1. william m. leroy - moderator president & ceo american legal & financial network...

TRANSCRIPT

1

William M. LeRoy - ModeratorPresident & CEOAmerican Legal & Financial Network “ALFN”

Alan S. Wolf, Esq. - PanelistPresident & Managing AttorneyThe Wolf Firm, A Law Corporation

Joseph J. Nardulli, Esq. - PanelistLead Trial Counsel The Wolf Firm, A Law Corporation

2

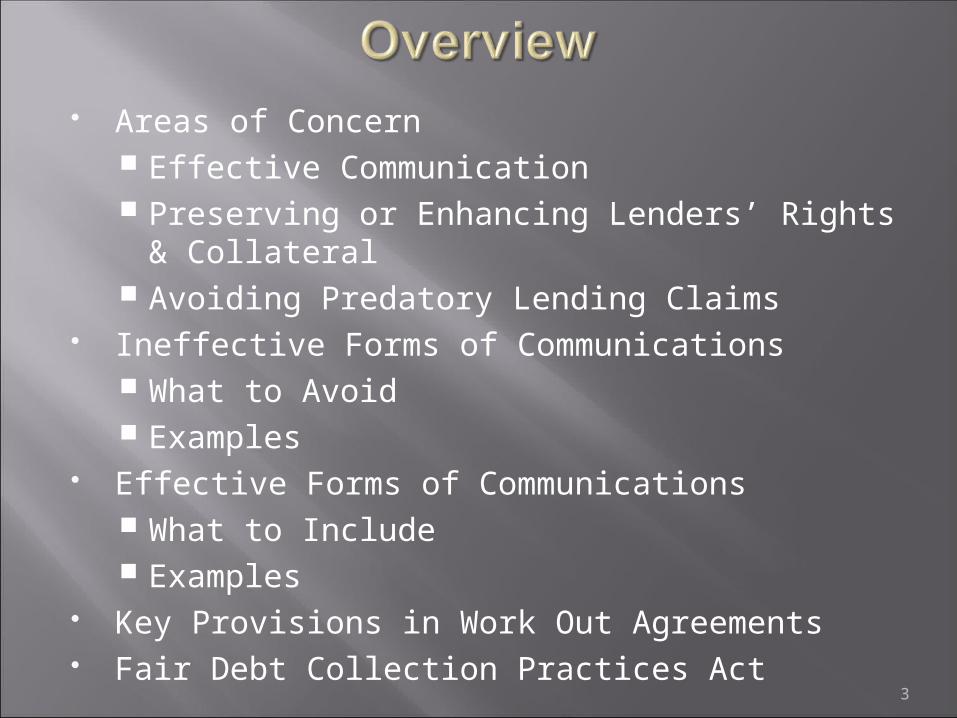

Areas of Concern Effective Communication Preserving or Enhancing Lenders’ Rights &

