11 th annual wasbo accounting seminar orientation for staff new to the school business office...

TRANSCRIPT

1111thth Annual WASBO Annual WASBOAccounting SeminarAccounting Seminar

Orientation for Orientation for Staff New to the Staff New to the School Business School Business

OfficeOfficePresented By:Presented By:Mark VanDerZee, Director of Business Services Menasha Mark VanDerZee, Director of Business Services Menasha School DistrictSchool DistrictNatalie Rew, CPA, DPI School Finance AuditorNatalie Rew, CPA, DPI School Finance AuditorGene Fornecker, CPA, DPI School Finance AuditorGene Fornecker, CPA, DPI School Finance Auditor

March 21, 2007March 21, 2007

Basic Guideposts Basic Guideposts for the for the

New Business New Business OfficialOfficial

Thoughts & IdeasThoughts & Ideas shared from shared from Experiences Experiences

and and NetworkingNetworking

Guideposts for the Guideposts for the New Business OfficialsNew Business Officials

Understand Your RoleUnderstand Your Role Build Relationships & NetworksBuild Relationships & Networks Get to Know Your ResourcesGet to Know Your Resources Develop Your Personal Develop Your Personal

& Personnel Skills& Personnel Skills

Guideposts for the Guideposts for the New Business OfficialsNew Business Officials

Understand Your RoleUnderstand Your Role Build Relationships & NetworksBuild Relationships & Networks Get to Know Your ResourcesGet to Know Your Resources Develop Your Personal Develop Your Personal

& Personnel Skills& Personnel Skills

School BoardSchool Board

Provides a Vision for Student Achievement Provides a Vision for Student Achievement shared by Board, Superintendent, Staff & shared by Board, Superintendent, Staff & CommunityCommunity

Approves Strategic Plan (Framework or Road Approves Strategic Plan (Framework or Road Map) with Stakeholders & AdministrationMap) with Stakeholders & Administration

Adopts Goals to Support the PlanAdopts Goals to Support the Plan Communicates the Communicates the

Plan to StakeholdersPlan to Stakeholders Keeps the Vision at Keeps the Vision at

the forefront of all the forefront of all DecisionsDecisions

Superintendent & Superintendent & Business OfficialBusiness Official

Recommends Visionary StrategiesRecommends Visionary Strategies Provides Information & RecommendationsProvides Information & Recommendations Ensures the Integrity of the Planning processEnsures the Integrity of the Planning process Implements the Board’s plan Implements the Board’s plan Ensures the Board’s plan is carried outEnsures the Board’s plan is carried out Works to ensure that the Works to ensure that the

Vision & Mission is kept in Vision & Mission is kept in the forefront of all the forefront of all DecisionsDecisions

Guideposts for the Guideposts for the New Business OfficialsNew Business Officials

Understand Your RoleUnderstand Your Role Build Relationships & NetworksBuild Relationships & Networks Get to Know Your ResourcesGet to Know Your Resources Develop Your Personal Develop Your Personal

& Personnel Skills& Personnel Skills

Building Relationships & Building Relationships & NetworksNetworks

Develop Rapport with Key StaffDevelop Rapport with Key Staff -first (1-first (1st)st) order of business order of business -fastest way to get you up to speed -fastest way to get you up to speed

Interview your StaffInterview your Staff -get a sense of what all they can do-get a sense of what all they can do -backup is essential in PR, AP, technology, etc. -backup is essential in PR, AP, technology, etc.

Surround yourself with Competent StaffSurround yourself with Competent Staff -you are only as good as those that work for you-you are only as good as those that work for you -assess strengths & weaknesses -assess strengths & weaknesses -work with each as individuals -work with each as individuals

Building Relationships & Building Relationships & NetworksNetworks

Depart from “Business as Usual”Depart from “Business as Usual” -stress innovation & new ways of doing business-stress innovation & new ways of doing business -support & create safe environment for risk taking -support & create safe environment for risk taking -ask staff what 2 things they would change and why -ask staff what 2 things they would change and why

Establish bases of SupportEstablish bases of Support -process issues & build support from Supt. & Board-process issues & build support from Supt. & Board -review intentions -review intentions beforebefore implementing implementing -make him/her/them feel a part of the process -make him/her/them feel a part of the process -participation in the process builds trust & -participation in the process builds trust & confidenceconfidence

Discuss with Supt. what Issues are ImportantDiscuss with Supt. what Issues are Important -identify any “sacred cows”-identify any “sacred cows”

Building Relationships & Building Relationships & NetworksNetworks

Provide Support for your StaffProvide Support for your Staff -show support for your staff often-show support for your staff often -everyone likes positives strokes when deserved -everyone likes positives strokes when deserved

Create networks with Local business Create networks with Local business managersmanagers -they are invaluable resources-they are invaluable resources

-they provide understanding support -they provide understanding support Get Involved with Your State Get Involved with Your State

AssociationAssociation -WASBO, SAA & Other Associations pay dividends-WASBO, SAA & Other Associations pay dividends -Participation is it’s own Reward -Participation is it’s own Reward

Basic Guideposts for the Basic Guideposts for the New Business OfficialsNew Business Officials

Understand Your RoleUnderstand Your Role Build Relationships & NetworksBuild Relationships & Networks Get to Know Your ResourcesGet to Know Your Resources Develop Your Personal Develop Your Personal

& Personnel Skills& Personnel Skills

Local ResourcesLocal Resources

Board Vision, Mission, Goals & PoliciesBoard Vision, Mission, Goals & Policies District or Administrative Policies & District or Administrative Policies &

ProceduresProcedures District Labor ContractsDistrict Labor Contracts Local OrdinancesLocal Ordinances Other Governments & Community ResourcesOther Governments & Community Resources Local Vendors & ContractorsLocal Vendors & Contractors Local Web ResourcesLocal Web Resources Students, Parents & StaffStudents, Parents & Staff

State & Federal State & Federal ResourcesResources

WI StatutesWI Statutes Department of Public Instruction (DPI)Department of Public Instruction (DPI) School Administrators Alliance (SAA)School Administrators Alliance (SAA) WASBO, WASDA, WASB, WERC, SNA, etc.WASBO, WASDA, WASB, WERC, SNA, etc. No Child Left Behind (NCLB)No Child Left Behind (NCLB) National School Lunch ProgramNational School Lunch Program Special Education (IDEA)Special Education (IDEA) TransportationTransportation Professional Web ResourcesProfessional Web Resources

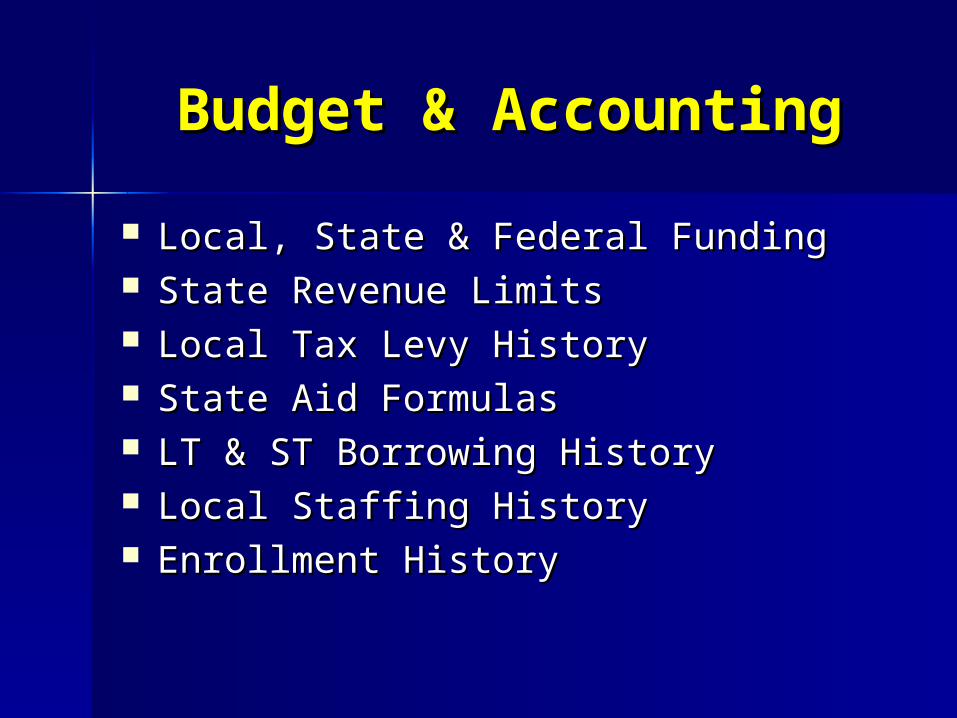

Budget & AccountingBudget & Accounting

Local, State & Federal Funding Local, State & Federal Funding State Revenue LimitsState Revenue Limits Local Tax Levy HistoryLocal Tax Levy History State Aid FormulasState Aid Formulas LT & ST Borrowing HistoryLT & ST Borrowing History Local Staffing HistoryLocal Staffing History Enrollment History Enrollment History

Basic Guideposts for the Basic Guideposts for the New Business OfficialsNew Business Officials

Understand Your RoleUnderstand Your Role Build Relationships & NetworksBuild Relationships & Networks Get to Know Your ResourcesGet to Know Your Resources Develop Your Personal Develop Your Personal

& Personnel Skills& Personnel Skills

Personal & Personnel Personal & Personnel SkillsSkills

Be Visible & Approachable as a ManagerBe Visible & Approachable as a Manager -get out in the school environment-get out in the school environment

Adopt a Decision-Making ProcessAdopt a Decision-Making Process -find out how decisions are made-find out how decisions are made -search out models if none currently exist -search out models if none currently exist

FlexibleFlexible but but ConsistentConsistent Decisions Decisions

CreativeCreative yet yet DisciplinedDisciplined Decisions Decisions -Don’t shoot from the Hip-Don’t shoot from the Hip -Don’t assume anything -Don’t assume anything -Take time to analyze & assess; -Take time to analyze & assess; -3 Ps = Process; Process; Process” -3 Ps = Process; Process; Process” -Anticipate the impact of the decision -Anticipate the impact of the decision beforebefore you do it. you do it. -Stay balanced -Stay balanced

DECISION MAKINGDECISION MAKING

is arguably the most critical component of is arguably the most critical component of business success, yet it remains the least business success, yet it remains the least

understood and most commonly understood and most commonly mishandled aspect of all mishandled aspect of all

senior management senior management

responsibilities.responsibilities.

