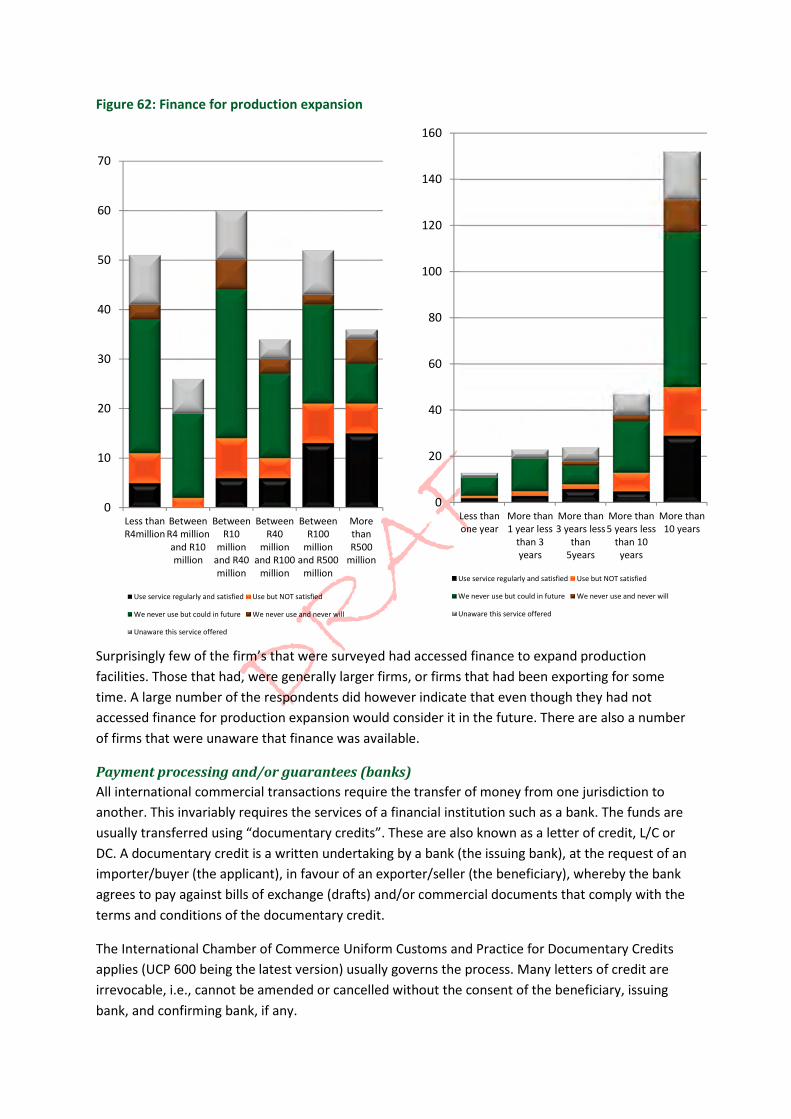

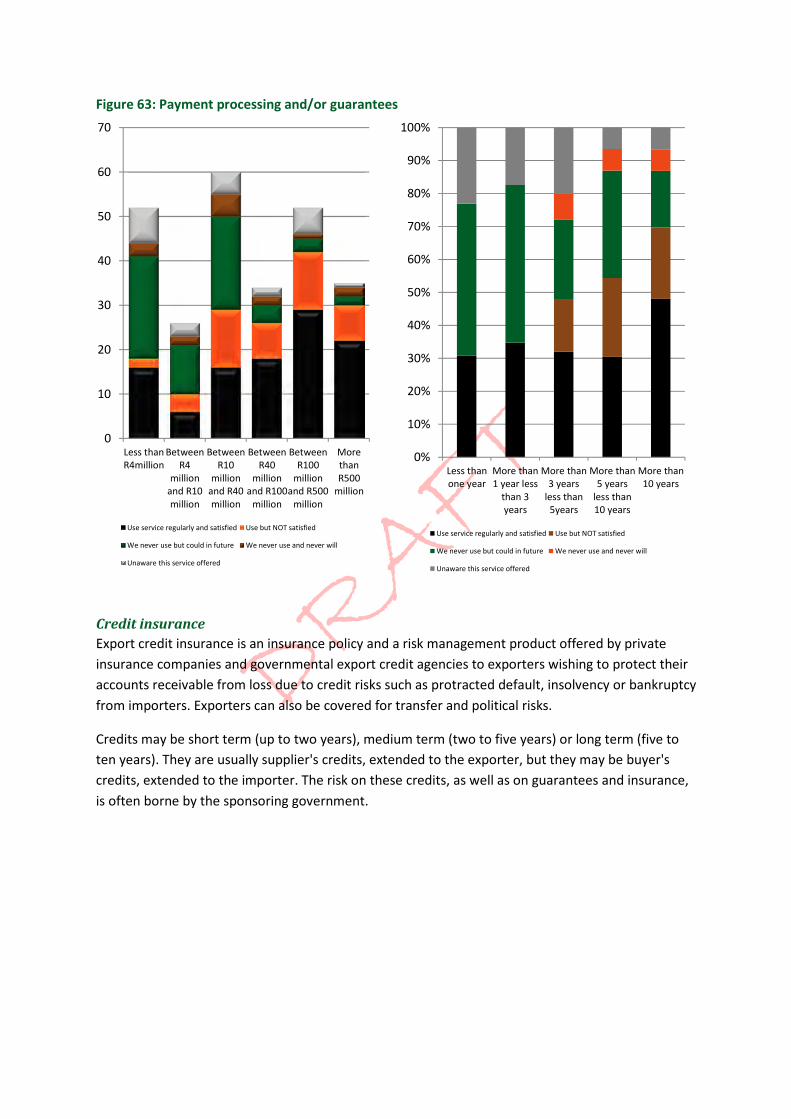

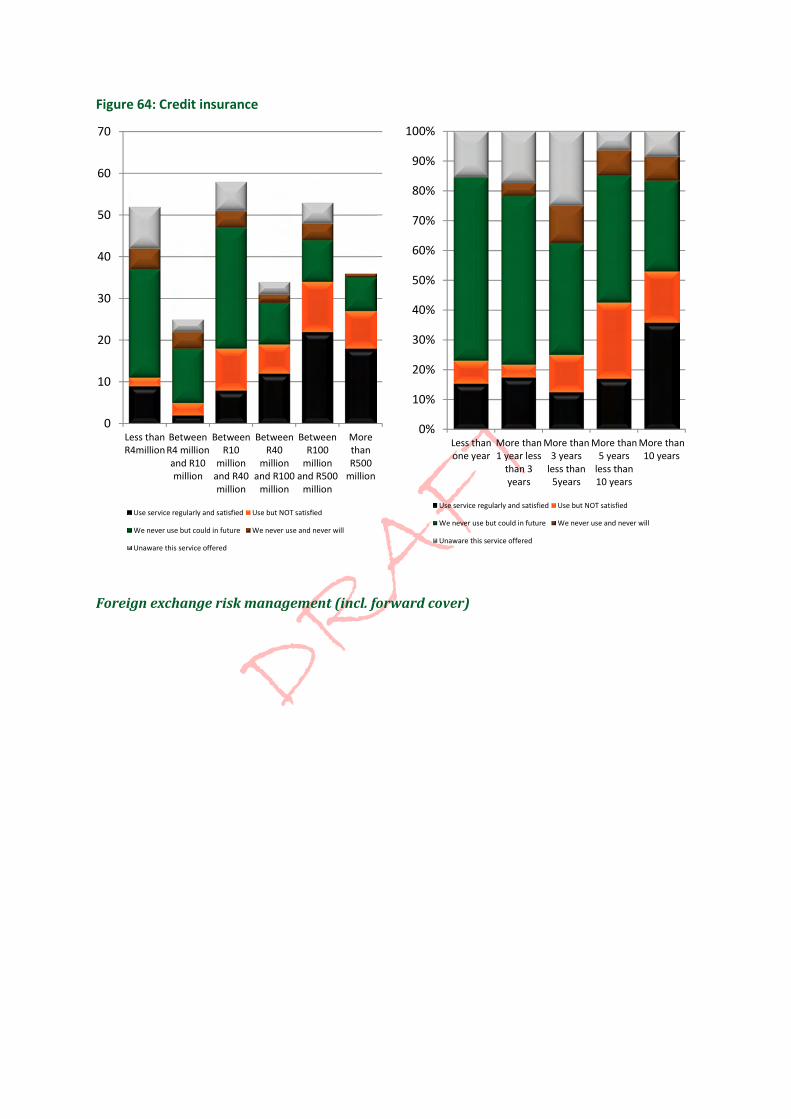

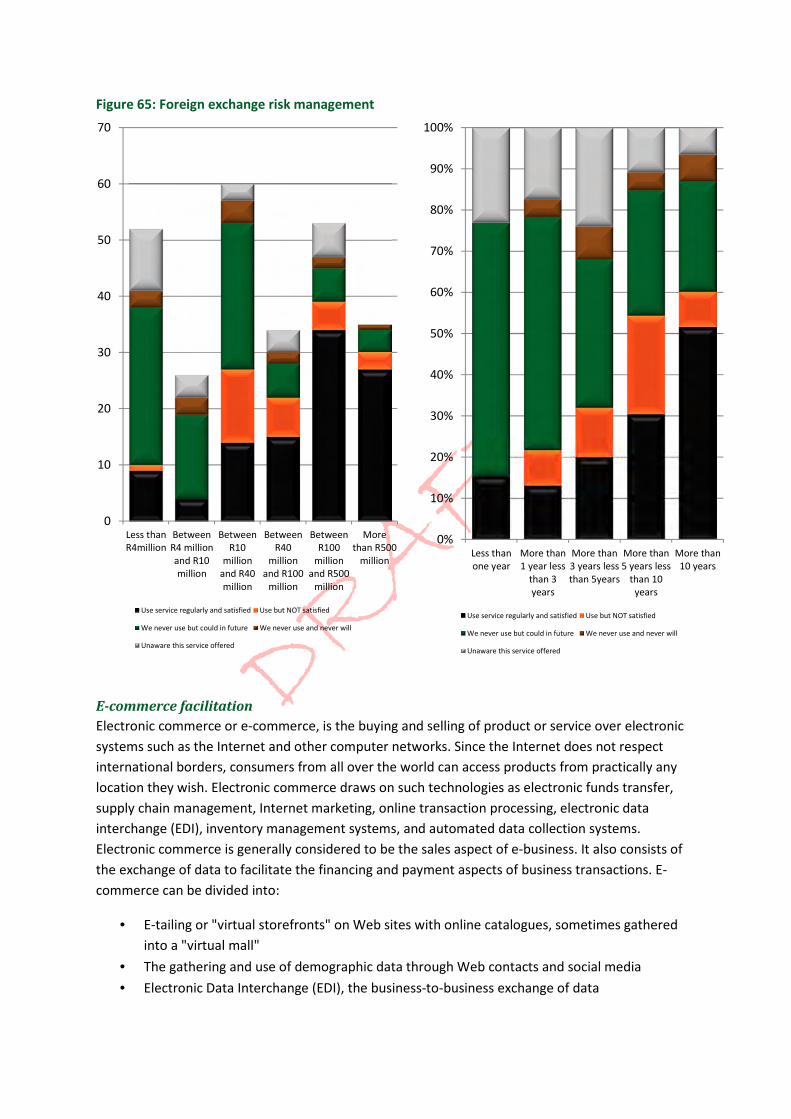

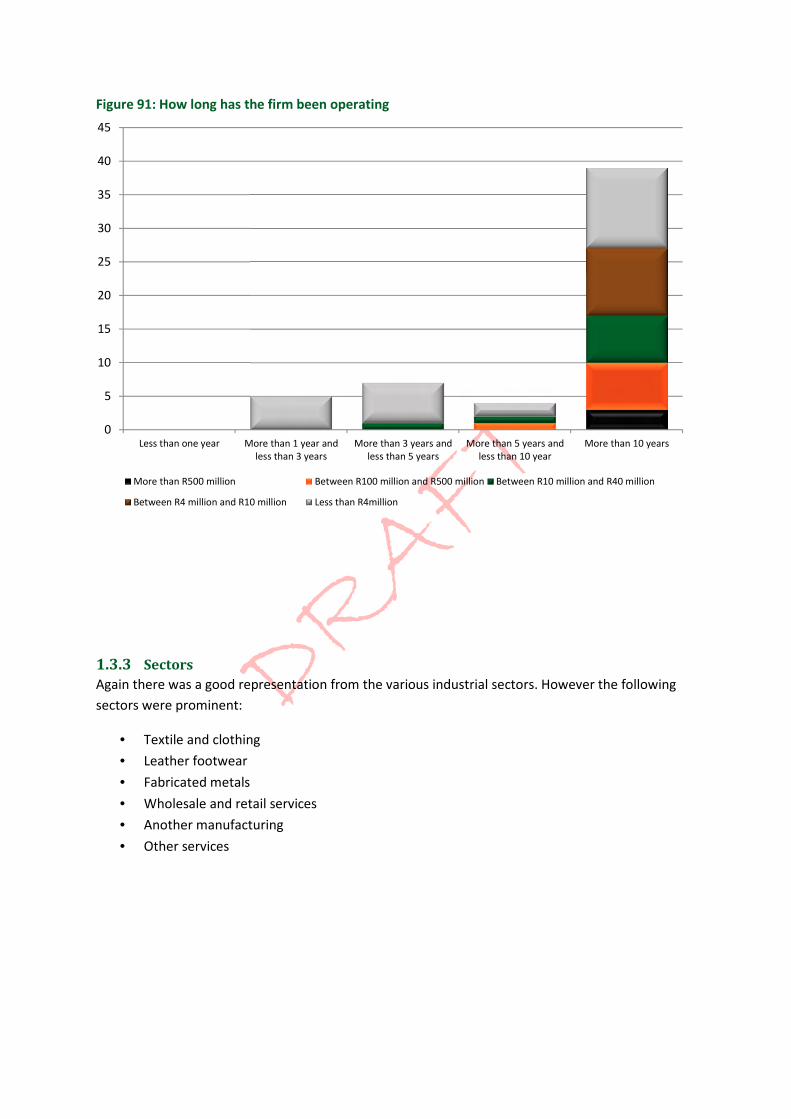

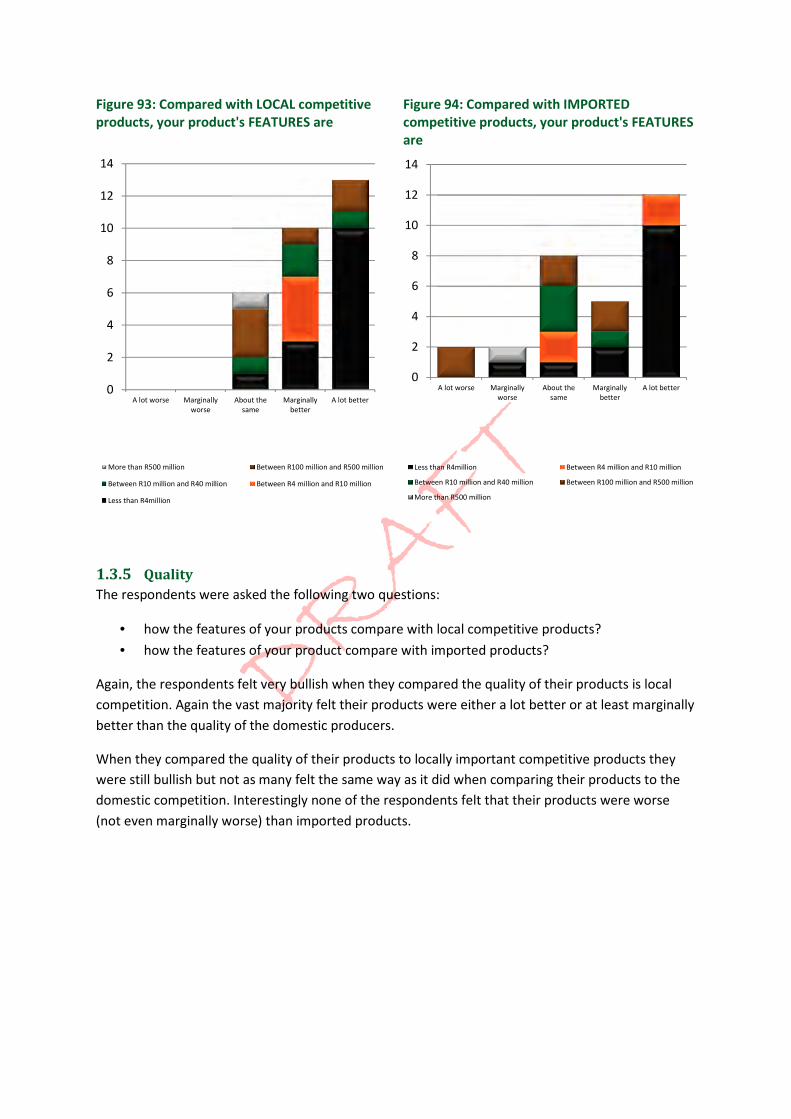

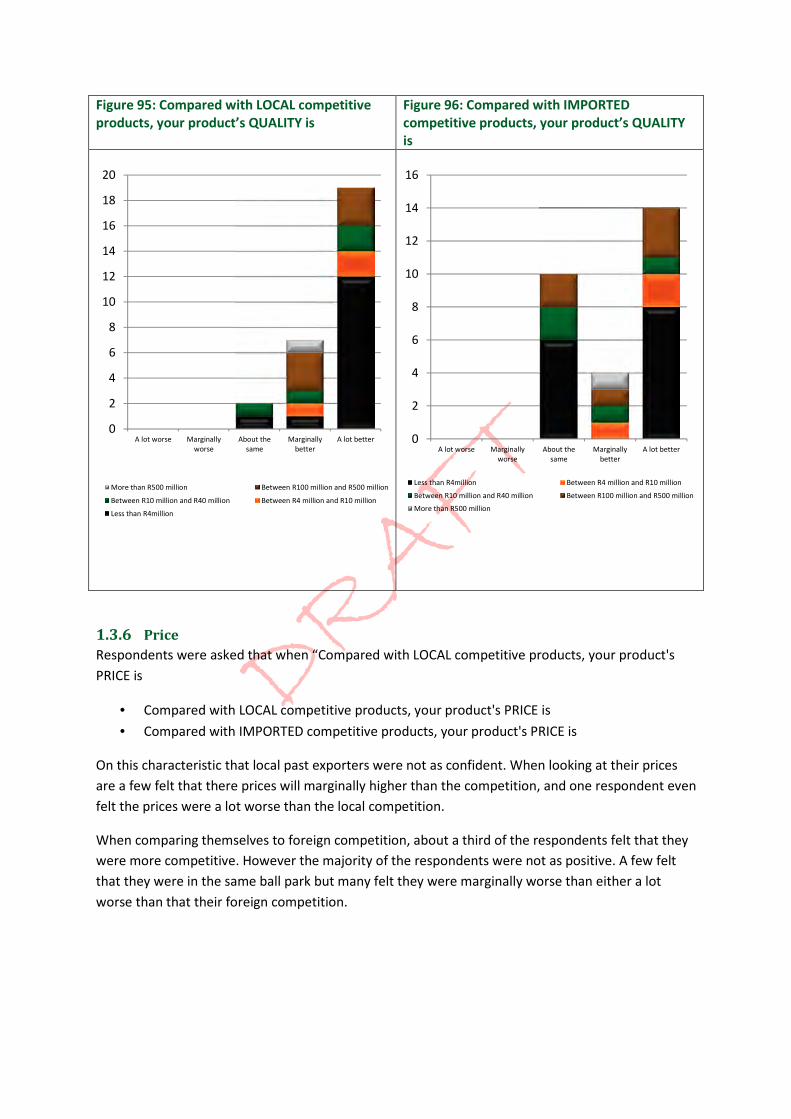

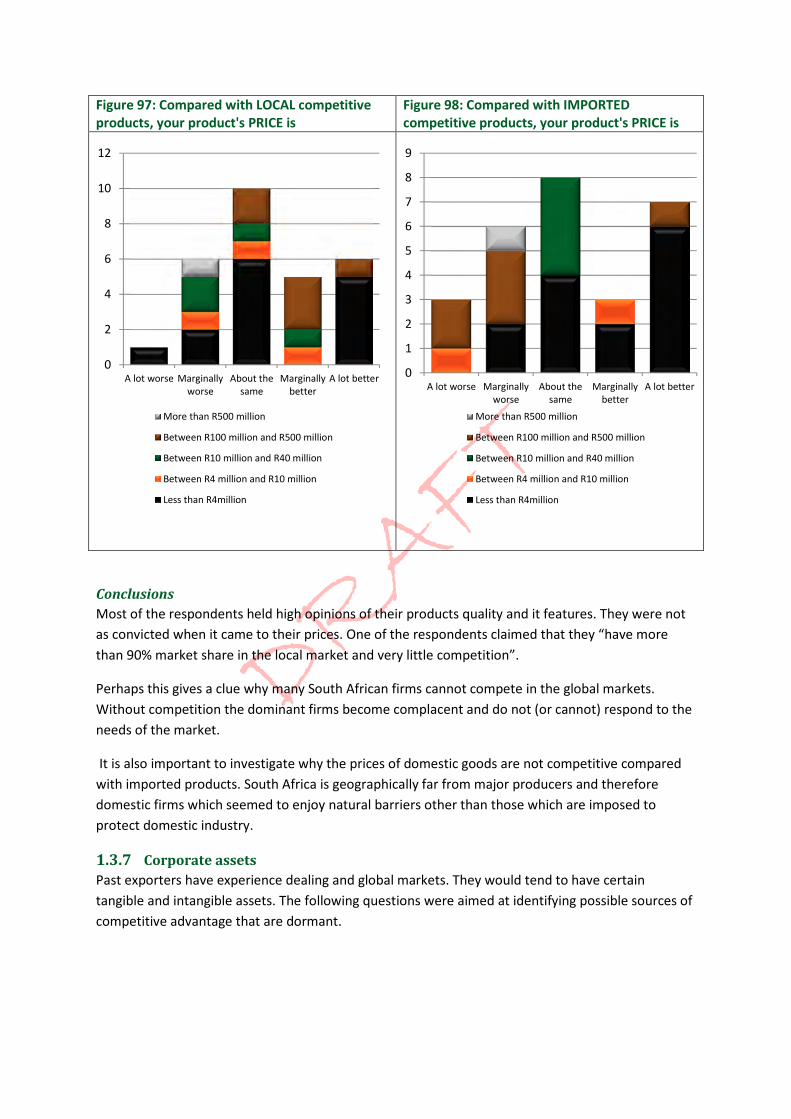

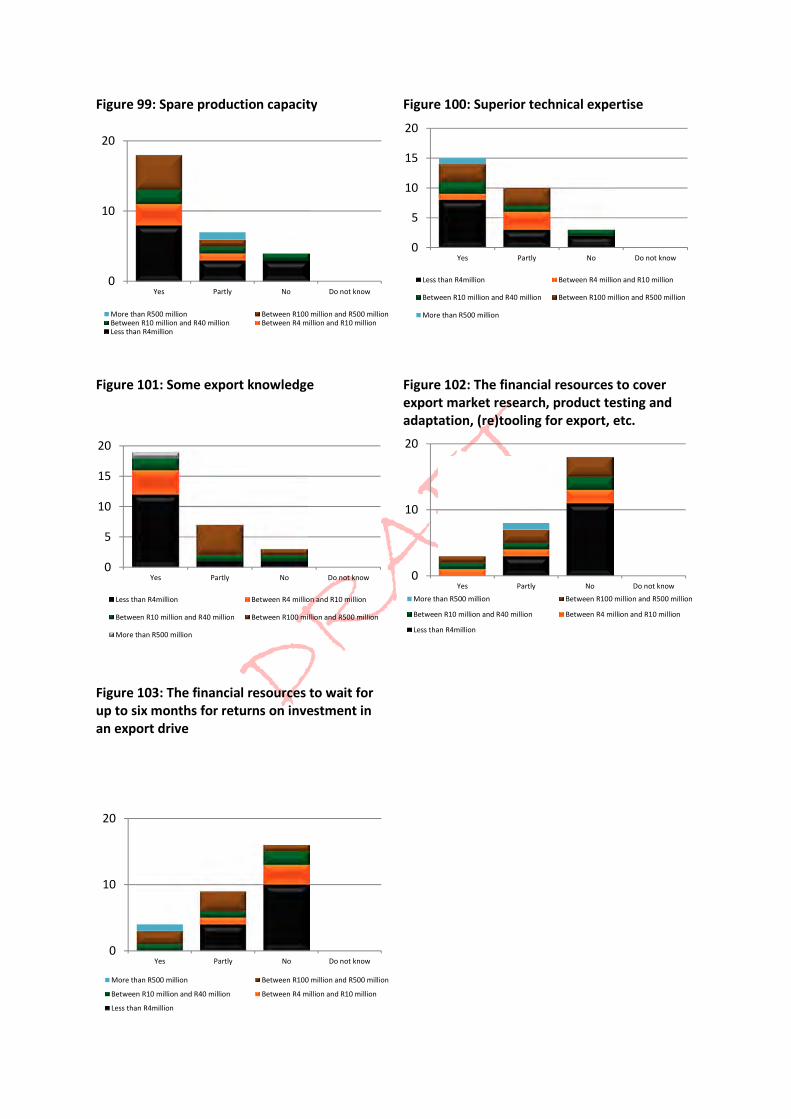

1 survey of exporters, past exporter and potential exporters · 1 survey of exporters, past...

