1 the quality of the payment system who’s concern?

TRANSCRIPT

1

The quality of the Payment SystemWho’s concern?

Copyright NCB ConsultingCopyright NCB Consulting

www.ncbconsulting.nlwww.ncbconsulting.nl

2

Content

Definition Payment SystemOversight (tasks and organisation)Poll/surveyConcern quality payment systemConcluding remarksQuestions

3

The Payment System - Definition

4

The Payment System - Definition

ALL LINKS IN THE CHAIN SHOULD BE STRONG

5

The payment chain:

Paymentinstrument

Channel/medium

Transaction processing

Clearing Settlement

6

The Payment System - Definition

• Starts and ends at the client

• Starts with Payment Instruments like: credit transfer, direct debit, debit and credit cards, e-purses and• In Payment Instruments are included Input Devices like the POS terminal, the home PC, the telephone equipment, an ATM with input facilities

7

The Payment System - Definition

•Channels: mail system and telecommunication connections like telephone lines, local networks, wide area networks like internet

•Other institutions like Acquirers, Clearing institutions, Issuers, Processors, Settlement institutions (incl. for securities settlement)

•Ends at the client via paper or electronic output

8

Legal Owner

Issuer

Clearing Institution

Acquirer

Issuing processor

Clearing processor

Acquiringprocessor

Settlement processor

Settlement Institution

Retailer

Networkprocessor

Acceptant Payment Service Provider

Scheme oriented organisation retail payments

Acceptantser

vice providor

Acquirer

Consumer

9

Basis of the Payment System:

10

Payment system is all about trust...

Trust Currency Trust Issuer Trust Payment system Trust Authenticity Trust Legal system

11

Mission of the central bank

A National Central Bank (NCB) is responsible for safeguarding financial stability.

More particularly, a NCB contributes to – defining and implementing the monetary policy; – promotes the smooth operation of the payment system; – and can supervise financial institutions and the financial

sector. – All NCB’s have an active role in payments. – Per NCB differences may exist in the active role in

payments.

12

Mission of the central bank

Scope

Monetary stability: stable currency

Financial sector stability: reliable financial

institutions

Payment system: smooth and secure

payments

13

Payments: different roles of a NCB

Operator - Cash - Large value payment system - Services to securities settlement systems

Overseer - Payment systems - Payment productsCatalyst

14

Oversight task

Oversight is a task of a central bank aiming:

– Contributing to the reduction of systemic risks by

performing oversight on the payment system

– Promoting the adequate functioning of the

payment system by performing oversight on this

system

– Contributing to financial stability

15

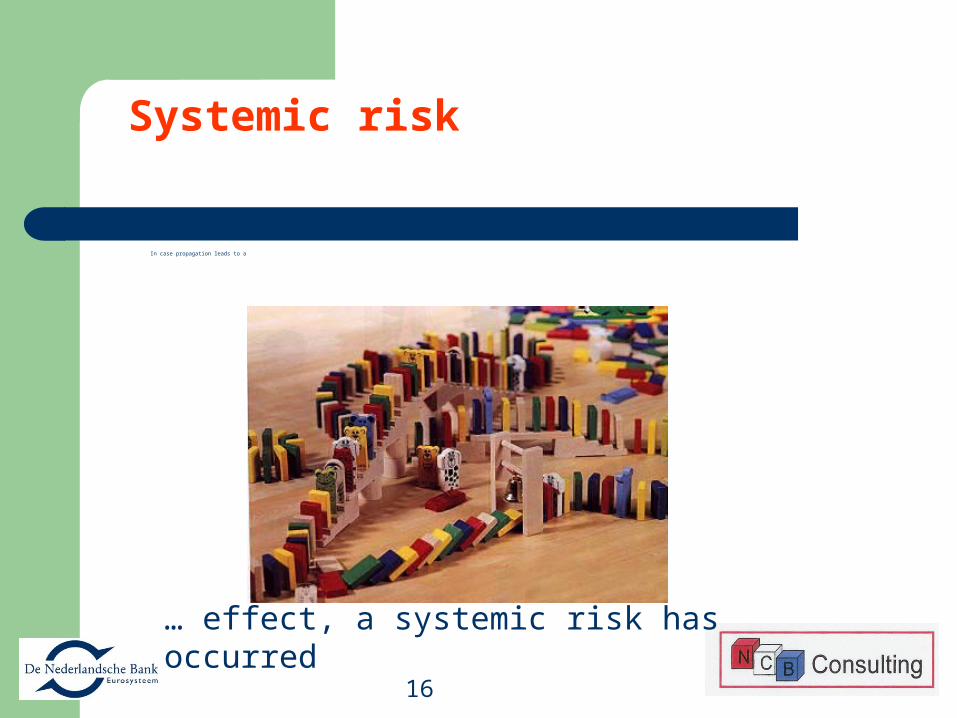

Systemic risk

Systemic risk is the risk that propagation of a serious failure in a sector of the society will imperil other sectors (a ‘domino’ effect).

The infection is propagated via the interfaces between the sectors

16

Systemic risk

In case propagation leads to a

… effect, a systemic risk has occurred

17

Oversight’s objectives

Objectives Reduce systemic risk Smoothen payment system Maintaining public confidence

in the safety of the payment system

18

Staffing: organisation at DNB

Multidisciplinary staff (11, including head of

department): lawyers, risk management experts,

(IT) auditors, economists

experience in securities, payments and / or

supervision

19

Deliverables of oversight

Assessment reports:

Initial assessment in case of new system

Partial assessment in case of major change

Annual oversight report

Internal: extensive, including sensitive findings

External: summary of conclusions

Regular oversight

Regular meetings (monthly, quarterly)

Regular reporting of statistics, incidents, financials (monthly quarterly)

Ad hoc reporting in case of crises

20

Standards

Assessments based on standards

Use of international standards if available

By using standards the level of playing field is guaranteed

Authority to set up minimum standards for the objects of oversight (oversight framework)

21

Oversight standards (1)

Wholesale

Core principles for systemically important

payments systems (SIPS) (BIS, 2001)

Terms of Reference for the assessment of

Large Value Payment Systems (LVPS) (ECB)

22

Oversight standards (2)

Retail

Framework for the Oversight on Card Payment

Systems (ECB)

Recommendations for Payment Products (DNB)

Oversight standards for Euro Retail Payment

Systems (ECB)

Electronic Money Security System Objectives

(ECB)

23

Oversight standards (3)

SecuritiesRecommendations for Central

Counterparties (CCPs) (CPSS/IOSCO, 2004)

Recommendations for Securities Settlement Systems (SSS) (CPSS/IOSCO, 2001)

24

Annual report Oversight

Transparency - ´Central banks should set out publicly their oversight policies, including the policy requirements or standards for systems and the criteria for determining which systems these apply to´, CPSS 2005

Enforcement tool – no legal instruments for Oversight, except ´moral suasion´

25

Trends / developments

Consolidation / concentration European consolidation underway

– TARGET2– Single European Payment Area (SEPA)– LCH.Clearnet mergers– Euroclear mergers

26

Trends / developments

Competition, fragmentation

MiFID and Code of conduct for clearing and

settlement

New trading platforms and CCPs compete with

incumbents (EMCF new CCP in the Netherlands)

Interoperability between trading platforms, CCPs and

CSDs create equal access and competition

27

Trends / developments

Specialisation

multiple operators/owners: card schemes, transaction

networks, imaging and clearing new providers of payment products/ payments services

telecom providers network providers public transport non bank ATM’s acceptant payment service providers

28

Trends / developments (1)

Consequences

Standardisation increasingly important

Increasing (need for) co-operation between overseers

(criteria, standards, approach)

Legal and oversight frameworks need to be harmonised

(MoU’s)

29

Trends / developments (2)

Consequences

Increasing (need for) co-operation with other regulators

(e.g. supervisors, securities regulators, etc.)