Michael MenardMichael Menard

MWorld Spring 2003MWorld Spring 2003

American Management AssociationAmerican Management Association

Personal & Personnel Personal & Personnel SkillsSkills

Set Goals for Yourself & DepartmentSet Goals for Yourself & Department -limit to 2 or 3 goals-limit to 2 or 3 goals -accomplish & do them well -accomplish & do them well -initial impressions last a long time -initial impressions last a long time

Don’t try to Control EverythingDon’t try to Control Everything -may actually lose control-may actually lose control -may go insane trying -may go insane trying

Don’t Try to Do EverythingDon’t Try to Do Everything -delegate responsibility-delegate responsibility -hold staff accountable -hold staff accountable

Personal & Personnel Personal & Personnel SkillsSkills

Look at the BIG pictureLook at the BIG picture -don’t get mired in minutia-don’t get mired in minutia -keep your eye on the end result -keep your eye on the end result

Don’t be Afraid to Admit mistakesDon’t be Afraid to Admit mistakes -it’s OK to say “I don’t know and -it’s OK to say “I don’t know and -“I will find out the answer & get back -“I will find out the answer & get back

Know your LimitationsKnow your Limitations -you can’t be expert on everything; no one -you can’t be expert on everything; no one expects it!expects it! -have a general sense about what’s going on -have a general sense about what’s going on -know a little about a lot of things -know a little about a lot of things

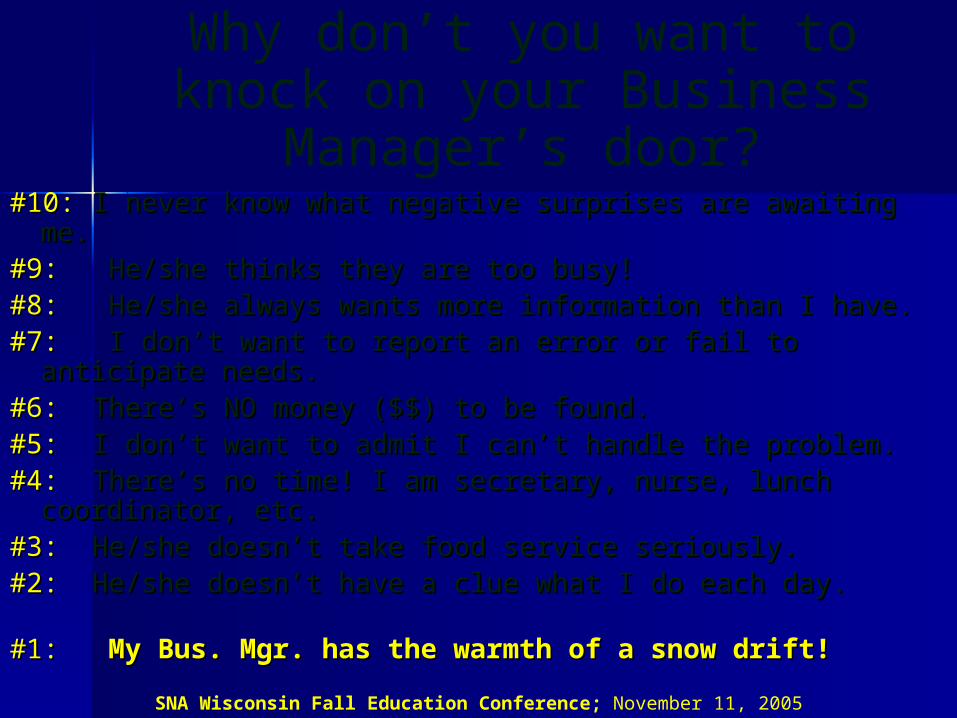

#10: #10: I never know what negative surprises are awaiting me.I never know what negative surprises are awaiting me.#9: #9: He/she thinks they are too busy!He/she thinks they are too busy!#8: #8: He/she always wants more information than I have.He/she always wants more information than I have.#7:#7: I don’t want to report an error or fail to anticipate I don’t want to report an error or fail to anticipate

needs.needs.#6: #6: There’s NO money ($$) to be found.There’s NO money ($$) to be found.#5: #5: I don’t want to admit I can’t handle the problem.I don’t want to admit I can’t handle the problem.#4: #4: There’s no time! I am secretary, nurse, lunch There’s no time! I am secretary, nurse, lunch

coordinator, etc.coordinator, etc.#3: #3: He/she doesn’t take food service seriously.He/she doesn’t take food service seriously.#2:#2: He/she doesn’t have a clue what I do each day.He/she doesn’t have a clue what I do each day.

#1: #1: My Bus. Mgr. has the warmth of a snow drift!My Bus. Mgr. has the warmth of a snow drift!SNA Wisconsin Fall Education Conference; November 11, 2005

Why don’t you want to knock on your Business Manager’s

door?

Personal & Personnel Personal & Personnel SkillsSkills

Be Friendly & Greet People with a SMILE!Be Friendly & Greet People with a SMILE! -even when you are up to your armpits in alligators! -even when you are up to your armpits in alligators!

Maintain a Sense of Humor!Maintain a Sense of Humor! -everything is relative!-everything is relative!

School Business School Business Management is not Easy!Management is not Easy!

Strength Strength WisdomWisdomCourageCourage

PersistencePersistencePerseverancePerseverance

*** SUCCESS ***

SCHOOL FINANCIAL SERVICES HOMEPAGE

All School Financial Services related resources in alphabetical order.

SAVE THIS PAGE AS A FAVORITEwww.dpi.wi.gov/sfs/index.html

WUFAR and WUFAR and GovernmentGovernment Accounting Accounting

FUND:FUND: A fiscal and accounting entity A fiscal and accounting entity

with a with a self-balancingself-balancing set of set of accounts…which are accounts…which are segregated for the purpose of segregated for the purpose of carrying on specific activities in carrying on specific activities in accordance with special accordance with special regulations, restrictions, or regulations, restrictions, or limitationslimitations

FUNDSFUNDS General Fund – Operating fund-Day to General Fund – Operating fund-Day to

day business not required to be day business not required to be reported in another fund (fund 10)reported in another fund (fund 10)

Funds used for a specified purposeFunds used for a specified purpose– Special Revenue (Fund 21-29)Special Revenue (Fund 21-29)– Debt Service (Funds 38 - 39)Debt Service (Funds 38 - 39)– Capital Projects (Funds 41 - 49)Capital Projects (Funds 41 - 49)– Fiduciary (Fund 72 - 73)Fiduciary (Fund 72 - 73)– Agency (Fund 60)Agency (Fund 60)– Community Service (Fund 80)Community Service (Fund 80)– Cooperative (Fund 90)Cooperative (Fund 90)

Proprietary funds – Business type Proprietary funds – Business type activities activities - - Food Service (Fund 50)Food Service (Fund 50)

GENERAL FUNDGENERAL FUND

FUND 10FUND 10

Financial transactions relating to Financial transactions relating to the district’s day to day business the district’s day to day business operations not required to be operations not required to be accounted for in other funds.accounted for in other funds.

SPECIAL REVENUE SPECIAL REVENUE FUNDSFUNDS

FUND 21FUND 21GIFTS AND DONATIONS RECEIVED FROM PRIVATE PARTIES GIFTS AND DONATIONS RECEIVED FROM PRIVATE PARTIES THAT CAN BE USED FOR DISTRICT OPERATIONSTHAT CAN BE USED FOR DISTRICT OPERATIONS

FUND 23FUND 23ANY REMAINING TEACH FUND BALANCE BEING USED TO MAKE ANY REMAINING TEACH FUND BALANCE BEING USED TO MAKE PAYMENTS ON A TEACH LOAN. NO NEW TEACH MONEYPAYMENTS ON A TEACH LOAN. NO NEW TEACH MONEY

FUND 27FUND 27SPECIAL EDUCATION AND RELATED SERVICES FUNDED SPECIAL EDUCATION AND RELATED SERVICES FUNDED WHOLLY OR IN PART WITH STATE OR FEDERAL SPECIAL WHOLLY OR IN PART WITH STATE OR FEDERAL SPECIAL EDUCATION AIDEDUCATION AID

FUND 29FUND 29SPECIAL REVENUE K-12 INSTRUCTIONAL PROGRAMS NOT SPECIAL REVENUE K-12 INSTRUCTIONAL PROGRAMS NOT REQUIRED TO BE REPORTED IN OTHER SPECIAL REVENUE REQUIRED TO BE REPORTED IN OTHER SPECIAL REVENUE FUNDS – Federal Indian Education & Head Start used for K-12FUNDS – Federal Indian Education & Head Start used for K-12

CAPITAL PROJECTS CAPITAL PROJECTS FUNDSFUNDS

FUND 41FUND 41Recording capital expenditures financed Recording capital expenditures financed

through an expansion tax levy. through an expansion tax levy.

FUND 48FUND 48 Recording capital expenditures financed through a Recording capital expenditures financed through a TIF district. (No districts in Wisconsin currently use TIF district. (No districts in Wisconsin currently use 48)48)

FUND 49 FUND 49 Recording capital expenditures financed through Recording capital expenditures financed through bondsbonds, , promissory notes , State Trust funds Loans, promissory notes , State Trust funds Loans, Or Land Contracts. Most Common.Or Land Contracts. Most Common.

OTHER SPECIAL OTHER SPECIAL PURPOSE FUNDSPURPOSE FUNDS

FOOD SERVICE FUND - FUND 50FOOD SERVICE FUND - FUND 50 ACCOUNT FOR THE DISTRICT’S ACTIVITIES ACCOUNT FOR THE DISTRICT’S ACTIVITIES RELATING TO RELATING TO PUPIL AND ELDERLYPUPIL AND ELDERLY FOOD FOOD SERVICE (May be a business type activity)SERVICE (May be a business type activity)

COMMUNITY SERVICE FUND - COMMUNITY SERVICE FUND - FUND FUND 8080

ACTIVITIES WHERE THE PRIMARY FUNCTION ACTIVITIES WHERE THE PRIMARY FUNCTION IS TO SERVE THE COMMUNITY– ADULT IS TO SERVE THE COMMUNITY– ADULT EDUCATION, DAY CARE, COMMUNITY POOL EDUCATION, DAY CARE, COMMUNITY POOL (Open to everyone in the community)(Open to everyone in the community)

TRUST FUNDSTRUST FUNDS

ASSETS HELD BY THE DISTRICT IN A ASSETS HELD BY THE DISTRICT IN A TRUSTEE CAPACITY FOR INDIVIDUALS TRUSTEE CAPACITY FOR INDIVIDUALS AND PRIVATE ORGANIZATIONS AND PRIVATE ORGANIZATIONS FUND 72FUND 72ACCOUNTS FOR GIFTS AND DONATIONS SPECIFIED ACCOUNTS FOR GIFTS AND DONATIONS SPECIFIED FOR THE BENEFIT OF PRIVATE INDIVIDUALS AND FOR THE BENEFIT OF PRIVATE INDIVIDUALS AND ORGANIZATIONS NOT UNDER THE CONTROL OF ORGANIZATIONS NOT UNDER THE CONTROL OF THE SCHOOL BOARD - SCHOLARSHIPSTHE SCHOOL BOARD - SCHOLARSHIPS

