1 gasb 45 implementation options acbo fall conference october 16, 2008 presented by geoffrey l....

TRANSCRIPT

1

GASB 45 Implementation Options

ACBO Fall ConferenceOctober 16, 2008

Presented byGeoffrey L. Kischuk, FSA, MAAA, FCA

Total Compensation Systems, Inc.

2

GASB 45 Implementation Options

• Must be elected at implementation

• Should reflect past practices

• Should reflect future intentions

• Involve your auditor!

3

Past Practices

• Some Districts have been accruing liability

• Some have designated reserves (may or may not match accrued liability)

• Some have set up “GASB qualifying trust”– Some have funded– Trust may have been set up before

implementation date

4

Implementation Options

• Retroactive Adoption

• One year Amortization

• “Short-term differences”

5

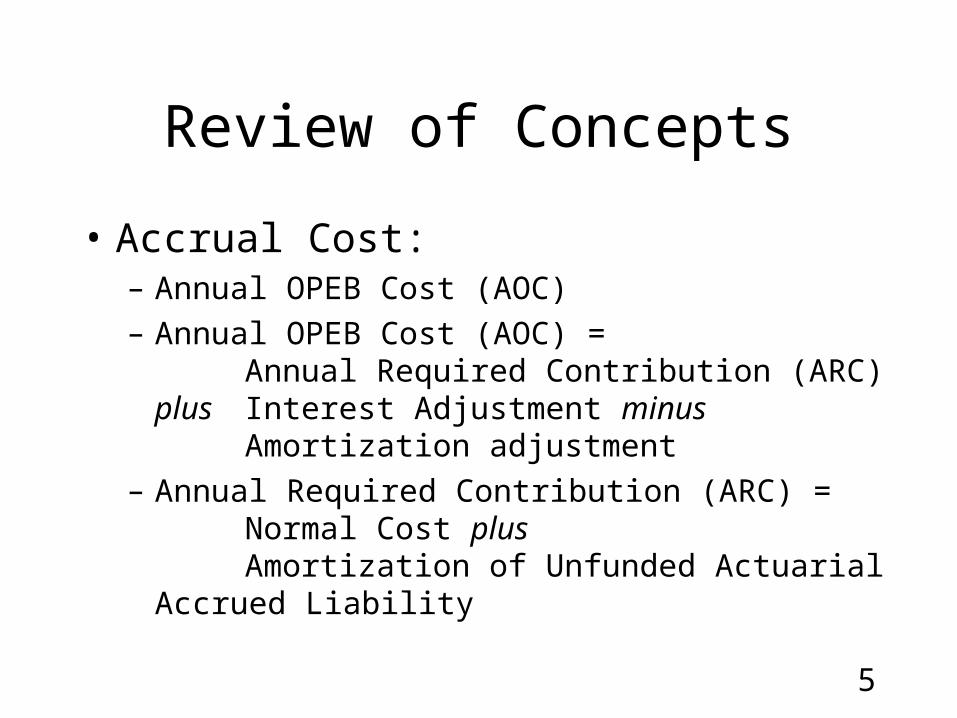

Review of Concepts

• Accrual Cost:– Annual OPEB Cost (AOC)– Annual OPEB Cost (AOC) =

Annual Required Contribution (ARC) plus Interest Adjustment minus

Amortization adjustment– Annual Required Contribution (ARC) =

Normal Cost plusAmortization of Unfunded Actuarial Accrued

Liability

6

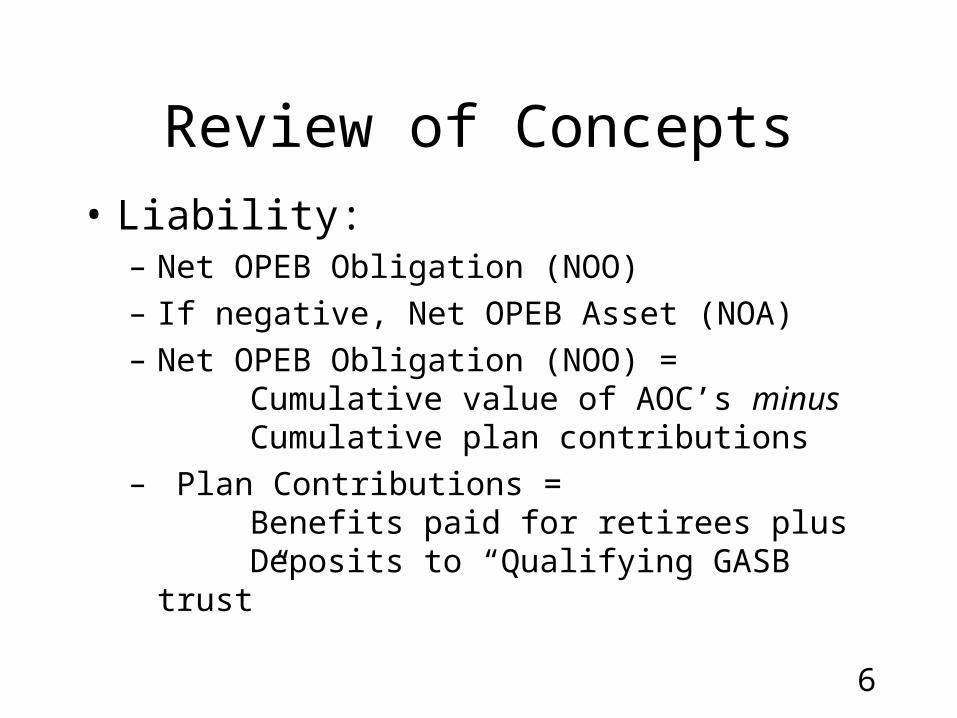

Review of Concepts

• Liability:– Net OPEB Obligation (NOO)– If negative, Net OPEB Asset (NOA)– Net OPEB Obligation (NOO) =

Cumulative value of AOC’s minusCumulative plan contributions

– Plan Contributions =Benefits paid for retirees plusDeposits to “Qualifying GASB trust”

7

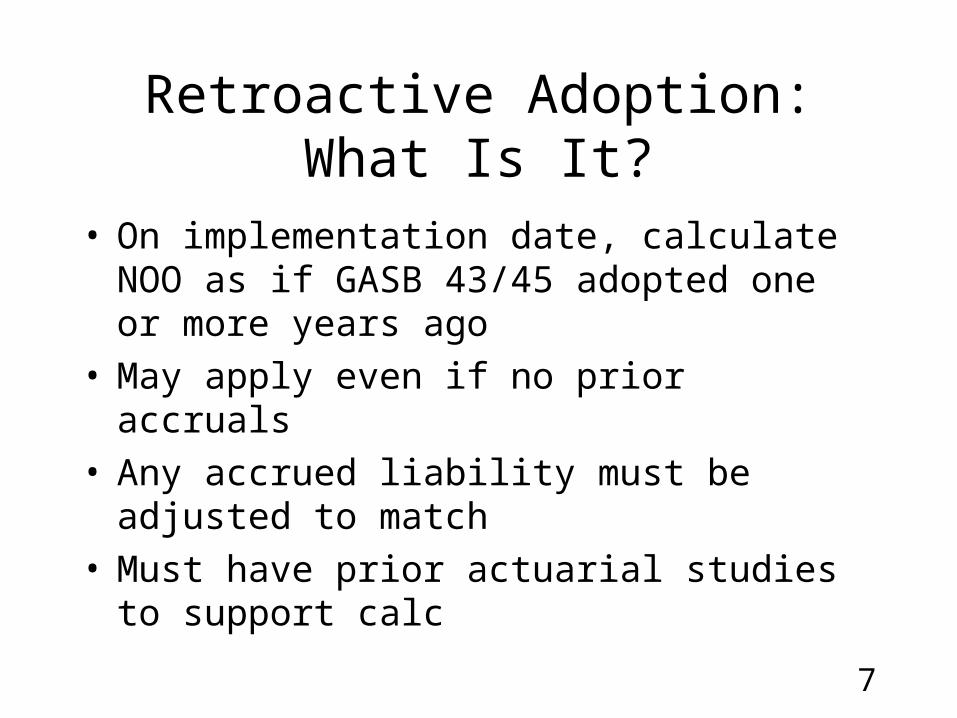

Retroactive Adoption: What Is It?

