October 23, 2015.

The CPP, which calls for the establishment of significant restrictions relating to carbon dioxide

(“CO2”) emissions from electric generating units, stands to significantly impact the Company’s

Alabama Power Company 2016 IRP

2

customers, as well as the customers of other electricity suppliers in Alabama, if the rule is

implemented in its current form. At this time, however, there is much uncertainty with the CPP.

On February 9, 2016, the U.S. Supreme Court granted a stay of the CPP, pending disposition of

petitions for its review with the U.S. Court of Appeals for the District of Columbia Circuit

(“D.C. Circuit”). The stay will remain in effect through the resolution of the litigation, whether

resolved in the D.C. Circuit or the Supreme Court. In view of this judicial activity, the Company

must consider the potential for the rule to be overturned or substantially modified, as well as the

possibility of its being upheld. Compounding this uncertainty is the fact that the CPP does not

apply directly to electric generating units, but instead must be implemented through the

development of a State Implementation Plan (“SIP”) by the Alabama Department of

Environmental Management (“ADEM”). While SIPs were due September 6, 2016, even prior to

the Supreme Court’s stay, ADEM had indicated its intent to request a two-year extension.

Many state plan pathways are available under the CPP. Given these possibilities, and accounting

for the extensive analysis and coordination that must take place before the SIP is completed by

ADEM and submitted to EPA for approval, the Company does not at this time have a CPP

compliance plan or otherwise definitively know the compliance implications for it and its

customers. Thus, the 2016 IRP does not reflect CPP compliance impacts.

While the Company has not yet developed a CPP compliance plan, this IRP reflects a

continuation of the Company’s efforts to have the system in a position to reasonably adapt to a

carbon constrained future. Since the 2013 IRP, the Company has removed the Barry 3 and

Gorgas 6-7 coal units from service. As part of its MATS compliance strategy, it also has

transitioned Greene County 1-2, Gaston 1-4, Barry 1-2 and Gadsden 1-2 from coal operation to

operation on natural gas. The remainder of the Company’s coal-fired generating units continues

to provide substantial economic benefit for customers.

Consistent with the 2013 IRP, the Company continues to explore adding to its generation mix

renewable resources that are projected to bring benefits to customers. This strategy is evidenced

by the Company’s procurement and development of over 400 MW of renewable energy over the

previous six years. Under these projects, the Company has rights to the environmental attributes,

Alabama Power Company 2016 IRP

3

including the renewable energy certificates (“RECs”), associated with the energy. Alabama

Power can retire some, or all, of these environmental attributes on behalf of its retail electric

customers or it can sell the environmental attributes, either bundled with energy or separately, to

third parties. The Company’s renewable resource strategy also now reflects recent action by the

APSC. On September 16, 2015, the APSC issued a certificate of convenience and necessity in

Docket No. 32382 authorizing the Company to develop or procure up to 500 MW of capacity

and energy from renewable energy and environmentally-specialized generating resources. Under

the certificate, Alabama Power is not required to develop or procure the entire 500 MW block of

resources. Rather, projects must satisfy certain specified eligibility criteria. First, the project must

involve a renewable energy resource (such as those identified in Alabama Code § 40-18-1(30))

or an environmentally specialized generating resource (such as combined heat and power), and

be no larger than 80 MW (measured in alternating current (AC) terms). Second, the project must

meet certain economic benefits criteria, namely, that it is expected to result in a positive

economic benefit for all of Alabama Power’s customers. Further, total projects submitted and

approved under the 500 MW certificate authority in any one given calendar year cannot exceed

160 MW without prior authorization from the Commission. In addition, any unexercised

authority under the certificate expires after six years.

Pursuant to the certificate authority in Docket No. 32382, the APSC has since approved three

solar projects. Specifically, on December 14, 2015, the APSC authorized Alabama Power to

construct and own two solar facilities at army installations served by the Company, which are

expected to go into commercial operation on or before December 31, 2016. Additionally, on

June 9, 2016, the APSC approved a power purchase agreement (“PPA”) for the output of a solar

facility near the town of LaFayette in Chambers County, which is expected to go into

commercial operation on or before December 31, 2017. These solar projects will be reflected in

subsequent IRPs. Alabama Power will receive all energy and associated RECs generated by

these projects, which it may use to serve its customers with solar energy or sell to third parties

for the benefit of customers. The Company will continue to consider and evaluate other projects

that would satisfy the criteria set forth in the Commission’s certificate order.

Recently, a new Reserve Margin Study was completed for the Southern Company electric system

(“System”). The detailed analysis reflected in that study supported the conclusion that the long-

Alabama Power Company 2016 IRP

4

term (i.e., greater than three years) target planning reserve margin should be increased from the

15.00 percent target to 16.25 percent while the short-term (i.e., less than three years) target

planning reserve margin should be increased from 13.50 percent to 14.75 percent. This was the

result of a number of factors, including the predicted effects of extreme cold weather events,

customer demand trends, and the penetration of intermittent renewable resources on the System.

Due to the benefits of load diversity, coordinated planning and operations, and the ability to

share resources, the Southern Company retail operating companies can together achieve these

System targets by each utilizing “diversified” reserve margins that are lower than the target

margins for the System. Using the current diversity factor, the Company’s “diversified targets”

corresponding to the new long-term and short term System targets are 14.74 and 13.26 percent,

respectively. Figure ES-1 compares the previous planning reserve margin targets to those

predicated on the new Reserve Margin Study.

FIGURE ES-1: Planning Reserve Margin Target Comparison

Previous

Reserve

Margin Study

Updated

Reserve

Margin Study

System Long-Term Planning Reserve Margin Target 15.00% 16.25%

System Short-Term Planning Reserve Margin Target 13.50% 14.75%

Diversified Long-Term Planning Reserve Margin Target 13.47% 14.74%

Diversified Short-Term Planning Reserve Margin Target 11.99% 13.26%

Since the 2016 IRP was developed and finalized prior to the completion of the new Reserve

Margin Study, the analysis underlying this 2016 IRP was predicated on the then existing 15.00

and 13.50 percent System target planning reserve margins. Consistent with the results of the new

Reserve Margin Study, Alabama Power has begun utilizing, for internal planning purposes, a

16.25 percent long-term System planning reserve margin target and a short-term System

planning reserve margin target of 14.75 percent. Absent further adjustments prompted by the

various factors impacting the system reserve margin, the newly revised reserve margin targets

will be reflected in future IRPs.

Alabama Power Company 2016 IRP

5

Demand-side management (“DSM”) represents an important ingredient in meeting customers’

needs in a reliable and cost-effective manner. However, due to lower avoided costs driven

primarily by natural gas prices and the slow pace of economic recovery in the state, the

introduction of new cost-effective DSM programs is more challenging. Nevertheless, the

Company believes there is value in continuing to identify and offer viable DSM programs,

including the potential benefits that such programs may bring for purposes of compliance with

present and future environmental requirements.

Based on the load forecast developed by the Company for the 2016 IRP, Alabama Power’s

customer electrical requirements can be met reliably with the Company’s current supply-side and

demand-side resources until 2035, at which time there is an indicated need to add intermediate

generating capacity to reliably meet projected demand. Although the Company currently does

not foresee the addition of any new, reliability-driven generating capacity until 2035, the

Company will continue to employ a strategy of identifying renewable resources and demand-side

options that are projected to bring benefits to customers. If and when such resources are

identified, the Company will seek authorization from the APSC for procurement or development

rights related to same.

A number of factors could influence the timing of the Company’s next capacity need and cause it

to accelerate from 2035, perhaps significantly. The most impactful of these would be the

retirement of existing generation in response to new environmental rules and requirements. Other

influencing factors include movement to a higher long-term planning reserve margin, the

addition of new customers, faster customer demand growth, and changes in demand-side

management programs. Future IRPs can be expected to appropriately reflect the impacts of all

such events and developments.

