1 legal & insurance workshop a fresh perspective on nonprofit law 2011 fundamental five+...

TRANSCRIPT

1

Legal & InsuranceWorkshop

A Fresh Perspective on Nonprofit Law

2011 Fundamental Five+ Non-Profit Capacity Training Series

presents

Tom PierceTom Pierce, Attorney at Law, LLLC

February 22, 2011

2

Mahalo to our Sponsors!

Office of Hawaiian Affairs - Community Building Economic Development Grant

Grants Central Station - program founder

Tri-Isle Resource Conservation & Development - Fiscal Sponsor

PlayBook Consulting Group - Fundamental Five+ Series Producer / Coordinator

3

More Free Workshops!

Increase Your Skills & Knowledge in these upcoming Fundamental Five+ workshops

March 8 Fundraising & Development Strategies

April 12 Grant Strategy & Writing

4

Agenda

8:30 am Welcome & Introductions

8:45 am Legal

9:45 am BREAK & Network & Submit Questions

10:00 am Insurance

11:15 pm BREAK & Network

11:30 pm Nonprofit Hypothetical – Problem Solving

12:15 pm Wrap-Up, Post-Test, Evaluations

12:30 pm Session Ends

5

Who’s in our Hui?

Public Charities? Foundations? Size (by employees) (by income)? Hospitals, churches, AOAOs, HOAs? Directors? EDs? Staff? How many at Financial Literacy?

6

I'd rather bechasingFrisbees

7

What we need is . . .

8

A Fresh Perspective . . .

9

A Fresh Perspective . . .

The best car safety device is a rear-view mirror with a cop in it. ~Dudley Moore

10

A Fresh Perspective . . .

I can read the fine print. This legal stuff actually makes sense. I'll become more confident to act. My board meetings can be more

efficient. I can avoid time consuming problems. Our best management practices keep

us legal

11

Today's Objectives

• What we will cover:– 501(c)(3) “Public Charities”– Governance issues (new area of IRS focus)– A few “grey” and possibly overlooked areas– Areas that will improve your nonprofit

practices

• What we won't cover:– The Basics (but will have quick refresher)– Other org types (e.g., social, political,

business orgs)– “No brainer” areas– Info covered in Financial Literacy workshop

12

Today's Objectives

• What today offers you:• For startups and prospective

nonprofits:– Get it right the first time– Alternative organization types

• For all other organizations– Ideas for refining existing approach– Tools for spotting and resolving critical

issues– Prudently managing risks

13

Covered Today

Quick 501(c)(3) refresher Governance

– Documents– Using Org documents to your benefit– Conflict of interest policy (how/why)– Compensation policy (how/why)– Relationship to Form 990

14

Covered Today (cont'd)

Donation issues– Pledge agreements– Contemporaneous gift acknowledgment– Form 8283– Meeting and maintaining “public support” test

Brief highlights– Fiscal sponsorship– Employment contracts, handbooks, job

review Liability issues (segue to insurance discussion)

15

Refresher

• ORGANIZATIONAL ISSUE BASICS– Vision– Mission– Goals/objectives– Strategic Plan– Budget

16

Refresher

• STATE ISSUE BASICS– HI Nonprofit Law (HI Rev. Statutes 414D)– Nonprofit corp– Membership corp– Articles

• Purpose– Bylaws– Fiduciary duty

17

Refresher

• FEDERAL ISSUE BASICS

• 501(c)(3)• Public charity• Foundation• Supporting

organization• Private benefit• Private inurement

• Disqualified person

• Insider• Determination

Letter• Public support• Facts and

Circumstances

18

Organizational Documents

“Organizational documents

are your best friend!”

19

Organizational Documents

• Articles– The nonprofit's “constitution”– Filed with DCCA– Usual source for . . .

