11. financial information

TRANSCRIPT

257

Registration No.: 199601027709 (400061-H)

11. FINANCIAL INFORMATION

Registration No.: 199601027709 (400061-H)

11.1 HISTORICAL CONSOLIDATED FINANCIAL INFORMATION

The historical audited consolidated financial information of our Group for the FYE 2018 to 2020 have been extracted from the Accountants’ Report set out in Section 12 of this Prospectus, which deals with the audited consolidated financial statements of our Group for the same Financial Years Under Review. You should read the historical audited consolidated financial information below together with:

• Management’s Discussion and Analysis of Financial Condition and Results of

Operations set out in Section 11.2 of this Prospectus; and • Accountants’ Report set out in Section 12 of this Prospectus.

(a) Historical consolidated statements of profit or loss and other comprehensive

income

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 RM’000 RM’000 Revenue 142,356 128,725 132,952 Less: Cost of sales (113,500) (104,425) (93,867) GP 28,856 24,300 39,085 Other income 369 525 514 Administrative expenses (9,609) (13,456) (11,777) Finance costs (1,203) (1,412) (1,840) PBT 18,413 9,957 25,982 Taxation (6,344) (2,135) (7,053) Profit for the financial year, representing total comprehensive income for the financial year

12,069 7,822 18,929

Profit/(Loss) attributable to: Owners of the parent 3,081 7,822 18,935 Non-controlling interests 8,988 - (7) (6) RCPS dividends payable/paid(1) - 88 15,252 Number of shares in issue (‘000)(2) 35,000 35,000 35,000 Depreciation and amortisation (RM’000) 708 1,162 2,014 Basic and diluted EPS (sen)(3) 0.09 0.22 0.11 Key financial ratios GP margin (%)(4) 20.27 18.88 29.40 PBT margin (%)(5) 12.93 7.74 19.54 PAT margin (%)(6) 8.48 6.08 14.24 Effective tax rate(%)

34.45 21.44 27.15

258

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION (Cont’d)

Notes:

(1) Dividends were paid to RCPS holders via internal generated funds. The remaining outstanding dividends payable to RCPS holders will be paid out by the end of 2021 via internal generated funds. The RCPS were fully converted as at the LPD.

(2) The number of ordinary shares.

(3) Basic EPS is calculated based on the consolidated profit for the financial year attributable to the owners of the parent and the weighted average number of shares in issue.

(4) Based on GP divided by revenue.

(5) Based on PBT divided by revenue.

(6) Based on PAT divided by revenue.

(7) Negligible.

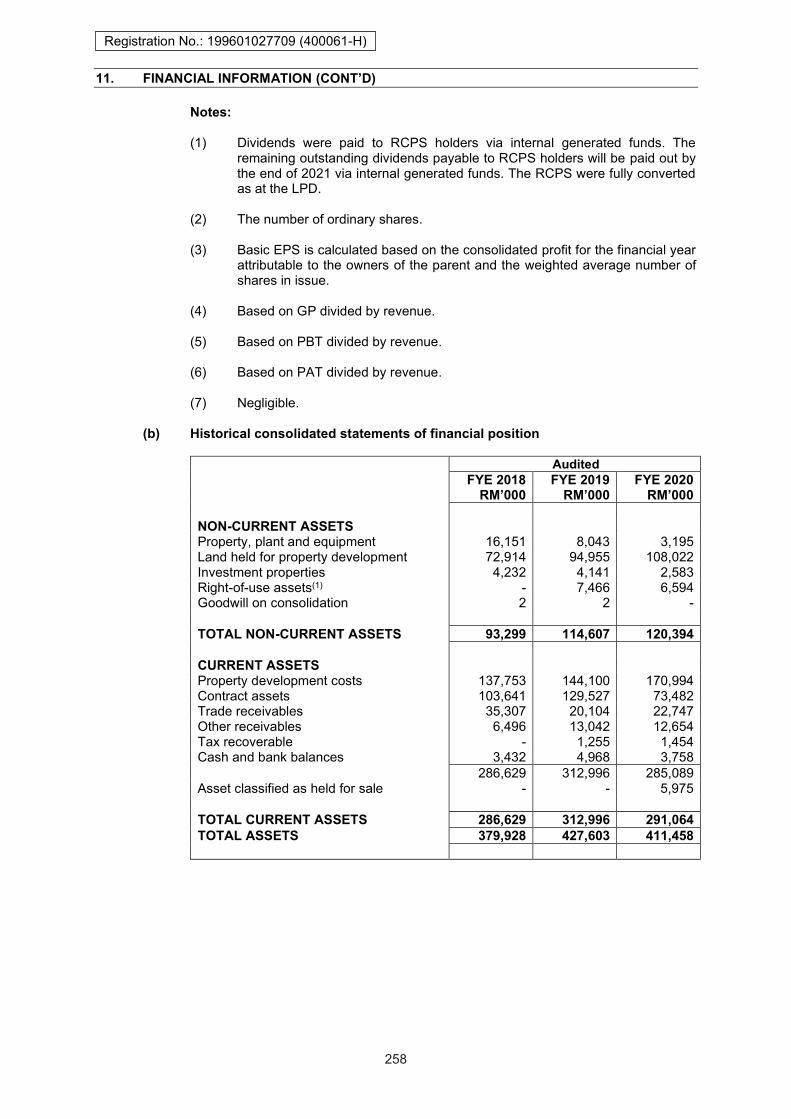

(b) Historical consolidated statements of financial position

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 RM’000 RM’000 NON-CURRENT ASSETS Property, plant and equipment 16,151 8,043 3,195 Land held for property development 72,914 94,955 108,022 Investment properties 4,232 4,141 2,583 Right-of-use assets(1) - 7,466 6,594 Goodwill on consolidation 2 2 - TOTAL NON-CURRENT ASSETS 93,299 114,607 120,394 CURRENT ASSETS Property development costs 137,753 144,100 170,994 Contract assets 103,641 129,527 73,482 Trade receivables 35,307 20,104 22,747 Other receivables 6,496 13,042 12,654 Tax recoverable - 1,255 1,454 Cash and bank balances 3,432 4,968 3,758 286,629 312,996 285,089 Asset classified as held for sale - - 5,975 TOTAL CURRENT ASSETS 286,629 312,996 291,064 TOTAL ASSETS 379,928 427,603 411,458

259

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION

Registration No.: 199601027709 (400061-H)

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 RM’000 RM’000 EQUITY AND LIABILITIES Share capital 35,000 35,000 35,000 RCPS 56,640 66,640 67,640 Retained earnings 21,106 15,550 19,233 Equity attributable to owners of the Company

112,746 117,190 121,873

Non-controlling interests 16,730 2 1,194 TOTAL EQUITY 129,476 117,192 123,067 NON-CURRENT LIABILITIES Finance lease liability 50 - - Lease liabilities - 1,014 1,057 Borrowings 40,767 94,313 32,769 Deferred tax liabilities 44 74 23 Other payables 6,657 7,190 7,765 TOTAL NON-CURRENT LIABILITIES 47,518 102,591 41,614 CURRENT LIABILITIES Trade payables 74,995 95,990 121,413 Other payables 28,960 43,003 50,281 Tax payable 9,933 10,035 15,626 Finance lease liability 21 - - Lease liabilities(1) - 283 411 Borrowings 89,025 58,509 59,046 TOTAL CURRENT LIABILITIES 202,934 207,820 246,777 TOTAL LIABILITIES 250,452 310,411 288,391 TOTAL EQUITY AND LIABILITIES 379,928 427,603 411,458 NA (RM’000) 129,476 117,192 123,067 NA per share (RM) 3.70 3.35 3.52

260

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION

Registration No.: 199601027709 (400061-H)

Note:

(1) Our Group had adopted MFRS 16 Leases using the modified retrospective approach effective in 1 January 2019. In accordance with the transition requirements under the Appendix C, paragraph 5(b) of this standard, comparatives are not restated. Our Group leases commercial properties and acquired motor vehicles through hire purchases arrangement which make up its rights-of-use assets, and the corresponding leases of the commercial properties make up its lease liabilities.