Currently cooperative oversight on VISA and

MasterCard has started

30

Cooperation other authorities

System Lead overseer and/or regulator Other overseers and/or regulators Wholesale TARGET2.NL DNB TARGET2 ECB ESCB CLS Federal Reserve G10-central banks and other central banks of issue

with a currency in CLS SWIFT National Bank of Belgium G10-central banks Securities ECC BaFin Bundesbank, AFM, DNB EMCF AFM/DNB Euroclear Nederland AFM/DNB Euroclear SA National Bank of Belgium and

CBFA AFM, DNB and regulators from France and the United Kingdom

MTS Amsterdam AFM/DNB LCH.Clearnet Group Ltd

Commission Bancaire AFM, DNB and regulators from France, Portugal and the United Kingdom

LCH.Clearnet SA Rotating regulator chairmanship Euronext countries

Other regulators from Belgium, France, the Netherlands and Portugal

Retail Acceptgiro, Chipknip, iDEAL, Incasso, PIN

DNB

Equens DNB Telegiro Nieuwe Stijl DNB UPSS DNB

31

Trust in The Payment SystemWho’s Concern?

32

Poll/survey

POLL/SURVEY WITH

THE AUDIENCE

33

Poll/survey (1)

Who uses for mobile phoning a mobile phone service

provider?

Who expects /requires that mobile phoning also will be

available abroad (using networks from other providers)?

Who expects support of its provider for secure and

continue telephoning?

Who is of the opinion that you has user also have a role

in the security of this service?

34

Poll/survey (2)

Who expects continuity and security of the mobile

communication as part of the services offered?

Would you change from provider if this provider proves

not to have this operational?

Who has the opinion that the mobile telephone operator

has to monitor (closely) that the services he offers

meets the requirements of the clients?

35

Poll/survey (3)

In case of availability of standards. Who has the opinion

that this operator has to be compliant to available

standards?

Who has the opinion that clients of commercial banks

may require the same as you require from your mobile

telephone operator regarding the security and continuity

of the payment services offered?

36

Poll/survey (4)

Outcome poll/survey

37

Trust in The Payment SystemWho’s Concern?

EQUAL TO SAVE THE CLIMATE

38

What options are possible and fully or partly operational in the Netherlands

Founding of a central owner of interbank payment

products

Setting by the owner of standards/regulations/rules

Monitoring by the owner on compliancy to these rules

and regulations

Internal discussion and cooperation via a national

organised association

39

What options are possible and fully or partly operational in the Netherlands

Structured communication with DNB (Dutch NCB)

Close cooperation with DNB regarding the security and

continuity of the payment system (Payment Escalation

Committee)

Participation in sector wide testing

40

What improvements can still be made?

(Periodic and structured) monitoring compliance

to standards/rules set by supervising

authorities.

Showing more transparency to the public

41

Concluding remarks (1)

Payment and securities (settlement) systems are of critical importance to a country and a country’s economy, especially during times of crisis

Payment systems … … facilitate the exchange of goods and

services… are necessary to conduct monetary policy… can be transmission channels of

‘disturbances’ (financial crises)

42

Concluding remarks (2)

Both retail and wholesale payment systems are important but have different profiles and different risks

Roles central bank: operator, catalyst and overseer

Mission DNB: to promote the smooth operation of payment systems, i.e. safe, efficient and accessible

43

Concluding remarks (3)

Securities settlement systems Are essential for monetary policy operations Link securities settlement and payment systems (via

DVP) Are important for well-functioning financial markets

INFRASTRUCTURES, in general Essential for Financial Stability

44

Concluding remarks (4)

Central Banks Play Key Role But all participants have to cooperate to guarantee the

required trust In the Netherlands the financial sector already showed

its responsibility Further improvements are still possible/recommended Many developments going on European level

45

Questions…

46

Time’s up………

P.W. Osse RE RA CISANCB Consulting+31 06 25 06 27 [email protected]

THANK YOU FOR YOUR ATTENTION