The 2016 IRP is in furtherance of Alabama Power’s goal of providing customers with short- and

long-term electric service, reliably and in an economically efficient manner, through a diverse

portfolio of supply-side and demand-side resources. The Company has developed a cost-

effective and balanced resource strategy while maintaining environmental compliance flexibility

for the benefit of customers. As a result, the Company is well-positioned to serve increases in

customer demand over the 20-year planning horizon. The Company believes the plan charts a

Alabama Power Company 2016 IRP

6

measured course in meeting customer demand in a dynamic regulatory environment, while also

maintaining rates below the national average.

Alabama Power Company 2016 IRP

7

I. INTRODUCTION

Alabama Power is an investor-owned electric utility, organized and existing under the laws of

the State of Alabama, and is a subsidiary of the Southern Company. Alabama Power is primarily

engaged in generating, transmitting and distributing electricity to the public in a large section of

Alabama, and its retail rates and services are regulated by the APSC.

The Company has approximately 1.46 million customers, of which approximately 86 percent

(1.25 million) are residential; 13.5 percent (198,000) are commercial; and 0.5 percent (6,800) are

industrial and other. Alabama Power has approximately 1.56 million transmission and

distribution poles, and approximately 84,000 miles of wire. The Company strives to maintain

cost-effective and reliable service to its customers. For the years 2013-2015, the Company had a

service reliability of 99.98 percent. Alabama Power has a diverse mix of, both owned and

contracted, supply-side and demand-side resource options, including hydroelectric, natural gas,

nuclear, coal, oil, renewablei, combined heat and power, DSM programs and other resources.

As of December 31, 2015, Alabama Power operated 78 Company-owned generating units (20

fossil steam, 41 hydroelectric, 2 nuclear, 5 combined cycle, and 10 combustion turbine) with a

generating capability of approximately 12,300 MW, as recognized in the 2016 IRP. Of the

energy delivered from Company-owned units for year 2015, 54.6 percent was sourced from coal-

fired resources, 23.2 percent from nuclear, 6.1 percent from hydroelectric, and 16.1 percent from

gas and oil. Additionally, the Company has contractual rights to the output of other resources

totaling over 1,000 MW of IRP recognized capacity. A detailed list of the Company’s existing

supply-side resources is shown in Appendix 1 in Figure A1-1.

The purpose of this document is to summarize the results of Alabama Power’s 2016 IRP and to

describe the process used in its development. The IRP serves as the foundation for certain

decisions affecting the Company’s portfolio of generating resources. Like those IRPs preceding

it, the 2016 IRP facilitates the Company’s ability to provide reliable and cost-effective electric

i As mentioned previously, and applicable to all references of renewable projects in the 2016 Integrated Resource Plan Summary Report, the Company has rights to the environmental attributes, including the renewable energy certificates (“RECs”), associated with the energy from these projects. Alabama Power can retire some, or all, of these environmental attributes on behalf of its retail electric customers or it can sell the environmental attributes, either bundled with energy or separately, to third parties.

Alabama Power Company 2016 IRP

8

service to its customers, while accounting for the risks and uncertainties inherent in planning for

electricity supply to meet expected demand. At the most basic level, the IRP yields an indicative

annual schedule of supply-side and demand-side resource additions that are integrated to

accomplish the aforementioned objectives, consistent with the Company’s duties and obligations

to the public as a regulated public utility. The Company’s IRP is performed through a

coordinated process utilized across the Southern Company retail operating companies, with the

assistance of their agent Southern Company Services, Inc. (“SCS”). The process used by

Alabama Power to develop the IRP comports with the provisions of the Public Utility Regulatory

Policies Act of 1978, as amended, which contemplates the use of appropriate integrated resource

planning by electric utilities.

In addition to Alabama Power, the Southern Company is the parent of Georgia Power Company,

Gulf Power Company, Mississippi Power Company, and Southern Power Company,

(collectively, the “Operating Companies”), as well as certain service and special-purpose

subsidiaries. Together with the other Operating Companies, Alabama Power participates in a

pooled operation of generating resources on the System for coordinating system operations and

joint dispatch of their generating units. There are well-recognized advantages and economies

gained from such pooled operations. In order to maximize these benefits, the retail Operating

Companies engage in the coordinated planning of additional resources. Although Alabama

Power participates in this coordinated planning process, the Company remains the final decision-

maker on any resource additions that it may require. Additionally, the System is represented on

the Southeastern Electric Reliability Council (“SERC”), a group of electric utilities (and other

electric-related utilities) coordinating operations and other measures to maintain a high level of

reliability for the electric system in the Southeastern United States. Likewise, Alabama Power

and the other retail Operating Companies, along with nine other transmission owners, are

sponsors of the Southeastern Regional Transmission Planning process (“SERTP”), which

provides an open, coordinated, and transparent transmission planning process for much of the

Southeast in accordance with the requirements of the Federal Energy Regulatory Commission

(“FERC”).

In order to anticipate future energy requirements and electrical demands of the customers it

serves, Alabama Power develops a load forecast that comprises a 20-year projection of the

Alabama Power Company 2016 IRP

9

expected growth in customer requirements. Alabama Power then develops an IRP that reflects,

using the best information reasonably available to the Company, the indicated optimal mix of

supply-side and demand-side resources to meet this projected load growth in customer peak

demand in a reliable and cost-effective manner. The 2016 IRP is predicated on the Company’s

summer peak demand because the System is projected to achieve peak customer demand in the

summer. Alabama Power has traditionally been considered summer peaking, meaning its annual

peak demand falls during the summer months; however, its customer demands have been

growing in the winter months. Indeed, in recent years, with colder weather, Alabama Power’s

winter peak demand has exceeded the summer peak demand. The Company’s most recent load

forecast projects dual peak demands, both in the winter and summer, where the winter peak

demand is slightly higher than the summer peak demand. The Company’s load forecast is

discussed further in the Section III.B.

The IRP is developed on a formal basis every three years and reviewed with the APSC staff. This

review keeps the APSC informed as to the timing of resource additions, while also helping to

ensure that the process yields results that are consistent with the Company’s ultimate goals of

minimizing rates and providing the desired level of service reliability. These goals are important

because they allow the Company to be competitive with other energy providers and promote

economic development within the State of Alabama.

Alabama Power Company 2016 IRP

10

II. ENVIRONMENTAL STATUTES AND REGULATIONSii

II.A. General

The Company’s operations are subject to extensive regulation by state and federal environmental

agencies under a variety of statutes and regulations governing environmental media, including

air, water, and land resources. Applicable statutes include: the Clean Air Act; the Clean Water

Act; the Comprehensive Environmental Response, Compensation, and Liability Act; the

Resource Conservation and Recovery Act; the Toxic Substances Control Act; the Emergency

Planning and Community Right-to-Know Act; the Endangered Species Act; the Migratory Bird

Treaty Act; the Bald and Golden Eagle Protection Act; and related federal and state regulations.

Compliance with these and other environmental requirements involves significant capital and

operating costs, a major portion of which is expected to be recovered through existing

ratemaking provisions. Through 2015, the Company had invested approximately $3.9 billion in

environmental capital retrofit projects to comply with these requirements, with annual totals of

approximately $349 million, $355 million, and $184 million for 2015, 2014, and 2013,

respectively. The Company expects that capital expenditures to comply with environmental

statutes and regulations will total approximately $851 million from 2016 through 2018, with

annual totals of approximately $319 million, $263 million, and $269 million for 2016, 2017, and

2018, respectively. These estimated expenditures do not include any potential capital

expenditures that may arise from the EPA’s final rules and guidelines or subsequently approved

state plans that would limit CO2 emissions from new, existing, and modified or reconstructed

fossil-fuel-fired electric generating units. The Company also anticipates costs associated with

closure in place and ground water monitoring of ash ponds in accordance with the Disposal of

Coal Combustion Residuals from Electric Utilities final rule (“CCR Rule”), which are not

reflected in the capital expenditures above, as these costs are associated with the Company’s

asset retirement obligation (“ARO”) liabilities.

