1 d&o liability insurance: where we have been - where we are going david m. gilfillan, sr. v.p....

TRANSCRIPT

1

D&O LIABILITY INSURANCE:

WHERE WE HAVE BEEN - WHERE WE ARE GOING

David M. Gilfillan, Sr. V.P. – AIGPatrick M. Kelly - Wilson, Elser, Moskowitz, Edelman & Dicker LLP

Paul Lefcourt, Senior V.P. – ECM Insurance Services, Inc. Management Liability Practice Liability

Evan J. Rosenberg, Sr. V.P. Chubb & Son

2

OVERVIEW

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• Evaluation of Public Company D&O Insurance Coverage and Exposure - An Historical Oversight

• Private D&O Issues

• Bankruptcy Issues

3 David M. Gilfillan - AIG

EVOLUTION OF PUBLIC COMPANY D&O INSURANCE COVERAGE AND EXPOSURE

1994 and prior - D&O policies covered the Directors and Officers only; the corporation was not covered as a defendant.

1994 - Equity Coverage for Corporation - sold by endorsement.

1995 - Entity Coverage in D&O policies - Nordstrom and Safeway .

4 David M. Gilfillan - AIG

1995 - PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 (“PSLRA”)

• Stayed discovery pending outcome of motion to dismiss.

• Allowed for sanctions for frivolous filings.

• Promoted process to have investors with largest financial stake in litigation become lead plaintiff instead of “race to court house” by law firms with stables of plaintiffs.

• Set high standard for “scienter” (intent to deceive).

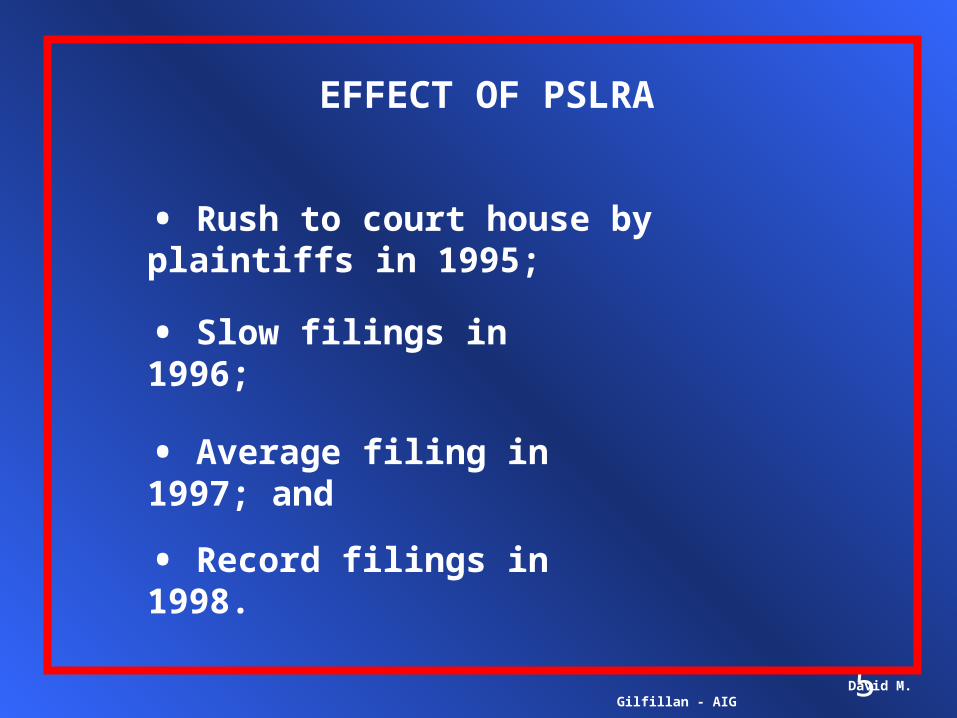

5 David M. Gilfillan - AIG

EFFECT OF PSLRA

• Rush to court house by plaintiffs in 1995;

• Slow filings in 1996;

• Average filing in 1997; and

• Record filings in 1998.

6 David M. Gilfillan - AIG

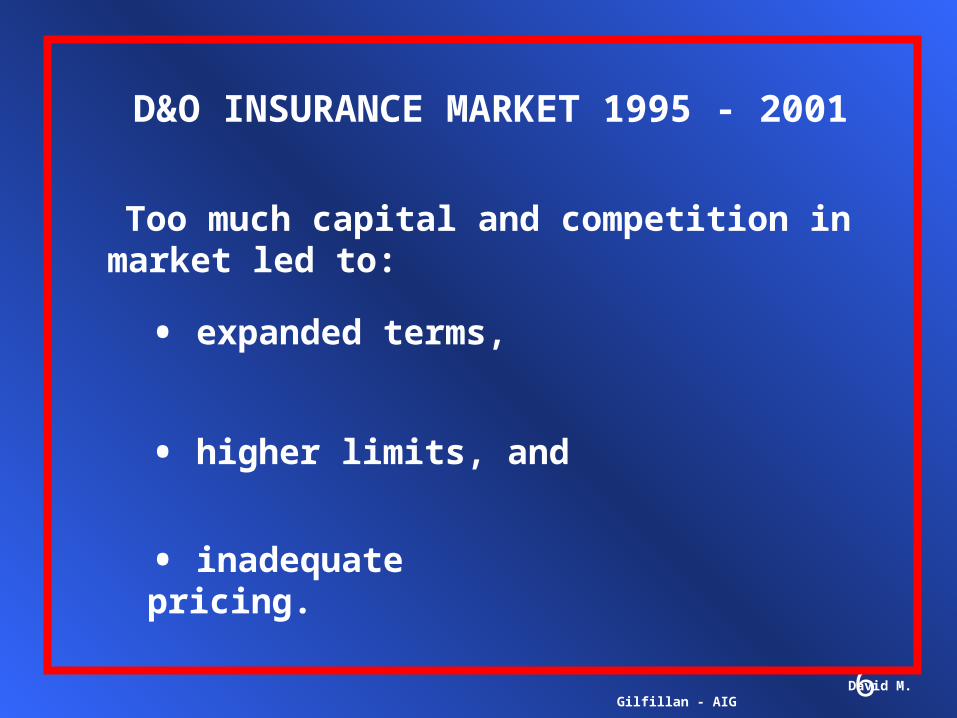

D&O INSURANCE MARKET 1995 - 2001

Too much capital and competition in market led to:

• expanded terms,

• higher limits, and

• inadequate pricing.

