16 a cesce ctivitysinglaterra.cesce.es/sites/all/themes/cesce/docs/memoria2016/...struct ure tim...

TRANSCRIPT

2016

C E S C E ’ SA C t i v i t y R E p o R t

C O N T E N T S

L E t t E R o F t H E C H A i R M A N

P 1 2

2

p R o F i L Eo F C E S C E

P 4

1

22CESCE’S ACtivity REpoRt 2016 22CESCE’S ACtivity REpoRt 2016

CONSULTANCY, SURETY AND CREDIT INSURANCE AND SOLUTIONS

3 . 1 P 1 9

EXPORT CREDITAGENCY (ECA)

3 . 2P 3 6

PERFORMANCE DURING THE YEAR4 . 2 P 6 2

INFORMATION AND SERVICES3 . 3 P 4 9

ECONOMIC ENVIRONMENT4 . 1 P 5 3

Business model3.1.1 P 2 0

Foreign sector support in 20163.2.1 P 3 7

Credit and surety insuranceand solutions

4.2.1P 6 3

International economic environment4.1.1 P 5 3Spain4.1.2 P 5 7

Commercial offer of insurance and financing3.1.2 P 3 0

The many faces of CESCE’s activities3.2.2 P 4 1Spanish ExportCredit Agency (ECA)

4.2.2P 6 7

Surety3.1.3 P 3 4

B U S i N E S S L i N E S

P 1 8

3

C E S C E i N 2 0 1 6

P 5 2

4

C O N T E N T S

3CESCE’S ACtivity REpoRt 2016

CESCE heads a group of companies whose common pro ject i s to prov ide

secur i ty in commerc ia l t ransact ions v ia comprehens ive management of

commerc ia l r i sk , in format ion and technology. I t i s a mixed-cap i ta l

company wi th a s ta te ma jor i ty, as we l l as the Expor t Cred i t Agency

(ECA) respons ib le for manag ing expor t c red i t insurance on beha l f o f

the Span ish S ta te .

P r o f i l e o f C E S C E

1

44CESCE’S ACtivity REpoRt 2016

To boost the robust growth of our customers over the long term by providing them with smart solutions for managing commercial credit encompassing the whole value chain of the business (market prospecting, management and coverage of risk, and access to financing), and with surety and guarantee solutions enabling them to tackle new projects and businesses.

To comply with our public obligation as managers of Export Credit Insurance on behalf of the State in a way which is technically rigorous and professional, which strictly complies with applicable legislation, and which is completely focused on support for Spanish companies’ internationalisation activities.

We would like to consolidate our position as the institution providing the best support to companies selling on credit

to other companies by designing innovative solutions which will always give us the edge over our competitors conceptually and technologically. We would also like to become the benchmark in the market for our quality of service, for the professional and personal development

commitment to society.

INNOVATION

SUPPORT FOR ECONOMIC ACTIVITY

AND INTERNATIONALISATION

CUSTOMER COMMITMENT

ETHICAL AND RESPONSIBLE CONDUCT

COMMITMENT TO PEOPLE

M I S S I O N

V I S I O N

V A L U E S

5CESCE’S ACtivity REpoRt 2016

FROFILE OF CESCE LEttER BUSiNESS LiNES CESCE iN 2016

Credit insurance,consultancy and surety

solutions

Spanish ExportCredit

Agency (ECA)

Information andservices

Argentina

DBK Informa

Experian

Logalty

Spain

Portugal

Colombia

Informa D&B CTIBrazil

Chile

Spain

France

Portugal

Colombia

Mexico

Peru

Venezuela(*) In credit and sureties

10countries

1. CESCE

2. CESCE France

3. CESCE Portugal

4. CESCE Argentina

5. CESCE Brazil

6. CESCE Chile

7. SEGUREXPO Colombia

8. CESCEMEX Mexico

9. SECREX Peru

10. LA MUNDIAL Venezuela

8

7 10

5

32

9

64

O n t h e l a r g e s c a l e

Commercial, financial and marketing information on

companies and entrepreneurs.

Comprehensive credit management services,

technological solutions and business process outsourcing.

Integrated services to help companies grow in every

phase of the business cycle.

Management of coverage on behalf of the Spanish state of the

commercial, political and extraordinary risks related to the

globalisation of Spanish companies.

S t r u c t u r e

4thgroup

worldwide*

2ndin

Spain*

P r e s e n c e i nE u r o p e a n d L a t i n A m e r i c a

1.13million

credit limitsin force

140,000clients

1,462employees

24sales

100agents

Most influential financial and

insurance company in social media

1

6CESCE’S ACtivity REpoRt 2016

FROFILE OF CESCE LEttER BUSiNESS LiNES CESCE iN 2016

Credit insurance,consultancy and surety

solutions

Spanish ExportCredit

Agency (ECA)

Information andservices

Argentina

DBK Informa

Experian

Logalty

Spain

Portugal

Colombia

Informa D&B CTIBrazil

Chile

Spain

France

Portugal

Colombia

Mexico

Peru

Venezuela(*) In credit and sureties

10countries

1. CESCE

2. CESCE France

3. CESCE Portugal

4. CESCE Argentina

5. CESCE Brazil

6. CESCE Chile

7. SEGUREXPO Colombia

8. CESCEMEX Mexico

9. SECREX Peru

10. LA MUNDIAL Venezuela

8

7 10

5

32

9

64

O n t h e l a r g e s c a l e

Commercial, financial and marketing information on

companies and entrepreneurs.

Comprehensive credit management services,

technological solutions and business process outsourcing.

Integrated services to help companies grow in every

phase of the business cycle.

Management of coverage on behalf of the Spanish state of the

commercial, political and extraordinary risks related to the

globalisation of Spanish companies.

