1 it industry performance: mid-year review 2002-03 press conference new delhi: january 10, 2003

TRANSCRIPT

1

IT Industry Performance: IT Industry Performance: Mid-Year Review 2002-03Mid-Year Review 2002-03

Press ConferenceNew Delhi: January 10, 2003

Eleventh in the Itops series of end-user surveys on IT hardware

since 1996-97

With this : Six year time series database

Annual trend for 6 consecutive years

Half-yearly trend for 9 consecutive periods

IItopstops 2002 pro28 2002 pro28

3

Uniform methodology since 96-97 to facilitate comparison

Nearly 14,000 face-to-face interviews conducted in this round

Study represents ‘All India Urban Market’

Sample allocation and universe projections extremely reliable

and robust

IItopstops 2002 pro 2002 pro CoverageCoverage

4

IItopstops 2002 pro 2002 pro Target groupTarget group

Establishment having at least one telephone line. 8000+ establishments covered Establishments classified as per ACE (Principal activity

performed at the establishment classified by number of employee) grid for representative sampling

Activities: • Manufacturing/ factory/ Warehouse• Office• Outlets• Government

Number of employees:• Less than 10 employees (Small establishments)• 10-50 (Medium establishments)• 50 + (Large establishments)

Most robust way to project establishment information to the universe

5

IItopstops 2002 pro 2002 pro Target groupTarget group

Household – SEC A/ B (refer shaded portion in the grid below Up market 6000+ households covered

ILLITE-RATE

SCHOOL SCHOOL SSC/ HSC SOME COLLEGE BUT NOT

GRAD

GRAD/ POST GRAD

GRAD/ POST GRAD

UPTO 4 YRS

5-9 YRS (GEN) (PROF)

UNSKILLED WORKER 8 8 7 6 6 6 6SKILLED WORKER 8 7 6 5 5 4 4PETTY TRADERS 8 6 6 5 5 4 4SHOP OWNERS 6 6 5 4 3 2 2BUSINESSMEN/ INDUSTRIALISTS EMPLOYING

0 EMPLOYEES 6 5 4 3 2 2 11- 10 EMPLOYEES 5 4 4 3 2 2 1

MORE THAN 10 EMPLOYEES 3 3 2 2 1 1 1SELF-EMPLOYEDPROFESSIONALSCLERICAL/SALESMEN 6 6 6 5 4 3 3SUPERVISOR LEVEL 6 6 5 5 4 3 2OFFICERS/ EXECUTIVES

- JUNIOR 5 5 5 4 3 2 2- MIDDLE/SENIOR 3 3 3 3 2 1 1

6 6 16 4 3 2

6

Data collected after ‘last mile’ - From location of installation No undercounting/over counting of goods in transit as in shipment data Includes direct imports by customers Validation of the estimates based on Vendor data

Accurate assessment of ‘who’ bought and ‘where’ used Not dependent on ‘perceptions’ of reseller/channel member/vendor

Emerging segments clearly identified as they ‘emerge’ Acceptance of technology products depends on customers

preparedness to accept them and innovative marketing by Vendors. Thus need to monitor customer end-user perspective and obtain cues

for innovative marketing ITOPS meets this need by providing “Proactive” Market tracking rather

than ‘reactive’ Estimates most reliable and accurate as no vested interest to distort

figures Inputs from demand and supply side considered for final estimates No vendor controversy

What is unique about the What is unique about the IItopstops study design?study design?

66½½ year time series database-how does it help? year time series database-how does it help?

Validating figures through past trends Forecasting accuracy

Identifying emerging trends

PC Sales projections vs. achieved AccuracyH2 99-00 99%Annual 99-00 97%H1 00-01 98%Annual 00-01 108%H2 01-00 102%Annual 01-02 101%

8

IItopstops: Comprehensive coverage: Comprehensive coverage

Product coverage:

Computers - Desktop PC, notebooks, servers

Printers - DMP, IJP, LJP

Peripherals - Monitors, keyboard, scanner,

zip drive, CD writer, Print server

UPS - UPS, battery

Networking - Incidence, size of networking (no. of nodes)

