1. gst an overview 2. path journey of gst law 2 ... scheme for sgst - for goods ... single rate for...

TRANSCRIPT

3/7/2013

1

1. GST an overview 2. Path journey of GST Law 2. Constitutional amendment Bill 2. Preparation for forth coming

GST Law

2 CA P.J. Johney

3/7/2013

2

JOURNEY TO GST LAW

3 CA P.J. Johney

BASICS

4 CA P.J. Johney

What is GST? - tax on Goods and Services

Taxable Event - supply of goods

- supply of services

- Import of goods or services

Taxable: When supply is made for

consideration

3/7/2013

3

5 CA P.J. Johney

Remove cascading effect of Taxes

Creation of a national market with free

movement of goods and services

Rationalise the structure of indirect taxation

Comprehensive and wider coverage of input

tax set-off and service tax set-off

Continuous chain of set-off till the consumer

6 CA P.J. Johney

Dual GST - Central GST

- State(s) GST

(also agreed by Task Force and Department of Revenue (DoR))

Tax is on ‘supply of goods and services’ for

consideration

Destination based consumption tax

Concurrent jurisdiction of Centre and State over

entire value chain

3/7/2013

4

7 CA P.J. Johney

Amount (in Rs.)

Basic value charged for supply of goods or services

10,000

Add: CGST @ 8% 800

Add: SGST @ 8% 800

Total price charged for Local supply of goods or services

11,600

Local Supply

Note: In the above illustration, the rate of CGST and SGST is assumed to be 8% each

8 CA P.J. Johney

Amount (in Rs.)

Basic value charged for supply of goods or services

10,000

Add: IGST @ 16% 1600

Total price charged for Interstate supply of goods or services

11,600

Interstate Supply

Note: In the above illustration, the rate of IGST is assumed to be 16% each

3/7/2013

5

9 CA P.J. Johney

Amount (in Rs.)

Basic value charged for supply of goods or services

10,000

Add: GST @ 0% 0

Total price charged for Local supply of goods or services

10,000

Exports

10 CA P.J. Johney

Multiple Statutes - one CGST Statute - separate SGST statutes for individual States - IGST statute

Uniformity in basic features - chargeability - definition of taxable event and taxable

person - measure of levy including valuation and

basis of classification - collection procedure

3/7/2013

6

11 CA P.J. Johney

Both CGST and SGST on same base Input Tax Credit

- CGST against CGST - SGST against SGST - no Cross utilization between CGST and

SGST exception: IGST

- rules for taking and utilization of credit for CGST and SGST to be aligned

- separate records to be maintained

12 CA P.J. Johney

Recommendation of task force for input tax credit - No distinction between inputs and capital goods - Full input credit on capital goods in the year of

