10th annual alumni business conference--refic panel

TRANSCRIPT

Capital Markets Overview

CAPITAL MARKETS OVERVIEW

DEBT PLACEMENT INVESTMENT SALES PRIVATE EQUITY & CORPORATE FINANCE STRUCTURED FINANCE NOTE SALES & NOTE SALE ADVISORY LOAN SERVICING

Special “thank you” to Mark Gibson, Colby Mueck and HFF.

Much of the analytical data compiled by HFF and provided by noted sources.

Capital Markets Overview

DISCLAIMER Forward-‐Looking Statements

Certain statements in this presenta-on are “forward-‐looking statements” within the meaning of the federal securi-es laws. Statements about our beliefs and expecta-ons and statements containing the words “may,” “could,” “would,” “should,” “believe,” “expect,” “an-cipate,” “plan,” “es-mate,” “target,” “project,” “intend” and similar expressions cons-tute forward-‐looking statements. These forward-‐looking statements involve known and unknown risks, uncertain-es and other factors that may cause results and performance in future periods to be materially different from any future results or performance suggested in forward-‐looking statements in this presenta-on. Investors, poten-al investors and other readers are urged to consider these factors carefully in evalua-ng the forward-‐looking statements and are cau-oned not to place undue reliance on such forward-‐looking statements. Any forward-‐looking statements speak only as of the date of this presenta-on and, except to the extent required by applicable securi-es laws, HFF (the Company) expressly disclaims any obliga-on to update or revise any of them to reflect actual results, any changes in expecta-ons or any change in events. If the Company does update one or more forward-‐looking statements, no inference should be drawn that it will make addi-onal updates with respect to those or other forward-‐looking statements.

Industry and Market Data

In this presenta-on, we rely on and refer to informa-on and sta-s-cs regarding economic condi-ons, trends, and our market in the sectors of that market in which we compete. In par-cular, we have obtained general industry informa-on and sta-s-cs from certain third-‐party sources. We believe that these sources of informa-on and es-mates are reliable and accurate, but we have not independently verified them.

