1 international compliance october 21, 2014 washington, dc william j. yonge morgan, lewis &...

TRANSCRIPT

1

INTERNATIONAL COMPLIANCE

October 21, 2014Washington, DC

WILLIAM J. YONGE

Morgan, Lewis & Bockius Condor House, 5-10 St. Paul's Churchyard | London EC4M 8AL United KingdomDirect: +44.20.3201.5646 | [email protected]

MARTHA MATTHEWS

Hudson Advisors LLC

Direct 214.515.6831 | [email protected]

80815238.2

2

Topics• ANTI-CORRUPTION

– The U.S. Foreign Corrupt Practices Act (“FCPA”)– The UK Bribery Act (“Bribery Act”)– Anti-Corruption Compliance Best Practice

• REGULATORY FRAMEWORK– UK Financial Services Regulatory Architecture– UK Authorised Businesses and Approved Individuals

• EU DIRECTIVE – AIFMD– EU AIFMD – Impact on U.S. AIFMs Marketing AIFs in the EU– Some other European Developments

80815238.2

3

THE FOREIGN CORRUPT PRACTICES ACT OF 1977(FCPA)

4

Where is bribery a problem?

Transparencyinternational.org/corruptionindexmap

5

Anti-Corruption Trends

Harmonization of global anti-corruption standards and common investigative practices

Information sharing and cross-debarment (particularly in banking)

Increased Global Enforcement Trends

Increased Cooperation Between Countries

Increased Enforcement – the U.S. is the most active regulator

6

RISKS• Key Risk Categories:

– Country Risk– Sector Risk– Transactional Risk– Business Opportunity Risk– Business Partnership Risk

• High Risk Considerations:– Gifts and hospitality– Use of Company Assets– Charitable and Political donations– Sponsorships

7

What is the FCPA?

The Foreign Corrupt Practices Act of 1977 as amended, makes it unlawful for certain persons and entities to make payments to influence foreign government officials for the purposes of obtaining, retaining or directing business to any person.

The FCPA applies to all U.S. persons and certain foreign issuers of securities.

In 1998 the FCPA was amended to apply to foreign firms and persons who cause, directly or through agents, an act in furtherance of such a corrupt payment to take place within the U.S. territories.

Applies to public and private companies.

8

Critical Elements of the FCPA

Key elements:

• Anti-bribery prohibitions prohibiting the giving or offering money, gifts or anything of value to a foreign government official to obtain or retain business. Enforced by the Securities and Exchange Commission (civil) and Department of Justice (criminal). The SEC has a specialized unit for enforcement of the FCPA.

• The FCPA also requires companies whose securities are listed in the U.S. to meet its accounting provisions requiring covered corporations to maintain adequate internal accounting controls and to keep accurate books and records reflecting transactions of the corporation. These controls seek to prevent accounting practices designed to hide corrupt payments.

9

How can I or my company be held liable under the FCPA?

• Extraterritorial reach• The following are subject to the FCPA:

– US individuals, wherever located– US companies– Foreign subsidiaries of US companies– Foreign companies registered with the Securities &

Exchange Commission (“SEC”), and the companies’ officers, directors, employees and agents

– Foreign individuals committing any act in furtherance of a violation in the US or aiding and abetting a violation

10

What are the consequences of an FCPA conviction for businesses?

• Anti-Bribery:– Civil penalties: disgorgement of profits and fines

of up to $500,000– Criminal penalties: $2 million fine per violation or

twice the gain/loss, or disgorgement of profits

• Accounting Provisions:– Civil penalties: $10,000 or disgorgement of gross

gain– Criminal penalties: $25 million fine per violation or

twice the gain/loss

11

What are the consequences of an FCPA conviction for individuals?

• Anti-bribery:– Civil penalties: Up to $100,000– Criminal penalties: Up to 5 years imprisonment and $250,000

fine

• Accounting Provisions:– Civil penalties: Up to $10,000 or gross gain– Criminal penalties: 20 years imprisonment and/or $5 million fine

• Employers cannot indemnify employees• Recent Trends:

– Senior management, General Counsel, VPs and CEOs (financial services in the top 3)

12

Collateral Consequences

– Debarment– Civil lawsuits– Expense intense, legal fees– Business disruption, possible loss of

D&O– Negative press, loss of investors– Violation of ethics and other policies,

breach of side letter arrangements

13

What are the elements of an Anti-Bribery violation?

• It is unlawful for– an issuer, domestic concern or anyone acting

within the jurisdiction of the United States– with “corrupt intent”– directly or indirectly– to offer, pay, promise to pay, or authorize

payment– of “anything of value”1

1 Cash; Cash equivalents; Employment; Meals; Gifts; Entertainment; Forgiveness of debt; Discounts; Golf; Travel; Free product

14

What are the elements of an Anti-Bribery violation? (2)

– to a “foreign official”2 for the purpose of obtaining or retaining business or securing any improper business advantage

– workers at state-owned or state controlled businesses considered to be a foreign official

– do not have to be an owner, applies if the government is deemed to exercise control over the state controlled entity

2 Non-US government official or employee; Non-US political candidate; Member of a

public international organization (e.g., United Nations, World Bank); Title is irrelevant;

Includes low-level employees of government agencies and state-owned entities

15

What is “corrupt intent”?

• The element that turns “anything of value” into a bribe

• Intent to induce the recipient to misuse his/her official position

• Conscious avoidance, i.e., knowledge of the high probability of a violation and steps taken to ensure that actual knowledge is not acquired

• Failure to investigate red flags

16

What does “directlyor indirectly” mean?

• No protection from liability for your agents’ violations if red flags existed.

• Agents include: distributors, consultants, attorneys, business partners, joint venture partners, etc.

17

What is considered a “business advantage”?

• To gain or retain a business advantage, e.g.:– To influence a license or permit determination– To influence a public tender– To influence a customs clearance decision– To gain a tax advantage– To influence a sale

• Result is irrelevant• Existence of payment is irrelevant – an offer

alone confers liability

18

What are Red Flags?

For example, Red Flags exist where your agent:

– Performs services in a high-risk country– Demands to be paid in cash– Cannot provide documentation to substantiate

services and expenses– Can “get things done” that others cannot, or in a

way that cannot be explained– Has a close relationship with a government

official with whom you do business

19

What are Risk Flags?