Collateral Avoiding Predatory Lending Claims

Ineffective Forms of Communications What to Avoid Examples

Effective Forms of Communications What to Include Examples

Key Provisions in Work Out Agreements Fair Debt Collection Practices Act

3

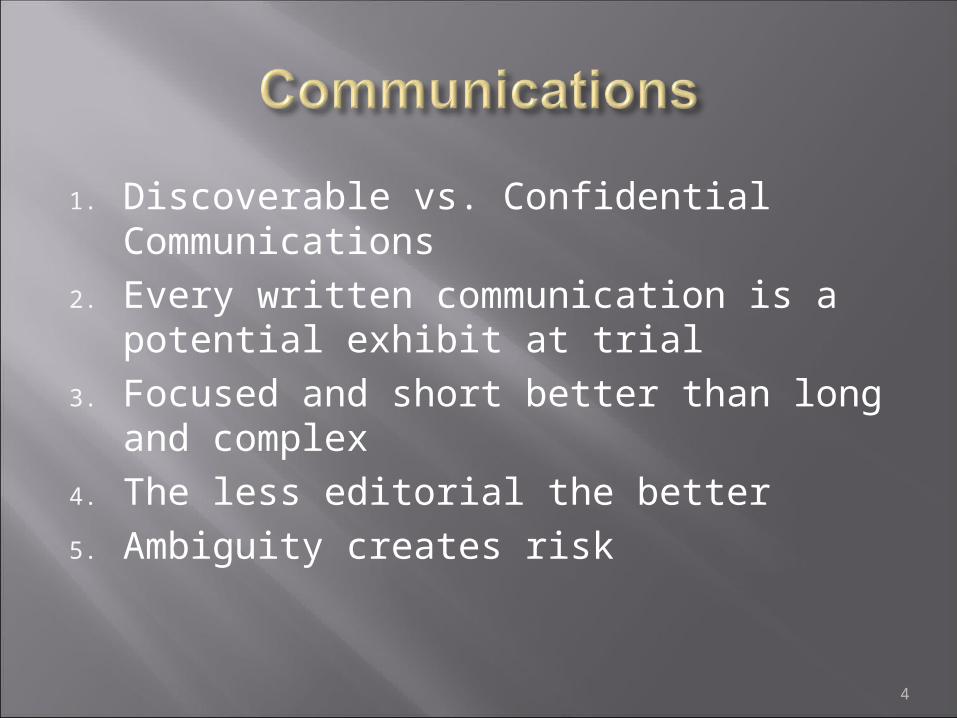

1. Discoverable vs. Confidential Communications

2. Every written communication is a potential exhibit at trial

3. Focused and short better than long and complex

4. The less editorial the better

5. Ambiguity creates risk

4

Unintended promises or assurances Ambiguous statements Conveying internal discord Poor follow-up Breaching the attorney/client privilege Heavy handed statements Untrue statements Oversell

5

1. John, I know the stress you are under. I assure you that the Bank will work with you to find a solution regarding your loan.

2. John, I do not care what kind of pressure you and your family are under, I am also under pressure with all the loan defaults the Bank has, including yours. This loan needs to be brought current and it needs to brought current now!

6

3. John; we do not have to make any “special” deals with you. I really don’t care what you have read about short sales, the bank is under no obligation to bend over backwards for you on your delinquent loan.

4. John; I can’t get Bank Management to pay attention. The proposal you made is very fair and should be reviewed favorably by the Bank. Hold tight for now and I will get back to you as soon as I can obtain authority.

7

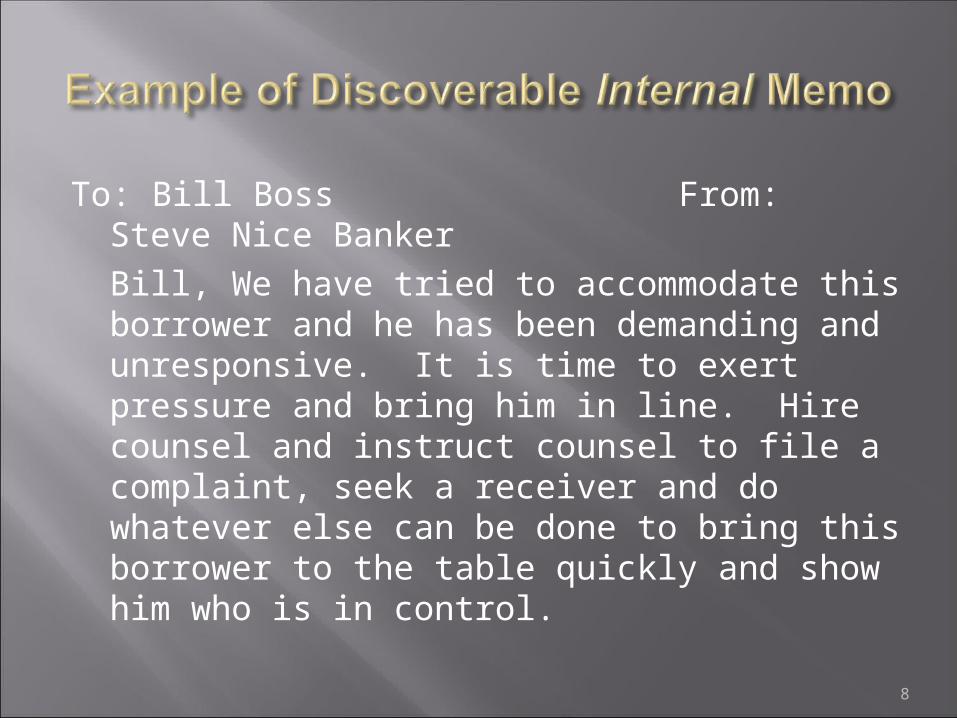

To: Bill Boss From: Steve Nice Banker

Bill, We have tried to accommodate this borrower and he has been demanding and unresponsive. It is time to exert pressure and bring him in line. Hire counsel and instruct counsel to file a complaint, seek a receiver and do whatever else can be done to bring this borrower to the table quickly and show him who is in control.