Capital Markets Overview

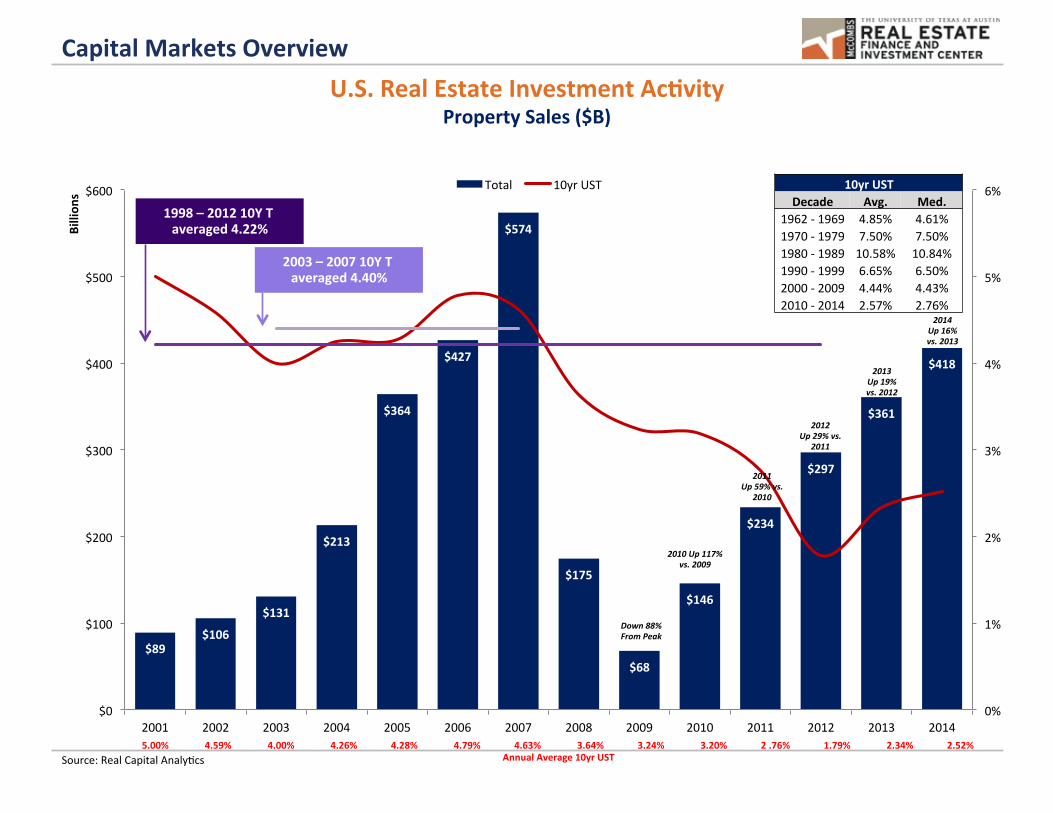

$89 $106

$131

$213

$364

$427

$574

$175

$68

$146

$234

$297

$361

$418

0%

1%

2%

3%

4%

5%

6%

$0

$100

$200

$300

$400

$500

$600

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Billion

s

Total 10yr UST

Source: Real Capital Analy-cs

U.S. Real Estate Investment AcOvity Property Sales ($B)

Down 88% From Peak

2010 Up 117% vs. 2009

2012 Up 29% vs.

2011

2003 – 2007 10Y T averaged 4.40%

1998 – 2012 10Y T averaged 4.22%

2013 Up 19% vs. 2012

2011 Up 59% vs.

2010

10yr UST Decade Avg. Med.

1962 -‐ 1969 4.85% 4.61% 1970 -‐ 1979 7.50% 7.50% 1980 -‐ 1989 10.58% 10.84% 1990 -‐ 1999 6.65% 6.50% 2000 -‐ 2009 4.44% 4.43% 2010 -‐ 2014 2.57% 2.76%

5.00% 4.59% 4.00% 4.26% 4.28% 4.79% 4.63% 3.64% 3.24% 3.20% 2 .76% 1.79% 2.34% 2.52% Annual Average 10yr UST