Networking prod - NIC, hubs

Internet - Active internet subscribers, modems

9

And the findings are …And the findings are …

10

PC Shipments: Half-yearly ComparisonPC Shipments: Half-yearly Comparison

834,650

1,046,995

803,055867,820

950,855

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

April-Sept00

Oct.00-Mar01

April-Sept.01

Oct.01-Mar02

April-Sept.02

• 18% growth over H1/2001-02

• 10% growth in sales over H2/2001-02

Uni

ts

11

PC Shipments: 1997-2003PC Shipments: 1997-2003

799,058

1,027,190

1,405,290

1,881,640

1,670,880

2,010,000

0

400,000

800,000

1,200,000

1,600,000

2,000,000

2,400,000

1997-98 1998-99 1999-00 2000-01 2001-02 2002-03*

• Expected Annual Growth over 2001-02: 20%

Uni

ts

*Estimated

12

PC Shipments Half-yearly Trend:PC Shipments Half-yearly Trend: Businesses Vs. Households Businesses Vs. Households

628,565 671,654777,995

196,167172,860

827,950

219,040

174,490

0

400000

800000

1200000

Oct.00-Mar.01

April-Sept.01 Oct.01-Mar02 April-Sept.02

Businesses Households

• Business Sector accounted for major proportion - 82% of the market

• Consumption in Businesses increased by 24% and households declined by 1% over H1/2001-02

• Consumption in Businesses improved by 16% and in households decreased by 11% over H2/2001-02

Uni

ts

13

Half-yearly PC Shipments : EnterprisesHalf-yearly PC Shipments : Enterprises

20 25 20 26

2727

2327

53 4857

47

0%

20%

40%

60%

80%

100%

Oct.00-March01

April-Sept.01 Oct.01-March02

April-Sept.02

Small Medium Large

• Larger Businesses continued to contribute maximum sales: 47% but proportion dropped from 48% in H1/2001-02 and from 57% in H2/2001-02

• Sales to Small enterprises registered the maximum growth; 29% over H1/2001-02 and 51% over H2/2001-02

• Sales to Larger Businesses improved by 21% while in Medium it improved by 24% over H1/2001-02

% U

nits

14

PC Shipments by Configuration PC Shipments by Configuration

• P-4 dominated the market with 51% market share followed by P III with 36%

• AMD/Cyrix etc. making their presence felt; Market share: 10%

Oct 01-Mar 02

Apr 02- Sep 02

Total PCs bought 803,057 867,821 950,885

Pentium 4 1.5 – 2 GHz

Pentium 4 upto 1.5 Ghz 30%

Pentium III 550 MHz and above 47% 45% 24%

Pentium III upto 450/ 500 MHz 7% 11% 12%

Pentium II 300/350 MHz and above 5% 4% 2%

2% 1% 1%

Pentium /Pentium Pro - -

Cyrix / AMD/Others/ not specified 21% 11% 10%

Apr 01-Sep 01

Configuration:

Pentium II 200/233/266 MHz /MMX

10%

10% -

-

28%

21%

15

20%

36%

44%

Indian Brands MNC brands

Assembled

H1/2001-02

• Assembled PC market share increased to 48% from 44%

• Share of MNC Brands decreased from 36% to 30%

22%

30%

48%

Indian Brands MNC brands

Assembled

H1/2002-03

The PC Market: Indian, MNC & Assembled The PC Market: Indian, MNC & Assembled

16

Half-Yearly: Share of Indian, MNC & Assembled Half-Yearly: Share of Indian, MNC & Assembled

• Share of Indian Brands increased to 22% in H1/2002-03 from 18% in H2/2001-02

• MNC brands shared dipped 4% but remains significant over H2/2001-02

• Assembled PC market share remained constant, but sales grew by 11%

17 23 20 22

2429 36 30

5948 44 48

1819

3423

4858

0

20

40

60

80

100

Oct 99-Mar 00

Apr 00-Sep 00

Oct 00-Mar 01

Apr 01-Sep 01

Oct 01-Mar02

Apr 02-Sep 02

Indian MNC Assembled

Mar

ket

sha

re

(%)

17

PC Shipments: The City-spreadPC Shipments: The City-spread

61%53% 59% 53%

20%

13%16%

11%

19%35%

25%36%

0%

20%

40%

60%

80%

100%

Oct.00-Mar.01 April-Sept.01 Oct.01-Mar.02 April-Sept.02

Top 4 Next 4 Others

• Market concentrated in Top 4 cities but proportion dropped significantly over H2/2001-02, however sales dropped by only 1%