TRANSCRIPT

DRAFT

1 Survey of exporters, past exporter and potential exporters

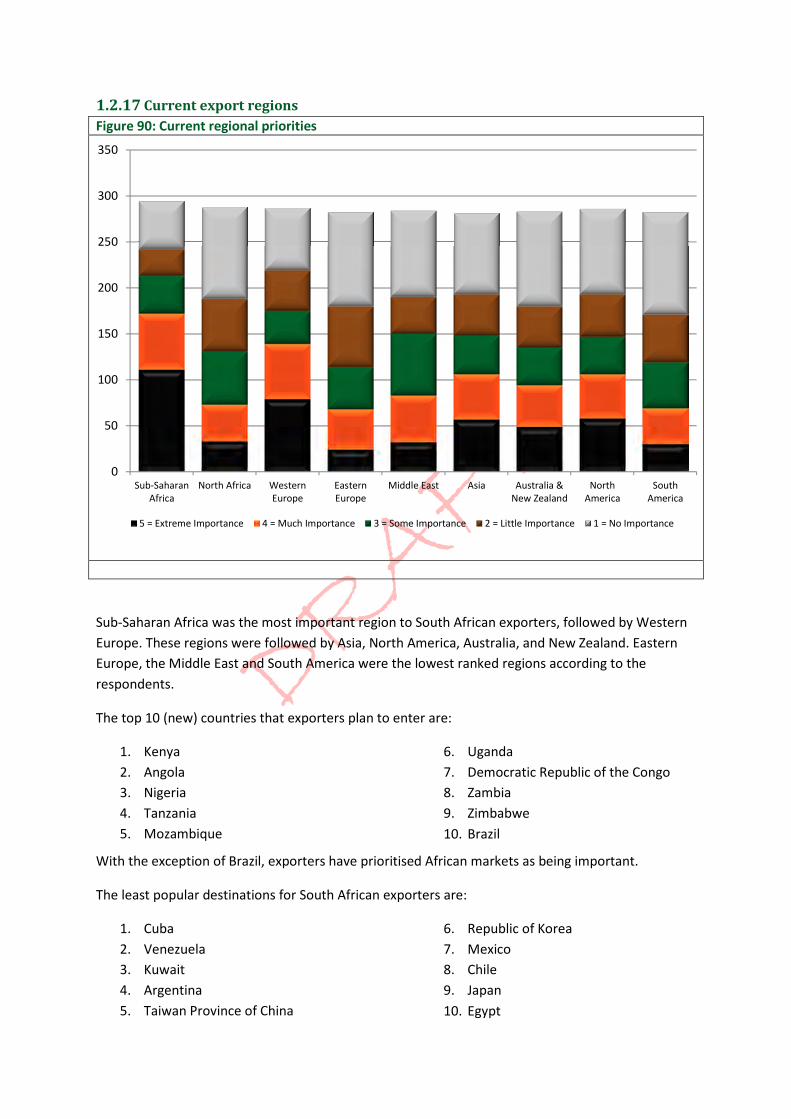

1.1 The purpose of the survey

The purpose of the survey was to solicit the opinions of exporters and to find out what products they

were exporting, where they were exporting to, what drivers and barriers they were experiencing,

etc.

Initially (in terms of the initial proposal) only existing exporters were to be surveyed. However, it was

felt that the opinions of non-exporters would be different to those of exporters. Non-exporters had

perceived problems and had not necessarily experienced the actual problems that current exporters

have. In terms of the “REN-approach”, it was also necessary to try and find out why exporters exited.

Therefore a separate survey was also prepared for past exporters.

There is no comprehensive exporter directory in South Africa. With the kind assistance of Neels

Bothma (of Exporthelp and UNISA) over 2000 exporters were identified. The following email was

sent to them:

Dear Exporter

One of the strategies that the South African government has adopted to reduce the very

high unemployment rate and to grow the economy is to increase exports. The Department

of Trade and Industry has appointed TIPS to review and revise the current National Export

Strategy. Part of this review includes getting the views of both current and past exporters as

well as potential exporters. It is important to understand both the drivers and the obstacles

that exporters face.

The National Export Strategy will cover the next 20 years (although only the next five years

will be spelt out in detail). The scope is national and therefore deals with all factors that will

have an impact on South Africa’s exports. It is not limited to the Department of Trade and

Industry’s functions but also includes, but not limited to, finance and logistics. The goal is to

advise government on ways to change policies that hinder private establishments like yours

and to develop new policies and programs that support productivity growth and

competitiveness. The results of the survey and other research could lead to substantial

changes that may affect your company and industry. Your opinion and participation in this

survey is vitally important.

It will be appreciated if you would complete one of the three surveys. Whether you are

currently exporting, have exported, or do not export, your opinions are important. Besides

the questions you will also have an opportunity to give your views on any aspects that you

feel are important to help grow South Africa’s exports. The questionnaires are online. Please

click on the appropriate questionnaire:

• Have never exporter (https://www.surveymonkey.com/s/nonexporter1 )

DRAFT

• Have exported but not on the past year

(https://www.surveymonkey.com/s/Pastexporter1 )

• Currently exporting (https://www.surveymonkey.com/s/NES_Current1 )

The completed questionnaires will be treated as confidential and only the TIPS researchers

will have access to your answers. Any comments that you do give will not be attributable to

you. You are therefore encouraged to be absolutely honest and highlight any aspects that

hamper your role in exporting.

In addition to this database, requests were also sent to organised business and to the Export

Councils, who in turn were requested to forward the email to the members. (It is possible that

opinions regarding the effectiveness Of Export Councils could be skewed.)

DTI (Department of Trade and Industry)’s own database was also used. This included exporters who

had used the export marketing assistance scheme or had been part of a capacity building

programme. (It is possible that the opinions of exporters that had benefited from various

government incentives would also skew the survey results.)

1.2 Responses to the survey of current exporters

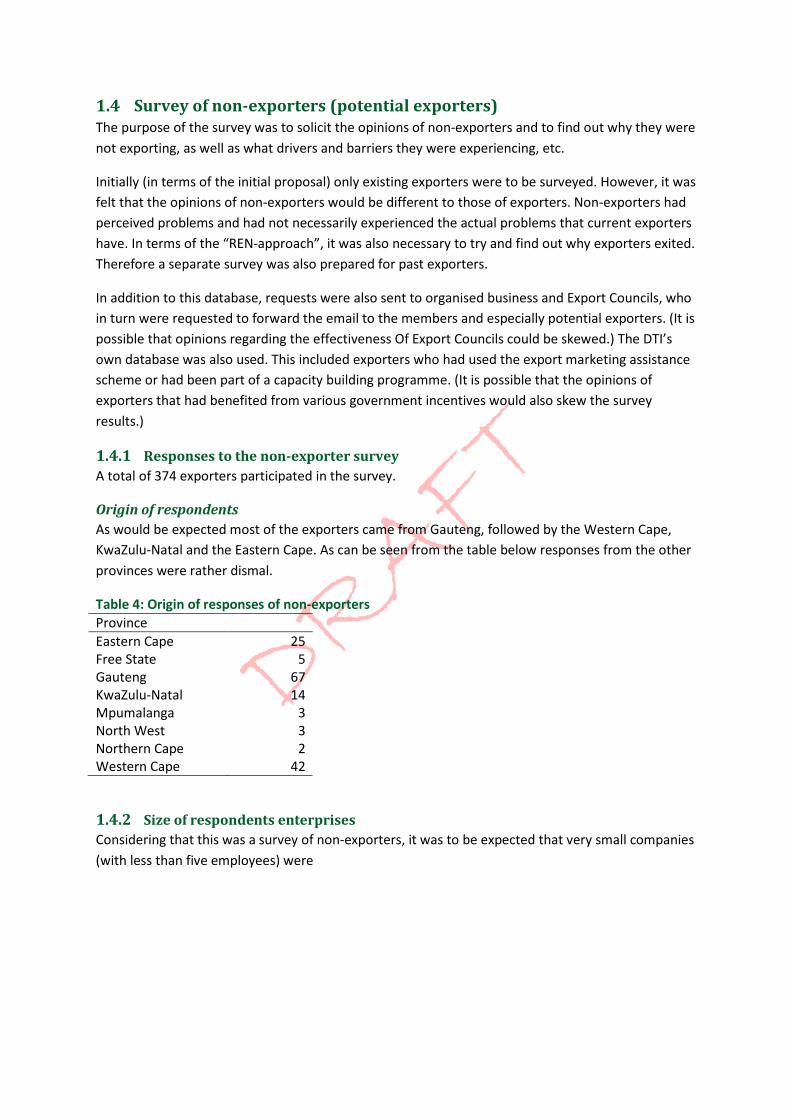

A total of 374 exporters participated in the survey.

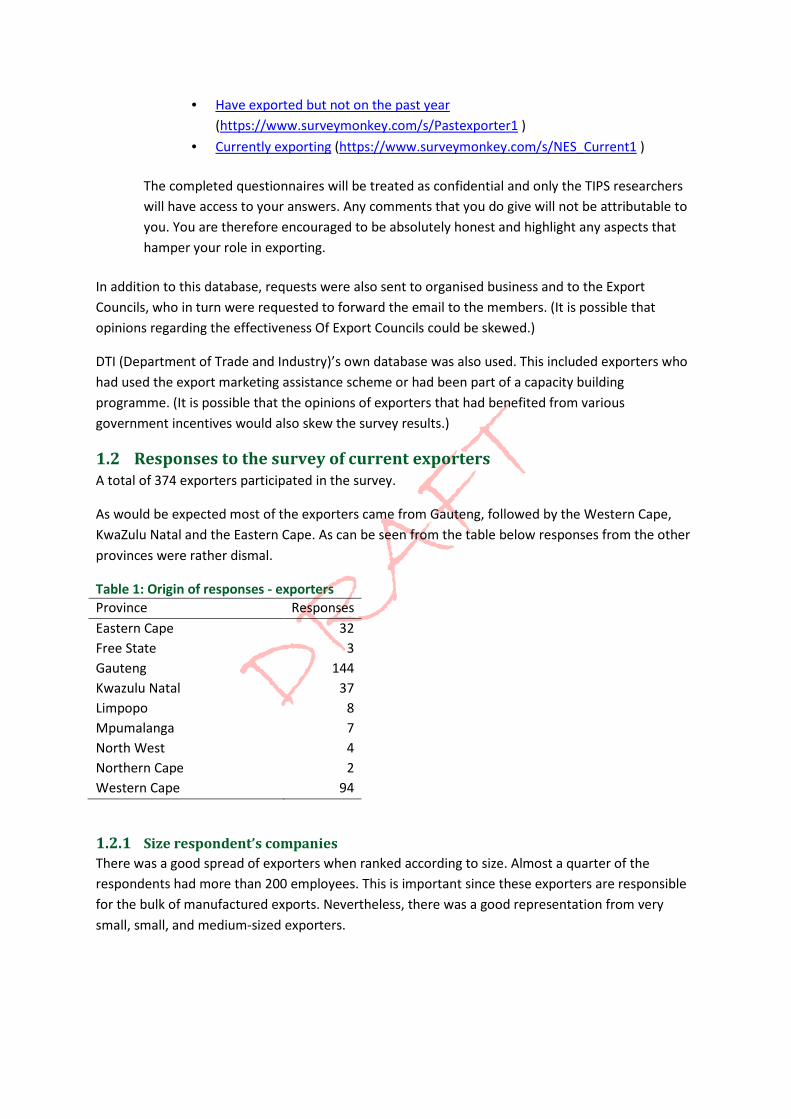

As would be expected most of the exporters came from Gauteng, followed by the Western Cape,

KwaZulu Natal and the Eastern Cape. As can be seen from the table below responses from the other

provinces were rather dismal.

Table 1: Origin of responses - exporters

Province Responses

Eastern Cape 32

Free State 3

Gauteng 144

Kwazulu Natal 37

Limpopo 8

Mpumalanga 7

North West 4

Northern Cape 2

Western Cape 94

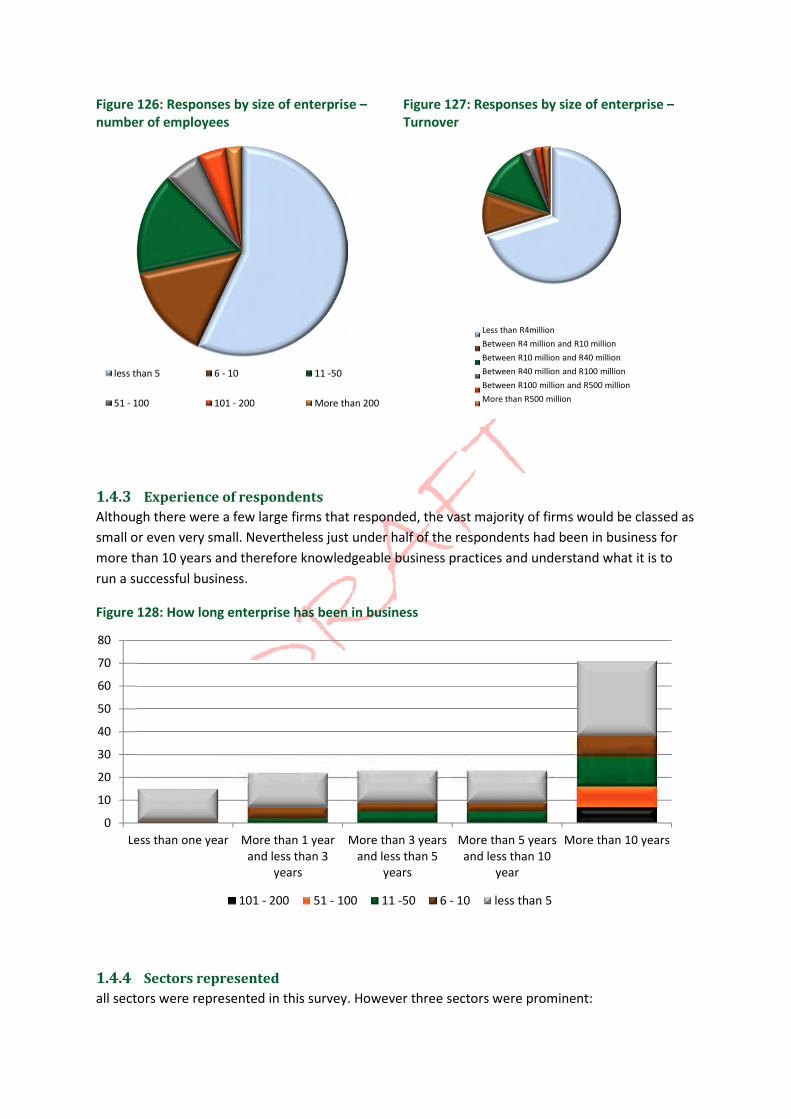

1.2.1 Size respondent’s companies

There was a good spread of exporters when ranked according to size. Almost a quarter of the

respondents had more than 200 employees. This is important since these exporters are responsible

for the bulk of manufactured exports. Nevertheless, there was a good representation from very

small, small, and medium-sized exporters.

DRAFT

Figure 1: Total number of full time paid

employees

Figure 2: Exporter size turnover

1.2.2 Sectors represented by respondent’s companies

less than

5

6 - 10

11 -50

51 - 100

101 - 200

More

than 200

Less than

R4million

Between

R4

million

and R10

million

Between

R10

million

and R40

million

Between

R40

million

and R100

million

Between

R100

million

and R500

million

More

than

R500

million

DRAFT

Figure 3: Classification of exporters

1.2.3 Exporter’s experience

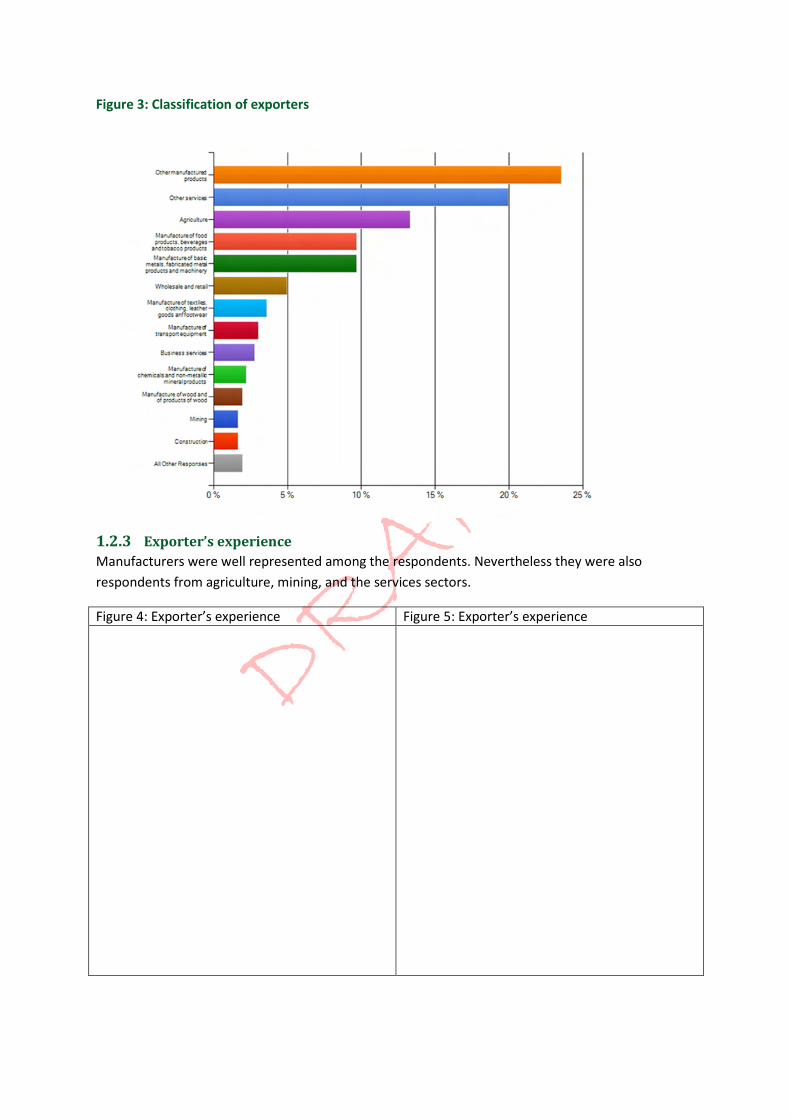

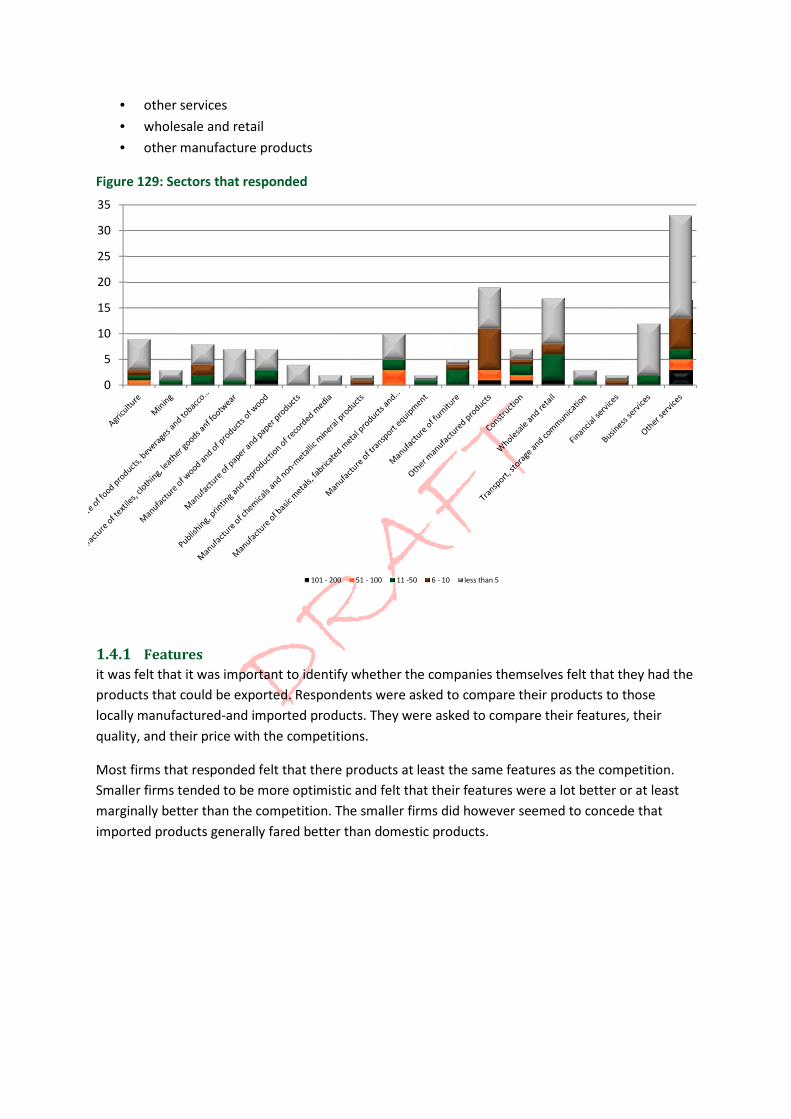

Manufacturers were well represented among the respondents. Nevertheless they were also

respondents from agriculture, mining, and the services sectors.