S t r u c t u r e

4thgroup

worldwide*

2ndin

Spain*

P r e s e n c e i nE u r o p e a n d L a t i n A m e r i c a

1.13million

credit limitsin force

140,000clients

1,462employees

24sales

100agents

Most influential financial and

insurance company in social media

1

7CESCE’S ACtivity REpoRt 2016

FROFILE OF CESCE LEttER BUSiNESS LiNES CESCE iN 2016

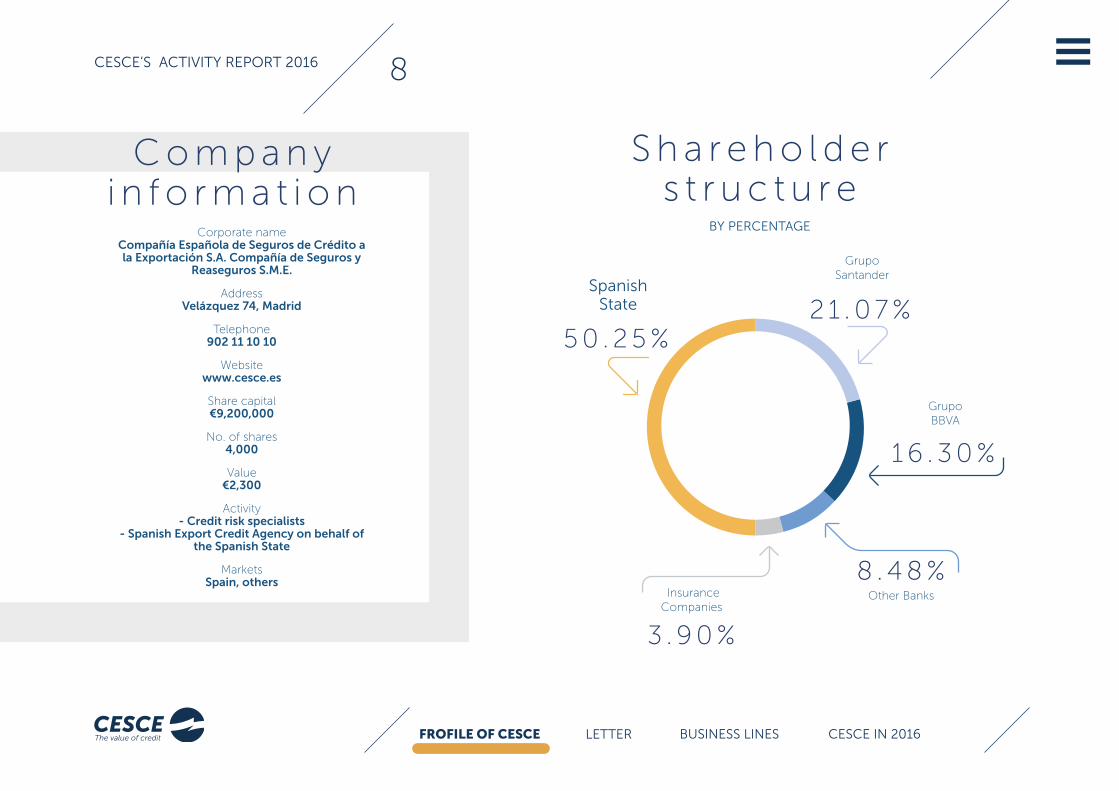

GrupoSantander

GrupoBBVA

Other Banks InsuranceCompanies

SpanishState

BY PERCENTAGE

3 . 9 0 %

1 6 . 3 0 %

8 . 4 8 %

2 1 . 0 7 %5 0 . 2 5 %

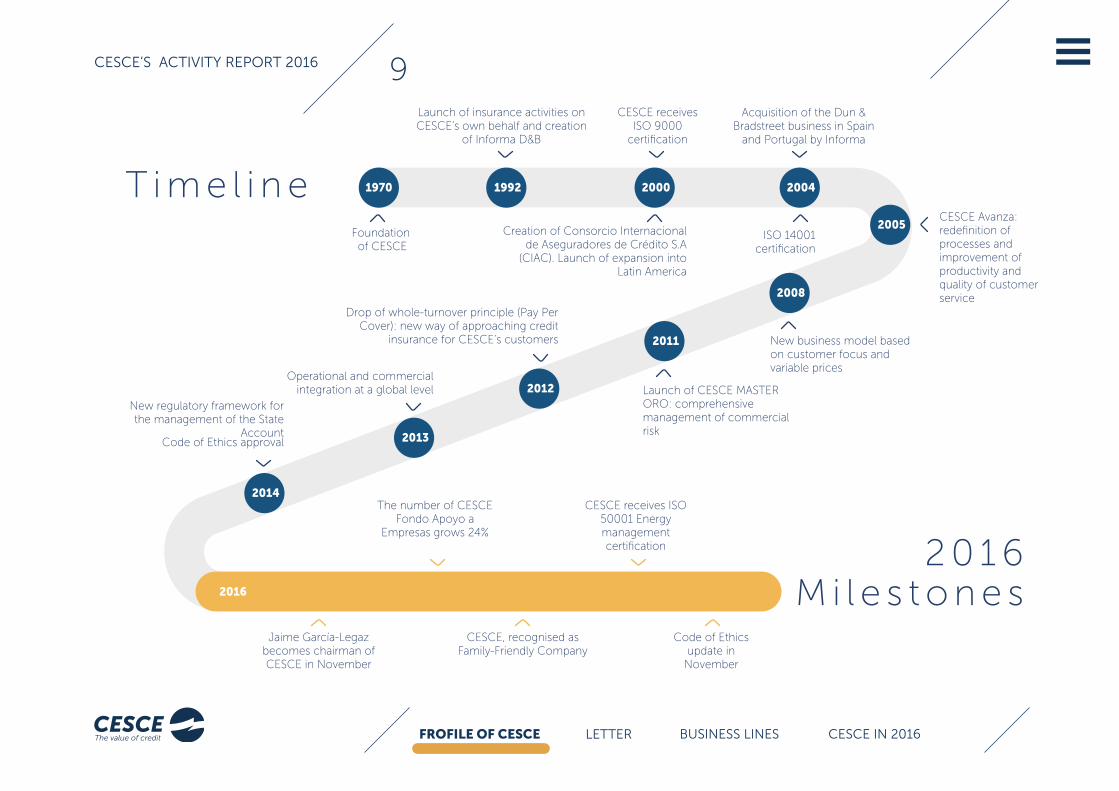

Foundation of CESCE

1970 1992 2000 2004

2005

2008

2011

2012

2013

2014

Launch of insurance activities on CESCE’s own behalf and creation

of Informa D&B

Acquisition of the Dun & Bradstreet business in Spain

and Portugal by Informa

CESCE receives ISO 9000

certification

ISO 14001certification

New business model based on customer focus and variable prices

Launch of CESCE MASTER ORO: comprehensive management of commercial risk

Operational and commercial integration at a global level

Jaime García-Legaz becomes chairman of CESCE in November

The number of CESCE Fondo Apoyo a

Empresas grows 24%

CESCE, recognised as Family-Friendly Company

CESCE receives ISO 50001 Energy management certification

Drop of whole-turnover principle (Pay Per Cover): new way of approaching credit

insurance for CESCE’s customers

Creation of Consorcio Internacional de Aseguradores de Crédito S.A

(CIAC). Launch of expansion into Latin America

CESCE Avanza: redefinition of processes and improvement of productivity and quality of customer service

2016

C o m p a n yi n f o r m a t i o n

S h a r e h o l d e rs t r u c t u r e T i m e l i n e

2 0 1 6M i l e s t o n e s

Code of Ethics update in

November

Code of Ethics approval

New regulatory framework for the management of the State

Account

Corporate nameCompañía Española de Seguros de Crédito a la Exportación S.A. Compañía de Seguros y

Reaseguros S.M.E.

AddressVelázquez 74, Madrid

Telephone902 11 10 10

Websitewww.cesce.es

Share capital€9,200,000

No. of shares4,000

Value€2,300

Activity - Credit risk specialists

- Spanish Export Credit Agency on behalf of the Spanish State

MarketsSpain, others

8CESCE’S ACtivity REpoRt 2016

FROFILE OF CESCE LEttER BUSiNESS LiNES CESCE iN 2016

GrupoSantander

GrupoBBVA

Other Banks InsuranceCompanies

SpanishState

BY PERCENTAGE

3 . 9 0 %

1 6 . 3 0 %

8 . 4 8 %

2 1 . 0 7 %5 0 . 2 5 %

Foundation of CESCE

1970 1992 2000 2004

2005

2008

2011

2012

2013

2014

Launch of insurance activities on CESCE’s own behalf and creation

of Informa D&B

Acquisition of the Dun & Bradstreet business in Spain

and Portugal by Informa

CESCE receives ISO 9000

certification

ISO 14001certification

New business model based on customer focus and variable prices

Launch of CESCE MASTER ORO: comprehensive management of commercial risk

Operational and commercial integration at a global level

Jaime García-Legaz becomes chairman of CESCE in November

The number of CESCE Fondo Apoyo a

Empresas grows 24%

CESCE, recognised as Family-Friendly Company

CESCE receives ISO 50001 Energy management certification

Drop of whole-turnover principle (Pay Per Cover): new way of approaching credit

insurance for CESCE’s customers

Creation of Consorcio Internacional de Aseguradores de Crédito S.A

(CIAC). Launch of expansion into Latin America

CESCE Avanza: redefinition of processes and improvement of productivity and quality of customer service

2016

C o m p a n yi n f o r m a t i o n

S h a r e h o l d e rs t r u c t u r e T i m e l i n e

2 0 1 6M i l e s t o n e s

Code of Ethics update in

November

Code of Ethics approval

New regulatory framework for the management of the State

Account

Corporate nameCompañía Española de Seguros de Crédito a la Exportación S.A. Compañía de Seguros y

Reaseguros S.M.E.

AddressVelázquez 74, Madrid

Telephone902 11 10 10

Websitewww.cesce.es

Share capital€9,200,000

No. of shares4,000

Value€2,300

Activity - Credit risk specialists

- Spanish Export Credit Agency on behalf of the Spanish State

MarketsSpain, others

9CESCE’S ACtivity REpoRt 2016

FROFILE OF CESCE LEttER BUSiNESS LiNES CESCE iN 2016

BY PERCENTAGEAND IN MILLIONS OF EUROS

IN MILLIONS OF €

20152014

IN MILLIONS OF €

20152014

IN MILLIONS OF €

20152014

BY PERCENTAGE

2015

2016 2016

2016 20162014

Insurance issuedon own behalf

Insurance issuedon behalf of the State

I n s u r a n c ei s s u e d

F i n a n c i a li n d i c a t o r s 50.4

T e c h n i c a lr e s u l t s

55.8

P r e -t a x

r e s u l t s

N e te q u i t y

C l a i m sr a t e

28%

399.4

25.7

39.2

75.6%410.9

19.5

31.6

32.9%

404.9

9 3 %€ 2 8 , 1 8 4 M

7 %€ 2 , 0 8 3 M

10CESCE’S ACtivity REpoRt 2016

FROFILE OF CESCE LEttER BUSiNESS LiNES CESCE iN 2016

BY PERCENTAGEAND IN MILLIONS OF EUROS

IN MILLIONS OF €

20152014

IN MILLIONS OF €

20152014

IN MILLIONS OF €

20152014

BY PERCENTAGE

2015

2016 2016

2016 20162014

Insurance issuedon own behalf

Insurance issuedon behalf of the State

I n s u r a n c ei s s u e d

F i n a n c i a li n d i c a t o r s 50.4

T e c h n i c a lr e s u l t s

55.8

P r e -t a x

r e s u l t s

N e te q u i t y

C l a i m sr a t e

28%

399.4

25.7

39.2

75.6%410.9

19.5

31.6

32.9%

404.9

9 3 %€ 2 8 , 1 8 4 M

7 %€ 2 , 0 8 3 M

11CESCE’S ACtivity REpoRt 2016

FROFILE OF CESCE LEttER BUSiNESS LiNES CESCE iN 2016

L e t t e r o f t h e c h a i r m a n

2

1212CESCE’S ACtivity REpoRt 2016

CESCE has fu l ly adapted to the new leg is la t ion on internat iona l i sat ion r i sks coverage on beha l f of the S tate”

“

Dear Friends,

It is a great pleasure to present you this year’s Annual Report. It provides an account of the company’s financial growth and its progress on Corporate Social Responsibility in 2016.

During this financial year, we completed the separation of the company’s public and private activities, strengthening CESCE’s work as an Export Credit Insurance Management Agency (ECA) on behalf of the Spanish State and making its private activity of consultancy, surety and credit insurance and solutions services completely independent, as well its information and business services subsidiaries.

CESCE has fully adapted to the new legislation on internationalisation risks coverage on behalf of the State passed in 2014, giving a new boost to activity on behalf of the State and opening new risk coverage markets.