• On implementation date, calculate NOO as if GASB 43/45 adopted one or more years ago

• May apply even if no prior accruals• Any accrued liability must be adjusted to match• Must have prior actuarial studies to support calc

8

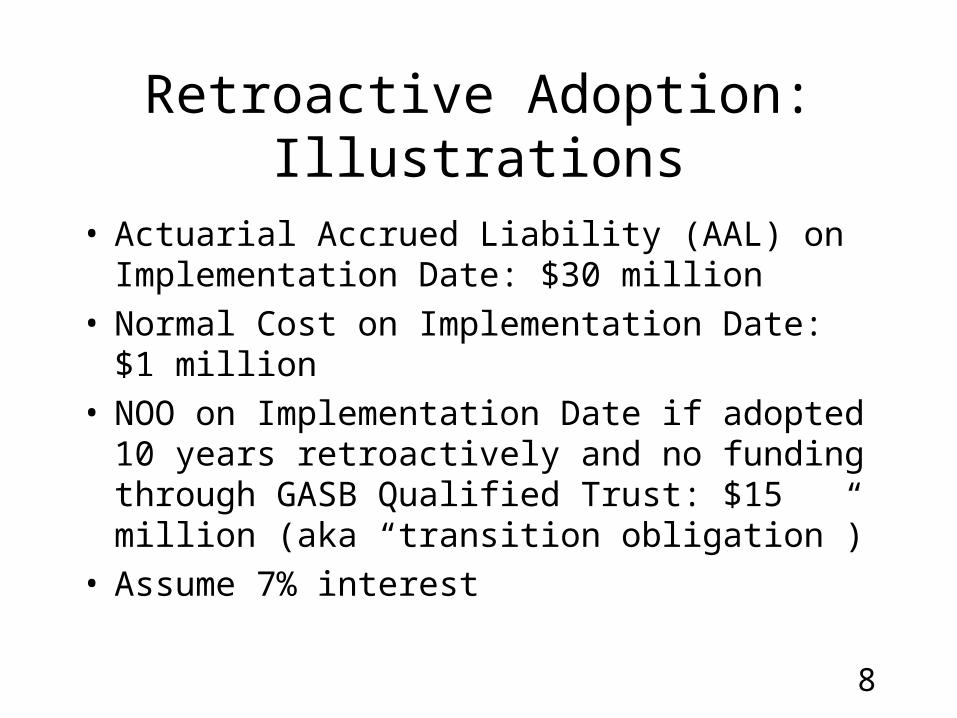

Retroactive Adoption: Illustrations

• Actuarial Accrued Liability (AAL) on Implementation Date: $30 million

• Normal Cost on Implementation Date: $1 million• NOO on Implementation Date if adopted 10 years

retroactively and no funding through GASB Qualified Trust: $15 million (aka “transition obligation”)