Figure 4: Exporter’s experience Figure 5: Exporter’s experience

DRAFT

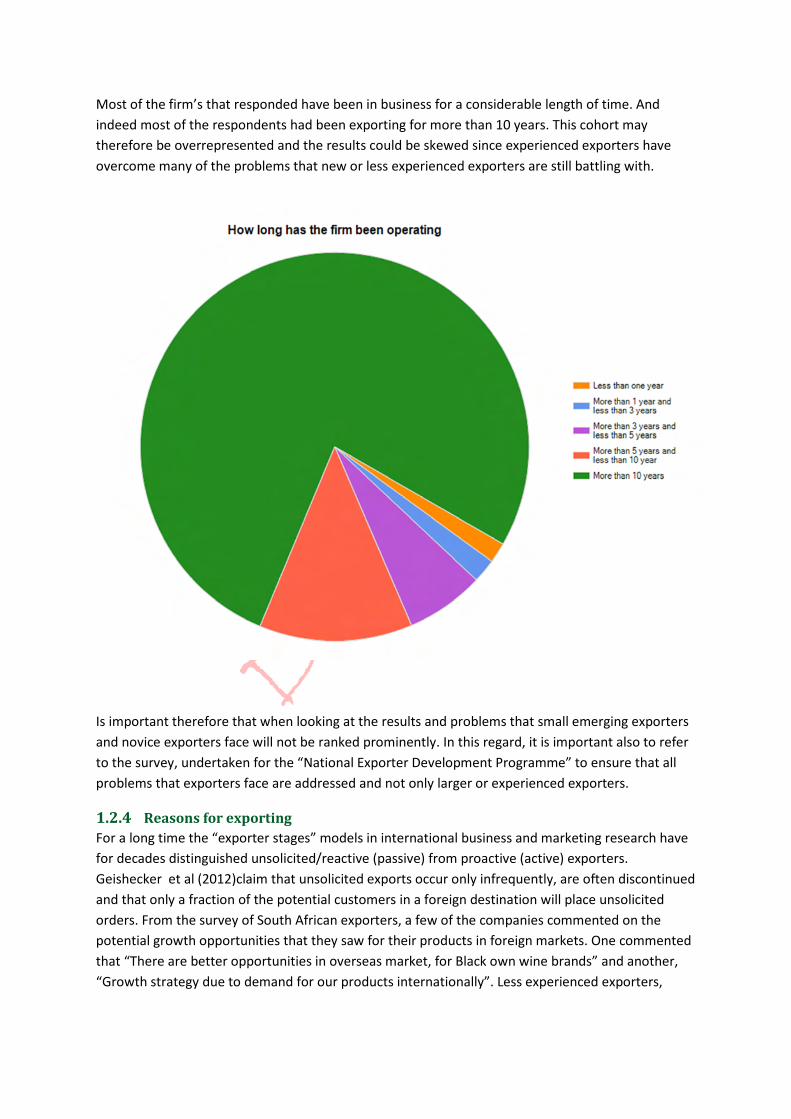

Most of the firm’s that responded have been in business for a considerable length of time. And

indeed most of the respondents had been exporting for more than 10 years. This cohort may

therefore be overrepresented and the results could be skewed since experienced exporters have

overcome many of the problems that new or less experienced exporters are still battling with.

Is important therefore that when looking at the results and problems that small emerging exporters

and novice exporters face will not be ranked prominently. In this regard, it is important also to refer

to the survey, undertaken for the “National Exporter Development Programme” to ensure that all

problems that exporters face are addressed and not only larger or experienced exporters.

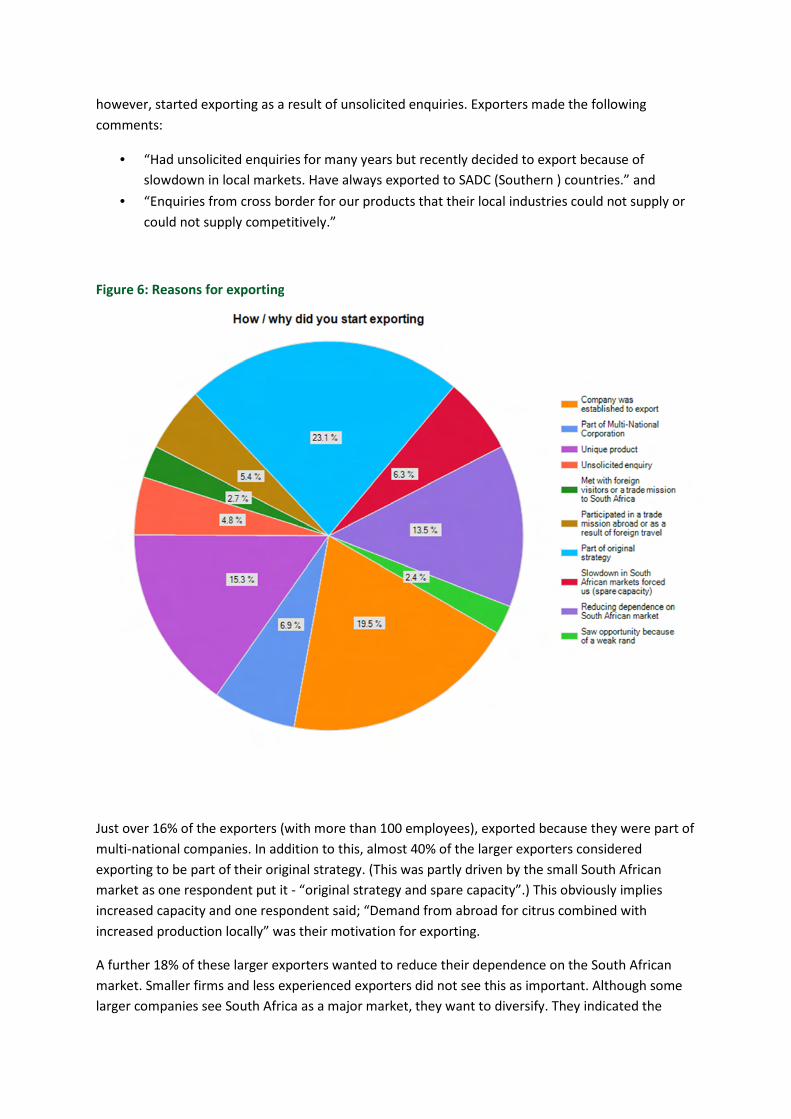

1.2.4 Reasons for exporting

For a long time the “exporter stages” models in international business and marketing research have

for decades distinguished unsolicited/reactive (passive) from proactive (active) exporters.

Geishecker et al (2012)claim that unsolicited exports occur only infrequently, are often discontinued

and that only a fraction of the potential customers in a foreign destination will place unsolicited

orders. From the survey of South African exporters, a few of the companies commented on the

potential growth opportunities that they saw for their products in foreign markets. One commented

that “There are better opportunities in overseas market, for Black own wine brands” and another,

“Growth strategy due to demand for our products internationally”. Less experienced exporters,

DRAFT

however, started exporting as a result of unsolicited enquiries. Exporters made the following

comments:

• “Had unsolicited enquiries for many years but recently decided to export because of

slowdown in local markets. Have always exported to SADC (Southern ) countries.” and

• “Enquiries from cross border for our products that their local industries could not supply or

could not supply competitively.”

Figure 6: Reasons for exporting

Just over 16% of the exporters (with more than 100 employees), exported because they were part of

multi-national companies. In addition to this, almost 40% of the larger exporters considered

exporting to be part of their original strategy. (This was partly driven by the small South African

market as one respondent put it - “original strategy and spare capacity”.) This obviously implies

increased capacity and one respondent said; “Demand from abroad for citrus combined with

increased production locally” was their motivation for exporting.

A further 18% of these larger exporters wanted to reduce their dependence on the South African

market. Smaller firms and less experienced exporters did not see this as important. Although some

larger companies see South Africa as a major market, they want to diversify. They indicated the

DRAFT

traditional stages of internationalisation, starting with exports and eventually establishing foreign

manufacturing facilities. Africa seems to be the logical destination but others include Australia.

Twenty six per cent of smaller exporters (with less than 100 employees) established their companies

to export, with an additional 16% including exports as part of their original strategy. Twenty per cent

had unique products that they felt would have global appeal. Smaller companies did not see

reducing their dependence on the South African market as being as important to larger companies.

Companies with between 11 and 50 employees started exporting as a result of unsolicited orders.

Hardly any of the exporters saw the value of the South African Rand as a potential driver. A few

companies (3%) with more than 200 employees however did see an undervalued currency as an

advantage. Incentives were important to one exporter of automotive equipment and they stated

that “MIDP (Motor Industry Development Programme) duty relief incentive scheme” was a

contributory factor in their decision to start exporting.

Although AGOA (African Growth Opportunities Act) was given as a driver to start exporting, it was

seen as a benefit.

Innovation was an important consideration in many companies starting to export. More than 15% of

exporters indicated that this was their prime motivation. It was a very important consideration for

firms that had been exporting for less than a year and accounted for more than 30% of those

exporters.

Being a Unique South African made product

More experienced companies indicated that inward-buying missions were a contributory factor to

the export efforts. One exporter indicated they started exporting as a result of the their participation

in the Design Indaba, Cape Town 2009 and 2012, where they made contact with EU importers. Less

experienced exporters on the other hand relied more in participation in foreign trade missions and

foreign travel. This indicates that:

• More resources should be given to inward-buying missions as the investment is more

sustainable; and

• More efforts should be put into developing local networks where foreign buyers can meet

with South African suppliers.

DRAFT

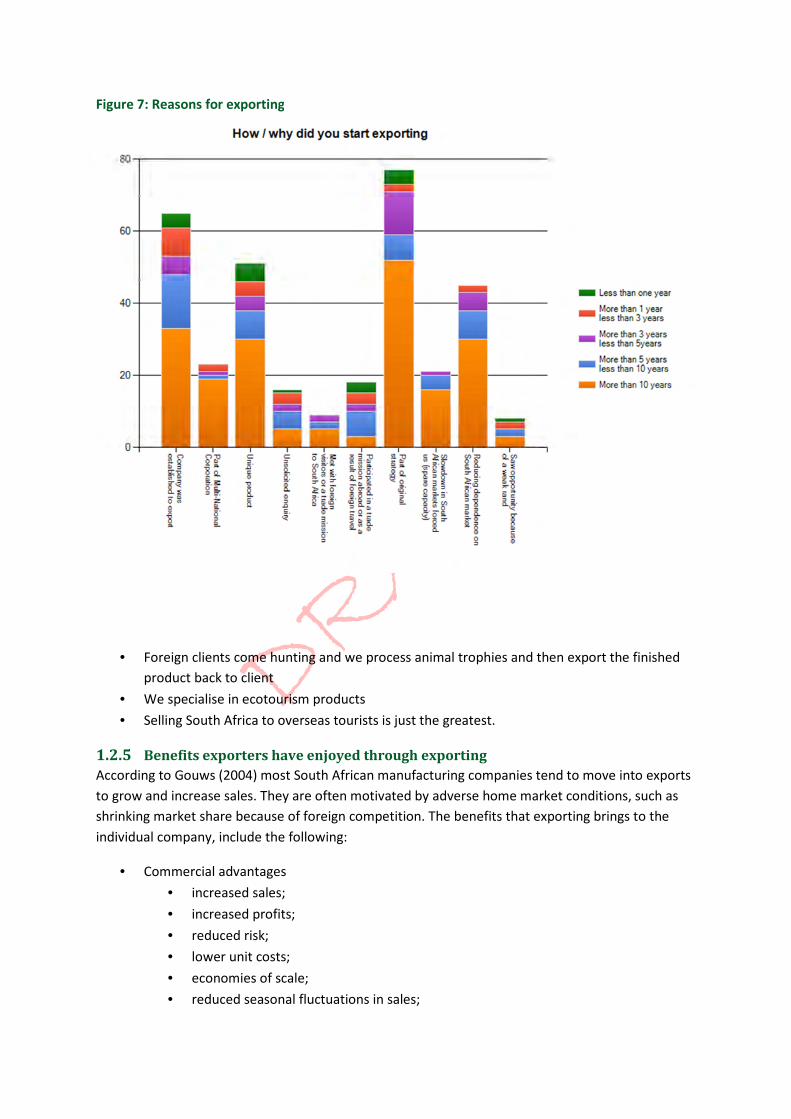

Figure 7: Reasons for exporting

• Foreign clients come hunting and we process animal trophies and then export the finished

product back to client

• We specialise in ecotourism products

• Selling South Africa to overseas tourists is just the greatest.

1.2.5 Benefits exporters have enjoyed through exporting

According to Gouws (2004) most South African manufacturing companies tend to move into exports

to grow and increase sales. They are often motivated by adverse home market conditions, such as

shrinking market share because of foreign competition. The benefits that exporting brings to the

individual company, include the following:

• Commercial advantages

• increased sales;

• increased profits;

• reduced risk;

• lower unit costs;

• economies of scale;

• reduced seasonal fluctuations in sales;

DRAFT

• extended product life cycle.

• Financial

• Organisational

The survey of exporters confirmed many of these reasons. Many exporters cited numerous

advantages that they have enjoyed because of their export efforts. One established exporter stated

that exports:

• Created a sustainable platform for local industry;

• Maintained our market position in established markets;

• Continued growth in emerging/new markets;

• Exports have assisted manufacturers to maintain/grow production levels, preserve jobs and

create employment opportunities.

The other exporter’s comments are discussed under the headings listed below.

Increased production and turnover

Most of the established exporters cited the increased turnover as a major advantage. This obviously

let to increased profits. In other cases it gave exporters the “ability to turn excess capacity to exports

when domestic demand is down and hence not putting workers on short time and or having to

retrench any staff.”

Increased exports also led to a “reduction of overall unit costs” which in turn contributed to

“increased margins.” Again this improved exporters’ profitability.

The “increased sales and better volumes” also “improved cash flow.” New exporters and exporters

with less know-how have had contradictory experiences.

Bigger profits

As has been pointed out in the section on increased production and turnover, exporting has

contributed to increased profitability of South African firms as well as their employees. One of the

respondents pointed to the higher his earning were largely because of .commissions

Incentives

The South African government’s incentives also contributed to firms profitability and thus their

benefits from exporting (DTI Government Incentives and TO BENEFIT FROM MIDP INCENTIVE)

Diversification of markets and risks

Exporters either have a defensive or offensive diversification strategy. Most South African exporters

had defensive reasons for diversification and spread the risk of market contraction. A few were

forced to diversify when the South African market conditions no longer offered opportunities for

growth. A few South African exporters took offensive positions and tried to conquer new markets

and to take opportunities that offered greater profitability than expansion opportunities.

A few exporters indicated that the slowdown in the global market has affected them and that more

effort was required in exporting in this environment. The 2008/09 however was a global recession

and practically all global markets were affected. Therefore the slowdown experienced in South

Africa was similar to those felt in other trading countries. Nevertheless for a few South African

DRAFT

companies exporting “has enabled us to survive, because South African manufacturing seems to be

shrinking. Keeping our volume high and therefore being competitive in local market.”

Exporters highlighted the positive “exposure to global markets” gave them and their companies.

They were exposed to global trends that had positive consequences for their South African

operations. .

Many of the exporters pointed to the reduced risk that the “diversification of customer base’

brought. “Additional customers and purchase orders” spread the risks. Domestic risks, such as

labour disputes that resulted in undesirable market condition, were offset through “more export

sales, and being able to have sales while the mining industry in SA is on strike.” Another commented

that “We stayed a viable concern that employs 85 people full time and between 100 and 600

contract labours depending on the export successes.”

Enterprise development

Enterprise development is critical to South Africa’s growth and development and is even included as

a component in the BBEEE (Broad-based Black Economic Empowerment) score cards. Because of

exporting a firm “assisted others to export.”

Economies of scale

Economies of scale are the cost advantages that enterprises obtains due to expansion – the

producer’s average cost per unit falls as the scale of output is increased. Economies of scale gave

South African exporter’s the ability “to secure business locally and internationally.” One exporter

said that the “additional revenue stream to support local overhead structure” and contributed to

“better utilisation of capacity” allowed them to “increased turnover and profit.” The economies of

scale global markets gave one exporter the “ability to invest in CAPEX.” Their “expansion allowed

them to create employment opportunities for South Africans”

Seasonality

A few exporters that produced or sold seasonable products found that they could balance the

seasons by selling to the northern hemisphere when appropriate. Their “turnover during South

Africa’s winter months dwindled and increased for northern hemisphere's summer.” “Umtha's

export sales to northern hemisphere during South Africa's winter boost sales in these quiet months.”

Technology and innovation

Exposure to foreign markets exposes manufacturers to new technologies, innovation and other

useful information that they may not have acquired without this exposure. Although innovation may

play a more important role in the firm’s decision to start exporting, successful exporting drives

process of innovation and technology acquisition.

One exporter highlighted the importance of “networking with other exporters and importers. Our

export customers have given as excellent input with range planners and these are invaluable in

understanding individual countries & their customer trends.” Another saw their “income in strong

currency” as important but their “exposure to technology” was equally so.

Another exporter pointed to the role exporting had in “developing and growing engineering

expertise in South Africa” this was augmented by “learning about and understanding the

DRAFT

requirements for the international market.” They also “enjoyed being part of the "international"

team.”

Export spillover, broadly defined as the positive externalities arising from a firms interaction with

firms of other nations, that links productivity. According to this theory, the improvement in domestic

firms‟ export performance is the consequence or result of export spillovers from other exporters or

multi-national corporations. hosha (specializing

Learning-by-doing is a concept within economic theory. It refers to the capability of workers to

improve their productivity by regularly repeating the same type of action. The increased productivity

is achieved through practice, self-perfection and minor innovations.

Foreign exchange

Even though the exchange rate in the past couple of years has not been favourable to South African

exporters, about a dozen experienced exporters (with more than 10 years) cited this as an

advantage they have derived from exporting. Although a few did indicate the negative influences,

most claimed it was positive. One exporter put it: “At times when the Rand/Dollar exchange rate

was very high, we were able to survive in difficult economic times. We have a world-wide customer

base.” Many were able to buy machinery and other inputs such as raw materials when the South

African Rand was strong which made them more competitive when the currency weakened.

They did however indicate that the risks associated with currency fluctuation had to be managed.

International and domestic recognition

“Export quality” has a ring of endorsement. Domestic consumers feel that if it is good enough for

foreign markets, it should be superior to goods that are only sold in the South African market. One

exporter cited ”Proof that our products are "world-class".”

Selling to international markets enhanced the brand “especially by becoming an international brand”

and winning the “loyalty from export customers.”

Exporters felt that they “become a better business by understanding the level of product quality and

service required to be a business of international standing.”

A few South African provinces award “an exporter of the year” to recognise the achievements of

their local businesses. These awards are well publicised and winners get suitable recognition.

Social benefits

People are social creatures and like to meet new friends. Exporting allows the to do this and as one

exporter put it “we have met numerous interesting people and have become good friends with

some of them. We have experienced many different cultures. I feel that it has benefited the country

too, to have the foreign currency coming in.” Another developed “valuable partnerships with

different companies in different countries.”

Social responsibility

Although mast of the exporters focused on economic and other commercial reasons for exporting,

social responsibility was also considered. One of the companies with less than five years exporting

experience said : “We have managed to uplift our community by employing more people, supplying

skills development and training, Keeping abreast with world-wide food trends. Meeting exporters,

DRAFT

importers, distributors and Supermarket chains. Foreign investment for South Africa. Sharing our

uniquely South African Products. Becoming a Fair Trade partner!” Another exporter, focusing on

green issues stated that they had “opened new materials for recycling Improved cash flow increased

sales”

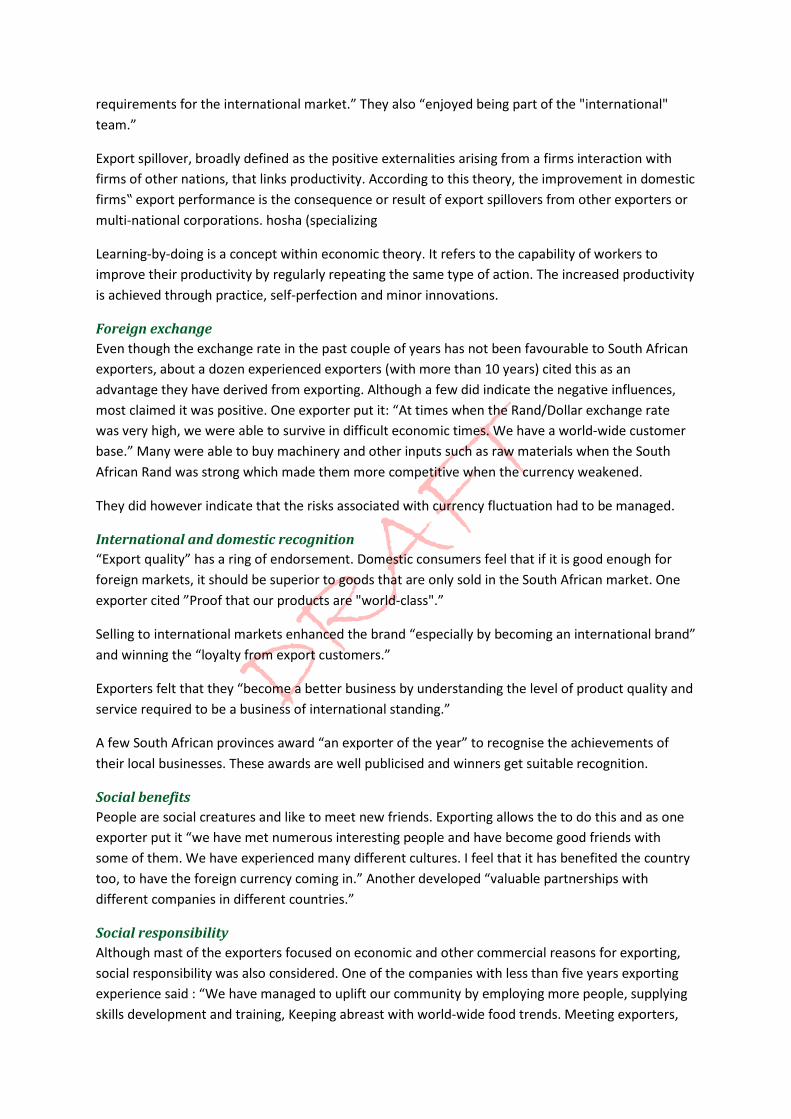

1.2.6 How exporters are currently exporting

Most exporters sold directly to the end user (either B2C1 or B2B

2). Most larger exporters (that

employed more than 200 people) sold directly to businesses. Smaller exporters (employing less than

100 people) sold marginally more to consumers. In addition to this a few of the respondents sold

directly to the foreign parent company or to the branch a subsidiary.