As a private insurer, CESCE has increased its commercial offer, incorporating financial support tools for the companies, regardless

of if they are credit insurance customers or not. CESCE Fondo Apoyo a Empresas grants business financing through factoring (without recourse), in domestic and export sales. This non-banking financing is provided at very competitive conditions, through a fully automated procedure, that allows our customers to receive the funds in their account in approximately 1.8 days since the request.

CESCE has redefined its customer relationship by developing its Customer Experience strategy, which involves going beyond satisfaction to provide a global, positive and differentiated experience. This strategy has been consolidated in 2016 and all areas of the company focus on customer management. Based on the idea that customer loyalty is closely related to the quality of service, CESCE has doubled its efforts to establish lines of communication through various channels in a consistent and coordinated manner.

In this light, the company consolidated its commercial offer on insurance services and solutions with the products CESCE MASTER

13CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LETTER BUSiNESS LiNES CESCE iN 2016

ORO and CESCE Classic, aimed to customers that exclusively request credit insurance coverage.

Moreover, the company has continued to expand the Pay Per Cover solution, the only flexible solution in the market that allows customised coverage of the specific risks that the customer wishes to insure, as well as the use of the CESCE’s risk systems without a credit insurance contract, through Risk Management.

During 2016, it has also reinforced its consultancy services, CESCE Consulting, customised services for each company, with tools that include risk and recoveries management, incorporate financial information from Informa D&B, and connect to its customers’ credit solutions.

Lastly, CESCE has consolidated its financing solutions with financial institutions by issuing Insurance Certificates and Liquidity Titles.

The tools provided by CESCE

Today, CESCE provides unique financing and commercial credit management tools to the market. These tools help its more than 140,000 customers in all stages of the business cycle and, in just a few years, they have positioned CESCE in fourth place globally in credit insurance. CESCE’s portfolio is diverse, in size and activity, as well as multinational.

Customers access these different tools via a multi-channel commercial system. Using the CESNET platform, customers can manage their risk portfolios over the internet from anywhere in the world from any device, while benefiting from the direct personal channels provided by CESCE: the telephone helpline and the company’s 24 sales offices and 100 agents dispersed throughout Europe and Latin America.

Within the information and services area, Informa D&B has consolidated its leadership in the provision of sectorial information, while the subsidiary CTI has maintained its business model focused on the outsourcing of BPO business processes.

CESCE applies the best international practices for the analysis, measurement and management of commercial risk. In recent years, CESCE has progressed significantly on the control, monitoring and measurement of its risks, as well as the creation of contingency plans for all the types, in order to meet the standards set by the European Union in the Solvency II Directive and the Delegated Regulation supplementing it.

Regarding corporate responsibility, CESCE has moved forward with its commitment with the 10 Principles of the Global Compact,

The company consol idated i t s commerc ia l of fer on insurance serv ices and so lut ions”

“

14CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LETTER BUSiNESS LiNES CESCE iN 2016

initiative of which it is a member since 2015 and whose ultimate goal is promoting ethical business management. Being a member gets us more actively involved in achieving the goals of the Global Compact.

Additionally, in its activity on behalf of the State, CESCE works actively to eradicate corruption in all its forms, including extortion. In line with the OECD’s Anti-Bribery Convention, CESCE’s Anti-Corruption Policy is applicable to any type of coverage granted on behalf of the State.

Consolidation of profits

CESCE S.A. closed the financial year with €25.4 million in profits after taxes, in the context of the economic recovery in Spain and the Eurozone and with fierce competition in the sector. Profit before taxes was €31.6 million, while the technical result was €19.5 million.

In 2016, domestic business (i.e., commercial operations in Spain) represented 58% of the total business of the company and foreign business (i.e., transactions with foreign companies), 42%.

Examples of the company’s fine performance include the combined direct insurance ratio, which at 87% remained for the seventh year running below the 95% target threshold; the frequent claims ratio, which remained stable; and the growth of the number of current policies by 6.5%, thanks to a sustained sales effort from CESCE. In 2016, CESCE did not register any claim of a significant amount that generated the application of the foreseen stop-loss insurance coverage, provided by the reinsurance ceded.

The development of risk prediction models and tools also enabled CESCE to consolidate its financial solvency: on 31 December,

CESCE’s net equity was €404.9 million compared to €410.9 million on the previous year. CESCE complies fully with the solvency capital required (SCR) by current EU legislation. At the same time, the capital gains accrued in CESCE’s financial assets portfolio amounts to €52.5 million. Of this amount, €37.6 million pertained to equity in non-CESCE group and non-affiliate companies and €14.9 million pertained to debt securities.

Of the total of premiums earned from direct insurance, that fell 7.6% resulting in €113 million, 27% corresponded to export credits, 62% to domestic credit insurance, 6% to premiums sold in the French and Portuguese branches and the other 5% to sureties.

Therefore, the premiums linked to export risk amounted to €31 million (-8%); domestic credit premiums, €70 million (-6%); direct insurance policies taken out in European branches, €7 million; and premiums earned from sureties, €5 million.

Direct insurance earned premiums (those earned after the corresponding accruals) added up to €111 million, a reduction of 11% on the previous year.

The premium decline happened in the general context of a reduction of the commercial insurance policy prices, where the company has increased its policy portfolio by 6.5%, thanks to its commercial strategy, based on increasing its knowledge about its customers to provide solutions to their problems throughout the business cycle.

With these parameters, CESCE has once again proven the stability of its business model based on intensive use of information and data analysis. This model does not see customers solely as potential

15CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LETTER BUSiNESS LiNES CESCE iN 2016

victims of risks, but rather as drivers of the economy and employment. CESCE’s job is to protect these customers against possible default situations and help them grow. In addition to supporting companies, CESCE is still working on creating positive experiences for its different channels (sales network, telephone helplines and online CESNET platform). It also continues boosting its support to entrepreneurs via various training activities, publishing reports, writing the blog “Asesores de Pymes” and establishing intense conversations on social media.

State account

The maintenance of the strong drive of foreign trade during this last year has allowed to maintain our activities, which have recovered from the drop registered during the crisis resolution, and to successfully combine the difficult missions of providing free market services and acting as last resort insurer, as well as keeping the instrument’s financial equilibrium.

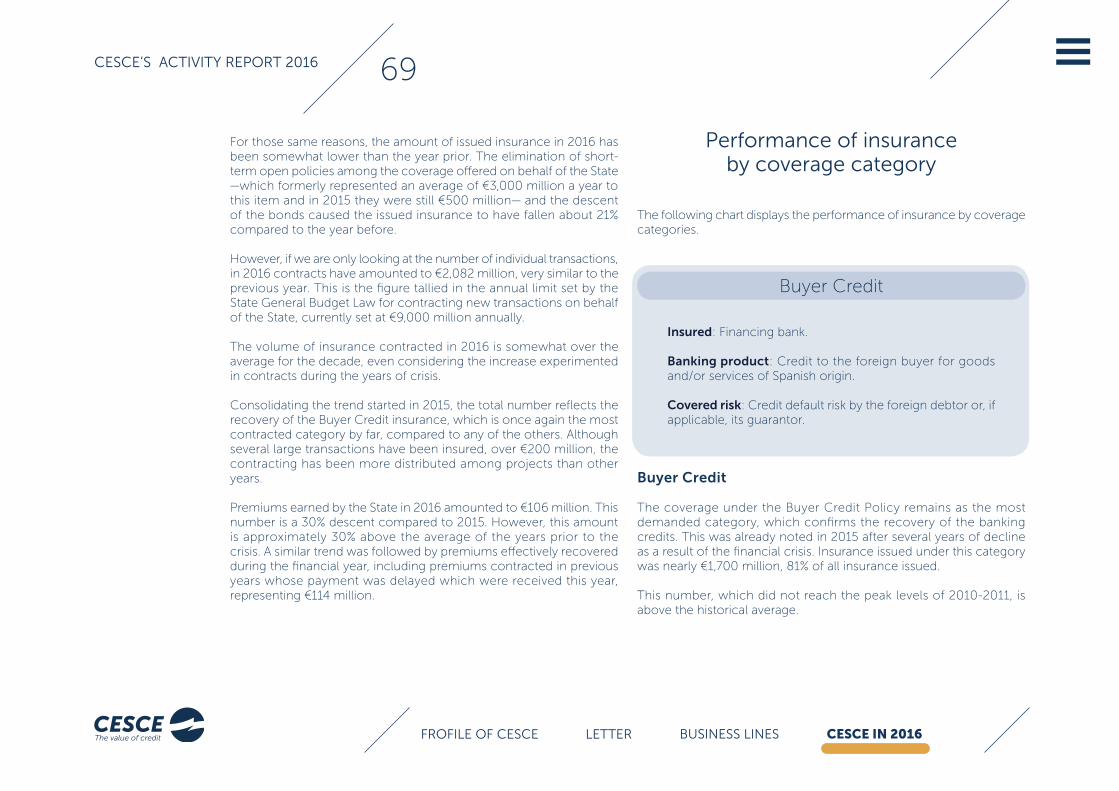

The volume of insurance policies issued on behalf of the State in 2016 is similar to that of 2015. The most requested policy was the Buyer Credit, with an approximate volume of €1,700 million over the about €2,000 million of insurance issued. This policy grew strongly compared to prior years. Following this policy are the Supplier Credit Policy (€176 million) and the Surety Insurance (€58 million).