purchase itself

3/7/2013

7

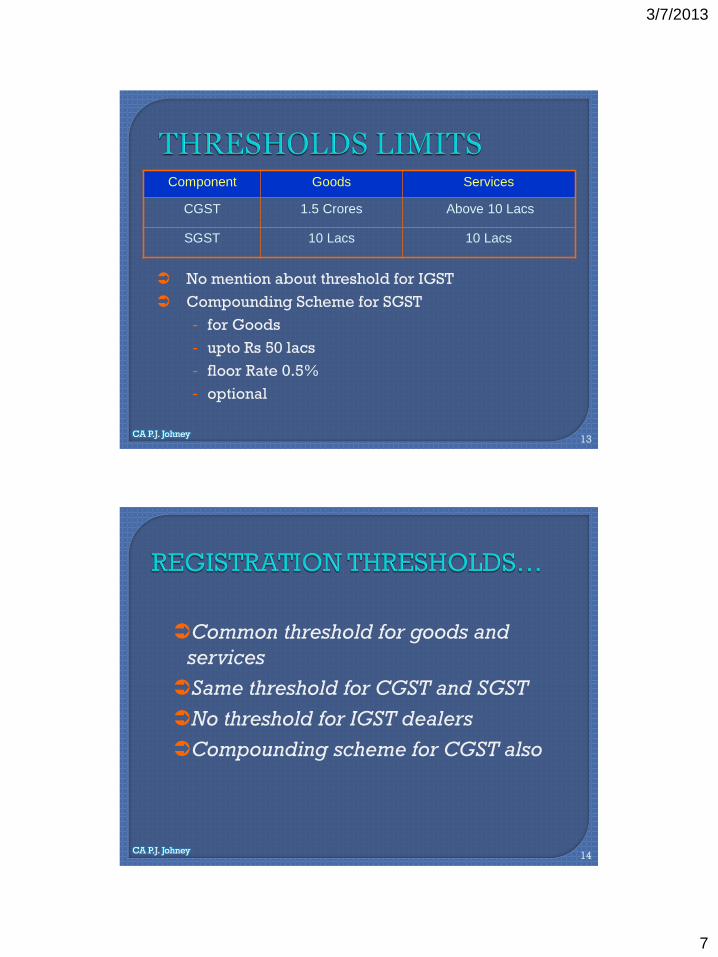

13 CA P.J. Johney

Component Goods Services

CGST 1.5 Crores Above 10 Lacs

SGST 10 Lacs 10 Lacs

No mention about threshold for IGST

Compounding Scheme for SGST

- for Goods

- upto Rs 50 lacs

- floor Rate 0.5%

- optional

14 CA P.J. Johney

Common threshold for goods and

services

Same threshold for CGST and SGST

No threshold for IGST dealers

Compounding scheme for CGST also

3/7/2013

8

15 CA P.J. Johney

For Goods - SGST

Two-rate structure - Lower Rate: for necessary items and goods of basic importance

- Standard Rate: for general goods

Special Rate for precious metals

Exempted goods (including goods of local

importance)

CGST may follow two-rate structure

16 CA P.J. Johney

For Services

Single Rate for both CGST and SGST

Exempted services

Issue of categorizing a supply: Goods or

Services?

- different rates of tax

- Different threshold

3/7/2013

9

17 CA P.J. Johney

Recommendation by Task Force

Single Rate for both goods and services

CGST @ 5% and SGST 7%

No classification between goods and

services

Issue of classifying goods or services for

place of supply?

18 CA P.J. Johney

Recommendation by DoR Single Rate for both goods and services under

SGST No two rate structure for goods Around 99 items to remain exempt under GST Common list of exemptions for both CGST and

SGST to be agreed Individual States will have no scope to expand

the exemption even for goods of local importance

3/7/2013

10

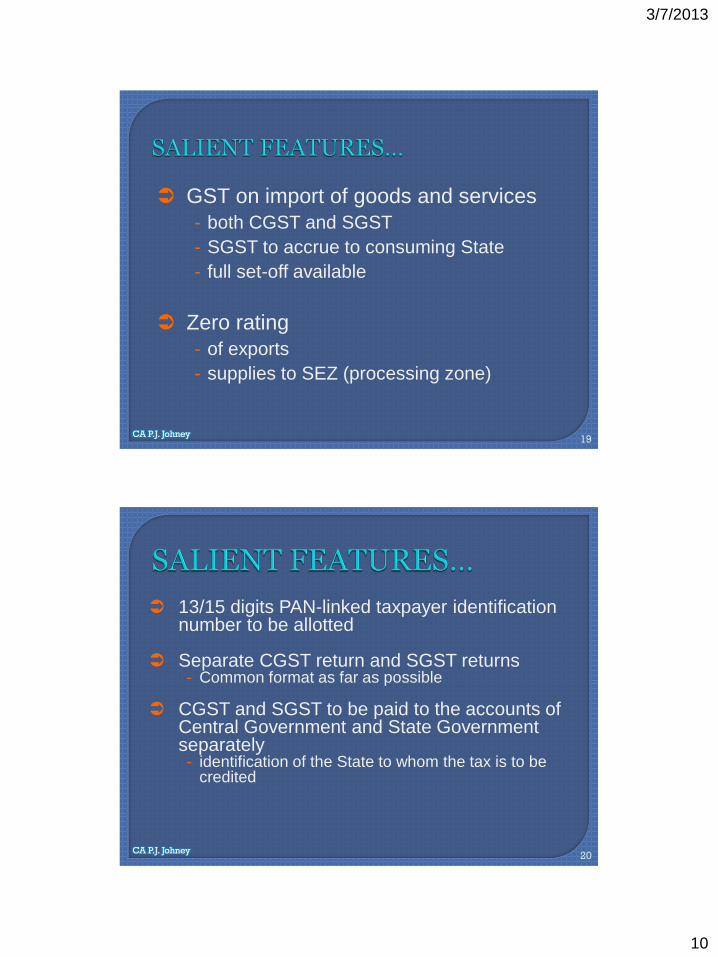

19 CA P.J. Johney

GST on import of goods and services

- both CGST and SGST

- SGST to accrue to consuming State

- full set-off available

Zero rating

- of exports

- supplies to SEZ (processing zone)