Foreign import agents or distributors were the second most preferred channel to use. This channel

was marginally preferred by smaller exporters (with less than 50 employees).

A few exporters used South African export agents. Although both large and small exporters used

South African agents, smaller exporters proportionately preferred this channel.

International trading houses are of various types and forms. They exist in a number of countries and

their activities and organisation vary according to the historical background and the scenario in

which they operate as well as national priorities and government policies. They are known by

different names in different countries:

• Trading Houses in Canada and Hong Kong,

• Sogo Shosha (general Trading House),

• Semen S by product) in Japan,

• Comercializadoras in Latin America,

• OSCI (Opérateur Spécialisé en Commerce Extérieur) in France,

• EMC (Export Management Company) and ETC (Export Trading Company) in the USA,

• Export House in India.

They procure locally and sell internationally, they procure internationally and sell locally and they

also procure internationally and sell internationally. They have the flexibility and the agility to work

in many markets with many products simultaneously as international marketing is their core

business. They serve as commercial intermediaries between suppliers and buyers located in different

countries. To this end they adopt the role of merchants, consortia managers and trade facilitators of

various sorts. As merchants they buy and sell on their own account and earn a margin.

Given the history of South Africa as a trading nation, and the importance of trading houses generally

across the world. It is rather surprising that so few established exporters are using this channel to

sell products internationally.

1 Business to Consumer

2 Business to Business

DRAFT

Figure 8: Current export channels

1.2.7 Use of the Internet in exporting

Very few exporters actually used the Internet to sell their products or services using e-commerce.

Smaller companies (with less than 50 employees) will most likely to use e-commerce as a tool to sell

globally. Only 25% of these companies used e-commerce, compared to only 3% of the large

companies that used extensively. Almost 50% of the companies (small, medium and large) surveyed

did not use e-commerce at all.

The majority of firms that are use online sources for export market research, and to acquire

intelligence. Smaller companies tended to make use of the Internet extensively while large

companies used it somewhat. Of concern is that just over 30% of all respondents across all sizes of

companies only used the web on a limited basis, if at all. Nearly 10% of large companies did not use

the Internet for export research and intelligence if at all.

A similar picture emerges for the use of the Internet to promote a company’s, products and services

globally. Almost 40% of all the respondents did use this tool extensively while 30% used it on a

limited basis, if at all.

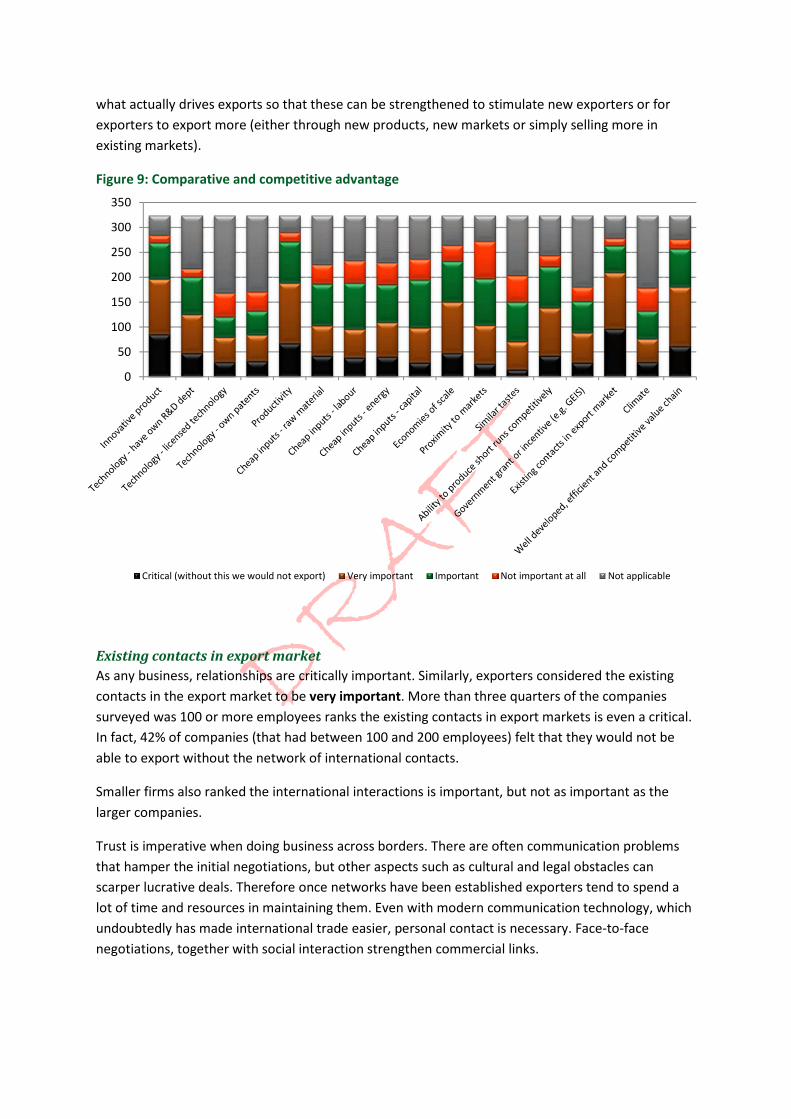

1.2.8 Comparative and competitive advantage

Firms export because they have some attribute that gives them some form of advantage in foreign

markets. These attributes have been debated and research extensively. It is important to understand

DRAFT

what actually drives exports so that these can be strengthened to stimulate new exporters or for

exporters to export more (either through new products, new markets or simply selling more in

existing markets).

Figure 9: Comparative and competitive advantage

Existing contacts in export market

As any business, relationships are critically important. Similarly, exporters considered the existing

contacts in the export market to be very important. More than three quarters of the companies

surveyed was 100 or more employees ranks the existing contacts in export markets is even a critical.

In fact, 42% of companies (that had between 100 and 200 employees) felt that they would not be

able to export without the network of international contacts.

Smaller firms also ranked the international interactions is important, but not as important as the

larger companies.

Trust is imperative when doing business across borders. There are often communication problems

that hamper the initial negotiations, but other aspects such as cultural and legal obstacles can

scarper lucrative deals. Therefore once networks have been established exporters tend to spend a

lot of time and resources in maintaining them. Even with modern communication technology, which

undoubtedly has made international trade easier, personal contact is necessary. Face-to-face

negotiations, together with social interaction strengthen commercial links.

0

50

100

150

200

250

300

350

Critical (without this we would not export) Very important Important Not important at all Not applicable

DRAFT

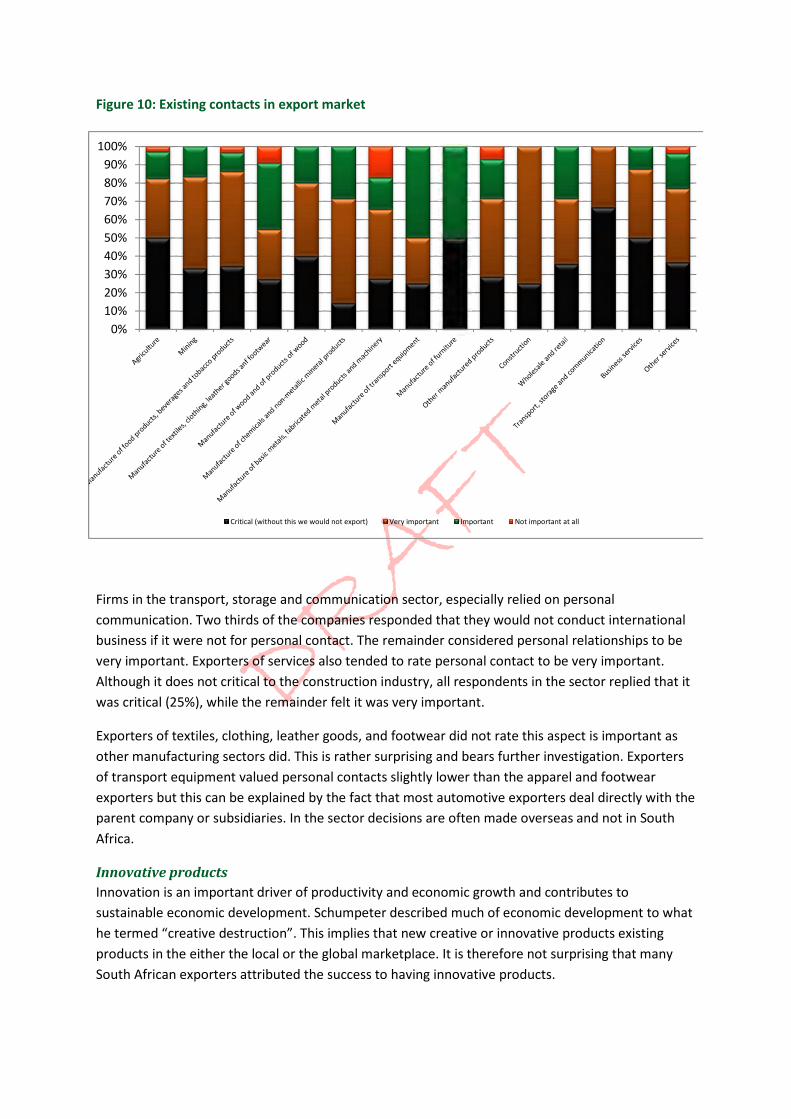

Figure 10: Existing contacts in export market

Firms in the transport, storage and communication sector, especially relied on personal

communication. Two thirds of the companies responded that they would not conduct international

business if it were not for personal contact. The remainder considered personal relationships to be

very important. Exporters of services also tended to rate personal contact to be very important.

Although it does not critical to the construction industry, all respondents in the sector replied that it

was critical (25%), while the remainder felt it was very important.

Exporters of textiles, clothing, leather goods, and footwear did not rate this aspect is important as

other manufacturing sectors did. This is rather surprising and bears further investigation. Exporters

of transport equipment valued personal contacts slightly lower than the apparel and footwear

exporters but this can be explained by the fact that most automotive exporters deal directly with the

parent company or subsidiaries. In the sector decisions are often made overseas and not in South

Africa.

Innovative products

Innovation is an important driver of productivity and economic growth and contributes to

sustainable economic development. Schumpeter described much of economic development to what

he termed “creative destruction”. This implies that new creative or innovative products existing

products in the either the local or the global marketplace. It is therefore not surprising that many

South African exporters attributed the success to having innovative products.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Critical (without this we would not export) Very important Important Not important at all

DRAFT

Figure 11: Innovative products

Manufacturers in particular, the food and fabricated metals sectors, relied on having innovative

products. However, exporters of services also relied on the innovative abilities to export. Established

sectors such as construction and mining did not rely on innovation to gain or retain their market

share.

Firms employing between 11 and 50 people relied on innovation the most. Thirty per cent of these

respondents claimed that having innovative products was critical for the export efforts and 80% of

them held that it was either critical, very important or importance. In this cohort 36% of the

respondents claimed that having their own research and development facilities was critical to the

export efforts, while a further 49% said it was either important or very important.

Large firms (with more than 200 employees) also attributed their export success to having

innovative products. However, only 10% of these firms claimed that it was critical. The majority of

firms that have been in business for longer than 10 years also recognised the importance of

innovation. More than a quarter of these firms would not export had it not been for their innovative

products. Practically, the entire cohort of these firms considered innovative products to or less least

be important to their exporting.

Very small firms with less than five employees, relied on innovative products. Forty per cent of these

respondents claimed that innovative products were either critical or very important to their export

drive.

Generally firms with less experience (five years or less) did not, however, recognise the importance

of innovative products.

0

10

20

30

40

50

60

70

80

Not important at all Important Very important Critical (without this we would not export)

DRAFT

Of all the firms considered having innovative products critical to the export efforts, 42% had their

own research and development departments and also considered that without this they would not

be in a position to export, A further 25% considered their research and development departments to

be very important.

• Innovative firms experienced the following barriers to expanding into foreign markets:

• Limited financial responses restricted access to finance (37%)

• High cost of imported inputs required for export purposes (53%)

• The high cost of undertaking marketing activities abroad (78%)

• High transport costs (67%)

• Lack of knowledge as to where to find practical advice or assistance (23%)

Productivity

Productivity is a measure of the efficiency of production. Productivity is a ratio of production output

to what is required to produce it (inputs). The measure of productivity is defined as a total output

per one unit of a total input. Although these definitions very general and insufficient to make the

phenomenon productivity understandable, it is a starting point, to understand the cost drivers in the

export competitiveness.

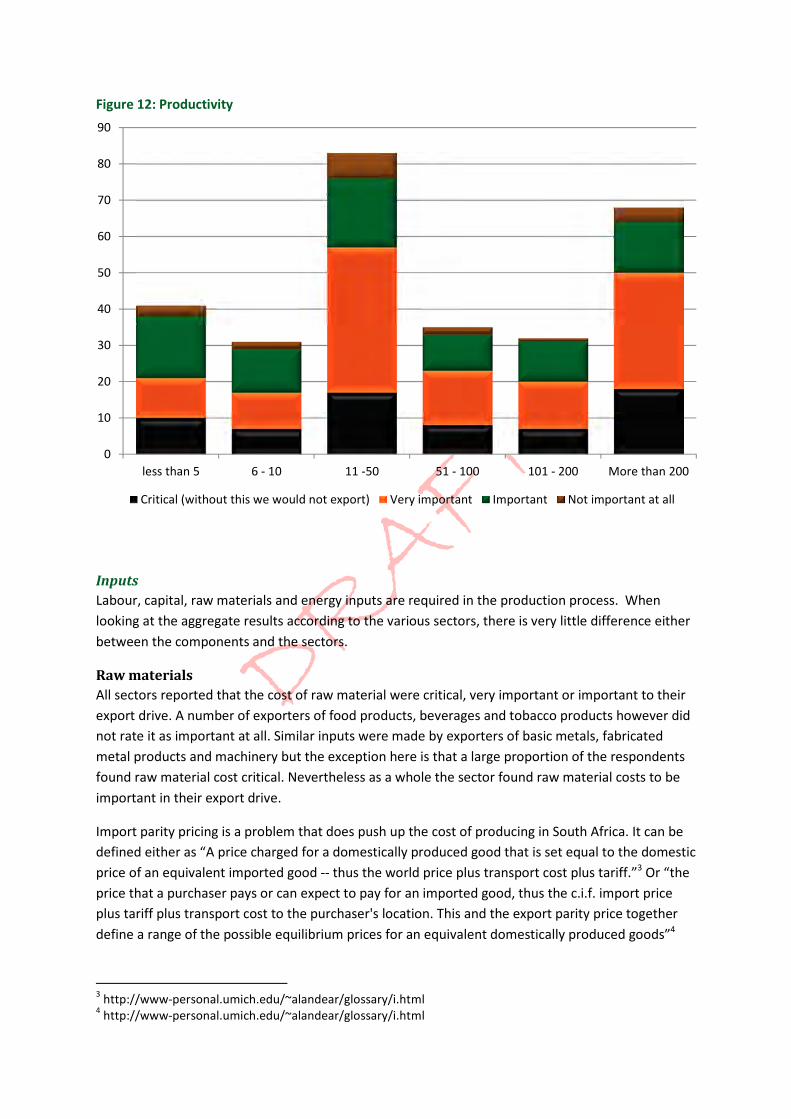

The majority of all firms, irrespective of the size, considered productivity to be at least important in

the export activities. Larger firms (with more than 200 employees) tended to view productivity

slightly more important than smaller firms (73% of these firms view productivity as either critical or

very important). Just over 50% of firms employing less than five people view productivity as being

critical or very important to the export ventures.

Exporters that were part of multi-national corporations, in particular, viewed productivity as

important to the export drive. However, the group that started in exporting due to meeting with

foreign visitors all agreed that productivity was important, with almost 90% considering it either

critical or at least very important to the export success.

DRAFT

Figure 12: Productivity

Inputs

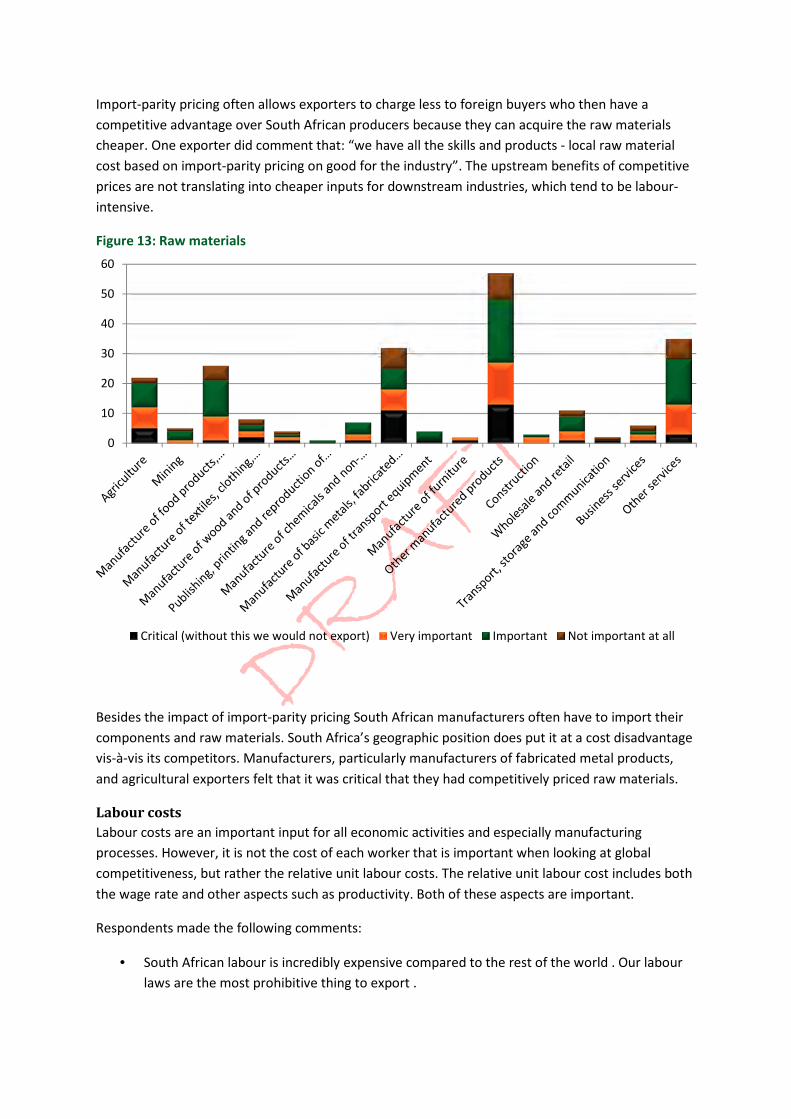

Labour, capital, raw materials and energy inputs are required in the production process. When

looking at the aggregate results according to the various sectors, there is very little difference either

between the components and the sectors.

Raw materials

All sectors reported that the cost of raw material were critical, very important or important to their

export drive. A number of exporters of food products, beverages and tobacco products however did

not rate it as important at all. Similar inputs were made by exporters of basic metals, fabricated

metal products and machinery but the exception here is that a large proportion of the respondents

found raw material cost critical. Nevertheless as a whole the sector found raw material costs to be

important in their export drive.

Import parity pricing is a problem that does push up the cost of producing in South Africa. It can be

defined either as “A price charged for a domestically produced good that is set equal to the domestic

price of an equivalent imported good -- thus the world price plus transport cost plus tariff.”3 Or “the

price that a purchaser pays or can expect to pay for an imported good, thus the c.i.f. import price

plus tariff plus transport cost to the purchaser's location. This and the export parity price together

define a range of the possible equilibrium prices for an equivalent domestically produced goods”4

3 http://www-personal.umich.edu/~alandear/glossary/i.html

4 http://www-personal.umich.edu/~alandear/glossary/i.html

0

10

20

30

40

50

60

70

80

90

less than 5 6 - 10 11 -50 51 - 100 101 - 200 More than 200

Critical (without this we would not export) Very important Important Not important at all

DRAFT

Import-parity pricing often allows exporters to charge less to foreign buyers who then have a

competitive advantage over South African producers because they can acquire the raw materials

cheaper. One exporter did comment that: “we have all the skills and products - local raw material

cost based on import-parity pricing on good for the industry”. The upstream benefits of competitive

prices are not translating into cheaper inputs for downstream industries, which tend to be labour-

intensive.

Figure 13: Raw materials

Besides the impact of import-parity pricing South African manufacturers often have to import their

components and raw materials. South Africa’s geographic position does put it at a cost disadvantage

vis-à-vis its competitors. Manufacturers, particularly manufacturers of fabricated metal products,

and agricultural exporters felt that it was critical that they had competitively priced raw materials.

Labour costs

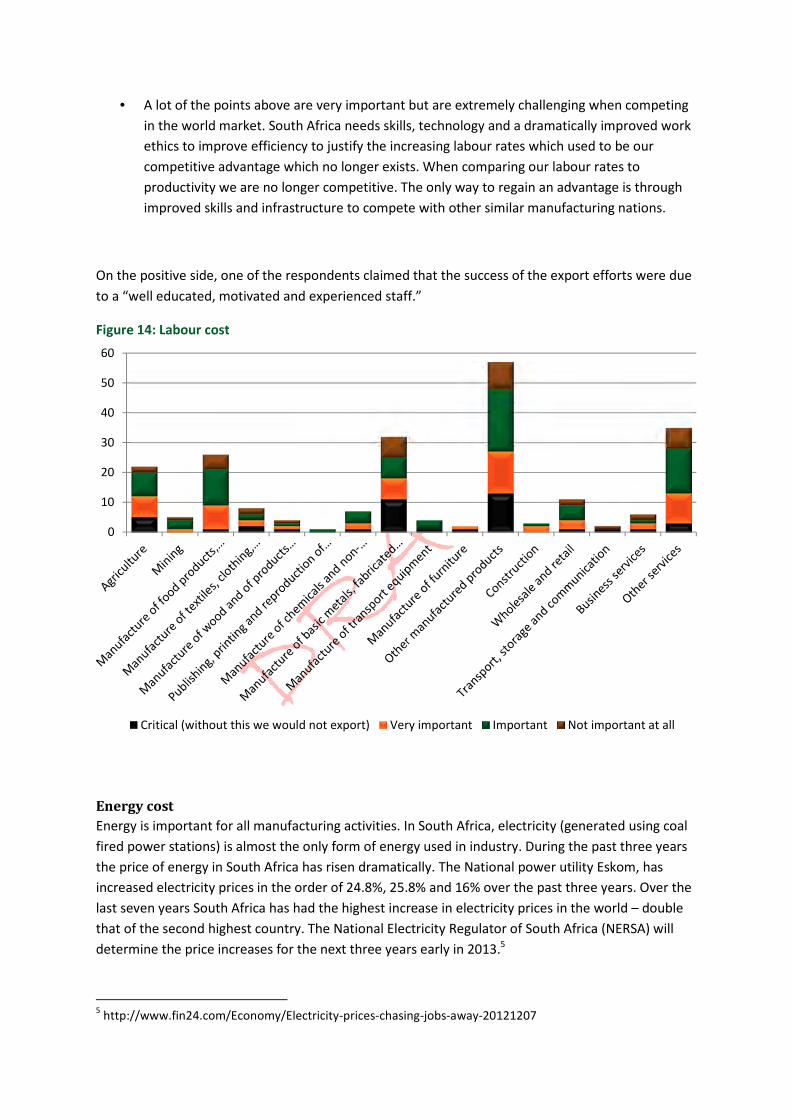

Labour costs are an important input for all economic activities and especially manufacturing

processes. However, it is not the cost of each worker that is important when looking at global

competitiveness, but rather the relative unit labour costs. The relative unit labour cost includes both

the wage rate and other aspects such as productivity. Both of these aspects are important.

