1/1/2016 what is a high deductible health plan? city and county of denver

TRANSCRIPT

1/1/2016

What is a High Deductible Health Plan?

City and County of Denver

Opening

A high deductible health plan and an HSA may sound confusing, but we are here today to help you better understand your new plan option.

High Deductible Health Plan

New in 2016 for all City and County of Denver employees

High Deductible Health Plan (HDHP)

A high deductible health plan (HDHP) is a type of health insurance plan that meets the deductible limits set by the Internal Revenue Service (IRS). The plan lets you open a health savings account and save money, tax-free.

Deductible: The amount you owe for health care services your health insurance or plan covers before your health insurance or plan begins to pay. For example, if your deductible is $1,350, you are responsible for all expenses at the discounted UHC rate until you’ve met the $1,350 deductible.

Preventive Care: Preventive care is covered at 100% on your HDHP. For a detailed list of services covered, go to www.uhcpreventivecare.com. Preventive care services are determined by US Preventive Task Force Alliance per health reform guidelines.

The Benefits of a HDHP

Low Up Front Premium!

Member is responsible for all costs up to $1,350 deductible for Employee only coverage and $2,700 deductible for Employee + 1 or more.

Member pays 20% coinsurance for medical services after deductible is met, and copays for prescription medications.

All expenses, including deductible, and pharmacy copays apply to the out-of-pocket maximum of $2,700 for individual and $5,400 for family.

Paired with a Health Savings Account (HSA) which is a bank account that you own to help pay for your qualified expenses

Best of all – The City and County is making an initial contribution of $600 (individual) and $1,200 (family) into your HSA account.

HOW DOES A HIGH DEDUCTIBLE HEALTH PLAN WORK?

High Deductible Health Plan

You have the freedom to use any doctor or hospital you want. The UHC Network will remain the same. The Network is Nationwide and you do not need to change your doctors.

You save money when you use health care providers in the Choice Plus network because they’ve agreed to charge lower prices.

You will have coverage if you receive care outside the network. However, you will likely pay more.

You save more whenyou stay in network.

High Deductible Health Plan

You do not need to choose a primary care provider (PCP).

The covered services remain the same, it is just how the services are paid which is changing. If you are currently in treatment (i.e. pregnancy, chiropractic, or diabetic) your treatment will not be impacted. A PCP can be helpful

in managing your care.

See any doctor, including specialists, without referrals.

Use $1350 Individual Deductible, $2,700 Family Deductible, 80% Coinsurance, and $2,700, $5,400 OOP.Preventive care is covered 100% when you use a network doctor.

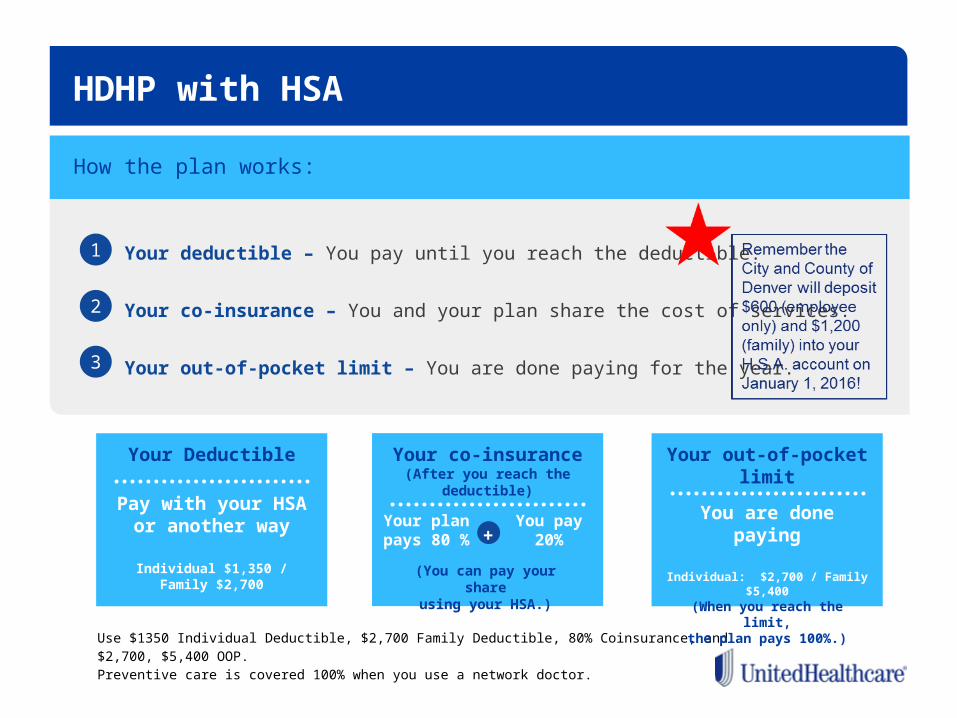

HDHP with HSA

How the plan works:

Your Deductible

Pay with your HSA or another way

Individual $1,350 / Family $2,700

Your co-insurance(After you reach the

deductible)

Your planpays 80 %

You pay 20%+

Your out-of-pocket limit

You are done paying

Individual: $2,700 / Family $5,400(When you reach the limit,

the plan pays 100%.)(You can pay your share

using your HSA.)

Your deductible – You pay until you reach the deductible.

Your co-insurance – You and your plan share the cost of services.

Your out-of-pocket limit – You are done paying for the year.

1

2

3

In 2016 - $1350 Individual Deductible, $2,700 Family Deductible, 80% Coinsurance, and $2,700, $5,400 OOP.Preventive care is covered 100% when you use a network doctor.

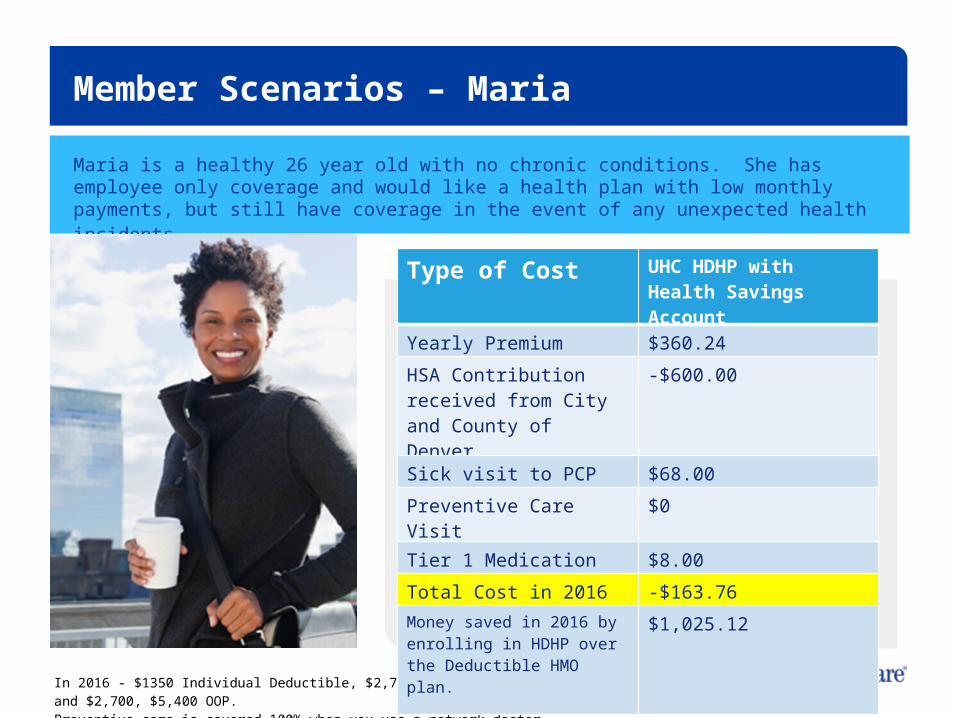

Member Scenarios – Maria

Maria is a healthy 26 year old with no chronic conditions. She has employee only coverage and would like a health plan with low monthly payments, but still have coverage in the event of any unexpected health incidents.

Your Deductible

Pay with your HSA or another way

Individual $1,350 / Family $2,750

Type of Cost UHC HDHP with Health Savings Account

Yearly Premium $360.24

HSA Contribution received from City and County of Denver

-$600.00

Sick visit to PCP $68.00

Preventive Care Visit $0

Tier 1 Medication $8.00

Total Cost in 2016 -$163.76

Money saved in 2016 by enrolling in HDHP over the Deductible HMO plan.

$1,025.12

In 2016, $1350 Individual Deductible, $2,700 Family Deductible, 80% Coinsurance, and $2,700, $5,400 OOP.Preventive care is covered 100% when you use a network doctor.