8

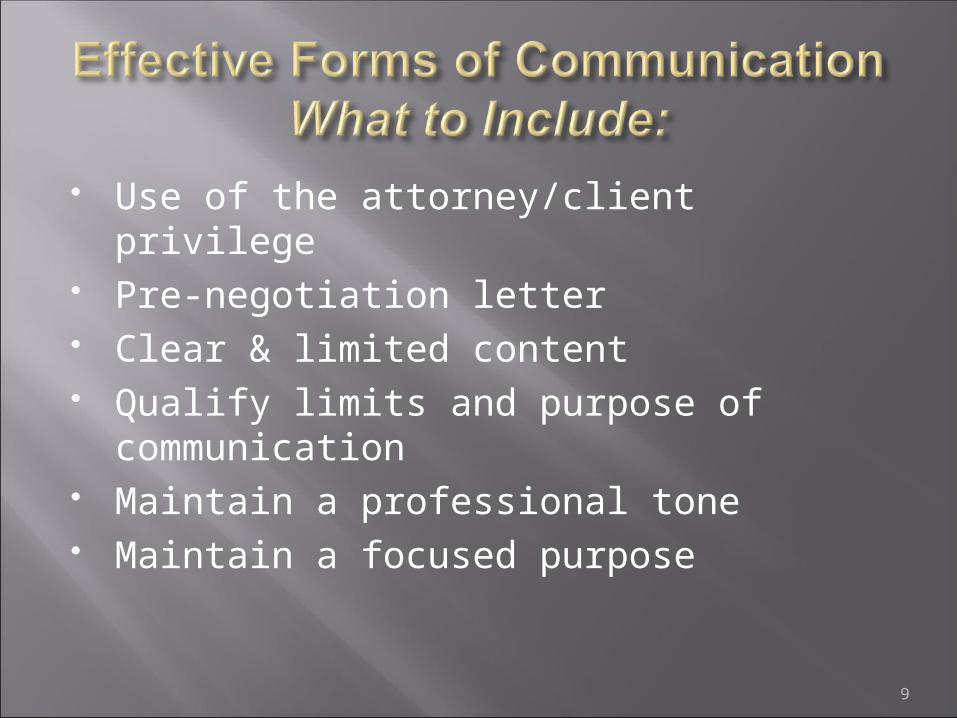

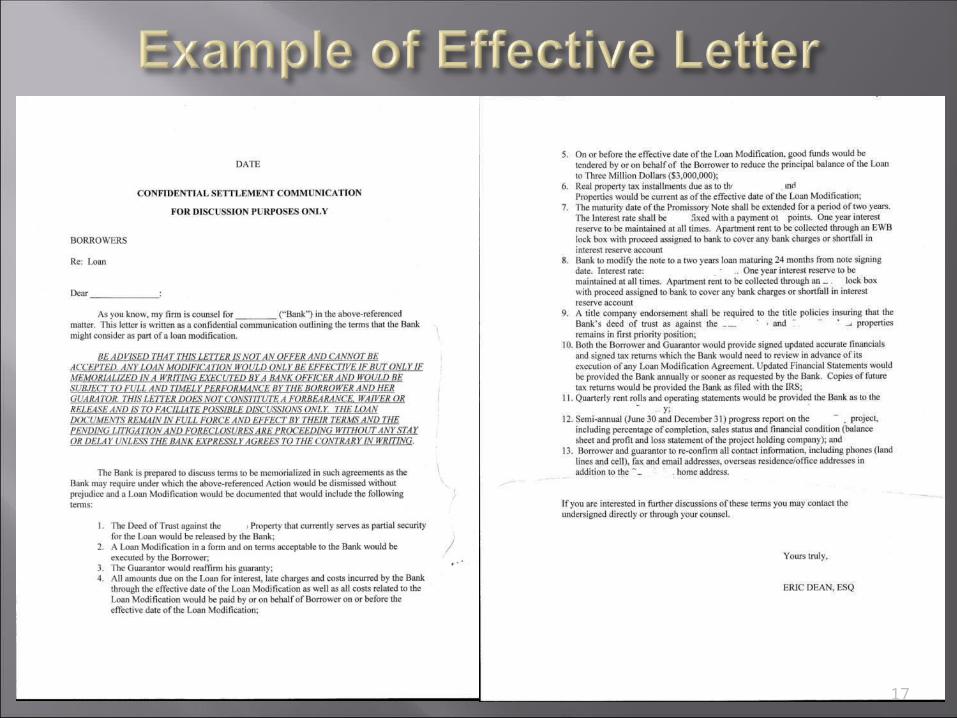

Use of the attorney/client privilege Pre-negotiation letter Clear & limited content Qualify limits and purpose of communication Maintain a professional tone Maintain a focused purpose