• Assume 7% interest

9

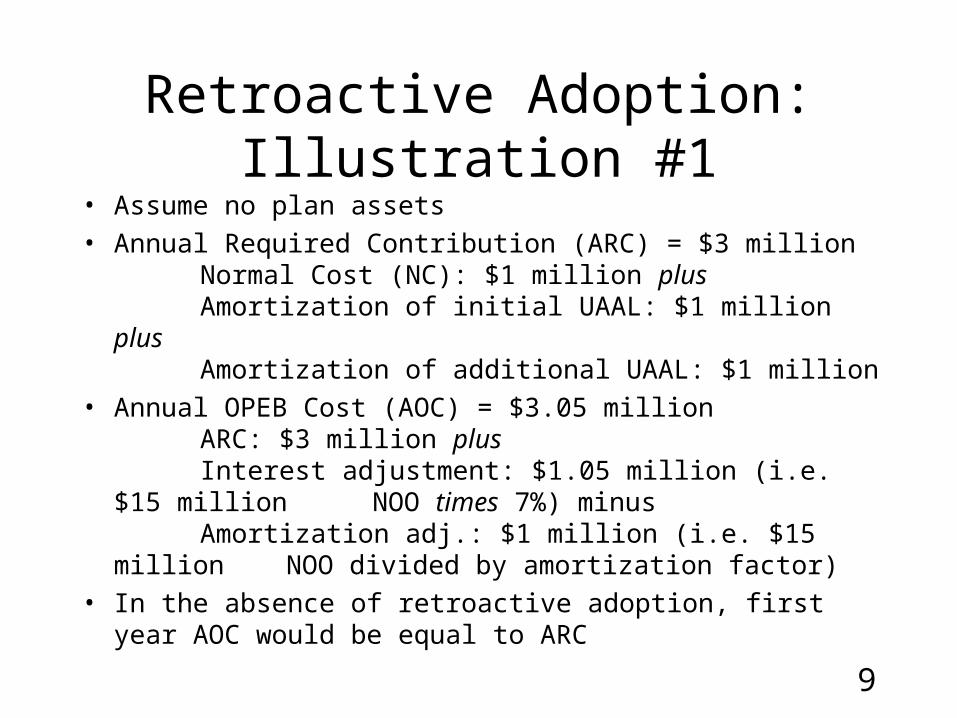

Retroactive Adoption: Illustration #1• Assume no plan assets

• Annual Required Contribution (ARC) = $3 millionNormal Cost (NC): $1 million plus

Amortization of initial UAAL: $1 million plusAmortization of additional UAAL: $1 million

• Annual OPEB Cost (AOC) = $3.05 million ARC: $3 million plusInterest adjustment: $1.05 million (i.e. $15 million NOO times 7%) minusAmortization adj.: $1 million (i.e. $15 million NOO divided by amortization factor)

• In the absence of retroactive adoption, first year AOC would be equal to ARC

10

Retroactive Adoption: Illustration #1

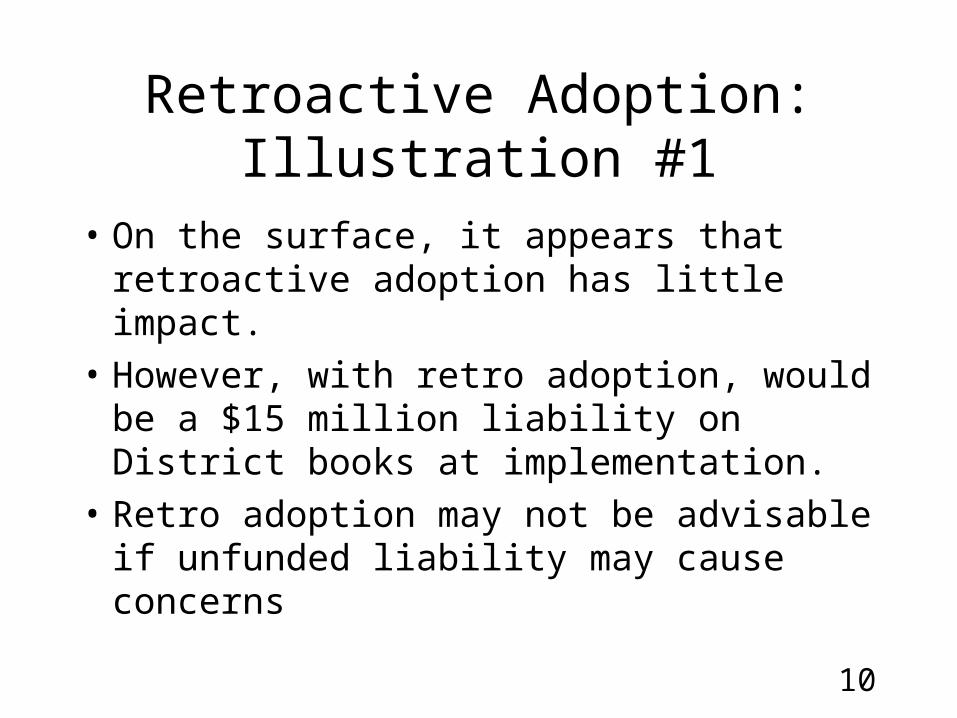

• On the surface, it appears that retroactive adoption has little impact.

• However, with retro adoption, would be a $15 million liability on District books at implementation.