7 David M. Gilfillan - AIG

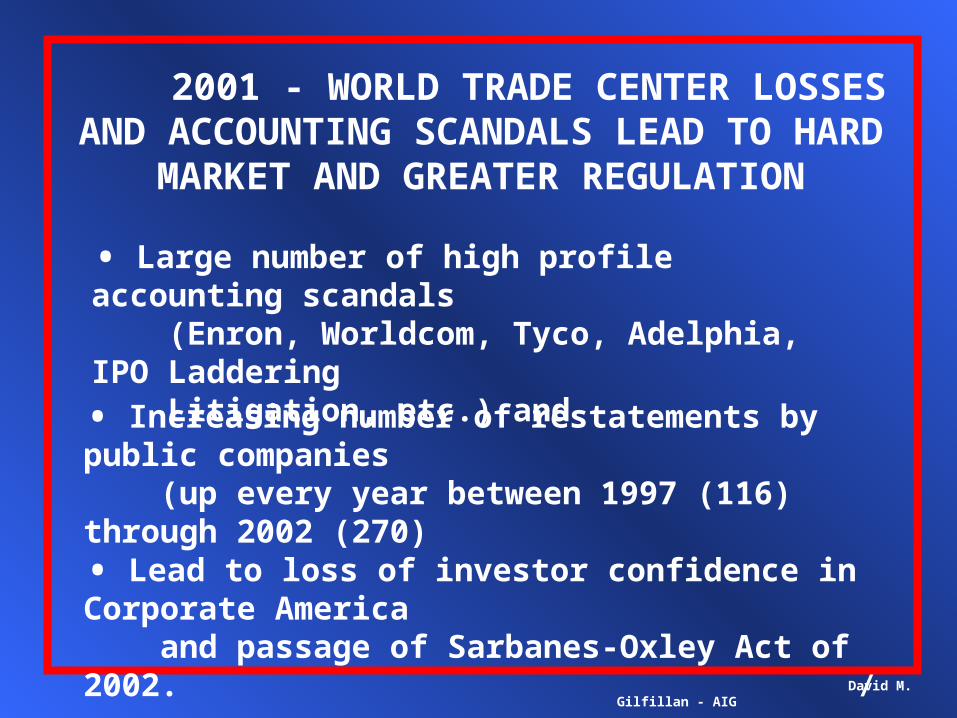

2001 - WORLD TRADE CENTER LOSSES AND ACCOUNTING SCANDALS LEAD TO

HARD MARKET AND GREATER REGULATION

• Large number of high profile accounting scandals (Enron, Worldcom, Tyco, Adelphia, IPO Laddering Litigation, etc.) and

• Increasing number of restatements by public companies (up every year between 1997 (116) through 2002 (270)

• Lead to loss of investor confidence in Corporate America and passage of Sarbanes-Oxley Act of 2002.

8 David M. Gilfillan - AIG

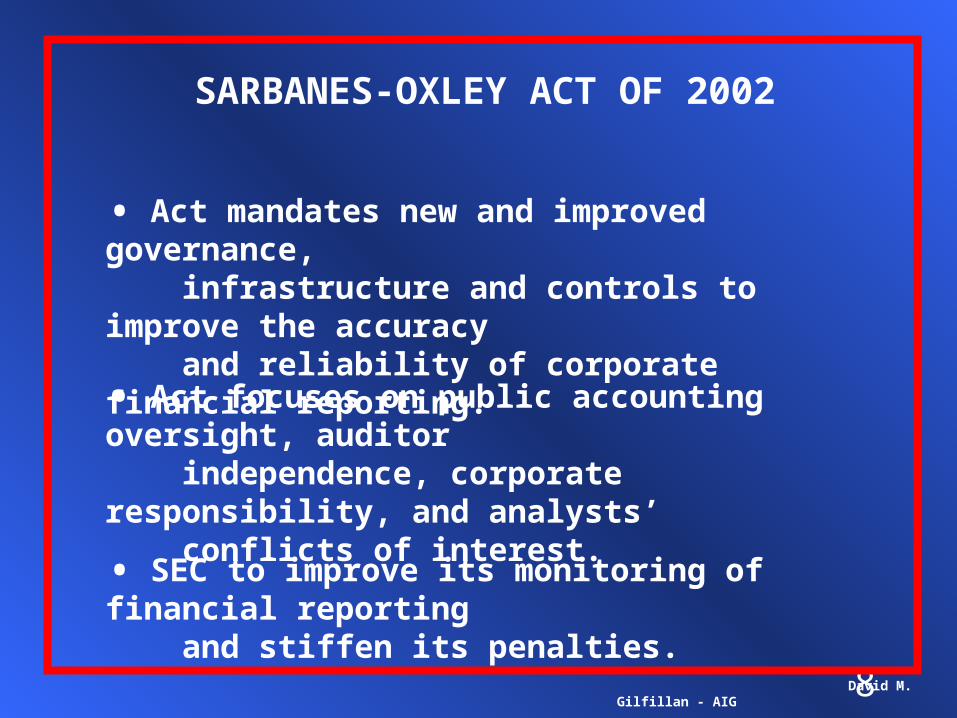

SARBANES-OXLEY ACT OF 2002

• Act mandates new and improved governance, infrastructure and controls to improve the accuracy and reliability of corporate financial reporting.

• Act focuses on public accounting oversight, auditor independence, corporate responsibility, and analysts’ conflicts of interest.

• SEC to improve its monitoring of financial reporting and stiffen its penalties.