261

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

261

Registration No.: 199601027709 (400061-H)

(c) Historical consolidated statements of cash flows

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 RM’000 RM’000 CASH FLOWS FROM OPERATING ACTIVITIES

PBT 18,413 9,957 25,982 Adjustments for: Amortisation of right-of-use-assets - 452 1,311 Depreciation of investment properties 109 91 60 Depreciation of property, plant and equipment

598 619 643

Gain on disposal of investment in subsidiary companies

- - (19)

Gain on disposal of property, plant and equipment

- (88) -

Gain on disposal of right-of-use assets

- (124) -

Goodwill on consolidation written off - 7 2 Interest expense 1,203 1,413 1,840 Interest income (8) (8) (4) Rent concession related to COVID-19 - - (8) Operating profit before working capital changes

20,315 12,319 29,807

Changes in working capital: Property development costs (3,151) 15,243 3,004 Trade and other receivables (18,380) 8,657 (2,254) Trade and other payables 63,132 35,032 17,555 Contract assets (103,641) (25,886) 56,045 (62,040) 33,046 74,350 Cash (used in)/from operations (41,725) 45,365 104,157 Interest received 8 8 4 Interest paid (6,457) (11,465) (8,517) Tax paid (838) (3,258) (1,713) (7,287) (14,715) (10,226) NET CASH (USED IN)/FROM OPERATING ACTIVITIES

(49,012) 30,650 93,931

262

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

262

Registration No.: 199601027709 (400061-H)

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 RM’000 RM’000 CASH FLOWS FROM INVESTING ACTIVITIES

Acquisition of non-controlling interests

- (30,000) -

Acquisition of subsidiary companies, net of cash acquired

4 - -

Additions to land held for property development

(69,796) (33,045) (35,714)

Additions of right-of-use assets - (1,863) - Purchase of property, plant and equipment

(1,928) (40) (271)

Proceeds from disposal of property, plant and equipment

- 88 -

Proceeds from disposal of right-of-use assets

- 3,150 -

Proceeds from partial disposal of a subsidiary company

- 2 1,198

Withdrawn deposit with licensed bank for fixed deposits pledged

20 - -

NET CASH USED IN INVESTING ACTIVITIES

(71,700) (61,708) (34,787)

CASH FLOWS FROM FINANCING ACTIVITIES

Drawdown of term loans 92,056 30,585 26,960 Repayment of term loans (1,378) (7,555) (92,967) Repayment of lease liabilities - (348) (259) Repayment of finance lease liability (20) - - RCPS dividends paid - (88) (88) Placement of deposit in Escrow Accounts

(2,331) - (511)

Proceeds from issuance of RCPS 33,240 10,000 1,000 NET CASH FROM/(USED IN) FINANCING ACTIVITIES

121,567 32,594 (65,865)

Net increase/(decrease) in cash and cash equivalents

855 1,536 (6,721)

Cash and cash equivalents at the beginning of the financial year

244 1,099 2,635

Cash and cash equivalents at the end of the financial year

1,099 2,635 (4,086)

263

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION

Registration No.: 199601027709 (400061-H)

11.2 MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS The following discussion and segmental analysis of our consolidated financial statements for FYE 2018 to 2020 should be read with the Accountants’ Report included in Section 12 of this Prospectus.

11.2.1 Overview of our business operations We are principally involved in property development. For the past Financial Years Under Review and as at the LPD, our Group’s portfolio of development projects were high-rise residential and mixed-use development projects. Please refer to Section 5.5 of this Prospectus for further information on our business activities. Since our commencement in property development activities, our strategy has been to focus on a small number of development projects at any one point in time. By focusing on a small number of development projects at a time, we are able to manage our costs and financial resources as well as focus our marketing activities on the said development projects to fully reap our return on investments for each project. As a testament, we have successfully sold all of our completed projects. Further, we have also fully sold all of our units under the Residensi Hektar Project and the flexi-suites in the GrenePark Village Project (Phase 1), as at the LPD. Please refer to Section 5.5.1.2(i) and Section 5.5.2.3 of this Prospectus for further information on the percentage of units sold for our development projects as at the LPD.

11.2.2 Overview of our financial results We specialise in property development and thus our Group’s revenue is mainly derived from the sale of our developments. As we have fully sold all of our completed projects as at the LPD, the revenues generated during the Financial Years Under Review were from the sale of on-going development projects. Our on-going development projects include the Residensi Hektar Project and GrenePark Village Project, which are high-rise residential and mixed-use developments. There were 2,400 condominium units under the Residential Hektar Project that were launched in 2018 and we have fully sold all units under the project as at the LPD. Parts of Phase 1 and Phase 2 of the GrenePark Village Project were launched, i.e.: • 254 units of flexi suites under Phase 1 were launched in FYE 2019;

• 294 units of SOHOs under Phase 1 were launched in FYE 2021;

• 188 units of SOHOs under Phase 2 were launched in FYE 2021; of which a total of 291 units were sold as at the LPD.

264

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

264

Registration No.: 199601027709 (400061-H)

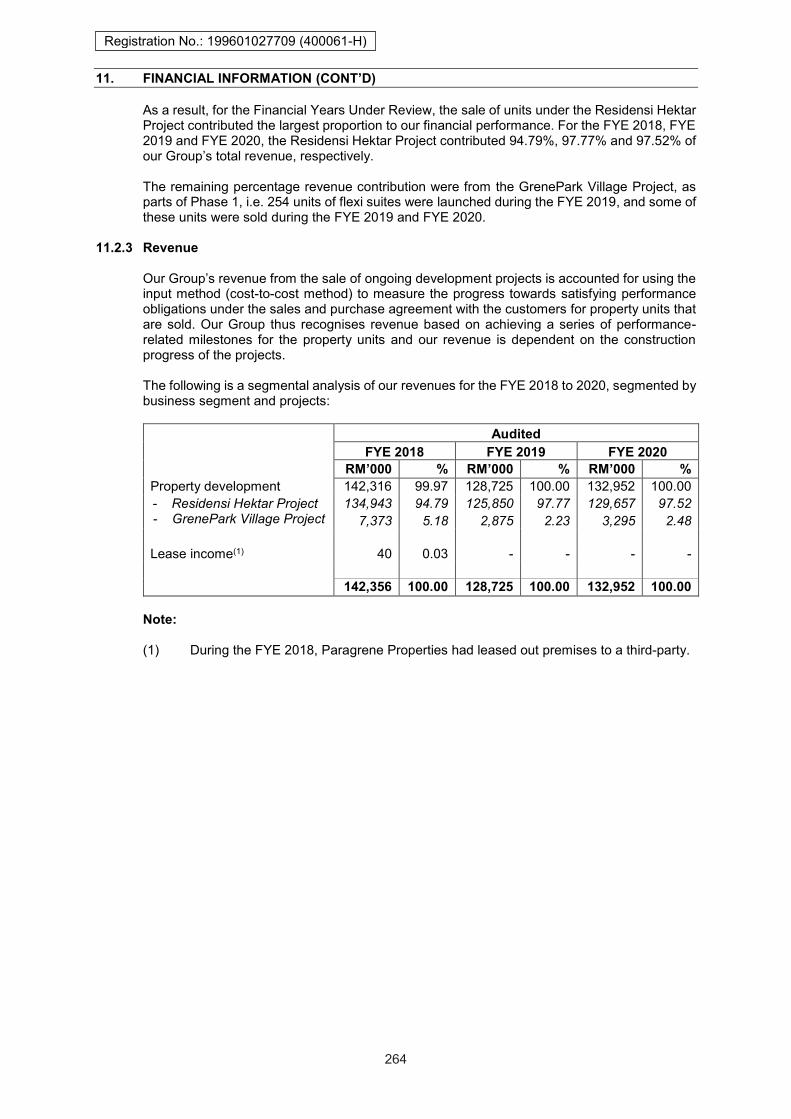

As a result, for the Financial Years Under Review, the sale of units under the Residensi Hektar Project contributed the largest proportion to our financial performance. For the FYE 2018, FYE 2019 and FYE 2020, the Residensi Hektar Project contributed 94.79%, 97.77% and 97.52% of our Group’s total revenue, respectively. The remaining percentage revenue contribution were from the GrenePark Village Project, as parts of Phase 1, i.e. 254 units of flexi suites were launched during the FYE 2019, and some of these units were sold during the FYE 2019 and FYE 2020.

11.2.3 Revenue

Our Group’s revenue from the sale of ongoing development projects is accounted for using the input method (cost-to-cost method) to measure the progress towards satisfying performance obligations under the sales and purchase agreement with the customers for property units that are sold. Our Group thus recognises revenue based on achieving a series of performance-related milestones for the property units and our revenue is dependent on the construction progress of the projects. The following is a segmental analysis of our revenues for the FYE 2018 to 2020, segmented by business segment and projects:

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 % RM’000 % RM’000 % Property development 142,316 99.97 128,725 100.00 132,952 100.00 - Residensi Hektar Project 134,943 94.79 125,850 97.77 129,657 97.52 - GrenePark Village Project 7,373 5.18 2,875 2.23 3,295 2.48 Lease income(1) 40 0.03 - - - - 142,356 100.00 128,725 100.00 132,952 100.00

Note:

(1) During the FYE 2018, Paragrene Properties had leased out premises to a third-party.

265

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

265

Registration No.: 199601027709 (400061-H)