FUND 73FUND 73ACCOUNTS FOR RESOURCES HELD IN TRUST FOR ACCOUNTS FOR RESOURCES HELD IN TRUST FOR FORMALLY ESTABLISHED OTHER POST FORMALLY ESTABLISHED OTHER POST EMPLOYMENT BENEFITS PLANS EMPLOYMENT BENEFITS PLANS (OPEB)(OPEB)

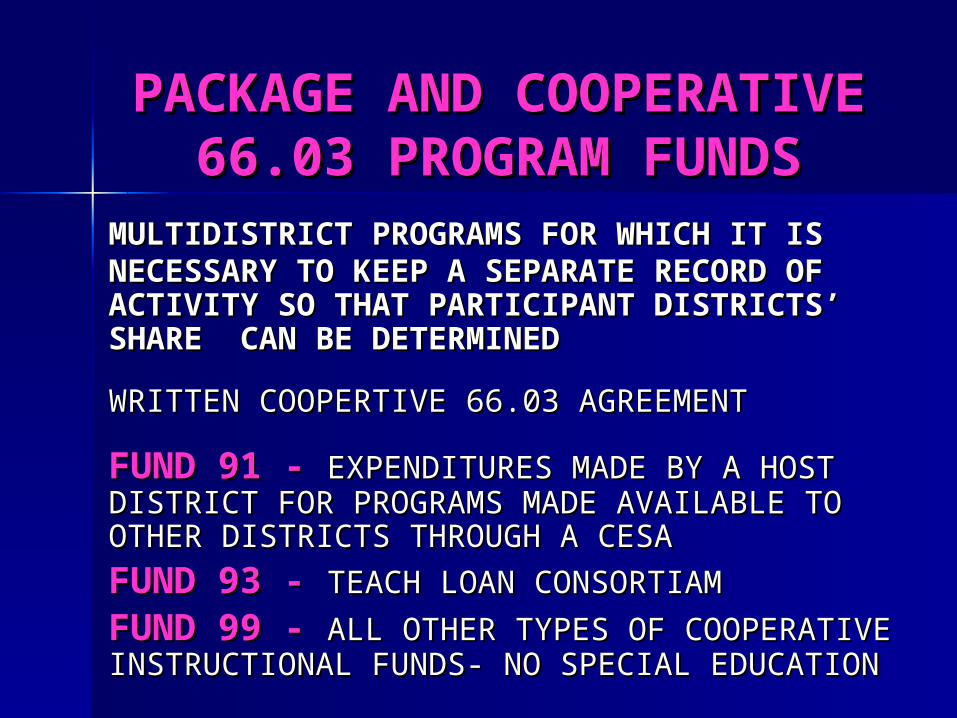

PACKAGE AND PACKAGE AND COOPERATIVE 66.03 COOPERATIVE 66.03

PROGRAM FUNDSPROGRAM FUNDSMULTIDISTRICT PROGRAMS FOR WHICH IT IS MULTIDISTRICT PROGRAMS FOR WHICH IT IS NECESSARY TO KEEP A SEPARATE RECORD OF NECESSARY TO KEEP A SEPARATE RECORD OF ACTIVITY SO THAT PARTICIPANT DISTRICTS’ ACTIVITY SO THAT PARTICIPANT DISTRICTS’ SHARE CAN BE DETERMINED SHARE CAN BE DETERMINED

WRITTEN COOPERTIVE 66.03 AGREEMENT WRITTEN COOPERTIVE 66.03 AGREEMENT

FUND 91 - FUND 91 - EXPENDITURES MADE BY A HOST EXPENDITURES MADE BY A HOST DISTRICT FOR PROGRAMS MADE AVAILABLE TO DISTRICT FOR PROGRAMS MADE AVAILABLE TO OTHER DISTRICTS THROUGH A CESAOTHER DISTRICTS THROUGH A CESA

FUND 93 - FUND 93 - TEACH LOAN CONSORTIAMTEACH LOAN CONSORTIAM

FUND 99 - FUND 99 - ALL OTHER TYPES OF COOPERATIVE ALL OTHER TYPES OF COOPERATIVE INSTRUCTIONAL FUNDS- NO SPECIAL EDUCATIONINSTRUCTIONAL FUNDS- NO SPECIAL EDUCATION

PACKAGE AND PACKAGE AND COOPERATIVE PROGRAM COOPERATIVE PROGRAM

FUNDSFUNDSFUND 91 - FUND 91 - EXPENDITURES MADE EXPENDITURES MADE

BY A HOST DISTRICT FOR BY A HOST DISTRICT FOR PROGRAMS MADE AVAILABLE TO PROGRAMS MADE AVAILABLE TO OTHER DISTRICTS THROUGH A OTHER DISTRICTS THROUGH A CESACESA

-- CESA MAKES THE PACKAGED CESA MAKES THE PACKAGED SERVICES AVAILABLE TO THE DISTRICTSERVICES AVAILABLE TO THE DISTRICT

- - REVENUE – CESA PAYS HOST DISTRICT REVENUE – CESA PAYS HOST DISTRICT FOR FULL COST OF PROGRAMFOR FULL COST OF PROGRAM

-- REVENUE MUST EQUAL EXPENDITURESREVENUE MUST EQUAL EXPENDITURES

TWO PARTS OF TWO PARTS OF ACCOUNTING ACCOUNTING

SYSTEMSYSTEMBASISBASIS

– WHEN SHOULD WE RECORD WHEN SHOULD WE RECORD THE TRANSACTION IN THE TRANSACTION IN ACCOUNTING RECORDSACCOUNTING RECORDS

CLASSIFICATION CLASSIFICATION – WHAT ACCOUNT CODE SHOULD WHAT ACCOUNT CODE SHOULD

WE USE TO RECORD A WE USE TO RECORD A TRANSACTION IN ACCOUNTING TRANSACTION IN ACCOUNTING RECORDSRECORDS

WUFAR ACCOUNTINGWUFAR ACCOUNTING SYSTEMSYSTEM

STATUTORY REQUIREMENT 115.28(13) STATUTORY REQUIREMENT 115.28(13) “PRESCRIBE A UNIFORM FINANCIAL “PRESCRIBE A UNIFORM FINANCIAL FUND ACCOUNTING SYSTEM”FUND ACCOUNTING SYSTEM”

MUST BE USED FOR ALL FINANCIAL MUST BE USED FOR ALL FINANCIAL REPORTS SUBMITTED TO THE DPI REPORTS SUBMITTED TO THE DPI – ANNUAL REPORTANNUAL REPORT– BUDGET REPORTBUDGET REPORT– SPECIAL EDSPECIAL ED

WUFARWUFARUPDATED AT LEAST TWICE UPDATED AT LEAST TWICE

A YEAR - Last updated A YEAR - Last updated September 2006September 2006

Next update May 2007Next update May 2007

PRINT IT OUTPRINT IT OUT

WUFAR ACCOUNTING WUFAR ACCOUNTING SYSTEMSYSTEM

PROVIDES CONSISTENT REPORTING FOR PROVIDES CONSISTENT REPORTING FOR COMPARABILITY FROM YEAR TO YEAR COMPARABILITY FROM YEAR TO YEAR AND BETWEEN DISTRICTS(UNIFORMITY)AND BETWEEN DISTRICTS(UNIFORMITY)

DISTRICTS ARE NOT REQUIRED TO USE DISTRICTS ARE NOT REQUIRED TO USE WUFAR AS ACCOUNTING SYSTEM (WUFAR AS ACCOUNTING SYSTEM (HIGHLY HIGHLY RECOMMENDEDRECOMMENDED))

ACCOUNT STRUCTURE CAN BE MODIFIED ACCOUNT STRUCTURE CAN BE MODIFIED TO MEET LOCAL INFORMATION TO MEET LOCAL INFORMATION REQUIREMENTSREQUIREMENTS

ACCOUNT ACCOUNT CLASSIFICATIONCLASSIFICATION

WEBSITE LINKWEBSITE LINK– www.dpi.wi.gov/sfs/wufar.htmlwww.dpi.wi.gov/sfs/wufar.html

WUFAR MANUALWUFAR MANUAL– ACCOUNT TITLES & DESCRIPTIONSACCOUNT TITLES & DESCRIPTIONS

MATRIXMATRIX– ALLOWABLEALLOWABLE ACCOUNTACCOUNT

CLASSIFICATIONS BY FUNDCLASSIFICATIONS BY FUND

WUFAR WEB LINKWUFAR WEB LINK

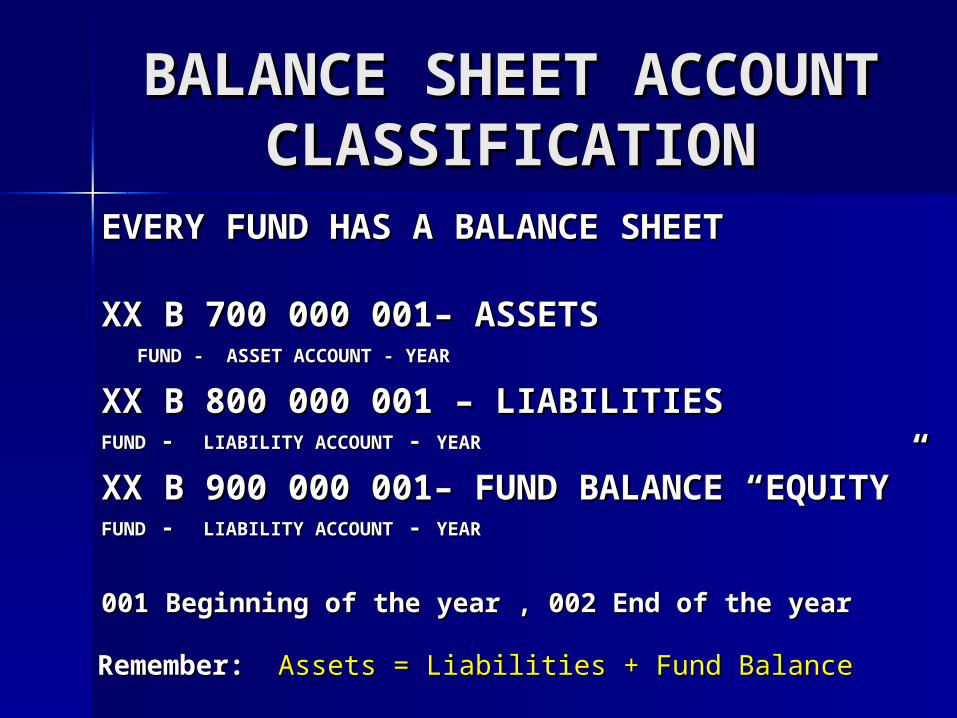

BALANCE SHEET BALANCE SHEET ACCOUNT ACCOUNT

CLASSIFICATIONCLASSIFICATIONEVERY FUND HAS A BALANCE SHEETEVERY FUND HAS A BALANCE SHEET

XX B 700 000 001– ASSETSXX B 700 000 001– ASSETS FUND - ASSET ACCOUNT - YEARFUND - ASSET ACCOUNT - YEAR

XX B 800 000 001 – LIABILITIESXX B 800 000 001 – LIABILITIESFUNDFUND - - LIABILITY ACCOUNTLIABILITY ACCOUNT - - YEARYEAR

XX B 900 000 001– FUND BALANCE XX B 900 000 001– FUND BALANCE “EQUITY”“EQUITY”FUNDFUND - - LIABILITY ACCOUNTLIABILITY ACCOUNT - - YEARYEAR

