1 wharton financial institutions center policy brief: personal finance david f. babbel fellow,...

TRANSCRIPT

1

Wharton Financial Institutions Center

Policy Brief: Personal Finance

David F. BabbelFellow, Wharton Financial Institutions Center

Professor of Insurance and Finance, The Wharton SchoolUniversity of Pennsylvania

LIBR5

2

David F. Babbel Professor of Insurance and Finance The Wharton School, Univ. of Pennsylvania

• Two year in-depth study of Fixed Indexed Annuities - six Ph.D. Economists – two senior actuaries

• Since inception in 1995 many FIAs have outperformed corporate and government bonds, equity mutual funds, and money markets in any combination

• Not in a year here and there but in every year!

(AnnuityDigest, July 26, 2009)

3

David F. Babbel Professor of Insurance and Finance The Wharton School, Univ. of Pennsylvania

A separate study, Investing Your Lump Sum in Retirement, says:

• “The list of positive attributes of annuities, i.e. guaranteed payments you cannot outlive, access to investment capital and legacy benefits, the argument for this income solution in retirement is compelling.”

• “The key in all of this is to begin by covering all of the basic living expenses with lifetime income annuities.”

(Policy Brief: Investing Your Lump Sum at Retirement, August, 2007)

4

David F. Babbel Professor of Insurance and Finance The Wharton School, Univ. of Pennsylvania

• “Then, to provide for additional desirable consumption levels, you will want to annuitize a goodly portion of the remainder of your assets while making provisions for extra emergency expenses.”

• “When this is undertaken, you can enjoy your retirement without the burden of financial worries and focus on productive uses of your time and attention!”

(Policy Brief: Investing Your Lump Sum at Retirement, August, 2007)

5

Facts aboutFixed Indexed Annuities

6

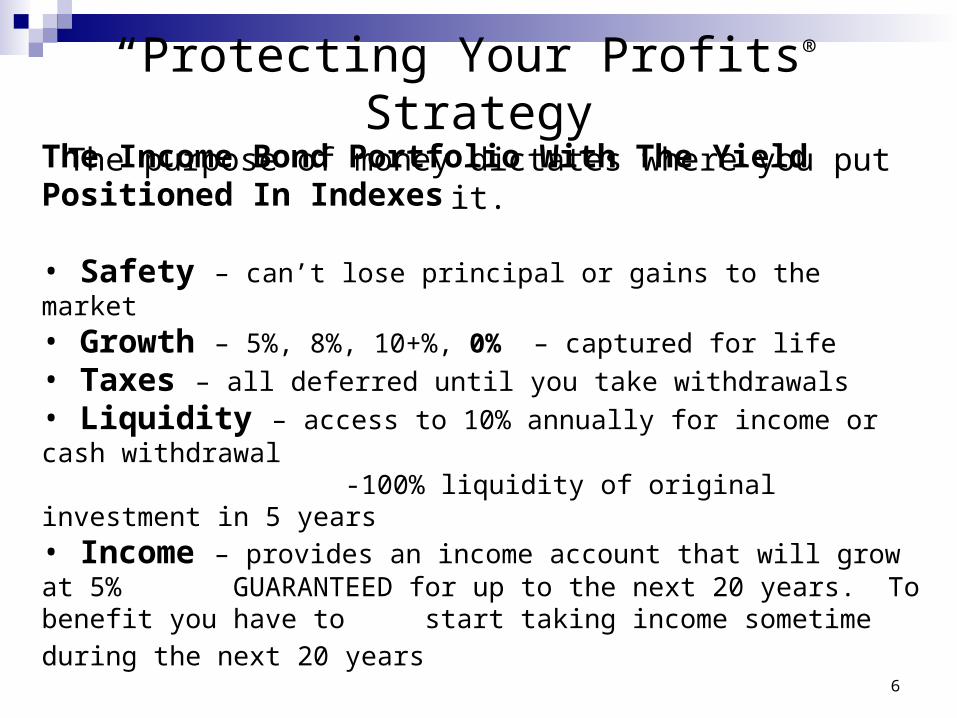

The Income Bond Portfolio With The Yield Positioned In Indexes

• Safety – can’t lose principal or gains to the market • Growth – 5%, 8%, 10+%, 0% – captured for life • Taxes – all deferred until you take withdrawals • Liquidity – access to 10% annually for income or cash withdrawal

-100% liquidity of original investment in 5 years• Income – provides an income account that will grow at 5%

GUARANTEED for up to the next 20 years. To benefit you have to start taking income sometime during the next 20 years

“Protecting Your Profits®” Strategy

The purpose of money dictates where you put it.