9 David M. Gilfillan - AIG

2001 TO PRESENT, NET EFFECT - D&O COVERAGE HAS RESTRICTED

• Less Availability

• Narrower Coverage

• Higher Premium

10Wilson, Elser, Moskowitz, Edelman & Dicker LLP

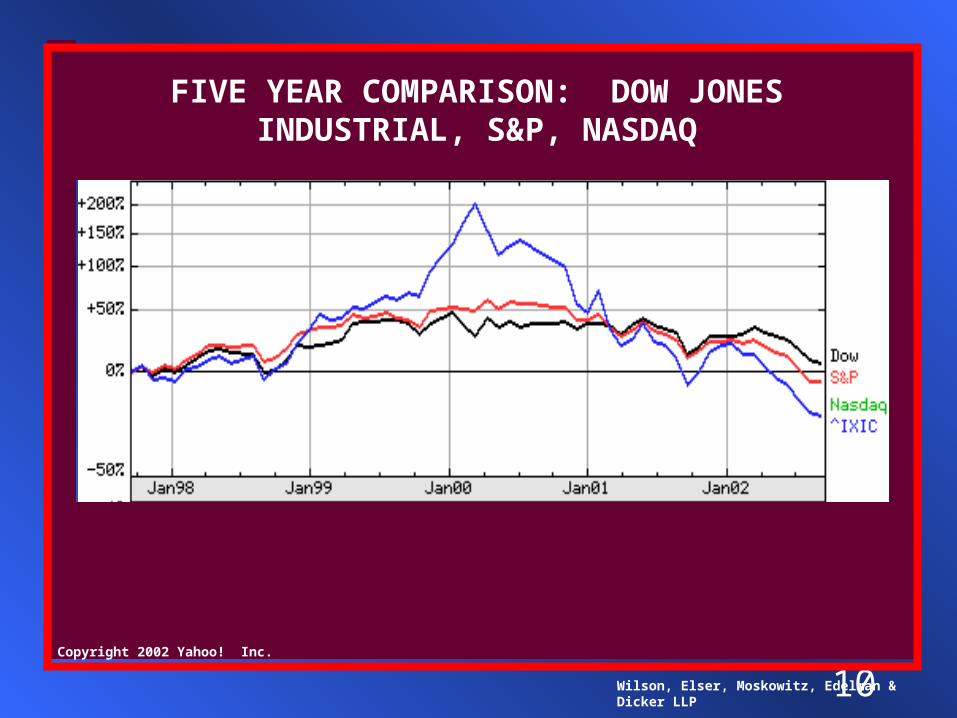

FIVE YEAR COMPARISON: DOW JONES INDUSTRIAL, S&P, NASDAQ

Copyright 2002 Yahoo! Inc.

11

COMPANIES RESTATING EARNINGS

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

2002

2001

2000

1999

1998

1997

330

207

233

216

158

116

12

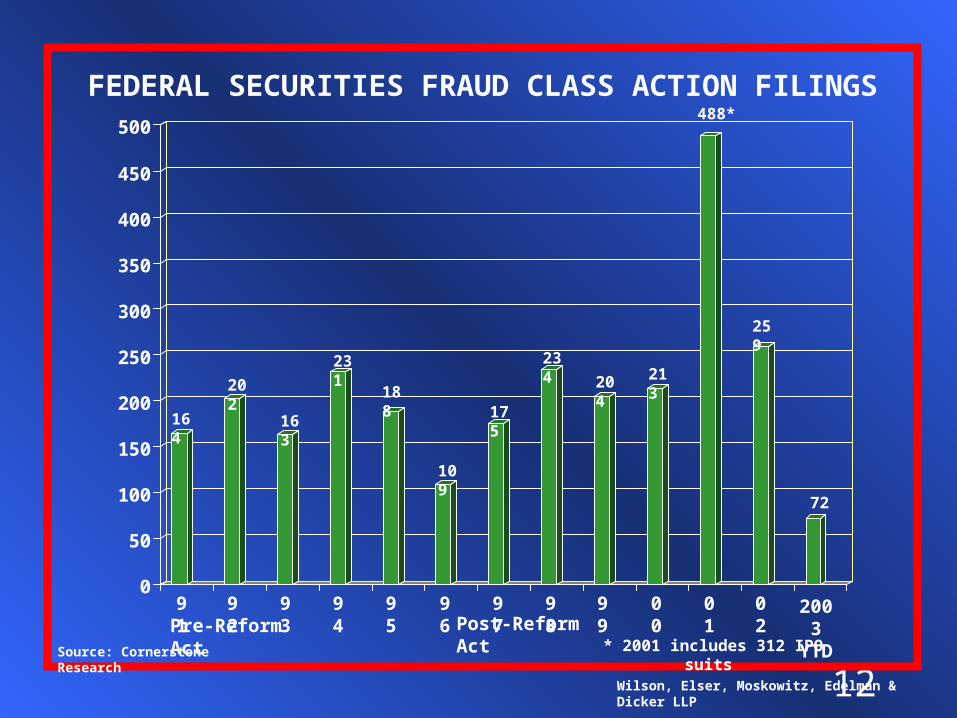

FEDERAL SECURITIES FRAUD CLASS ACTION FILINGS

0

50

100

150

200

250

300

350

400

450

500

91 92 93 94 95 96 97 98 99 00 01 02Pre-Reform Act Post-Reform Act

Source: Cornerstone Research

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

164

202

163

231

188

109

175

234

204 213

488*

259

* 2001 includes 312 IPO suits

2003YTD

72

13

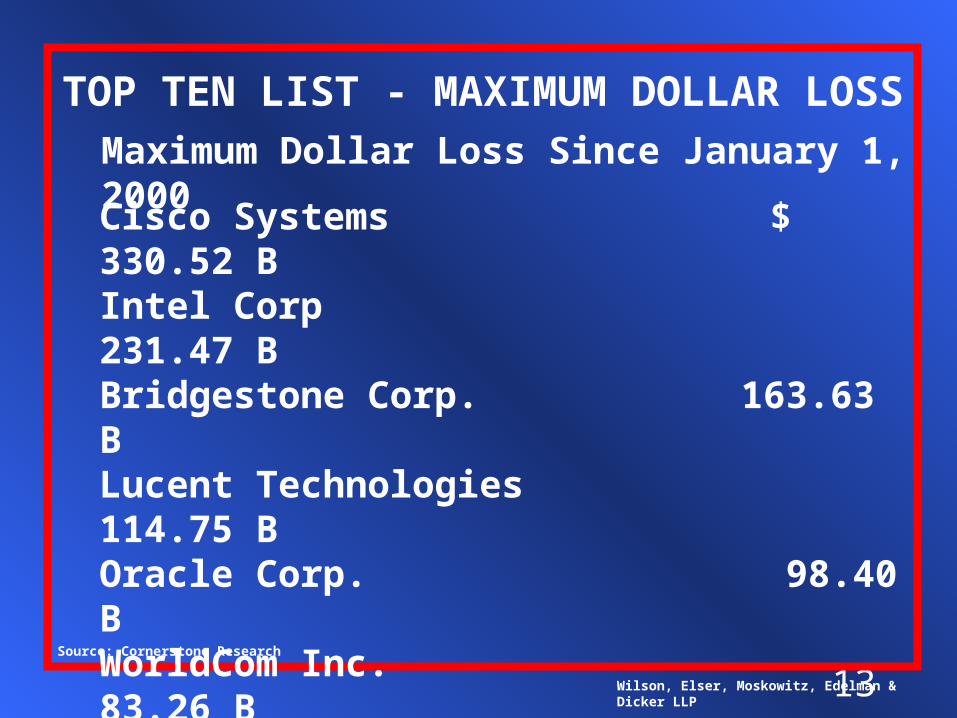

TOP TEN LIST - MAXIMUM DOLLAR LOSS

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

Maximum Dollar Loss Since January 1, 2000

Cisco Systems $ 330.52 BIntel Corp 231.47 BBridgestone Corp. 163.63 BLucent Technologies 114.75 BOracle Corp. 98.40 BWorldCom Inc. 83.26 BInternet Infrastructure 78.53 BNortel Networks Corp. 77.04 BDiamler Chrysler AG 63.35 BAT&T Corp. 61.44 B