• Proportion of ‘Next Four’ fell sharply to 11% from 16% (H2/2001-02) with sales dropping 27%

• Robust consumption growth in smaller towns: 30% over H1/2001-02 and 56% over H2/2001-02

18

Enterprises PC Market: The City-spreadEnterprises PC Market: The City-spread

75%59% 61%

53%

18%

8% 12%9%

6%

33% 27%38%

0%

20%

40%

60%

80%

100%

Oct.00-Mar.01 April-Sept.01 Oct.01-Mar.02 April-Sept.02

Top 4 Next 4 Others

• Overall Establishment/Business market grew by 24% over H1/2001-02; and 16% over H2/2001-02

• Market concentrated in Top 4 cities; while proportion dropped over H2/2001-02, the consumption remained constant

• Proportion of ‘Next Four’ cities fell sharply from 12% in H2/2001-02 to 9%

• Proportion of Smaller towns increased significantly to 38% marking a 63% increase in consumption over H2/2001-02

19

Profile of PC buyers: First time Vs. Repeat Profile of PC buyers: First time Vs. Repeat

68% 61% 71% 67%

32% 39% 29% 33%

0%

20%

40%

60%

80%

100%

Oct.00-Mar.01

April-Sept.01

Oct.01-Mar.02

April-Sept.02

First Time buyer Repeat buyer

• First time buyers accounted for 51% of PC sales

• In the business segment, repeat buyers accounted for 59% of sales while in

households first time buyer accounted for 88% of sales

% B

uyer

s

20

Profile of Household PC buyers:Profile of Household PC buyers:Socio Economic ClassificationSocio Economic Classification

71% 62% 57% 48%

39%

28% 38%44%

10% 5% 8%

0%

20%

40%

60%

80%

100%

Oct.00-Mar.01

April-Sept.01

Oct.01-Mar.02

April-Sept.02

SEC C

SEC B

SEC A

% buyers

• Sales to SEC A declined by 23% over H1/2001-02 and by 26% over H2/2001-02

• Sales to SEC B increased by 56% over H1/2001-02 and by over 2% H2/2001-02

• Gradual penetration into SEC C: accounted for 8% of the total households

21

Half-yearly Note book ShipmentsHalf-yearly Note book Shipments

Uni

ts

• Growth declined by 5% over H1/2001-02 and by 14% over H2/2001-02

• Top 4 cities accounted for 70% of sales

• Share of smaller towns increased to 23% from 9% in H1/2001-2 and 8% in H2/2001-02 growing 139% and 137% respectively.

33,660

21,17023,570

20,199

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Oct. 00-Mar.01 April-Sept.00 Oct. 01-Mar.02 April-Sept.02

22

Notebooks Enterprise Market: Half yearlyNotebooks Enterprise Market: Half yearly

18%27% 25% 26%

26%26% 33% 23%

56%47% 41% 51%

0%

20%

40%

60%

80%

100%

Oct00-Mar.01

April-Sept.01

Oct.01-Mar.02

April-Sept.02

Large

Medium

Small

% U

nits

• Notebook sales remained concentrated in Large businesses; sales grew by 5% over H1/2001-02 and by 8% over H2/2001-02

• Consumption in small and medium enterprises recorded negative growth: (-)10% in small and (-)15% in medium over H1/2001-02

23

Half-yearly Market: ServersHalf-yearly Market: Servers

35,470

27,00723,874

28,046

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Oct.00-Mar.01 April-Sept.01 Oct.01-Mar.02 April-Sept.01

• Server sales grew by 4% over H1/2001-02 and by 17% over H2/2001-02

• Top 4 cities accounted for 89% of sales growing 64% over H2/2001-02

• Sales to smaller and medium businesses grew by 87% and 53% over H1/2001-02 respectively; however consumption in larger businesses dropped by 44%

• Small enterprises accounted for 35% of the sales while medium and large accounted for 34% and 31% respectively.