Member Scenarios – Tom

Tom is a father of 2 young children and a spouse who is expecting their third child in 2016. He has family coverage and needs a plan that makes the most financial sense.

Pay with your HSA or another way

Individual $1,350 / Family $2,750

Type of Cost UHC HDHP with Health Savings Account

Yearly Premium $3,458.04

HSA Contribution received from City and County of Denver

-$1,200.00

4 Sick visits to PCP $272.00

4 Preventive Care Visits $0

Urgent Care Visit $110.00

Emergency Room Visit $1,800.00

4 Day Hospital IP Admit $3,210.00

Tier 1 Medication $8.00

Total Cost in 2016 $7,658.04

Money saved in 2016 by enrolling in HDHP over the Deductible HMO plan.

$1,468.04

Consumerism and the HDHPHow do I know how much my healthcare costs?

The cost of care – how will you know?

13

Utilize UHC’s Treatment Cost Estimator available on www.myuhc.com.

Use Tier 1 Medications when appropriate, the UHC Pharmacy Drug list is available on www.myuhc.com.

Seek care at appropriate place of service (i.e. utilize urgent care rather than emergency room)

Ask Questions!

We have many tools available to make you a wise consumer of healthcare.

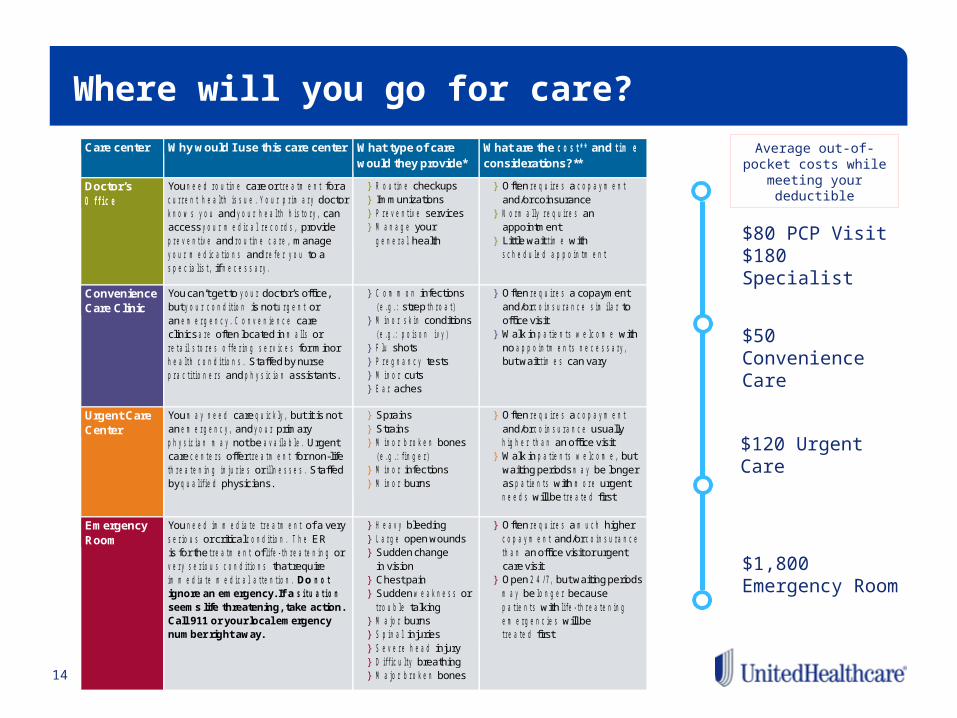

Where will you go for care?

14

Care center Why would I use this care center What type of care would they provide*

What are the cost** and tim e considerations?**

Doctor’s Office

You need routine care or trea tm ent for a curren t hea lth issue . Your prim ary doctor know s you and your hea lth h is tory, can access your m edica l records , provide preventive and routine care , manage your m ed ications and refer you to a specialis t, if necess ary.

} R outine checkups } Immunizations } Preventive services } M anage your

genera l health

} Often requires a copaym ent and/or coinsurance

} N orm ally requires an appointment

} Little wait tim e with scheduled appointm ent

Convenience Care Clinic

You can’t get to your doctor’s office, but your condition is not urgent or an em ergency. C onven ience care clinics are often located in m alls or re ta il s tores o ffering serv ices for minor health conditions. Staffed by nurse prac titioners and physic ian assistants.