• Retro adoption may not be advisable if unfunded liability may cause concerns

11

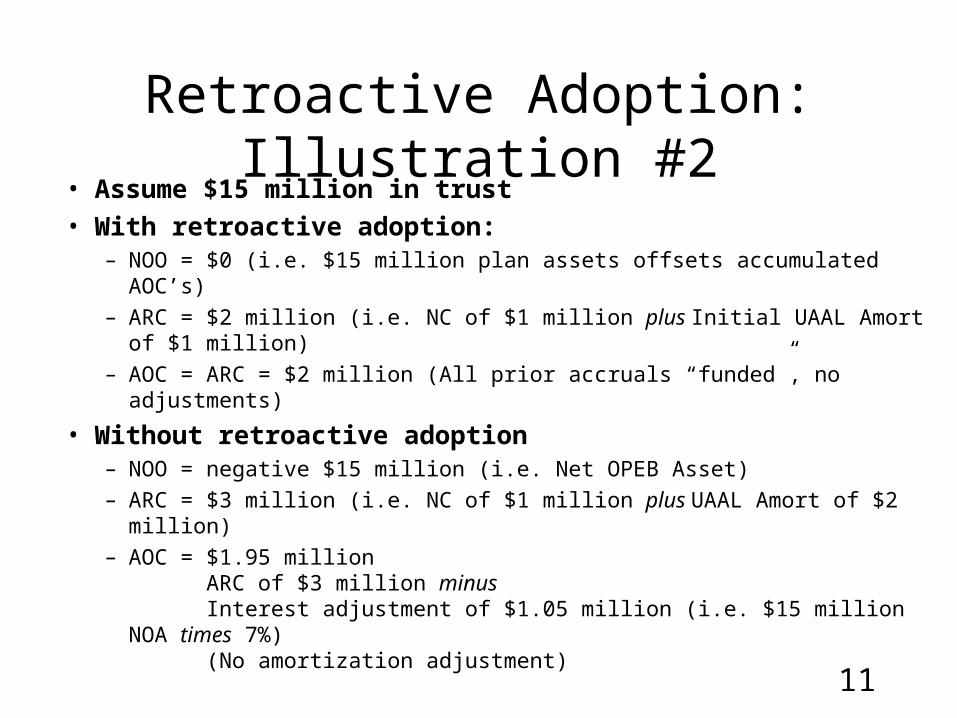

Retroactive Adoption: Illustration #2• Assume $15 million in trust

• With retroactive adoption:– NOO = $0 (i.e. $15 million plan assets offsets accumulated AOC’s)

– ARC = $2 million (i.e. NC of $1 million plus Initial UAAL Amort of $1 million)

– AOC = ARC = $2 million (All prior accruals “funded”, no adjustments)

• Without retroactive adoption– NOO = negative $15 million (i.e. Net OPEB Asset)

– ARC = $3 million (i.e. NC of $1 million plus UAAL Amort of $2 million)

– AOC = $1.95 millionARC of $3 million minusInterest adjustment of $1.05 million (i.e. $15 million NOA times

7%)(No amortization adjustment)

12

Retroactive Adoption: Illustration #2

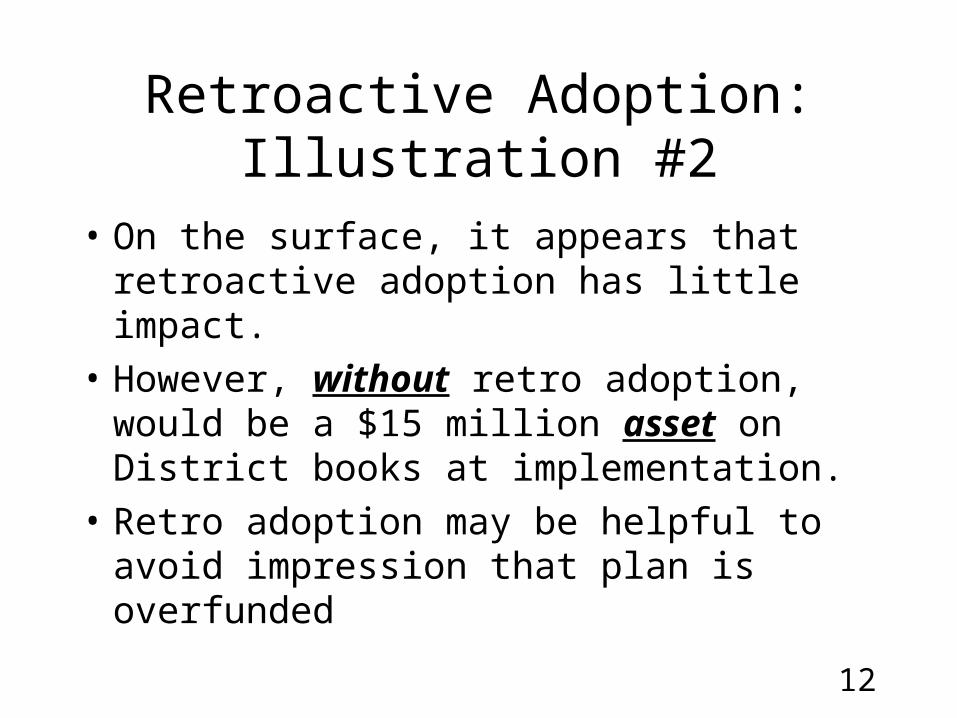

• On the surface, it appears that retroactive adoption has little impact.