The Company’s ultimate environmental compliance strategy, including potential unit retirement

and replacement decisions, and future environmental capital expenditures will be affected by the

iiThe information in this section is drawn from the combined annual report on Form 10-K of The Southern Company and the Operating Companies for the year ended December 31, 2015, as filed with the Securities and Exchange Commission. Any material difference between the information contained therein and this section is unintended and the annual report should be referenced as the controlling discussion.

Alabama Power Company 2016 IRP

11

final requirements of new or revised environmental regulations, including the environmental

regulations described below; the outcome of any legal challenges to the environmental rules; the

cost, availability, and existing inventory of emissions allowances; and the Company’s fuel mix.

Compliance costs may arise from existing unit retirements, installation of additional

environmental controls, upgrades to the transmission system, closure and monitoring of CCR

facilities, and adding or changing fuel sources for certain existing units.

Compliance with any new federal or state legislation or regulations relating to air, water, and

land resources or other environmental and health concerns could significantly affect the

Company. Although new or revised environmental legislation or regulations could affect many

areas of the Company’s operations, the full impact of any such changes is not known. Many of

the Company’s commercial and industrial customers may also be affected by existing and future

environmental requirements, which for some may have the potential to ultimately affect their

demand for electricity.

II.B. Air Quality

Compliance with the Clean Air Act and resulting regulations has been and will continue to be a

significant focus for the Company. Additional controls to further reduce air emissions, maintain

compliance with existing regulations, and meet new requirements may become necessary in the

future, depending on further actions taken by EPA.

In 2012, the EPA finalized the Mercury and Air Toxics Standards (“MATS”) rule, which

imposed stringent emissions limits for acid gases, mercury, and particulate matter on coal- and

oil-fired electric utility steam generating units. The compliance deadline set by the final MATS

rule was April 16, 2015, with provisions for extensions to April 16, 2016. The implementation

strategy for the MATS rule includes emission controls, retirements, and fuel conversions to

achieve compliance by the deadlines applicable to each Company unit. On June 29, 2015, the

Supreme Court issued a decision finding that, in developing the MATS rule, the EPA had failed

to properly consider costs in its decision to regulate hazardous air pollutant emissions from

electric generating units. On December 15, 2015, the D.C. Circuit remanded the MATS rule to

the EPA without vacatur to respond to the Supreme Court’s decision. The EPA’s supplemental

Alabama Power Company 2016 IRP

12

finding in response to the Supreme Court’s decision, which the EPA finalized on April 15, 2016,

did not have any impact on the MATS rule compliance requirements and deadlines.

The EPA regulates ground level ozone concentrations through implementation of an eight-hour

ozone National Ambient Air Quality Standard (“NAAQS”). In 2008, the EPA adopted a revised

eight-hour ozone NAAQS, and published its final area designations in 2012. All areas within the

Company’s service territory have achieved attainment of the 2008 standard. On October 26,

2015, the EPA published a more stringent eight-hour ozone NAAQS. This new standard could

potentially require additional emission controls, improvements in control efficiency, and

operational fuel changes and could affect the siting of new generating facilities. States will

recommend area designations by October 2016, and the EPA is expected to finalize them by

October 2017.

The EPA regulates fine particulate matter concentrations on an annual and 24-hour average

basis. All areas within the Company’s service territory have achieved attainment with the 1997

and 2006 particulate matter NAAQS, and the EPA has officially redesignated former

nonattainment areas within the service territory as attainment for these standards. In 2012, the

EPA issued a final rule that increases the stringency of the annual fine particulate matter

standard. The EPA completed final designations for the 2012 annual standard for Alabama in

March 2015, and no new nonattainment areas were designated within the Company’s service

territory.

Final revisions to the NAAQS for sulfur dioxide (“SO2”), which established a new one-hour

standard, became effective in 2010. No areas within the Company’s service territory have been

designated as nonattainment under this rule; however, the EPA has not completed the

designation process. The EPA has finalized a data requirements rule to support additional

designation decisions for SO2 in December 2017 and December 2020, which could result in

nonattainment designations for areas within the Company’s service territory. Implementation of

the revised SO2 standard could require additional reductions in SO2 emissions and increased

compliance and operational costs.

Alabama Power Company 2016 IRP

13

In February 2014, the EPA proposed to delete from the Alabama State Implementation Plan

(“SIP”) the Alabama opacity rule that the EPA approved in 2008, which provides operational

flexibility to affected units. This action by the EPA was in response to a 2013 ruling by the U.S.

Court of Appeals for the Eleventh Circuit that vacated an earlier attempt by the EPA to rescind

its 2008 approval. The EPA’s latest proposal characterizes the proposed deletion as an error

correction within the meaning of the Clean Air Act. The Company believes this interpretation of

the Clean Air Act to be incorrect. If finalized, this proposed action could affect unit availability

and result in increased operations and maintenance costs for affected units.

The Company’s service territory is subject to the requirements of the Cross State Air Pollution

Rule (“CSAPR”). CSAPR is an emissions trading program that limits SO2 and nitrogen oxide

emissions from power plants in 28 states in two phases, with Phase I having begun in 2015 and

Phase II beginning in 2017. On July 28, 2015, the D.C. Circuit issued an opinion invalidating

certain emissions budgets under the CSAPR Phase II emissions trading program for a number of

states, including Alabama, but rejected all other pending challenges to the rule. The court’s

decision leaves the emissions trading program in place and remands the rule to the EPA for

further action. As noted earlier, all areas in Alabama have achieved attainment with the 2008

ozone standard. On December 3, 2015, the EPA published a proposed revision to CSAPR to

address interstate transport of emissions for downwind areas that are struggling to meet the 2008

ozone NAAQS. The EPA’s proposed revision would revise existing ozone-season emission

budgets for nitrogen oxide for certain states, including Alabama, beginning in 2017. The EPA

proposes to finalize this rulemaking by summer 2016.

The EPA finalized regional haze regulations in 2005, with a goal of restoring natural visibility

conditions in certain areas (primarily national parks and wilderness areas) by 2064. The rule

involves the application of best available retrofit technology (“BART”) to certain sources,

including fossil fuel-fired generating facilities, built between 1962 and 1977 and any additional

emissions reductions necessary for each designated area to achieve reasonable progress toward

the natural visibility conditions goal by 2018 and for each 10-year period thereafter. In July

2013, ADEM submitted to the EPA a required regional haze mid-course review, concluding that

no changes to the Alabama SIP are necessary to maintain reasonable progress toward visibility

goals. What constitutes BART has been the subject of litigation and is still an unresolved issue

Alabama Power Company 2016 IRP

14

for some Company operated units and therefore, the ultimate impact to Alabama Power and its

customers from BART is not known.

In 2012, the EPA published proposed revisions to the New Source Performance Standard

(“NSPS”) for Stationary Combustion Turbines (“CT”). If finalized as proposed, the revisions

would apply the NSPS to all new, reconstructed, and modified CTs (including CTs at combined

cycle units) during all periods of operation, including startup and shutdown, and alter the criteria

for determining when an existing CT has been reconstructed.

On June 12, 2015, the EPA published a final rule requiring certain states (including Alabama) to

revise or remove the provisions of their SIPs relating to the regulation of excess emissions at

industrial facilities, including fossil fuel-fired generating facilities, during periods of startup,

shut-down, or malfunction (“SSM”) by no later than November 22, 2016.

The Company has developed and continuously updates a comprehensive environmental

compliance strategy to assess compliance obligations associated with the current and proposed

environmental requirements discussed above. As part of this strategy, the Company has

developed a compliance plan for the MATS rule that includes reliance on existing emission

control technologies, the construction of baghouses to provide an additional level of control on

the emissions of mercury and particulates from certain generating units, the use of additives or

other injection technology, the use of existing or additional natural gas capability, and unit

retirements. Additionally, certain transmission system upgrades were required. The Company’s

compliance strategy reduced its coal-fired resources by 1,595 MW. Of the 1,595 MW reduction

in coal-fired resources, 920 MW were fuel switched to natural gas and 675 MW were retired or

placed on inactive reserve. These decisions resulted in a transformation of the Company’s

generating fleet, as shown in Figure II-B-1.

