1 dtcc executive forum managing market-wide risk at warp speed low latency in a fragmented world rob...

TRANSCRIPT

1

DTCC Executive Forum

Managing Market-wide Risk at Warp SpeedLow Latency in a Fragmented World

Rob Hegarty

Managing Director, Market Structure

DTCC

November 23, 2009

2

Market Structure Isn’t Just for Trading Anymore!

Trading business models:• Exchange• Auction• Crossing • Order-book• Open outcry• Over-the-counter• Electronic• Voice

Clearance & Settlement business models:• Centrally• Bi-laterally• Multi-laterally• Uncleared

• Physical Settlement• Book entry

Source: DTCC

33

A comparison of Equity Market Structures in the US and Europe draws a deep contrast between models

United States

Trading

Clearing

Settlement

Single CCP

Clearing cost per side

$ 0.003€ 0.002

$ 0.034€ 0.023

Exchange rate € 0.67 to $ as of November 17, 2009

Europe

WBS

ENX

NOX

DBS

ISE

BSI

OBS

SIX

LSECHX

TQS

NOE BTS

SMP NAE

NEM

CPACLN LCH ERXCCG XCLECPFEF

AT

BE FR NL PT

SE DKFI

DEGB

IT

NO

CH

SXB SXE

IE

60

DTCC (NSCC)

Single CSDDTCC (DTC)

Source: DTCC

4

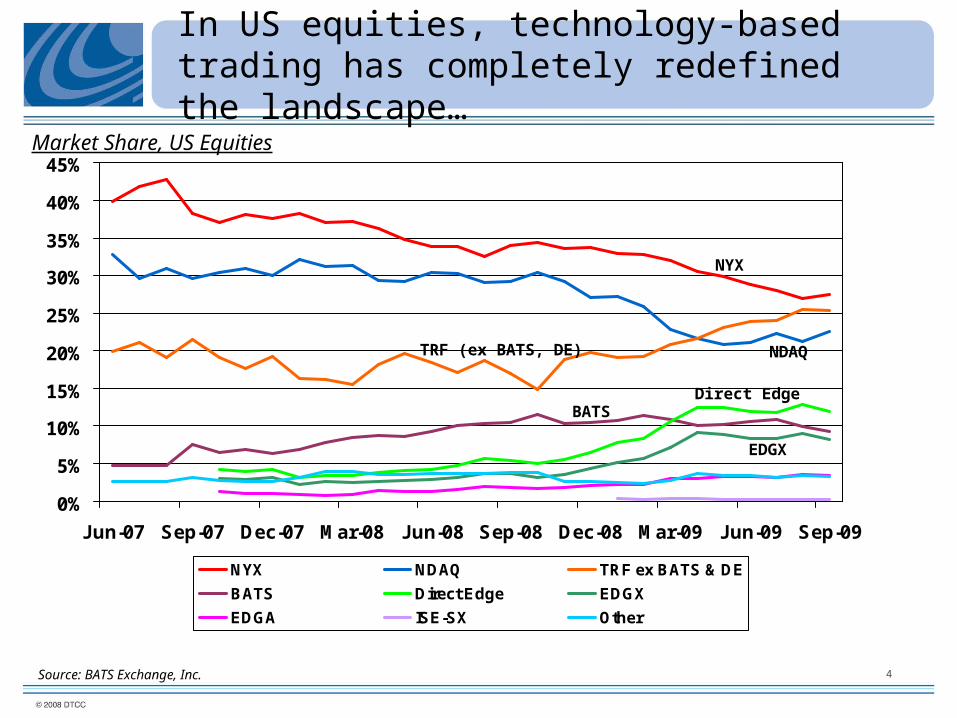

In US equities, technology-based trading has completely redefined the landscape…

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Jun-07 Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09

NYX NDAQ TRF ex BATS & DE

BATS Direct Edge EDGX

EDGA ISE-SX Other

NYX

NDAQTRF (ex BATS, DE)

Direct EdgeBATS

EDGX

Source: BATS Exchange, Inc.