Uni

ts

24

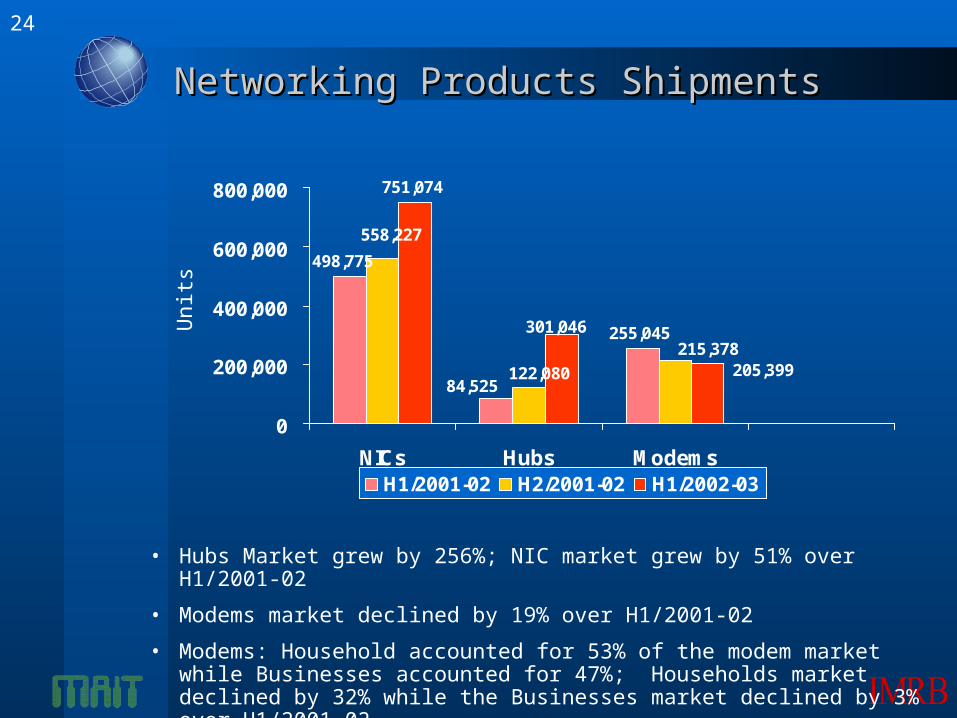

Networking Products ShipmentsNetworking Products Shipments

751,074

498,775

84,525

255,045

558,227

215,378

122,080 205,399

301,046

0

200,000

400,000

600,000

800,000

NICs Hubs Modems

H1/2001-02 H2/2001-02 H1/2002-03

• Hubs Market grew by 256%; NIC market grew by 51% over H1/2001-02

• Modems market declined by 19% over H1/2001-02

• Modems: Household accounted for 53% of the modem market while Businesses accounted for 47%; Households market declined by 32% while the Businesses market declined by 3% over H1/2001-02

Uni

ts

25

Printers - DMP Vs. Inkjet Vs. Laser Printers - DMP Vs. Inkjet Vs. Laser

163,300 157,206189,202

144,330

34,651

42,927

272,883

207,112

221,620

192,601

26,33038,020

0

100,000

200,000

300,000

400,000

500,000

Oct.00-Mar.01

April-Sept.01

Oct.01-Mar.02

April-Sept.02

Inkjet printer

Laser printer

Dot MatrixPrinter

• Total Printer sales declined by 3% over H1/2001-02 and by 15% over H2/2001-02

• Sales of Dot-Matrix declined by 8%; and Inkjet by 7% over H1/2001-02; Sales of Laser printers grew by 63%

• Sales of Inkjet printers grew 33% in the Business Segment but declined 42% in the Households sector as compared to H1/2001-02; while that of Dot-Matrix in Business segment declined by 4% and by 36% in Households

Uni

ts474,206

390,650

445,473

379,858

26

Printers - Where are we headed ?Printers - Where are we headed ?

46% 47% 39%51%

38%

9%

11%

43% 42%52%

40%51%

11% 11%9%

0%

20%

40%

60%

80%

100%

1998-99 1999-2000

2000-01 2001-02 2002-03

Inkjet Printer

Laser Printer

Dot MatrixPrinter

• 2002-03: Overall Printers sales expected to remain flat

* Estimated

477,305%

Uni

ts844,000590,335 827,820

*

836,122

27

UPS Shipments: Half-yearly trendUPS Shipments: Half-yearly trend

• Sales grew by 26% over H1/2001-02

• Businesses accounted for 66% and Households for the rest 34% of Market

• Top 4 cities accounted for 56% with consumption growing 65% over H1/2001-02

• Overall consumption in the Business segment grew by 132%; while in Large Businesses it grew by 276%