The demand of these last two products, that was highest during the years of crisis, decreased significantly in 2016 as a result of the economic recovery, to the benefit of the Buyer Credit.

SMEs continue to be a priority for CESCE as proven by the different activities on behalf of the State as well as of the company. It is also worth mentioning the participation of CESCE in flagship projects of its multinationals, such as the Panama Canal Expansion or the Makkah-Medina high speed railway in Saudi Arabia.

Innovation and environment

During 2016, CESCE continued to focus on its RDI strategy, clearly supporting innovation and continuous improvement of the technology used. The projects initiated during the financial year have been fundamentally customer-focused, including the development of information tools designed to improve commercial decision-making, as well as new products aimed at meeting market needs. CESCE also continued to pay special attention to the optimisation of internal processes in order to ensure cost savings and improved efficiency. This work was rewarded with tax deductions, as some of the investments made have been recognised as technological innovations.

The vo lume of insurance pol ic ies i ssued on beha l f of the S tate in 2016 i s s imi la r to that of 2015”

“

16CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LETTER BUSiNESS LiNES CESCE iN 2016

In the last year, CESCE also introduced improvements in Ecocheck with the purpose of increasing the quality of the information of transactions in study, gathering a more comprehensive knowledge on the projects that could benefit from our coverage. With this leverage, technical and procedural changes were also introduced oriented to improving customer experience when using the tool.

In 2016, CESCE advanced in its commitment to environment, the “energy” that drives us to improve. We applied for the ISO 50001 Energy Management Certification, which was obtained at the beginning of December 2016.

With this boost, CESCE also applied for the certification BREEAM “In-Use Part 2” (non-domestic use buildings), that certifies the building management level in all its aspects, including environmental, but also others related to maintenance, well-being, etc. The BREEAM certification was received on 23 March 2017.

Strategic Plan

During 2016, we strove to balance our business targets with the expectations of our customers and suppliers as well as the wider community. We are dedicated to our shareholders and, despite being a public company, our mission is to be as profitable as possible in any of the possible and future scenarios. We expect great challenges in the future, both in our activity as a Risk Managing Agent on behalf of the State and our activity as an insurer on our own behalf. CESCE can and must grow, also, in Latin America.

The Board of Directors recognises the talent in CESCE and it has therefore decided to create a Strategic Plan. The company needs a

new impulse and, thus, a new growth strategy has been created. We must not fear change: “Fear of change is the death of a company” and this includes the digital challenge, which will involve deep changes in our customer focus. It requires the commitment of all of us, of the management, of each and every one of the employees in our organisation and the loyal cooperation of our suppliers. To all of you, I express my most sincere thanks..

JaImE GarCía-LEGaz PONCE Chairman of CESCE

17CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LETTER BUSiNESS LiNES CESCE iN 2016

P r i n c i p l e s o ft h e c o m m e r c i a l p r o p o s a l

T h e c e n t r a l e l e m e n t o f r i s ki s t h e d e b t o r , n o t t h e c u s t o m e r

The bas ic un i t of the r i sk i s not the insured , but ra ther the insured ’s debtor . Hence, CESCE ana lyses the r i sk of

each debtor and he lps i t s customers re ta in the best and protect themselves aga inst the worst .

V a r i a b l e p r i c e s a n dc o v e r a g e

The customer i s not requ i red to insure i t s ent i re debtor por t fo l io , i t on ly has to dec ide the leve l o f coverage i t

wants to take out a t any g iven moment .

C r e d i t i n s u r a n c e d o e sn o t d e p e n d o n t h e c y c l e

Pr ices a re set on the bas i s o f the fu ture es t imated cost o f acc idents us ing pred ic t ion mechan isms , regard less of

the resu l t s o f prev ious financ ia l years .

B u s i n e s s l i n e s

3CONSULTANCY, SURETY AND CREDIT INSURANCE AND SOLUTIONS

3 . 1 P 1 9

EXPORT CREDITAGENCY (ECA)

3 . 2P 3 6

INFORMATION AND SERVICES3 . 3 P 4 9

Business model3.1.1 P 2 0

Foreign sector support in 20163.2.1 P 3 7

Commercial offer of insurance and financing3.1.2 P 3 0

The many faces of CESCE’s activities3.2.1 P 4 1

Surety3.1.3 P 3 4

1818CESCE’S ACtivity REpoRt 2016

P r i n c i p l e s o ft h e c o m m e r c i a l p r o p o s a l

T h e c e n t r a l e l e m e n t o f r i s ki s t h e d e b t o r , n o t t h e c u s t o m e r

The bas ic un i t of the r i sk i s not the insured , but ra ther the insured ’s debtor . Hence, CESCE ana lyses the r i sk of

each debtor and he lps i t s customers re ta in the best and protect themselves aga inst the worst .

V a r i a b l e p r i c e s a n dc o v e r a g e

The customer i s not requ i red to insure i t s ent i re debtor por t fo l io , i t on ly has to dec ide the leve l o f coverage i t

wants to take out a t any g iven moment .

C r e d i t i n s u r a n c e d o e sn o t d e p e n d o n t h e c y c l e

Pr ices a re set on the bas i s o f the fu ture es t imated cost o f acc idents us ing pred ic t ion mechan isms , regard less of

the resu l t s o f prev ious financ ia l years .

C o n s u l t a n c y , s u r e t y a n d c r e d i t i n s u r a n c e a n d s o l u t i o n s

3.1

CESCE boosts the growth of companies w i th in tegrated and f lex ib le commerc ia l insurance , sure ty and consu l tancy so lu t ions that make bus iness processes eas ie r : cus tomer search , r i sk management and coverage , access to f inanc ing , and consu l tancy.

19CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

3.1.1

Business model

CESCE has a differential business model, which breaks traditional credit insurance schemes to offer integrated and flexible solutions for commercial insurance, consultancy and sureties with intensive use of information and automated data analysis.

Based on the premise that it is the customer’s debtor rather than the customer who is responsible for any claims, CESCE focuses its activity

on shielding companies against bad customers and helping them find and keep good customers.

With this logic, CESCE sets variable coverage prices depending on the payment history of each of its customer’s debtors and it offers customers the opportunity of deciding which transactions they deem most critical, without the need to cover the entire portfolio.

Premiums are set based of the estimated future cost of claims regardless of the results of previous financial years.

From those general principles, CESCE builds its business model on five cornerstones: customer focus, technological leadership, operational excellence, international outlook and financial stability.

CUSTOMER FOCUS

TEChNOLOGICAL LEADERShIP

OPERATIONAL ExCELLENCE

INTERNATIONAL OUTLOOk

FINANCIAL STABILITy

Business model cornerstones

20CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

CESCE is committed to customer service. All its activities are oriented to facilitating their main business processes (seeking and monitoring customers, internationalisation and financing) and to protect them against default.

This strategy is supported by the analytical, digital and predictive knowledge of customers. To understand what they need at each moment and foresee their future requirements, CESCE has a sophisticated Customer Relationship Management (CRM) tool, which records all the customer information and defines action guidelines based on their needs, the significance a specific situation has for that customer and the customer’s level of satisfaction with the company.

Constantly evolving, CESCE updated its CRM platform in 2016 to include the functionalities of the new services and the specific features of the customers that contract them. In addition, it boosted the customer active listening programme (VOC), to know the customers’ evaluation first hand, to identify improvement lines and to anticipate possible problems related to the customers.

CUSTOMER FOCUS

21CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

multi-channel experience

Beyond simply satisfying customer needs, CESCE offers them positive and distinctive experiences, pursuant to its Customer Experience strategy, which involves all the areas of the company.

Aware of the importance of maintaining an open channel with its clients in a global and digitised environment, the company boosts a multi-channel experience, where the customer has the same experience regardless of the media and they can start a transaction in one channel or media and finish it in another one.

CESCE’s customers can access the full solution portfolio via three channels: the sales network, the telephone helplines and the CESNET digital platform.

• Sales network:

The personal contact of the 100 agents and the 24 sales offices of CESCE plays a fundamental role in the creation of positive experiences. Added to the team’s experience is the knowledge provided by the CRM tool, that allows them to anticipate the needs of the customers and provide the appropriate situation in each moment.

• Telephone helplines

The Customer Service Centre has a team trained to quickly answer the customers’ requests and, if necessary, redirect the call to the business area experts.

In 2016, the CSC solved 117,984 queries in Europe and Latin America, 82% more than in 2015. 95% of requests were resolved within 24 hours and the rate of complaints was only 0.17%.

M u l t i - c h a n n e l c o m m e r c i a ls t r a t e g y

T h r e e c h a n n e l s , o n e e x p e r i e n c e

P e r s o n a l s e r v i c e

E x p e r i e n c e + C M R

1 1 7 , 9 8 4 q u e r i e s

A g i l i t y a n d c o n v e n i e n c e

9 0 % o f t r a n s a c t i o n s

R i s k M a n a g e m e n t

P o t e n t i a l c u s t o m e r s e a r c h

P o r t f o l i o m o n i t o r i n g

A c c e s s t o fi n a n c i n g

S a l e s n e t w o r k

T e l e p h o n e h e l p l i n e s

C E S N E T p l a t f o r m

22CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

• CESNET platform

The CESNET operating platform channels more than 90% of transactions. From this

digital channel, CESCE offers solutions covering all business stages: customers can manage their

risks and follow up on their policies; and they can access the financing and potential customer search

services, as well as the portfolio monitoring services.