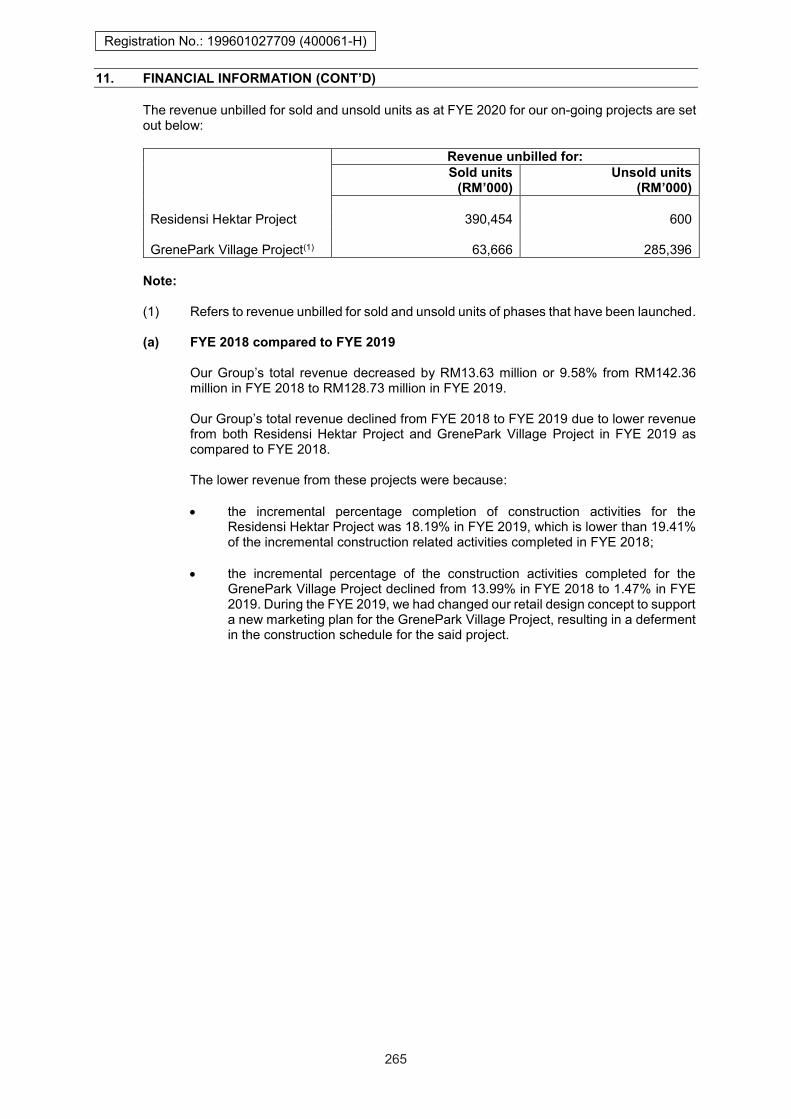

The revenue unbilled for sold and unsold units as at FYE 2020 for our on-going projects are set out below:

Revenue unbilled for: Sold units Unsold units (RM’000) (RM’000) Residensi Hektar Project 390,454 600 GrenePark Village Project(1) 63,666 285,396

Note:

(1) Refers to revenue unbilled for sold and unsold units of phases that have been launched.

(a) FYE 2018 compared to FYE 2019

Our Group’s total revenue decreased by RM13.63 million or 9.58% from RM142.36 million in FYE 2018 to RM128.73 million in FYE 2019. Our Group’s total revenue declined from FYE 2018 to FYE 2019 due to lower revenue from both Residensi Hektar Project and GrenePark Village Project in FYE 2019 as compared to FYE 2018.

The lower revenue from these projects were because:

the incremental percentage completion of construction activities for the

Residensi Hektar Project was 18.19% in FYE 2019, which is lower than 19.41% of the incremental construction related activities completed in FYE 2018;

the incremental percentage of the construction activities completed for the

GrenePark Village Project declined from 13.99% in FYE 2018 to 1.47% in FYE 2019. During the FYE 2019, we had changed our retail design concept to support a new marketing plan for the GrenePark Village Project, resulting in a deferment in the construction schedule for the said project.

266

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION

Registration No.: 199601027709 (400061-H)

(b) FYE 2019 compared to FYE 2020

Our Group’s total revenue increased by RM4.23 million or 3.28% from RM128.73 million in FYE 2019 to RM132.95 million in FYE 2020. The increase in our Group’s total revenue was due to higher revenue generated from both Residensi Hektar Project and GrenePark Village Project in FYE 2020 as compared to FYE 2019. The increase in revenue from the Residensi Hektar Project was largely because there were an additional 48 units sold in FYE 2020. This was partially offset by a marginally lower incremental percentage completion of construction activities for the Residensi Hektar Project in FYE 2020 of 17.56%, as compared to 18.19% in FYE 2019. Meanwhile, the increase in revenue from the GrenePark Village Project was largely because there were a higher number of units sold in FYE 2020 as compared to FYE 2019. Number of units sold under the project grew from 22 units in FYE 2019 to 55 units in FYE 2020.

11.2.4 Cost of sales and GP

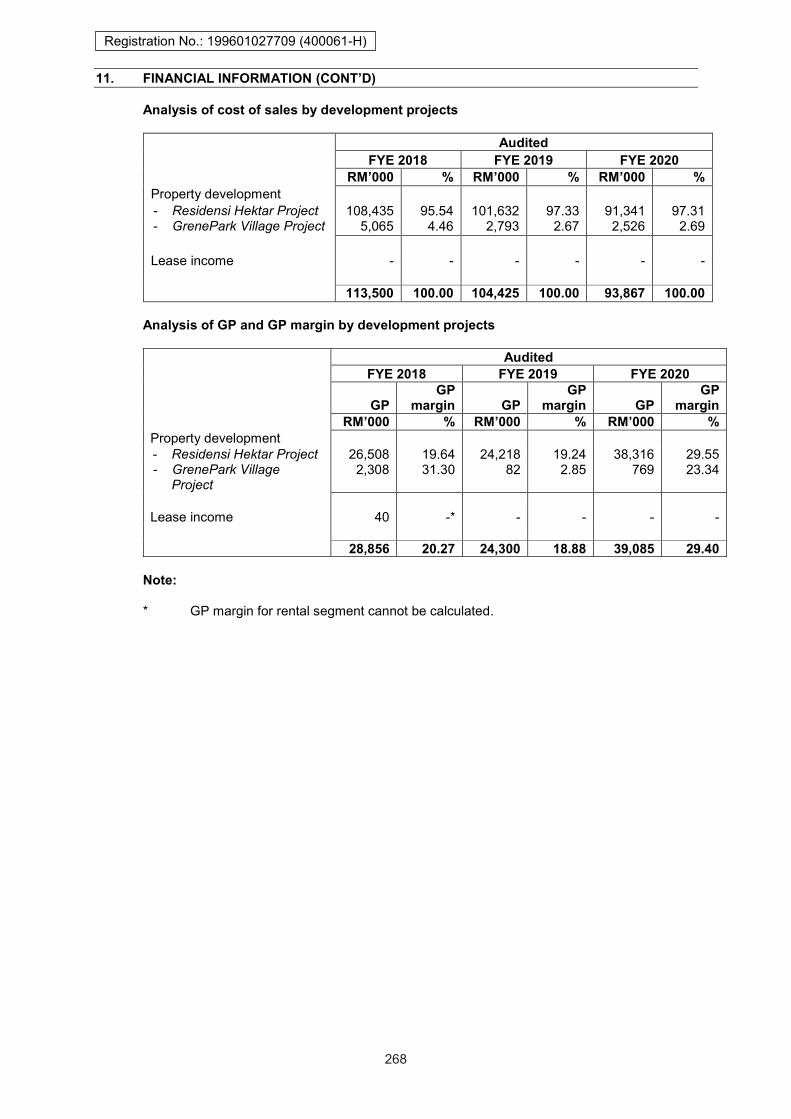

Our cost of sales comprises property development expenditure which includes construction costs, land costs, capitalised borrowing costs and other development costs. Analysis of cost of sales by components

FYE 2018 FYE 2019 FYE 2020 RM’000 % RM’000 % RM’000 % Construction costs(1) 92,409 81.42 84,529 80.95 73,859 78.69 Land costs 5,462 4.81 5,016 4.80 5,115 5.45 Capitalised borrowing costs(2) 2,521 2.22 2,337 2.24 2,368 2.52 Development costs 13,108 11.55 12,543 12.01 12,525 13.34 113,500 100.00 104,425 100.00 93,867 100.00

Notes:

(1) Being construction works undertaken by our contractors. (2) Being interests incurred in the financing of land and construction costs.

267

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION

Registration No.: 199601027709 (400061-H)

(a) Construction costs

Construction costs constitute the largest proportion to our Group’s cost of sales. Construction costs refer to all construction related activities for our on-going projects including foundation and piling, civil and structural, mechanical and electrical, and infrastructure construction works. The construction related activities of our on-going development projects are undertaken by third-party contractors and as such, our construction cost is mostly fees incurred by these third-party contractors. Construction costs incurred accounted for 81.42%, 80.95% and 78.69% of our Group’s total cost of sales in the FYE 2018, FYE 2019 and FYE 2020, respectively. Overall, construction costs declined from RM92.41 million in FYE 2018 to RM84.53 million in FYE 2019 and RM73.86 million in FYE 2020.

(b) Land costs

Land costs is the second largest component of our cost of sales. It refers to the costs of acquiring the land and any related expenses such as stamp duty and legal fees. The land costs incurred accounted for 4.81%, 4.80% and 5.45% of our Group’s total cost of sales in the FYE 2018, FYE 2019 and FYE 2020, respectively. Land costs decreased from RM5.46 million in FYE 2018 to RM5.02 million in FYE 2019, and increased to RM5.12 million in FYE 2020.

(c) Capitalised borrowing costs

Capitalised borrowing costs refer to the interests incurred in the financing of land and construction costs. The capitalised borrowing costs incurred accounted for 2.22%, 2.24% and 2.52% of our Group’s total cost of sales in the FYE 2018, FYE 2019 and FYE 2020, respectively. Capitalised borrowing costs decreased from RM2.52 million in FYE 2018 to RM2.34 million in FYE 2019, and increased to RM2.37 million in FYE 2020.

(d) Development costs

Development costs include professional fees, commissions, consultancy services such as architectural and landscape design, soil investigation and survey fees, landowners’ entitlement and fees payable to authorities. Other development costs incurred accounted for 11.55%, 12.01% and 13.34% of our Group’s total cost of sales in the FYE 2018, FYE 2019 and FYE 2020, respectively. Other development costs increased from RM13.11 million in FYE 2018 to RM12.54 million in FYE 2019, and further decreased to RM12.53 million in FYE 2020.