Alabama Power Company 2016 IRP

15

FIGURE II-B-1: APC Generating Capacity by Fuel Type

The ultimate impacts on the Company of the eight-hour ozone, fine particulate matter and SO2

NAAQS, the Alabama opacity rule, CSAPR, regional haze regulations, the MATS rule, the

NSPS for CTs, and the SSM rule will depend on the specific provisions of the proposed and final

rules, the resolution of pending and future legal challenges, and the development and

implementation of rules at the state level. These regulations could result in significant additional

capital expenditures and compliance costs that could affect future unit retirement and

replacement decisions.

II.C. Water Quality

The EPA’s final rule establishing standards for reducing effects on fish and other aquatic life

caused by new and existing cooling water intake structures at existing power plants and

manufacturing facilities became effective in October 2014. The effect of this final rule will

depend on the results of additional studies and implementation of the rule by regulators based on

site-specific factors, as well as on the outcome of ongoing legal challenges. National Pollutant

Discharge Elimination System permits issued after July 14, 2018 must include conditions to

implement and ensure compliance with the standards and protective measures required by the

rule.

55.6%17.8%

13.1%

13.5% CoalGasHydroNuclear

45.5%

26.4%

13.8%

14.3% CoalGasHydroNuclear

Pre-MATS Post-MATS

Alabama Power Company 2016 IRP

16

On November 3, 2015, the EPA published a final effluent guidelines rule that imposes stringent

technology-based requirements for certain wastestreams from steam electric power plants. The

revised technology-based limits and compliance dates will be incorporated into future renewals

of National Pollutant Discharge Elimination System permits at affected units and will require the

installation and operation of multiple technologies sufficient to ensure compliance with

applicable new numeric wastewater compliance limits. Applicability dates between November 1,

2018 and December 31, 2023 will be established by ADEM in permits based on information

provided for each applicable wastestream. The ultimate impact of these requirements will depend

on pending and any future legal challenges, compliance dates, and the selection of available

technology. Engineering and procurement is now underway to convert fly and bottom ash

handling to dry or hybrid systems that, in compliance with the rule, will have no discharge of

water.

On June 29, 2015, the EPA and the U.S. Army Corps of Engineers jointly published a final rule

revising the regulatory definition of waters of the United States for all Clean Water Act

(“CWA”) programs. The final rule significantly expands the scope of federal jurisdiction under

the CWA and could have significant impacts on economic development projects, which could

affect customer demand growth. In addition, this rule could significantly increase permitting and

regulatory requirements and costs associated with the siting of new facilities and the installation,

expansion, and maintenance of transmission and distribution lines. The rule became effective

August 28, 2015, but on October 9, 2015, the U.S. Court of Appeals for the Sixth Circuit issued

an order staying its implementation. The ultimate impact of the final rule will depend on the

outcome of this and other pending legal challenges as well as the EPA’s and the U.S. Army

Corps of Engineers’ field-level implementation of the rule.

These water quality regulations could result in significant additional capital expenditures and

compliance costs that could affect future unit retirement and replacement decisions.

II.D. Coal Combustion Residuals

The Company currently manages CCR at on-site storage units consisting of landfills and surface

impoundments (“CCR Units”) at six generating plants. In addition to on-site storage, the

Company also sells a portion of its CCR to third parties for beneficial reuse. Individual states

Alabama Power Company 2016 IRP

17

regulate CCR and the State of Alabama has its own regulatory requirements. The Company has

an inspection program in place to assist in maintaining the integrity of its coal ash surface

impoundments.

On April 17, 2015, the EPA published the CCR Rule in the Federal Register, which became

effective on October 19, 2015. The CCR Rule regulates the disposal of CCR, including coal ash

and gypsum, as non-hazardous solid waste in CCR Units at active generating power plants. The

CCR Rule does not automatically require closure of CCR Units, but includes minimum criteria

for active and inactive surface impoundments containing CCR and liquids, lateral expansions of

existing units, and active landfills. Failure to meet the minimum criteria can result in the required

closure of a CCR Unit. Although the EPA does not require individual states to adopt the final

criteria, states have the option to incorporate the federal criteria into their state solid waste

management plans in order to regulate CCR in a manner consistent with federal standards. The

EPA’s final rule continues to exclude from regulation the beneficial use of CCR.

Based on initial cost estimates for closure in place and groundwater monitoring primarily related

to ash ponds pursuant to the CCR Rule, the Company recorded AROs related to the CCR Rule.

The Company expects to continue to periodically update these estimates as further analysis is

performed, including evaluation of the expected method of compliance, refinement of

assumptions underlying the cost estimates (such as the quantities of CCR at each site), and the

determination of timing considerations (such as the potential for closing ash ponds prior to the

end of their currently anticipated useful life). The Company is currently completing an analysis

of the plan of closure for all ash ponds, including the timing of closure and related cost recovery

through regulated rates subject to APSC approval. Based on the results of that analysis, the

Company may accelerate the timing of some ash pond closures, which could increase its ARO

liabilities from the amounts presently recorded. The ultimate impact of the CCR Rule will

depend on the Company’s ongoing review of the CCR Rule, the results of initial and ongoing

minimum criteria assessments, and the outcome of legal challenges.

II.E. Global Climate Issues

On October 23, 2015, the EPA published two final actions that would limit CO2 emissions from

fossil fuel-fired electric generating units. One of the final actions contains specific emission

Alabama Power Company 2016 IRP

18

standards governing CO2 emissions from new, modified, and reconstructed units. The other final

action, known as the Clean Power Plan (“CPP”), establishes guidelines for states to develop

plans to meet EPA-mandated CO2 emission rates or emission reduction goals for existing units.

The EPA’s final guidelines require state plans to meet interim CO2 performance rates between

2022 and 2029 and final rates in 2030 and thereafter. At the same time, the EPA published a

proposed federal plan and model rule that, when finalized, states can adopt or that would be put

in place if a state either does not submit a state plan or its plan is not approved by the EPA. On

February 9, 2016, the Supreme Court granted a stay of the CPP, pending disposition of petitions

for appellate review. The stay will remain in effect through the resolution of the litigation,

whether resolved in the D.C. Circuit or the Supreme Court.

These guidelines and standards could result in operational restrictions and material compliance

costs, including capital expenditures, which could affect future unit retirement and replacement

decisions. However, the ultimate financial and operational impact of the final rules on the

Company will depend upon numerous factors, such as the Company’s ongoing review of the

final rules; the outcome of legal challenges, including legal challenges filed by the retail

Operating Companies; individual state implementation of the EPA’s final guidelines, including

the potential that state plans impose different standards; additional rulemaking activities in

response to legal challenges and related court decisions; the impact of future changes in

generation and emissions-related technology and costs; the impact of future decisions regarding

unit retirement and replacement, including the type and amount of any such replacement

capacity; and the time periods over which compliance will be required.

The United Nations 21st international climate change conference took place in late 2015. The

result was the adoption of the Paris Agreement, which establishes a non-binding universal

framework for addressing greenhouse gas emissions based on nationally determined

contributions. It also sets in place a process for increasing those commitments every five years.

The ultimate impact of this agreement will depend on its ratification and implementation by

participating countries.

Alabama Power Company 2016 IRP

19

III. INTEGRATED RESOURCE PLAN

III.A. Process Overview

The integrated resource planning process is designed to identify the types of resources necessary

to serve the long-term expected growth in the energy and demand requirements of Alabama

Power’s customers. Aided by the IRP, the Company is able to effectively develop a resource

strategy that provides for cost-effective, reliable service.