Flexibility is one of CESNET’s main features. Customers may configure the platform to receive alerts on any device or ensure

the system automatically applies their policies, if they wish to. The system also allows the customer to transfer all the information they need to manage their risks to their own computer.

Attracting new customers

CESCE uses the most advanced marketing strategies to attract new clients. If in prior years the strategy was focused on contacting potential customers using its online tools, in 2016 CESCE has concentrated its efforts in attracting the best ones, segmenting and cultivating those that are most likely to hire its services. As a result, conversion ratios have improved and the cost of the campaigns has been reduced, in the framework of a strategy automating all stages of the marketing process.

The CESNET operat ing p lat form channels more than 90% of t ransact ions”

“

23CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

CESCE is intelligence applied to commercial risk management. Since 2008, the company has created a digital innovation and transformation strategy to understand and cover the needs of its customers. This has been done following three principles:

1. To turn the analytic knowledge of the customers into a strategic asset.

2. To create a flexible technological architecture by exploiting the elasticity of cloud provisioning.

3. To know how to apply knowledge and adapt to the digital reality that surrounds it, which requires the firm will of the members of CESCE.

In 2016, this strategy was translated in a €5.9 million RDI investment.

TEChNOLOGICAL LEADERShIP

8

7

6

5

4

3

2

1

0

2012 2013 2014 20152010 2011

IN MILLIONS OF EUROS

3.34

6.84

4.56

7.00

2.46

3.61

5.90

2016

Evo lu t ion o f i nves tment in RDI

24CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

Analytic knowledge

The key processes of the company are not only automated, but also designed to incorporate cognitive capacities.

The information is integrated throughout the supply chain via an automated connection. This allows to process millions of pieces of data on thousands of companies stored in multiple information sources in order to predict default risk, control claims, evaluate credit lines, analyse portfolio quality and orient in the search for potential customers.

This system is fed by different sources: data provided by the customers; information on sectors and countries prepared by the team of analysts; and prediction models and databases from CESCE’s subsidiary Informa D&B providing information on over 240 million companies in almost 200 countries worldwide.

The cooperation and bidirectional information exchange with partners, customers and employees via intelligent use of social media enables the access points, combining classic environments (agents, offices) and digital access.

Technological provisioning

CESCE uses technology as a facilitator of its innovative strategy.

The company leverages technological provisioning in the cloud because it allows for the speedy implementation of new innovative projects and represents a significant savings in operational and investment costs, as it provides cutting-edge technology under the pay-per-use formula. In this line, CESCE has entered into strategic alliances with technological market leaders such as IBM, Google and Salesforce.

As a result of the agreement with IBM, the Innovation Observatory was born. Among the other features, it continuously analyses the application of digital capabilities to CESCE’s strategy.

In 2016, the Innovation Observatory dedicated its efforts to defining a hybrid cloud technological architecture that will streamline the technological capacity provisioning, evidence of the application of Big Data technology to obtain information on Spanish companies.

The key processes of the company are automated and des igned to incorporate cogni t i ve capac i t ies ”

“

25CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

CESCE has a global and digital operational system based on the intensive use of information technology.

In a changing digital environment, the company’s key processes are modelled and automated to optimise them and to reduce costs. Thus, 90% of coverage decisions and 80% of claims payments are done automatically. This process benefits both CESCE and its customers: the company improves its efficiency and reduces its costs, while the customers experience shorter wait times and indemnitites being paid more quickly.

Digitisation of front office services

The insurer has also developed several initiatives designed to digitise front office services, such as digital marketing (360° customer vision, social and mobile marketing), customer experience (design of the customer experience, behavioural patterns, application of strategies), and distribution and sales channels (agent mobility, social media channels, innovation in products and services).

OPERATIONAL ExCELLENCE

Surety platform

CESCE has implemented, initially in Colombia, an online platform to immediately answer (price and issue of bond or guarantee) its customers’ requests on the different types of guarantees, especially from brokers. The platform is already available for those brokers that request it.

Bank and non-bank financing

Within the company’s services, bank and non-bank financing services deserve special consideration. Starting from an insured invoice, the access to financing is quick and easy.

Customer experience

CESCE has designed a programme to promptly inform its customers, via its commercial network, of the relevant events (exclude non-payments from coverage, cancel coverage of certain risk limits, communicate the right to low claims bonuses, etc.). This programme is constantly growing and being reviewed, to provide better customer service.

26CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

CESCE’s business model is based on its great analytical ability to transform data into knowledge and, therefore, data is a valuable asset for the company.

Protecting information is a priority within its technological strategy. In a world that is more and more globalised, where physical boundaries are diluted in cyberspace, CESCE has opted for incorporating cybersecurity as a fundamental design element in Technological Architecture.

The cybersecurity focus is oriented to a continuous analysis of the risks according to the Information Security Management System, pursuant to ISO/IEC 27001 standard, which sets a cycle for the continuous improvement of prediction, prevention, detection and answer of security incidents.

Cybersecurity at CESCE

27CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

CESCE is present in ten countries. In Europe, in addition to its head office in Spain, it has branches in France and Portugal. In Latin America, it has subsidiaries in the main markets: Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela.

CESCE’s presence in Latin America is channelled via the International Consortium of Credit Insurers (CIAC), in which CESCE has a majority shareholding (63.12%). The other shareholders in this joint venture are the insurance company Münchener Rück (15.04%), and the banks BBVA (10.92%) and Santander (10.92%).

Significant growth in credit

Fy2016 has been for CESCE a major step in its path to leading the Latin American market of insurance and solutions for commercial credit management.

Regarding credit, all the subsidiaries of the group achieved significant growth in business volume. CESCE was the international operator with greatest growth in the region. In an environment complicated

by economic difficulties in several countries, its client portfolio has increased more than 30%, while the aggregated volume of the premiums earned by Latin American subsidiaries has grown more than 90%.

In this context, the CESCE MASTER ORO system proved its efficiency in economic crisis scenarios, such as in Brazil.

Highlighted position in the surety branch

In the surety market, where the company has a prominent position with more than 4,000 current policies, the number of clients kept increasing, although the growth of premiums was more modest due to high competition in prices.

In its continuous improvement process, CESCE has enhanced its information systems in countries such as Peru and Chile, which has enabled the optimisation of the automatic portfolio evaluation and classification mechanisms. These mechanisms were already functional in Brazil, Colombia and Mexico.

Globally-integrated company

CESCE operates as a globally-integrated company. In 2016, it has perfected the corporate tools that enable process integration in all subsidiaries.

Likewise, it has continued developing new tools to manage its business lines. In that sense, it is worth highlighting the consolidation of the CRM platform for customer management.

INTERNATIONAL OUTLOOk

28CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

CESCE follows the best international practices for the analysis, measurement and management of commercial risk. Its ability to predict future risks, as well as the payments and recoveries scheduling method used to calculate them, make it so that, each year, the technical provisions for claims are sufficient to face the payments derived from the claims at a reasonable caution level.

In recent years, the company has made significant progress on the control, monitoring and measurement of its risks, as well as the creation of contingency plans for all the types, in order to meet the standards set by the European Union in the Solvency II Directive and the Delegated Regulation supplementing it.

This initiative took effect on 1 January 2016 after the Spanish Parliament approved Law 20/2015, of 14 July 2015, on the Regulation, Supervision and Solvency of Insurance and Reinsurance Companies (LOSSEAR) together with the Regulation on the Organisation, Supervision and Solvency of Insurance and Reinsurance Companies (Royal Decree 1060/2015, of 20 November), which incorporate the

European Directives into the legal framework and constitute the basic legal texts regulating the requirements of the new Solvency II regime.

The most remarkable innovations introduced by the new legislation include a new method of calculating solvency requirements, a reinforced governance system, the unification of information systems by institutions, a new supervision model offering the supervisor greater functions, a pre-authorisation system and the capacity to issue technical guides and notices.

CESCE complies fully with the solvency capital required (SCR) by current legislation in the EU.

rating strengthening

The company continued to generate trust in 2016. Standard & Poor’s (S&P) maintained CESCE’s rating of BBB+, with stable outlook during the Fy. The rating agency believes that CESCE, based on criteria manifesting its credibility in a sovereign stress scenario, has a satisfactory business risk profile and a strong financial risk profile.

In 2017, the agency confirmed CESCE’s rating, but improved its outlook, which went from “stable” to “positive”. In that sense, the agency indicates that after a significant shrinking of the business volume in the last six years, the improvement of the economic conditions in Spain in the four last years has had a positive impact on the insurer’s claims experience.

Standard & Poor’s has announced that it could increase the ratings of CESCE within the next 24 months, if it increases Spain’s rating and if the business crunch were less significant.

FINANCIAL STABILITy

29CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

Risk coverage

• Pay Per Cover: the customer chooses which of its customers to monitor so that later, if it so desires, it may cover the non-payment risk

• Full Cover: the customer insures its whole portfolio and the price of each transaction depends on the payment performance of the debtor

Market prospecting

Processes Technology Analysis

• Spain: Prospecta databases - 2 million companies

• Abroad: GRS Global - 250 million companies in 200 countries

• Country Risk: reports, fact sheets, macroeconomic tables,among others

RiskManagement

• Advanced mechanism to control risks based on statistical models using the internet and mobile phones

• Specialist consultants

Financing • CESCE Fondo Apoyo a Empresas

• Insurance Certificates

• Liquidity Titles

CESCE MASTER ORO P a y P e r C o v e r a n d F u l l C o v e r

CONSULTANCY

3.1.2

Commercial offer of consultancy services, and

insurance and credit solutions

CESCE provides a comprehensive answer to company needs. Its CESCE MASTER ORO solution allows customers to intelligently insure and control its commercial risks, as well as to search for new customers and receive financing.