Source: Cornerstone Research

14

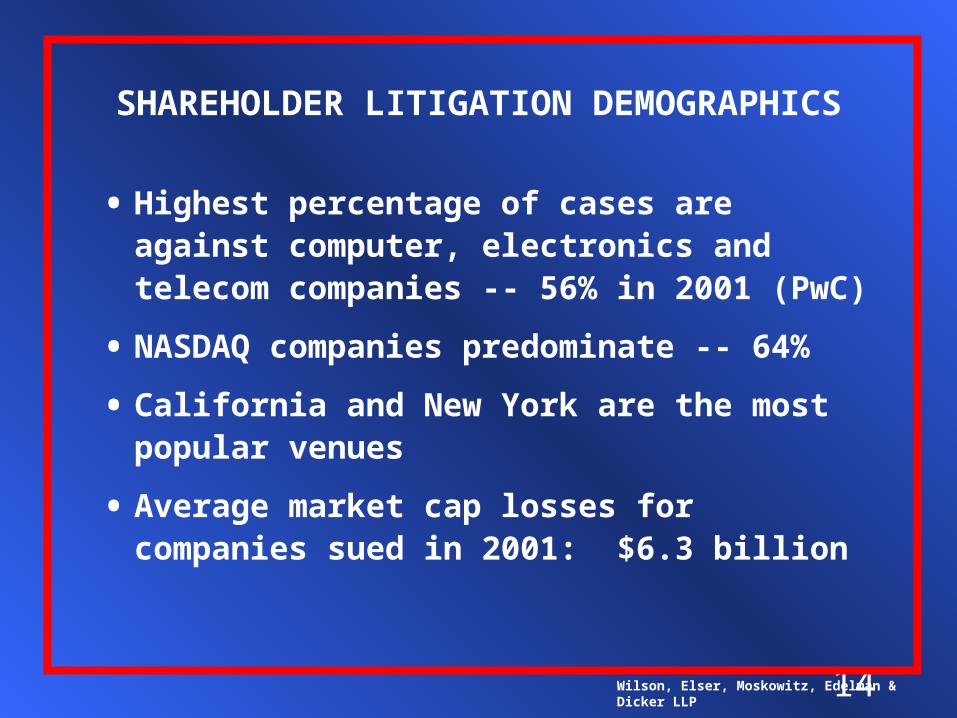

SHAREHOLDER LITIGATION DEMOGRAPHICS

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• Highest percentage of cases are against computer, electronics and telecom companies -- 56% in 2001 (PwC)