• Voting rights information• Scope of nonprofit's purpose• Scope of directors' power• Liability and indemnification

information• Authorization to amend Articles/Bylaws

20

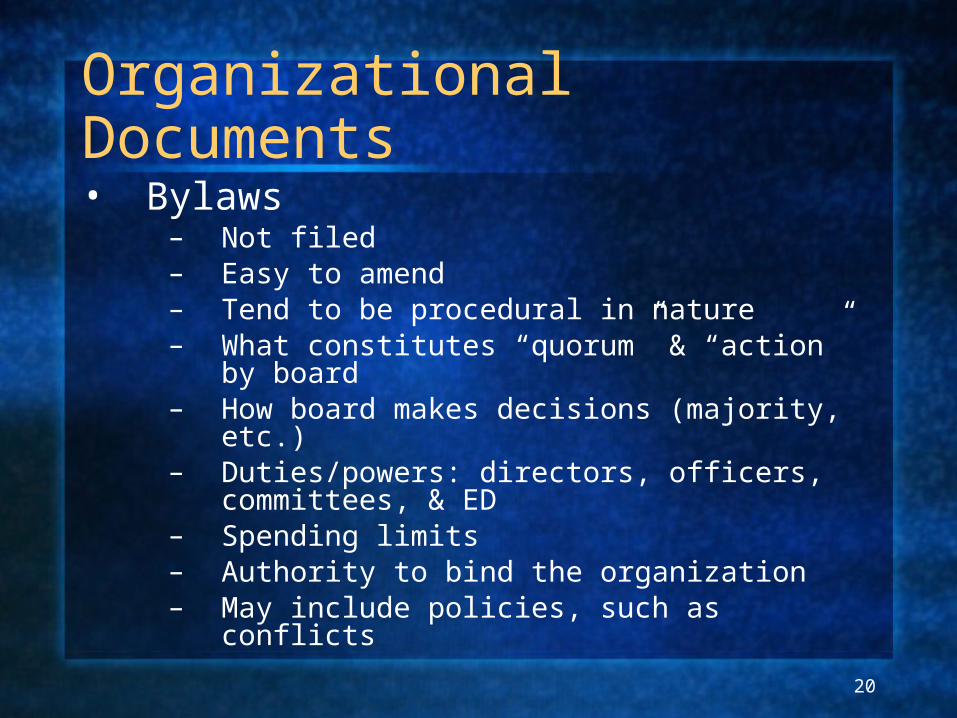

Organizational Documents

• Bylaws– Not filed– Easy to amend– Tend to be procedural in nature– What constitutes “quorum” & “action” by

board– How board makes decisions (majority, etc.)– Duties/powers: directors, officers,

committees, & ED– Spending limits– Authority to bind the organization– May include policies, such as conflicts

21

22

Organizational Documents

AGENDAS• ID discussion

items• ID decisions• Set timelines• ID responsible

presenters• Remind

committees• (See template)

MINUTES• Memorialize

decisions• Who's responsible

for follow up• Don't make it

verbatim• Executive session• (See template)

23

Organizational Documents

• Policies and Resolutions– Policies establish ways of dealing with

anticipated situations• Conflict of Interest Policy• Compensation Policy• Policies regarding donors/donations• Policies specific to your mission

– Resolutions memorialize important decisions

• (e.g., Resolution to purchase a property)

24

Organizational Documents

• Organizational Docs are not static.– Understand their uses so you can adjust

them as needs arise or problems are solved. Such as . . .

– Does the board keep coming back to some issue again and again?

– Are there continuous misunderstandings between the board and staff?

– Are third parties confused about how the organization acts on certain matters?

25

Organizational Documents

“Secretary Binder”– Articles– Bylaws– Policies– Resolutions– Past minutes– Executive

session minutes– DCCA Filings– Determination

Letter– Strategic Plan

• Conduct a yearly “orientation” for all directors

26

Conflicts Policy

• IRS – Enhanced Scrutiny– Testimony– Form 1023 changes– Form 990 changes

27

Conflicts Policy (IRS Concerns)

DETERRENCE OF ABUSES WITHIN TAX -EXEMPT ORGANIZATIONS AND GOVERNMENT ENTITIES

The Need for Enhanced Governance [T]ax-exempt organizations . . . have not been immune from leadership failures. We need go no further than our daily newspapers to learn that some charities and private foundations have their own governance problems. Specifically, we have seen business contracts with related parties, unreasonably high executive compensation, and loans to executives. We at the IRS also have seen an apparent increase in the use of tax-exempt organizations as parties to abusive transactions. All these reflect potential issues of ethics, internal oversight, and conflicts of interest.