• However, without retro adoption, would be a $15 million asset on District books at implementation.

• Retro adoption may be helpful to avoid impression that plan is overfunded

13

Retroactive Adoption: Illustration #3

• No assets in trust, but trust set up prior to Implementation Date

• Receivable can be set up on Trust books with offsetting payable on District books (“Short-term Difference”)

• Effect can be the same as Illustration #2

14

Retroactive Adoption: Illustration #4

• No assets in trust, trust set up on or after Implementation Date

• Receivable can be set up on Trust books with offsetting payable on District books (“Short-term Difference”)

• Effect can be the same as Illustration #2 except in first year AOC will include adjustments

15

One Year Amortization

• Start with NOO of $0

• Accrue entire Initial AAL at end of first year

• AAL arising from actuarial gains/losses, plan changes, etc. amortized as they arise

16

One Year Amortization: Illustrations

• Actuarial Accrued Liability (AAL) on Implementation Date: $30 million

• Normal Cost on Implementation Date: $1 million• Assume 7% interest• Assume annual “pay-as-you-go” cost of $1

million

17

One Year Amortization: Illustration #1

• Assume no plan assets• Annual Required Contribution (ARC) = $31 million

Normal Cost (NC): $1 million plusAmortization of UAAL: $30 million (i.e one year)

• First year Annual OPEB Cost (AOC) = ARC• Second year ARC consists only of NC ($1 million)• Second year AOC: $3.1 million

ARC of $1 million plusInterest adjustment of $2.1 million (i.e. NOO of $30

milliontimes 7%)

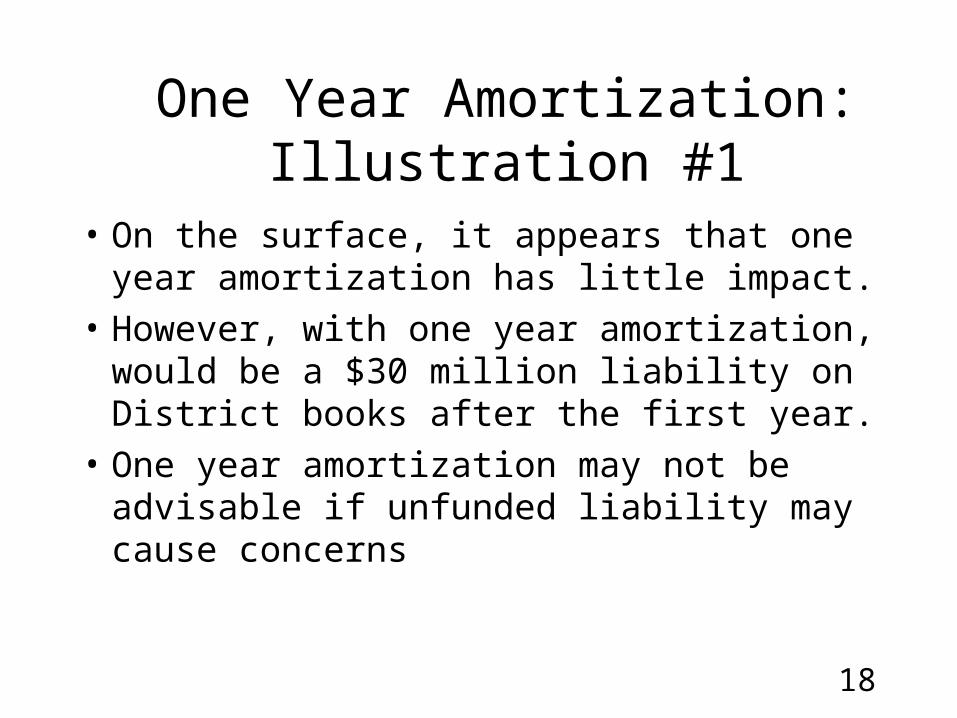

18

One Year Amortization: Illustration #1

• On the surface, it appears that one year amortization has little impact.