• NASDAQ companies predominate -- 64%

• California and New York are the most popular venues

• Average market cap losses for companies sued in 2001: $6.3 billion

15

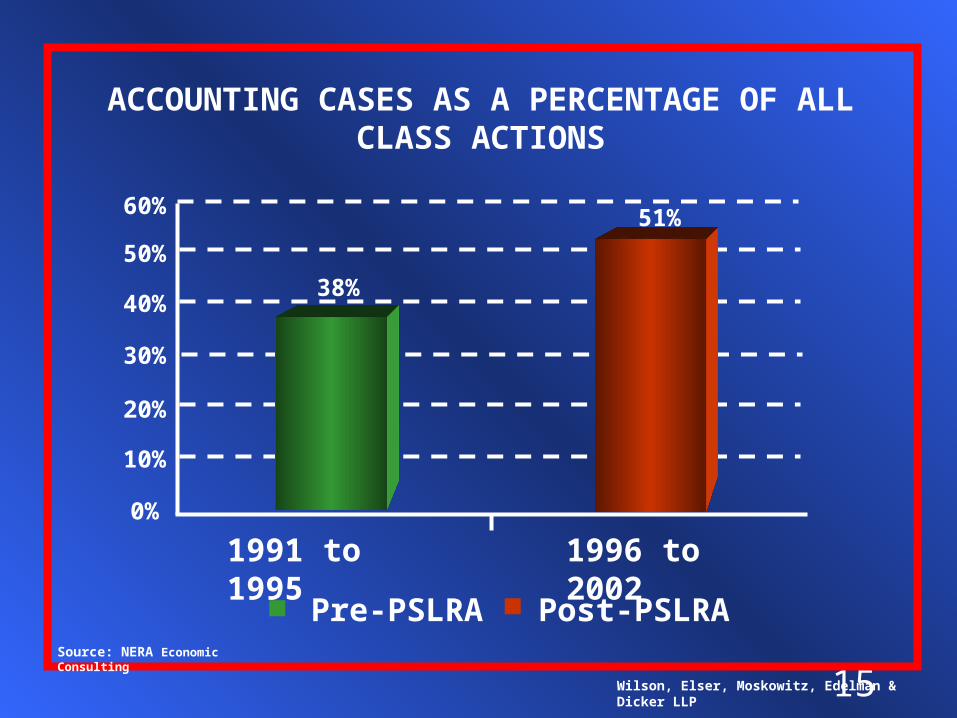

ACCOUNTING CASES AS A PERCENTAGE OF ALL CLASS ACTIONS

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

Source: NERA Economic Consulting

1991 to 1995 1996 to 2002

Pre-PSLRA Post-PSLRA

60%

0%

50%

40%

30%

20%

10%

38%

51%

16

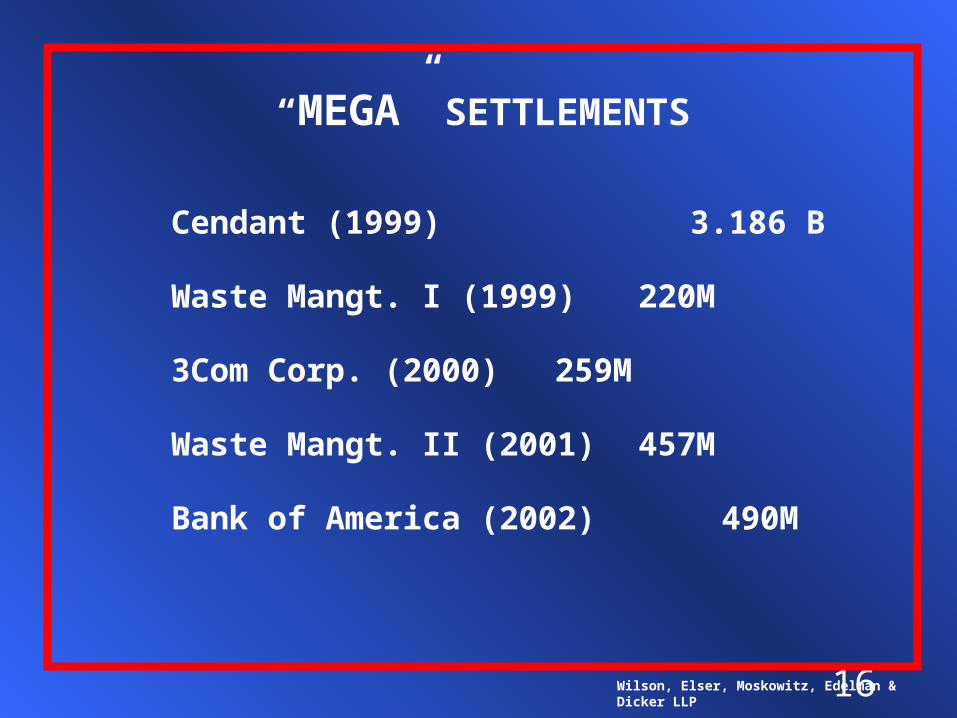

“MEGA” SETTLEMENTS

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

Cendant (1999) 3.186 B

Waste Mangt. I (1999) 220M

3Com Corp. (2000) 259M

Waste Mangt. II (2001) 457M

Bank of America (2002) 490M

17

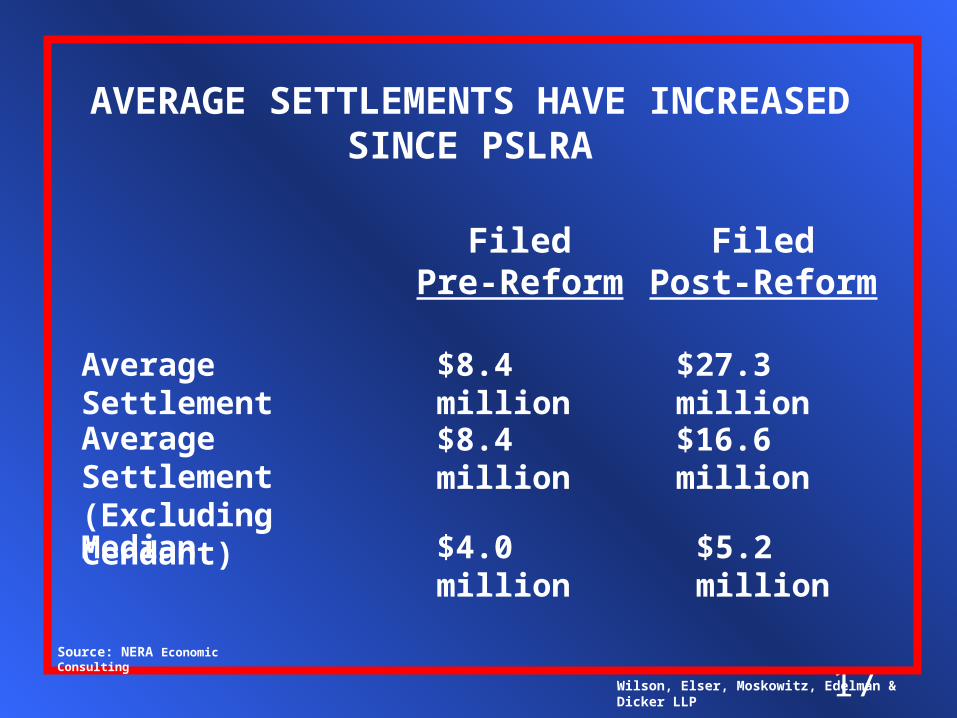

AVERAGE SETTLEMENTS HAVE INCREASED SINCE PSLRA

FiledPre-Reform

FiledPost-Reform

Average Settlement $8.4 million $27.3 million

Average Settlement(Excluding Cendant)

$8.4 million $16.6 million

Median $4.0 million $5.2 million

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

Source: NERA Economic Consulting

18

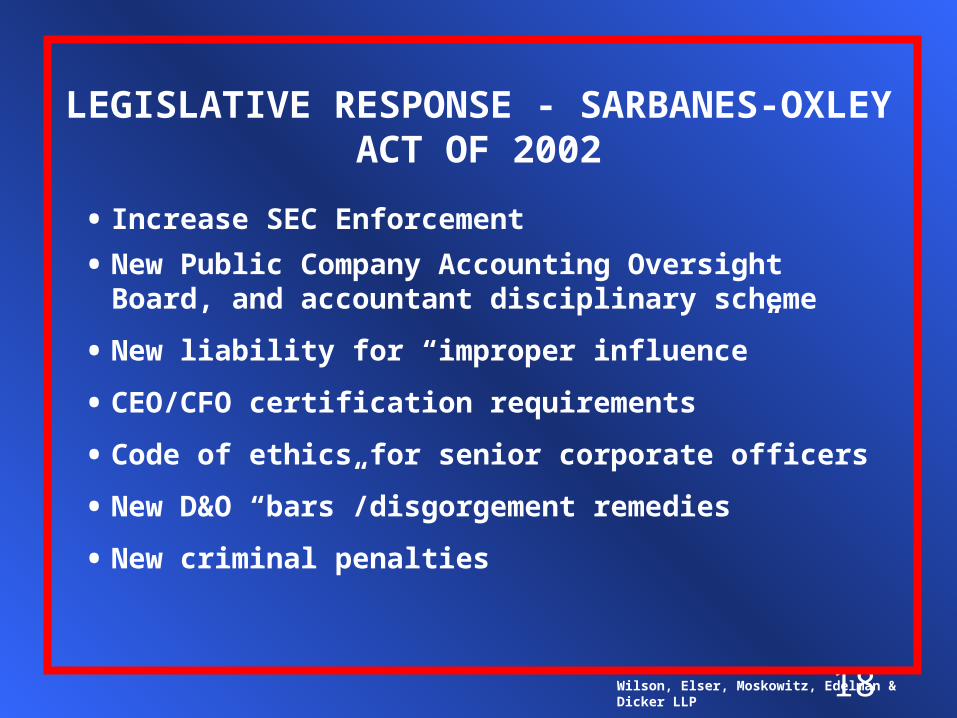

LEGISLATIVE RESPONSE - SARBANES-OXLEY ACT OF 2002

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• Increase SEC Enforcement

• New Public Company Accounting Oversight Board, and accountant disciplinary scheme

• New liability for “improper influence”