28

Conflicts Policy (IRS Testimony)

The publication will explore practices that are not necessarily required by law but that may elevate the standards, conduct, and workings of exempt organizations. Although the IRS does not have authority to require organizations to follow specific practices, organizations without effective governance controls are more likely to have compliance problems. The publication is intended to provide exempt organizations, and in particular public charities, with a list of practices that will help guard against abuses involving, among other things, inappropriate financial transactions and operations. Among the topics we expect to cover are standards of integrity; the role, selection and duties of the governing board; conflict of interest policies; record -keeping; checks and balances that help p revent abuses; and fundraising practices, to name a few.

29

Conflicts Policy (Form 990)

30

Conflicts Policy (Form 990)

31

Conflicts Policy (Form 990)

32

Conflicts Policy (Basic Rule)

• Can the organization reasonably get a more advantageous transaction or arrangement from someone without a conflict?

• If not, can the disinterested directors confirm . . .

– In organization's best interest,– For its own benefit, and– Is fair and reasonable

33

Conflicts Policy (Basic Rule)

• Not all conflicts involve $$• Not just directors can have conflicts

– Officers– Employees– Disqualified persons– Other organization agents– Even the organization!

34

Conflicts Policy (Drafting & Use)

• Policy is contextual to org's activities

• Make document understandable and easy to apply to a situation

• For example . . .

35

Conflicts Policy (Drafting & Use)

• “Thou shalt not. . . . excess benefit transaction, et cetera, et cetera . . .”

36

Conflicts Policy (Drafting & Use)

• IRS sample policy – avoid, if possible

• Provide yearly orientation & discussion

• Sign acknowledgment of review

37

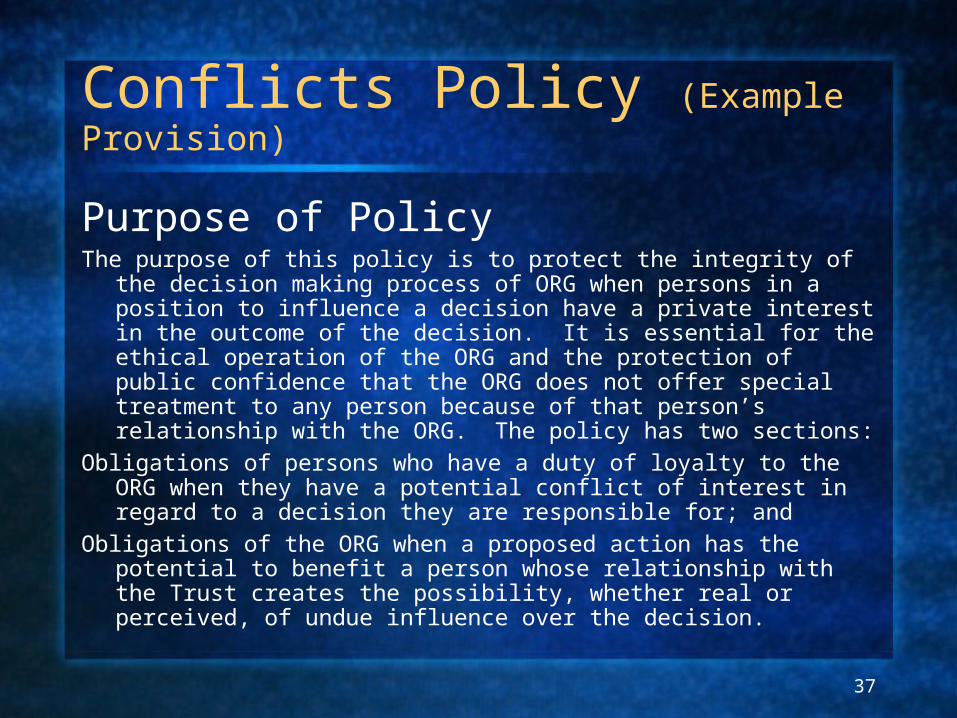

Conflicts Policy (Example Provision)

Purpose of PolicyThe purpose of this policy is to protect the integrity of the

decision making process of ORG when persons in a position to influence a decision have a private interest in the outcome of the decision. It is essential for the ethical operation of the ORG and the protection of public confidence that the ORG does not offer special treatment to any person because of that person’s relationship with the ORG. The policy has two sections:

Obligations of persons who have a duty of loyalty to the ORG when they have a potential conflict of interest in regard to a decision they are responsible for; and

Obligations of the ORG when a proposed action has the potential to benefit a person whose relationship with the Trust creates the possibility, whether real or perceived, of undue influence over the decision.