268

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

268

Registration No.: 199601027709 (400061-H)

Analysis of cost of sales by development projects Audited FYE 2018 FYE 2019 FYE 2020 RM’000 % RM’000 % RM’000 % Property development - Residensi Hektar Project 108,435 95.54 101,632 97.33 91,341 97.31 - GrenePark Village Project 5,065 4.46 2,793 2.67 2,526 2.69 Lease income - - - - - - 113,500 100.00 104,425 100.00 93,867 100.00

Analysis of GP and GP margin by development projects Audited FYE 2018 FYE 2019 FYE 2020

GP GP

margin GP GP

margin GP GP

margin RM’000 % RM’000 % RM’000 % Property development - Residensi Hektar Project 26,508 19.64 24,218 19.24 38,316 29.55 - GrenePark Village

Project 2,308 31.30 82 2.85 769 23.34

Lease income 40 -* - - - - 28,856 20.27 24,300 18.88 39,085 29.40

Note:

* GP margin for rental segment cannot be calculated.

269

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

269

Registration No.: 199601027709 (400061-H)

(a) FYE 2018 compared to FYE 2019

Our Group’s total cost of sales decreased by RM9.08 million or 8.00% from RM113.50 million in FYE 2018 to RM104.43 million in FYE 2019. The lower cost of sales in FYE 2019 was attributed to: cost of sales for the Residensi Hektar Project decreased by RM6.80 million

from RM108.44 million in FYE 2018 to RM101.63 million in FYE 2019. This was as a result of lower cost incurred for the project as the incremental progress completion for construction related activities for the Residensi Hektar Project was 18.19% in FYE 2019, which is lower than 19.41% of the incremental construction related activities completed in FYE 2018.

cost of sales for the GrenePark Village Project declined by RM2.27 million or

44.86%, from RM5.07 million in FYE 2018 to RM2.79 million in FYE 2019 due to a change in retail design concept that resulted in a deferment in the project’s construction schedule. Thus, the incremental percentage of the construction related activities completed for the GrenePark Village Project declined from 13.99% in FYE 2018 to 1.47% in FYE 2019.

Our Group’s GP declined by RM4.56 million or 15.79% from RM28.86 million in FYE 2018 to RM24.30 million in FYE 2019 due to lower contribution from both the Residensi Hektar Project and GrenePark Village Project. Our GP performance for the respective projects are as follows: GP from the Residensi Hektar Project declined by RM2.29 million or 8.64%,

from RM26.51 million in FYE 2018 to RM24.22 million in FYE 2019 due to lower revenues generated for the project in FYE 2019 as compared to FYE 2018.

Nevertheless, GP margin maintained at 19.64% in FYE 2018 and 19.24% in FYE 2019.

GP margin for the GrenePark Village Project fell from 31.30% in FYE 2018 to

2.85% in FYE 2019 due to a substantial fall in revenue derived from the project in the financial year and an upward revision in development costs incurred during the year.

270

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION

Registration No.: 199601027709 (400061-H)

(b) FYE 2019 compared to FYE 2020

Our Group’s total cost of sales decreased by RM10.56 million or 10.11%, from RM104.43 million in FYE 2019 to RM93.87 million in FYE 2020 mainly due to: • lower cost of sales for the Residensi Hektar Project as the incremental

percentage of construction related activities completed for the Residensi Hektar Project declined from 18.19% in FYE 2019 to approximately 17.56% in FYE 2020.

• lower cost of sales for the GrenePark Village Project as there were minimal

construction activities carried out for the GrenePark Village Project in FYE 2020 (i.e. 0.63%) due to COVID-19 disruption on construction progress and further retail design enhancements which resulted in the deferment in the construction schedule.

As a result, our Group’s GP increased by RM14.79 million or 60.84%, from RM24.30 million in FYE 2019 to RM39.09 million in FYE 2020 due to the higher revenues derived from both of the Residensi Hektar Project and GrenePark Village Project in FYE 2020 as compared to FYE 2019. Overall, our GP margin increased from 18.88% in FYE 2019 to 29.40% in FYE 2020, mainly due to higher GP margin from the Residensi Hektar Project and GrenePark Village Project. The GP performance for both projects are as illustrated below:

• GP for the Residensi Hektar Project increased by RM14.10 million or 58.21%,

from RM24.22 million in FYE 2019 to RM38.32 million in FYE 2020 largely due to an increase in revenue generated and lower costs incurred from the project in the financial year. There were lower costs incurred as a result of re-measurement of bill of quantities for the Residensi Hektar Project. This led to an improved GP margin from 19.24% in FYE 2019 to 29.55% in FYE 2020.

• GP for the GrenePark Village Project increased by RM0.69 million or 837.80%,

from RM0.08 million in FYE 2019 to RM0.77 million in FYE 2020 in line with an increase in revenue generated and lower costs incurred from the project in the financial year. The lower cost in FYE 2020 for the GrenePark Village Project was because of the revision in development cost in FYE 2019 which was not recurring in FYE 2020. This also led to the GP margin recovering to 23.34% in FYE 2020, from 2.85% in FYE 2019.

271

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

271

Registration No.: 199601027709 (400061-H)

11.2.5 Other income

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 % RM’000 % RM’000 % Lease income 356 96.48 305 58.10 275 53.50 Gain on disposal of property, plant and equipment, and subsidiaries

- - 212 40.38 19 3.70

Wage subsidies(1) - - - - 150 29.18 Forfeited utilities deposit from tenant

5 1.36 - - - -

Forfeited deposit and interests received from buyers

- - - - 58 11.28

Bank interests 8 2.16 8 1.52 4 0.78 Rent concession related to COVID-19

- - - - 8 1.56

369 100.00 525 100.00 514 100.00

Note:

(1) Wage subsidies are subsidies received for the Wage Subsidy Programme that was launched by PERKESO in an effort to cushion any adverse impacts resulting from the implementation of MCO during the FYE 2020.

(a) FYE 2018 compared to FYE 2019

Other income increased by RM0.16 million or 42.28% from RM0.37 million in FYE 2018 to RM0.53 million in FYE 2019. The increase was due to a gain on disposal of a residential property in Vila Puncak Desa, Kuala Lumpur, and a motor vehicle for operational use, amounting to RM0.21 million. This was partially offset by lower lease income recognised in FYE 2019, from RM0.36 million in FYE 2018 to RM0.31 million in FYE 2019. Lease income derived in FYE 2018 were from 2 commercial properties located in Menara Amcorp and Amcorp Trade Centre in Selangor, and we ceased renting out 1 of these properties by end of FYE 2018.

(b) FYE 2019 compared to FYE 2020 Other income declined by RM0.01 million or 2.10%, from RM0.53 million in FYE 2019 to RM0.51 million in FYE 2020 largely because there were no gains on disposal of properties in FYE 2020. However, this was partially offset by gains on disposal of subsidiaries, i.e. Hyperstraits and Grenelight of RM0.02 million, and wage subsidies of RM0.15 million received from PERKESO in an effort to cushion the impact of the COVID-19 pandemic on companies’ financial performance in the year.

272

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

272

Registration No.: 199601027709 (400061-H)

11.2.6 Administrative expenses

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 % RM’000 % RM’000 % Staff costs 3,186 33.15 6,928 51.49 5,722 48.59 Depreciation and amortisation

708 7.36 1,162 8.64 2,014 17.10

Legal and professional fees 649 6.75 1,143 8.50 786 6.67 Directors’ remuneration 620 6.45 720 5.35 624 5.30 Security charges, services and sinking fund

484 5.04 477 3.55 508 4.31

Marketing costs 1,631 16.97 1,305 9.70 469 3.98 Assessments, quit rent, stamp duty and other fees

932 9.70 351 2.61 347 2.94

Upkeep of offices, properties and vehicles

163 1.70 182 1.35 305 2.59

Travelling and transport charges

188 1.96 269 2.00 212 1.80

Rental 455 4.74 419 3.11 242 2.05

Others(1) 593 6.18 500 3.70 548 4.67 9,609 100.00 13,456 100.00 11,777 100.00

Note:

(1) Others mainly include insurance, printing and stationery, maintenance and sinking fund, IT expenses as well as interests and charges.

(a) FYE 2018 as compared to FYE 2019

Administrative expenses increased by RM3.85 million or 40.04% from RM9.61 million in FYE 2018 to RM13.46 million in FYE 2019 mainly due to: higher staff and staff related costs as our headcount grew from 35 employees

in FYE 2018 to 50 employees in FYE 2019 in line with the launches of the Residensi Hektar Project and Phase 1 of the GrenePark Village Project;

higher depreciation of right-of-use assets such as Residensi Hektar Project’s

sales gallery, a commercial property located in Menara Amcorp, Selangor, and a motor vehicle for our operational use; and

higher professional fees for management services in respect of the issuance of

RCPS, and consultancy service.

This was partially offset by lower marketing costs as there were less marketing expenditure to promote the Residensi Hektar Project as most of the units were sold in FYE 2018. There were also lower financial structuring fee, penalties, quit rent assessment and subscription fees.

273

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

273

Registration No.: 199601027709 (400061-H)

(b) FYE 2019 as compared to FYE 2020

Administrative expenses decreased by RM1.68 million or 12.48%, from RM13.46 million in FYE 2019 to RM11.78 million in FYE 2020 mainly due to: lower staff and staff related costs as there were no bonuses and lower

allowances paid during the year; lower professional fees incurred for management services in respect of

issuance of RCPS and consultancy service; lower marketing costs as the marketing for the Residensi Hektar Project ceased

in the financial year as almost all units were sold; and lower rental expenses as we ceased renting the Residensi Hektar Project’s

sales gallery.