001 Beginning of the year , 002 End of the year001 Beginning of the year , 002 End of the yearRemember: Remember: Assets = Liabilities + Fund BalanceAssets = Liabilities + Fund Balance

900 000 – FUND 900 000 – FUND BALANCE “EQUITY”BALANCE “EQUITY”

Fund Balance Reserves and Fund Balance Reserves and DesignationsDesignations

THREE PARTSTHREE PARTSRESERVEDRESERVED 931 000931 000 Segregation of fund balance for Segregation of fund balance for restricted purposes not available for appropriationrestricted purposes not available for appropriationDESIGNATEDDESIGNATED 932 000932 000 Formal budgetary action to Formal budgetary action to maintain working cash or other tentative uses.maintain working cash or other tentative uses.UNAPPROPRIATEDUNAPPROPRIATED – UNDESIGNATED 933 000– UNDESIGNATED 933 000 Change in revenues over expenditures. Change in revenues over expenditures.

ARE BUDGETARY APPROPRIATION ACCOUNTS – ARE BUDGETARY APPROPRIATION ACCOUNTS – REQUIRES BOARD APPROVALREQUIRES BOARD APPROVAL

CHANGES REQUIRE BOARD ACTIONCHANGES REQUIRE BOARD ACTION

Statement of Statement of Revenues and Revenues and ExpendituresExpenditures

REVENUESREVENUES – RECORDED WHEN – RECORDED WHEN AVAILABLE TO FUND CURRENT AVAILABLE TO FUND CURRENT ACTIVITIES (KNOWN & MEASURABLE)ACTIVITIES (KNOWN & MEASURABLE)

EXPENDITURESEXPENDITURES – WHETHER WHAT YOU – WHETHER WHAT YOU ARE PURCHASING CAN BE USED FOR ARE PURCHASING CAN BE USED FOR CURRENT ACTIVITIESCURRENT ACTIVITIES

BEGINNING FUND BALANCE + BEGINNING FUND BALANCE + REVENUESREVENUES – – EXPENDITURESEXPENDITURES = ENDING FUND = ENDING FUND BALANCEBALANCE

REVENUEREVENUEPROPERTY TAX LEVY PROPERTY TAX LEVY - FISCAL YEAR LEVIED- FISCAL YEAR LEVIED

STATE/FEDERAL AID – “FORMULA STATE/FEDERAL AID – “FORMULA DRIVEN” - DRIVEN” - YEAR ENTITLEDYEAR ENTITLED

STATE/FEDERAL AID – “REIMBURSABLE STATE/FEDERAL AID – “REIMBURSABLE GRANTS” GRANTS” – CLAIMS BASED ON EXPENDITURES– CLAIMS BASED ON EXPENDITURES

GIFTS/MISCELLANEOUS CASH GIFTS/MISCELLANEOUS CASH COLLECTIONSCOLLECTIONS– RECEIVED AMOUNTRECEIVED AMOUNT

Revenue Account Revenue Account CodingCoding

REVENUEREVENUE– XX XX RR – XXXXXX – – XXXXXX – XXXXXX – – XXXXXX– FUND – FUNCTION – FUND – FUNCTION – SOURCESOURCE – – PROJECTPROJECT

SOURCESOURCE – Define revenue by its origin. Where did – Define revenue by its origin. Where did the money come from? the money come from? Tax levy Federal Aid, Student fees, Tax levy Federal Aid, Student fees, etc.etc.

PROJECTPROJECT – – DPI reserves project codes 100-599 (See aid DPI reserves project codes 100-599 (See aid register account codes) Use project codes above 600 to register account codes) Use project codes above 600 to group internal projects. group internal projects.

Typically no function Typically no function

Exception: All Transfers-in must use a 4XXXXX Exception: All Transfers-in must use a 4XXXXX function (See WUFAR)function (See WUFAR)

Revenue Accounts Revenue Accounts “SOURCES”“SOURCES” Per Per

WUFARWUFARAll revenues, long term debt proceeds and All revenues, long term debt proceeds and “interfund transfers-in” must be coded as a “interfund transfers-in” must be coded as a SOURCESOURCE

100 - Interfund Transfers 100 - Interfund Transfers 200 - Local Sources 200 - Local Sources 300/400 - School Districts 300/400 - School Districts 500 – CESAS 500 – CESAS 600 – State600 – State700 – Federal 700 – Federal 800 – Debt800 – Debt900 – Other 900 – Other

See also the Aid register Coding of Federal and See also the Aid register Coding of Federal and State ProgramsState Programs

EXPENDITURE EXPENDITURE RECOGNITIONRECOGNITION

WHEN ITEMS ARE USED/PLACED IN WHEN ITEMS ARE USED/PLACED IN SERVICESERVICE

WHEN SERVICES ARE PROVIDEDWHEN SERVICES ARE PROVIDED– ““SUMMER PAYROLLS” & RELATED SUMMER PAYROLLS” & RELATED

BENEFITSBENEFITS

– UNSETTLED CONTRACTS – NO UNSETTLED CONTRACTS – NO ADDITIONAL COST UNTIL SETTLEMENT – ADDITIONAL COST UNTIL SETTLEMENT – LAST DATE: OCTOBER 1LAST DATE: OCTOBER 1

EXPENDITURESEXPENDITURES

EXPENDITURESEXPENDITURES

XX XX EE– – XXX XXXXXX XXX – – XXXXXX – XXX – XXXFUND – FUND – FUNCTIONFUNCTION – – OBJECTOBJECT – PROJECT – PROJECTInstructional functions in 6 fundsInstructional functions in 6 funds 26 26 OBJECT ACCOUNTSOBJECT ACCOUNTS associated with each associated with each

instructional function instructional function 100 - Salaries100 - Salaries 200 – Benefits200 – Benefits 300 - Purchased services 300 - Purchased services 400 – Non Capital Objects400 – Non Capital Objects

500 – Capital Objects500 – Capital Objects 600 – Debt Retirement600 – Debt Retirement 700 – Insurance and Judgments 700 – Insurance and Judgments 800 – Transfers800 – Transfers 900 – Other900 – Other

Expenditure Expenditure Accounts Accounts

““FunctionsFunctions””100 000 – INSTRUCTION100 000 – INSTRUCTION200 000 – SUPPORT SERVICES 200 000 – SUPPORT SERVICES (Guidance, Library, (Guidance, Library, Supervision, Business Administration, Maintenance, Central Supervision, Business Administration, Maintenance, Central services… services…

300 000 - COMMUNITY SERVICES 300 000 - COMMUNITY SERVICES 400 000 – NON – PROGRAM 400 000 – NON – PROGRAM ((Interfund transfers, Interfund transfers, adjustment and refunds, Revenue transit to others)adjustment and refunds, Revenue transit to others)

INSTRUCTIONAL FUNCTIONS PERMITTED IN 6 FUNDS

INSTRUCTION IS RESTRICTED TO INTERACTIONS INSTRUCTION IS RESTRICTED TO INTERACTIONS BETWEEN PUPILS AND TEACHERSBETWEEN PUPILS AND TEACHERS

REPORTING REPORTING REQUIREMENTSREQUIREMENTS

SCHOOL FINANCE REPORTING PORTAL

All School Financial Services reports are accessed through the School Finance reporting Portal.

SAVE THIS PAGE AS A FAVORITEwww.dpi.wi.gov/sfs/index.html

Finance Reporting PortalFinance Reporting Portal

District HomepageDistrict Homepage

Status and DeadlinesStatus and Deadlines

Financial Data HomeFinancial Data Home

Financial ReportsFinancial Reports

Aid Certification PI-1505 ACAid Certification PI-1505 AC - The purpose of this report is to - The purpose of this report is to provide the department with school district annual report data that provide the department with school district annual report data that will be used in the October 15th certification of aid.will be used in the October 15th certification of aid.Due August 24Due August 24

Annual Report PI-1505Annual Report PI-1505 – This application collects complete year end – This application collects complete year end fiscal data for reporting, verification, and auditing purposes.fiscal data for reporting, verification, and auditing purposes.Due October 1Due October 1

Budget Report PI-1504Budget Report PI-1504 – This application collects budgeted fiscal – This application collects budgeted fiscal data for estimating general state aids. Per WI Stats. s. 65.90:Every data for estimating general state aids. Per WI Stats. s. 65.90:Every district annually must formulate a budget and hold public hearings district annually must formulate a budget and hold public hearings thereon.thereon.Due December 7

Tax Levies PC-401Tax Levies PC-401 - This application collects school district tax levy - This application collects school district tax levy information creates individual municipal tax certification pages, and information creates individual municipal tax certification pages, and reports information to both DPI and the Department of Revenue. reports information to both DPI and the Department of Revenue. Due October 26

Financial ReportsFinancial Reports

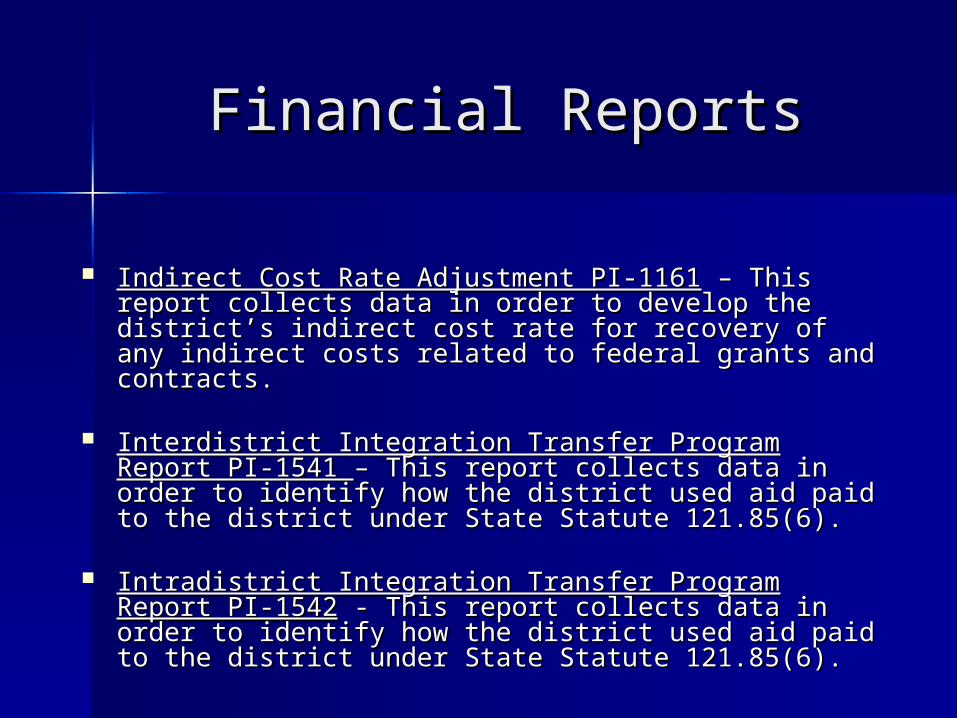

Indirect Cost Rate Adjustment PI-1161Indirect Cost Rate Adjustment PI-1161 – This report – This report collects data in order to develop the district’s indirect collects data in order to develop the district’s indirect cost rate for recovery of any indirect costs related to cost rate for recovery of any indirect costs related to federal grants and contracts.federal grants and contracts.