38

Compensation Policy

• Excessive compensation most common type of “private inurement” (unreasonable private benefit received by an insider)

• Instance of private inurement, however small, can mean “intermediate sanctions” (on both charity, deciding “manager,” and the employee or insider) or loss of revocation of charity's tax exempt status

• IRS questions charities re compensation on both application & 990s

39

Compensation Policy (Form 990)

40

Compensation Policy (Form 990)

41

Compensation Policy

• “Compensation” includes all benefits, such as: salary, medical, retirement, expense allowance, insurance benefits

• To be reasonable, must be approx equal exchange of benefits between charity & employee

• This does not mean a charity cannot pay its employee what he/she is entitled

42

Compensation Policy

• Whether excessive factors include:– Compensation paid to (1) similar orgs, (2) for

equivalent positions, (3) in similar geographical areas

– Charity's need for the particular person's services

– Person's education, background, experience– Size & complexity of charity's income/assets– Disparity between charity employees' income– Number of hours worked

43

Compensation Policy

• Key to defending compensation is to show the directors have actively considered factors & can document their decision:

– Detailed job description– Show comparative salaries considered– No conflicts in decisionmaking process– All benefits (incl., e.g., cars, laptops),

accounted for, including on W-2s

• Comp policy can assure your okay because IRS has a “rebuttable presumption” policy

44

Compensation Policy

• IRS Safe Harbor Provision (payments to insiders presumed reasonable if:

– Board obtained & relied on comparables (3 needed for charity w/$1myn income)

– Board approved in advance total compensation package

– No actual or potential conflicts during decision making

– Board adequately and contemp-oraneously documented its decision

45

Donations

• Contemporaneous acknowledgment of gift (WCA)

– $250 or more? Written contemporaneous acknowledgment required for donor to obtain deduction

– Recent court decisions: No WCA? No deduction (even if other records exist, such as a Form 8283 or canceled checks).

– “Contemporaneous” = not later than 1/31 of following year (but don't wait)

46

Donations (WCA)

• Include this information– Name of organization– Amount of cash donation– Description of non-cash donation– “No goods or services were provided

by the organization in return for the contribution”

– OR good faith estimate of value of goods/services provided

47

Donations (Pledge Agreements)

• Large enough donation to require care?

• Donor directing aspects of the gift?• Consider written pledge agreement• Draft with care• Gift must be voluntary• But there may be ways to make