• Third party risk can arise from the use of intermediaries• Lack of transparency in business dealings• Lack of effective democratic institutions• Lack of independent media• A culture that tends to encourage circumvention of rules,

nepotism and similar distortions to an open market• Pressure to conform to cultural norms• The prevalence of requests to make facilitation

payments to expedite processes

20

What are the FCPA Accounting Provisions?

• Require:1. the maintenance of complete accurate books and

records

2. the establishment and maintenance of a system of internal controls sufficient to provide reasonable assurance that:a. Transactions are executed in accordance with

management’s general/specific authorization;

b. Transactions are recorded as necessary to permit preparation of financial statements that conform with generally accepted accounting principles and to maintain accountability for assets;

21

What are the FCPA Accounting Provisions? (2)

c. Access to assets is permitted only in accordance with management’s general/specific authorization; and

d. Recorded accountability for assets is compared with existing assets at reasonable intervals, and appropriate action is taken to address differences.

22

Are there any defenses to the FCPA?

1. Bona fide promotional expenditures

– Payments directly related to product demonstration or promotion

– Must be reasonable

2. Written local law

23

Are there any exceptions to the FCPA?

• Facilitating payments – intended to expedite routine, non-discretionary actions

– Extremely narrow defense

– Facilitating payments are illegal under other laws

24

Facilitation Payments

Australia

The Criminal Code defines a facilitation payment to be a payment which is of nominal value (the term is not defined in the Code); paid to a foreign official for the sole purpose of expediting a routine action; documented as soon as possible.

Canada

Toughened laws in 2013. Similar to the UK, facilitation payments are considered small bribes and are on the same footing as other unlawful payments.

25

Facilitation Payments (2)United States

As defined by the FCPA of 1977 and clarified in amendments, only payments to a foreign official, political party or party official for routine government action such as processing payments, papers, permits, or to expedite performance of non-

discretionary duties performed in a normal course of business.

United Kingdom

The United Kingdom’s Bribery Act 2010 provides in clear terms that it is a crime for any individual or company with a UK

presence to bribe a public official. This includes “facilitation payments” – money or goods given to a public official to perform, or speed up the performance of, an existing duty.

26

RELATED LAWS

• Conspiracy• Racketeering• Mail and Wire Fraud• Travel Act• Money Laundering• Certification and Reporting Violations• Tax Violations

27

THE UK BRIBERY ACT

28

What is the Bribery Act?

UK law became effective in 2011 that criminalizes:

1. Public official bribery

2. Commercial bribery

3. Failing to prevent bribery on your organization’s behalf

29

Why is Bribery Act compliance important?

• Bribery requests are common in many countries• The consequences of Bribery Act violations can

be severe• The Bribery Act has strict liability provisions• Applies to broad array of corrupt conduct• Applies to bribery in and outside of the UK, and

in some cases, to activity with no connection to the UK

30

What are the consequences of a Bribery Act violation?

• Corporate Penalties: Unlimited fines• Individual Penalties: Up to 10 years

imprisonment• Potential confiscation of the proceeds of the

crime• Potential public procurement ban

31

How can I or my company be held liable under the Bribery Act?

• Extremely broad jurisdiction

– UK companies (wherever they do business)– Non-UK companies that “carry on” business in the UK– Liability for “associated persons” (e.g., employees,

agents, subsidiaries), even where the acts occur outside of the UK

– No facilitating payments exception

32

Can my corporation be held liable?

• YES – if it carries on business in the UK, for failing to prevent bribes that are made on its behalf by associated persons, even if the conduct occurs outside of the UK

• Strict Liability Offense• Example:

– Russian company sells widgets in the UK, Russia & Kazakhstan. Company’s attorney in Kazakhstan bribes a Kazakh official to obtain a business license for the Company’s Kazakh operations. Company can be held liable for a Bribery Act violation for failing to prevent the bribery, even if it did not know or approve of it

33

Are there any defenses?

• Yes

• Full defense if the organization can provide it had adequate procedures designed to prevent associated persons from engaging in bribery.

34

ANTI-CORRUPTION COMPLIANCE – BEST PRACTICES

35

What can I do to mitigate FCPA and Bribery Act liability?

• Establish and maintain an effective anti-corruption compliance program

• Compliance programs:– Can prevent bribery– Can detect bribery– Are expected by US and UK authorities– Can provide a defense to violations

36

What are the components of an effective anti-corruption compliance program?

1. Senior management commitment

2. Business model review

3. Due diligence, evaluation and impact assessments

4. Proportionate policies and procedures

5. Communication / Training

6. Monitoring and review

37

What should the policies and procedures do?

• Establish a clear message that the company has a zero tolerance policy for bribery

• Establish guidelines for promotional expenditures and expense reimbursements

• Set forth steps for performing due diligence of and contracting with business partners

38

Cultivate a Culture of Compliance Amongst Employees

• Train all employees

• Special focus on employees with contacts with government officials

• Consider training business partners

39

What is oversight and monitoring?

• Written contracts with all business partners– Contracts with anti-corruption certifications– Contracts with audit rights

• Due diligence:– Do research on your employees and business partners– Understand how your business partners were identified or

recommended– Understand the services to be provided and how the payment

will be made– Conduct a red flags analysis– Know your exposure to, or contacts with, government officials

40

Why do I need financial controls?

• They detect bribery and mitigate bribery risk

• FCPA has Accounting provisions that require issuers to maintain a system of financial controls designed to prevent bribery and the falsification of books and records

• Bribery Act guidance encourages the adoption and maintenance of financial and commercial controls to mitigate bribery risk

41

Do I have to audit all of my business units and all of my business expenditures and

partners?• Consider a risk-based approach

– Periodic audit of expenses involving government officials

– Periodic visits to/meetings with business partners in high risk regions

– Assessment of select high risk transactions

• Document all audits and reviews

42

How do I respond to alleged violations?

• Conduct a prompt and effective internal investigation effectively using internal and external resources

• Remediate

– Ensure the misconduct is stopped

– Address lapses, if any, in controls and implement

improvements

– Consider appropriate disciplinary measures

43

How do I respond to alleged violations? (2)

– Terminate business relationships with relevant agents

– Conduct corrective training

– Consider disclosure to appropriate authorities

– Outside auditors

– Financial statements/regulatory filings

– US or foreign authorities

44

Overview Europe-wide vs US

EU features mainly civil law, codified jurisdictions save for UK common law

National legal codes and processes differ across EU• Italy: it is a defence that a bribe was paid in response to

extortion• Parts of Spain do not prohibit deduction of bribes for

computing tax liabilities• France forbids French companies from giving

information to foreign enforcement agencies

45

Overview Europe-wide vs US (2)• No private sector whistle-blowing protections in Germany,

France, Italy and Spain

• Since 2002 US has pursued twice as many formal bribery actions as rest of world.