9

To: Bill Boss From: Steve Nice Banker

CC: Attorney

Bill, The borrower has failed to agree to a resolution acceptable to the Bank. Please therefore, have counsel pursue legal redress to protect the Bank’s claims and collateral, including the filing of a complaint and requesting the appointment of a receiver. Our goal remains reaching a consensual resolution of the loans, if the borrower will agree to terms acceptable to the Bank. Hopefully, the borrower will move forward with discussions of a work out, once suit is filed.

10

11

12

13

14

15

16

17

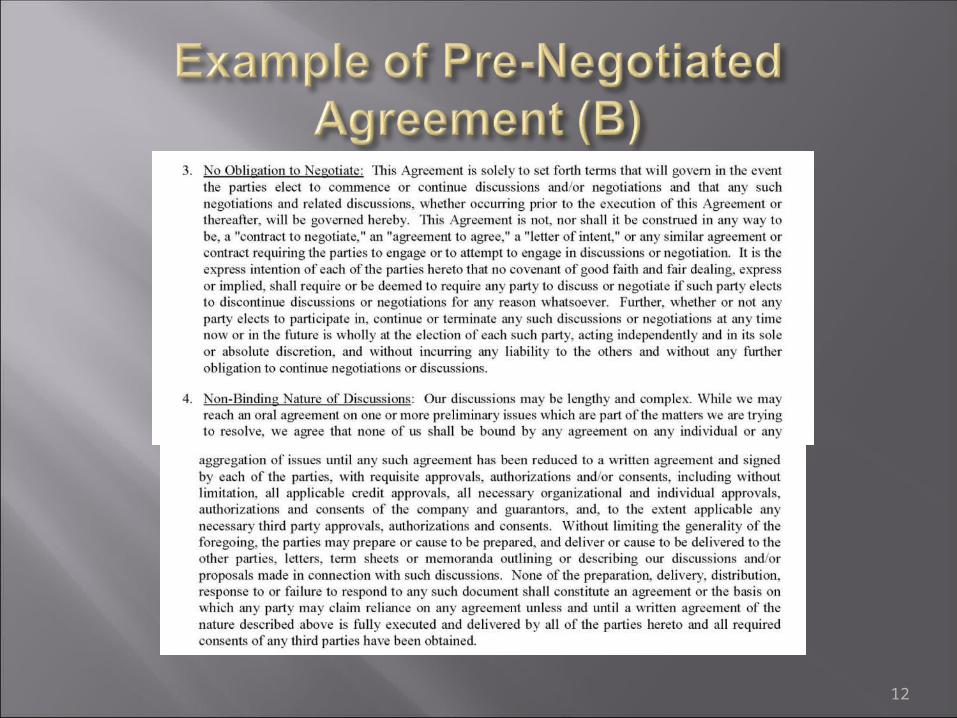

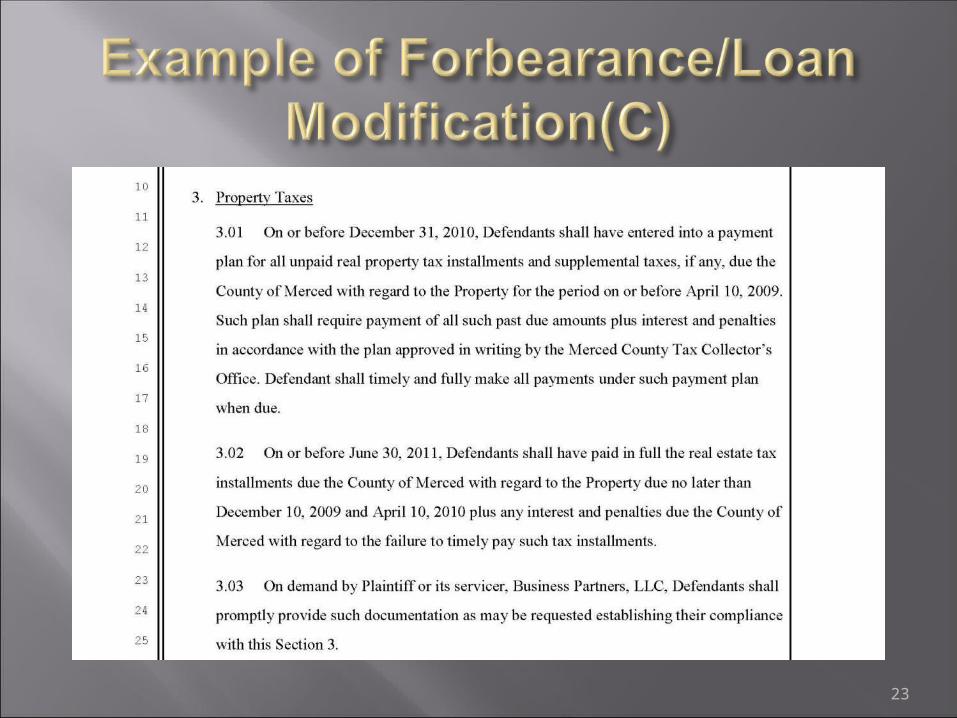

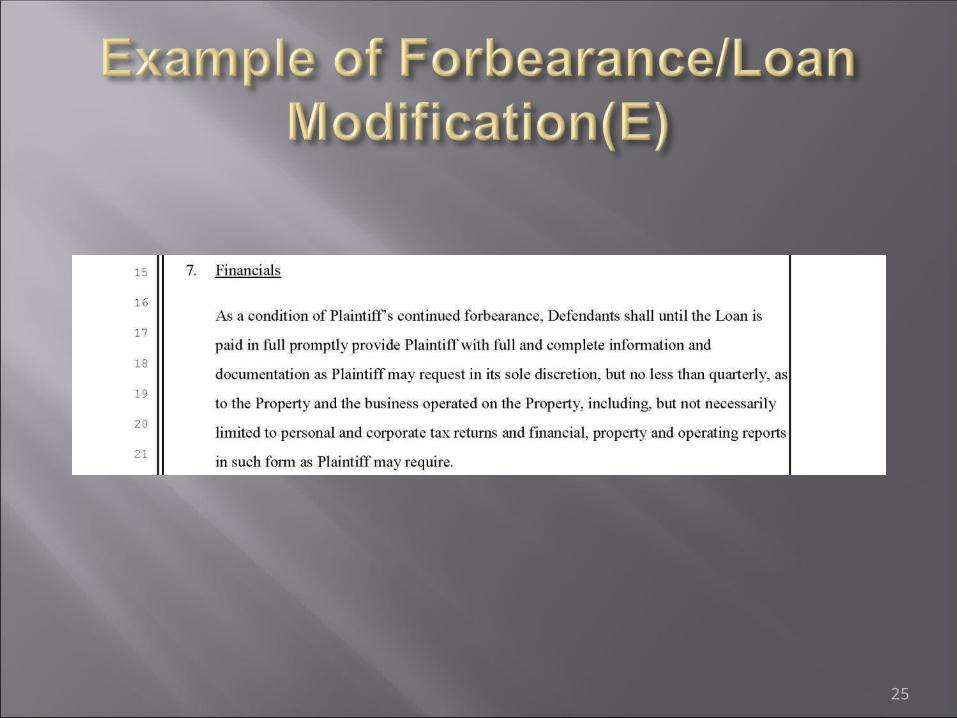

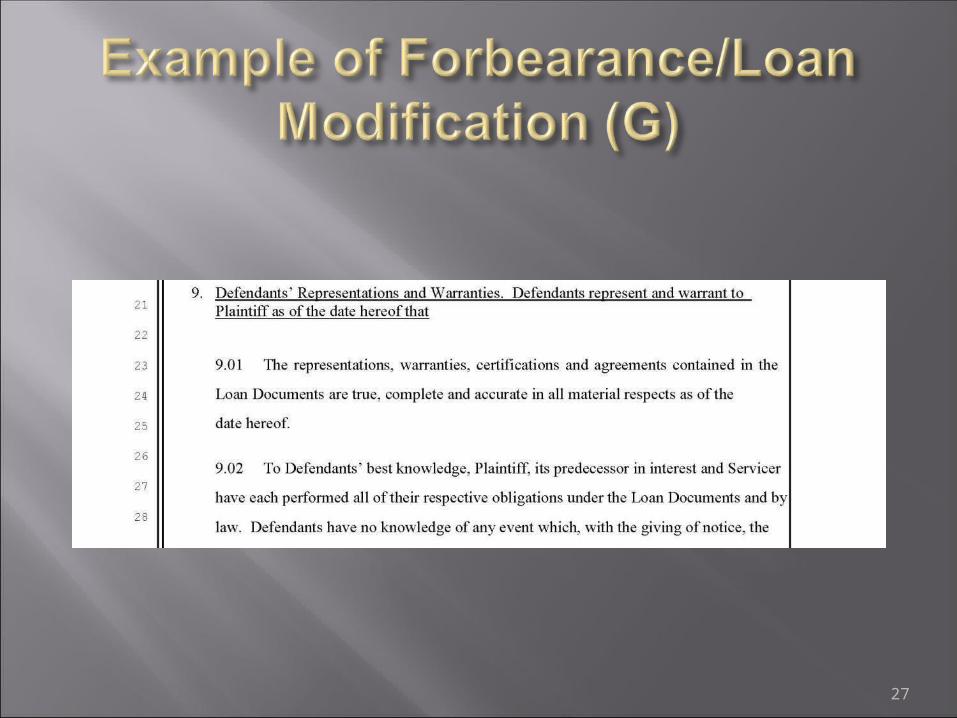

Must include: Clean description of borrower responsibilities Approval and acknowledgement of guarantors Clean description of limits of agreement Acknowledgement of loan documents & status Releasing claims by borrower Statement of conditions to forbearance on

modification Consequences of a default

18

19

20

21

22

23

24

25

26

27

28

29

Transfer of ownership or servicing rights when the loan is in default Meaning of Default

30

Must be a Private Communication The answering machine problem.

Hours- 8 a.m. and 9 p.m. local time Cannot speak to borrower if borrower represented by an attorney.