pledge binding and enforceable

48

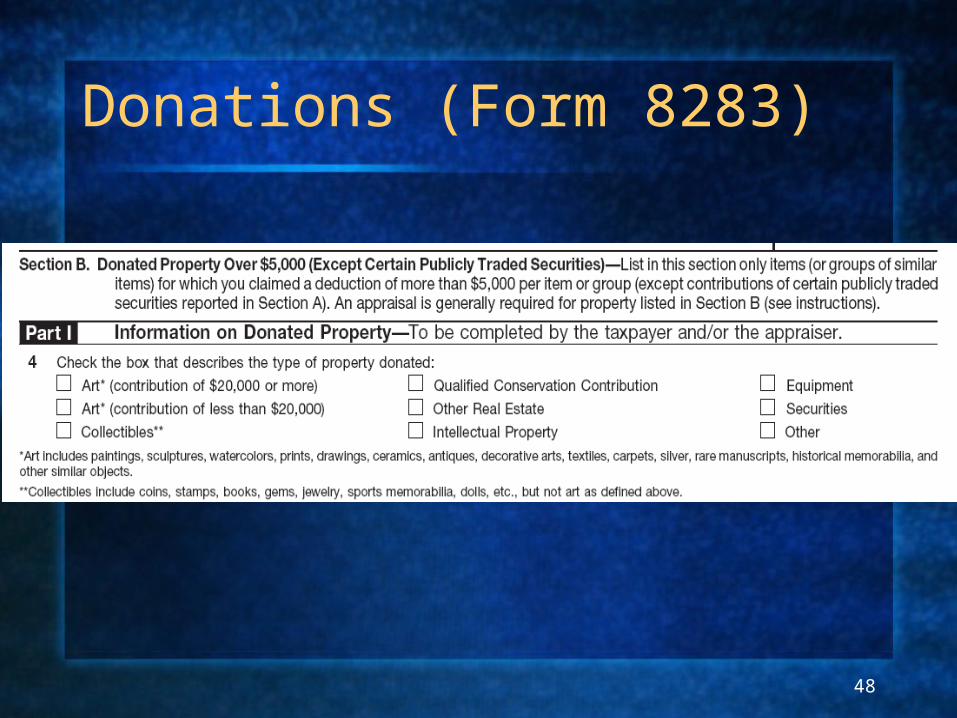

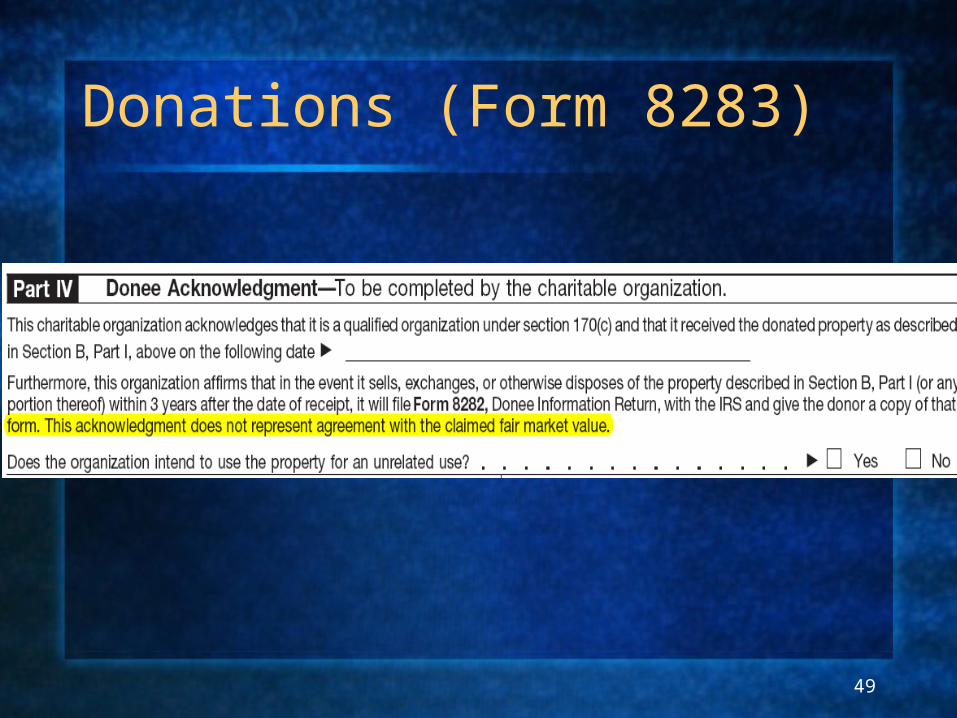

Donations (Form 8283)

49

Donations (Form 8283)

50

Donations (“Public Support Test”)

• Public Support =• (1) “normally,” a (2) “substantial part” of its

(3) “total support” qualifies as “public support.”

• Public Support FractionPublic Support/Total Support =

– % of Public Support• 33 1/3 % for categorical qualification• 10% minimum plus “facts & circumstances”

test

51

Donations (“Public Support Test”)

• Beware:– Small organizations: large multi-year

gifts could destroy public support– Large organizations: large

endowments could destroy public support

– BUT, there is the facts and circumstances test

52

Fiscal Sponsorship

• Nonprofits can support a nonexempt person or organization financially

• Must use an accepted practice . . .– Direct– Independent contractor– Preapproved grant relationship– Supporting organization

53

Employment Issues

• Employment contracts• Job descriptions• Employee handbooks• Biannual employee review

54

Liability Issues

Liability issues Suits relating to you organization's land or

premises Suits relating to the actions or omissions of

your organization, or your directors, or your volunteers

Suits related to contracts (incl. donation promises)

Employment disputes

55

Liability Issues

• Who is protected?– Nonprofit immunity (not fail safe)– Organization indemnification of

directors and other volunteers• In articles?• In bylaws?• By resolution?