20 CA P.J. Johney

13/15 digits PAN-linked taxpayer identification number to be allotted

Separate CGST return and SGST returns - Common format as far as possible

CGST and SGST to be paid to the accounts of Central Government and State Government separately - identification of the State to whom the tax is to be

credited

3/7/2013

11

21 CA P.J. Johney

Separate authorities for administration, assessment, enforcement, scrutiny and audit for CGST & SGST

- Task force - recommended uniform compliance and enforcement procedure

- Uniform registration system and harmonised dispute resolution, advance rulings, scrutiny, audit etc.

22 CA P.J. Johney

Power to Centre to tax goods

Power to States - to tax services

- to tax import of goods and services

A binding mechanism on both Centre and the

States for harmonious rate structure

(expected)

3/7/2013

12

23 CA P.J. Johney

Central taxes to be subsumed

- Central Excise Duty

- Additional Excise Duty

- Excise duty levied under Medical and

Toiletries Preparation Act

- Service Tax

- Countervailing Duty

- Special Additional Duty

- Surcharge

- Cess

24 CA P.J. Johney

State taxes to be subsumed

- VAT / Sales tax

- Entertainment tax (not levied by local

bodies)

- Luxury tax

- Taxes on lottery, betting and gambling

- State Cesses and Surcharges

- Entry tax not in lieu of octroi

3/7/2013

13

25 CA P.J. Johney

Tax on Alcoholic Beverages - outside the purview of GST - States to continue to levy State Excise and VAT

- DoR – to be subsumed in GST

Tax on Tobacco Products - subjected to GST - Centre may levy excise duty over and above

GST

26 CA P.J. Johney

Tax on Petroleum Products - outside the purview of GST - Centre levies to continue - State levies to continue

Natural Gas – yet to be decided?

DoR – Petroleum product including natural gas should be included under GST

3/7/2013

14

27 CA P.J. Johney

Emissions fuels, tobacco products and

alcohol

- Subject to dual levy of GST and Excise

- No input credit for excise

28 CA P.J. Johney

Industrial incentives - cash refund schemes after collection of tax

Special Industrial Area Schemes

- to continue up to legitimate expiry time - Centre and State could provide reimbursement after

collecting GST

Any new exemption, remission scheme will not be allowed

3/7/2013

15

29 CA P.J. Johney

Recommendation by Task Force

Area based exemption to discontinue

Direct investment linked cash subsidy for

balanced regional development (if necessary)