• CEO/CFO certification requirements

• Code of ethics for senior corporate officers

• New D&O “bars”/disgorgement remedies

• New criminal penalties

19Wilson, Elser, Moskowitz, Edelman & Dicker LLP

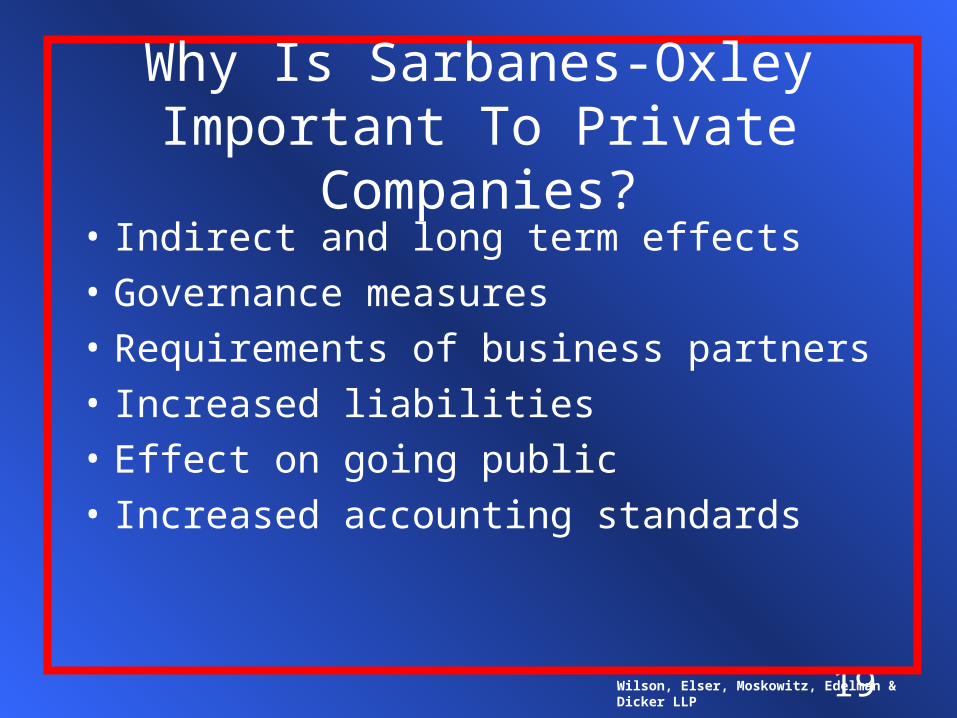

Why Is Sarbanes-Oxley Important To Private Companies?

• Indirect and long term effects

• Governance measures

• Requirements of business partners

• Increased liabilities

• Effect on going public

• Increased accounting standards

20

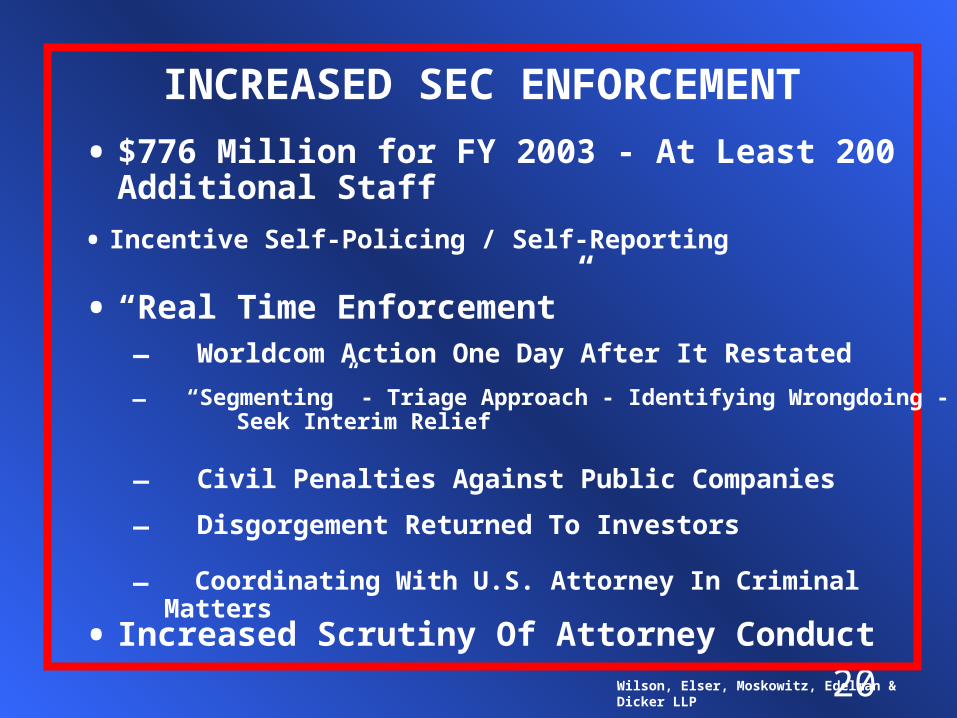

INCREASED SEC ENFORCEMENT

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• $776 Million for FY 2003 - At Least 200 Additional Staff

– Worldcom Action One Day After It Restated

• Incentive Self-Policing / Self-Reporting

• “Real Time Enforcement”

– “Segmenting” - Triage Approach - Identifying Wrongdoing - Seek Interim Relief

– Civil Penalties Against Public Companies

– Disgorgement Returned To Investors

– Coordinating With U.S. Attorney In Criminal Matters

• Increased Scrutiny Of Attorney Conduct

21

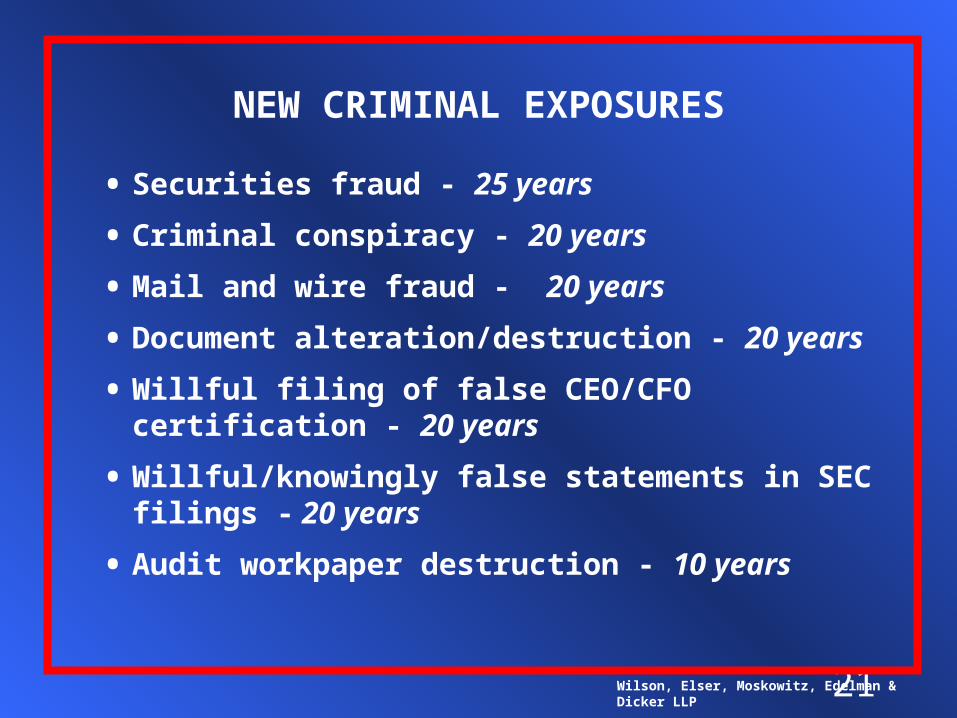

NEW CRIMINAL EXPOSURES

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• Securities fraud - 25 years