2014 Up 16% vs. 2013

Capital Markets Overview

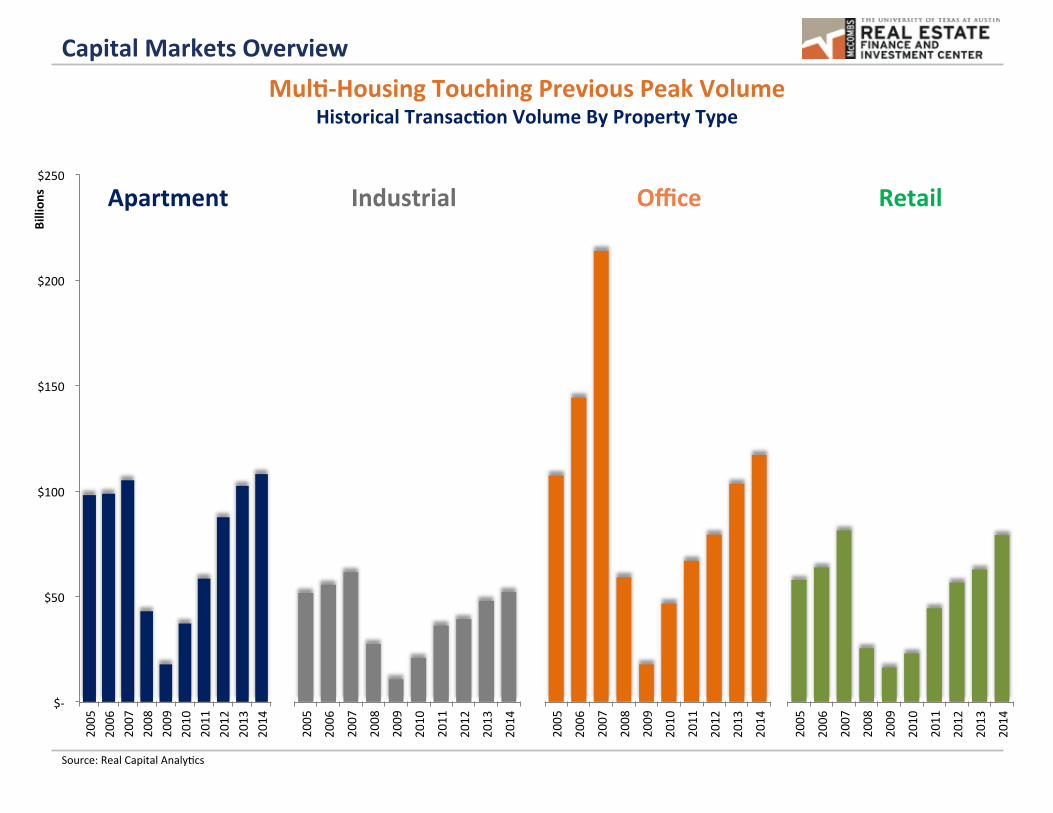

$-‐

$50

$100

$150

$200

$250

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Billion

s

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

MulO-‐Housing Touching Previous Peak Volume Historical TransacOon Volume By Property Type

Source: Real Capital Analy-cs

Apartment Industrial Office Retail

Capital Markets Overview

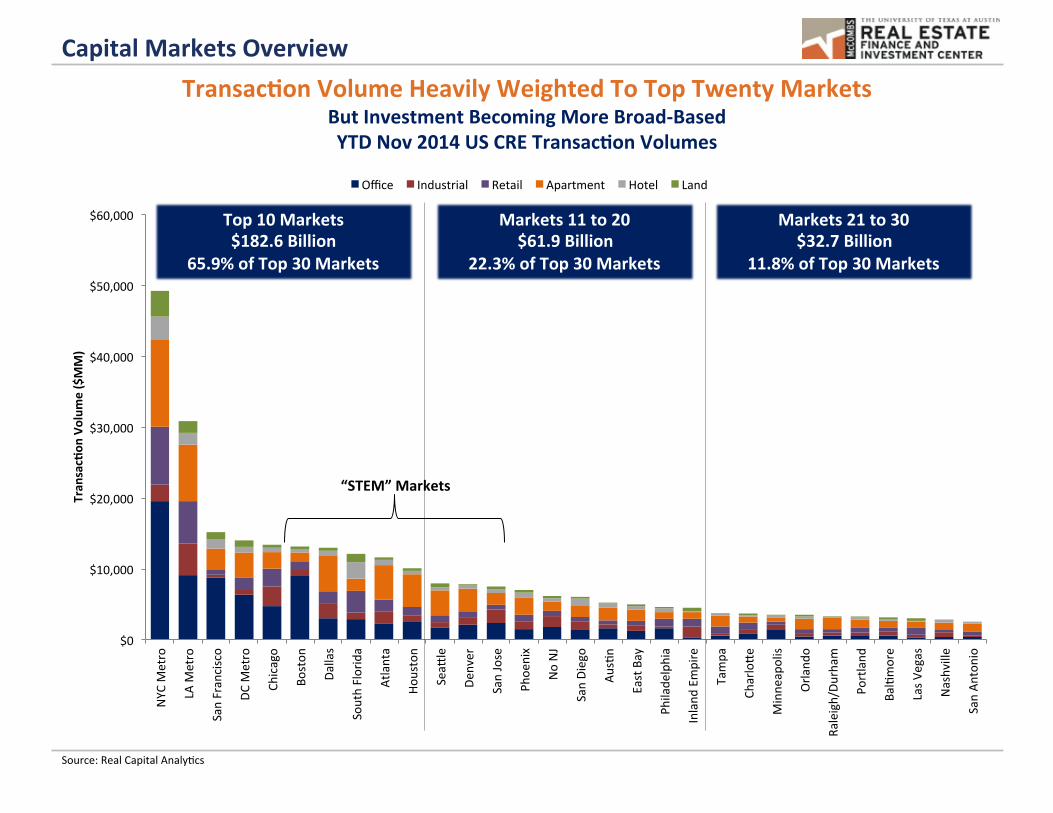

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

NYC

Metro

LA M

etro

San Francisco

DC M

etro

Chicago

Boston

Dallas

South Florida

Atlanta

Houston

Seac

le

Denver

San Jose

Phoe

nix

No NJ

San Diego

Aus-n

East Bay

Philade

lphia

Inland

Empire

Tampa

Charloce

Minne

apolis

Orla

ndo

Raleigh/Du

rham

Portland

Bal-more

Las V

egas

Nashville

San An

tonio

Tran

sacOon

Volum

e ($MM)