30 CA P.J. Johney

Proposed GST is a destination-based

consumption tax

IGST – a new model designed to collect tax

and regulate inter-state transactions

Task Force - Modified Bank Model

recommended over IGST

DoR – Agreed with IGST but recommended

common threshold for better working

3/7/2013

16

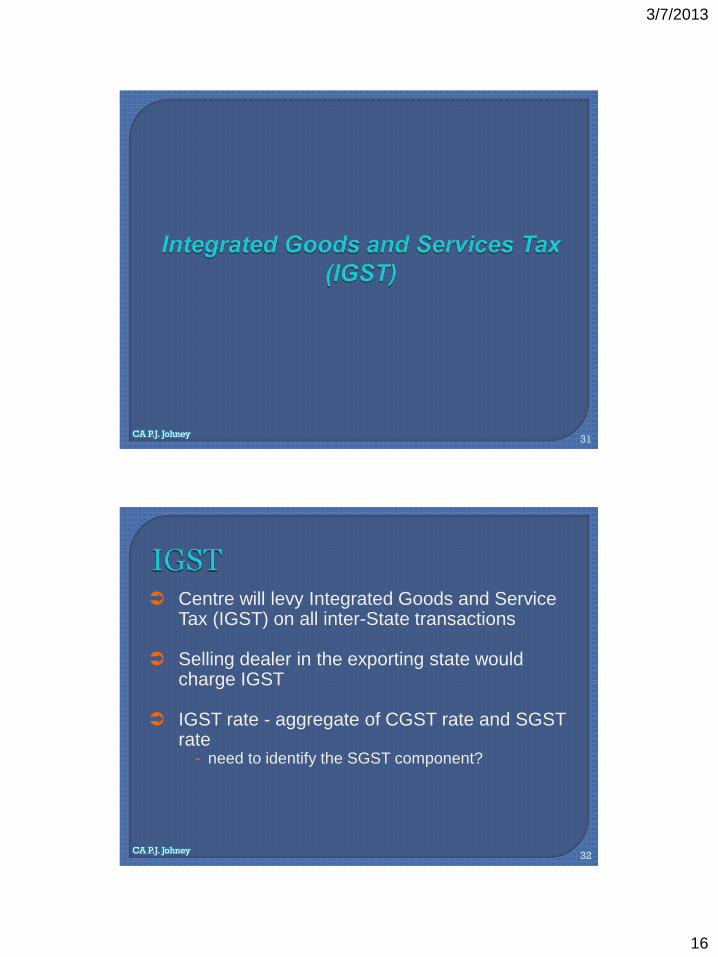

31 CA P.J. Johney

32 CA P.J. Johney

Centre will levy Integrated Goods and Service Tax (IGST) on all inter-State transactions

Selling dealer in the exporting state would charge IGST

IGST rate - aggregate of CGST rate and SGST rate

- need to identify the SGST component?

3/7/2013

17

33 CA P.J. Johney

(Task Force)

Seller in the exporting/originating state - to charge and collect CGST and SGST from the

buyer

Seller to pay - SGST - to the credit of Destination State

Government

- CGST – to Central Government

Buyer avail credit of the SGST and CGST

Consignment sales and branch transfers

across states - To be treated as inter-state transaction between two

independent dealers

34 CA P.J. Johney

Co. X (Delhi)

Co. Y (Punjab)

Central

Agency Output liability of Co. X

IGST @ 12% = Rs 12 cr

Inter-State sale

State Border

Assuming consideration = Rs.100 cr

Input Tax Credit of Co. X

CGST = Rs 8 cr

SGST = Rs 10 cr

3/7/2013

18

35 CA P.J. Johney

Co X (Delhi)

Co Y (Punjab)

Central

Agency

Payment of Tax by Co X

IGST Liability = Rs 12 Cr

Credit of Co X:

CGST = (Rs 8 Cr)

SGST = NIL

Net IGST Payable Rs 4 Cr – paid to Central Government

Option I

Take Credit of

CGST

36 CA P.J. Johney

Co X (Delhi)

Co Y (Punjab)

Central

Agency

Payment of Tax by Co X IGST Liability = Rs 12 Cr

Credit of Co X:

CGST = (Rs 8 Cr)

SGST = (Rs 4 Cr)#

Net IGST Payable NIL

Option II

Take Credit of

SGST

# Delhi Government will remit Rs 4 Cr to Central Agency

3/7/2013

19

37 CA P.J. Johney

Co X (Delhi)

Co Y (Punjab)

Central

Agency

Inter-state sale Co Z

(Punjab)

Local Sale

Rs 150 Cr

Local Sale by Co Y-

CGST(6%) SGST(4%)

Output Liability Rs 9 Cr Rs 6 Cr

Less: IGST Credit Rs 9 Cr# - .

NIL Rs 6 Cr – paid to State

# No remittance by Central Agency to Punjab

38 CA P.J. Johney

Seller (Delhi)

Invoice Buyer (Head Office) (Delhi)

Buyer (Factory) (Haryana)

- Whether transaction be subject to

IGST or SGST?

- Whether any tax be applicable on

transaction between Head Office and

Factory?

3/7/2013

20

39 CA P.J. Johney

Seller (Delhi)

Invoice Buyer (Head Office) (Punjab)

Buyer (Factory) (Haryana)

- Whether IGST credit can be taken in

Punjab or Haryana?

- Whether any tax be applicable on

transaction between Head Office and

Factory?

- How can IGST credit be utilized or transferred

by the Head Office?

40 CA P.J. Johney

State A

Dealer 2 Dealer 1

Dealer 3

State B

Invoice

Goods

- Issues under the CST Act

- How IGST solves the issue?

3/7/2013

21

41 CA P.J. Johney

THE CONSTITUTIONAL (115th

AMENDMENT) BILL, 2011

42 CA P.J. Johney

1. TO ENABLE AND TO FACILITATE INTRODUCTION OF GOODS AND

SERVICE TAX (GST) IN INDIA.