• Criminal conspiracy - 20 years

• Mail and wire fraud - 20 years

• Document alteration/destruction - 20 years

• Willful filing of false CEO/CFO certification - 20 years

• Willful/knowingly false statements in SEC filings - 20 years

• Audit workpaper destruction - 10 years

22

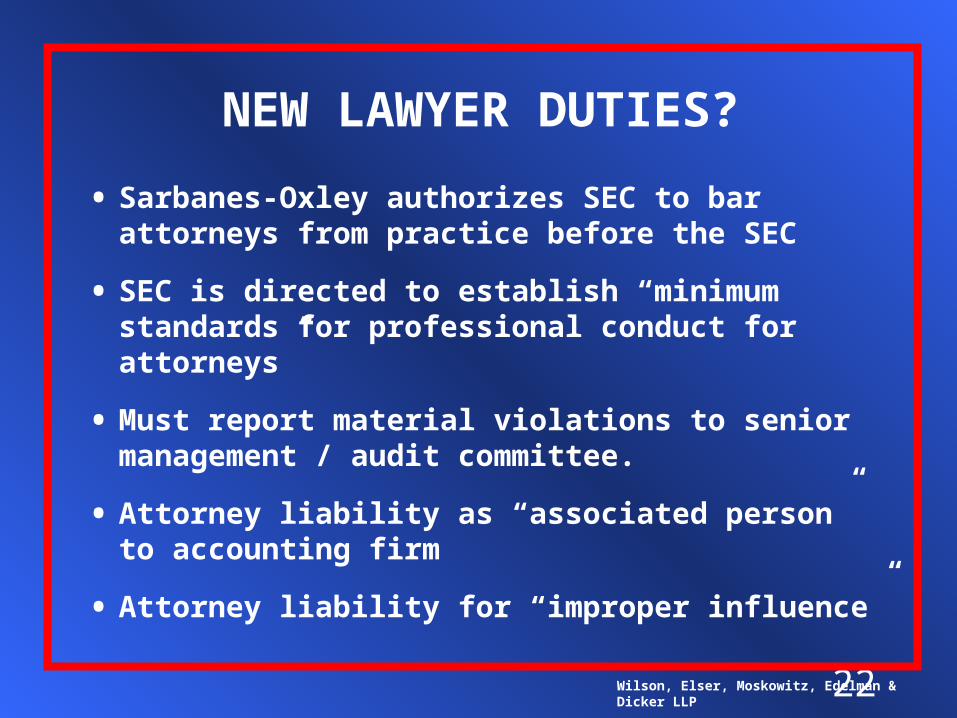

NEW LAWYER DUTIES?

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• Sarbanes-Oxley authorizes SEC to bar attorneys from practice before the SEC

• SEC is directed to establish “minimum standards for professional conduct for attorneys”

• Must report material violations to senior management / audit committee.

• Attorney liability as “associated person” to accounting firm

• Attorney liability for “improper influence”

23

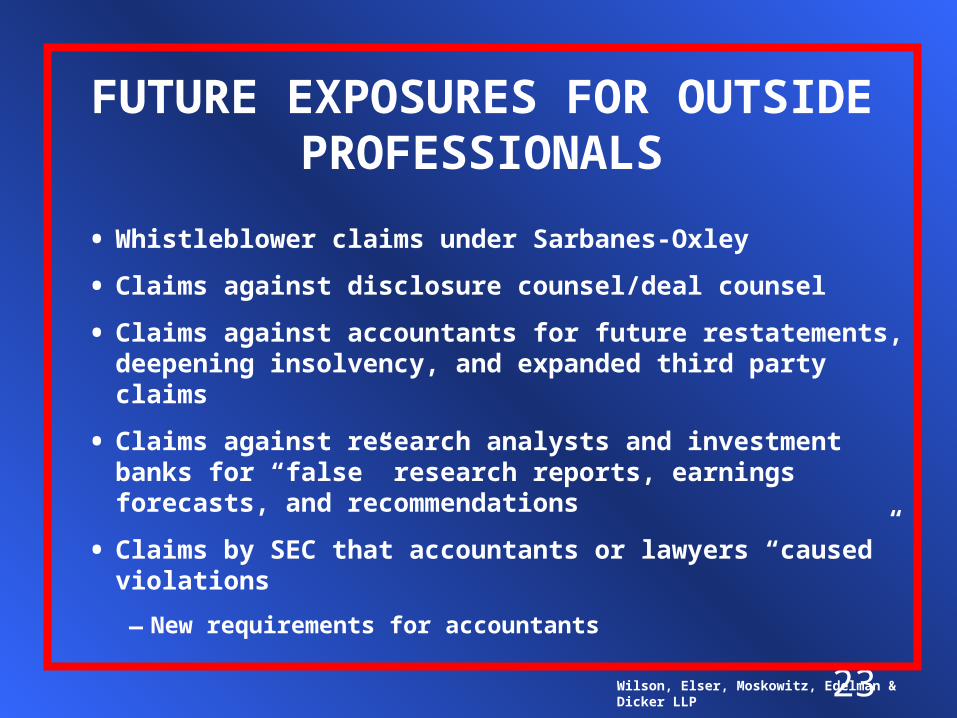

FUTURE EXPOSURES FOR OUTSIDE PROFESSIONALS

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• Whistleblower claims under Sarbanes-Oxley

• Claims against disclosure counsel/deal counsel

• Claims against accountants for future restatements, deepening insolvency, and expanded third party claims

• Claims against research analysts and investment banks for “false” research reports, earnings forecasts, and recommendations