Interdistrict Integration Transfer Program Report PI-1541 Interdistrict Integration Transfer Program Report PI-1541 – This report collects data in order to identify how the – This report collects data in order to identify how the district used aid paid to the district under State Statute district used aid paid to the district under State Statute 121.85(6). 121.85(6).

Intradistrict Integration Transfer Program Report PI-1542Intradistrict Integration Transfer Program Report PI-1542 - This report collects data in order to identify how the - This report collects data in order to identify how the district used aid paid to the district under State Statute district used aid paid to the district under State Statute 121.85(6). 121.85(6).

Financial ReportsFinancial Reports

Sage Class Expansion Claim PI-7206 Sage Class Expansion Claim PI-7206 - This report - This report collects data from districts eligible to receive Sage aid collects data from districts eligible to receive Sage aid on debt service expenses.on debt service expenses.

Special Education Claim – Annual PI-1505 SESpecial Education Claim – Annual PI-1505 SE – This – This report collects year end special education fiscal data for report collects year end special education fiscal data for special education categorical aid eligibility.special education categorical aid eligibility.

Special Education Claim – Budget PI-1505 SESpecial Education Claim – Budget PI-1505 SE - This - This report collects budgeted special education fiscal data report collects budgeted special education fiscal data for estimating special education categorical aid for estimating special education categorical aid eligibility.eligibility.

State Tuition Claim Form PI-1524State Tuition Claim Form PI-1524 – This report collects – This report collects data needed to calculate state tuition payments to data needed to calculate state tuition payments to districts as per State Statute 121.79.districts as per State Statute 121.79.

BUDGET FINANCIAL BUDGET FINANCIAL REPORT (PI-1504)REPORT (PI-1504)

The School Finance Services team has The School Finance Services team has developed budget adoption worksheets developed budget adoption worksheets to assist the districtto assist the district

Budget Hearing and AdoptionBudget Hearing and Adoption

http://www.dpi.wi.gov/sfs/budhear.htmlhttp://www.dpi.wi.gov/sfs/budhear.html

Budget Development and Planning- Budget Development and Planning- Revenue Limit Executable Worksheet Revenue Limit Executable Worksheet

http://www.dpi.wi.gov/sfs/buddev.htmlhttp://www.dpi.wi.gov/sfs/buddev.html

PI-1505 ACPI-1505 AC““Aid Certification Data Aid Certification Data Form”Form”Two options available for filing PI-1505 AC via internetTwo options available for filing PI-1505 AC via internet

Manually enter PI-1505 AC dataManually enter PI-1505 AC data Load strip file to annual, complete the annual Load strip file to annual, complete the annual

before PI-1505AC due datebefore PI-1505AC due date School Finance reporting Portal SAFR School Finance reporting Portal SAFR

http://dpi.wi.gov/sfs/index.htmlhttp://dpi.wi.gov/sfs/index.html

Only selected data from full financial report necessary Only selected data from full financial report necessary to certify Equalized Aid on October 15to certify Equalized Aid on October 15

Only data Only data 43 lines – Most districts will use maybe 1543 lines – Most districts will use maybe 15

PI-1506 ACPI-1506 ACAuditor aid Auditor aid CertificationCertificationAuditor verifies the PI-1505 AC. Amounts Auditor verifies the PI-1505 AC. Amounts reported by auditors override PI 1505AC reported by auditors override PI 1505AC amounts.amounts.

Quick Audits created and Quick Audits created and posted to internetposted to internet

Due September 8Due September 8thth

PI-1506 verification of PI1505 SE and no PI-1506 verification of PI1505 SE and no valid license testing. Due September 15valid license testing. Due September 15thth

– Mail paper formMail paper form

SeptemberSeptember

– Preliminary Aid Estimate Preliminary Aid Estimate created and posted to created and posted to internetinternet

– PI 1506 AC site reopens for PI 1506 AC site reopens for auditors to amend data auditors to amend data through October 2ndthrough October 2nd

PI-1505PI-1505(Full Financial Annual (Full Financial Annual Report)Report)

Two options available for filing PI-1505 Two options available for filing PI-1505 via internetvia internet

Manually enter PI-1505 dataManually enter PI-1505 dataLoad strip file to annualLoad strip file to annualSchool Finance reporting Portal School Finance reporting Portal

SAFR SAFR http://dpi.wi.gov/sfs/index.htmlhttp://dpi.wi.gov/sfs/index.html

AUDITED FINANCIAL AUDITED FINANCIAL STATEMENTSSTATEMENTS

Filed by auditorFiled by auditorSchool District must have School District must have Fixed asset appraisals Fixed asset appraisals completed by June 30thcompleted by June 30th

Audits are Due Audits are Due December 1December 1stst

SPECIAL EDUCATION SPECIAL EDUCATION Budget and Annual (PI-1505 Budget and Annual (PI-1505 SE)SE)

• Fund 27Fund 27• Budget Special Education Budget Special Education

Claim (2006-2007)Claim (2006-2007)Due December 7, 2007Due December 7, 2007

• Annual Special Education Claim Annual Special Education Claim (PI-1505 SE)(PI-1505 SE)• Due September 3Due September 3stst 2007 2007

Non-Financial Data HomeNon-Financial Data Home

Non-Financial ReportsNon-Financial Reports

Pupil Count – Summer PI-1804/1805Pupil Count – Summer PI-1804/1805 – This application – This application collect pupil count data at the end of the summer collect pupil count data at the end of the summer preceding the regular school year. The district will preceding the regular school year. The district will receive membership credit in the aid and revenue limit receive membership credit in the aid and revenue limit calculations.calculations.

Pupil Count – September PI-1563Pupil Count – September PI-1563 – This application – This application collects pupil count data as of the third Friday in collects pupil count data as of the third Friday in September. The district will receive membership credit September. The district will receive membership credit in the aid and revenue limit calculations.in the aid and revenue limit calculations.

Pupil Count – January PI-1563Pupil Count – January PI-1563 - This application collects - This application collects pupil count data as of the second Friday in January. The pupil count data as of the second Friday in January. The district will receive membership credit in the aid district will receive membership credit in the aid calculation.calculation.

Non-Financial ReportsNon-Financial Reports Youth Challenge Academy PI 1563-YCAYouth Challenge Academy PI 1563-YCA – This – This

application collects pupil data on students attending the application collects pupil data on students attending the National Guard’s Challenge Academy at Fort McCoy. National Guard’s Challenge Academy at Fort McCoy. The district will receive membership credit in the aid The district will receive membership credit in the aid and revenue limit calculations. and revenue limit calculations.

Pupil Transportation PI-1547Pupil Transportation PI-1547 – This application collects – This application collects pupil data for transportation categorical aid eligibility.pupil data for transportation categorical aid eligibility.

School Calendar PI-1505 CalSchool Calendar PI-1505 Cal – This application collects – This application collects data on the district’s days of instruction and is used to data on the district’s days of instruction and is used to determine compliance with Wisconsin Statute determine compliance with Wisconsin Statute §121.006(2)(a). §121.006(2)(a).

School Census PI-1505 CensusSchool Census PI-1505 Census - This report collects - This report collects school census data as of June 30 for the purpose of school census data as of June 30 for the purpose of paying out Common School Library Aid to Wisconsin paying out Common School Library Aid to Wisconsin School Districts. School Districts.

PUPIL COUNTPUPIL COUNT

Primary purpose:Primary purpose:– Used to calculate FTE for Used to calculate FTE for

revenue limit and equalization revenue limit and equalization aidaid

– Wisconsin public school districts Wisconsin public school districts are required to undertake a 3rd are required to undertake a 3rd Friday in September and 2nd Friday in September and 2nd Friday in January pupil count and Friday in January pupil count and report them to the DPI.report them to the DPI.

PUPIL COUNTPUPIL COUNT

The School Finance Services team The School Finance Services team has developed a PI 1563 has developed a PI 1563 worksheetworksheet

Complete the worksheet prior to Complete the worksheet prior to entering the internet-based entering the internet-based reporting program. reporting program. Available at: Available at: http://www.dpi.wi.gov/sfs/membrpthttp://www.dpi.wi.gov/sfs/membrpt2.html2.html

PUPIL PUPIL TRANSPORTATIONTRANSPORTATION

Pupil Transportation AidPupil Transportation Aid

WI Statute 121.58WI Statute 121.58DPI pays DPI pays pupil transportation aidpupil transportation aid based on student based on student ridership for students who are ridership for students who are actually actually transportedtransported by the school district. Due August by the school district. Due August 1st1st

Aid paid at per pupil rate based on distance Aid paid at per pupil rate based on distance and days enrolledand days enrolled

School districts receive aid based on data School districts receive aid based on data submitted at school finance reporting submitted at school finance reporting portal:portal:– https://www2.dpi.state.wi.us/safr/https://www2.dpi.state.wi.us/safr/

Pupil Transportation Pupil Transportation (cont.)(cont.)