2. TO PROVIDE FOR CONCURRENT TAXING POWERS TO UNION AS

WELL AS STATES FOR LEVYING GST

3. TO ENABLE GST TO REPLACE OR SUBSUME INDIRECT TAXES

LEVY OF INTEGRATED GST (IGST)

4. DISTRIBUTION OF REVENUE

5. CREATION OF GST COUNCIL and GST DISPUTE SETTLEMENT

AUTHORITY

6. DISTRICT COUNCILS AND REGIONAL COUNCILS TO LEVY TAX ON

ENTERTAINMENT AND AMUSEMENT.

3/7/2013

22

43 CA P.J. Johney

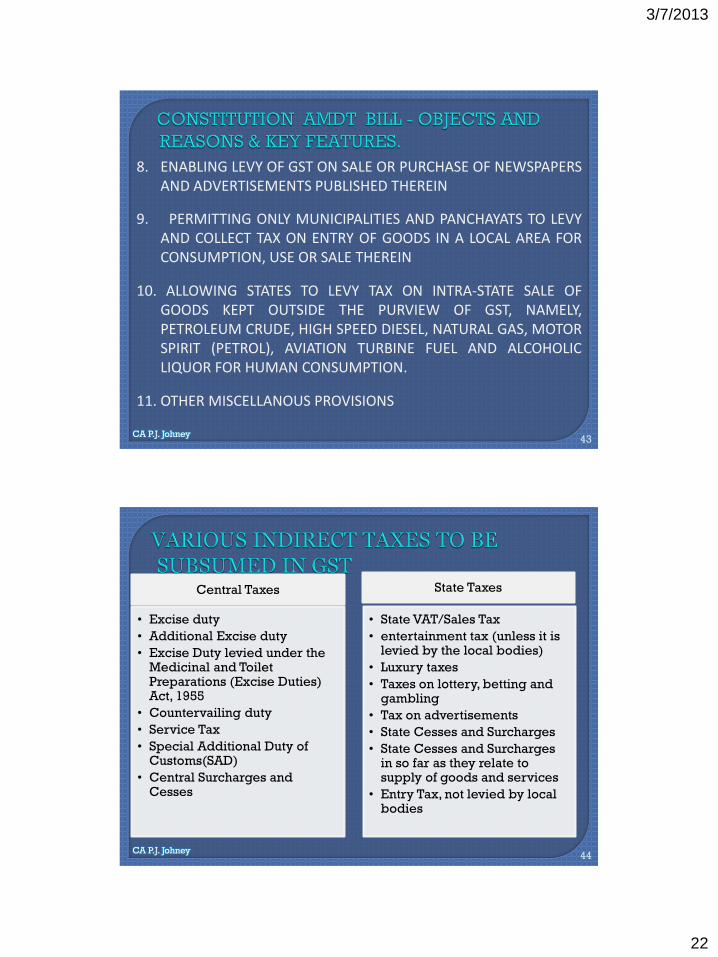

8. ENABLING LEVY OF GST ON SALE OR PURCHASE OF NEWSPAPERS AND ADVERTISEMENTS PUBLISHED THEREIN

9. PERMITTING ONLY MUNICIPALITIES AND PANCHAYATS TO LEVY AND COLLECT TAX ON ENTRY OF GOODS IN A LOCAL AREA FOR CONSUMPTION, USE OR SALE THEREIN

10. ALLOWING STATES TO LEVY TAX ON INTRA-STATE SALE OF GOODS KEPT OUTSIDE THE PURVIEW OF GST, NAMELY, PETROLEUM CRUDE, HIGH SPEED DIESEL, NATURAL GAS, MOTOR SPIRIT (PETROL), AVIATION TURBINE FUEL AND ALCOHOLIC LIQUOR FOR HUMAN CONSUMPTION.