Respondents made the following comments:

• South African labour is incredibly expensive compared to the rest of the world . Our labour

laws are the most prohibitive thing to export .

0

10

20

30

40

50

60

Critical (without this we would not export) Very important Important Not important at all

DRAFT

• A lot of the points above are very important but are extremely challenging when competing

in the world market. South Africa needs skills, technology and a dramatically improved work

ethics to improve efficiency to justify the increasing labour rates which used to be our

competitive advantage which no longer exists. When comparing our labour rates to

productivity we are no longer competitive. The only way to regain an advantage is through

improved skills and infrastructure to compete with other similar manufacturing nations.

On the positive side, one of the respondents claimed that the success of the export efforts were due

to a “well educated, motivated and experienced staff.”

Figure 14: Labour cost

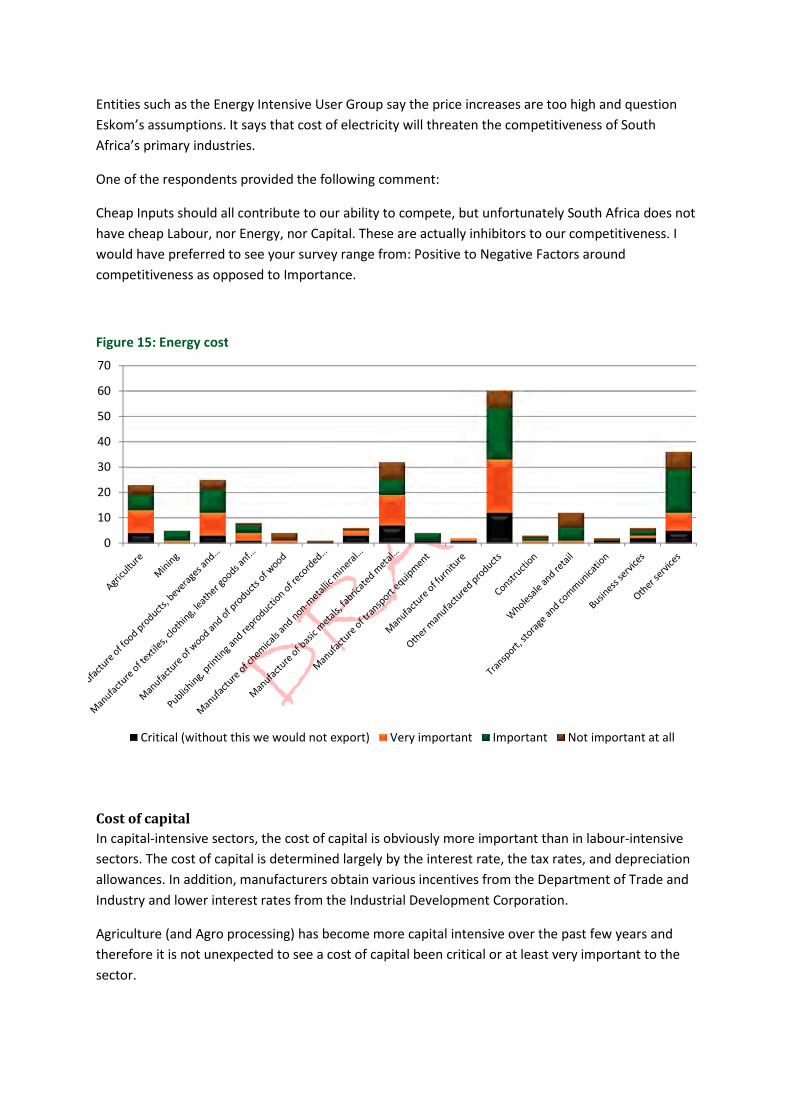

Energy cost

Energy is important for all manufacturing activities. In South Africa, electricity (generated using coal

fired power stations) is almost the only form of energy used in industry. During the past three years

the price of energy in South Africa has risen dramatically. The National power utility Eskom, has

increased electricity prices in the order of 24.8%, 25.8% and 16% over the past three years. Over the

last seven years South Africa has had the highest increase in electricity prices in the world – double

that of the second highest country. The National Electricity Regulator of South Africa (NERSA) will

determine the price increases for the next three years early in 2013.5

5 http://www.fin24.com/Economy/Electricity-prices-chasing-jobs-away-20121207

0

10

20

30

40

50

60

Critical (without this we would not export) Very important Important Not important at all

DRAFT

Entities such as the Energy Intensive User Group say the price increases are too high and question

Eskom’s assumptions. It says that cost of electricity will threaten the competitiveness of South

Africa’s primary industries.

One of the respondents provided the following comment:

Cheap Inputs should all contribute to our ability to compete, but unfortunately South Africa does not

have cheap Labour, nor Energy, nor Capital. These are actually inhibitors to our competitiveness. I

would have preferred to see your survey range from: Positive to Negative Factors around

competitiveness as opposed to Importance.

Figure 15: Energy cost

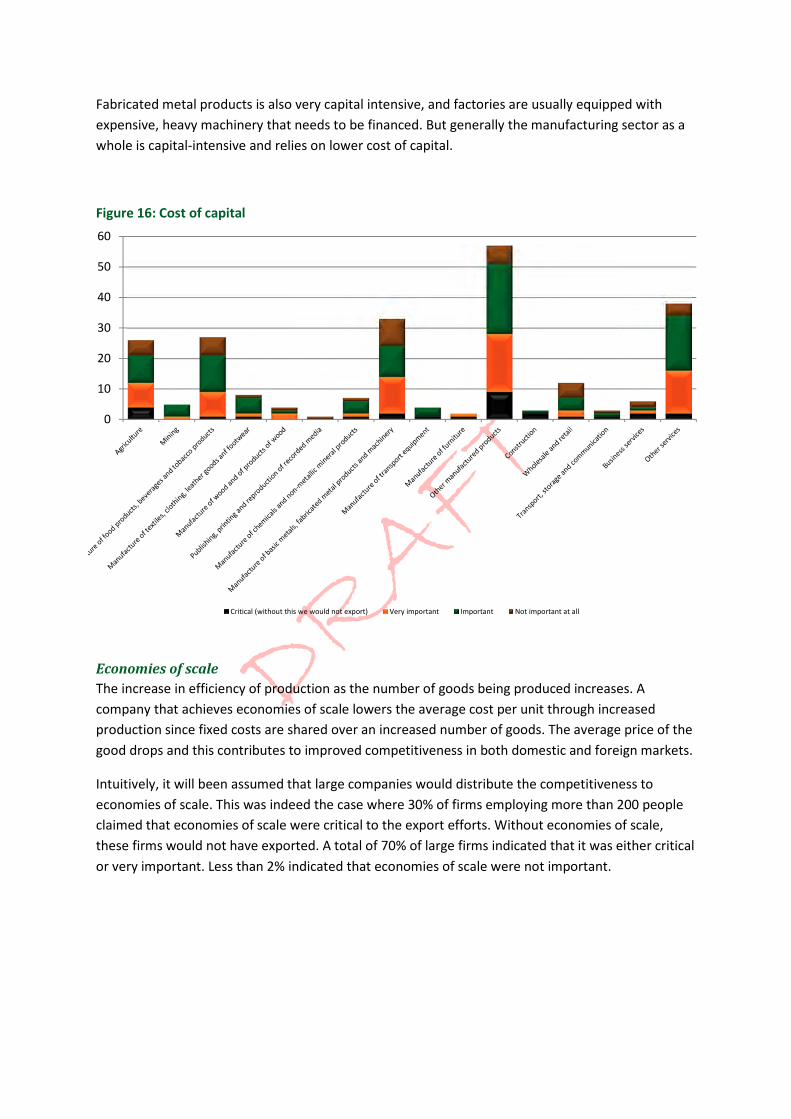

Cost of capital

In capital-intensive sectors, the cost of capital is obviously more important than in labour-intensive

sectors. The cost of capital is determined largely by the interest rate, the tax rates, and depreciation

allowances. In addition, manufacturers obtain various incentives from the Department of Trade and

Industry and lower interest rates from the Industrial Development Corporation.

Agriculture (and Agro processing) has become more capital intensive over the past few years and

therefore it is not unexpected to see a cost of capital been critical or at least very important to the

sector.

0

10

20

30

40

50

60

70

Critical (without this we would not export) Very important Important Not important at all

DRAFT

Fabricated metal products is also very capital intensive, and factories are usually equipped with

expensive, heavy machinery that needs to be financed. But generally the manufacturing sector as a

whole is capital-intensive and relies on lower cost of capital.

Figure 16: Cost of capital

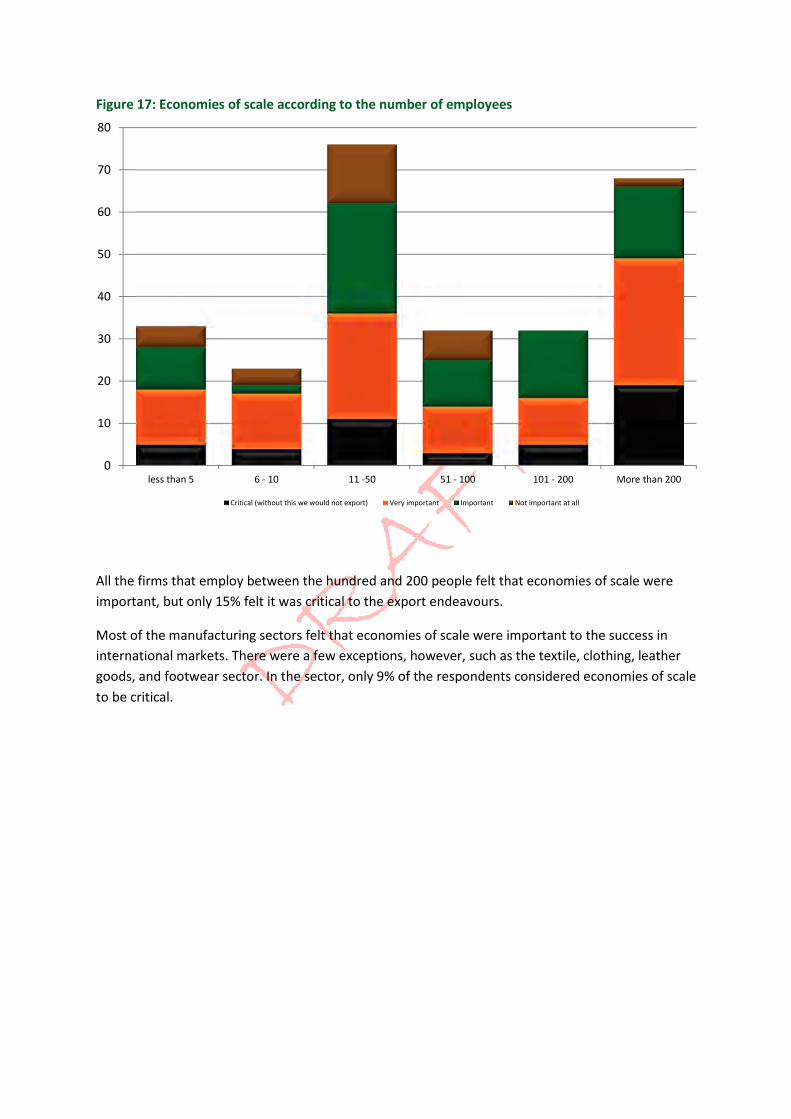

Economies of scale

The increase in efficiency of production as the number of goods being produced increases. A

company that achieves economies of scale lowers the average cost per unit through increased

production since fixed costs are shared over an increased number of goods. The average price of the

good drops and this contributes to improved competitiveness in both domestic and foreign markets.

Intuitively, it will been assumed that large companies would distribute the competitiveness to

economies of scale. This was indeed the case where 30% of firms employing more than 200 people

claimed that economies of scale were critical to the export efforts. Without economies of scale,

these firms would not have exported. A total of 70% of large firms indicated that it was either critical

or very important. Less than 2% indicated that economies of scale were not important.

0

10

20

30

40

50

60

Critical (without this we would not export) Very important Important Not important at all

DRAFT

Figure 17: Economies of scale according to the number of employees

All the firms that employ between the hundred and 200 people felt that economies of scale were

important, but only 15% felt it was critical to the export endeavours.

Most of the manufacturing sectors felt that economies of scale were important to the success in

international markets. There were a few exceptions, however, such as the textile, clothing, leather

goods, and footwear sector. In the sector, only 9% of the respondents considered economies of scale

to be critical.

0

10

20

30

40

50

60

70

80

less than 5 6 - 10 11 -50 51 - 100 101 - 200 More than 200

Critical (without this we would not export) Very important Important Not important at all

DRAFT

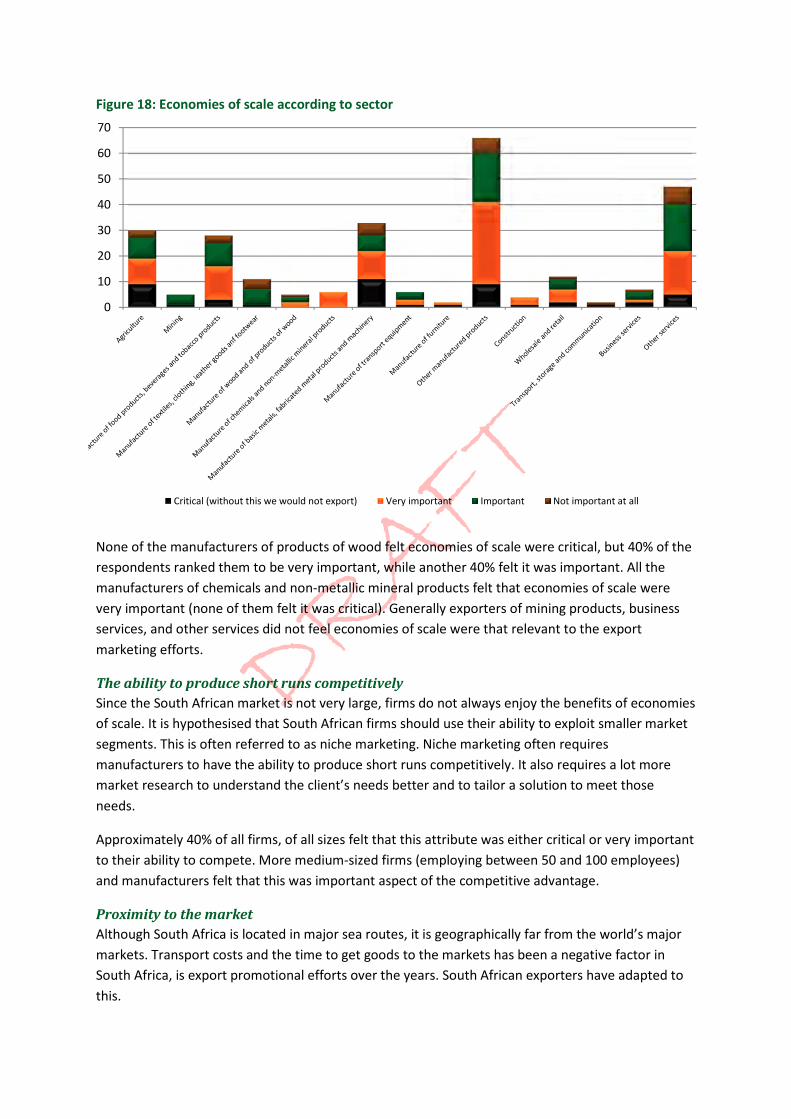

Figure 18: Economies of scale according to sector

None of the manufacturers of products of wood felt economies of scale were critical, but 40% of the

respondents ranked them to be very important, while another 40% felt it was important. All the

manufacturers of chemicals and non-metallic mineral products felt that economies of scale were

very important (none of them felt it was critical). Generally exporters of mining products, business

services, and other services did not feel economies of scale were that relevant to the export

marketing efforts.

The ability to produce short runs competitively

Since the South African market is not very large, firms do not always enjoy the benefits of economies

of scale. It is hypothesised that South African firms should use their ability to exploit smaller market

segments. This is often referred to as niche marketing. Niche marketing often requires

manufacturers to have the ability to produce short runs competitively. It also requires a lot more

market research to understand the client’s needs better and to tailor a solution to meet those

needs.

Approximately 40% of all firms, of all sizes felt that this attribute was either critical or very important

to their ability to compete. More medium-sized firms (employing between 50 and 100 employees)

and manufacturers felt that this was important aspect of the competitive advantage.

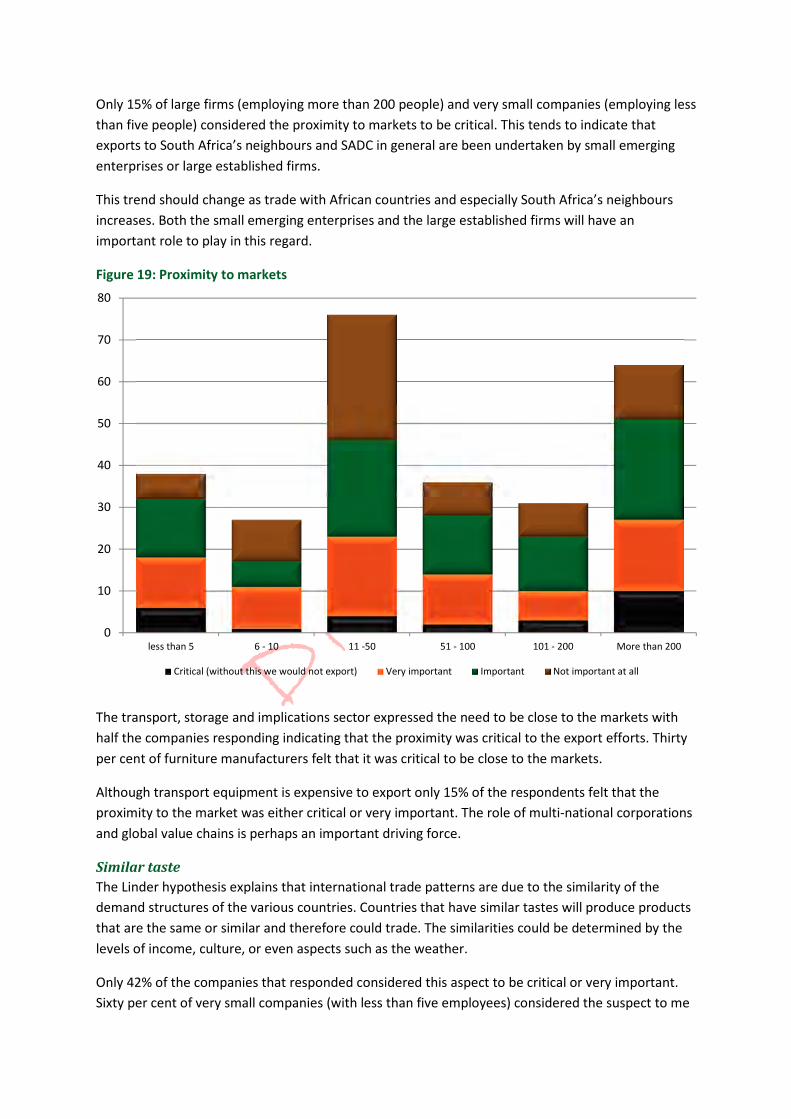

Proximity to the market

Although South Africa is located in major sea routes, it is geographically far from the world’s major

markets. Transport costs and the time to get goods to the markets has been a negative factor in

South Africa, is export promotional efforts over the years. South African exporters have adapted to

this.

0

10

20

30

40

50

60

70

Critical (without this we would not export) Very important Important Not important at all

DRAFT

Only 15% of large firms (employing more than 200 people) and very small companies (employing less

than five people) considered the proximity to markets to be critical. This tends to indicate that

exports to South Africa’s neighbours and SADC in general are been undertaken by small emerging

enterprises or large established firms.

This trend should change as trade with African countries and especially South Africa’s neighbours

increases. Both the small emerging enterprises and the large established firms will have an

important role to play in this regard.

Figure 19: Proximity to markets

The transport, storage and implications sector expressed the need to be close to the markets with

half the companies responding indicating that the proximity was critical to the export efforts. Thirty

per cent of furniture manufacturers felt that it was critical to be close to the markets.

Although transport equipment is expensive to export only 15% of the respondents felt that the

proximity to the market was either critical or very important. The role of multi-national corporations

and global value chains is perhaps an important driving force.

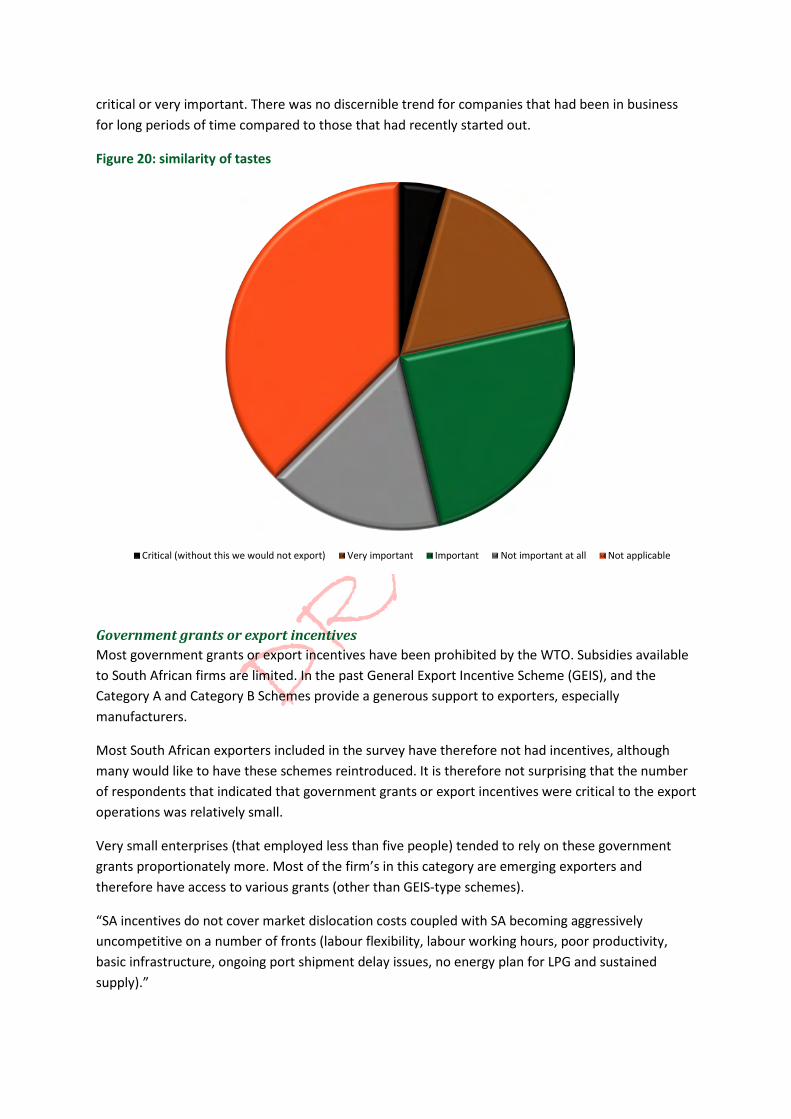

Similar taste

The Linder hypothesis explains that international trade patterns are due to the similarity of the

demand structures of the various countries. Countries that have similar tastes will produce products

that are the same or similar and therefore could trade. The similarities could be determined by the

levels of income, culture, or even aspects such as the weather.