1997-2013 – number of formal foreign bribery actions:

US – 316 Denmark – 15

UK – 46 Netherlands – 11

Germany – 20 France – 10

46

Overview Europe-wide vs US (3)

Extractive industries sector has been subject to more foreign and domestic bribery enforcement actions than any other sector followed by manufacturing/service provider; aerospace/defence/security; and health care sectors.

47

US themes

• Prosecutions of and enforcement against individuals a top priority

• DoJ and SEC continue to examine closely travel and entertainment expense claims

• Use of bargaining tools, NPAs, to reward companies/individuals for self-reporting cooperating and remedial actions

48

Recent Cases

• JP Morgan Chase hiring practices - “the sons and daughters case”. Exchange of investment banking business in exchange for hiring government official’s relatives through “fast tracking”. This was a whistleblower case. Parallel investigation SEC/DOJ. Public disclosure required. Spreadsheets include about 30 employees with ties to state-owned companies or party officials. The U.S. authorities now investigating at least 5 other Wall Street banks that have business ties in China.

• Morgan Stanley - exchange of investment management business and acquiring real estate for self and official. Morgan Stanley received declination to prosecute because its compliance policies and monitoring uncovered the actions. The individuals relinquished $3.4 million in real estate, a personal fine of $250K and permanently barred from securities industry (bad actor label).

49

UK themes

DPAs are deals entered into between corporations (not individuals) and prosecutors where prosecution can be avoided by fulfillment of conditions.

The power to use DPAs came into force in UK in 2014.

Conditions will generally include a combination of financial penalty reparation to victims and obligation to implement a compliance program

50

UK themes (2)

FCA reviews have found:

• inadequate systems and controls for assessing bribery/corruption risk re monitoring third-party relationships, such as those with agents or introducers

• anti-bribery training programs often fail to identify and then focus on risks specific to their business

51

UK FINANCIAL SERVICES REGULATORY ARCHITECTURE

52

UK Financial Services Regulatory Architecture

• Predecessor tripartite architecture responsible for financial stability in UK: HM Treasury, Bank of England and FSA

• Abolished in 2013 due to failure in 2007/2008 financial crisis

• FSA ceased to exist

• Three new regulators

53

UK Financial Services Regulatory Architecture (2)

The new regulators• Financial Policy Committee (FPC) – responsible for

macro-prudential regulation

• Prudential Regulation Authority (PRA) – responsible for micro-prudential regulation of systemically important firms

• Financial Conduct Authority (FCA) – to inherit the majority of FSA’s existing roles and functions

54

UK Financial Services Regulatory Architecture (3)

FCA is:• responsible for the conduct of business regulation of all

firms, including those regulated for prudential matters by PRA

• responsible for the prudential regulation of firms not regulated by PRA

• responsible for FSA’s market conduct regulatory functions save for systemically important infrastructure which was transferred to Bank of England

55

UK Financial Services Regulatory Architecture (4)

• The Financial Services Act 2012 contains the core provisions for the government’s structural reforms. The original Bill was published on 27 January 2012 and after Parliamentary scrutiny received Royal Assent on 19 December 2012

• The Act largely amends existing legislation making extensive changes to the Financial Services and Markets Act 2000, as well as to Bank of England Act 1998 and Banking Act 2009

56

Roles of FPC, FCA and PRA in New Regulatory Architecture

Bank of England

Protecting and enhancing the stability of the financial system of the United Kingdom, aiming to work with other relevant bodies including the Treasury, the PRA and the FCA. The Bank’s Special Resolution Unit is responsible for resolving failing banks using the special resolution regime

FPCContributing to the Bank’s objective to protect and enhance

financial stability through identifying and taking action to remove or reduce systemic risks, with a view to protecting and enhancing the resilience of the UK financial system

FPC powers of recommendation and direction to address systemic risk

FCAEnhancing confidence in the UK financial system by facilitating

efficiency and choice in services, securing an appropriate degree of consumer protection, and protecting and enhancing the integrity of

the UK financial system

Conduct regulationPrudential & conduct

regulation

Systemic infrastructure – central counterparties, settlement systems and

payment systems

Prudentially significant firms – deposit takers, insurance, some investment

firms

Investment firms & exchanges, other financial services providers – including

IFAs, investment exchanges, insurance brokers and fund managers

Source: HM Treasury, A New Approach to Financial Regulation: Building a Stronger System (February 2011)

Prudential regulation

PRAEnhancing financial stability by promoting the

safety and soundness of PRA-authorised persons, including minimising the impact of

their failure

Prudential regulation

Subsidiary

57

FCA – Regulated Only Firms

FCA – regulated only firms number about 24,500 covering personal investment firms, insurance intermediaries, mortgage intermediaries, investment managers, non-deposit taking lenders, corporate finance, wholesale firms, custodians, professional firms, markets, collective investment schemes, other brokers, managing agents, most investment firms and others (e.g., travel insurance only and media firms)

58

Dually Regulated Firms

Dually regulated firms number about 2,150 covering banks, building societies, investment banks, credit unions, friendly societies, life insurers, general insurers, wholesale insurers, commercial insurers and reinsurers, Lloyd’s and Lloyd’s Agents and a small number of “significant” investment firms

59

• In UK:• financial services businesses must not only become authorised

by FCA/PRA to conduct regulated activities• they must also not allow individuals to perform controlled

functions on their behalf without the prior approval of FCA/PRA

• Controlled functions cover, for example, director, CEO, non-executive director, compliance officer, chief risk officer, head of division, advising, trading, managing investments

• Approved persons are subject to Statements of Principle for Approved Persons and a Code of Practice for Approved Persons

UK: Authorised Businesses and Approved Individuals

60

UK: Authorised Businesses and Approved Individuals (2)

• The consequences of becoming an approved person are far-reaching. Once a person has become an approved person, they are effectively individually regulated by the FCA or the PRA (or both) and are therefore personally accountable to the regulator in question. This has implications for the standards of conduct approved persons are expected to maintain and the disciplinary action that the regulators can take against them.