11. OTHER MISCELLANOUS PROVISIONS

44 CA P.J. Johney

Central Taxes

• Excise duty

• Additional Excise duty

• Excise Duty levied under the Medicinal and Toilet Preparations (Excise Duties) Act, 1955

• Countervailing duty

• Service Tax

• Special Additional Duty of Customs(SAD)

• Central Surcharges and Cesses

State Taxes

• State VAT/Sales Tax

• entertainment tax (unless it is levied by the local bodies)

• Luxury taxes

• Taxes on lottery, betting and gambling

• Tax on advertisements

• State Cesses and Surcharges

• State Cesses and Surcharges in so far as they relate to supply of goods and services

• Entry Tax, not levied by local bodies

3/7/2013

23

45 CA P.J. Johney

ARTICLE -245 Extent of laws made by Parliament and by the

Legislatures of States.—

(1) Subject to the provisions of this Constitution, Parliament may make laws

for the whole or any part of the territory of India, and the Legislature of a

State may make laws for the whole or any part of the State.

(2) No law made by Parliament shall be deemed to be invalid on the ground

that it would have extra-territorial operation.

ARTICLE 246. Subject-matter of laws made by Parliament and by the

Legislatures of States.—

(1) Notwithstanding anything in clauses (2) and (3), Parliament has

exclusive power to make laws with respect to any of the matters

enumerated in List I in the Seventh Schedule (in this Constitution referred

to as the “Union List”).

46 CA P.J. Johney

(2) Notwithstanding anything in clause (3), Parliament,

and, subject to clause (1), the Legislature of any State

also, have power to make laws with respect to any of the

matters enumerated in List III in the Seventh Schedule (in

this Constitution referred to as the “Concurrent List”).

(3) Subject to clauses (1) and (2), the Legislature of any

State has exclusive power to make laws for such State or

any part thereof with respect to any of the matters

enumerated in List II in the Seventh Schedule (in this

Constitution referred to as the “State List”').

(4) Parliament has power to make laws with respect to

any matter for any part of the territory of India not included

in a State notwithstanding that such matter is a matter

enumerated in the State List.

3/7/2013

24

47 CA P.J. Johney

NEW ARTICLE - 246A.

Notwithstanding anything contained in articles 246 and

254, Parliament and the legislature of every State,

have power to make laws with respect to goods and

services tax imposed by the Union or by that State

respectively:

Provided that Parliament has exclusive power to make

laws with respect to goods and services tax where the

supply of goods, or of services, or both takes place in the

course of inter-State trade or commerce.

48 CA P.J. Johney

Composition Union Finance Minister – Chairperson

Union Minister of State in charge of revenue

Minister in charge of finance or taxation or other minister

by each State Govt.