Market Share, US Equities

5

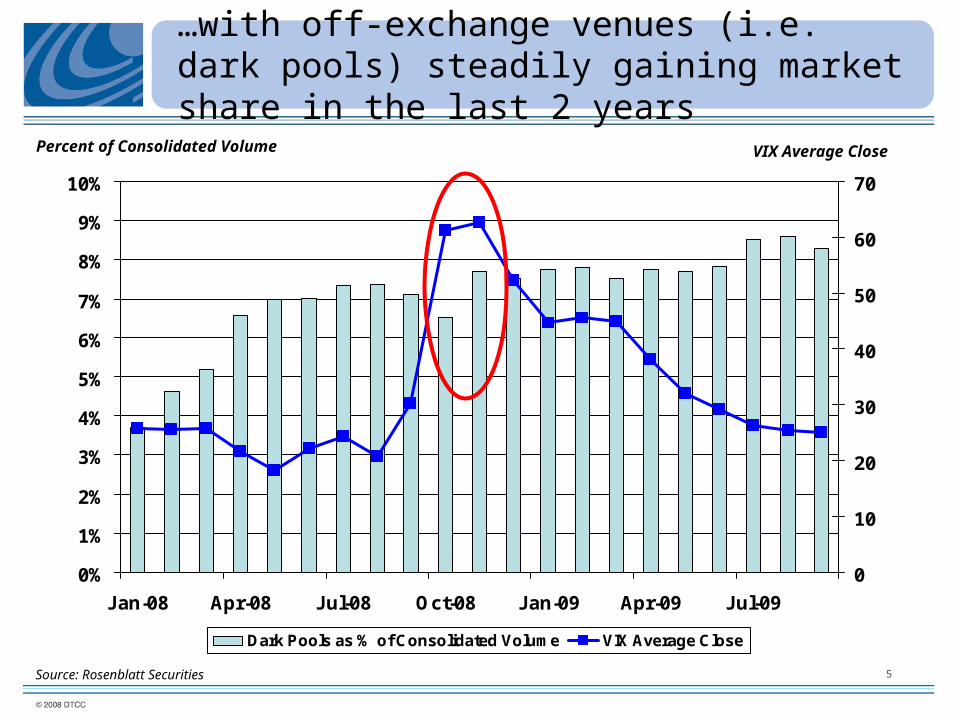

…with off-exchange venues (i.e. dark pools) steadily gaining market share in the last 2 years

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09

0

10

20

30

40

50

60

70

Dark Pools as % of Consolidated Volume VIX Average Close

Source: Rosenblatt Securities

Percent of Consolidated Volume VIX Average Close

6

…leading to the emergence of some big players in the equity execution business – that aren’t exchanges

CREDIT SUISSE CROSSFINDER

17%

GOLDMAN SACHS SIGMA X

15%

KNIGHT LINK13%

GETCO EXECUTION SERVICES

13%

LEVEL ATS7%

MORGAN STANLEY MS POOL

6%

UBS PIN5%

CITI MATCH4%

BARCLAYS LX4%

LIQUIDNET4%

ITG POSIT3%

INSTINET CBX3%

NYFIX MILLENNIUM2%

BIDS TRADING2%

PIPELINE TRADING1%

BNY CONVERGEX VORTEX

1%

Source: Rosenblatt Securities, August 2009

Breakdown of Dark Pool volume (8.6% of total volume)

7

With the same effect spilling over to Europe

Source: Federation of European Securities Exchanges

8

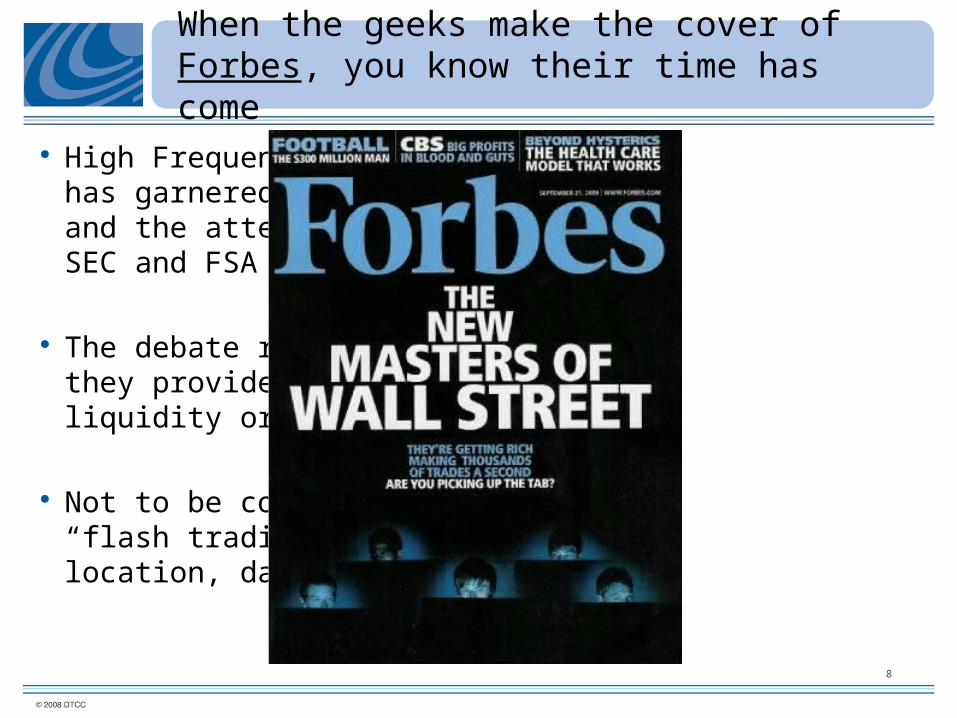

When the geeks make the cover of Forbes, you know their time has come

High Frequency Trading has garnered headlines…and the attention of the SEC and FSA

The debate rages: Are they providers of liquidity or bandits

Not to be confused with “flash trading”, co-location, dark pools, ….

9

Competing forces within the global financial markets help shape the future of market structure

10

Post-trade or at-trade risk management for high frequency trading: Why?

More feasible for cross-market monitoring

Low-latency platforms make “at-trade” or “simul-trade” risk management more of a reality…and a necessity

Cancellation rates of 99.99%– Imagine doing pre-trade on

all those orders that never get executed

Protect the HFT business from systemic failure

11

DTCC Executive Forum

Managing Market-wide Risk at Warp SpeedLow Latency in a Fragmented World

Rob Hegarty

Managing Director, Market Structure

DTCC

November 23, 2009