This value proposal is completed with the consultancy services offered by CESCE Consulting and that contribute to the consistency of the business processes with the risk management systems.

CESCE MASTER ORO

Risk Management

Companies may monitor the payment performance of their customers through the Risk Management service. This portfolio analysis and monitoring system may be used to monitor the risks of the debtors

30CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

that the customer chooses in real time through the most appropriate device in each context via the CESNET digital platform.

This monitoring mechanism is based on statistical decision models that manage millions of data about thousands of companies, and it feeds on the experience of a team of 70 professionals in 10 countries with more than 40 years’ experience in the insurance sector.

The monitoring services offered by CESCE include Dun Trade, which enables customers to compare their companies’ real situation with the competition, the market and the sector, and hence to adjust collection and payment times. Among other benefits, the Dun Trade programme enables customers to ascertain how debtors are paying other suppliers providing their information to Dun Trade.

Risk coverage

CESCE MASTER ORO offers two risk coverage categories: Pay Per Cover and Full Cover.

• Pay Per Cover allows policyholders to decide which risks to transfer, with no obligation to cover their entire portfolio. The company monitors the full customer portfolio and can activate coverage, whenever it wishes, for those risks deemed most critical. In addition, CESCE recommends a customised risk transfer strategy to optimise budgets with a Customised Risk Transfer Report.

• Full Cover provides total protection to companies as it covers the risk of all the sales, offering them a coverage commitment related to their customers’ level of risk. The benefit compared to other companies lies in the fact that it offers different prices for debtors who perform differently.

The two solutions cover defaults of up to 95% of a company’s sales and compensation is paid within 60 days of the information about the claim being received.

In both categories, CESCE MASTER ORO integrates services tailored to the needs of each company, such as the identification of potential customers, the monitoring of customer portfolios and access to immediate financing.

In 2016, this flexible innovative solution attracted more than 500 new customers.

It is also possible to take out solely insurance coverage through the CESCE Classic policy.

The CESCE MASTER ORO proposa l i s completed wi th consu l tancy serv ices”

“

31CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

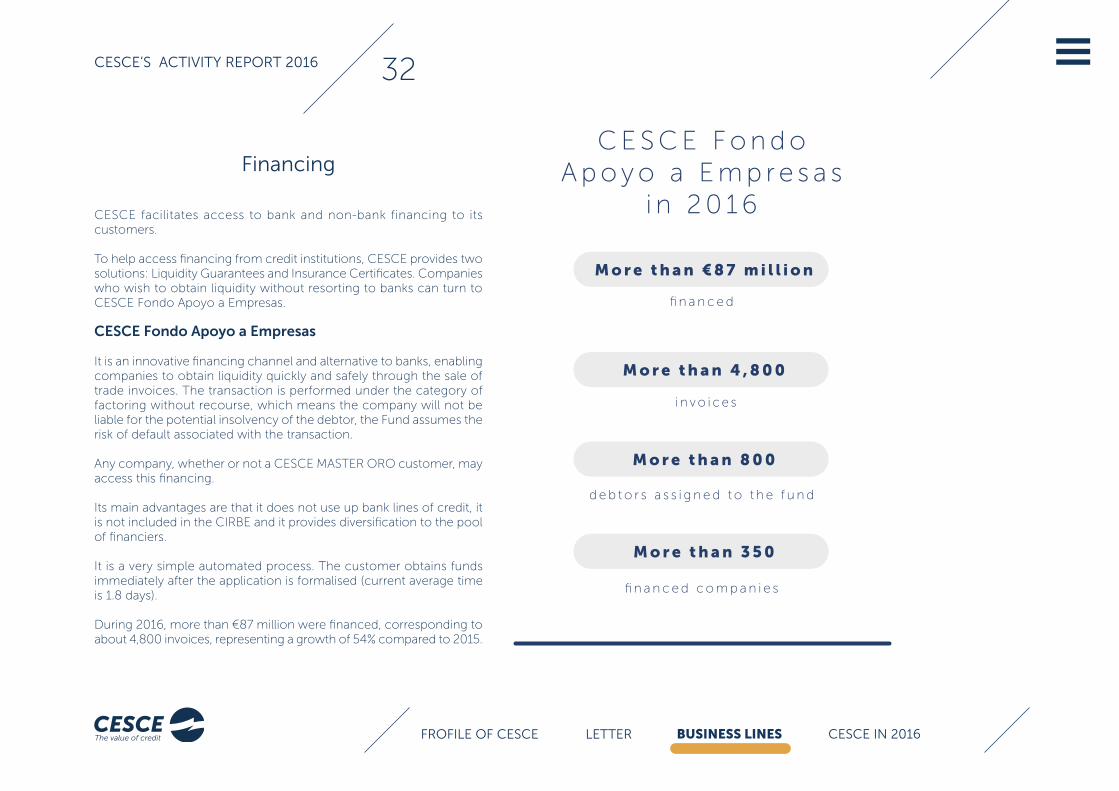

C E S C E F o n d oA p o y o a E m p r e s a s

i n 2 0 1 6

fi n a n c e d

M o r e t h a n € 8 7 m i l l i o n

M o r e t h a n 4 , 8 0 0

M o r e t h a n 8 0 0

M o r e t h a n 3 5 0

i n v o i c e s

d e b t o r s a s s i g n e d t o t h e f u n d

fi n a n c e d c o m p a n i e s

Financing

CESCE facilitates access to bank and non-bank financing to its customers.

To help access financing from credit institutions, CESCE provides two solutions: Liquidity Guarantees and Insurance Certificates. Companies who wish to obtain liquidity without resorting to banks can turn to CESCE Fondo Apoyo a Empresas.

CESCE Fondo apoyo a Empresas

It is an innovative financing channel and alternative to banks, enabling companies to obtain liquidity quickly and safely through the sale of trade invoices. The transaction is performed under the category of factoring without recourse, which means the company will not be liable for the potential insolvency of the debtor, the Fund assumes the risk of default associated with the transaction.

Any company, whether or not a CESCE MASTER ORO customer, may access this financing.

Its main advantages are that it does not use up bank lines of credit, it is not included in the CIRBE and it provides diversification to the pool of financiers.

It is a very simple automated process. The customer obtains funds immediately after the application is formalised (current average time is 1.8 days).

During 2016, more than €87 million were financed, corresponding to about 4,800 invoices, representing a growth of 54% compared to 2015.

32CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

The number of companies financed by the Fund grew by 24%, with 846 debtors transferred to the fund in 16 countries.

Factoring

CESCE also offers Póliza Factoring, which is specifically designed for financial institutions and collaboration agreements with different Spanish or Latin American financial institutions to facilitate the customers access to financing through the issue of guarantees.

In the context of factoring, CESCE is already a renowned entity, member of ASOFACTORING (Colombian Association of Factoring) and AEF (Spanish Association of Factoring) alongside the major banks.

The company keeps working both to consolidate its various factoring-oriented solutions and to create growth and economic/financial restructuring alternatives for companies.

Access to bank financing

CESCE MASTER ORO customers are provided with solutions facilitating access to bank financing and can benefit from the issue of Liquidity Titles and Insurance Certificates.

• Insurance Certificates are documents confirming the existence of cover for specific invoices under the insurance policy.

The Insurance Certificates issuing service enables customers to request certificates for invoices declared to the insurance expiring 25 days or more after the request, on credits issued to debtors living anywhere in the world; the company will simultaneously indicate the financial institution to be compensated in the event of default.

• Liquidity Titles are documents issued by CESCE for invoices covered by the insurance. These documents meet the criteria for constituting a CESCE personal guarantee in favour of Financial Institutions, as acknowledged by the Bank of Spain pursuant to the Basel II regulations.

CESCE issues Liquidity Titles or Insurance Certificates after validating the compliance of the insurance terms and conditions, as well as carrying out a technical and commercial verification of the trade credits for which CESCE’s customer wishes to obtain the indicated guarantee. To date, no other credit insurer performs such processes.

Through these two financing solutions, CESCE has issued more than €680 million worth of guarantees in favour of various financial institutions to help its customers get access to financing.

The f inanc ing of CESCE Fondo Apoyo a Empresas grew by 54%, up to €87 mi l l ion”

“

33CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

Market prospecting

CESCE supports companies in their search and selection of customers via the Market Prospecting service.

Customers get access to a list of 2 million Spanish companies along with an analysis and valuation of each company for coverage purposes based on Prospecta, the largest database in the market. CESCE offers customers who wish to expand internationally the GRS Global service, through which potential customers may be sought from over 250 million companies worldwide.

This information is supplemented by the Country Risk service, which offers a diagnosis of risks arising from trade and investment abroad including macroeconomic charts, Country Risk reports and documents on Spain.

Customers also have access to Prens@mail, a service monitoring the press and significant legal incidents segmented by company.