– Online transportation report Online transportation report filed with DPIfiled with DPI

Pupil Transportation Pupil Transportation (cont.)(cont.) Supporting documents:

– Listing which contains:Listing which contains: Pupils transported at least Pupils transported at least onceonce

Home to school distance per Home to school distance per pupilpupil

Days enrolled per pupilDays enrolled per pupil

ACCOUNTING ACCOUNTING TRANSACTIONSTRANSACTIONS

PROPERTY TAX LEVIESPROPERTY TAX LEVIES

LEVIES INTO FUND 10, 38, 39, 41, LEVIES INTO FUND 10, 38, 39, 41, 8080

THE TOTAL LEVY IS REVENUETHE TOTAL LEVY IS REVENUE– SOURCE 211 – CURRENT LEVYSOURCE 211 – CURRENT LEVY– SOURCE 212 – CHARGEBACK LEVY SOURCE 212 – CHARGEBACK LEVY

(FUND 10 ONLY)(FUND 10 ONLY) TAXES RECEIVABLE AT JUNE 30TAXES RECEIVABLE AT JUNE 30

PROPERTY TAX REFUNDSPROPERTY TAX REFUNDS

USUALLY PAYMENT TO MUNICIPALITY USUALLY PAYMENT TO MUNICIPALITY FOR UNCOLLECTED PERSONAL FOR UNCOLLECTED PERSONAL PROPERTY TAXESPROPERTY TAXES– FUND 10 FUNCTION 492 000 OBJECT 972FUND 10 FUNCTION 492 000 OBJECT 972(10 E 492 000 972)(10 E 492 000 972)

COLLECTION OF REFUNDCOLLECTION OF REFUND– FUND 10 SOURCE 972 (10 R 000 000 972)FUND 10 SOURCE 972 (10 R 000 000 972)

SOURCE 212 LEVY – NET PAYMENTSSOURCE 212 LEVY – NET PAYMENTS**– OPTIONALOPTIONAL– NOT NEGATIVENOT NEGATIVE

* NET OF OBJECT 972 MINUS SOURCE 972* NET OF OBJECT 972 MINUS SOURCE 972

PROPERTY TAX REFUNDS PROPERTY TAX REFUNDS (cont’d)(cont’d)

ONLY LEVY FOR UNCOLLECTED ONLY LEVY FOR UNCOLLECTED TAXES PAID OR HAVE BEEN TAXES PAID OR HAVE BEEN BILLED BY THE MUNICIPALITY BILLED BY THE MUNICIPALITY AND YOU INTEND TO PAY THEMAND YOU INTEND TO PAY THEM

OVER LEVY RESULTS IN TAXING OVER LEVY RESULTS IN TAXING WITHOUT PROPER WITHOUT PROPER AUTHORIZATIONAUTHORIZATION

Long-Term DebtLong-Term Debt

If used for acquiring capital If used for acquiring capital assets, receipted into Capital assets, receipted into Capital Projects Fund & expended out of Projects Fund & expended out of therethere

Capital items include buildings, Capital items include buildings, equipment, books equipment, books

General Fund? – highly unlikely but General Fund? – highly unlikely but can be used if for operational can be used if for operational purposes—must notify DPIpurposes—must notify DPI

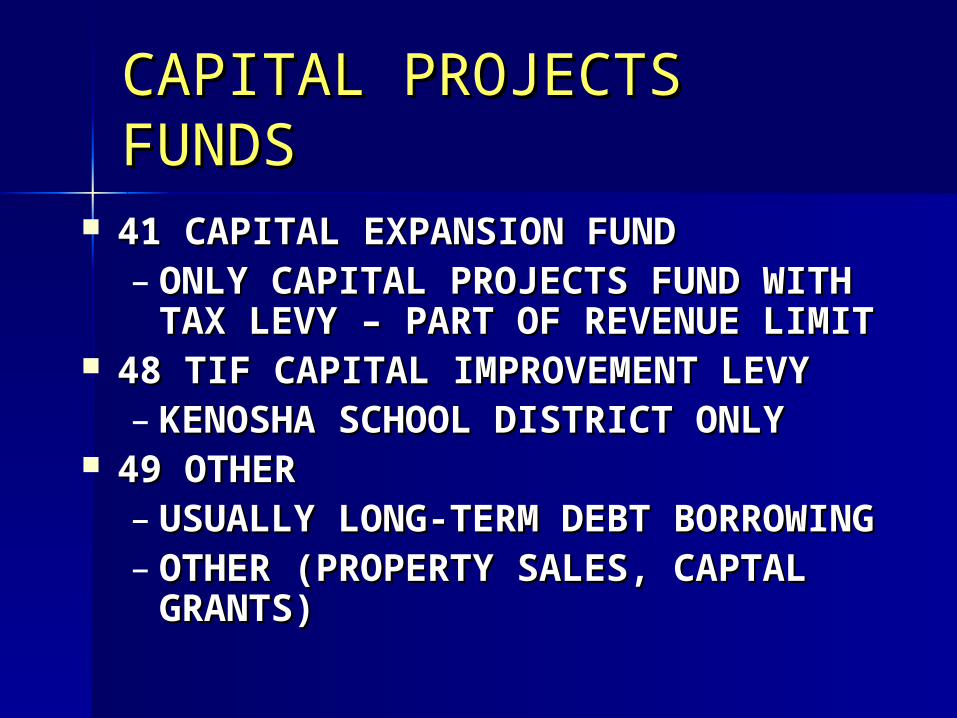

CAPITAL PROJECTS CAPITAL PROJECTS FUNDSFUNDS

41 CAPITAL EXPANSION FUND41 CAPITAL EXPANSION FUND– ONLY CAPITAL PROJECTS FUND ONLY CAPITAL PROJECTS FUND

WITH TAX LEVY – PART OF REVENUE WITH TAX LEVY – PART OF REVENUE LIMITLIMIT

48 TIF CAPITAL IMPROVEMENT LEVY48 TIF CAPITAL IMPROVEMENT LEVY– KENOSHA SCHOOL DISTRICT ONLYKENOSHA SCHOOL DISTRICT ONLY

49 OTHER49 OTHER– USUALLY LONG-TERM DEBT USUALLY LONG-TERM DEBT

BORROWINGBORROWING– OTHER (PROPERTY SALES, CAPTAL OTHER (PROPERTY SALES, CAPTAL

GRANTS)GRANTS)

DEBT SERVICE FUNDSDEBT SERVICE FUNDS

38 NON-REFERENDUM 38 NON-REFERENDUM DEBTDEBT– TAX LEVIES “TAX LEVIES “UNDERUNDER” ”

REVENUE LIMIT CAPREVENUE LIMIT CAP 39 OTHER DEBT39 OTHER DEBT

– TAX LEVIES “TAX LEVIES “OUTSIDEOUTSIDE” ” REVENUE LIMIT CAPREVENUE LIMIT CAP

““TEMPORARY” FUNDSTEMPORARY” FUNDS

CAPITAL PROJECTS CAPITAL PROJECTS WITH LONG-TERM DEBTWITH LONG-TERM DEBT

DEBT SERVICE FUND DEBT SERVICE FUND FOR PAYMENTS ON FOR PAYMENTS ON LONG-TERM DEBTLONG-TERM DEBT

DEBT TRANSACTIONSDEBT TRANSACTIONS

FOR EACH TYPE OF DEBT:FOR EACH TYPE OF DEBT:– BEGINNING BALANCE BEGINNING BALANCE PLUSPLUS– NEW DEBT INCURRED NEW DEBT INCURRED MINUSMINUS

– PRINCIPAL PAYMENTS PRINCIPAL PAYMENTS EQUALSEQUALS

– ENDING BALANCEENDING BALANCE

DEBT TRANSACTIONSDEBT TRANSACTIONS

LONG – TERM DEBT PROCEEDS LONG – TERM DEBT PROCEEDS GO INTO A FUND AS A GO INTO A FUND AS A “SOURCE”“SOURCE”

LONG – TERM DEBT PAYMENTS LONG – TERM DEBT PAYMENTS OUT OF A FUND AS AN OUT OF A FUND AS AN EXPENDITUREEXPENDITURE

CASH (TEMPORARY CASH (TEMPORARY BORROWING) GENERAL FUND BORROWING) GENERAL FUND BALANCE SHEETBALANCE SHEET

CASH FLOW BORROWINGCASH FLOW BORROWING

GENERAL FUND TRANSACTIONGENERAL FUND TRANSACTION– BALANCE SHEET TRANSACTION BALANCE SHEET TRANSACTION

FOR PRINCIPAL AMOUNTSFOR PRINCIPAL AMOUNTS– INTEREST EXPENSE – ACCRUAL AT INTEREST EXPENSE – ACCRUAL AT

JUNE 30JUNE 30 INTEREST REVENUEINTEREST REVENUE

– IN FUND PRODUCING INCOMEIN FUND PRODUCING INCOME– INTEREST RECEIVABLE AT JUNE 30 INTEREST RECEIVABLE AT JUNE 30

CASH FLOW BORROWING CASH FLOW BORROWING (cont’d)(cont’d)

Accounting transactions:Accounting transactions:– Dr. CashDr. Cash $1,000,000$1,000,000– Cr. Temporary Notes Payable Cr. Temporary Notes Payable

$1,000,000$1,000,000– (Acct. 10B 811 100)(Acct. 10B 811 100)

– Dr. Interest Expense $ 40,000Dr. Interest Expense $ 40,000– (10E 682 283 000)(10E 682 283 000)

– Cr. Interest Payable $ 40,000Cr. Interest Payable $ 40,000– (10B 811 700)(10B 811 700)

CAPITAL LEASECAPITAL LEASE

““BORROWING” FROM A VENDOR BORROWING” FROM A VENDOR TO ACQUIRE ITEMTO ACQUIRE ITEM

JOURNAL ENTRY TO RECORD JOURNAL ENTRY TO RECORD FINANCING TRANSACTION (Dr. FINANCING TRANSACTION (Dr. Capital Outlay and Cr. Source 878)Capital Outlay and Cr. Source 878)

PRINCIPAL AND INTEREST PRINCIPAL AND INTEREST PAYMENT TRANSACTIONS AS PAYMENT TRANSACTIONS AS PAYMENTS ARE MADE (Objects PAYMENTS ARE MADE (Objects 678/688; Function 281000)678/688; Function 281000)

BOND ANTICIPATION BOND ANTICIPATION NOTESNOTES OFTEN TAKEN OUT PRIOR TO OFTEN TAKEN OUT PRIOR TO

RECEIVING PROCEEDS OF RECEIVING PROCEEDS OF “PERMANENT” DEBT ISSUANCE“PERMANENT” DEBT ISSUANCE

WHEN RECEIVED CREDIT WHEN RECEIVED CREDIT “LOANS” SOURCE 873 – “LOANS” SOURCE 873 – CAPITAL PROJECTS FUNDCAPITAL PROJECTS FUND