• Approved persons are required to satisfy standards of conduct that are appropriate to the role they perform and, in particular, must comply with the Statements of Principle and Codes of Practice issued by the FCA and the PRA

61

UK: Authorised Businesses and Approved Individuals (3)

• Those Statements and Codes provide the main basis for sanctions against approved persons. If approved persons' behaviour fails below the requisite standards of conduct, they may face disciplinary action, which can result in penalties, ranging from a public censure to being banned from the financial services industry

62

FCA

FCA has:

• a single strategic objective to ensure that markets for financial services work well

• three operational objectives

– securing an appropriate degree of protection for consumers

– protecting and enhancing integrity of UK financial system

– promoting effective competition in consumer interest

• a duty to promote effective competition in consumer interest

63

FCA (2)

FCA is responsible for:

• regulating standards of conduct in retail and wholesale markets

• supervising trading infrastructures that support these markets

• prudential supervision of firms that are not PRA-regulated

• UKLA

64

FCA’s New Powers

FCA’s new powers to ban:

• products that pose unacceptable risks to consumers, subject to a consultation process

• such products without consultation for up to 12 months where prompt intervention required

• misleading financial promotions, without resort to enforcement process

65

FCA’s New Powers (2)

FCA’s certain other new powers:

• to announce publicly fact of disciplinary action vs a firm or individual

• to regulate and sanction investment exchanges, sponsors and primary information providers, as FSA currently has regarding investment firms

• took responsibility for consumer credit in 2014

66

FCA’s Supervisory Approach

Four conduct supervision categories based on risks posed to customers and the market:

C1 broadly, banking and insurance groups with a very large number of retail customers and universal/investment banks with very large client assets and trading operations

C2 broadly, firms across all sectors with a substantial number of retail customers and/or large wholesale firms

C3 broadly, firms across all sectors with retail customers and/or a significant wholesale presence

67

FCA’s Supervisory Approach (2)

C4 broadly, smaller firms, including almost all intermediaries

• C1 and C2 firms will have a nominated supervisor

• C3 and C4 firms will not and instead be supervised by a team of sector specialists

Three prudential supervision categories for FCA-only firms:

CP1 (prudentially critical)

CP2 (prudentially significant)

68

FCA’s Supervisory Approach (3)

CP3 (prudentially insignificant)

Under FCA, supervision will be more judgement-based, starting at the firm’s business model and strategy and leading to early intervention on basis of assessment of conduct risk rather than crystallised issues

69

PRA

PRA has two objectives:

• to promote the safety and soundness of all firms it regulates, focusing primarily on the harm firms can cause to stability of UK financial system

• specifically for insurers, to contribute to securing an appropriate degree of protection for those who are, or may become, policy holders

70

PRA (2)

PRA is responsible for:

• authorisation of banks, building societies, insurers and certain designated investment firms, in conjunction with FCA

• prudential supervision of same

PRA’s powers did not change significantly from FSA’s

71

EU AIFMD – IMPACT ON U.S. AIFMSMARKETING AIFS IN THE EU

72

EU AIFMD – Impact on U.S. AIFMsMarketing AIFs in the EU

• AIFMD transposition heatmap• Application of AIFMD to U.S. AIFMs• Key exemptions• Private Placement Overlay• Variable Private Placement Geometry• Key Points:

– Annual Report– Disclosure to Investors– Annex IV Reporting to Regulators

• Private Equity Requirements• Summary of routes to EU investors

73

EU AIFMD – Impact on U.S. AIFMsMarketing AIFs in the EU (2)

• Practical steps for U.S. access to UK investors

• Other impacts of AIFMD on US investment advisers

74

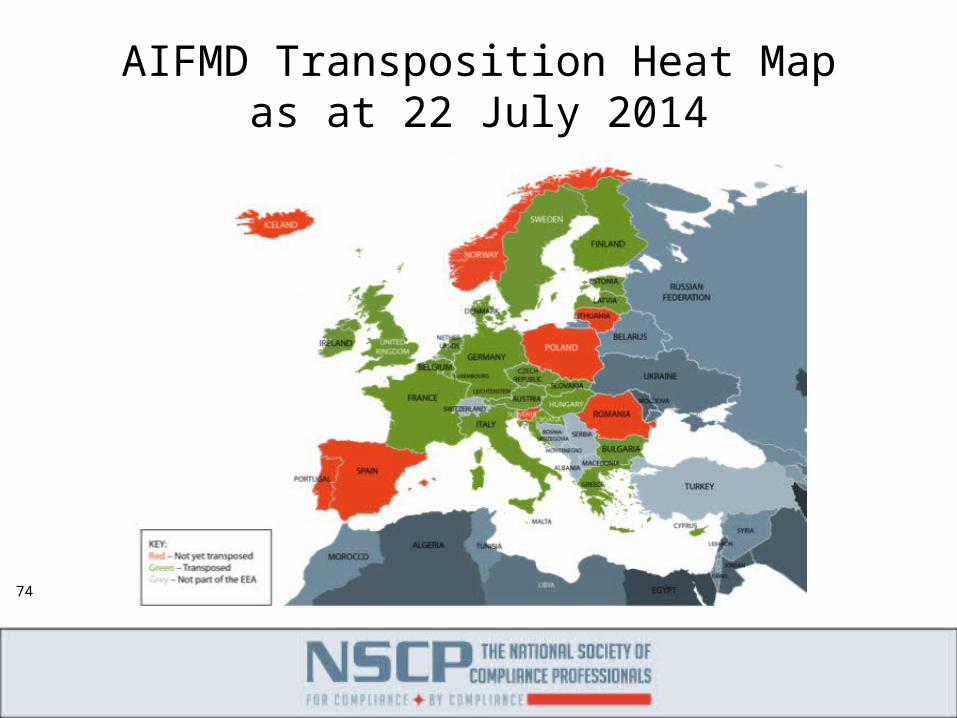

AIFMD Transposition Heat Mapas at 22 July 2014

75

Application of AIFMD to U.S. AIFMs

• U.S. (and other non-EU) AIFMs which market1 AIFs2 to EU3 professional investors4

• U.S. AIFMs5 which manage6 EU AIFs7 (from 2015)

1 “Marketing” means “a direct or indirect offering or placement at the initiative of the AIFM or on behalf of the AIFM of units or shares of an AIF it manages

to or with investors domiciled or with a registered office in the Union”

2 An “AIF” is a collective investment undertaking including investment compartments thereof which raises capital from a number of investors with a view to

investing it in accordance with a defined investment policy for the benefit of those investors and is not a UCITS

3 In this presentation “EU” refers to the 28 member states of the European Union. Iceland, Liechtenstein and Norway are expected to agree to “sign up” to

AIFMD but have not yet done so. The formal name for the EU in combination with those three countries is the European Economic Area. Switzerland does

not participate in the EEA

4 A professional investor is an investor which is considered to be a professional client or may, on request, be treated as a professional client within the

meaning of Annex II to Directive 2004/39/EC (“MiFID”)

5 “AIFMs” means legal persons whose regular business is managing one or more AIFs.