Function To make recommendations to the Union and States

Taxes to be subsumed in GST

Taxable and exempted goods and services

Threshold limit of turnover

Rates of GST

Any other matter relating to GST

Decisions to be made with the consensus of all

members present

3/7/2013

25

49 CA P.J. Johney

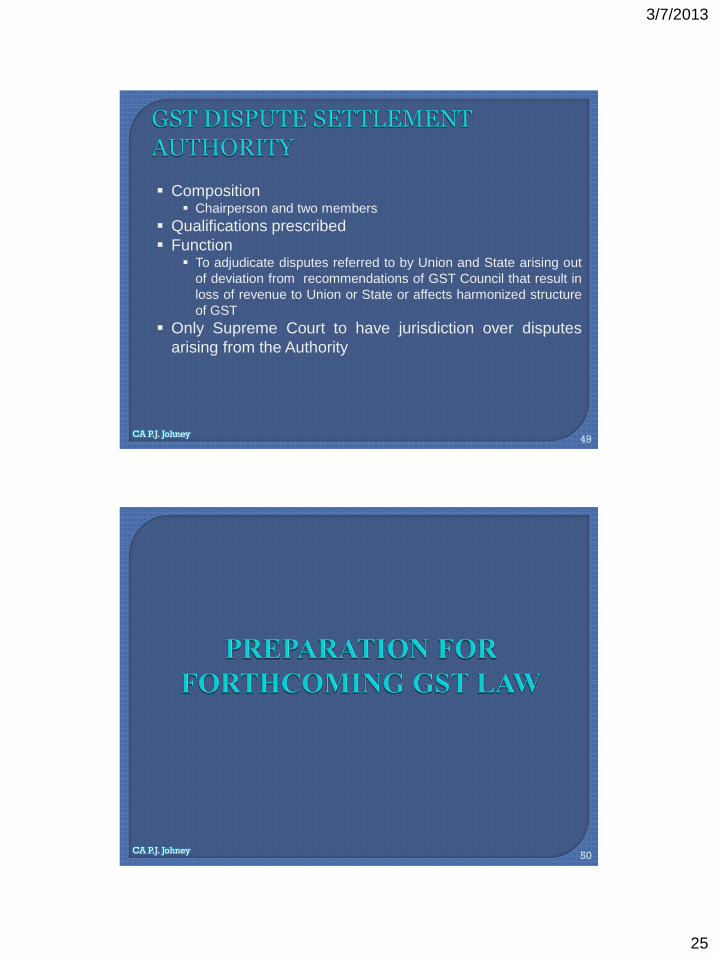

Composition Chairperson and two members

Qualifications prescribed

Function To adjudicate disputes referred to by Union and State arising out

of deviation from recommendations of GST Council that result in

loss of revenue to Union or State or affects harmonized structure

of GST

Only Supreme Court to have jurisdiction over disputes

arising from the Authority

50 CA P.J. Johney

3/7/2013

26

51 CA P.J. Johney

Tax is on ‘supply of goods or services for consideration’

Scope of the term ‘supply’? -is it anything done for consideration?

Scope of the term ‘goods’? - will it cover immovable property?

52 CA P.J. Johney

Tax is on ‘supply of goods or services for consideration’

Scope of the term ‘services’?

-need for enumeration of all services (positive list) or specifying negative list? -fate of common-man services such as medical facilities? -will it cover royalty, works contract, hire-purchase etc.?

3/7/2013

27

53 CA P.J. Johney

Scope of the term ‘consideration’?

- will it include non-monetary consideration?

- will Third Party consideration be included?

- will it include the following:-

compensation for early termination

penalty for breach of contract

security deposits and forfeiture of deposits

overpayments

54 CA P.J. Johney

Whether the term ‘goods’ will be defined? -should it include only tangible goods?

-current disputes

Whether immovable property be included as

goods? -difference in ‘goods’ for tax purposes and ‘goods’ as

per Sale of Goods Act, 1930

3/7/2013

28

55 CA P.J. Johney

Basis for giving input tax?

Whether a separate definition of ‘input’ or ‘input

service’ required?

Credit should be available on anything used in or

in relation to business

56 CA P.J. Johney

Identifying the Service Recipient -person making the payment?

3/7/2013

29

57 CA P.J. Johney

Services of conversion/processing provided by job-worker can be classified as supply of goods/service under GST regime.

The value of supply made by the job-worker shall be chargeable to both CGST and SGST.

Job worker would be entitled to take input tax credit of goods and services used in making the taxable supply.

58 CA P.J. Johney

Single or Multiple Supply?

-different rates for goods and services

-combination of taxable supplies and exempt

supplies

Principles for classification

-principal or ancillary supply

-economically single / indivisible supply

3/7/2013

30

59 CA P.J. Johney

Task Force Report

One positive rate each for CGST and SGST on

all goods and services

One zero rate for all goods and service exported

out of India

No issue for single or multiple supply or supply of

goods or services

60 CA P.J. Johney

How to avail credit on stock

transfer?

Issue of pre-determined sales? -No longer relevant as tax is

destination based

3/7/2013

31

61 CA P.J. Johney

Time period for refund of accumulated credit?

- no refund under CENVAT

- varied practices under State VAT Acts

White paper indicates - time bound manner

62 CA P.J. Johney

Refund available for exports,

purchase of capital goods, input

tax at higher rate than output tax

3/7/2013

32

63 CA P.J. Johney

Supplies in relation to SEZ non-processing zones? - whether Doctrine of Promissory Estoppel apply?

Supplies made to special projects such as

International Competitive Bidding (ICB), etc?

Supplies made to EOU, STP, EHTP etc.?

64 CA P.J. Johney

Treatment for opening credit in the books of accounts on the date of implementation of GST?

-VAT credit -CENVAT credit

Any credit not taken and accounted for as on the

date of implementation of GST -whether such credit will be allowed? -need to review whether all such credits have been duly accounted for

3/7/2013

33

65 CA P.J. Johney

• A sum of Rs. 9,000 crore towards the first

installment of the balance of CST

compensation provided in the budget.

* Work on draft GST Constitutional

amendment bill and GST law expected to

be taken forward.

66 CA P.J. Johney

•Record Keeping

•Tax Planning

•Departmental Audit •External Audit of VAT Records •System Audit •Certifications •Assisting the Government

3/7/2013

34

67 CA P.J. Johney