CONSULTANCy

CESCE Consulting provides companies with efficient tools and methods to control commercial credit risks, granting them the freedom to manage and control default, combining the company’s business processes efficiently with the risk management systems supporting it.

3.1.3

Surety

CESCE offers companies and people surety insurance, also called bonds, guarantees or compliance policies, depending on each country’s legislation. With this product, the company holds policyholders harmless against any claims made by different public authorities or from the private sector, regarding financial liabilities which may be incurred as a result of breaching their obligations arising from either a contract (construction works, supply or provision of services) or from a legal provision.

The main surety categories offered by CESCE in Spain and Latin America are:

• Public tenders (bid maintenance);

• Performance bonds;

• Advance payments, supplies;

• Labour obligations;

• Maintenance, quality of goods and services or stability of works and constructions;

• Customs obligations;

• Purchasing of advertising time on television;

• The Spanish Agricultural Guarantee Fund (FEGA).

34CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

the issued premiums, although more than 12,000 documents were issued. however, important growth is registered in the number of clients, since during 2016 1,755 new policyholders were added with a total of 4,266 current policies.

For 2017, the main challenge is to continue exploring the niche of smal and medium-sized sureties, with the implementation of the technological tool Sisnet, which already operates in Spain and Colombia, providing a high level of automation of the transactions thanks to the decision engine Mazinger.

In the functional sphere, the underwriting policies of all the subsidiaries were updated and unified. Regarding risk follow-up and standardisation, with a new appointed global manager, the risk profile was created, identifying those that could be followed up to prevent or foresee possible breaches from the policyholders. Steps were taken towards standardisation, which intends to avoid surety or bond execution.

During the fiscal year, the Global Surety Committee, integrated by the global managers of Sureties, Risks and Reinsurance and by the delegate of the Commercial Corporate Directorate, considered and approved more than one hundred transactions, which exceeded local attributions due to the amount or nature of the risk, for CESCE and its subsidiaries in Latin America.

At the end of 2016, the Global Reinsurance Unit led the process of reinsurance contracting for Latin America for 2017, with important

terms and conditions for the business, such as the special capacities for global surety customers, those that request

CESCE’s services from different subsidiaries.

For 2017, the main cha l lenge i s to cont inue exp lor ing the n iche of smal l and medium-s ized suret ies ”

“

In 2016, the surety branch was marked by the fierce competition to win business, which volume has been reduced.

In the Spanish market, CESCE held 8.33% of the market share, although total premiums decreased 10% compared to 2015. This decrease is less than that of other insurers. Surety customers in

Spain (1,295 in total) are mainly traditional companies with a vast experience in the business and transactions

guaranteed by CESCE.

In Latin America, the “war on rates” is stronger and has generated a

significant reduction of the premiums in the markets,

especially in Brazil and Colombia , which

led to CESCE’s subsidiaries to

reg is ter an increase of

b a r e l y 2% in

35CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

E x p o r t C r e d i t A g e n c y ( E C A ) 3.2

The management of the Expor t Cred i t Insurance i s ent rus ted to CESCE who exc lus ive ly manages , s ince i t s c reat ion a lmost 50 years ago, r i sk coverage on beha l f o f the S ta te . In th i s t ime, the nature of commerc ia l t ransact ions and f inanc ing s t ructures has dras t ica l l y evo lved . In 2016, CESCE cont inued to adapt i t s p roducts and procedures to meet the cur rent needs of the sector.

The Spanish export sector still shows great dynamism and continues to be one of the growth engines of the Spanish economy. To support this sector, the Spanish Administration offers companies embarking on commercial or business projects in foreign markets specific instruments designed to facilitate their work, among which Export Credit Insurance, managed by CESCE. With this instrument, the State offers tools to mitigate great part of the risks that arise during the different stages of the internationalisation process, through a wide array of insurance and guarantee categories.

36CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

3.2.1

Foreign sector support in 2016

2016 was a relatively good year for CESCE’s State Account. After several years of atypical activities, due to the record highs registered in the first years of the crisis as well as the sudden drop that came afterwards, 2015 meant a return to normal and in 2016 the contract-level has remained similar.

Regarding the distribution of new contracting among the types of insurance, we are returning to a more traditional model, headed by buyer credit, as the type of coverage with more contracts (81% of the total, compared to 34% in 2012). There is less focus on a single project this year, although as usual, the larger transactions represent an important part of new contracting, 50% of which went to four projects in Chile, Peru, Angola and Oman.

On the other hand, the amount of guarantee contracts has continued to fall as a result of CESCE’s lower participation in the risk, due to the smaller average amount and also a smaller number of transactions.

Evolution of the Berne Union

The positive trend of CESCE’s numbers contrasts with the figures registered by the Berne Union which, contrarily, show a slight descent of activity. As is known, the Berne Union gathers the main global export

credit and investment insurers, including the main ECAs. Its members, dispersed all around the world, insure or lend about US$2 trillion each year, or approximately 10% of the world trade.

In 2016, the ECAs of the Berne Union reported less global transactions than the year before. They explain the drop by the setback in the sectors related to hydrocarbons, the effects of the sanctions on several markets important for the ECAs, such as Russia or Iran, or the lesser activity of the main European agencies of the aeronautical sector. The overall figures also reflect the reduced activity of US Eximbank, still limited for political reasons.

The main destinations of the export credit awarded by the ECA group in the Berne Union in 2016 have been the US, Brazil, Turkey, Russia, Saudi Arabia and India. Additionally, claims have increased, with a great number of the defaults occurring in Spain, Ukraine, Russia and Iran. After several years of very low claim rates, several ECAs anticipate numbers to increase. As a counterpoint, prospects for recoveries are fine, especially for those negotiated by the Paris Club.

For the second year running, Beatriz Reguero, director of the State Account Area at CESCE, chaired the Medium- and Long-Term Committee of the Berne Union.

CDGaE (Government Economic affairs Committee)

In 2016, ten transactions have been subject to the approval mechanism for “exceptional” transactions, that require reporting to the CDGAE and the approval of the Secretary of State for Trade. This category includes, but is not limited to, large-scale transactions (credits of more than €400 million or more than €150 million if project finance or guarantees are involved), transactions with debtors already representing a significant burden of risk, or transactions in hIPC countries.

37CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

Logically the functioning of this procedure was altered in 2016 due

to the political impasse the country found itself in and which translated into

longer-than-usual response times.

Market trends

CESCE has issued the first guarantee over buyer credit for a transaction in Indonesia. With this product, it

offers the financing bank, in this case BBVA, an irrevocable guarantee payable upon first demand, covering 100% of the

credit and its interests, and CESCE assumes the documentary and legal risk of the transaction. The guaranteed transaction is of

moderate size and duration, and it stands out because it is the first time this relatively new product for CESCE is used.

We still receive queries regarding financing in local currency but they have not yet resulted in specific policies. Once more, CESCE wishes to remind customers that it can cover credits in local currency and not apply the crystallisation clause (i.e. the obligation to convert the outstanding balances of the debt to hard currency after a default).

2016 has been the year with record high issuing of letters of intent. CESCE has issued almost 60 letters, related to projects in many countries, among them, standing out due to the great number of requests, are Iran, Egypt and Argentina, countries in which there is a great interest, which will foreseeably come to fruition in the near future. Iran and Argentina, traditional destination of CESCE insurance, are countries in which coverage has been reopened, after years of suspension.

On the other hand, coverage with Cuba, restarted in 2014 for transactions with a maximum payment term of a year, had to be suspended in mid-2016 as a result of the non-payments registered

38CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

once the insured credit amounts started to expire. At this time, many of these defaults still exist and CESCE has had to indemnify; therefore, it is not expected to resume the coverage in the near future.

Although it is not news, it is worth mentioning the continuous interest of Spanish companies in two other traditional markets, Ecuador and Angola, where CESCE’s involvement has almost reached its peak. Indeed, in these two countries, demand greatly exceeds CESCE’s capacity. To increase capacity and be able to meet the excess demand, CESCE has decided to resort to the private reinsurance market.

Collaboration with the private reinsurance

CESCE’s decision to resort to private reinsurance is the result of the aim to free up capacity in those countries where the coverage limit has been reached, or is close to being reached, and the insurance demand by exporters is greater than those limits. It is also a mechanism that allows flexibility in the eligibility requirements for transactions where there is excess foreign stock, in accordance with the normal rules, thus allowing a greater involvement than what CESCE could assume without resorting to these structures.

The cooperation with private insurers allows transferring part of the new risks or part of the risks in the portfolio, limiting or reducing CESCE’s retained interest and, therefore, the ceiling usage.

When this report was written, CESCE was finalising the details on the transfer of several projects from the two countries mentioned, Angola and Ecuador, to private operators.

Among the ECAs around us, in the last years, these types of structures have become the normal practice. Until now, the experience with CESCE’s State Account in reinsurance schemes was limited to the cooperation between ECAs, under the framework of reciprocal facultative reinsurance agreements, which allowed to insure, via a one-stop scheme, financial structures for multisourcing projects, spreading the risks between the ECAs of the countries participating in the commercial structure.

Improvements to CESCE products

CESCE continues to review the general conditions of its main insurance policies. If 2015 was the year of revamping the Bond policy, now called Bonds Enforcement Risk Insurance for Issuers, in 2016 the efforts have concentrated on the Works Insurance and the Documentary Credits. As the great innovation of this last category, it is important to mention the inclusion of commercial risks among the risks covered within open policies as well as in individual ones. This means that, with private issuers of letters of credit, the coverage is no longer limited to political or catastrophic risks, but it also includes the default of the issuing bank.