Office Industrial Retail Apartment Hotel Land

Source: Real Capital Analy-cs

TransacOon Volume Heavily Weighted To Top Twenty Markets But Investment Becoming More Broad-‐Based YTD Nov 2014 US CRE TransacOon Volumes

Top 10 Markets $182.6 Billion

65.9% of Top 30 Markets

Markets 11 to 20 $61.9 Billion

22.3% of Top 30 Markets

Markets 21 to 30 $32.7 Billion

11.8% of Top 30 Markets

“STEM” Markets

Capital Markets Overview Major Markets Have Recovered Peak Pricing

Major Markets Are 11.0% Above Previous Peak – Non-‐Major Markets Are -‐9.7% Off Peak – NaOonal 0.2% Off Peak Major Markets Have Increased 81.1% Since Bocom, Approximately 1.4x 56.9% Gain By Non-‐Major Markets

Source: Moody’s Analy-cs/Real Capital Analy-cs Major Markets include Boston, Chicago, Los Angeles, New York, San Francisco and Washington, D.C. This index measures prices changes in US commercial real estate, based on the completed sales of the same commercial proper-es over -me, known as the “repeat-‐sales methodology.”

80

100

120

140

160

180

200

220

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Na-onal Major Markets Non-‐Major Markets

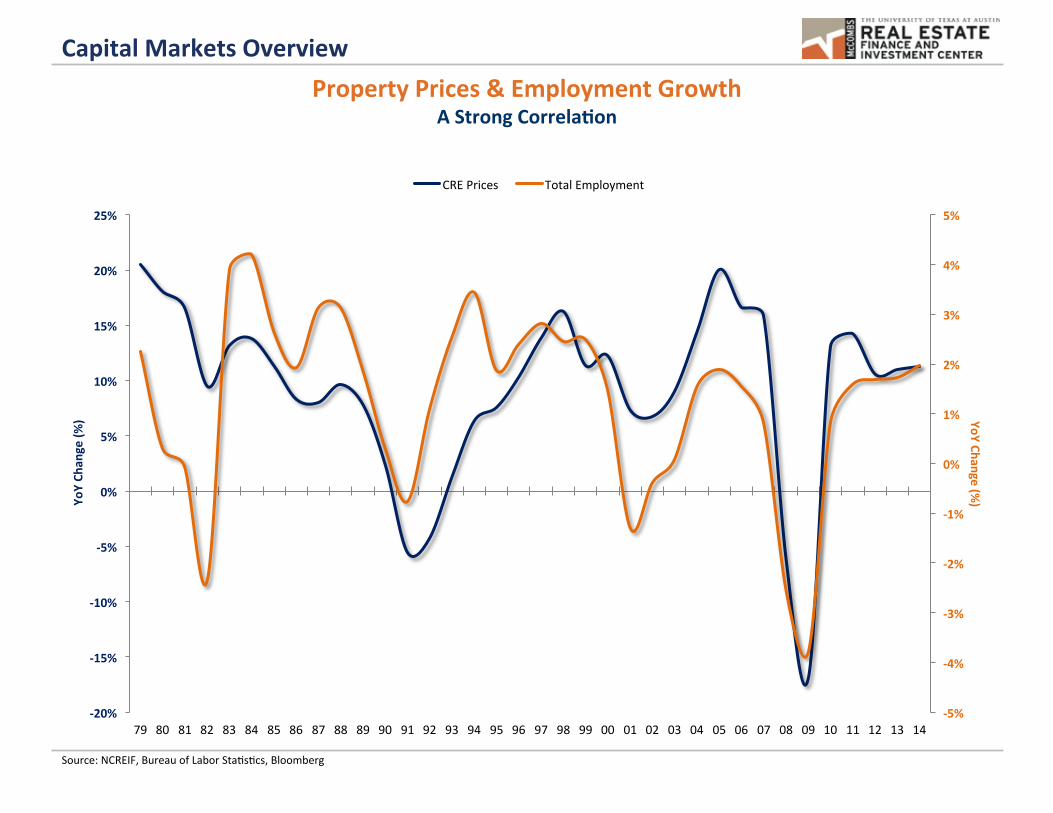

Capital Markets Overview Property Prices & Employment Growth

A Strong CorrelaOon

Source: NCREIF, Bureau of Labor Sta-s-cs, Bloomberg

-‐5%

-‐4%

-‐3%

-‐2%

-‐1%

0%

1%

2%

3%

4%

5%

-‐20%

-‐15%

-‐10%

-‐5%

0%

5%

10%

15%

20%

25%

79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

YoY Change (%) Yo

Y Ch

ange (%

)