56

Liability Issues

• How to reduce exposure:– Risk management policies and

practices– Insurance

57

Quick Wrap-Up Stay familiar with your governing documents Adopt and use simple, understandable conflicts

and compensation policies Be diligent and vigilant on donation activities Consider fiscal sponsorship opportunies Treat employee relationships with care and

memorialize it Be attentive to liability exposure and affirmatively

manage it Present your CPA with Form 990 governance

info

58

Five Action Items for Now

1. Schedule a governance document orientation/discussion meeting

2. Calendar a form 990 review time 3. Check your donation acknowledgment

protocol4. Review your employee relations docs5. Evaluate how your volunteers are

indemnified

NETWORKING BREAK15 minutes

Next up: Plotting a SWOT

60

More Free Workshops!

Increase Your Skills & Knowledge in these upcoming Fundamental Five+ workshops

March 8 Fundraising & Development Strategies

April 12 Grant Strategy & Writing

61

Agenda

8:30 am Welcome & Introductions

8:45 am Legal

9:45 am BREAK & Network & Submit Questions

10:00 am Insurance

11:15 pm BREAK & Network

11:30 pm Nonprofit Hypothetical – Problem Solving

12:15 pm Wrap-Up, Post-Test, Evaluations

12:30 pm Session Ends

62

2011 Fundamental Five+ Non-Profit Capacity Training Series

February 22, 2011

Directors & Officers Insurance and

Cyber Liability InsuranceA General Overview for Non-Profit Organizations

Chuck Pedone, Regional VPDebbie Elliott, Underwriting Manager

A Member of the Tokio Marine Group

Director’s and Officer’s Coverage: What is Covered?

D&O Liability covers the directors and officers for their management decisions on behalf of the organization. Without this coverage, the Directors’ and Officers’ personal assets are at risk.

Even Non-Profits NEED D&O!

Nonprofits By the Numbers

- There are 1.3 million charities, private foundations and religious congregations in U.S.

- The number of charitable organizations has doubled since 1974.

- NP sector includes 11.7 million paid employees (9% of U.S. workforce) work in the nonprofit sector.

Non-Profit figures (cont.)

• Job growth in Nonprofit Sector (2.5%) outpaces growth in business (1.8%) and government (1.6%) Sectors.

• Diverse Group – Includes Healthcare, Education, Social Services, Foundations, etc.

• About 50% of all adults volunteer each year.

• 9 out of 10 households make charitable contributions.

• $207 billion in individual donations annually.

• $41 billion in corporate contributions are made annually.