} C om m on infections (e.g .: strep throat)

} M inor sk in conditions (e .g.: po ison ivy)

} F lu shots } Pregnancy tests } M inor cuts } Ear aches

} Often requires a copayment and/or co insurance s im ila r to office visit

} Walk in pa tien ts w elcom e with no appointm ents necess ary, but wait tim es can vary

Urgent Care Center

You m ay need care quick ly, but it is not an em ergency, and your primary physic ian m ay not be ava ilab le . Urgent care cente rs offer treatm ent for non-life threa ten ing in juries or illnesses. Staffed by qualified physicians.

} Sprains } Strains } M inor broken bones

(e.g.: finger) } M inor infections } M inor burns

} Often requires a copaym ent and/or coinsurance usually h igher than an office visit

} Walk in patients w elcom e, but waiting periods m ay be longer as patien ts with m ore urgent needs will be treated first

Emergency Room

You need im m edia te treatm ent of a very serious or critical cond ition . The ER is for the treatm ent of life -th rea ten ing or very serious conditions that require im m ediate m edica l a tten tion . Do not ignore an emergency. If a situation seems life threatening, take action. Call 911 or your local emergency number right away.

} H eavy bleeding } Large open wounds } Sudden change

in vision } Chest pain } Sudden w eakness or

trouble talking } M ajor burns } Spinal injuries } S evere head injury } D ifficu lty breathing } M ajor broken bones

} Often requires a m uch higher copaym ent and/or coinsurance than an office visit or urgent care visit

} Open 24/7, but waiting periods m ay be longer because patients with life -threa ten ing em ergencies will be treated first

Average out-of-pocket costs while meeting your

deductible

$80 PCP Visit$180 Specialist

$50 Convenience Care

$120 Urgent Care

$1,800 Emergency Room

HOW DOES THE PLAN WORK WITH AN HSA?

How the plan works with an HSA

Think of an HSA as a savings plan for health care you’ll need today, tomorrow and into the future.

It’s a real bank account, but you don’t pay federal income tax on the money you deposit into it and the money you use for qualified medical expenses. Your savings also grows tax free.

You can even build your savings into a nest egg for retirement. Your savings grow from year to year. There’s no “use it or lose it” rule.

The money is there when you need it. And it’s yours to keep.

WHY HAVE A HEALTH SAVINGS ACCOUNT?

18

Health Savings Account

You own it.

It has triple tax benefits.

Anyone can contribute.

It’s not just for doctor visits.

You can invest it.

You can save it for the future.

Your employer is making an up-front contribution of $600 (employee only) and $1,200 (family) your HSA. There is no match required!

WHO IS ELIGIBLE TO OPEN AN HSA?

20

Eligibility

You are covered under an eligible high-deductible health plan (HDHP).

You are covered by no other health coverage, unless it is permissible coverage like vision or dental.

You are not enrolled in Medicare.

You cannot be claimed as a dependent on someone else’s tax return.

To deposit money into an HSA, you must be enrolled in an HSA-eligible health plan.

Some other restrictions apply. Please consult your tax, benefits or financial advisor.

You are eligible if:

2016 HSA GUIDELINES – AS ESTABLISHED BY THE IRS

2016 Contribution Limits

The IRS limits how much you can put into your HSA each year.

Source: National Data as Reported by HHS through March 10, 2015

The 2016 limits are:

Family Coverage

IndividualCoverage

$3,350

$6,750

Are you 55 or older?You can put in an extra $1,000 this year.

WHO IS OPTUMBANK?

OptumBank

UnitedHealthcare’s preferred health care bank is dedicated to helping people save for health care.

The national leader in HSA banking with more than a million account holders.

Offers the convenience of banking through myuhc.com.

WHAT IS A HEALTH SAVINGS ACCOUNT (HSA)?

Health Savings Account (HSA)

A health savings account (HSA) is a bank account that lets people put money aside, tax-free, to save and pay for health care expenses.

The Internal Revenue Service (IRS) limits who can open and put money into an HSA.

http://bcove.me/36evndji

Video

How to open your HSA with OptumBank

Yes, they are a real bank and the largest HSA bank in the country.

OptumBank is focused only on health care and helping you save.

Three different account types.

Each has different monthly maintenance fees which are waived once a specified dollar amount is reached.

Some earn interest on account balances.

You can invest the money in mutual funds after a certain dollar amount is reached (level of money needed for investments differs by account type).

Will be linked to your insurance plan to make things easy.

The City and County of Denver will provide you a URL link to open your bank account with OptumBank during Open Enrollment.