CRE Prices Total Employment

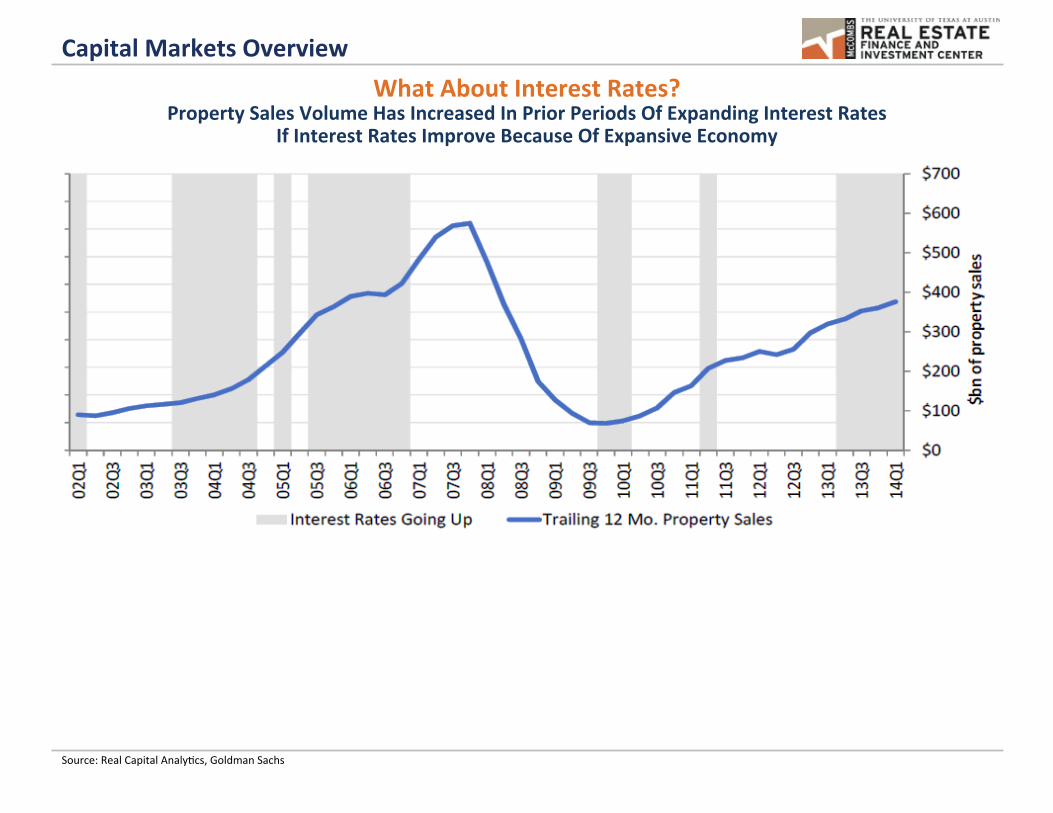

Capital Markets Overview What About Interest Rates?

Property Sales Volume Has Increased In Prior Periods Of Expanding Interest Rates If Interest Rates Improve Because Of Expansive Economy