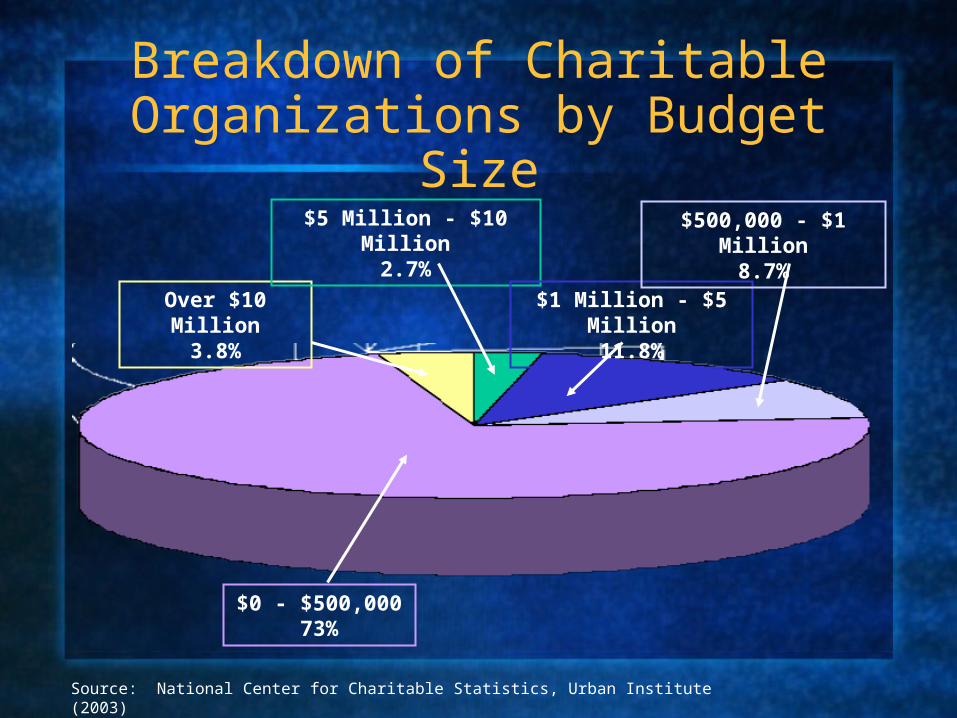

Breakdown of Charitable Organizations by Budget Size

$0 - $500,00073%

Over $10 Million3.8%

$5 Million - $10 Million2.7%

$1 Million - $5 Million11.8%

$500,000 - $1 Million8.7%

Source: National Center for Charitable Statistics, Urban Institute (2003)

What is covered?

• Types of Allegations / Causes of Damages• Breach of Duties

– Duty of Care– Duty of Loyalty– Duty of Obedience

• Mismanagement -Business Judgment Rule• Error & Omission (broad)• Improper Disclosure or Failure to Disclose

Who is covered?

• Directors & Officers, Governor, Trustee• Employee, Volunteer• Spouses (vicariously)• Estates/Heirs• Entity (including majority owned subs)• Management Committee Member or member of the

Board of Managers (LLC)• Others – specifically named

Potential Claimants

• Insiders – staff member, employee

• Outsiders – Third parties with a business or other relationship with the nonprofit

• The Entity itself – Derivative suits brought by its members

• Directors – Board members suing each other

• Beneficiaries (service recipients) – Those whom the nonprofit is in business to help alleging wrongdoing or injury from the NP’s actions OR failure to act

• Members – allegations of harming the interests of the member

• Special Relationships – Includes groups such as students, patients, etc.

• Government Officials – State Attorneys General, IRS, Federal regulators

EPLI

Employment Practices Liability: -> 17 defined acts including retaliation and mental anguish or emotional distress

The BIG THREE: WRONGFUL TERMINATION SEXUAL HARRASMENT DISCRIMINATION 3rd party: “current customer, supplier, vendor, business invitee or other client of the

Private Company” alleges discrimination or harassment

CLAIM EXAMPLES: A shareholder and former employee of a private company sued the Company and its

CEO alleging that after he opposed the Company’s purchase of the assets of another corporation the CEO partially owned, he was terminated. Wrongful termination/retaliation of a hostile work environment claim

An age discrimination lawsuit was brought by a 62 year old sales representative who was employed by the Insured. He was terminated by the Insured for not meeting his sales quotas. His job was then given to a younger employee with less experience. There existed no documentation of poor performance or disciplinary actions. Paid out $350,000.

Fiduciary, Workplace Violence, Internet Liability

• Fiduciary Liability - Provides coverage for negligent acts, errors or omissions in the administration of a benefit plan and/or acting in a fiduciary capacity for a company plan subject to laws of ERISA. This includes: - Giving counsel to employees- Providing interpretations and handling records- Effecting enrollment, termination or cancellation of employees or participants under any benefit plan

• Workplace Violence – Provides coverage in the event of a Workplace Violence Act- Workplace Violence Act include actual or alleged intentional and unlawful use of or threat to use deadly force with the intent to cause harm- Damages include business interruption expense and public image restoration expense

• Internet Liability - Coverage for the publishing exposure that a non-profit has as a result of having a website- Libel, Slander, defamatory or disparaging material- Infringement of copyright, service mark, trademark, trade name, title or slogan- Improper use of literary or artistic titles, formats or performances

Claim examples

• Discrimination (race, sex, age, membership, etc.)