6 “Managing AIFs” means performing at least portfolio management or risk management functions

7 EU AIFs are AIFs which are either (a) authorised or registered in a member state or have their registered office and/or head office in a member state

76

Application of AIFMD to U.S. AIFMs (2)

• U.S. AIFMs may be given a passport to market AIFs to EU professional investors in late 2015. If so, a U.S. AIFM who wishes to use the passport will require to be authorised under AIFMD in its chosen member state of reference and comply fully with AIFMD re EU business

• U.S. AIFMs managing a non-EU AIF and not marketing it in EU are not subject to AIFMD at all

• NPPRs may be abolished in 2018, leaving only the AIFMD passport route to marketing AIFs to EU professional investors for all AIFMs, both EU and U.S.

77

Key Exemptions

• Small AIFMs8 (still subject to local notification and disclosure requirements - member states may impose stricter requirements)

• Reverse solicitation, whereby a professional investor established in EU may invest in AIFs on its own initiative. This has been labelled “reverse solicitation”– When relying on reverse solicitation, non-EU AIFMs should:

• check local law of member state for restrictions on reverse solicitation

• ensure they have appropriate policies and procedures in place to create an audit trail for each investor

8 broadly, AIFMs who manage portfolios of “Small” AIFs whose total assets across all the AIFs that they manage (a) including any acquired through use of

leverage do not exceed EUR100 million or (b) do not exceed EUR500 million where the portfolio is unleveraged and no redemption rights are exercisable

for 5 years from date of initial investment in the AIF

78

Key Exemptions (2)

• Under UK AIFMD Regulations, the marketing restrictions do not apply to an offering or placement of an AIF to an investor made at the initiative of that investor

• UK FCA guidance reads:– “A confirmation from the investor that the offering or

placement of units or shares of the AIF was made at its initiative, should normally be sufficient to demonstrate that this is the case, provided this is obtained before the offer or placement takes place. However, AIFMs should not be able to rely upon such confirmation if this has been obtained to circumvent the requirements of AIFMD.”

79

Private Placement Overlay

U.S. AIFMs may continue to market AIFs in EU under national private placement regimes (“NPPRs”) to at least 2018 provided target member state permits that locally, the AIFMD private placement overlay (“PPO”) is satisfied and any local requirements are met.

The PPO obliges AIFMs to comply with:

• transparency requirements for annual reports, pre-investment and ongoing disclosure to investors and reporting to regulators

• private equity requirements, where they acquire major holdings in EU non-listed companies or “control” of an EU company (whether or not listed)

80

Private Placement Overlay (2)

The PPO also requires:• cooperation agreements for systemic risk oversight between the

regulators of the states in which marketing is to occur, the third country of non-EU AIFM and the third country of non-EU AIF

• neither the third country of the non-EU AIFM nor AIF is listed as “non-cooperative” by Financial Action Task Force (“FATF”)

• agreements exist between each of U.S. CFTC, SEC, OCC and Federal Reserve and almost all EU member state regulators. Bermuda, BVI, Cayman and Channel Islands also covered.

• AIFMD allows member states to impose locally stricter requirements for private placement, additional to those mandated under AIFMD10

10 For example, the appointment of a depositary to a non-EU AIF to be marketed into Denmark or Germany will be required under Danish and German

implementation respectively, subject to the local transitional provision.

81

Private Placement Overlay (3)

Locally, most member states have a notification or registration requirement

• some (e.g., UK) require a simple notification after which marketing can commence immediately

• some (e.g., Denmark and Germany) require a substantive, lengthy registration process

82

Variable Private Placement Geometry

• Marketing in the UK straightforward, subject to FCA notification requirements

• Germany – requirement for a depositary “lite” function to be undertaken in addition to registration with BaFin

• Denmark – similar to Germany

• Austria, Italy, Spain and France – marketing not allowed

• Netherlands, Sweden – marketing generally allowed, subject to notification

83

Annual Report: Key Points

• U.S. AIFMs must produce an annual report for each AIF they market in the EU making it available to the regulator in each target member state and to EU investors on request

• Made available no later than six months from the end of the financial year

• The annual report must not only include typical financial information about the AIF but also:– total amount of remuneration for the financial year, split into fixed and

variable remuneration, paid by the AIFM to its staff and the number of beneficiaries including, where relevant, carried interest paid by the AIF

84

Annual Report: Key Points (2)

– the aggregate amount of remuneration broken down by senior management and members of staff of the AIFM whose actions have a material impact on the risk profile of the AIF (e.g., portfolio managers, traders, sales; and heads of finance, legal, HR, risk and compliance)

– an overview of its remuneration policy– an allocation or breakdown of remuneration information re: each

AIF– The accounting information must be prepared in accordance with

the accounting statements of the country where the AIF is established and be audited. The auditor’s report must be reproduced. The audit must meet international accounting standards in force in the country of the AIF’s registered office

85

Disclosure To Investors: Key Points

Laundry list of itemised pre-sale requirements, including, notably:

• AIF’s valuation procedure and pricing methodology• AIF’s liquidity risk management, including redemption rights in both

normal and exceptional circumstances, and existing redemption arrangements

• how fair treatment of investors is ensured (including, potentially, detailed side letter disclosures)

Review PPMs to ensure all required AIFMD disclosures made; potentially produce an AIFMD wrapper