Source: Real Capital Analy-cs, Goldman Sachs

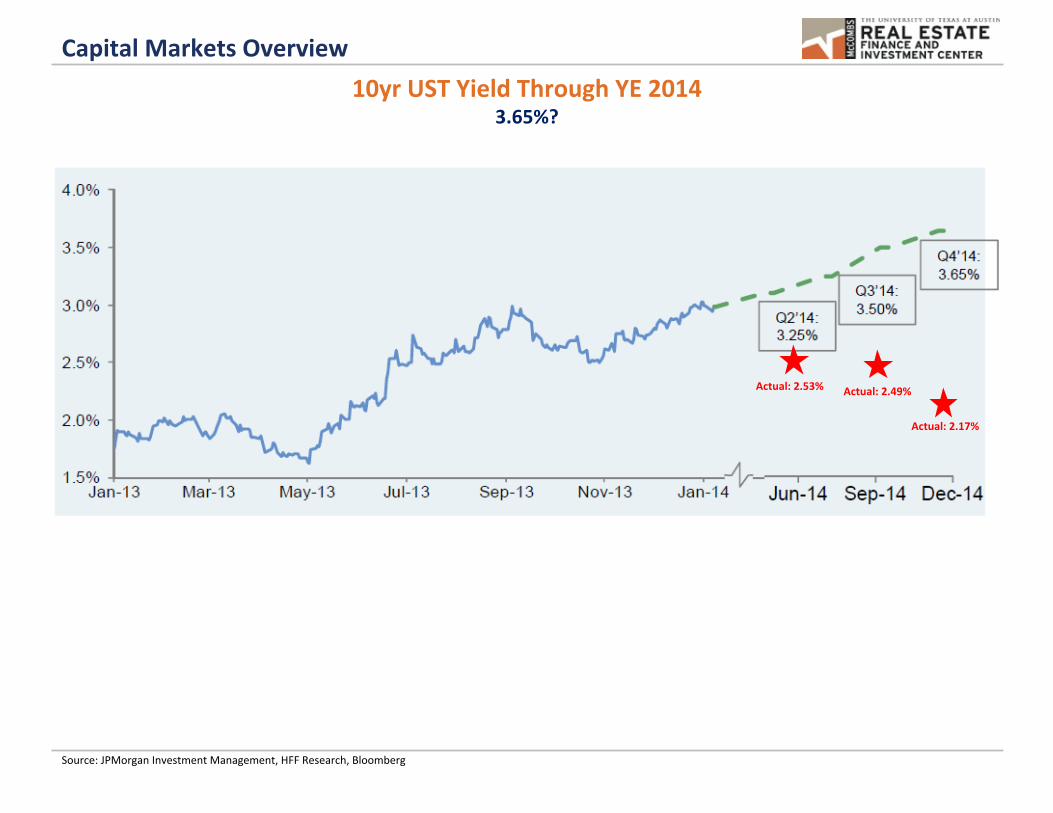

Capital Markets Overview 10yr UST Yield Through YE 2014

3.65%?