This was partially offset by higher depreciation of right-of-use assets (namely the sales gallery for the GrenePark Village Project), and 2 motor vehicles for our operational use.

11.2.7 Finance costs

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 % RM’000 % RM’000 % Finance lease liability 4 0.33 - - - - Lease liabilities - - 47 3.33 68 3.70 Term loans 706 58.69 833 58.99 890 48.37 Overdraft interest - - - - 51 2.77 RPS - - - - 256 13.91 Landowner’s entitlement interest(1)

493 40.98 532 37.68 575 31.25

1,203 100.00 1,412 100.00 1,840 100.00

274

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

274

Registration No.: 199601027709 (400061-H)

Note:

(1) This is in respect of provision of landowner’s entitlement that is payable by Hektar Aneka, pursuant to the JVA entered with the Landowner.

(a) FYE 2018 as compared to FYE 2019

Finance costs increased by approximately RM0.21 million or 17.37%, from RM1.20 million in FYE 2018 to RM1.41 million in FYE 2019. This was mainly due to: an increase in borrowing interest, net of interest capitalised into property

development expenditure to finance working capital of RM0.13 million, a motor vehicle for operational use, acquisition of our head office located in Amcorp Trade Centre and a commercial property in Menara Amcorp, Selangor to be held for investment purposes;

an increase in lease liabilities of RM0.05 million due to the adoption of MFRS 16; and

an unwinding of discount on landowner’s entitlement of RM0.53 million.

(b) FYE 2019 as compared to FYE 2020 Finance costs increased by RM0.43 million or 30.31%, from RM1.41 million in FYE 2019 to RM1.84 million in FYE 2020. This was mainly due to: dividend in relation to debt component of the RPS recognised as finance cost

amounting to RM0.26 million;

overdraft interest of RM0.05 million to finance working capital;

increase in lease liabilities of RM0.02 million for rental of sales gallery for the GrenePark Village Project and motor vehicles for operational use; and

an increase in term loan of RM0.06 million for working capital.

275

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

275

Registration No.: 199601027709 (400061-H)

11.2.8 PBT and Effective Tax Rate

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 RM’000 RM’000 PBT 18,413 9,957 25,982 PBT margin (%) 12.93 7.74 19.54 Taxation 6,344 2,135 7,053 Effective tax rate (%) 34.45 21.44 27.15 Statutory tax rate (%) 24.00 24.00 24.00

(a) FYE 2018 as compared to FYE 2019

PBT decreased by RM8.46 million or 45.92%, from RM18.41 million in FYE 2018 to RM9.96 million in FYE 2019 mainly due to a fall in revenue from the Residensi Hektar Project and GrenePark Village Project. PBT margin also decreased from 12.93% in FYE 2018 to 7.74% in FYE 2019. The fall in PBT margin was largely contributed by the fall in GP margin of the GrenePark Village Project. The effective tax rate for FYE 2018 was higher than the statutory tax rate of 24.00% mainly due to deferred tax assets not recognised during the financial year amounting to RM1.29 million. The effective tax rate for FYE 2019 was lower than the statutory tax rate of 24.00% mainly due to utilisation of previously unrecognised deferred tax assets amounting to RM0.64 million.

(b) FYE 2019 as compared to FYE 2020 PBT increased by RM16.03 million or 160.94%, from RM9.96 million in FYE 2019 to RM25.98 million in FYE 2020 largely due to higher revenue generated from the Residensi Hektar Project and the GrenePark Village Project. PBT margin also increased from 7.74% in FYE 2019 to 19.54% in FYE 2020 in line with the increase in GP margin for both the Residensi Hektar Project and the GrenePark Village Project. Other contributing factors were the decrease in administrative expenses from RM13.46 million in FYE 2019 to RM11.78 million in FYE 2020. The effective tax rate for FYE 2020 was higher than the statutory tax rate of 24.00% mainly due to higher non-deductible expenses of approximately RM0.56 million.

276

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

276

Registration No.: 199601027709 (400061-H)

11.2.9 Significant Factors Affecting our Growth and Financial Performance Section 8 details a number of risk factors relating to our business and the industry in which we operate. Some of these risk factors have an impact on our Group’s revenue and financial performance. The main factors which affect our revenues and profits include but are not limited to the following:

(i) Impact of prevailing market conditions in the property market in Malaysia and

specifically, in Klang Valley As most of our property development projects are located in Klang Valley, we are dependent on the prevailing market conditions of the property market in Malaysia and specifically, in Klang Valley, for the sales performance of our property units as well as the development planning of our future projects. This includes factors beyond our control such as changes in political environment or sudden outbreak of diseases. According to the IMR report, the demand for residential and commercial properties, including mixed-use properties, in Kuala Lumpur and Selangor were adversely affected by the MCO that was implemented in Malaysia to curb the spreading of the COVID-19 pandemic in 2020. The transaction values for residential properties in Kuala Lumpur and Selangor fell from RM33.8 billion in 2019 to approximately RM30.0 billion in 2020. Similarly, the transaction values for commercial properties in Kuala Lumpur and Selangor fell from RM17.6 billion in 2019 to approximately RM10.2 billion in 2020. Despite the fall in transaction values for residential and commercial properties in Kuala Lumpur and Selangor, we did not experience any adverse impact on our Group’s revenues and the sales performance of our property units in FYE 2020. However, there is no assurance that any such situations will not adversely affect our business and financial performance in the future.

(ii) Impact of the outbreak of COVID-19 and the MCO The MCOs, total lockdown and Phase 1 of the NRP that were implemented in an effort to curb the COVID-19 pandemic throughout 2020 and 2021 had resulted in disruptions and restrictions for various industries, including the property industry. The first MCO, total lockdown and Phase 1 of the NRP have resulted in delays in the progress of our Group’s development projects. The progress of construction activities for our on-going projects will continue to delay so long as restrictions are imposed to curb the spread of the COVID-19 pandemic. Further details on the disruptions are illustrated in Section 5.5.12 of this Prospectus. Premised on the above, the progress completion of our Residensi Hektar Project and GrenePark Village Project were impacted in the FYE 2020. Incremental progress completion of construction activities for the Residensi Hektar Project declined from 18.19% in FYE 2019 to approximately 17.56% in FYE 2020, while incremental progress completion of construction activities for the GrenePark Village Project declined from 1.47% in FYE 2019 to 0.63%. There were minimal construction activities undertaken at the GrenePark Village Project as there were further retail design enhancements to cater for changes in prevailing market conditions in light of the COVID-19 pandemic.

277

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

277

Registration No.: 199601027709 (400061-H)

(iii) Impact of claims arising from LADs The timely completion of property development projects undertaken by our Group is dependent on many external factors inherent in property development. Any prolonged interruptions or delays in completing a project may result in our buyers imposing LAD on us which could affect our volatility in our revenue and profitability as well as cash flows. For the Financial Years Under Review and up to the LPD, there were no claims made by our customers arising from LADs.

(iv) Impact of inflation There was no material impact of inflation on our Group’s historical financial results for the Financial Years Under Review. Nevertheless, there can be no assurance that future inflation would not have an impact on our business operations and financial performance.

(v) Impact of government, fiscal and monetary policies Our business is subject to risks relating to Government policies implemented in Malaysia that could impact the property market. This includes changes in government policies in relation to housing, land, development and tax policies, which could adversely affect the performance of the property market and value of properties in Malaysia. Any restrictive policy changes by Bank Negara Malaysia such as upward changes in the overnight policy rate by Bank Negara Malaysia, could restrict the purchasing ability of buyers. This would likely have a negative impact on consumer sentiment and purchasing power, and dampen the overall demand for properties. Although our current properties are priced at an average selling price of RM500,000 and below so that they are affordable to a wider target market, any upward changes in overnight policy rates by Bank Negara Malaysia may cause negative impact on consumer sentiment and purchasing power, consequently adversely affect demand for our property units. In addition, our ability to obtain financing and the costs of financing are also dependent monetary and fiscal policies as determined by the Government, amongst other factors.

(vi) Impact of interest rates As at 31 December 2020, our Group’s total borrowings was RM93.28 million, consisting of lease liabilities, term loans and bank overdrafts. All of our borrowings are interest bearing. In this respect, we face financial risks relating to increase in interest rates that may have an impact on our financial performance including profitability and margins. For the FYE 2018 to 2020 and up to the LPD, we have not defaulted on any payments of either principal sums and/or interests in relation to our borrowings.

278

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

278

Registration No.: 199601027709 (400061-H)

11.2.10 Liquidity and Capital Resources

(i) Working capital

We finance our operations with cash generated from operations, credit extended by trade payables and/or financial institutions as well as cash and bank balances. As at the LPD, our facilities from financial institutions comprise term loans, lease liabilities and bank overdrafts.

Our Board is confident that our working capital will be sufficient for our existing and foreseeable requirements for a period of 12 months from the date of this Prospectus, taking into consideration the following: (a) Our closing cash balance of approximately RM5.96 million as at LPD; (b) Our expected future cash flows from operations; and (c) Our total banking facilities as at LPD of RM54.11 million, which have been fully

utilised. We carefully consider our cash position and ability to obtain further financing before making significant capital commitments, such as new land acquisition and commencement of new property development projects.