The 2016 IRP, which has a 20-year planning horizon, indicates the optimal mix of resources

necessary to meet customers’ future load requirements. Using the best information available at

the time of its development, the IRP provides the basis for estimating potential capital

expenditures that may be required for future generating capacity additions. The IRP process is

heavily dependent on models, data, and inputs that constitute highly confidential and proprietary

information of the Company.

In the IRP, both supply-side and demand-side options are evaluated and integrated on a

consistent basis through the use of marginal cost analysis. This approach ensures that both

supply-side and demand-side options are identified for potential selection and deployment when

such options represent a viable economic choice.

As shown in Figure III-A-1, integrated resource planning is a dynamic process that continuously

evaluates existing and potential resource options in an effort to identify the best combination, in

terms of reliability and expected total cost for serving customers.

Alabama Power Company 2016 IRP

20

FIGURE III-A-1: Alabama Power IRP Process

UPDATE MARGINAL COST PROJECTIONS

BASED ON LATEST IRP . Revised Fuel Cost . Revised Technology Cost . Regulatory Compliance

MARGINAL COST DEMAND-SIDE

EVALUATIONS

MARGINAL COST SUPPLY-SIDE

EVALUATIONS

. Modification of Existing Resources . Purchased Power Options

RESOURCE MIX ANALYSIS AND BENCHMARK

EVALUATIONS . Reliability Requirements . Existing Resources Characteristics Update . Future Generation Options . Cost Effectiveness . Sensitivity Analysis

INTEGRATION

CURRENT INTEGRATED RESOURCE

PLAN

. Adjustment to Benchmark Plan . Resource Scheduling . Financial Assessment

LOAD FORECAST

. Identification of Possible DSOs . Screening & Analysis . Market Program Design

. End-Use Modeling

. Econometric Modeling

. Customer Analysis

PRIOR INTEGRATED RESOURCE

PLAN

UPDATE MARGINAL COST PROJECTIONS

BASED ON LATEST IRP LOAD FORECAST

LOAD FORECAST

Alabama Power Company 2016 IRP

21

The principal components in the process are as follows:

Update Marginal Cost Projections Based on Latest IRP

Marginal cost projections are derived using the previous IRP. These projections are then

updated to recognize any significant changes in costs such as fuel, technology and regulatory

compliance.

Load Forecast

A forecast of future energy and peak demand requirements for the next 20 years is developed.

This forecast incorporates an estimate of future economic conditions and trends in customer

energy usage.

Marginal Cost Demand-Side Evaluations

Demand-side management (“DSM”, sometimes also referred to as demand-side options, or

“DSO”) programs are evaluated on a marginal cost basis. This procedure is used to identify cost-

effective DSM programs for inclusion in the IRP.

Marginal Cost Supply-Side Evaluations

Marginal cost evaluations are performed to determine if modifications to existing resources or

power purchases from other suppliers are economically viable.

Resource Mix Analysis and Benchmark Evaluations

This part of the IRP process involves the development of an optimum resource mix. The resource

mix is a flexible, iterative analysis that allows for integration of the appropriate combination of

resources that will serve the projected load at the lowest expected total cost (both fixed and

variable), while maintaining a target reliability guideline. This step includes sensitivity analyses

to establish boundaries within which the conclusions of a benchmark plan remain valid.

The resource mix analysis incorporates the impacts of existing and projected DSM programs,

revised load information, and updated cost information (including fuel, capital, operation and

maintenance). It also incorporates the most recent information on the characteristics of existing

resources, both supply-side and demand-side.

Alabama Power Company 2016 IRP

22

The flexibility of the IRP process allows insertion of marginal cost results from the supply-side

or demand-side options in any sequence. The result is a benchmark plan from which the most

cost-effective combination can be determined in an integration step.

In planning future resource additions, consideration is given to uncertainties associated with

unforeseen unit outages, abnormal weather and load forecast deviations. In order to minimize the

effects of these uncertainties, criteria are established that qualify and quantify an appropriate

level of capacity reserves. These reserves are planned to be available so as to account for the

potential inability to meet load requirements due to generation shortfalls resulting from

uncertainties inherent in the resource planning process. The criteria are called reserve criteria and

are specified as margins. The minimum long-term target reserve margin guideline, which is

periodically reviewed and re-evaluated, is based on economic analyses, operating experience and

system operation input, and seeks to minimize the combined cost of new generating capacity,

production costs, and customer-related costs associated with outages.

The 2016 IRP utilized a minimum long-term System target planning reserve margin guideline of

15.00 percent. By virtue of load diversity across the Southern Company electric system, a

minimum long-term target reserve margin of 15.00 percent can be met if each Operating

Company maintains a minimum long-term reserve margin of at least 13.50 percent. In other

words, by participating in the Southern Company pool, Alabama Power can maintain a long-term

reserve margin of 13.50 percent but realize a level of reliability equivalent to a long-term reserve

margin of 15.00 percent, thereby avoiding the cost of building or purchasing additional resources

associated with the 1.50 percent differential. These capacity savings represent one of the

recognized benefits of operating as a pool.

As discussed in Section III.D. of this report, an updated Reserve Margin Study indicates the need

to increase the System’s long-term target planning reserve margin. Due to the timing of the

completion of the study, the 2016 IRP does not reflect a higher target planning reserve margin

target. However, subsequent to the completion of the new study, the Company has begun

utilizing, for planning purposes, an updated long-term System planning reserve margin target of

16.25 percent, which equates to a long-term diversified planning reserve margin target for

Alabama Power of 14.74 percent. Absent further adjustments prompted by the various factors

Alabama Power Company 2016 IRP

23

impacting the system reserve margin, the newly revised reserve margin targets will be reflected

in future IRPs.

Integration

Demand-side and supply-side options identified as cost-effective choices for resource additions,

but not previously reflected in a benchmark plan, are incorporated into the IRP in the integration

phase. This phase consists of determining the Company’s best alternative for meeting the

resource needs identified in the benchmark plan, coordinating resource additions with those of

the other retail Operating Companies, and performing a financial assessment of the plan.

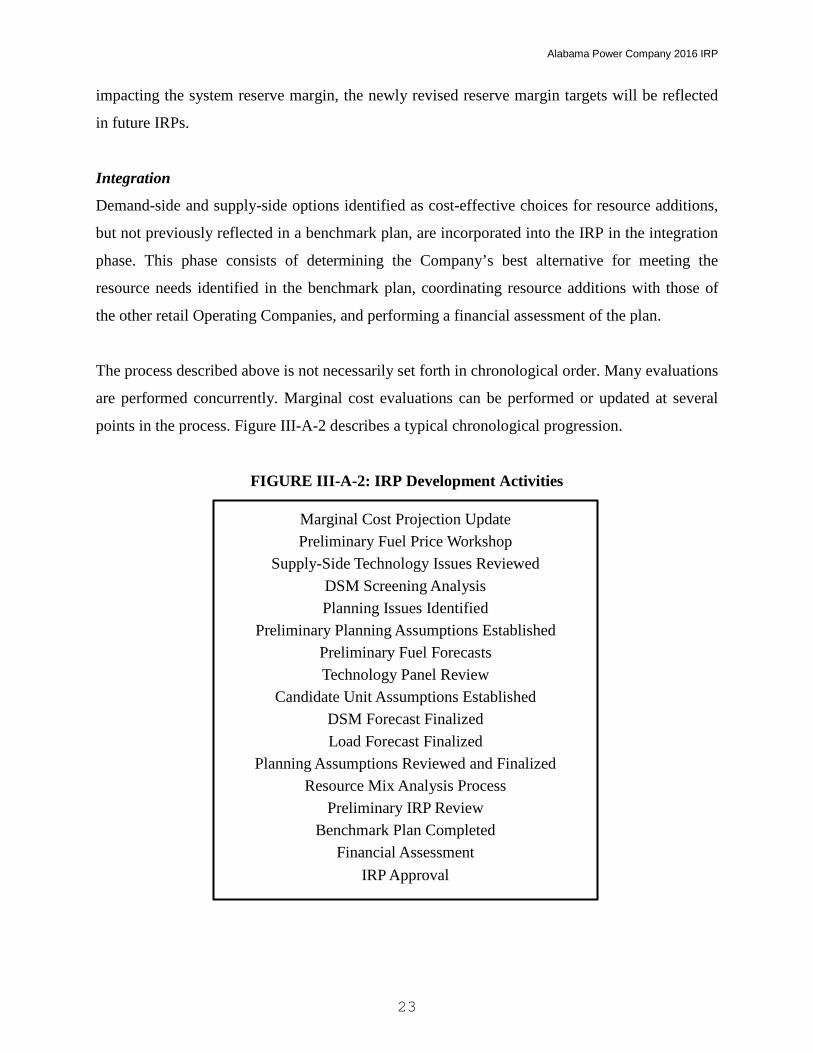

The process described above is not necessarily set forth in chronological order. Many evaluations

are performed concurrently. Marginal cost evaluations can be performed or updated at several

points in the process. Figure III-A-2 describes a typical chronological progression.