But can speak to borrower if borrower represented by a nonlawyer who holds a power of attorney granted by the debtor. Edwards, FTC Staff Opinion Letter (Feb. 7, 1991).

Must communicate as if least sophisticated consumer The California case

No harassment, abuse or threats. No False or misleading representations

31

Debt collector must disclose that it is attempting to collect a debt and that any information obtained may be used to collect the debt. In subsequent communications, the debt collector must disclose that the communication is from a debt collector. 15 USC §1692e(11).

32

Within 5 days of initial communication a notice containing the debt amount, the creditor's name, a statement that the debt is assumed to be valid unless the consumer disputes the validity of all or any part of the debt within 30 days after receiving the notice, and a statement that on written request the debt collector will provide the consumer with the original creditor's name and address. 15 USC §1692g(a); Legal proceedings are not an initial communication 15 USC

1692g(d).

33

California has its own statute (Rosenthal Act)

34

If you have any further questions that were not addressed in this presentation, or want to contact one of our speakers, please email Matt Bartel, COO of ALFN, at [email protected]. Thank you for your participation in this webinar. Please complete the brief survey which you will be directed to at the conclusion of this presentation.

ALFN provides the information contained in these webinars as a public service for educational and general information purposes only, and not provided in the course of an attorney-client relationship. It is not intended to constitute legal advice or to substitute for obtaining legal advice from an attorney licensed in the relevant jurisdiction.

Use of ALFN Webinar Materials The information, documents, graphics and other material made available through this Webinar are intended for use solely in connection with the American Legal and Financial Networks (hereinafter “ALFN”) educational activities. These materials are proprietary to ALFN, and may be protected by copyright, trademark and other applicable laws. You may download, view, copy and print documents and graphics incorporated in the documents from this Webinar ("Documents") subject to the following: (a) the Documents may be used solely for informational purposes related to the educational programs offered by the ALFN; and (b) the Documents may not be modified or altered in any way. Except as expressly provided herein, these materials may not be used for any other purpose, and specifically you may not use, download, upload, copy, print, display, perform, reproduce, publish, license, post, transmit or distribute any information from ALFN Webinars in whole or in part without the prior written permission of ALFN. 35