INTEREST PAYMENTS ON BANS INTEREST PAYMENTS ON BANS – DEBT SERVICE FUND – – DEBT SERVICE FUND – TRANSFER IN OR LEVY TRANSFER IN OR LEVY

DEBT REFINANCINGDEBT REFINANCING

INCUR NEW DEBT AND USE INCUR NEW DEBT AND USE PROCEEDS TO “PAY OFF” PROCEEDS TO “PAY OFF” EXISTING DEBTEXISTING DEBT

““PAY OFF” MAY INCLUDE PAY OFF” MAY INCLUDE PAYMENT OF NEW DEBT PAYMENT OF NEW DEBT PROCEEDS TO ESCROW AGENTPROCEEDS TO ESCROW AGENT

TAKES PLACE IN DEBT SERVICE TAKES PLACE IN DEBT SERVICE FUNDFUND

CONTACT DPI FOR ASSISTANCE CONTACT DPI FOR ASSISTANCE WITH RECORDINGWITH RECORDING

TEACH PROGRAMTEACH PROGRAM

TEACH FUND (23) USEDTEACH FUND (23) USED FUND 93 IF COOPERATIVE FUND 93 IF COOPERATIVE

FISCAL AGENT – NOT COMMONFISCAL AGENT – NOT COMMON ACCOUNTS FOR ALL FUNDS ACCOUNTS FOR ALL FUNDS

RECEIVED FOR TEACH BOARDRECEIVED FOR TEACH BOARD– BLOCK GRANTBLOCK GRANT– LOANSLOANS

CAN HAVE A BALANCE OR CAN HAVE A BALANCE OR DEFICITDEFICIT

TEACH PROGRAM TEACH PROGRAM LOANSLOANS

TRACK THE CASHTRACK THE CASH PROCEEDS IN TO FUND 23PROCEEDS IN TO FUND 23 REPAYMENT OF LOANS FROM REPAYMENT OF LOANS FROM

FUNDING SOURCE DISTRICT WISHES FUNDING SOURCE DISTRICT WISHES TO USE – FUND 10 OR 23TO USE – FUND 10 OR 23– DEBT SERVICE FUND ONLY LOAN TAKEN DEBT SERVICE FUND ONLY LOAN TAKEN

OUT AS GENERAL OBLIGATION DEBT – OUT AS GENERAL OBLIGATION DEBT – RARERARE

DISTRICT PAYMENT GETS CODED AS DISTRICT PAYMENT GETS CODED AS EXPENDITUREEXPENDITURE

STATE MATCHES ANNUAL PRINCIPAL STATE MATCHES ANNUAL PRINCIPAL PAYMENT PAYMENT

UNSETTLED EMPLOYEE UNSETTLED EMPLOYEE CONTRACTSCONTRACTS

IF UNSETTLED WHEN FILING IF UNSETTLED WHEN FILING REPORT– NO ADDITIONAL COST REPORT– NO ADDITIONAL COST RECORDEDRECORDED

IF SETTLEMENT OCCURS AFTER IF SETTLEMENT OCCURS AFTER FILING REPORT BUT BEFORE FILING REPORT BUT BEFORE OCTOBER 1, AMEND REPORT TO OCTOBER 1, AMEND REPORT TO SHOW INCREASED COSTSHOW INCREASED COST

SETTLEMENT AFTER OCTOBER 1 – SETTLEMENT AFTER OCTOBER 1 – COST OF YEAR SETTLEMENT OCCURS COST OF YEAR SETTLEMENT OCCURS ININ

PAYROLL ITEMSPAYROLL ITEMS

ACCRUAL AT JUNE 30 FOR ACCRUAL AT JUNE 30 FOR EMPLOYEE SERVICES PROVIDEDEMPLOYEE SERVICES PROVIDED– SALARIESSALARIES– RELATED BENEFITSRELATED BENEFITS– INCLUDES “SUMMER PAYROLLS”INCLUDES “SUMMER PAYROLLS”

NO ACCRUAL FOR POST-NO ACCRUAL FOR POST-EMPLOYMENT BENEFITSEMPLOYMENT BENEFITS

SPECIFIC RULES FOR SPECIFIC RULES FOR UNSETTLED CONTRACTSUNSETTLED CONTRACTS

SELF FUND HEALTH SELF FUND HEALTH BENEFITSBENEFITS DISTRICT SELF FUNDS DISTRICT SELF FUNDS

HEALTH/DENTAL BENEFITSHEALTH/DENTAL BENEFITS PRIVATE PLAN ADMINISTRATOR PRIVATE PLAN ADMINISTRATOR

USUALLY INVOLVEDUSUALLY INVOLVED PREMIUM EQUIVALANCY USED PREMIUM EQUIVALANCY USED

FOR BUDGETING/COSTINGFOR BUDGETING/COSTING FINAL REPORTED EXPENDITURES FINAL REPORTED EXPENDITURES

MUST BE ACTUAL COST FOR MUST BE ACTUAL COST FOR FISCAL YEAR – INCLUDING INBNR FISCAL YEAR – INCLUDING INBNR COSTS COSTS

SELF-FUNDED HEALTH SELF-FUNDED HEALTH BENEFITSBENEFITS

SERIES OF GENERAL FUND SERIES OF GENERAL FUND BALANCE SHEETS ACT AS BALANCE SHEETS ACT AS “INSURANCE COMPANY”“INSURANCE COMPANY”

LIABILITY ACCOUNT VS LIABILITY ACCOUNT VS RESERVED FUND BALANCERESERVED FUND BALANCE

5% ADJUSTMENT ACCOUNT 5% ADJUSTMENT ACCOUNT – SOURCE/OBJECT 965SOURCE/OBJECT 965

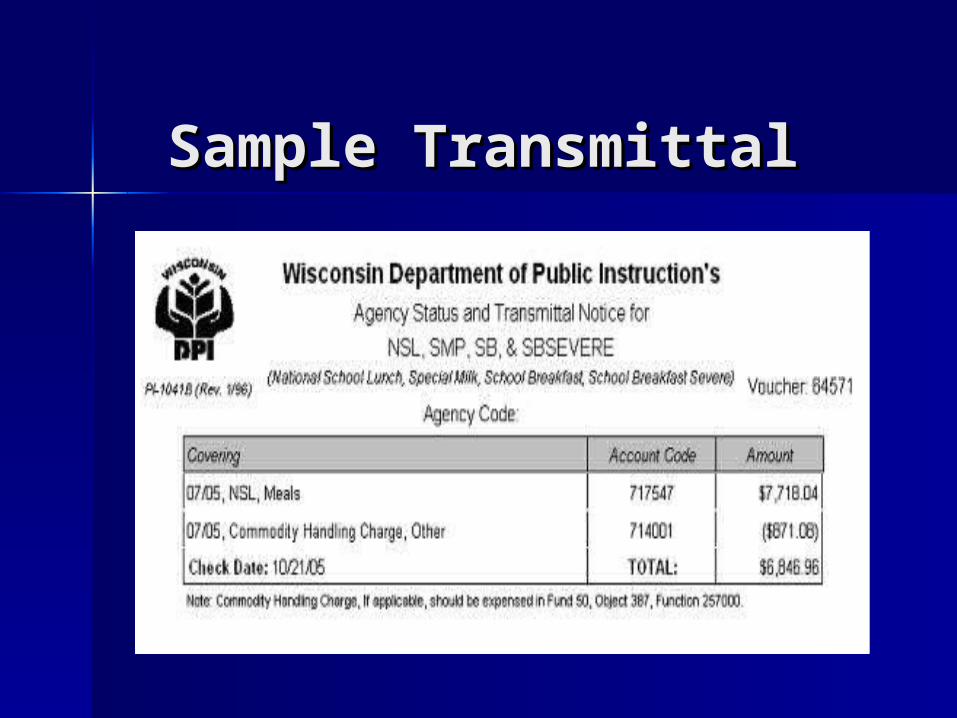

COMMODITY COMMODITY HANDLING CHARGESHANDLING CHARGES

New in fiscal 04-05New in fiscal 04-05 Handling charges for commodities will Handling charges for commodities will

be subtracted from federal food be subtracted from federal food service aid paymentsservice aid payments

District must report the gross federal District must report the gross federal revenue (Source 700s)revenue (Source 700s)

Handling charges are recorded as Handling charges are recorded as Object 387 Function 257 000Object 387 Function 257 000

Handling charges will be identified on Handling charges will be identified on Aids Register as a negative amountAids Register as a negative amount

Sample TransmittalSample Transmittal

Internet Reporting Internet Reporting

Referenda ReportingReferenda ReportingLong-Term Debt ReportingLong-Term Debt Reporting

Reporting Upcoming Reporting Upcoming Referenda and ResultsReferenda and Results

Districts notify DPI of upcoming Districts notify DPI of upcoming referendum within 10 days of referendum within 10 days of resolution adoptionresolution adoption

Reporting via DPI portalReporting via DPI portal https://www2.dpi.state.wi.us/safr/https://www2.dpi.state.wi.us/safr/ Forms PI 1572-A and PI 1572-B Forms PI 1572-A and PI 1572-B

are no longer in paper formare no longer in paper form

Reporting Upcoming Reporting Upcoming Referenda and Results Referenda and Results

(cont’d)(cont’d)

Reporting Upcoming Reporting Upcoming Referenda and Results Referenda and Results

(cont’d)(cont’d)

Click to add details for upcoming referendum

Reporting Upcoming Reporting Upcoming Referenda and Results Referenda and Results

(cont’d)(cont’d) Information required is same as what Information required is same as what

was requested on paper Form PI 1572was requested on paper Form PI 1572

--District contact--District contact

--Purpose of borrowing or use of --Purpose of borrowing or use of revenue limit dollarsrevenue limit dollars

--Actual wording of resolution --Actual wording of resolution questionquestion

--Actual results of election --Actual results of election

Reporting Upcoming Reporting Upcoming Referenda and Results Referenda and Results

(cont’d)(cont’d) Debt referendum: Dollar amount of Debt referendum: Dollar amount of

proposed borrowingproposed borrowing Revenue limit referendum: Dollar Revenue limit referendum: Dollar

amount of increases in revenue limit amount of increases in revenue limit authority and years involvedauthority and years involved--Recurring exemption: no end year--Recurring exemption: no end year--Non recurring exemption: must list --Non recurring exemption: must list start and stop years and amounts for start and stop years and amounts for all yearsall years

Reporting Upcoming Reporting Upcoming Referenda and Results Referenda and Results

(cont’d)(cont’d)

Reporting Upcoming Reporting Upcoming Referenda and Results Referenda and Results

(cont’d)(cont’d)

Referenda filing Referenda filing requirementsrequirements Copy of adopted resolution Copy of adopted resolution

authorizing electionauthorizing election Copy of board of canvassers Copy of board of canvassers

statement which reports official vote statement which reports official vote tallytally