Note requirements for ongoing post-sale disclosures to investors

86

“Annex IV” Reporting to Regulators: Key Points

Who needs to report? • The AIFM

To whom must reports be made? • Authority in AIFM’s home member state• In case of U.S. AIFM marketing in EU, authority in each member state where fund marketed

Starting when? • Date of marketing notification/registration in relevant member state

Reporting level • Aggregated reporting at AIFM level• Detailed reporting for each AIF managed and each AIF marketed in the EU

Reporting period • Reporting periods ending on the last day of March, June, September and December

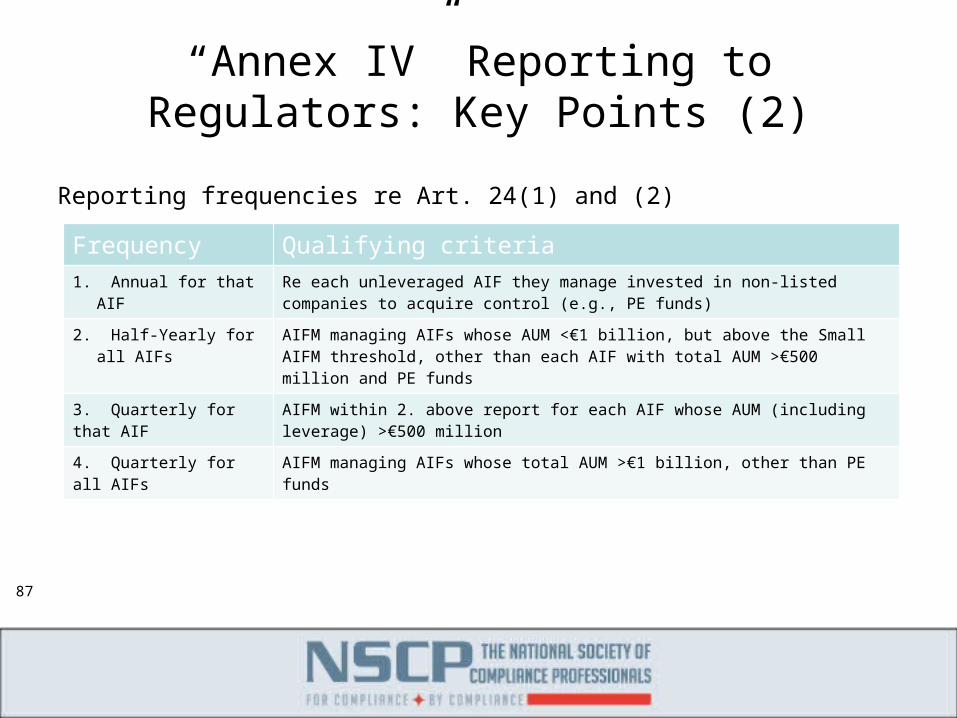

Reporting frequency • Depends on volume of AIFs’ AUM and investment policy (frequencies are quarterly, half yearly and annually)

Reporting deadline • “As soon as possible”, not later than one month after the end of the reporting period• Extended period of 15 days for funds of funds

Form of reporting • Annex IV report to be filed electronically using solely the XML reporting template published by ESMA

• In UK report must be sent electronically to: [email protected]

87

“Annex IV” Reporting to Regulators: Key Points (2)

Frequency Qualifying criteria1. Annual for that AIF Re each unleveraged AIF they manage invested in non-listed companies to acquire

control (e.g., PE funds)

2. Half-Yearly for all AIFs AIFM managing AIFs whose AUM <€1 billion, but above the Small AIFM threshold, other than each AIF with total AUM >€500 million and PE funds

3. Quarterly for that AIF AIFM within 2. above report for each AIF whose AUM (including leverage) >€500 million

4. Quarterly for all AIFs AIFM managing AIFs whose total AUM >€1 billion, other than PE funds

Reporting frequencies re Art. 24(1) and (2)

88

“Annex IV” Reporting to Regulators: Key Points (3)

Art. 24(1) – AIFM specific Art. 24(1) – AIF specific Art. 24(2) – further AIF specific Art. 24(4) - leverage

AIFM shall regularly report to the competent authorities of its home Member State

AIFM shall regularly report to the competent authorities of its home Member State

An AIFM shall, on request, for each AIF it manages and each AIF it markets in the EU report the following to the competent authorities of its home Member State

An AIFM managing AIFs employing leverage on a substantial basis11 shall make available to the competent authorities of its home Member State information about the overall level of leverage employed by each one

• main instruments in which it is trading

• on markets of which it is a member or where it actively trades

• on the investment strategies, principal exposures and most important concentrations of each AIF it manages

• % of the assets subject to special arrangements arising from their illiquid nature

• new arrangements for managing the liquidity of the AIF

• risk profile of the AIF and the risk management systems

• information on the main categories of assets

• re: EU AIFMs only, results of its stress tests on each AIF’s investment and liquidity risks

• break-down between leverage arising from borrowing of cash or securities

• leverage embedded in financial derivatives

• extent to which the AIF’s assets have been reused under leveraging arrangements

11 Under Level 2 Regulation, the tipping point is when the exposure of an AIF calculated according to the commitment method exceeds 3 x its NAV.

NB: for a non-EU AIFM, information at the level of the AIFM should only cover the AIFs marketed in the EU.

89

“Annex IV” Reporting to Regulators: Key Points (4)

• Annex IV Form12 the counterpart to SEC Form PF– only 1/3 identical to Form PF– remainder requires data to be processed differently from, or data not

required by, Form PF– common set of reporting requirements for all AIFs regardless of AIF

type, with some questions for PE only; accordingly, entire form must be completed for all AIFs, irrespective of strategy

– in contrast Form PF imposes different reporting obligations depending on size of firm and type of strategy

– 38 questions at AIFM level of which 27 can be pre-populated– over 300 questions at AIF level

12 Technically, “AIFMD Consolidated Reporting Template” in XML v1.1 and v1.2 comprising one tab at AIFM level and three tabs at AIF level

90

“Annex IV” Reporting to Regulators: Key Points (5)