• However, with one year amortization, would be a $30 million liability on District books after the first year.

• One year amortization may not be advisable if unfunded liability may cause concerns

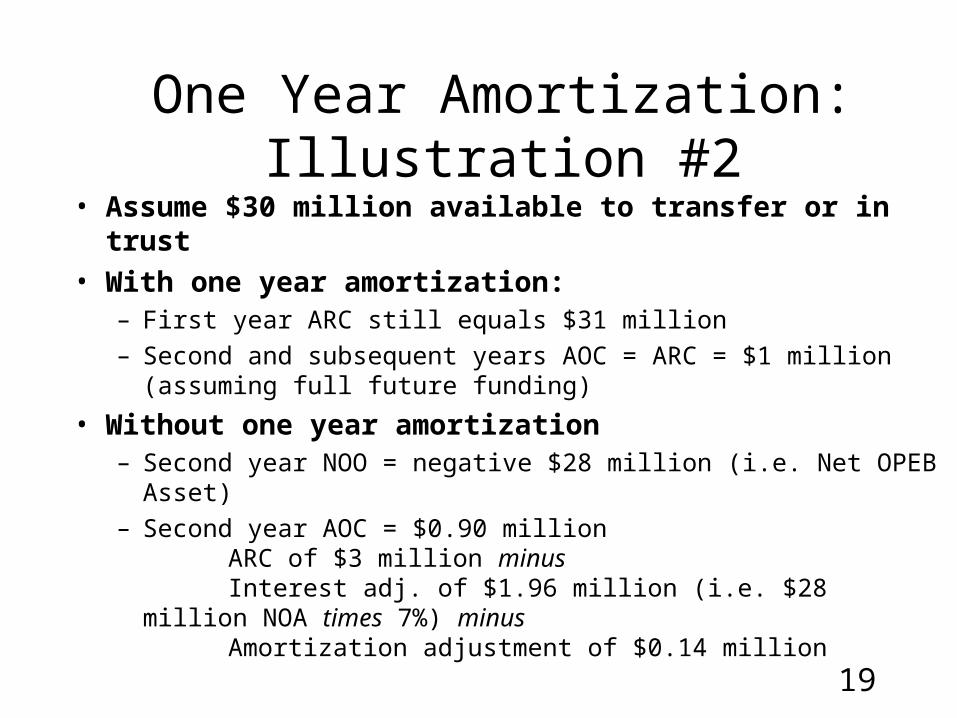

19

One Year Amortization: Illustration #2• Assume $30 million available to transfer or in trust

• With one year amortization:– First year ARC still equals $31 million

– Second and subsequent years AOC = ARC = $1 million (assuming full future funding)

• Without one year amortization– Second year NOO = negative $28 million (i.e. Net OPEB Asset)

– Second year AOC = $0.90 millionARC of $3 million minusInterest adj. of $1.96 million (i.e. $28 million NOA times 7%)