• Civil Rights and other Statutory violations (ADA, FMLA, ERISA, EPA)

• Wrongful Termination of employees and improper hiring practices

• Inefficient administration or supervision

• Waste of corporate assets

• Misleading reports or representations

• Libel and Slander (publishers, bloggers, newsletters, web pages)

• Failure to deliver services

• Acts beyond granted authority

• Breach of fiduciary duty (duties of care, loyalty and obedience)

• Antitrust Claims (accreditation, restriction of trade)

Cyber Liability Emerging Risk

• Information and Intellectual Property are an organization’s most valuable asset today

• No longer a “Bricks & Mortar” world

• Impact of a data breach on an organization is huge– Financial– Business Distraction – Loss of Customers– Damage to Reputation

Filling the Gaps

The Cyber Risks to which an enterprise is exposed fall into two general categories and insurance coverage is available for both:1) Those losses suffered by an enterprise (1st Party Losses)2) An enterprise's liability to third parties (3rd Party Losses)

Standard Property, Liability or Crime policies will not traditionally cover damage to or loss of intangible assets (data and systems) so there exists a significant gap in coverage, both in terms of exposure and because of the ever greater dependency on technology to be able to do business.

PHLY’s Cyber Security Liability policy works to fill these gaps.

Perils

Fraud

Virus Transmission

Natural Disaster

Employee Sabotage

SystemMalfunction

Power failure

Human Error

Hacker Attack

Computer Network

The Need• 46 States and many foreign jurisdictions including the European

Union have enacted privacy breach laws to protect consumers

• HIPAA requires that Personal Health Information (PHI) be safeguarded with specific fines per patient

• California requires that companies must notify their CA customers whenever there is a security breach of their Personally Identifiable Information (PII) – note the law applies based on residency of the customer, not the company responsible for the breach

• Emerging laws – Massachusetts, FTC Red Flag Rules, others

Who is Exposed to Privacy Risk

• Any organization holding:• Sensitive customer/patient information• Sensitive employee information• Confidential third party information

• Industries• Financial Institutions• Healthcare Organizations• Retail

• Service Providers • Outsourcing, Call Centers, Payroll, etc.

PCI Credit Card Standards

A worldwide information security standard developed by the Payment Card Industry Security Standards Council (PCI SSC)

Created to help organizations who process card payments to prevent credit card fraud through increased controls around data and its exposure to compromise

The standard applies to all organizations which hold, process, or pass cardholder information from any card branded with the logo of one of the card brands

HIPAA Privacy Standards

Health Insurance Portability and Accountability Act of 1996 (HIPAA), Public Law 104-191, was enacted on August 21, 1996

Protects all "individually identifiable health information" held or transmitted by a covered entity or its business associate, in any form or media, whether electronic, paper, or oral. The Privacy Rule calls this information "protected health information (PHI)."

HIPAA governs Healthcare Providers, Health Plan Providers, and Healthcare Clearinghouses

HIPAA Privacy Standards cont’d

Prior to 02/18/2009

On or after 02/18/2009

Penalty Amount

Up to $100 per violation

$100 to $5,000 per violation

Calendar Year Cap

$25,000 $1,500,000

Penalties for Noncompliance Violations

Data Breach – Costs are Significant

• Regulatory issues – notice requirements, fines/penalties, injunctive relief

• 70% of a Company’s assets are tied to information resources

• Harm to reputation

• Hard dollar remediation costs, including liability issues

• Costs to re-secure the data

• Hackers, Cyber terrorists, Malware, Spear Phishers, Industrial Spies

• Improper Disposal, In-house Incompetence and

Negligence

• 87% of breaches are avoidable with proper

controls/methods

Questions/ Suggestions ???

Contact your Insurance Agent

Contact Philadelphia Insurance Companies

Chuck Pedone, [email protected]

Debbie Elliott, [email protected]

83

Test Your Knowledge

Our funder (and we!) want to know how effective this workshop was for you.

This 5-minute Post-Workshop Quiz helps us gauge your progress and our success.

Mahalo.

84

Help Us Serve You Better!

Please take 5 more minutes to complete the Workshop Evaluation so that we can

improve this and future offerings

Mahalo.

85

Mahalo

For More Information or to Register for an Upcoming Workshop

Leslie Mullens (808) [email protected]

Fundamental Five+Nonprofit Capacity Training

Series