Only 42% of the companies that responded considered this aspect to be critical or very important.

Sixty per cent of very small companies (with less than five employees) considered the suspect to me

0

10

20

30

40

50

60

70

80

less than 5 6 - 10 11 -50 51 - 100 101 - 200 More than 200

Critical (without this we would not export) Very important Important Not important at all

DRAFT

critical or very important. There was no discernible trend for companies that had been in business

for long periods of time compared to those that had recently started out.

Figure 20: similarity of tastes

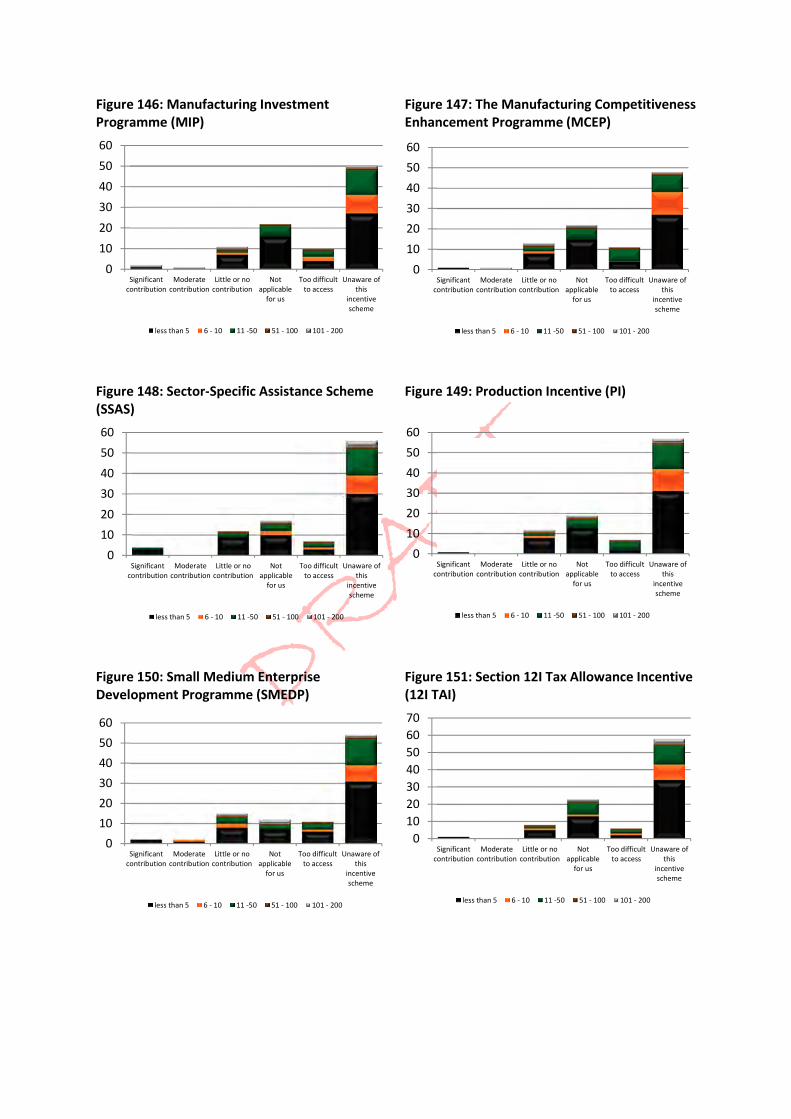

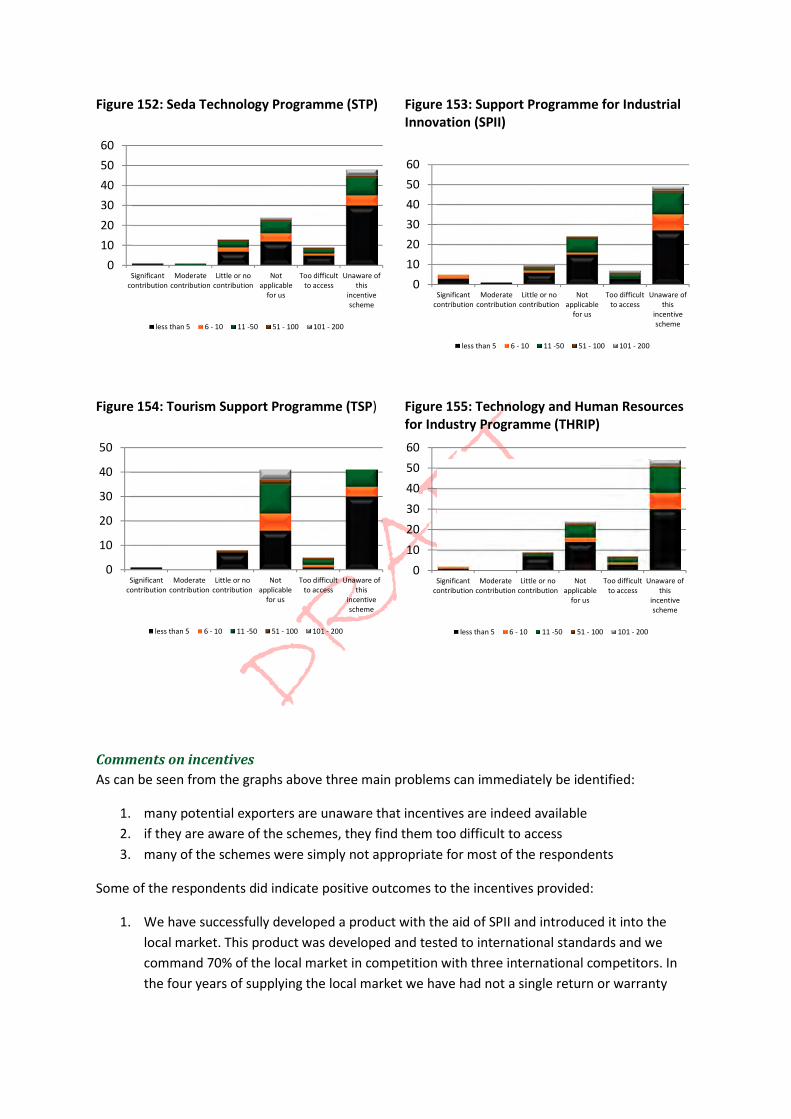

Government grants or export incentives

Most government grants or export incentives have been prohibited by the WTO. Subsidies available

to South African firms are limited. In the past General Export Incentive Scheme (GEIS), and the

Category A and Category B Schemes provide a generous support to exporters, especially

manufacturers.

Most South African exporters included in the survey have therefore not had incentives, although

many would like to have these schemes reintroduced. It is therefore not surprising that the number

of respondents that indicated that government grants or export incentives were critical to the export

operations was relatively small.

Very small enterprises (that employed less than five people) tended to rely on these government

grants proportionately more. Most of the firm’s in this category are emerging exporters and

therefore have access to various grants (other than GEIS-type schemes).

“SA incentives do not cover market dislocation costs coupled with SA becoming aggressively

uncompetitive on a number of fronts (labour flexibility, labour working hours, poor productivity,

basic infrastructure, ongoing port shipment delay issues, no energy plan for LPG and sustained

supply).”

Critical (without this we would not export) Very important Important Not important at all Not applicable

DRAFT

Figure 21: similarity of tastes

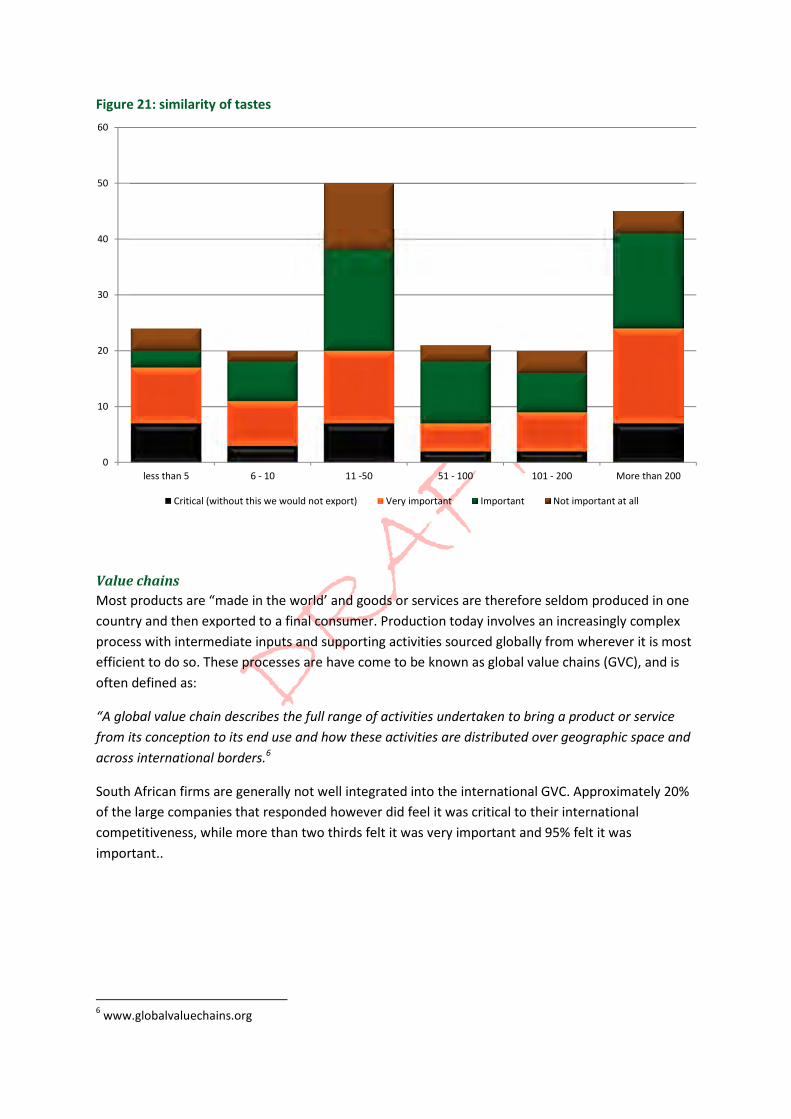

Value chains

Most products are “made in the world’ and goods or services are therefore seldom produced in one

country and then exported to a final consumer. Production today involves an increasingly complex

process with intermediate inputs and supporting activities sourced globally from wherever it is most

efficient to do so. These processes are have come to be known as global value chains (GVC), and is

often defined as:

“A global value chain describes the full range of activities undertaken to bring a product or service

from its conception to its end use and how these activities are distributed over geographic space and

across international borders.6

South African firms are generally not well integrated into the international GVC. Approximately 20%

of the large companies that responded however did feel it was critical to their international

competitiveness, while more than two thirds felt it was very important and 95% felt it was

important..

6 www.globalvaluechains.org

0

10

20

30

40

50

60

less than 5 6 - 10 11 -50 51 - 100 101 - 200 More than 200

Critical (without this we would not export) Very important Important Not important at all

DRAFT

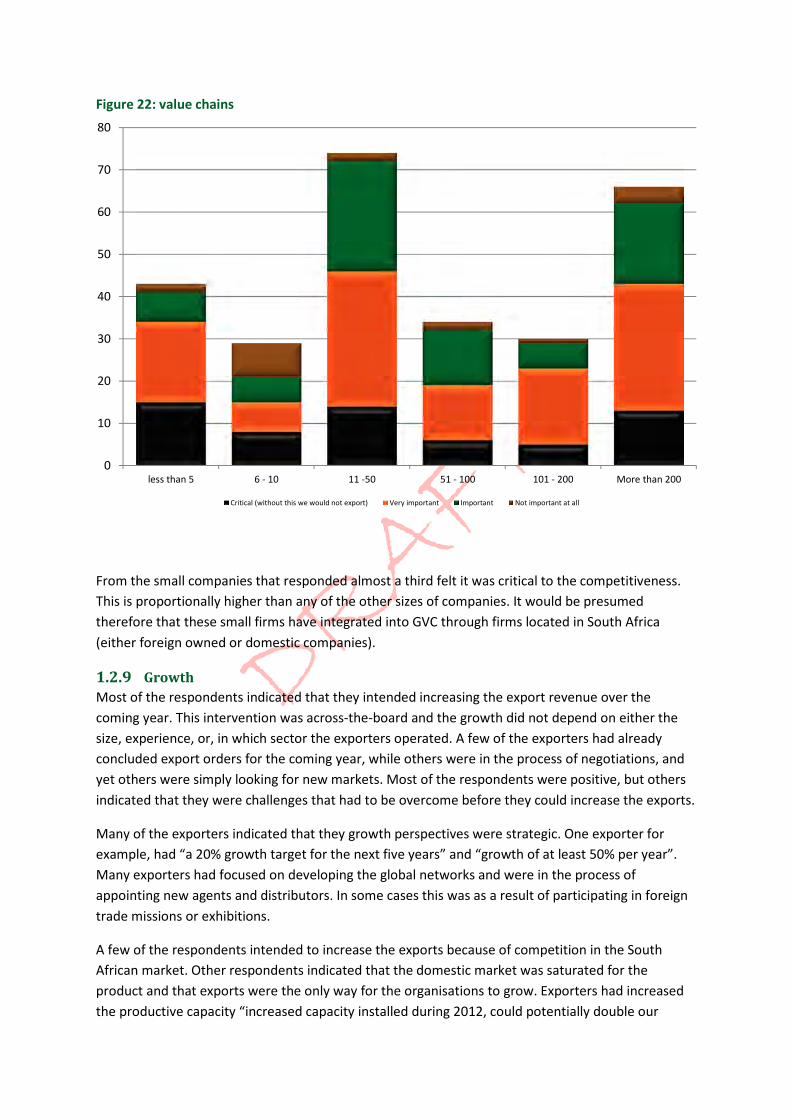

Figure 22: value chains

From the small companies that responded almost a third felt it was critical to the competitiveness.

This is proportionally higher than any of the other sizes of companies. It would be presumed

therefore that these small firms have integrated into GVC through firms located in South Africa

(either foreign owned or domestic companies).

1.2.9 Growth

Most of the respondents indicated that they intended increasing the export revenue over the

coming year. This intervention was across-the-board and the growth did not depend on either the

size, experience, or, in which sector the exporters operated. A few of the exporters had already

concluded export orders for the coming year, while others were in the process of negotiations, and

yet others were simply looking for new markets. Most of the respondents were positive, but others

indicated that they were challenges that had to be overcome before they could increase the exports.

Many of the exporters indicated that they growth perspectives were strategic. One exporter for

example, had “a 20% growth target for the next five years” and “growth of at least 50% per year”.

Many exporters had focused on developing the global networks and were in the process of

appointing new agents and distributors. In some cases this was as a result of participating in foreign

trade missions or exhibitions.

A few of the respondents intended to increase the exports because of competition in the South

African market. Other respondents indicated that the domestic market was saturated for the

product and that exports were the only way for the organisations to grow. Exporters had increased

the productive capacity “increased capacity installed during 2012, could potentially double our

0

10

20

30

40

50

60

70

80

less than 5 6 - 10 11 -50 51 - 100 101 - 200 More than 200

Critical (without this we would not export) Very important Important Not important at all

DRAFT

exports”, “Increase production from ~50k to ~80k over the next year. Similarly increase exports

number”, “WILL HAVE EXTRA PLANT CAPACITY”

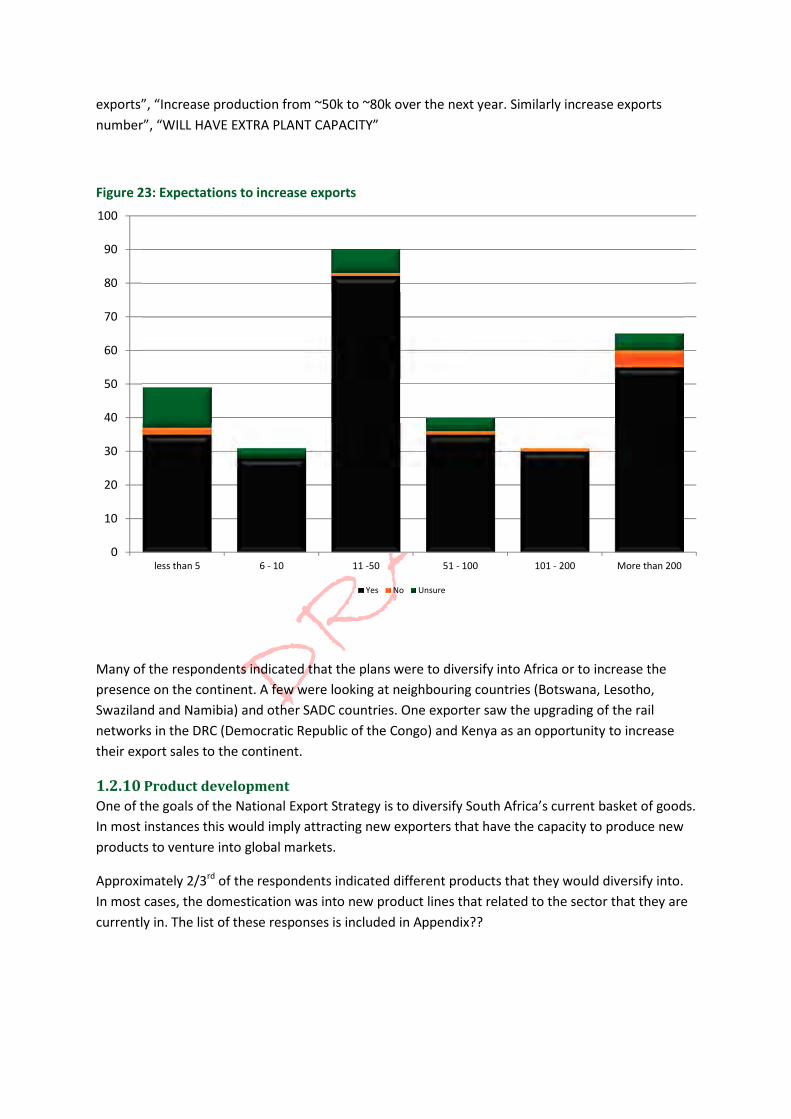

Figure 23: Expectations to increase exports

Many of the respondents indicated that the plans were to diversify into Africa or to increase the

presence on the continent. A few were looking at neighbouring countries (Botswana, Lesotho,

Swaziland and Namibia) and other SADC countries. One exporter saw the upgrading of the rail

networks in the DRC (Democratic Republic of the Congo) and Kenya as an opportunity to increase

their export sales to the continent.

1.2.10 Product development

One of the goals of the National Export Strategy is to diversify South Africa’s current basket of goods.

In most instances this would imply attracting new exporters that have the capacity to produce new

products to venture into global markets.

Approximately 2/3rd

of the respondents indicated different products that they would diversify into.

In most cases, the domestication was into new product lines that related to the sector that they are

currently in. The list of these responses is included in Appendix??

0

10

20

30

40

50

60

70

80

90

100

less than 5 6 - 10 11 -50 51 - 100 101 - 200 More than 200

Yes No Unsure

DRAFT

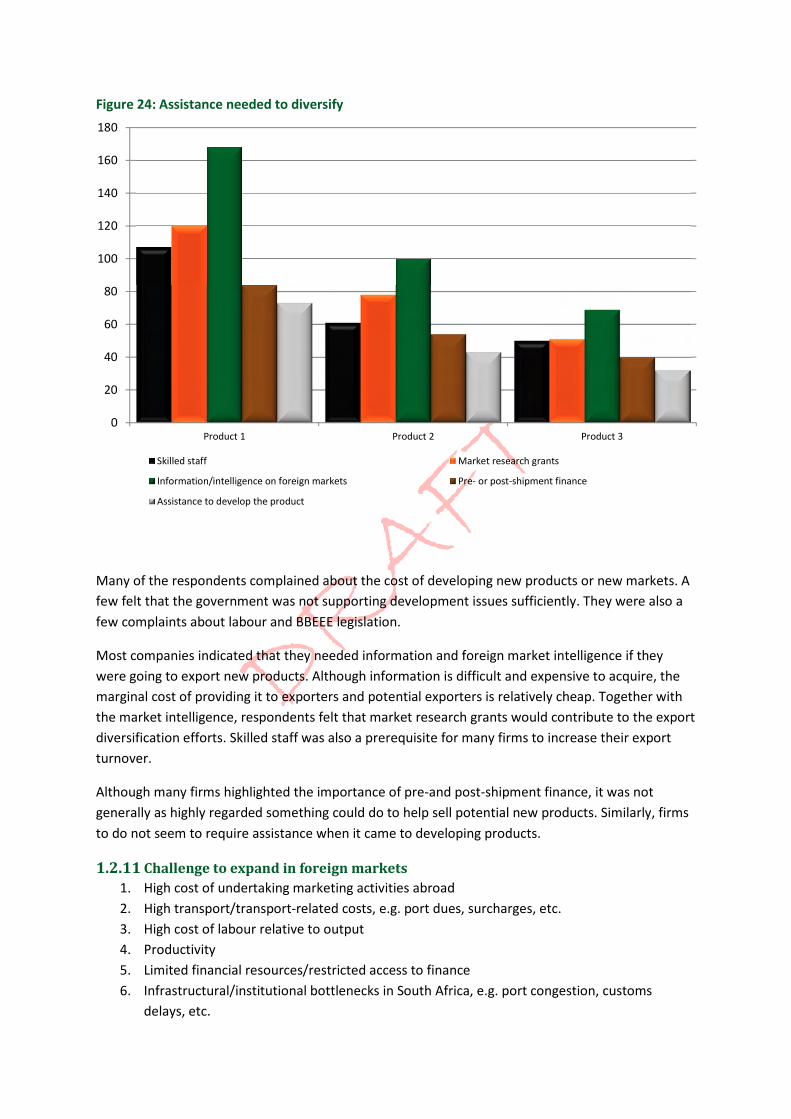

Figure 24: Assistance needed to diversify

Many of the respondents complained about the cost of developing new products or new markets. A

few felt that the government was not supporting development issues sufficiently. They were also a

few complaints about labour and BBEEE legislation.