minusAmortization adjustment of $0.14 million

20

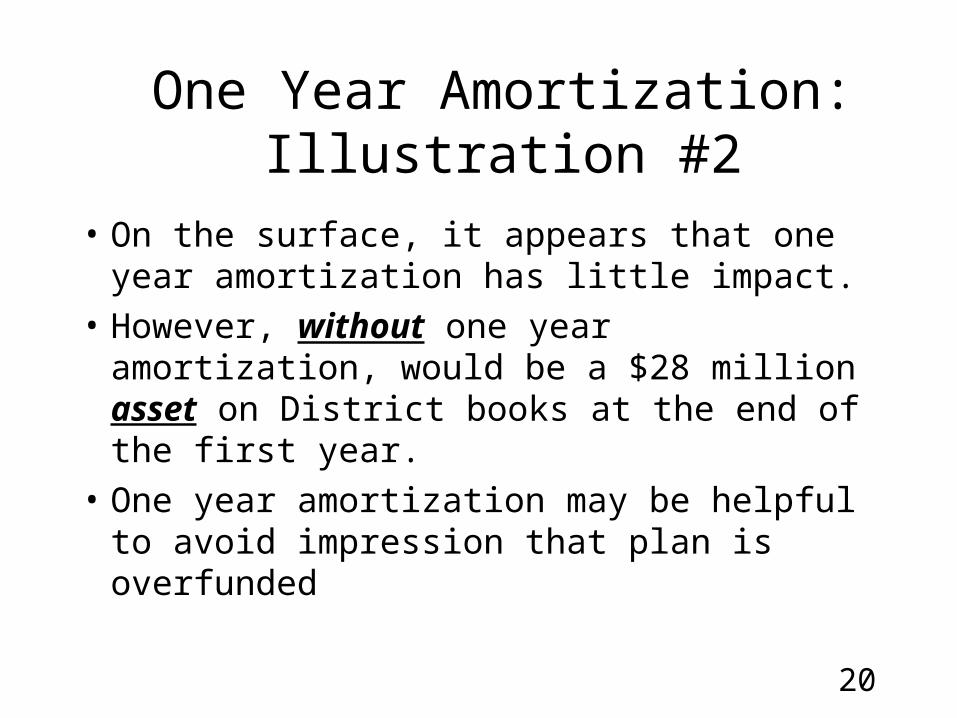

One Year Amortization: Illustration #2

• On the surface, it appears that one year amortization has little impact.

• However, without one year amortization, would be a $28 million asset on District books at the end of the first year.

• One year amortization may be helpful to avoid impression that plan is overfunded

21

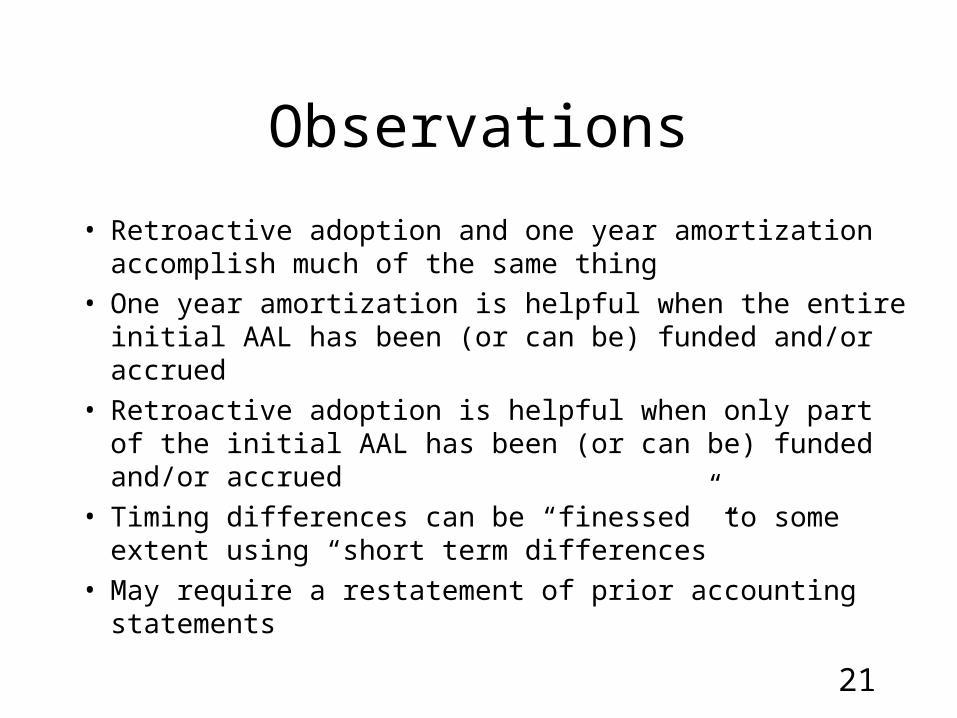

Observations

• Retroactive adoption and one year amortization accomplish much of the same thing

• One year amortization is helpful when the entire initial AAL has been (or can be) funded and/or accrued

• Retroactive adoption is helpful when only part of the initial AAL has been (or can be) funded and/or accrued

• Timing differences can be “finessed” to some extent using “short term differences”

• May require a restatement of prior accounting statements

22

Short Term Differences

• Contributions that were not made when intended• Contribution must be made by the later of:

– The next actuarial valuation; or

– One year

• Can be used to count contributions made in one period toward the ARC in a prior period

• Auditor can help with appropriate accounting entries

23

Thank you!

Questions??