– Member FDIC

Benefits of the HSA Debit Card

You will receive a UnitedHealthcare HSA Debit Card

Provided by OptumHealth Bank

Use at doctor’s office or pharmacy

Withdraw cash at ATM*

Get additional cards for family members

Free online bill pay

Checks (optional, $10 for $25)

*Access fees may also be charged by ATM owner.

Easy access to HSA dollars

PAYING FOR SERVICES RECEIVED

31

Payment for Services

Use your Optum Bank HSA Debit MasterCard® at a pharmacy, doctor’s office or other health care provider. Payment at time of service is only required for pharmacy charges.

Reimburse yourself for qualified health care expenses from your HSA.

Pay bills online at no charge, or pay with checks linked to your HSA, if you choose to purchase them.

You can use your HSA to pay for qualified medical, dental and vision expenses, such asdoctor visits, prescriptions and hospital visits, to name only a few.

There’s no “use it or lose it” rule. You decide whether to spend your money on health carenow or to build your savings for expenses later.

Payment is simple:

32

Payment for Services

The HSA payment process:

Present ID card to doctor

Doctor sends claim to UnitedHealthcare.UnitedHealthcare applies network discount, sends back to doctor.

Doctor then bills you for payment. After deductible, doctor bills you for your share of co-insurance.

When you have claim activity, you will receive a Health Statement.

1

2

3

4

RECAP OF HDHP WITH HSA

34

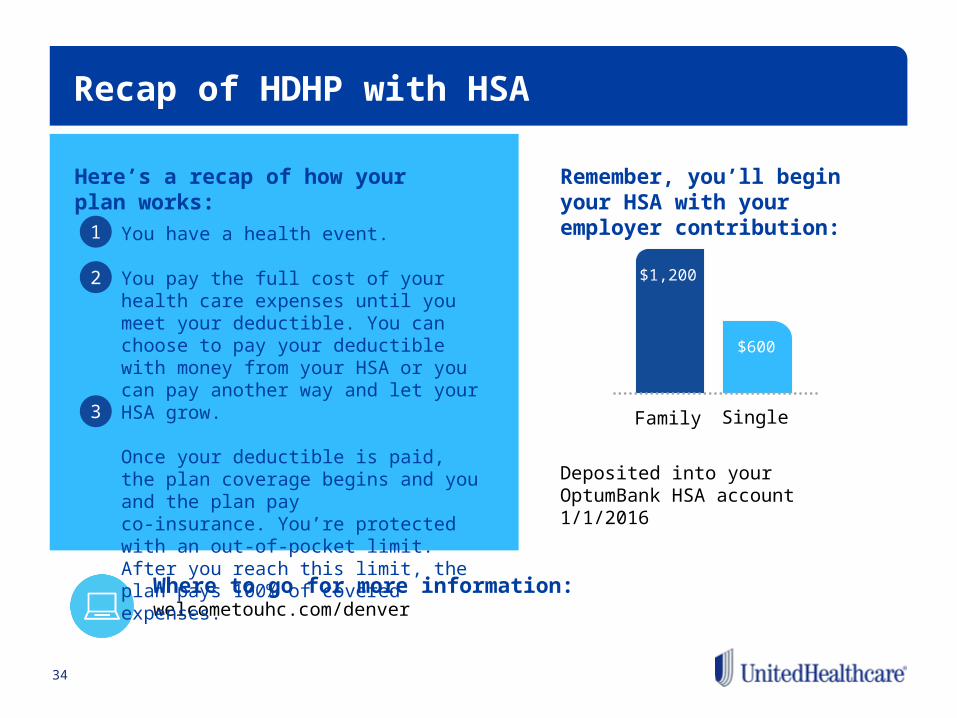

Recap of HDHP with HSA

Here’s a recap of how your plan works:

Where to go for more information:welcometouhc.com/denver

Deposited into your OptumBank HSA account 1/1/2016

Remember, you’ll begin your HSA with your employer contribution:

Family Single

$600

$1,200

1 You have a health event.

You pay the full cost of your health care expenses until you meet your deductible. You can choose to pay your deductible with money from your HSA or you can pay another way and let your HSA grow.

Once your deductible is paid, the plan coverage begins and you and the plan pay co-insurance. You’re protected with an out-of-pocket limit. After you reach this limit, the plan pays 100% of covered expenses.

2

3

Sidewalk Talk - Video

35

http://www.uhc.tv/uhc_video/whats-an-hsa