(ii) Cash Flows

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 RM’000 RM’000 Net cash (used in)/from operating activities (49,012) 30,650 93,931 Net cash used in investing activities (71,700) (61,708) (34,787) Net cash from/(used in) financing activities 121,567 32,594 (65,865) Cash and cash equivalents 1,099 2,635 (4,086)(1)

Note: (1) The cash and cash equivalents in FYE 2020 is negative due to a bank overdraft

amount of approximately RM5.00 million, the facility of which is still in place and is available as at LPD.

279

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

279

Registration No.: 199601027709 (400061-H)

FYE 2018 Net cash for operating activities In FYE 2018, we generated operating cash flows before working capital changes of RM20.32 million. Our net cash used in operating activities was RM49.01 million after accounting for key items as set out below: increase in contract assets of RM103.64 million due to increase in accrued

billings as construction progress was ahead of billing issued to buyers for Residensi Hektar Project and GrenePark Village Project; and

increase in property development costs of RM3.15 million due to construction

progress during the year for Residensi Hektar Project and GrenePark Village Project.

This was partially offset by: increase in trade payables of RM39.66 million and other payables of RM18.94

million as construction activities progressed for Residensi Hektar Project, as well as amount due from Hektar Aneka, which was then an associate company which we owned 50.00% equity interest during the financial year, of RM4.53 million; and

increase in trade receivables of RM22.60 million which was offset by a

decrease in other receivables of RM4.22 million due to outstanding progress billings from end-financiers for the Residensi Hektar Project.

280

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

280

Registration No.: 199601027709 (400061-H)

Net cash for investing activities In FYE 2018, we recorded net cash used in investing activities of RM71.70 million mainly due to reclassification of land held for development for the GrenePark Village Project and GreneForest City Project amounting RM69.80 million, and purchase of computers and software, furniture, equipment for our sales gallery and office, and renovation for office amounting to RM1.93 million. The was partially offset by withdrawn fixed deposits pledged of RM0.02 million. Net cash for financing activities In FYE 2018, we recorded net cash from financing activities of RM121.57 million mainly due to: drawdown of term loan for our Residensi Hektar Project’s land, construction

costs and working capital of RM92.06 million; and proceeds from issuance of RCPS of RM33.24 million. This was partially offset by: placement of deposit in Escrow accounts amounting to RM2.33 million; repayment of term loans for the residential and commercial properties in Vila

Puncak Desa, Komplex Rimbun Scott and Kiara Hills in Kuala Lumpur, and Menara Amcorp and Amcorp Trade Centre in Selangor, and working capital of RM1.38 million; and

repayment of finance lease liability for motor vehicle of RM0.02 million.

281

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

281

Registration No.: 199601027709 (400061-H)

FYE 2019 Net cash for operating activities In FYE 2019, we generated operating cash flows before working capital changes of RM12.32 million. Our net cash from operating activities was RM30.65 million after accounting for key items as set out below: increase in trade payables and other payables of RM35.03 million, due to

higher construction progress mainly for the Residensi Hektar Project in the financial year;

decrease in property development costs of RM15.24 million as the construction

progressed mainly for the Residensi Hektar Project in the financial year; and decrease in trade receivables of RM15.20 million due to outstanding progress

billings from buyers, which was offset by an increase in other receivables of RM6.55 million.

This was substantially offset by an increase in contract assets of RM25.89 million due to increase in accrued billings as construction progress was ahead of billings issued to buyers for the Residensi Hektar Project and GrenePark Village Project. Net cash for investing activities In FYE 2019, we recorded net cash used in investing activities of RM61.71 million mainly due to: an increase in land held for property development and development costs for the

GrenePark Village Project and GreneForest City Project due to land clearing activities of RM33.05 million;

acquisition of 50.00% equity interest in Hektar Aneka for a cash consideration of

RM30.00 million; addition of commercial units in Amcorp Trade Centre which will be rented out, and

motor vehicles for our operational use of RM1.86 million; and renovation of one of our offices in Amcorp Trade Centre and sales gallery for the

GrenePark Village Project amounting to RM0.04 million.

282

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

282

Registration No.: 199601027709 (400061-H)

This was partially offset by: proceeds from disposal of a residential property in Villa Puncak Desa, Kuala

Lumpur amounting to RM3.15 million; and proceeds from disposal of a motor vehicle of RM0.09 million. Net cash for financing activities In FYE 2019, we recorded net cash from financing activities of RM32.59 million mainly due to: drawdown of term loan that was largely for the financing of the Residensi

Hektar Project amounting to RM30.59 million; and proceeds from issuance of RCPS of RM10.00 million. This was partially offset by repayment of term loans for the Residensi Hektar Project’s and GrenePark Village Project’s land, residential and commercial properties in Vila Puncak Desa, Komplex Rimbun Scott and Kiara Hills in Kuala Lumpur, and Menara Amcorp and Amcorp Trade Centre in Selangor, and working capital of RM7.56 million.

FYE 2020 Net cash for operating activities In FYE 2020, we generated operating cash flows before working capital changes of RM29.81 million. Our net cash from operating activities was RM93.93 million after accounting for key items as set out below: decrease in contract assets of RM56.05 million mainly due to decrease in

accrued billing for the Residensi Hektar Project as billings were issued to buyers; and

increase in trade payables of RM25.42 million and other payables of RM7.30

million as construction activities progressed for the Residensi Hektar Project.

This was partially offset by: decrease in property development costs amounting to RM3.00 million as

construction progressed for the Residensi Hektar Project; and increase in trade receivables of RM2.64 million which was offset by other

receivables of RM0.39 million as there were more outstanding from buyers.

283

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

283

Registration No.: 199601027709 (400061-H)

Net cash for investing activities In FYE 2020, we recorded net cash used in investing activities of RM34.79 million mainly due to additions of land held for property development for the GreneForest City Project and GrenePark Village Project amounting to RM35.71 million, and costs of renovation and purchase of computers for our offices in Amcorp Trade Centre amounting to RM0.27 million. This was partially offset by proceeds from the partial disposal of non-controlling interests in Grene Residencia Sdn Bhd of RM1.20 million. Net cash for financing activities In FYE 2020, we recorded net cash used in financing activities of RM65.87 million mainly due to: repayment of bank borrowings for the Residensi Hektar Project’s and

GrenePark Village Project’s lands, properties and working capital, amounting to RM92.97 million;

placement of deposit with licensed bank for Hektar Aneka of RM0.51 million; repayment of lease liabilities for office, sales gallery for GrenePark Village

Project and motor vehicles for our operational use amounting to RM0.26 million; and

dividend paid to RCPS holders of RM0.09 million. This was partially offset by drawdown of term loan to finance the construction costs for the Residensi Hektar Project of RM26.96 million and proceeds from RCPS of RM1.00 million.

284

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

284

Registration No.: 199601027709 (400061-H)

(iii) Borrowings

As at 31 December 2020, our Group’s total borrowings was RM93.28 million, all of which were interest bearing and denominated in RM. Our bank borrowing details as at FYE 2020 are set out below:

As at FYE 2020

Payable within

12 months Payable after 12

months Total RM’000 RM’000 RM’000 Lease liabilities(1) 411 1,057 1,468 Term loans(2) 54,046 32,769 86,815 Bank overdraft(3) 5,000 - 5,000 Total 59,457 33,826 93,283 Gearing ratio (times) 0.73

Notes: (1) Lease liabilities were mainly used for rental of leasehold properties and motor

vehicles. (2) Term loans were mainly utilised for the purchase of land and properties, and

working capital. (3) Bank overdraft were used for working capital purposes.

As at FYE 2020, our floating and fixed rate borrowings are set out below:

As at FYE 2020 Floating rate

borrowings(1) Fixed rate

borrowings(2) Total RM’000 RM’000 RM’000 Total borrowings 85,158 8,125 93,283

Notes: (1) Includes term loans and bank overdraft. (2) Includes lease liabilities and term loans.

285

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

285

Registration No.: 199601027709 (400061-H)

As at LPD, we do not have any borrowings which are non-interest bearing and/or in foreign currency. We have not defaulted on payments of principal sums and/or interests in respect of any of our borrowings throughout FYE 2018 to FYE 2020, and up to LPD. As at LPD, neither our Company nor any of our subsidiaries is in breach of any terms and conditions or covenants associated with the credit arrangement or bank loan which can materially affect our financial position and results or business operations or the investments by holders of our securities. Over FYE 2018 to FYE 2020, we have not experienced any claw back or reduction in the facilities limit granted to us by our lenders.

11.2.11 TYPES OF FINANCIAL INSTRUMENTS USED, TREASURY POLICIES AND OBJECTIVES

Save as disclosed in Section 11.2.10(iii) of this Prospectus above, we do not have or utilise any other financial instruments or have any other treasury policies. All our financial instruments are used towards purchase of properties, motor vehicles and working capital for our property development business. As at 31 December 2020, save for our lease liabilities and some of our term loans which are based on fixed rates, all our other facilities are based on base lending rate plus or minus a rate which varies depending on the type of facility.

11.2.12 MATERIAL CAPITAL COMMITMENTS

As at the LPD, save as disclosed below, we do not have any other material capital commitments:

Capital commitment

Source of funds

Internal generated

funds/Bank borrowings IPO proceeds

RM’000 RM’000 RM’000 Land held for property development:

Authorised and contracted for - GreneForest City Land 113,284 113,284 - - Setiawangsa Land 105,518 105,518 -

Total 218,802 218,802 -

The above land held for property development comprises our GreneForest City Land and Setiawangsa Land. The material capital commitments above shall be funded through our internally generated funds and/or bank borrowings at our discretion.