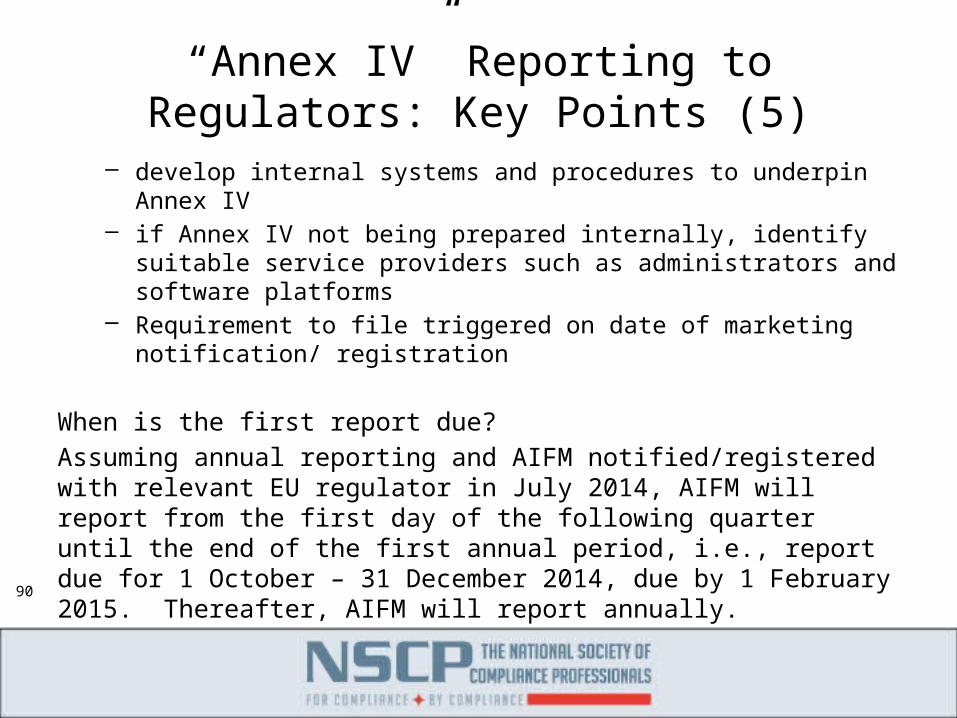

– develop internal systems and procedures to underpin Annex IV– if Annex IV not being prepared internally, identify suitable service

providers such as administrators and software platforms– Requirement to file triggered on date of marketing notification/

registration

When is the first report due?

Assuming annual reporting and AIFM notified/registered with relevant EU regulator in July 2014, AIFM will report from the first day of the following quarter until the end of the first annual period, i.e., report due for 1 October – 31 December 2014, due by 1 February 2015. Thereafter, AIFM will report annually.

91

“Annex IV” reporting to regulators: Key Points (6)

Feeder AIFs• Individual reports for feeder AIFs of same master AIF• No look through to holdings of master AIF

Fund of funds• No look through to the holdings of underlying funds

Non-EU Master AIF not marketed in EU with feeder AIF marketed in EU

92

“Annex IV” reporting to regulators: Key Points (7)

Non-EU Master AIF not marketed in EU with EU feeder AIF• requirement to report Art. 24(2) information on the non-EU

master if the master and feeder share the same AIFM

93

Private equity requirements

Notification of major holdings in EU non-listed companies

• Competent authorities must be notified of the proportion of voting rights in such companies held by the AIF when the proportion reaches or crosses the thresholds of 10%, 20%, 30%, 50% and 75%

Disclosure in case of acquisition of control of EU companies (whether or not listed)

94

Private equity requirements (2)• When an AIF acquires, individually or jointly, control over a

non-listed or a listed EU company, the AIFM managing the AIF must make specified disclosures to that company, its shareholders and to regulators:– control of a non-listed company refers to control of >50% of

its voting rights– control of a listed company varies between EU countries. In

the UK, the threshold is 30% of voting rights– ban on “asset stripping” for 24 months after acquisition of

control of a non-listed or listed EU company

95

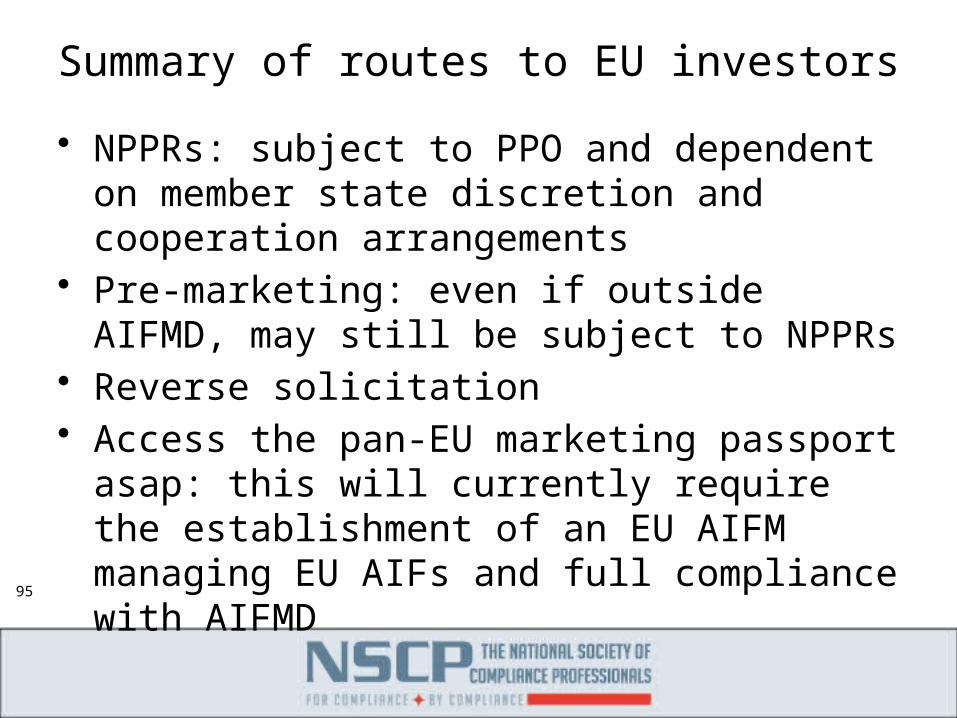

Summary of routes to EU investors

• NPPRs: subject to PPO and dependent on member state discretion and cooperation arrangements

• Pre-marketing: even if outside AIFMD, may still be subject to NPPRs

• Reverse solicitation• Access the pan-EU marketing passport asap:

this will currently require the establishment of an EU AIFM managing EU AIFs and full compliance with AIFMD