On the other hand, the CDGAE recently approved the expansion of the Line for SMEs, passing a new tranche of €100 million. It is worth recalling that this Line does not only cover guaranteed transactions but also pre-financing or operating credits, which is expected to help facilitate exporting SMEs’ access to this type of financing.

CESCE cont inued rev iewing the genera l condi t ions of i t s main insurance pol ic ies in 2016”

“

39CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

In fact, the policy covering the liquidity financing or pre-financing, known as Bank Guarantees, is one of those being reviewed at this time. Within this category, CESCE covers the bank financing the default risk of a credit granted to an exporting company, provided that the contract financed is an export contract.

These last changes are framed in an action plan oriented to improve the products and services to small and medium-sized enterprises.

OECD Innovations

As is known, the Export Credit Insurance on behalf of the State is highly regulated, within our borders and outside of them. On an international level, the main applicable rule is the OECD Arrangement, establishing the conditions for the states to offer support for financing exports. The Arrangement regulates, among other aspects, the duration of credits, their interest rate and the price of the insurance policy. It is a

live agreement that the participating states try to continuously adapt to the market reality.

One of the agreed changes during 2016, after years of negotiating, has been the calculation method of the price that ECAs have to charge for the coverage of credit transactions granted to debtors or guarantors in category 0 countries, which comprises all the richest countries of the OECD. The new system will improve the conditions for debtors with better rating and increase the price for debtors with worse rating, especially in long-term credits. One of the great advantages of the agreement is that the system is transparent and predictable and, most important, equally applied to all.

Although CESCE does not cover many transactions in this market segment, in the past it has supported several large scope projects in those countries. On the other hand, it also affects the Spanish companies that receive credits with cover from foreign ECAs.

The CDGAE recent ly approved the expans ion of the L ine for SMEs , pass ing a new t ranche of €100 mi l l ion”

“

40CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

3.2.2

The many faces of CESCE’s activities

In this section, CESCE explains the activities it carries out as Export Credit Agency, by presenting a selection of projects where official support has contributed to the success of the global experience of Spanish businesses.

41CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

Const ruct ion and equ ipment of the hosp i ta l in Los Ce ibos , Guayaqui l - Ecuador

Puentes y Calzadas Infraestructuras S. L. U., in consortium with the public Chinese company Sinohydro, won a contract, signed at the end of 2015 with Instituto Ecuatoriano de la Seguridad Social. The object of the contract was building and equipping the hospital at Los Ceibos, in the city of Guayaquil, including preventative maintenance for 5 years of the medical equipment in the hospital complex.

The opportunity of participating in this important international project has been a great milestone in the international career of the Galician group Puentes y Calzadas, which already has 40 years of business experience.

CESCE participates in the transaction granting Buyer Credit coverage, which partially finances the transaction, granted by Deutsche Bank S. A. E., Banco Bilbao Vizcaya Argentaria S. A., Banco Santander S. A., Société Genéralé Sucursal en España and Banco Popular Español S. A. to the buyer from Ecuador and whose payment is guaranteed by the Republic of Ecuador.

Exporter Puentes y Calzadas Infraestructuras S. L. U.

Contractor Instituto Ecuatoriano de la Seguridad Social

Country Ecuador

Value of transaction US$200 million

Type of transaction Financing through Buyer Credit

Term of execution 14 months

Term of financing 7 years

Sector Construction

Date closed November 2016 (policy signature)

Financing banks/Insured

Financial syndicate formed by Deutsche Bank S. A. E., Banco Bilbao Vizcaya Argentaria S. A., Banco Santander S. A., Société Genéralé Sucursal en España and Banco Popular Español S. A.

Risks covered Credit coverage granted by the financial syndicate to the buyer to pay for the export transaction.

CESCE Insurance Type Buyer Credit Insurance Policy

42CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

F i rs t s tage of the adaptat ion to the new fue l spec i f icat ions of the re f inery in La pampi l la - peru

The execution of Stage I of the Project of the Refinery at La Pampilla started in 2010. The aim was to renovate the refinery and adapt it to the new environmental specifications in Peru, as well as to invest to increase the company’s profitability pursuant to its business plan. Thus, once the commitments that RELAPASAA had acquired with the Peruvian administration to comply with current legislation were met, the diesel units started operating in August last year.

The transaction had an investment of US$444.6 million and has had financing with coverage by CESCE for a value of US$252.5 million. The policy signed by the Insured Banks entered in force on 29 November 2016.

Exporter Repsol S. A.

Contractor Refinería La Pampilla S. A. A. (RELAPASAA)

Country Peru

Value of transaction US$444.6 million

Type of transaction Financing through Buyer Credit

Term of execution 6 years

Term of financing 10 years

Sector Oil & Gas

Date closed November 2016 (policy signature)

Financing banks/Insured

Financial syndicate formed by Banco Santander S. A. (Agent), Banco Bilbao Vizcaya Argentaria S. A., Banco Sabadell Miami, Credit Agricole Corporate & Investment Bank, Commerzbank AG, Sucursal en España and Intesa Sanpaolo S.p.A., Sucursal en España

Risks coveredCredit coverage granted by the financial syndicate to the buyer to pay for the export transaction.

CESCE Insurance Type Buyer Credit Insurance Policy

43CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

The joint venture formed by the Geological and Mining Institute of Spain, the National Laboratory of Energy and Geology of Portugal, and Impulso Industrial Alternativo S. A. signed a contract with the Geological Institute of Angola to carry out the “Geological and underground resource mapping for the south area of Angola on 476,512 km2” (37.5% of the total territory) within the National Geology Plan developed in the country, “PLANAGEO”.

It is a flagship project, with a total funding of US$400 million, with the aim of placing value on the geological resources of the country to find alternatives to oil production and favour the country’s development. It essentially implies the creation of geological, geochemical and geophysical maps of the different regions, as well as specific maps of concrete areas.

It is important to mention that the companies of this exporting JV have vast experience in carrying out this type of projects. They will develop the project with a good knowledge of the Angolan territory.

In this case, CESCE has supported the exporting company with buyer credit insurance granted by the financial syndicate of BBVA and Banco Santander, of which the Republic of Angola is debtor.

Exporter

Joint Venture: Geological and Mining Institute of Spain, National Laboratory of Energy and Geology of Portugal, and Impulso Industrial Alternativo S. A.

Contractor Geological Institute of Angola

Country Angola

Value of transaction US$115.31 million

Type of transaction Financing through Buyer Credit

Term of execution 60 months

Term of financing 7 years

Sector Geological and Mining Resources

Date closed June 2016 (policy signature)

Financing banks/Insured

Bank syndicate comprising Banco Bilbao Vizcaya Argentaria S. A. and Banco Santander S. A.

Risks coveredDefault risk of the credit granted by the financial syndicate for the export transaction payment.

CESCE Insurance Type Buyer Credit Insurance Policy

Geolog ica l and underground resource mapping for South Angola wi th in the nat iona l geology p lan p lanageo - Angola

44CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

Sa le of a t ra in ing sh ip of 110 metres in length - indones ia

Construcciones Navales P. Freire S. A. signed at the end of 2013 a contract with the Ministry of Defence of the Republic of Indonesia for the sale of a sail training ship of 110 metres in length, including spare parts, tools, training, building a pier at the destination and technical assistance, among others.

The designed vessel has a classical silhouette, resembling the training ship “Juan Sebastián Elcano”. It will have capacity for 200 people on board, barque-style and a sail area of 3,350 m2. Its main purpose will be training cadets for the Indonesian Navy.

C.N.P. Freire has vast experience in building vessels of many types, including towing, fishing, merchant, oceanographic and offshore. The entity has two factories (Bouzas and Coia), that are 500 metres apart, and that have a total surface of 42,000 square metres. CESCE has experience in covering another transaction (in 2002) with the same shipyard for the sale of a vessel to the Government of Namibia.

On this occasion, CESCE supported the exporting company through Buyer Credit insurance. The insurance covers credit granted by the banking syndicate (BNP Paribas Fortis and Société Générale) to the Republic of Indonesia to finance the export contract.

Exporter Construcciones Navales P. Freire S. A.

Contractor Ministry of Defence

Country Indonesia

Value of transaction US$71,560,000

Type of transaction Financing through Buyer Credit

Term of execution 2.5 years

Amortisation term 4 years

Sector Naval

Date closed April 2016 (policy signature)

Financing banks/Insured

Financial syndicate formed by BNP Paribas Fortis and Société Générale

Agent Bank BNP Paribas

Risks covered

Credit coverage granted by the financial syndicate to the Republic of Indonesia to finance the export transaction.

CESCE Insurance Type Buyer Credit Insurance Policy

45CESCE’S ACtivity REpoRt 2016

FRoFiLE oF CESCE LEttER BUSINESS LINES CESCE iN 2016

Supply and ins ta l la t ion of a i rcraf t ass i s tance equ ipment at the i s lamabad a i rpor t - pak is tan

In mid-2016, CESCE signed both insurance policies to cover some risks stemming from the contract that ADELTE had signed with the Pakistan Civil Aviation Authority to supply and install passenger boarding bridges and other land assistance equipment and its associated civil works for the new terminal of the Islamabad airport, in Pakistan.