FIGURE III-A-2: IRP Development Activities

Marginal Cost Projection Update Preliminary Fuel Price Workshop

Supply-Side Technology Issues Reviewed DSM Screening Analysis Planning Issues Identified

Preliminary Planning Assumptions Established Preliminary Fuel Forecasts Technology Panel Review

Candidate Unit Assumptions Established DSM Forecast Finalized Load Forecast Finalized

Planning Assumptions Reviewed and Finalized Resource Mix Analysis Process

Preliminary IRP Review Benchmark Plan Completed

Financial Assessment IRP Approval

Alabama Power Company 2016 IRP

24

III.B. LOAD FORECAST

The Company annually produces a short-term and long-term energy and peak demand forecast

for territorial customers of Alabama Power, including projections of customer growth, peak

demand (MW), and monthly energy consumption (kWh). The 2016 IRP reflects a load forecast

for the years 2016-2035.

Underlying this load forecast are economic data and forecasts supplied by Moody’s Analytics.

These economics incorporate available benchmarked employment and demographic data as well

as other economic indicators for the state, all of which support the development of econometric

models for the forecast of the number of customers, the energy sales to the customers and the

peak demand required to meet customers’ needs. End use models are used when possible to

incorporate long term effects of appliance saturation and increased efficiency trends on sales. As

might be expected, this forecast continues to reflect the ongoing, lingering effects of the

worldwide economic recession.

Although Alabama Power has traditionally been considered summer peaking, meaning its annual

peak demand falls during the summer months, its customer demands have been growing in the

winter months. In recent years, with colder weather, Alabama Power’s winter peak demand has

exceeded the summer peak demand. The 2014 actual winter peak was 12,610 MW prior to the

utilization of the Company’s interruptible and demand management options. The 2014 winter

peak was over 1,200 MW higher than the 2014 summer peak. The Company’s most recent load

forecast projects dual peak demands, both in the winter and summer, where the winter peak

demand is slightly higher than the summer peak demand with projected growth rates which are

lower than what was reflected in the 2013 IRP. As such, the 2016 IRP forecast reflects the

effects of both a slower economic recovery in the near term and greater levels of appliance and

lighting efficiencies.

These forecast results are heavily dependent on the economic forecast of employment in

Alabama. Another influencing factor is lower demand for commodities produced in Alabama,

which has weakened in the wake of lower oil prices and a stronger dollar. It is important to note

that, although the current forecast is somewhat lower than the forecast used in the 2013 IRP, it

Alabama Power Company 2016 IRP

25

nonetheless reflects economic growth in Alabama and continued employment recovery from the

Great Recession.

As discussed previously, although the Company’s most recent peak demand forecast is slightly

higher in the winter season, the 2016 IRP is still based on the Company’s summer peak because

the System is still projected to peak in the summer season throughout the planning horizon. The

Company will continue to assess the winter/summer peak comparison and any implications it

may have to the coordinated planning process in the future.

III.C. FUEL FORECAST

Both short-term (current year plus two) and long-term (year four and beyond) fuel and allowance

price forecasts are developed for use in the Company’s planning activities, business case

analyses, and decision making. Short-term forecasts are updated monthly as part of the

Company’s fuel budgeting process and marginal pricing dispatch procedures. The long-term

forecasts are developed each year for use in the Company’s planning activities. Charles River

Associates (“CRA”), the Company’s scenario modeling consultant, produces the long-term fuel

price forecasts for natural gas and coal.

The development of the long-term forecasts is a highly collaborative effort between CRA, SCS,

and the retail operating companies. CRA’s MRN-NEEM national, multi-sector, energy-economy

model, with support from other CRA models, was used to generate integrated results for natural

gas and coal prices, in five-year increments, for the period 2020 through 2055. The integrated

modeling approach makes it possible to develop forecasts for natural gas, petroleum, and coal

prices that are internally consistent with one another and with other variables and feedbacks

involving economic growth, electricity consumption, and output across many sectors and

regions. The integrated approach takes a set of assumptions about market fundamentals and then

solves for the prices that make the quantity supplied equal to the quantity demanded in all

markets. In addition, the integrated approach simulates interactions among different markets and

thereby reveals how such things as environmental regulations and natural gas supply outlooks

shape the disposition of economic output across sectors, as well as the competition between coal

and natural gas as a generation fuel.

Alabama Power Company 2016 IRP

26

The modeling process began with the calibration of the MRN-NEEM model to the most recent

Energy Information Agency (“EIA”) Annual Energy Outlook (“AEO”), in this case the AEO

2015 Reference case. The AEO 2015 Reference case assumes a continuation of only those

environmental policies in place (finalized, but not necessarily implemented) at the time of the

forecast, while the CRA analysis assumes that other proposed rules that the EPA has yet to

finalize (or has finalized since EIA performed its Reference case forecast) will come into effect.

As a result, the CRA forecasts anticipate a larger decrease in coal plant fleet size, which tends to

raise natural gas prices relative to EIA projections.

III.D. RESERVE MARGIN

Because electric utility customers expect and depend on a high level of service reliability, a retail

electric utility should have an economically balanced margin of generating capacity in excess of

the peak load. To have this reserve capacity available when it is needed, a utility must plan much

further beyond the upcoming season because the processes to procure additional capacity, such

as building a new unit or completing a PPA, can take several years. The purpose of a Reserve

Margin is to determine an appropriate amount of reserve capacity that should be targeted for the

System at any point in the future.

Four primary reasons for having this reserve capacity are:

1) Weather: The System’s load forecasts are based on average weather conditions

over the past 20 years. If the weather is hotter than normal during warm seasons or

colder than normal during cold seasons, the load will be higher. Drought conditions

and temperature-related impacts on unit outputs can also significantly affect the

System’s load and capacity balance.

2) Economic Growth Uncertainty: It is impossible to project exactly how many new

customers a utility will have or how much power existing customers will use from

season to season. Based on historical projections and actual economic growth, peak

demand may grow more than expected during the period required to procure new

resources.

Alabama Power Company 2016 IRP

27

3) Unit Performance: By their very nature, machines can be expected to fail from

time to time. While the System has a proven history of very low forced outage rates,

there have been occasions when higher than average levels of capacity on the

System have been in a concurrent forced outage condition.

4) Market Availability Risk: The ability to obtain resources from the wholesale

power market when needed to address a short-term System resource adequacy issue

is subject to uncertainty. In general, having access to resources in neighboring

regions does enhance a region’s reliability due to load and resource diversity.

However, the amount, cost, and deliverability of those resources are subject to the

external region’s resource-adequacy situation and transmission capability at any

given time. While a region can expect support from its neighbors, that region must

carry adequate reserves to handle situations where access to resources outside the

region is limited.