96

Practical steps for US access to UK investors

A US AIFM must give written notification to FCA before marketing an AIF it manages

Notification must confirm:• the AIFM is responsible for complying with the UK’s

AIFMD regime• the AIFM complies with the requirements of AIFMD

regarding annual reports, disclosure to investors and reporting to regulators

• if applicable, the AIFM complies with the Private Equity Requirements

97

Practical steps for US access to UK investors (2)

• appropriate cooperation arrangements are in place between relevant regulators

• the country of the non-EU AIFM and any non-EU AIF is not listed as Non-Cooperative by FATF

A US Small AIFM must give written notification to FCA before marketing an AIF it managesNotification must confirm:• the AIFM is responsible for complying with the UK’s

AIFMD regime• the AIFM is a third country Small AIFM

98

Practical steps for US access to UK investors (3)

The US Small AIFM must provide FCA with information on:

• the main instruments in which it trades• the principal exposures and most important concentrations

of the AIFs that it manages

In both cases, simple notification process requiring no waiting time for FCA approval

99

Practical steps for US access to UK investors (4)

FCA may revoke entitlement to market subject to due process

Pre-marketing in UK continues to be regulated by the UK’s pre-AIFMD financial promotion regime

100

Sanctions for contravention of UK regulations

• US AIFMs marketing non-EU AIFs into UK in contravention of the UK AIFMD Regulations could face imprisonment for a term not > 3 months and/or a fine

• Agreements entered into in contravention of the UK AIFMD Regulations may, in certain circumstances, be unenforceable by the US AIFM

101

Other impacts of AIFMD on US investment advisers

US sub-adviser (discretionary) to EU AIFM• an EU AIFM who wishes to delegate to a US sub-adviser

must satisfy the following conditions:– the AIFM must justify the delegation objectively– the delegation must take the form of a written agreement– delegation of portfolio management or risk management

may only be conferred on authorised or registered advisers and where that is not so, the AIFM’s regulator must consent

– where portfolio management or risk management is delegated, there must be a cooperation arrangement between regulator of EU AIFM and regulator of delegate. US SEC and CFTC have entered into such arrangements

102

Other impacts of AIFMD on US investment advisers (2)

– the AIFM must demonstrate delegate has sufficient resources, relevant staff are of sufficiently good repute and experience and is qualified and able to undertake functions

– the AIFM must ensure that delegate undertakes the delegated functions effectively and in compliance with its obligations as an AIFM under AIFMD

– the AIFM must comply with detailed obligations to monitor, instruct and supervise the delegate

• US sub-advisers may be subjected contractually to remuneration requirements

103

Other impacts of AIFMD on US investment advisers (3)

• Under the regime, EU AIFMs may require their sub-adviser to separate functionally remuneration structures between portfolio management, risk management and valuation

• ESMA indicates in guidance that the remuneration regime generally be extended to entities to which EU AIFMs delegate portfolio or risk management

• The above regime will bite from the moment an EU AIFM becomes authorised under AIFMD

104

Other impacts of AIFMD on US investment advisers (4)

US advisers delegating to an EU sub-adviser (discretionary)

• US managers of AIFs investing in Europe through an EU sub-adviser must consider the issue carefully, with particular reference to costs– will the EU sub-adviser be classified as the AIFM of the non-

EU AIF? If so, the sub-adviser will be subject to AIFMD structural and operational constraints

– EU AIFMs of a non-EU AIF marketed in EU must ensure AIF has appointed a depositary and comply with certain other requirements

– a non-EU AIFM need only comply with the PPO

105

OTHER EUROPEAN DEVELOPMENTS

106

Matters MIFID 2

The new EU MIFID 2 directive and regulation were published in the Summer. Member states have until July 2016 to adopt and publish implementing measures and apply them from 3 January 2017.

MIFID 2 makes many modifications to MIFID. Notably, three categories of entity will be bought into scope of MIFID regulation for the first time:

• New Third Country Firm (“TCF”) Regime• High Frequency Algorithmic Trading Technique Users• Commodity and Commodity Derivative Dealers

107

Matters MIFID 2 (2)

New TCF Regime

EU branch requirement

Member states have discretion to require a TCF which intends to provide investment services to retail and/or professional clients within its territory to establish a local branch subject to authorisation and supervision by the relevant EU regulator

Member states will not be permitted to impose the branch requirement on TCFs which provide investment services at the “exclusive invitation of the client” (aka reverse solicitation)

Should the UK decide to adopt the branch requirement, the current useful and generous registration exemption for non-EU overseas persons would likely be abrogated

108

Matters MIFID 2 (3)

EU cross-border services passport

TCFs may provide investment services on a cross-border basis to eligible counterparties and professional clients EU-wide provided they are registered with ESMA and, broadly, the TCF is based in an equivalent regime

Other aspects

In connection with MiFID2, ESMA recently issued a consultation document, featuring a proposal to ban the receipt of most investment research in return for dealing commissions

In June 2014 FCA tightened its rules on use of dealing commission and banned investment managers from paying for “corporate access services” using dealing commissions

109

Matters MAR 2The new EU Market Abuse Regulation (“MAR”) was published in the Summer and will be directly applicable EU-wide from 3 July 2016

MAR will replace completely the current EU Market Abuse Directive which was published in April 2004

MAR represents an attempt by the European Commission to introduce a single European rulebook on market abuse

• expands the scope of the regime in terms of covered markets and products

• introduces more stringent regulation• introduces new procedures for market soundings• designed to dovetail with MIFID 2

110

US AND EU FUND STRUCTURES JURISDICTIONAL CONTRASTS

111

The familiar master-feeder structure is largely driven by US conditions.

In the EU that structure is not typical for funds that have no taxable US investors.

US and EU fund structures – jurisdictional contrasts

112

Master Feeder Structure

Principals

Investment Manager

Master Fund(Cayman LP or Cayman Company that checks the

box to be treated as a partnership)

Non-US FeederFund

(Cayman Company)

US Feeder Fund(Delaware LP or Cayman Company that checks the box to be treated

as a partnership)

PrimeBroker

AdminServices

Non USInvestors

US TaxExempt

Investors

US TaxableInvestors

113

Single Entity Fund Structure

Principals

Investment Manager

Fund(Company in Cayman, Ireland or other appropriate

non-US domicile)

Non-US Investors US Tax Exempt Investors

PrimeBroker

Administrator