Most companies indicated that they needed information and foreign market intelligence if they

were going to export new products. Although information is difficult and expensive to acquire, the

marginal cost of providing it to exporters and potential exporters is relatively cheap. Together with

the market intelligence, respondents felt that market research grants would contribute to the export

diversification efforts. Skilled staff was also a prerequisite for many firms to increase their export

turnover.

Although many firms highlighted the importance of pre-and post-shipment finance, it was not

generally as highly regarded something could do to help sell potential new products. Similarly, firms

to do not seem to require assistance when it came to developing products.

1.2.11 Challenge to expand in foreign markets

1. High cost of undertaking marketing activities abroad

2. High transport/transport-related costs, e.g. port dues, surcharges, etc.

3. High cost of labour relative to output

4. Productivity

5. Limited financial resources/restricted access to finance

6. Infrastructural/institutional bottlenecks in South Africa, e.g. port congestion, customs

delays, etc.

0

20

40

60

80

100

120

140

160

180

Product 1 Product 2 Product 3

Skilled staff Market research grants

Information/intelligence on foreign markets Pre- or post-shipment finance

Assistance to develop the product

DRAFT

7. High cost of imported inputs required for export purposes

8. Shortage of available personnel skilled in imports/exports

9. Lack of time to devote to a more active export drive

10. Difficulty in locating individuals/entities that are qualified to offer practical advice and/or

assistance

11. High expense associated with obtaining practical advice and/or assistance

12. Poor quality assistance from existing sources

13. National export website (portal)

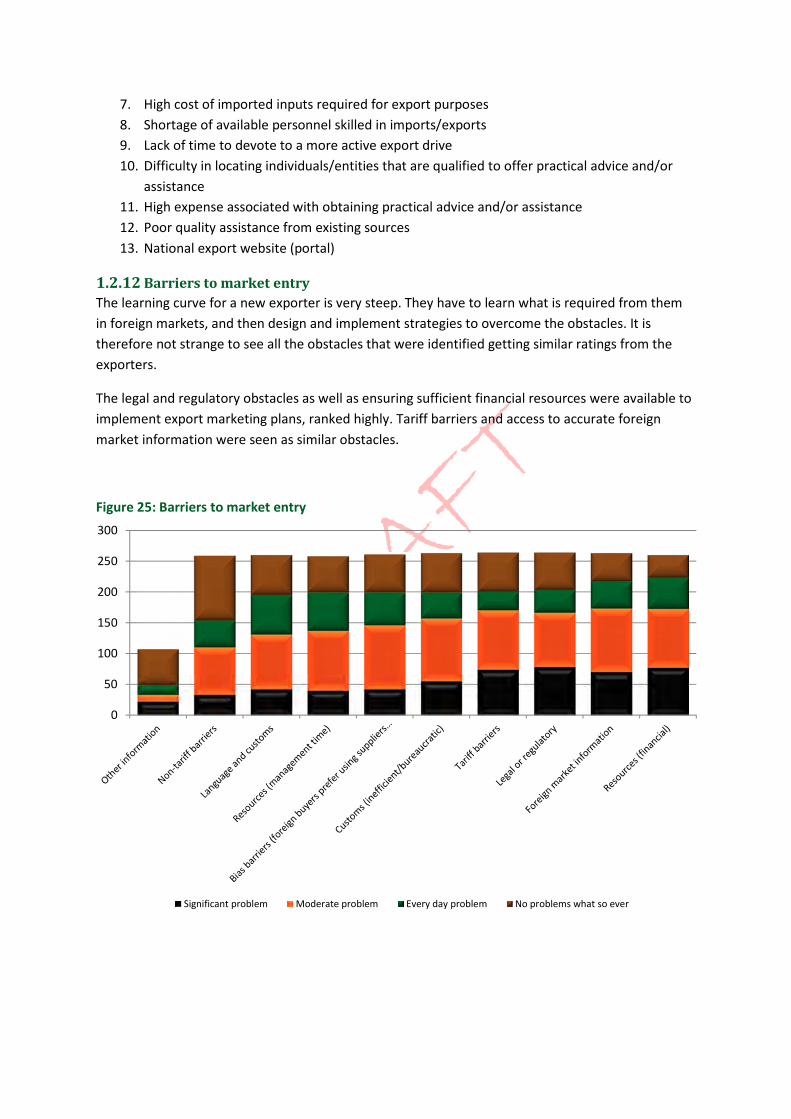

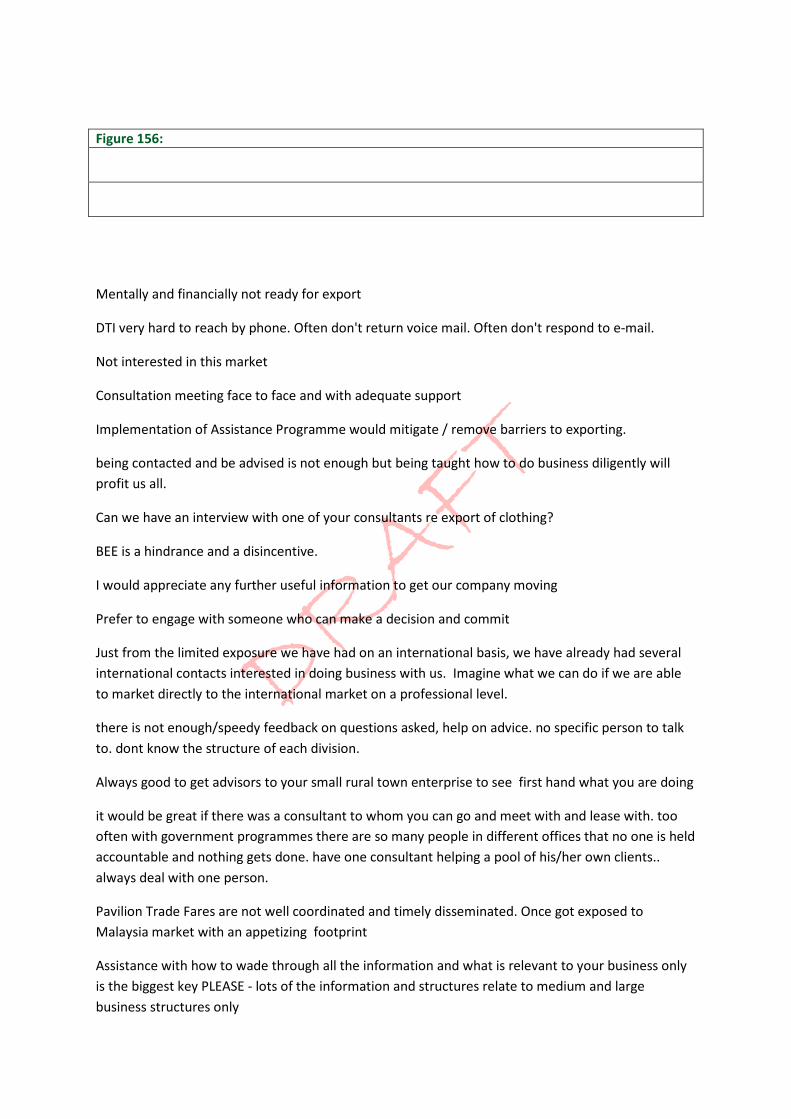

1.2.12 Barriers to market entry

The learning curve for a new exporter is very steep. They have to learn what is required from them

in foreign markets, and then design and implement strategies to overcome the obstacles. It is

therefore not strange to see all the obstacles that were identified getting similar ratings from the

exporters.

The legal and regulatory obstacles as well as ensuring sufficient financial resources were available to

implement export marketing plans, ranked highly. Tariff barriers and access to accurate foreign

market information were seen as similar obstacles.

Figure 25: Barriers to market entry

0

50

100

150

200

250

300

Significant problem Moderate problem Every day problem No problems what so ever

DRAFT

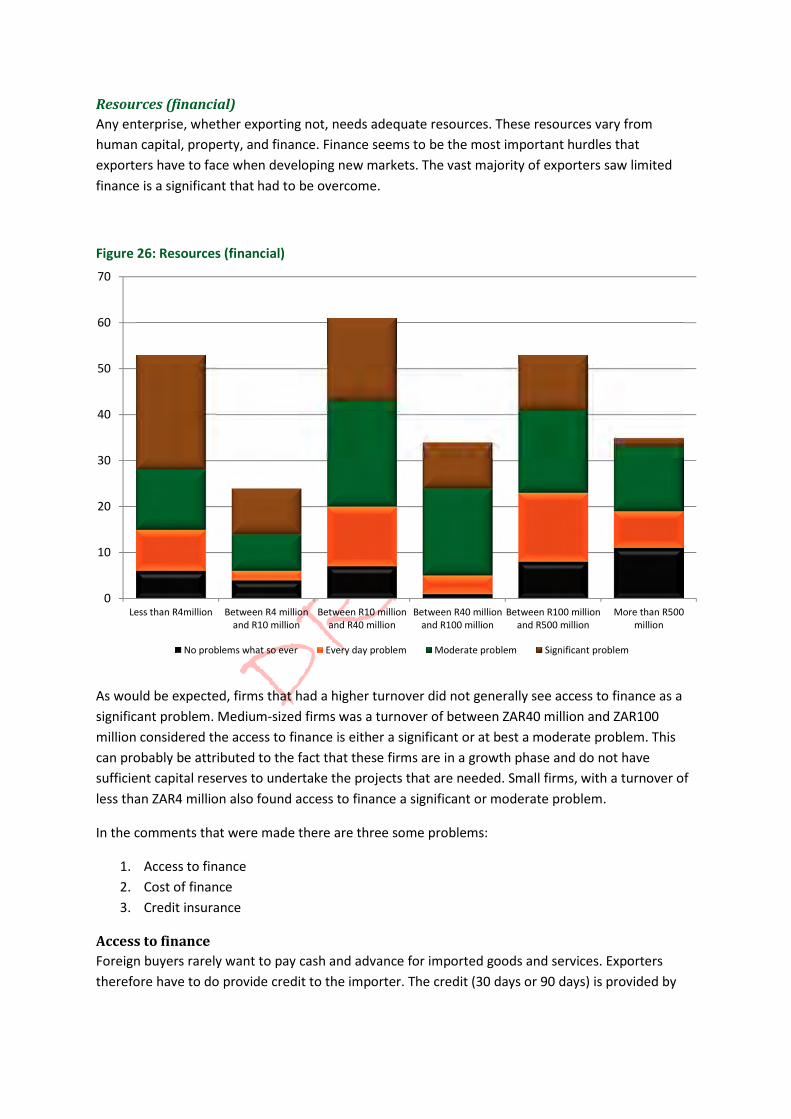

Resources (financial)

Any enterprise, whether exporting not, needs adequate resources. These resources vary from

human capital, property, and finance. Finance seems to be the most important hurdles that

exporters have to face when developing new markets. The vast majority of exporters saw limited

finance is a significant that had to be overcome.

Figure 26: Resources (financial)

As would be expected, firms that had a higher turnover did not generally see access to finance as a

significant problem. Medium-sized firms was a turnover of between ZAR40 million and ZAR100

million considered the access to finance is either a significant or at best a moderate problem. This

can probably be attributed to the fact that these firms are in a growth phase and do not have

sufficient capital reserves to undertake the projects that are needed. Small firms, with a turnover of

less than ZAR4 million also found access to finance a significant or moderate problem.

In the comments that were made there are three some problems:

1. Access to finance

2. Cost of finance

3. Credit insurance

Access to finance

Foreign buyers rarely want to pay cash and advance for imported goods and services. Exporters

therefore have to do provide credit to the importer. The credit (30 days or 90 days) is provided by

0

10

20

30

40

50

60

70

Less than R4million Between R4 million

and R10 million

Between R10 million

and R40 million

Between R40 million

and R100 million

Between R100 million

and R500 million

More than R500

million

No problems what so ever Every day problem Moderate problem Significant problem

DRAFT

the exporter when the goods are received by the importer. The exporter therefore has to carry the

cost of finance, while the goods are transit.

Although numerous trade finance, methods and instruments have been developed to meet the

needs of traders throughout the trade cycle, it is not always readily available to all exporters,

especially emerging exporters or very small exporters.

Pre-shipment financing is for the period prior to the shipment of goods, to support pre-export

activities such as wages raw material and overhead costs that are needed as inputs for the

production of the goods that are going to be exported. Pre-shipment finance is especially important

to small enterprises because the international sales cycle is usually longer than the domestic sales

cycle. Pre-shipment finance can take the form of short-term loans, overdrafts or cash credits.

Exporters that responded made the following comments:

• Capital / funding is useful to take advantage of established positions to grow our brands to be

significant leaders and shareholders in export markets. South Africa has a wonderful

opportunity to this but lack of funding limits our possibilities.

• Capital tied up during manufacture.

• Lack of funds to develop larger supply base.

• not enough funding available and not prepared to accept personal surety.

• Capital tied up during manufacture.

Post-shipment finance on the other hand, is for the period following the shipment of the goods. The

competitiveness of exporters often depends on the ability to provide buyers with attractive credit

terms has described above, stop post-shipment finance ensures liquidity of the exporter until the

purchaser receives the products and the exporter receives payment. Post-shipment finance is usually

short term.

Cost of finance

The cost of finance, or the interest rate, varies across countries. Often, it is higher in South Africa,

then in many of the trading partners. This puts South African exporters as a disadvantage.

• this is a major problem with SMME (Small-, Micro- and Medium-sized Enterprises)’s in the wine

industry our sector does not cater specially for BEE (Black Economic Empowerment) businesses

in the wine industry and access to funding has to much red tape.

• difficulty obtaining trade finance.

• The costs to a small company are horrendous.

• The payment terms of large mining companies are not supplier friendly and dictates substancial

levels of working capital.

Although the South African commercial banks are well positioned to provide all the necessary

services to South African exporters that are established, they did not always appreciate the

developmental aspects. It is therefore important that the developmental financial institutions play a

big role in assisting emerging exporters develop new markets.

DRAFT

• DTI assists with some relief, but IDC (Industrial Development Corporation) does not recognise

an export marketing service as being worthy of assisting ! Black Empowered entities are

completely bereft of funds and banks will not assist.

• We were working in Mozambique for a very big South African client who did not believe in SME

(Small- and medium-sized Enterprises)’s This made me realise that large companies speak the

SME speak but don’t want them as they cut the rates in the market. We needed bridging

finance so we did not have to ask the client for quick payment turnaround which in turn gave

him knowledge on our cash flow which was a major disadvantage to us.

Credit insurance

It is more risky providing credit to foreign buyers, then it is to South African buyers. Legal systems

across the world are different and very expensive to use. Besides a commercial risk, there is also

political and transfer risk when dealing across borders. Credit insurance is an insurance policy and a

risk management product offered by private insurance companies and governmental export credit

agencies to business entities wishing to protect their accounts receivable from loss due to credit

risks such as protracted default, insolvency or bankruptcy.

Respondents felt that the cover offered to South African exporters was not comparable to that

available to the foreign competitors:

• Limited Credit Insurance companies, conservative risk policies.

• Credit guarantee not available on exports to Zimbabwe. Development of the market for our

brands requires terms which are a burden.

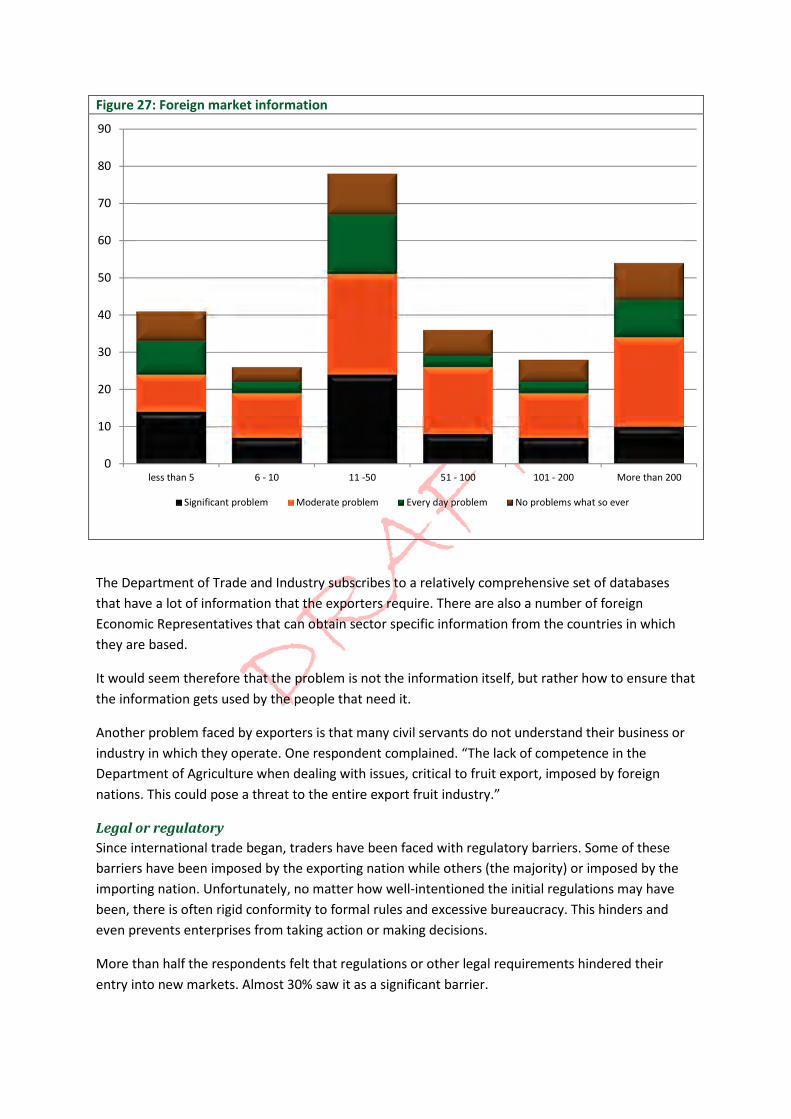

Foreign market information

Most of the exporters need accurate market intelligence. Approximately ¾ of the exporters surveyed

indicated that obtaining this foreign market information was either a significant or moderate

problem.

DRAFT

Figure 27: Foreign market information

The Department of Trade and Industry subscribes to a relatively comprehensive set of databases

that have a lot of information that the exporters require. There are also a number of foreign

Economic Representatives that can obtain sector specific information from the countries in which

they are based.

It would seem therefore that the problem is not the information itself, but rather how to ensure that

the information gets used by the people that need it.

Another problem faced by exporters is that many civil servants do not understand their business or

industry in which they operate. One respondent complained. “The lack of competence in the

Department of Agriculture when dealing with issues, critical to fruit export, imposed by foreign

nations. This could pose a threat to the entire export fruit industry.”

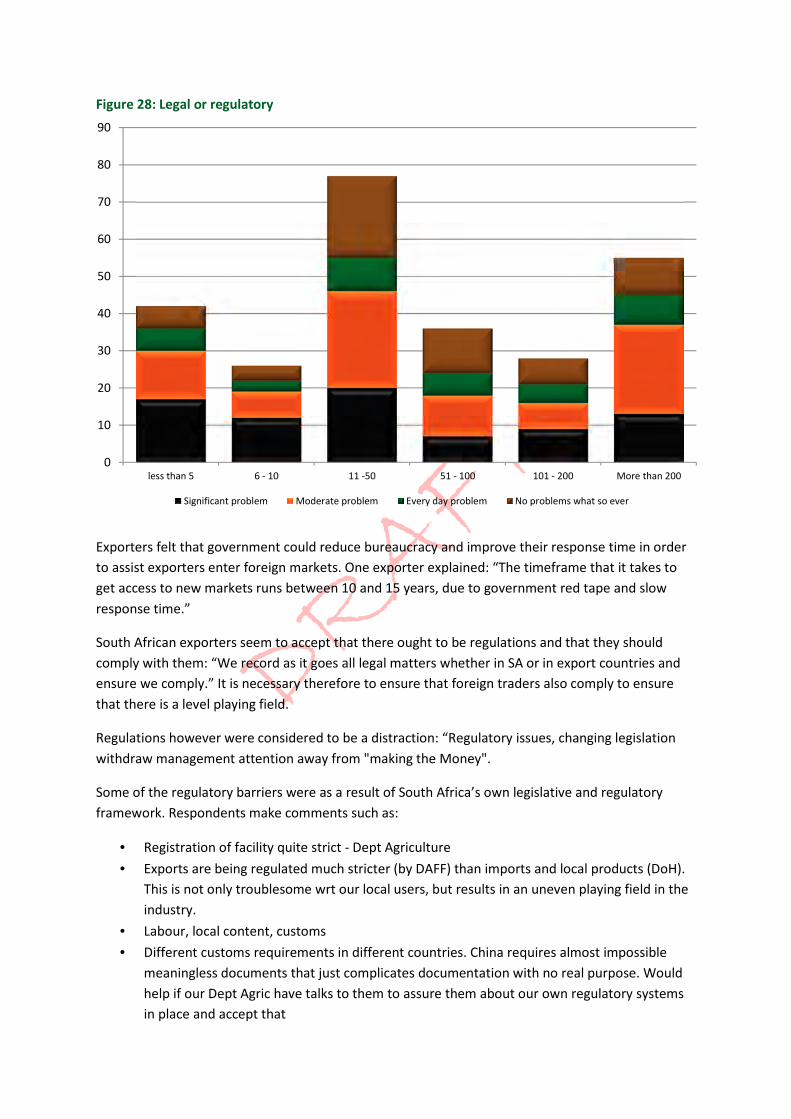

Legal or regulatory

Since international trade began, traders have been faced with regulatory barriers. Some of these

barriers have been imposed by the exporting nation while others (the majority) or imposed by the

importing nation. Unfortunately, no matter how well-intentioned the initial regulations may have

been, there is often rigid conformity to formal rules and excessive bureaucracy. This hinders and

even prevents enterprises from taking action or making decisions.

More than half the respondents felt that regulations or other legal requirements hindered their

entry into new markets. Almost 30% saw it as a significant barrier.

0

10

20

30

40

50

60

70

80

90

less than 5 6 - 10 11 -50 51 - 100 101 - 200 More than 200

Significant problem Moderate problem Every day problem No problems what so ever

DRAFT

Figure 28: Legal or regulatory

Exporters felt that government could reduce bureaucracy and improve their response time in order

to assist exporters enter foreign markets. One exporter explained: “The timeframe that it takes to

get access to new markets runs between 10 and 15 years, due to government red tape and slow

response time.”

South African exporters seem to accept that there ought to be regulations and that they should

comply with them: “We record as it goes all legal matters whether in SA or in export countries and

ensure we comply.” It is necessary therefore to ensure that foreign traders also comply to ensure

that there is a level playing field.

Regulations however were considered to be a distraction: “Regulatory issues, changing legislation

withdraw management attention away from "making the Money".

Some of the regulatory barriers were as a result of South Africa’s own legislative and regulatory

framework. Respondents make comments such as:

• Registration of facility quite strict - Dept Agriculture

• Exports are being regulated much stricter (by DAFF) than imports and local products (DoH).

This is not only troublesome wrt our local users, but results in an uneven playing field in the

industry.