286

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION

Registration No.: 199601027709 (400061-H)

11.2.13 MATERIAL LITIGATION AND CONTINGENT LIABILITIES Save as disclosed in Section 14.4 in this Prospectus, we are not engaged in any material litigation, claim or arbitration either as plaintiff or defendant and there is no proceeding pending or threatened or any fact likely to give rise to any proceeding which might materially or adversely affect our position or business as at LPD. As at LPD, save as disclosed below, our Directors confirm that there are no material contingent liabilities incurred by our Group, which upon becoming enforceable may have a material effect on our Group’s business, financial results or position: RM’000 Bank guarantees for deposits with the housing and local authorities as

well as utilities provider 839 For utilities providers such as Indah Water Konsortium and Tenaga Nasional Berhad, we need to give guarantee when handing over our completed property development to them.

11.2.14 KEY FINANCIAL RATIOS The key financial ratios of our Group for FYE 2018 to 2020 are as follows:

Audited FYE 2018 FYE 2019 FYE 2020 Trade receivables turnover (days) 62(1) 79(1) 59(2) Trade payables turnover (days) 126(3) 239(3) 328(4) Current ratio (times) 1.41(5) 1.51(5) 1.18(5) Gearing ratio (times) 1.12(6) 1.27(6) 0.73(6)

Notes:

(1) Computed based on average trade receivables as at year end over revenue for the

year multiplied by 365 days for each financial year. (2) Computed based on average trade receivables as at year end over revenue for the

year multiplied by 366 days for each financial year. (3) Computed based on average trade payables (excluding retention sum) as at year end

over costs of sales for the year multiplied by 365 days for each financial year. (4) Computed based on average trade payables (excluding retention sum) as at year end

over revenue for the year multiplied by 366 days for each financial year. (5) Computed based on current assets divided by current liabilities. (6) Computed based on total loans and borrowings less cash and bank balances (termed

as net debt) divided by total shareholders’ equity.

287

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

287

Registration No.: 199601027709 (400061-H)

No inventories ratio and inventories ageing were included as our Group does not hold any completed property units as all completed property units for projects undertaken by our Group have been fully sold. (i) Trade receivables turnover

The normal credit period granted by our Group to our buyers is 30 days from the date of progress billings. As the revenue for our property development activities will be recognised using the percentage of completion method, the movements in our Group’s revenue from property development activities may not be in line with the movements in the trade receivables turnover, days as trade receivables are recorded based on progress billings issued to the buyers. Our trade receivables turnover days for FYE 2018 to FYE 2020 were between 59 and 79 days, which have exceeded the credit period granted to our buyers, mainly due to longer processing time taken by the end-financiers before releasing the payment to us. The Residensi Hektar Project is one of the projects under the Residensi Wilayah, which is an affordable housing scheme providing comfortable, quality and affordable homes to Federal Territory residents. As it is under the Residensi Wilayah, the time taken to process loan drawdowns is generally longer than the usual 30 days. This is because buyers of affordable housing under Residensi Wilayah may take longer to pay the differential sum between the purchase price of the property and amount financed through the mortgage loans. Out of the 2,400 units available under the Residensi Hektar Project, we sold 2,350 units in the FYE 2018. Moreover, many of these units were sold towards the end of FYE 2018. Thus, this led to the high trade receivables turnover in FYE 2018 and FYE 2019. In the FYE 2020, 48 units under the Residensi Hektar Project and 55 units of the flexi-suites units launched under the GrenePark Village Project were sold. Buyers for units under the GrenePark Village Project obtained financing from end-financiers which were commercial banks, and these commercial banks typically process loan drawdowns within the 30-day period. However, as there were still sales for units under the Residensi Hektar Project, the processing of loan drawdowns was still subject to longer loan processing period. Nevertheless, our trade receivables turnover days in the FYE 2020 were lower than in previous FYEs, at 59 days.

288

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

288

Registration No.: 199601027709 (400061-H)

The ageing analysis of our trade receivables as at FYE 2020 is as follows:

Not past

due

Past due

Total 1-30

days 31-60 days

More than 60 days

RM’000 RM’000 RM’000 RM’000 RM’000 Trade receivables

17,387 1,270 1,273 2,817 22,747

% of trade receivables 76.44% 5.58% 5.60% 12.38% 100.00%

Subsequent collections as at LPD

(17,303) (1,187) (1,202) (2,543) (22,235)

Net trade receivables after subsequent collections

84 83 71 274 512

Our Group has not encountered any major disputes with our buyers. With respect to overdue debts, we have generally been able to collect payment eventually as evident by our subsequent collections after FYE 2020. As such, our management was of view that the overdue trade receivables were recoverable and no impairment was made in FYE 2020. Our management closely monitors the recoverability of our overdue trade receivables on a regular basis, and, when appropriate, provides for impairment of these trade receivables. Trade receivables comprise substantially of amounts due from buyers with end financing facilities from end-financiers. Between FYE 2018 and FYE 2020, an average of 95.00% our Group’s buyers utilised end-financing facilities. In respect of buyers with no end financing facilities, our Group retains the legal title to all property units sold until the full contracted sales value is settled. In the past, we have experienced cancellations of sales, and the deposits forfeited were recognised as other income. Save for the reversal of any profits or losses from the progress billings and the income from the forfeiture, there is no other significant impact of such cancellations to us. For the Financial Years Under Review up to the LPD, there have been 6 cancellations of sales of such nature, out of units that were sold under the GrenePark Village Project.

289

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

289

Registration No.: 199601027709 (400061-H)

(ii) Trade payables turnover

The normal trade credit terms granted to our Group is up to 210 days, including the extended credit terms of an additional 180 days granted by a major contractor for a particular development project. The extended credit terms of which are subject to the certain conditions which have been met. Other credit terms are assessed and approved on a case-by-case basis. Our average trade payables turnover days for the FYE 2018, FYE 2019 and FYE 2020 were 126 days, 239 days and 328 days respectively. From FYE 2018 to FYE 2020, our average trade payables turnover days have increased in line with higher billings received from our contractors and consultants as the percentage progress completion of construction activities increases, particularly for the Residensi Hektar Project. A large part of these billings was from our main contractor, i.e. Vizione Builder, which contributed a large proportion to our trade payables. In addition to the above, our average trade payables turnover days increased to 328 days in FYE 2020 as a large proportion of invoices received from our suppliers were raised in the last quarter of FYE 2020. As such, we were not able to release payments to these suppliers prior to the end of FYE 2020. As illustrated below, 16.71% of our trade payables were outstanding for more than 90 days. Nevertheless, it should be noted that we had subsequently made payments of RM81.33 million to our suppliers, as indicated in the table below, with the issuance of new ordinary shares to increase our Group’s share capital, as illustrated in Section 5.1.2 of this Prospectus.

290

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

290

Registration No.: 199601027709 (400061-H)

The ageing analysis of our trade payables as at FYE 2020 is as follows:

Retention sum

Not past due

Past due

1-30

days 31-60 days

61-90 days

More than 90

days Total RM’000 RM’000 RM’000 RM’000 RM’000 RM’000 RM’000 Trade

payables 27,738 60,190 530 7,456 5,212 20,287 121,413

% of trade

payables 22.85% 49.57% 0.44% 6.14% 4.29% 16.71% 100.00%

Subsequent

payments as at LPD

(129) (60,190) (120) (6,099) (5,193) (9,602) (81,333)

Net trade

payables after subsequent collections

27,609 - 410 1,357 19 10,685 40,080

There are no disputes in respect of any trade payables and no legal action has been initiated by our suppliers to demand for payment. Nonetheless, our Group shall monitor our payment processes more closely to avoid future delays in payment.

(iii) Current ratio

Our current ratio throughout the Financial Years Under Review is as follows:

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 RM’000 RM’000 Current assets 286,629 312,996 291,064 Current liabilities 202,934 207,820 246,777 Net current assets 83,695 105,176 44,287 Current ratio (times) 1.41 1.51 1.18

Our current ratio maintained throughout the Financial Years Under Review, ranging from 1.18 to 1.51 times. This indicates that our Group can meet our current obligations as our current assets such as inventory and trade receivables, which can be readily converted to cash, together with our cash in the bank are enough to meet immediate current liabilities.