7

Moderate returns that never experience a loss can

outperform the stock market over time.

8

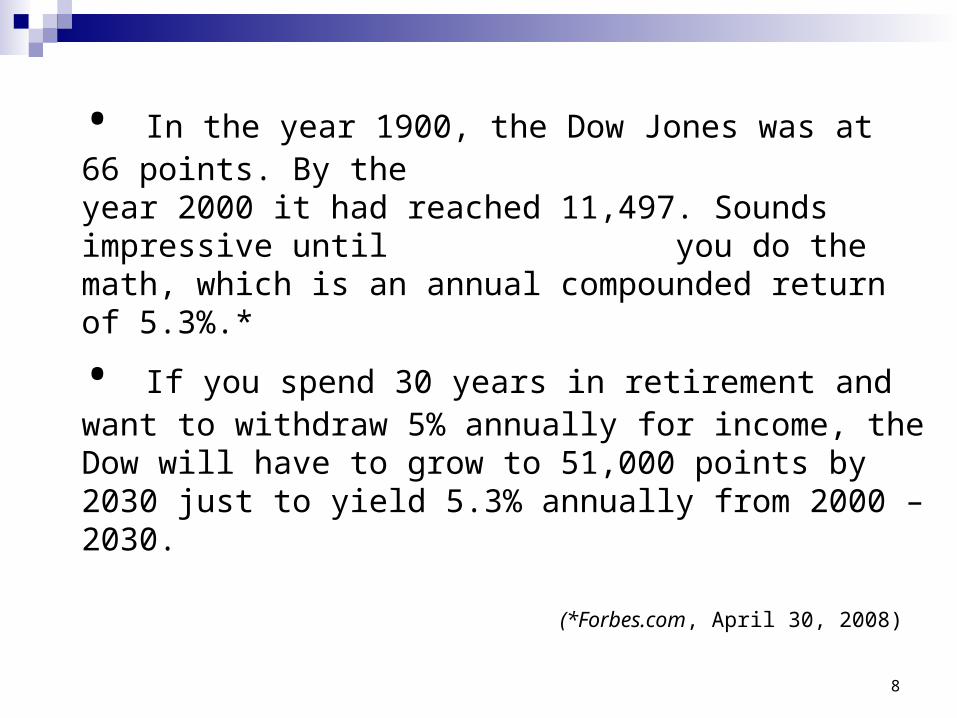

• In the year 1900, the Dow Jones was at 66 points. By theyear 2000 it had reached 11,497. Sounds impressive until you do the math, which is an annual compounded return of 5.3%.*

• If you spend 30 years in retirement and want to withdraw 5% annually for income, the Dow will have to grow to 51,000 points by 2030 just to yield 5.3% annually from 2000 – 2030.

(*Forbes.com, April 30, 2008)

9

There's tremendous power in annual reset – If youdon’t capture the gains while they are there, you will likelylose them (they are only paper gains).

DJIA – November 13, 1997 7,487DJIA – March 18, 2009 7,486

Twelve years and nothing to show for it!

No one has retired on unrealized gains!