Source: JPMorgan Investment Management, HFF Research, Bloomberg

Actual: 2.53% Actual: 2.49%

Actual: 2.17%

Capital Markets Overview

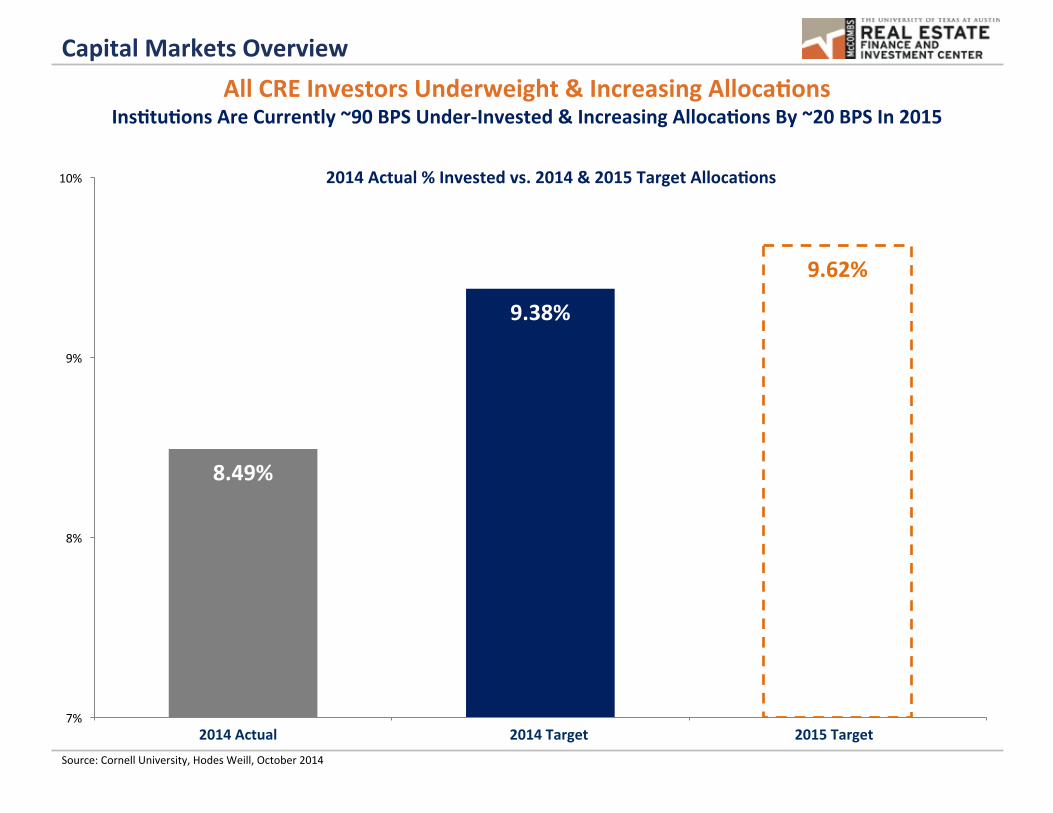

Source: Cornell University, Hodes Weill, October 2014

All CRE Investors Underweight & Increasing AllocaOons InsOtuOons Are Currently ~90 BPS Under-‐Invested & Increasing AllocaOons By ~20 BPS In 2015