• Labour, local content, customs

• Different customs requirements in different countries. China requires almost impossible

meaningless documents that just complicates documentation with no real purpose. Would

help if our Dept Agric have talks to them to assure them about our own regulatory systems

in place and accept that

0

10

20

30

40

50

60

70

80

90

less than 5 6 - 10 11 -50 51 - 100 101 - 200 More than 200

Significant problem Moderate problem Every day problem No problems what so ever

DRAFT

• Our own governments compliance requirements takes up to much valuable time

• DAFF personnel shortages

• Especially - Labour laws, mining law, BEE,

• BEE will kill the company in two years

Foreign regulations on food and wine also seem to present problems for exporters:

• Lack of funding to attend international buyers offices and promote. Nigeria - Nafdac number

for example, you need R50 000 to obtain before exporting, please assist.

• Nigeria is very difficult with NAFDAQ

• NAFDAC registration of wine in Nigeria is expensive.

• NAFDAC (NIGERIA)

• Phyto Sanitary regulations or agreements not in Place

• Phytosanitory, no bi-lateral trade agreements with some countries

• USDA laws

• Insurance (liabilities, food related)

• ISO 93485 and FDA

• Products obviously have to meet export markets' food safety requirements

Labelling and packaging legislation is often complex and difficult to comply with.

• EU and FDA Legislation regarding packaging requirements, and assignment of responsibilities

given the lack of personnel based there

• Translated back labels

• Obtaining the CE mark on our yachts

Quality

• Problems with establishing ISO 9000 qualification

• Registration of products in foreign markets take too long and the processes are very tedious.

• Registering products in certain countries can be a nightmare: such as South America and

Israel. Obtaining Freesale certificates etc. is a challenge

The regulatory burdens will not uniform across all countries. Exporters felt that it “depends on the

country - some places are better than others.” “Some markets like China and USA has got very

difficult regulations to enter market.” Another exporter made the comment that regulations are

“market dependant, but generally EU compliance suffices apart from N America.

Exporters also felt that the South African government could be more helpful in overcoming some of

the legal and regulatory barriers. They felt that there was “limited advice to Exporters of any system,

regulation changes etc”. SMEs did not have the necessary resources comply with regulations and

were therefore also affected: “It is very costly for a small business to obtain all the required

accreditations and certifications.”

The regulations often vary within countries: “Setting up franchise agreements in different countries

is very expensive. For example, in the USA, we have to set up a different franchise agreement per

state, as the franchise laws differ in some states.”

DRAFT

The sector needs assistance with understanding the technical regulatory requirements for boat

building in different countries and the level of compliance. For example some countries require

inspections and certifications that can cost an SME up to R50 000. This is not sustainable with small

boat orders. In addition the regional and provincial requirements differ in some countries eg

Australia and Brazil. If the dti were able to appoint sector specific technical experts to provide this

advice to the industry it would significantly reduce the barrier to entering a new market.

Exporters also had issues with trademarks both in South Africa (that needed to be protected from

foreign competition) and assistance with registering their trademarks internationally.

Negotiating contracts is difficult at the best of times, but it’s complicated with different legal

systems operating across the world. Exporters indicated a need for assistance with legal compliances

and contractual issues.

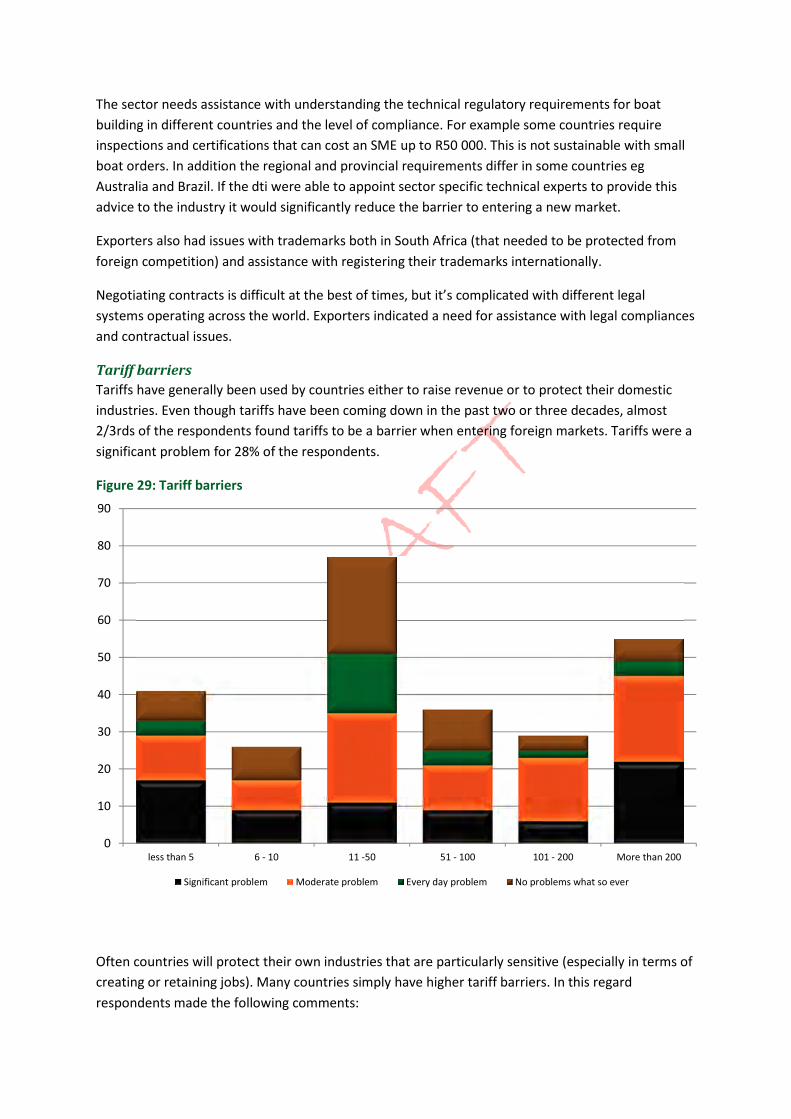

Tariff barriers

Tariffs have generally been used by countries either to raise revenue or to protect their domestic

industries. Even though tariffs have been coming down in the past two or three decades, almost

2/3rds of the respondents found tariffs to be a barrier when entering foreign markets. Tariffs were a

significant problem for 28% of the respondents.

Figure 29: Tariff barriers

Often countries will protect their own industries that are particularly sensitive (especially in terms of

creating or retaining jobs). Many countries simply have higher tariff barriers. In this regard

respondents made the following comments:

0

10

20

30

40

50

60

70

80

90

less than 5 6 - 10 11 -50 51 - 100 101 - 200 More than 200

Significant problem Moderate problem Every day problem No problems what so ever

DRAFT

• Certain markets have barriers. Particular problem is lack of free trade agreements in several

Asian countries versus our competitor countries.

• Tariffs for wine exports some countries duties too high, SA need to reduce duty on wine to

increase sales

• India, Thailand - very high import duties on wine, makes our landed cost exorbitant

• China, India and Turkey have duties on our nuts

• Africa is the big problem in this respect

• China, India, Mexico

• India has a 35% import tariff for South African citrus. Russia and China also have but less.

Can it not be solved through our BRICS membership ?

• Only some countries such as S.America: their import duties are very high

• US import duties, make it prohibitive to export any cosmetics into the USA

• Customs and Government tax on the wine industry is too high. Out of a bottle of R18.00, the

farmer only gets R0.33,

• Especially in emerging markets where growth is coming from and wine consumption is new.

Help on this matter (reducing tariff barriers) should be made a priority.

• Please do something about import taxes/ surcharges into China!

• Japan, Israel, Europe

• Import duties of our products into the EU versus other African countries

• EU tariff change on concentrate fruit purees

• High tariffs in China, Philippines, north Africa (Kenya, etc.), and other

• India is potentially our biggest buyer as they love fruit (Hindu) but.... citrus is for example

duty'd by 40% plus. We are a member of BRICS and do not clash with their growers, but no

real action by our government. This matter is of unbelievable importance and can

conceivably change our fruit export landscape.

• Tariff in India is very high (30%) making the product very expensive to the end user.

• The most significant problem in Sub-Sahara is not so much the Tariff, but the fact that some

operators avoid it, hence rendering product "legally" imported unsaleable

• The current tariffs into Brazil are extremely high and do not encourage BRICS trade from a

boat building perspective.

• Cannot export to Brazil or India because of import duties (20 - 30%). Have to appoint local

agents/manufacturers who invariably cheat.

• Anti-dumping duties on imported steel ropes that are not even manufactured in S.A.!

• Asia and South America protect their markets more than SA does

• Duties on wine too high we as BEE company are unable to enter the industry being taxed the

same as the corporate companies is highly unfair which gives us disadvantage and barrier to

market entry.

Free Trade Agreements also made it difficult for South African exporters to penetrate foreign

markets:

• Competing against COMESA

• The South African LCV Market is based on the Thailand LCV (1 tonne Market). They have

critical mass, we don't but we have to follow their lead. For RSA companies to compete with

ASEAN countries we are restricted by their FTA.

DRAFT

• Certain Markets favour buying local (ie Nigeria) where there is a current ban of Imported

Office Furniture

Exporters suggested that government assist with the “difficulties and cost to get rebate/ bond store

up and running”

A few exporters complained about the South African port costs and felt that “ports are over

regulated and extremely expensive.”

One exporter felt that the South African VAT regulations presented a significant barrier to entering

new markets if “VAT on exports if not physically exporting.”

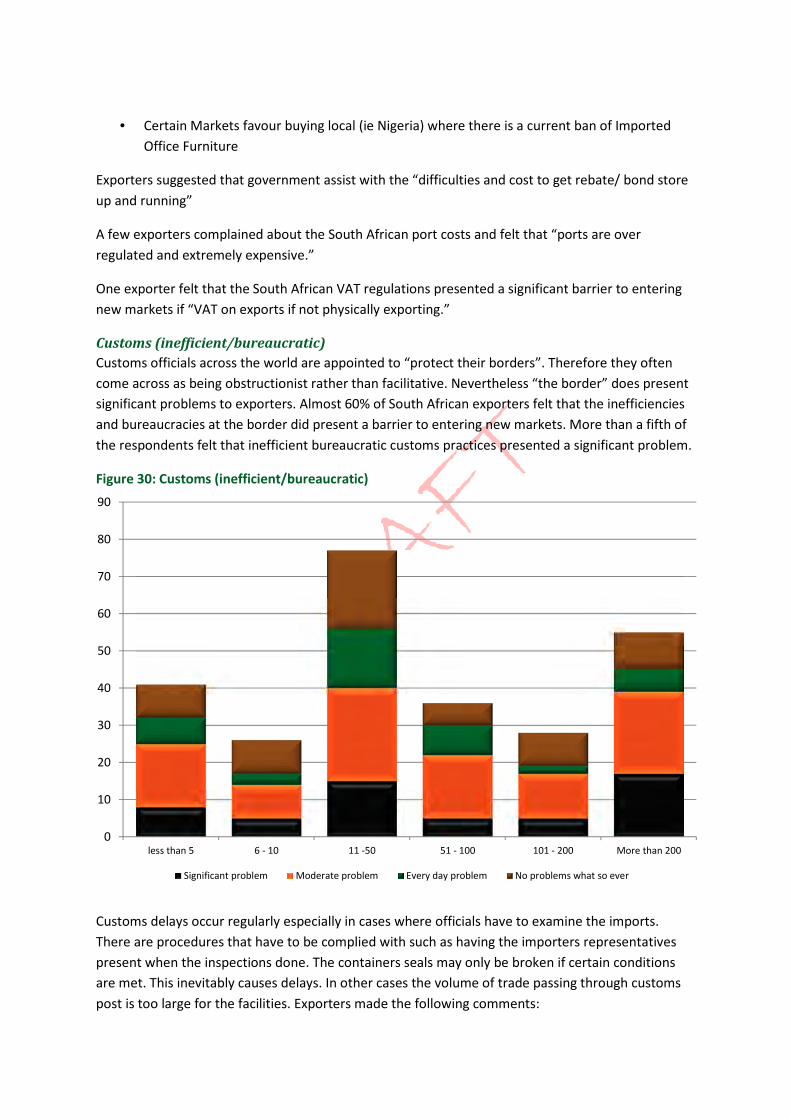

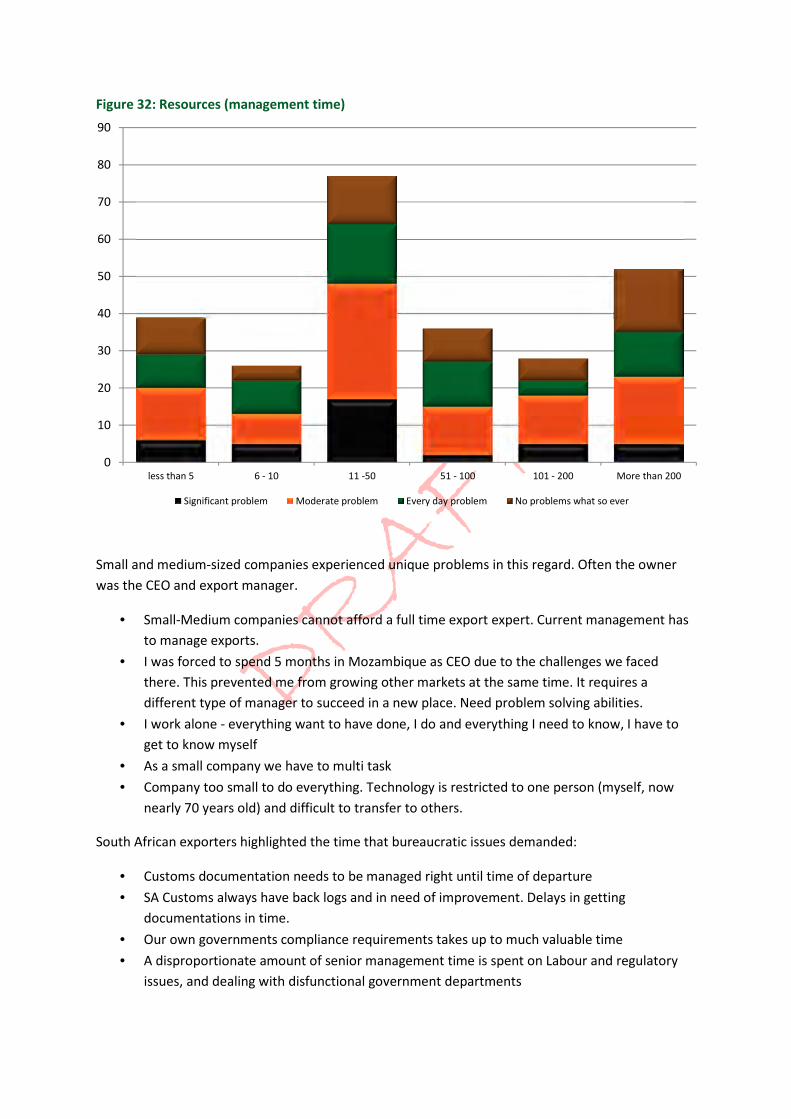

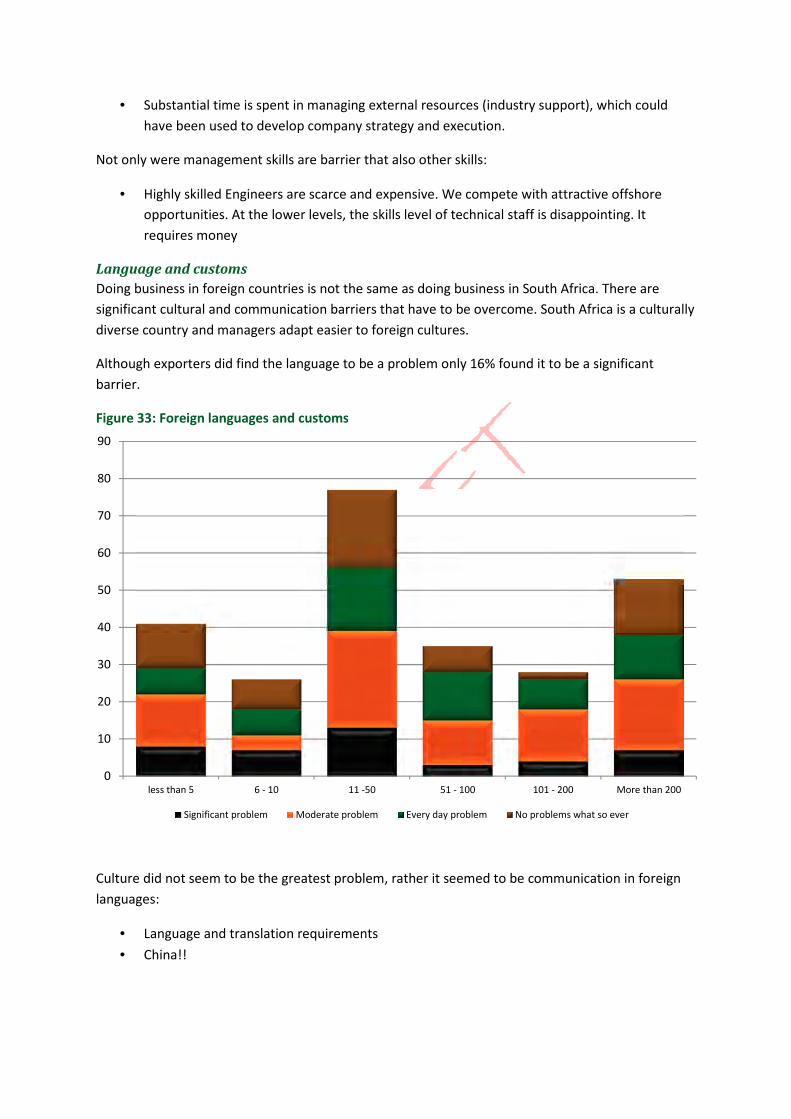

Customs (inefficient/bureaucratic)

Customs officials across the world are appointed to “protect their borders”. Therefore they often

come across as being obstructionist rather than facilitative. Nevertheless “the border” does present

significant problems to exporters. Almost 60% of South African exporters felt that the inefficiencies

and bureaucracies at the border did present a barrier to entering new markets. More than a fifth of

the respondents felt that inefficient bureaucratic customs practices presented a significant problem.

Figure 30: Customs (inefficient/bureaucratic)

Customs delays occur regularly especially in cases where officials have to examine the imports.

There are procedures that have to be complied with such as having the importers representatives

present when the inspections done. The containers seals may only be broken if certain conditions

are met. This inevitably causes delays. In other cases the volume of trade passing through customs

post is too large for the facilities. Exporters made the following comments:

0

10

20

30

40

50

60

70

80

90

less than 5 6 - 10 11 -50 51 - 100 101 - 200 More than 200

Significant problem Moderate problem Every day problem No problems what so ever

DRAFT

• We almost lost the company this year due to a 5 month customs delay in Mozambique. I

would see a big benefit of Wesgro providing export support.

• Zimbabwe border is difficult

• Massive fines imposed on small human errors, and no motivations, explanations accepted.

• Serious delays at border post with Zimbabwe

• Problem releasing Safmarine containers in Genoa

• Barriers at destination port when importing from South Africa

In a few cases respondents complained about corruption at Customs “in the lands we export to, to

much corruption, our containers can be delayed for weeks while someone waits for his "fee".”

Bureaucratic & corrupt especially Africa.

Customs officials often seem to be “very high handed attitude places unnecessary extra costs on

incoming products to make exports expensive -- Customs do not help -- only hinder the process.”

Labour unrest at Customs (or even at the ports) can cause considerable delays. Even in South Africa

when “strikes delay imported goods therefore there is a delay in assembly thus late supply to

clients.” “Only when importing components, to combine with locally-made components, for later

export. Repeated delays experienced (when already late) in having goods released from customs.”

Manufacturing in bond:

• Difficulties and cost to get rebate/ bond store up and running

• For example, we were able to load LCL shipments in Durban. We have been banned by DBN

Customs from doing so and therefore, market is lost. SOS Bonded Warehouse cost is too

expensive. Although goods were always packed and loaded under Customs Supervision.

South African Customs could also be more helpful in “some 'challenges' in getting HS code

determinations from SARS”

Documentation is also a problem:

• Turnaround to prepare documents can be done more quickly.

Bias barriers (foreign buyers prefer using suppliers in their country)

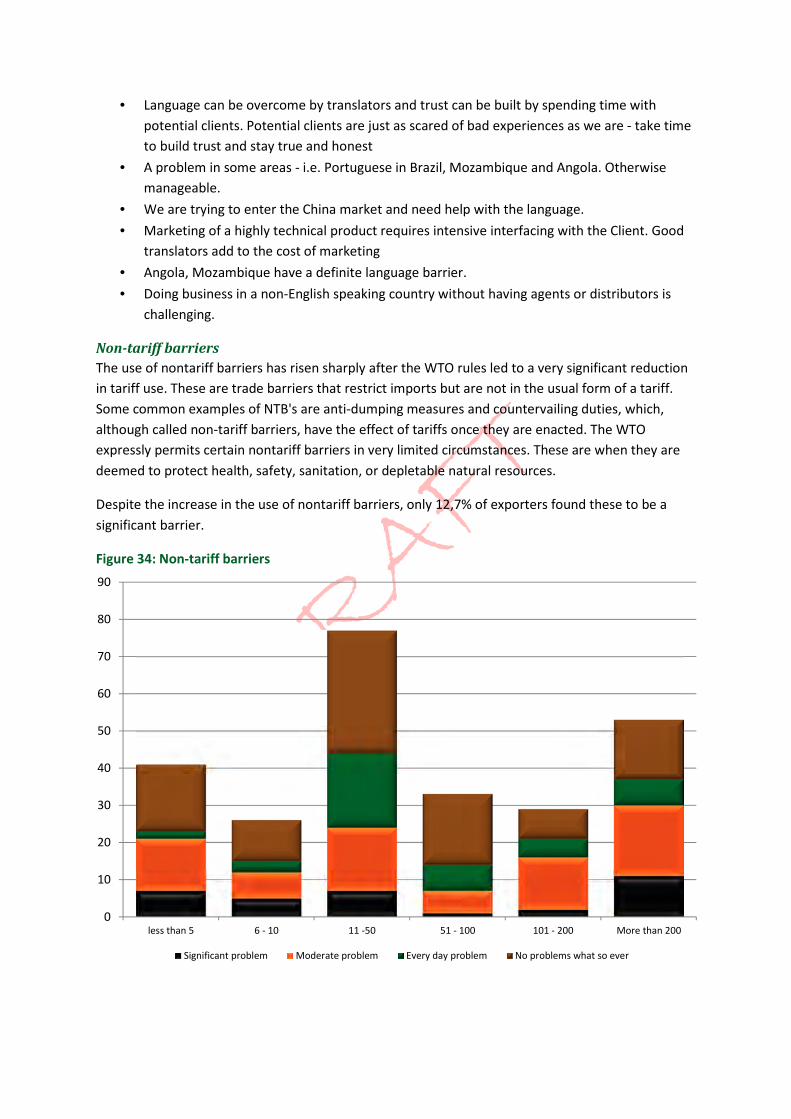

Marketing is the process of communicating the value of a product or service to customers.