10

The Dow Jones Industrial Average has suffered huge one-day declines. Here are the Dow’s biggest daily declines through September 17, 2001:

Oct. 19, 1987 ↓ 508 (22.6% drop, the Black Monday crash)

Oct. 27, 1997 ↓ 554 (third largest dollar loss in history)

Aug. 31, 1998 ↓ 513 (fourth largest dollar loss in history)

April 14, 2000 ↓ 618 (second largest dollar loss in history)

Sept. 17, 2001 ↓ 685 (More than $700 billion in wealth obliterated)

11

Since September 15, 2008, the declines are becoming larger and more frequent:

Sept. 15, 2008 ↓ 504 (Lehman Bros. & Merrill Lynch collapse)

Sept. 29, 2008 ↓ 778 (largest point loss in history)

October 15, 2008 ↓ 733 (second largest point loss in history)

December 1, 2008 ↓ 680 (fourth largest point loss in history)

March 9, 2009 (Down 53.78% from the all-time high on Oct 9, 2007)

12

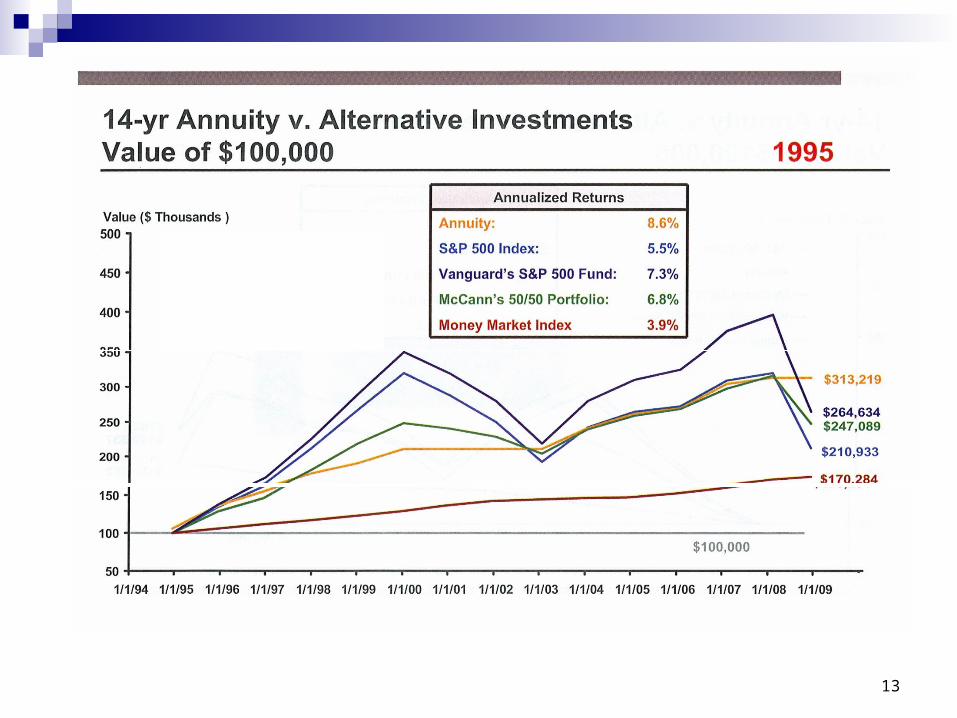

13

14

DJIA 1900 – 2000 5.3%S&P 500 Jan 1995 – Jan 2009 5.5%FIA Jan 1995 – Jan 2009 8.6%

You can put up your money, take all the risk and earn 5.3 - 5.5%, doubling your money in 13.3 years

OR you can put up your money, take no market risk and earn 8.6%, doubling your money in 8.3 years

15

Income You Can Not Outlive

• Grows at a Guaranteed Rate during deferral

• Payout is determined by age and value in the income account

• Payout continues for LIFE, regardless if the accumulation value is depleted

• You maintain control of the accumulation value

• NO fees

16

Have you ever gone to a dealership and asked them to show you a car that gets

300 mpg?

One Hybrid Vehicle - Two Engines

17

One Hybrid Vehicle

Accumulation Engine> 0-20%> 10% per year withdrawals> Withdraw up to 50% in one day> 10% bonus> S&P 500 Index> Dow Jones Index> 10-year U.S. Treasury Bond> Fixed Account> Children can inherit balance of principal

Income Engine> 5% annual growth> 5% lifetime income*> 10% bonus> Income lasts for you & your spouse if you elect the spouse option> Income just like pensions and social security is not inheritable by the children

*Varies by age

YOU GET THE PERFORMANCE OF WHICHEVER ENGINE DOES BETTER

Two Engines