While each of these four factors on its own creates a need for capacity reserves, a confluence of

all these risk factors would pose considerable risk. A very high reserve level would be required

to meet customers’ load demands, plus operating reserve requirements, in order to prepare for a

simultaneous occurrence of all such events. However, maintaining such high levels of capacity

reserves would come at significant expense and would address a scenario with a very low

probability. The more appropriate approach to setting the optimum target reserve margin is to

minimize the combined expected costs of maintaining reserve capacity, production costs, and

customer costs associated with service interruptions, adjusting for value at risk.

In order to understand and quantify the overlap of the four contributing factors to the need for

reserve margins, the Strategic Energy and Risk Valuation Model (“SERVM”) is utilized.

SERVM is a system dispatch model that evaluates the ability of the System’s capacity resources

to meet load obligations every hour in a year for thousands of combinations of weather, load

forecast deviations, and unit performance issues. The model quantifies, in dollar cost, two

components of reliability-related costs:

1. Production costs, including sales and purchases

Alabama Power Company 2016 IRP

28

2. Customer cost of outages (i.e., the cost of expected unserved energy, or “EUE”)

The analysis is performed on a range of planning reserve margins. With lower reserve margin

levels, the reliability costs are high and vary widely, but the cost of carrying reserves is low. At

higher reserve margin levels, the reliability costs are low, but the cost of carrying reserves is

high. The objective of this analysis is to determine the target reserve margin where the sum of

these costs (i.e., those related to reliability and those related to carrying reserves) is minimized

(i.e., the minimum cost point).

The cost considerations that the analysis seeks to minimize reflect very different risk

characteristics. The trade-off between relatively static capacity costs and highly volatile

reliability costs is difficult to measure. The approach taken to account for this inherent difference

is to evaluate the risk using the risk metric Value at Risk (“VaR”), at confidence levels between

85 percent and 95 percent. Value at Risk was calculated by subtracting the average cost from

each specific scenario’s cost. For a number of mild weather or slow load growth scenarios, the

total cost was lower than average. For the extreme cases, the scenario cost was much higher than

average. The 85 percent confidence VaR represents the total cost in the 85 percent case, minus

the average cost. The risk tradeoff can be seen in the flatness of the total cost “U” curve near the

optimum reserve margin point; a reserve margin a few percentage points higher than the

optimum reserve margin would not cost much more on average and would eliminate a number of

expensive scenarios, thereby lowering risk.

A minimum long-term System target planning reserve margin guideline of 15.00 percent was

used in the 2016 IRP. As noted previously, peak load diversity enables the System to meet that

15.00 percent target guideline if each Operating Company maintains a reserve margin of at least

13.50 percent. These planning reserves protect against a shortfall in capacity and a loss of load

due to unforeseen future events, such as greater than expected load growth or unusual weather.

Based on the load forecast and target reserve margins utilized in the 2016 IRP, the Company has

sufficient resources to provide an appropriate level of reserves to meet customers’ electrical

needs until 2033. Beginning in 2033, the Company’s reserve margin is projected to fall below its

diversified target planning reserve margin guideline (13.50 percent). The projected capacity

Alabama Power Company 2016 IRP

29

deficit below target in 2033, combined with sufficient Southern system reserves, is not large

enough to result in a resource addition for Alabama Power. By 2035, however, Alabama Power

is projected to have a need for new intermediate resources to maintain its target planning reserve

margin guideline. A number of factors could influence the timing of the Company’s next

capacity need and cause it to accelerate from 2035, perhaps significantly. The most impactful of

these would be the retirement of existing generation in response to new environmental rules and

requirements. Other influencing factors include movement to a higher long-term planning

reserve margin, the addition of new customers, faster customer demand growth, and changes in

demand-side management programs.

As discussed earlier, a new Reserve Margin Study was completed after the 2016 IRP was

finalized and demonstrates that the System planning reserve margin targets of 15.00 percent

(long-term) and 13.50 percent (short-term) no longer provide the appropriate balance between

the cost of reliability and cost of additional resources. A number of factors drove this change,

including the predicted effects of extreme cold weather events, customer demand trends, and the

penetration of intermittent renewable resources on the System. The updated study supports an

increase in these System planning reserve targets. Informed by the study, the Company has

begun utilizing, for planning purposes, a 16.25 percent long-term System planning reserve

margin target and a 14.75 percent short-term System reserve margin target, which equate to

diversified (individual retail operating company) planning reserve margin targets of 14.74 and

13.26 percent, respectively. Absent further adjustments prompted by the various factors

impacting the system reserve margin, the newly revised reserve margin targets will be reflected

in the Company’s future IRPs. Holding all other elements in the 2016 IRP constant, the

application of the revised long-term target planning reserve margin would result in Alabama

Power’s reserve margin falling below its diversified target a couple of years earlier than 2033.

III.E. RESOURCE OPTIONS

The process that led to the development of the 2016 IRP included consideration of demand-side

and supply-side options. Detailed analyses were performed on viable options to ensure that cost-

effective resource alternatives were identified to meet projected load growth and satisfy the

appropriate reliability criteria.

Alabama Power Company 2016 IRP

30

The Company will add supply-side and/or demand-side, active or passive, resources to maintain

the Company’s minimum long-term target planning reserve margin guideline. An active DSM

program is one that is dispatchable or controllable (“activated”) by the Company at the time of

need. In contrast, a passive DSM is an alternative adopted by customers that becomes embedded

in their electric energy use pattern and requirement. The effects of passive DSM additions are

captured in the load forecast in the form of peak load reduction megawatts.

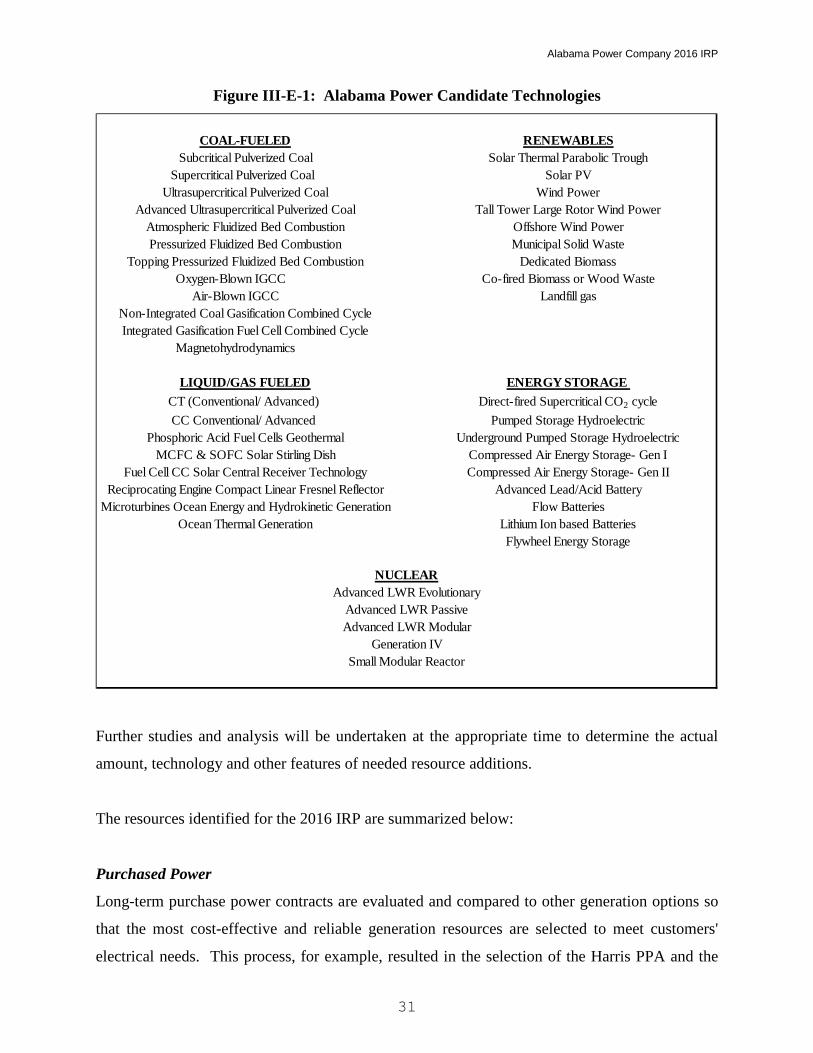

A list of technology options is shown in Figure III-E-1. Assumptions for cost, performance,

design maturity, regulatory approval, and other parameters for uncommitted resource options

continue to change. The following list represents, but is not all-inclusive of, resource option

technologies that may be selected in the future:

Alabama Power Company 2016 IRP

31

Figure III-E-1: Alabama Power Candidate Technologies

Further studies and analysis will be undertaken at the appropriate time to determine the actual

amount, technology and other features of needed resource additions.