2014 Actual % Invested vs. 2014 & 2015 Target AllocaOons

8.49%

9.38%

9.62%

7%

8%

9%

10%

2013 2014 2015f 2014 Actual 2014 Target 2015 Target

Capital Markets Overview

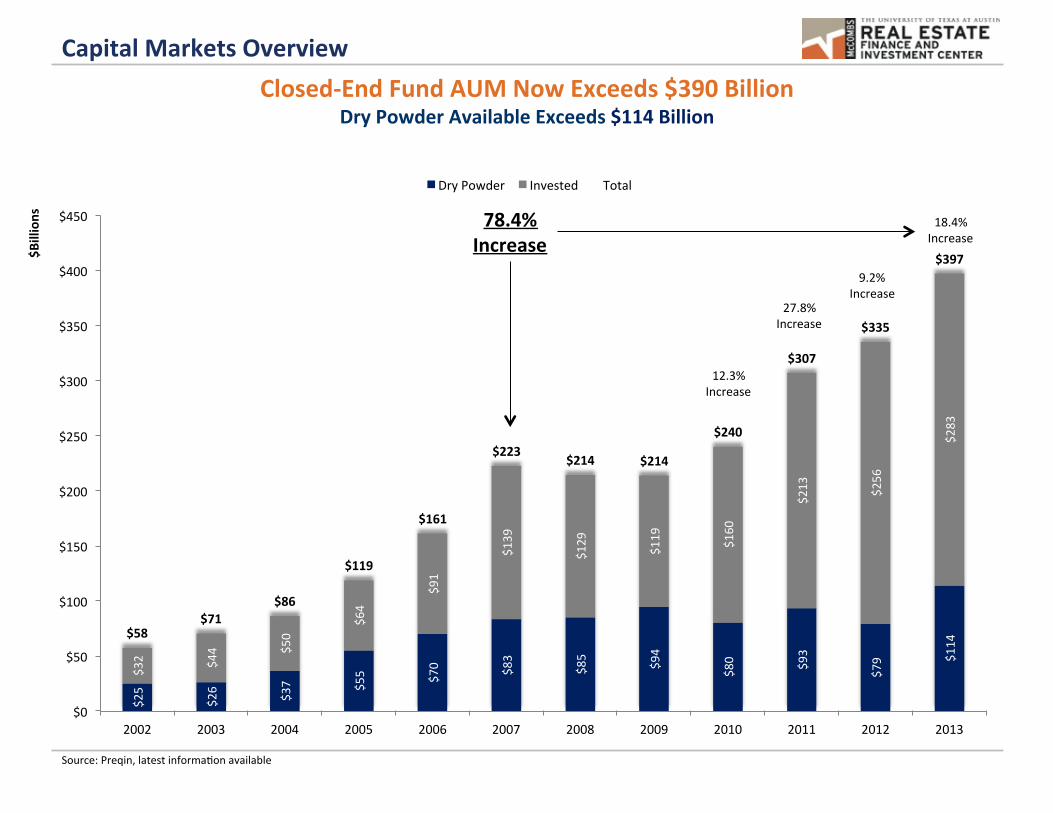

$25

$26 $37 $55 $70 $83

$85 $94

$80 $93

$79 $1

14

$32 $44 $5

0

$64

$91

$139

$129

$119

$160

$213

$256

$283

$58 $71

$86

$119

$161

$223 $214 $214

$240

$307

$335

$397

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Dry Powder Invested Total

9.2% Increase

27.8% Increase

12.3% Increase

Closed-‐End Fund AUM Now Exceeds $390 Billion Dry Powder Available Exceeds $114 Billion

18.4% Increase

78.4% Increase

Source: Preqin, latest informa-on available

$Billions

Capital Markets Overview

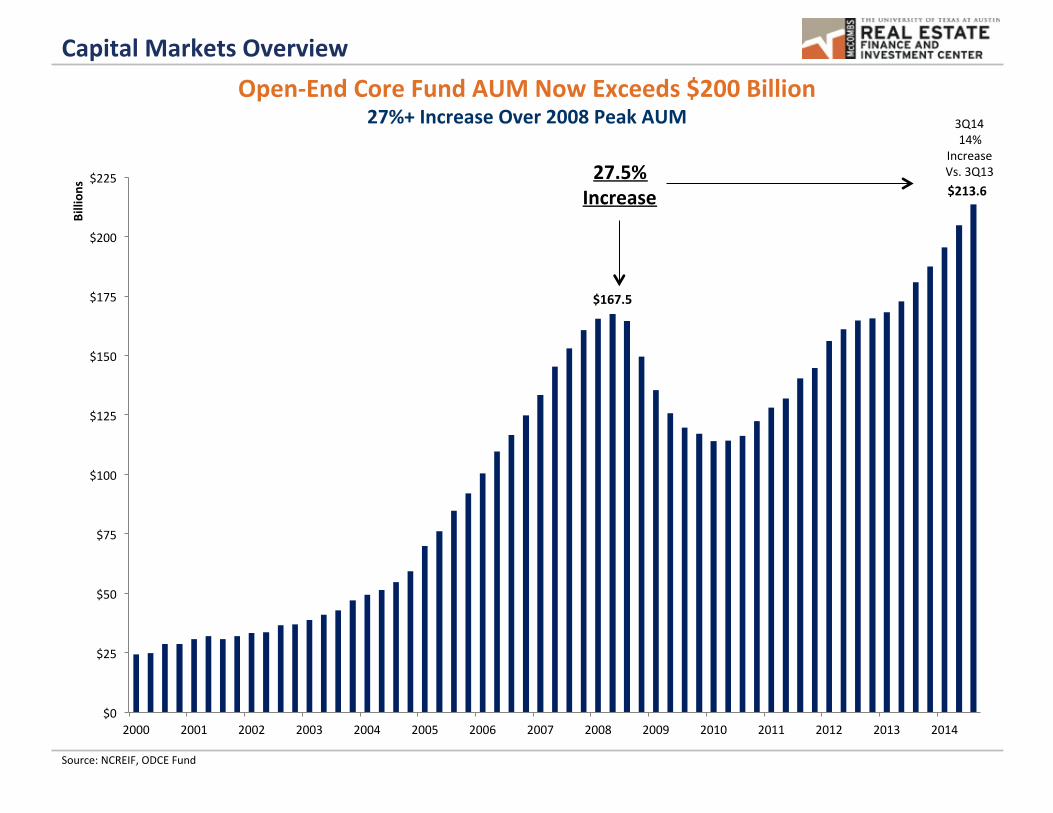

$167.5

$213.6

$0

$25

$50

$75

$100

$125

$150

$175

$200

$225

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Billion

s Open-‐End Core Fund AUM Now Exceeds $200 Billion

27%+ Increase Over 2008 Peak AUM

27.5% Increase

Source: NCREIF, ODCE Fund

3Q14 14%

Increase Vs. 3Q13