Due at DPI within 10 days of electionDue at DPI within 10 days of election Can be faxed to Gene Fornecker, Can be faxed to Gene Fornecker,

608/266-2840 or mailed608/266-2840 or mailed

Referenda StatisticsReferenda Statistics

Users can access from our Users can access from our database listings of referenda database listings of referenda that have passed or failed for that have passed or failed for both debt and revenue limit both debt and revenue limit questionsquestions

Data can be downloaded into Data can be downloaded into EXCEL for statistical analysis EXCEL for statistical analysis purposespurposes

https://www2.dpi.state.wi.us/safr/https://www2.dpi.state.wi.us/safr/all_referenda.aspall_referenda.asp

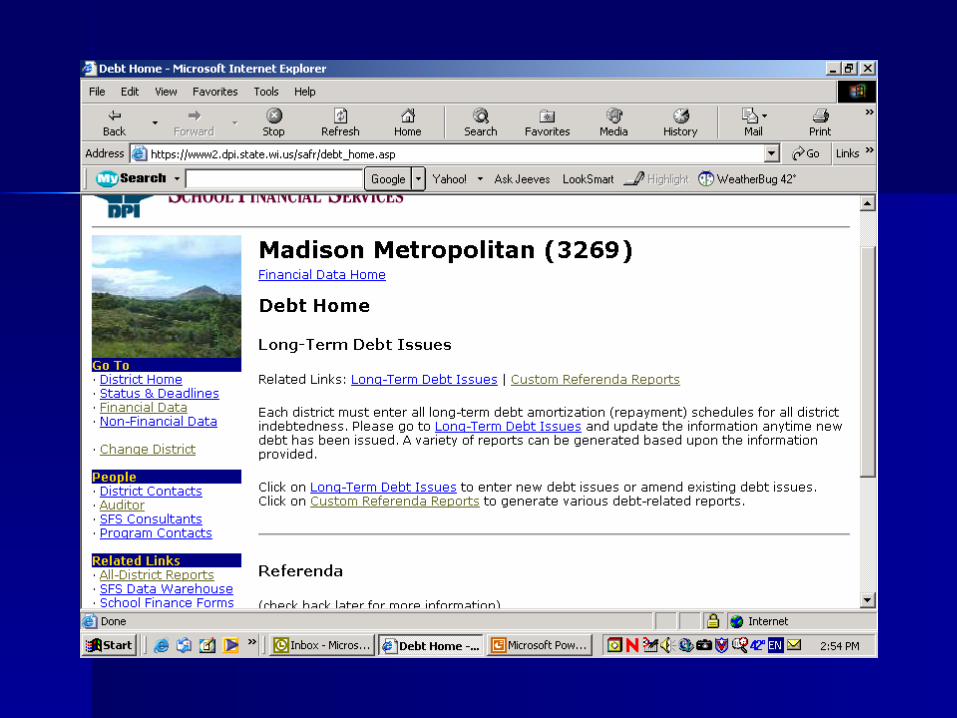

Reporting District Long-Reporting District Long-Term DebtTerm Debt

Districts are now required to notify Districts are now required to notify DPI via the reporting portal any DPI via the reporting portal any changes in their long-term debt changes in their long-term debt repayment schedulesrepayment schedules

Prepayments of principal, Prepayments of principal, refinancings, new loans will require refinancings, new loans will require adjustments by districtadjustments by district

Updating of online debt schedules can Updating of online debt schedules can be done at any time during the yearbe done at any time during the year

Reporting District Long-Reporting District Long-Term DebtTerm Debt

Debt amortization schedules must Debt amortization schedules must be entered as part of Annual be entered as part of Annual Report submission process if not Report submission process if not updated previouslyupdated previously

Reporting via DPI portalReporting via DPI portal https://www2.dpi.state.wi.us/safr/https://www2.dpi.state.wi.us/safr/

Reporting District Long-Reporting District Long-Term DebtTerm Debt The district’s Annual Report has built The district’s Annual Report has built

in edits to check the following:in edits to check the following:– 08B debt balances at beginning and end 08B debt balances at beginning and end

of yearof year– Function 281000, 283000, 285000, Function 281000, 283000, 285000,

289000 principal and interest amounts 289000 principal and interest amounts agree to debt schedulesagree to debt schedules

– New debt proceeds will be verified New debt proceeds will be verified against referenda database if Fund 39 against referenda database if Fund 39 debtdebt

Questions?Questions?

SPECIAL EDUCATION SPECIAL EDUCATION FUND 27FUND 27

SPECIAL EDUCATIONSPECIAL EDUCATION SOME BASIC PRINCIPLESSOME BASIC PRINCIPLES::

COSTS OF PROVIDING SPECIAL EDUCATION AND COSTS OF PROVIDING SPECIAL EDUCATION AND RELATED SERVICES RELATED SERVICES

COSTS FUNDED BY A COMBINATION OF STATE, COSTS FUNDED BY A COMBINATION OF STATE, LOCAL AND FEDERAL DOLLARSLOCAL AND FEDERAL DOLLARS

ALL EXPENDITURES AND RELATED REVENUE ALL EXPENDITURES AND RELATED REVENUE ACCOUNTED FOR IN FUND 27ACCOUNTED FOR IN FUND 27

CONSOLIDATES STATE, FEDERAL AND LOCAL CONSOLIDATES STATE, FEDERAL AND LOCAL SPECIAL EDUCATION ACCOUNTING IN ONE FUNDSPECIAL EDUCATION ACCOUNTING IN ONE FUND

SPECIAL EDUCATION SPECIAL EDUCATION ACCOUNTINGACCOUNTING

SPECIAL EDUCATION FUND (FUND SPECIAL EDUCATION FUND (FUND 27) ALWAYS CLOSED OUT WITH A 27) ALWAYS CLOSED OUT WITH A TRANSFER FROM THE DISTRICT’S TRANSFER FROM THE DISTRICT’S GENERAL FUNDGENERAL FUND

REPRESENTS “BOTTOM LINE” COST REPRESENTS “BOTTOM LINE” COST OF SPECIAL EDUCATION AND OF SPECIAL EDUCATION AND RELATED SERVICES TO DISTRICTRELATED SERVICES TO DISTRICT

SPECIAL EDUCATION SPECIAL EDUCATION PROGRAMSPROGRAMS

PROGRAM OPERATED BY THE DISTRICT PROGRAM OPERATED BY THE DISTRICT (DISTRICT EMPLOYS PERSONNEL)(DISTRICT EMPLOYS PERSONNEL)

PROGRAM OPERATED WITH A PROGRAM OPERATED WITH A CONSORTIUM OF SCHOOLCONSORTIUM OF SCHOOL

PROGRAM OPERATED BY CESAPROGRAM OPERATED BY CESA

PROGRAM OPERATED BY CCDEBPROGRAM OPERATED BY CCDEB

SPECIAL EDUCATION SPECIAL EDUCATION CLAIMCLAIM

STATE SPECIAL EDUCATION STATE SPECIAL EDUCATION CATEGORICAL AID BASED ON:CATEGORICAL AID BASED ON:–REPORT FILED WITH DPI VIA DATA REPORT FILED WITH DPI VIA DATA FILE (E-MAIL)FILE (E-MAIL)BUDGET REPORT - NOVEMBERBUDGET REPORT - NOVEMBERANNUAL REPORT - SEPTEMBERANNUAL REPORT - SEPTEMBER

SPECIAL EDUCATION SPECIAL EDUCATION ACCOUNT CODING ACCOUNT CODING (Cont.)(Cont.)

PROJECT CODES USED TO IDENTIFY PROJECT CODES USED TO IDENTIFY HOW EXPENDITURES ARE FUNDEDHOW EXPENDITURES ARE FUNDED

STATE CATEGORICAL AIDSTATE CATEGORICAL AIDGRANT PROGRAM AIDEDGRANT PROGRAM AIDEDCHARGED TO CESA FOR PACKAGE CHARGED TO CESA FOR PACKAGE PROGRAM EXPENSESPROGRAM EXPENSES

NONE OF THE ABOVENONE OF THE ABOVE

SPECIAL EDUCATION SPECIAL EDUCATION ACCOUNT CODINGACCOUNT CODINGhttp://http://www.dpi.wi.gov/sfs/speced.htmlwww.dpi.wi.gov/sfs/speced.html

MEDICAID “SBS” MEDICAID “SBS” SERVICESSERVICES

PROVIDED TO CHILDREN WITH PROVIDED TO CHILDREN WITH DISABILITIES (SPECIAL EDUCATION)DISABILITIES (SPECIAL EDUCATION)

COST IN SPECIAL EDUCATION FUND (27)COST IN SPECIAL EDUCATION FUND (27)

REVENUE IN GENERAL FUND (10)REVENUE IN GENERAL FUND (10)

CANNOT CHARGE MEDICAID COSTS CANNOT CHARGE MEDICAID COSTS AGAINST FEDERAL GRANT FUNDSAGAINST FEDERAL GRANT FUNDS

NOT A DEDUCTIBLE FOR STATE NOT A DEDUCTIBLE FOR STATE CATEGORICAL SPECIAL ED CATEGORICAL SPECIAL ED

PSYCHOLOGISTS/SOCIAL PSYCHOLOGISTS/SOCIAL WORKERS/NURSES/COUNSELOWORKERS/NURSES/COUNSELORSRS

MUST BE EMPLOYED NOT CONTRACTEDMUST BE EMPLOYED NOT CONTRACTED ONLY PORTION OF TIME RESPONSIBLE ONLY PORTION OF TIME RESPONSIBLE

FOR SPECIAL EDUCATIONFOR SPECIAL EDUCATION METHODS USED FOR ALLOCATIONMETHODS USED FOR ALLOCATION TYPES OF ACTIVITIES ELIGIBLE FOR TYPES OF ACTIVITIES ELIGIBLE FOR

SPECIAL EDUCATION AIDSPECIAL EDUCATION AID http://www.dpi.wi.gov/sfs/ltrjan12_0http://www.dpi.wi.gov/sfs/ltrjan12_0

6.html6.html

COOPERATIVE COOPERATIVE AGREEMENT AGREEMENT

66.030166.0301

Please attend Thursday Please attend Thursday session regarding session regarding Special Education Special Education

programprogram

Thanks & Thanks & Good LuckGood Luck

QUESTIONS?QUESTIONS?

School Finance AuditorsSchool Finance Auditors

Kathy Guralski - (608) 266-3862Kathy Guralski - (608) [email protected]@dpi.state.wi.us

Natalie Rew - (608) 267-9212Natalie Rew - (608) [email protected]@dpi.state.wi.us

Gene Fornecker - (608) 267-Gene Fornecker - (608) 267-78827882