The resources identified for the 2016 IRP are summarized below:

Purchased Power

Long-term purchase power contracts are evaluated and compared to other generation options so

that the most cost-effective and reliable generation resources are selected to meet customers'

electrical needs. This process, for example, resulted in the selection of the Harris PPA and the

COAL-FUELED RENEWABLESSubcritical Pulverized Coal Solar Thermal Parabolic Trough

Supercritical Pulverized Coal Solar PVUltrasupercritical Pulverized Coal Wind Power

Advanced Ultrasupercritical Pulverized Coal Tall Tower Large Rotor Wind PowerAtmospheric Fluidized Bed Combustion Offshore Wind PowerPressurized Fluidized Bed Combustion Municipal Solid Waste

Topping Pressurized Fluidized Bed Combustion Dedicated BiomassOxygen-Blown IGCC Co-fired Biomass or Wood Waste

Air-Blown IGCC Landfill gasNon-Integrated Coal Gasification Combined CycleIntegrated Gasification Fuel Cell Combined Cycle

Magnetohydrodynamics

LIQUID/GAS FUELED ENERGY STORAGE CT (Conventional/ Advanced) Direct-fired Supercritical CO2 cycleCC Conventional/ Advanced Pumped Storage Hydroelectric

Phosphoric Acid Fuel Cells Geothermal Underground Pumped Storage HydroelectricMCFC & SOFC Solar Stirling Dish Compressed Air Energy Storage- Gen I

Fuel Cell CC Solar Central Receiver Technology Compressed Air Energy Storage- Gen IIReciprocating Engine Compact Linear Fresnel Reflector Advanced Lead/Acid Battery

Microturbines Ocean Energy and Hydrokinetic Generation Flow BatteriesOcean Thermal Generation Lithium Ion based Batteries

Flywheel Energy Storage

NUCLEARAdvanced LWR Evolutionary

Advanced LWR PassiveAdvanced LWR Modular

Generation IVSmall Modular Reactor

Alabama Power Company 2016 IRP

32

Calhoun Power PPA for certification by the APSC. Alabama Power will continue to evaluate

purchase power options as a part of its IRP process, with the goal being to provide customers

with reliable energy at the lowest practical cost. This evaluation includes consideration of an

appropriate balance of Company-owned/controlled assets, as opposed to PPAs that provides a

contractual right to power from assets controlled by third parties. Relevant in this regard is the

practice of rating agencies to treat long term PPA obligations as a debt equivalent, which

adversely impacts the Company’s capital structure for ratings purposes and, thus, represents a

cost to the Company. Short-term power purchases are used when appropriate to meet short-term

capacity needs.

Renewable Resources

Consistent with the 2013 IRP, the Company continues to explore adding to its generation mix

renewable resources that are projected to bring benefits to customers. This strategy is evidenced

by the Company’s procurement and development of over 400 MW of renewable energy over the

previous six years. Under these projects, the Company has rights to the environmental attributes,

including the renewable energy certificates (“RECs”), associated with the energy. Alabama

Power can retire some, or all, of these environmental attributes on behalf of its retail electric

customers or it can sell the environmental attributes, either bundled with energy or separately, to

third parties.

The Company’s renewable resource strategy also now reflects recent action by the APSC. On

September 16, 2015, the Commission issued to the Company a certificate of convenience and

necessity in Docket No. 32382 authorizing the development or procurement of up to 500 MW of

capacity and energy from renewable energy and environmentally-specialized generating

resources. In accordance with the certificate, Alabama Power is not required to develop or

procure the entirety of the 500 MW. Rather, projects presented to the Commission for approval

must satisfy certain eligibility criteria. First, the project must involve a renewable energy

resource (such as those identified in Alabama Code § 40-18-1(30)) or an environmentally

specialized generating resource (such as combined heat and power), and be no larger than 80

MW (measured in alternating current (AC) terms). Second, the project must meet certain

economic benefits criteria, namely, that it is expected to result in a positive economic benefit for

all of Alabama Power’s customers. The APSC will consider projects up to 160 MW of the

Alabama Power Company 2016 IRP

33

certificated amount annually; any proposal in excess of that annual threshold requires prior

authorization. In addition, any unexercised authority under the certificate expires after six years.

Consistent with the certificate authority, the APSC subsequently approved two projects on

December 14, 2015. Specifically, on December 14, 2015, the APSC authorized Alabama Power

to construct and own two solar facilities at army installations served by the Company, which are

expected to go into commercial operation on or before December 31, 2016. Additionally, on

June 9, 2016, the APSC approved a power purchase agreement (“PPA”) for the output of a solar

facility near the town of LaFayette in Chambers County, which is expected to go into

commercial operation on or before December 31, 2017. These solar projects will be reflected in

subsequent IRPs. Alabama Power will receive all energy and associated RECs generated by

these projects, which it may use to serve its customers with solar energy or sell to third parties

for the benefit of customers.

Given the authorization in Docket No. 32382, the Company has removed the 25 MW of generic

renewable resources identified in the 2013 IRP. Additional renewable resources will be added to

its plan as they are identified, either through the exercise of the authority under that certificate or

through another vehicle.

Cogeneration/Combined Heat and Power (“CHP”)

Currently, the Alabama Power system includes more than 500 MW of Company-owned CHP

generation. Cogeneration and CHP have been options for the Company for many years.

During the 1990s, when the Company needed to add new generation to reliably meet the load

obligations of its customers, Alabama Power was able to develop new generation resources near

certain customer facilities. These new generating facilities provided cost-effective capacity and

energy to all of its customers, while also satisfying the steam needs of the specific customers at

those locations. More recently, the Company has used a program authorized by the APSC to

certify two PPAs for rights to capacity and energy from two customer-owned CHP facilities.

The Company’s success in identifying CHP projects that are expected to bring benefits to all

customers is attributable in large part to the APSC’s recognition that resource and capacity

Alabama Power Company 2016 IRP

34

additions do not follow a one-size-fits-all approach. This is particularly so with CHPs, where a

good working arrangement between all parties is essential for these projects to be developed, and

where an adaptive regulatory process is critical to the project’s success.

Future Generation

Based on the load forecast utilized in the 2016 IRP, increases in customer electrical demand can

be met with the Company’s existing generation and demand-side resources until 2035.

Beginning in 2035, the 2016 IRP indicates that additional intermediate generation capacity will

be required to meet forecasted increases in customer electrical demand throughout the remainder

of the planning horizon. As noted previously, a number of factors could influence the timing of

the Company’s next capacity need and cause it to accelerate from 2035, perhaps significantly.

The most impactful of these would be the retirement of existing generation in response to new

environmental rules and requirements. Other influencing factors include movement to a higher

long-term planning reserve margin, the addition of new customers, faster customer demand

growth, and changes in demand-side management programs. Future IRPs can be expected to

appropriately reflect the impacts of all such events and developments.

Demand-Side Management Programs

Alabama Power is committed to both economic growth and environmental stewardship within

the state. In concert with customer needs and desires, Alabama Power works to ensure that it

continues to have the reliable and cost-effective energy needed to promote the interests of the

region. In doing so, Alabama Power continues to be an industry leader in cost-effective demand

side management programs. The Company implements DSM measures and programs that are

designed to reduce customers’ energy bills, improve their competitiveness, assist with system