• Consumption in Households declined by 34%

Uni

ts202,208

176,098

199,359221,227

0

50,000

100,000

150,000

200,000

250,000

Oct.00-Mar.01 April-Sept.01 Oct.01-Mar.02 April-Sept.02

28

Other peripherals SalesOther peripherals Sales

837,431 834,031

870,450869,073

977145975310

600,000

800,000

1,000,000

Keyboards Monitors

April - Sept.01 Oct.01-Mar.02 April - Sept.02U

nits

• Keyboards and Monitors have grown by 16% and 17% respectively over H1/2001-02

29

58%31%

10%0%

1%

14" 15" 17" 20" 21"

Monitor Market by Size Monitor Market by Size

• 14” & 15” continued to dominate the market

• Market share of 17” increased marginally, but sales grew by 32%

Units: 834,031

April -Sept.2001

46%

41%

11%

2%

0%

14" 15" 17" 20" 21"

Units: 977,154

April -Sept.2002

30

Active Internet entities: 1998 - 2002Active Internet entities: 1998 - 2002

92%83%

64%51% 45% 48%

8%17%

36%49% 55% 52%

0%

25%

50%

75%

100%

1997 1998 1999 2000 2001 2002

Home

Business

March 98 March 99 March2000 March 2001 March 2002 Sept.

2002

150,000 350,000 651,000 1,127,125 1,29,3806 1,306,356

CAGR:

- Business: 93%

- Home: 220%

• CAGR: 120%

(Definition: Entities are establishments/individual with internet connection; an entity may house/be multiple user/s)

31

74%

10%

1%

8%

1% 6%

Dial-up ISDN

Leased Line DSL

Cable VSAT

Mode of Internet Access in BusinessesMode of Internet Access in Businesses

72%

10%

1%

6%

3% 9%

Dial-up ISDN

Leased Line DSL

Cable VSAT

March 2002 September 2002

32

Internet owning House-holds by location and by SECInternet owning House-holds by location and by SEC

Town Class March 2001 Sept. 2001 March 2002 Sept.

2002

Top 4 72% 68% 63% 68%

Next 4 18% 23% 25% 19%

Other 8 10% 9% 12% 14%

SEC March 2001 Sept. 2001 March 2002 Sept.

2002

SEC A 73% 79% 71% 77%

SEC B 17% 21% 29% 23%

• Break up by Town-Class:

• Break up by Socio-Economic Profile:

33

Internet Penetration September 2002Internet Penetration September 2002

Business Segment Home

Overall 40% 11%

Top 4 Metros 42% 13%

Next 4 Metros 41% 9%

Other 8 Metros 29% 9%

SEC A - 20%

SEC B - 4%

• Internet Penetration by Town class and Socio-Economic Classification

• Break-up of Internet Connection in Business Entities:

Indian Pvt. 91%

MNC 2%

Govt./PSU 7%

SummarySummary

Product Units Value (Rs. Crs.)

H1/02-03 H1/01-02 % H1/02-03 H1/01-02 %ComputersDesktops 950,855 803,055 18 2,355 2,210 7Notebooks 20,199 21,170 -5 145 169 -14Servers 28,046 27,005 4 404 432 -7PrintersDot-matrix 144,330 157,205 -8 124 147 -16 Laserjet 42,927 26,330 63 108 74 46Inkjet 192,601 207,112 -7 80 83 - 4Line 1,754 1,840 -5 24 28 -14OthersKeyboards 975,310 837,430 16 ** ** **Monitors 977,145 834,030 17 597 490 22UPS 221,227 176,100 26 ** ** **NetworkingNIC 751,074 498,775 51 - - -Hub 301046 84,525 256 - - -Modem 178,271 255,045 -30 - - - Internet 1,306,356* 1,293,806** 10%* September 2002; ** March 2002

35

Forecast for second-half of 2002-03Forecast for second-half of 2002-03

Product Total Market Market forecast for Forecast for 2002-03 Oct. 02-March.03

PCs 2,010,000 1,060,000

Dot-matrix 325,000 180,000Inkjet 432,000 240,000Laserjet 87,000 45,000

UPS 480,000 260,000

36

Thank you!Thank you!