291

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

291

Registration No.: 199601027709 (400061-H)

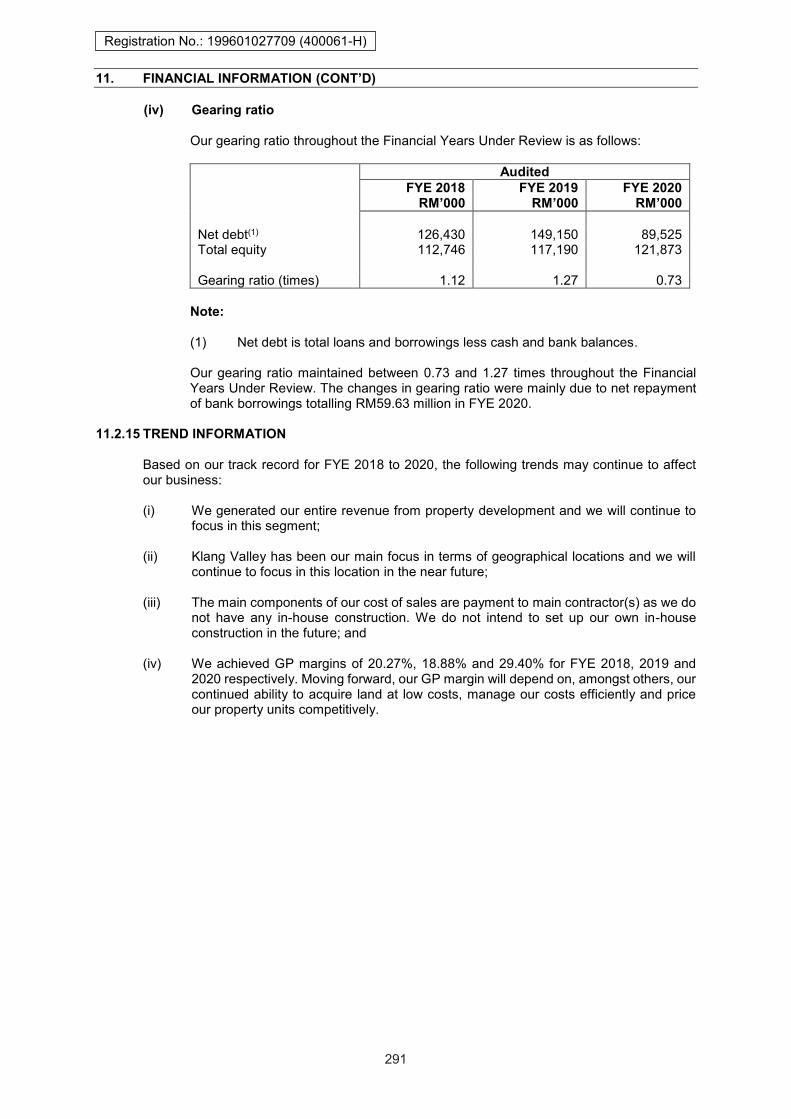

(iv) Gearing ratio

Our gearing ratio throughout the Financial Years Under Review is as follows:

Audited FYE 2018 FYE 2019 FYE 2020 RM’000 RM’000 RM’000 Net debt(1) 126,430 149,150 89,525 Total equity 112,746 117,190 121,873 Gearing ratio (times) 1.12 1.27 0.73

Note: (1) Net debt is total loans and borrowings less cash and bank balances.

Our gearing ratio maintained between 0.73 and 1.27 times throughout the Financial Years Under Review. The changes in gearing ratio were mainly due to net repayment of bank borrowings totalling RM59.63 million in FYE 2020.

11.2.15 TREND INFORMATION

Based on our track record for FYE 2018 to 2020, the following trends may continue to affect our business: (i) We generated our entire revenue from property development and we will continue to

focus in this segment; (ii) Klang Valley has been our main focus in terms of geographical locations and we will

continue to focus in this location in the near future; (iii) The main components of our cost of sales are payment to main contractor(s) as we do

not have any in-house construction. We do not intend to set up our own in-house construction in the future; and

(iv) We achieved GP margins of 20.27%, 18.88% and 29.40% for FYE 2018, 2019 and

2020 respectively. Moving forward, our GP margin will depend on, amongst others, our continued ability to acquire land at low costs, manage our costs efficiently and price our property units competitively.

292

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

292

Registration No.: 199601027709 (400061-H)

As at LPD, after all reasonable enquiries, our Board confirms that, our operations have not been and are not expected to be affected by any of the following:

(i) Known trends, demands, commitments, events or uncertainties that have had or that

we reasonably expect to have, a material favourable or unfavourable impact on our Group’s financial performance, position and operations other than those discussed in Sections 11.2.8, 11.2.12 and 11.2.14;

(ii) Material commitments for capital expenditure save as disclosed in Section 5.4; (iii) Unusual, infrequent events or transactions or any significant economic changes that

have materially affected the financial performance, position and operations of our Group save as discussed in Sections 11.2.3, 11.2.4, 11.2.5, 11.2.6, 11.2.7, 11.2.8, 11.2.9 and 11.2.10;

(iv) Known trends, demands, commitments, events or uncertainties that are reasonably

likely to make our Group’s historical financial statements not necessarily indicative of the future financial performance and position other than those discussed in Sections 11.2.9 and 11.2.15.

Given the moderate outlook of the property development industry in Kuala Lumpur and Selangor (collectively referred to as Klang Valley) as set out in the IMR Report in Section 7, the status of our property sales which is not materially affected by the impact of the COVID-19 and MCO situation at this juncture, our Board believes that our revenue will remain sustainable for this immediate financial year. Nevertheless, with our Group’s competitive strengths set out in Section 5.5.1.2 and our Group’s intention to implement the business strategies as set out in Section 5.8, our Board remains optimistic about the long-term future prospects of our Group.

11.2.16 ORDER BOOK The nature of our Group’s business is property development and hence sales of property units are commonly on a one-off basis. As such, our Group does not have an order book.

11.2.17 SIGNIFICANT CHANGES Save as disclosed in this Prospectus, no significant changes have occurred which may have a material effect on the financial position and results of our Group.

293

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION

Registration No.: 199601027709 (400061-H)

11.3 CAPITALISATION AND INDEBTEDNESS

The table below summarises our capitalisation and indebtedness:

(i) as at 31 August 2021; and (ii) After adjusting for the effects of Public Issue and utilisation of proceeds.

Unaudited as at 31 August 2021

Proforma after the Public Issue and use of

Proceeds(1) RM’000 RM’000 Indebtedness Current: Unsecured Bank overdraft 5,000 5,000 Lease liabilities(2) 514 514 Secured Term loans 15,128 15,128 Lease liabilities(3) 214 214 Non-current: Unsecured Lease liabilities(2) 92 92 Secured Term loans 25,272 25,272 Lease liabilities(3) 786 786 Total indebtedness 47,006 47,006 Capitalisation Equity attributable to owners of the parent 288,650 [●] Total capitalisation 288,650 [●] Total capitalisation and indebtedness 325,042 [●] Contingent liabilities(4) 5,000 5,000 Gearing ratio (times)(5) 0.16 [●]

294

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION

Registration No.: 199601027709 (400061-H)

Notes: (1) After the Public Issue of RM[●] of which RM[●] will be allocated for project development

expenses, RM[●] for working capital and RM[●] for estimated listing expenses.

(2) Lease liabilities in respect of tenancies for leasehold buildings. (3) Lease liabilities in respect of leases under hire purchase arrangements. (4) This is in respect of the on-going legal case in the High Court of Shah Alam (Civil Suit

No: BA-22NCVC-55-02/2021). (5) Calculated based on total indebtedness divided by total capitalisation.

11.4 DIVIDEND POLICY

Our income and ability to pay dividends is dependent upon the dividends we receive from our Company and its subsidiaries, present or future. The payment of dividends is thus dependent on factors including our distributable profits, operating results, financial condition, capital expenditure plans. The dividends payable or paid by our Group for FYE 2018, 2019 and 2020 are as follows:

FYE 2018 FYE 2019 FYE 2020 RM’000 RM’000 RM’000 RCPS dividends payable/ paid(1) - 88 15,252

Note:

(1) Dividends were paid to RCPS holders via internal generated funds. The remaining

outstanding dividends payable to RCPS holders will be paid out by the end of 2021 via internal generated funds. The RCPS were fully converted as at the LPD.

This dividend is not expected to have any impact on the execution and implementation of our Group’s future plans or strategies. Save for the above, since 1 January 2021 up to the LPD, we have not declared any dividends. Save for certain banking restrictive covenants we are subject to, there are no dividend restrictions imposed on us as at the LPD.

295

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

11. FINANCIAL INFORMATION (Cont’d)

295

Registration No.: 199601027709 (400061-H)

Moving forward, we target a pay-out ratio of up to 20% of our PAT of each financial year on a consolidated basis after considering our capital requirements including working capital and capital expenditure. The actual dividend pay-out will depend upon a number of factors, including our Group's financial performance, capital expenditure requirements, general financial condition and any other factors considered relevant by our Board. Investors should note that this dividend policy merely describes our present intention and shall not constitute legally binding statements in respect of our Company’s future dividends which are subject to modification (including non-declaration thereof) at our Board’s discretion. Dividend payments, capital gains and profits from dealing in our shares will not be subject to Malaysian taxation (not applicable to entities including companies with trading of shares as their principal business activity). No withholding tax is imposed on the above transactions. Potential investors are advised to consult their professional tax advisors if they are in any doubt as to the taxation implication of subscribing, holding or disposing of and dealing in our shares.

296

Registration No.: 199601027709 (400061-H)

Registration No : 199601027709 (400061-H) 11. FINANCIAL INFORMATION 11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

(CONT’D)

Registration No.: 199601027709 (400061-H) |

11. FINANCIAL INFORMATION (CONT’D)

11.5 REPORTING ACCOUNTANTS’ REPORT ON THE PRO FORMA CONSOLIDATEDSTATEMENTSOF FINANCIAL POSITION

UHY(4F1411)Chartered AccountantsSuite 11.05, Level 11

The Gardens South Tower28 September 2021 Mid Valley City

Lingkaran Syed Putra

The Board of Directors 59200 Kuala LumpurParagrene Land Berhad Phone +60 3 2279 3088No. 9 07, Level 9 Fax +603 2279 3099

—— Email [email protected] Tower B, Amcorp Trade Centre Web wwwiuhy.commny.18 Persiaran Barat, 46050 Petaling JayaSelangor Darul Ehsan Malaysia

Dear Sirs/Madams,

PARAGRENE LAND BERHADREPORTING ACCOUNTANTS REPORT ON COMPILATION OF THE PRO FORMACONSOLIDATED STATEMENTS OF FINANCIAL POSITION