• Claims by SEC that accountants or lawyers “caused” violations

– New requirements for accountants

24

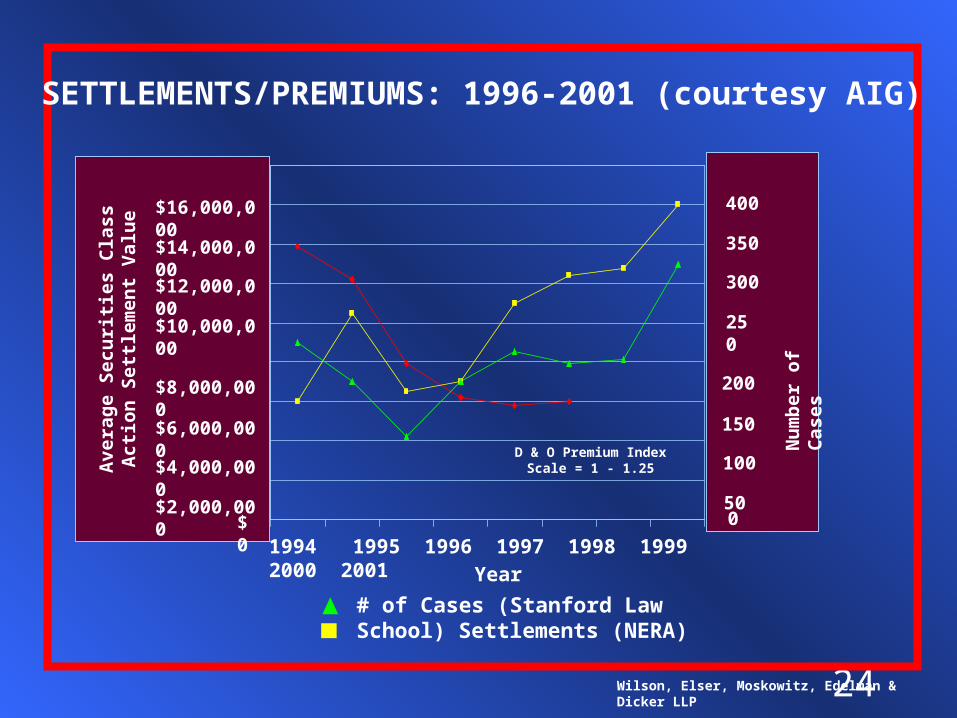

SETTLEMENTS/PREMIUMS: 1996-2001 (courtesy AIG)

Wilson, Elser, Moskowitz, Edelman & Dicker LLP

0

2

4

6

8

10

12

14

16

18

1994 1995 1996 1997 1998 1999 2000 2001

Year

400

350

300

250

200

150

100

50

0

Nu

mb

er o

f C

ases

# of Cases (Stanford Law School) Settlements (NERA)

Ave

rage

Sec

uri

ties

Cla

ss A

ctio

n

Set

tlem

ent

Val

ue

$16,000,000

$14,000,000

$12,000,000

$10,000,000

$8,000,000

$6,000,000

$4,000,000

$2,000,000

$0

D & O Premium Index Scale = 1 - 1.25

25

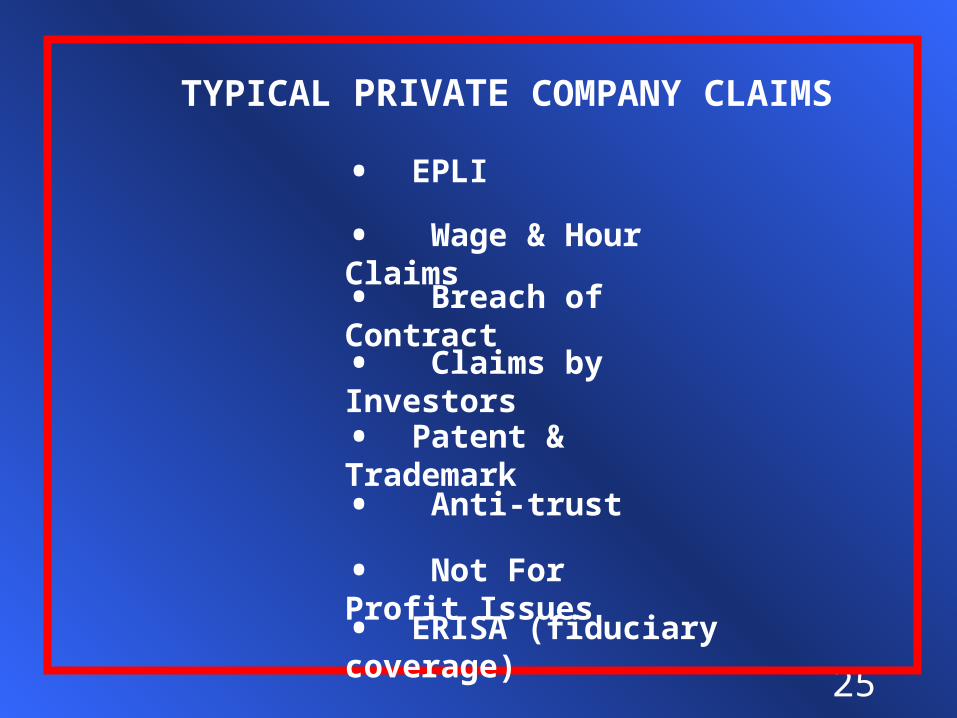

• EPLI

TYPICAL PRIVATE COMPANY CLAIMS

• Breach of Contract

• Wage & Hour Claims

• Claims by Investors

• Patent & Trademark

• Anti-trust

• ERISA (fiduciary coverage)

• Not For Profit Issues

26Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• Claims by employees that their employer has retaliated against them for whistle blowing, complaints about hostile work environment, etc.

- - specific EPLI sublimits.

- - increased Self-Insured Retention for EPL claims.

EPLI - RETALIATION

• D&O policies often are written with:

• California issues.

27Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• Certain “regulatory” type wage and hour claims may be presented directly by the insured company’s employees:

WAGE AND HOUR CLAIMS

“off the clock” - typically class actions by employees for uncompensated work, i.e., Wal-Mart, Nordstroms, etc;

Mis-classifying employees - incorrectly classifying employees as “management” to avoid paying overtime;

“Deleting” overtime - managers “deleting” overtime actually clocked by employees to contain expenses.

• D&O policies often contain an exclusion for Fair Labor Standards Act claims that will be triggered by such claims.

• D&O policy will typically contain a Regulatory Exclusion barring coverage for claims by Federal and State agencies such as the FDIC.

28Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• Typical policy language excludes Loss “based on or attributable to any actual or alleged contractual liability of the Company or any other Insured under any express contract or agreement . . .”

BREACH OF CONTRACT CLAIMS

• Most often suits are between vendor and the insured company - expressly excluded;

• Suits by D&Os for stock options - usually outside the definition of Loss, which excludes employment benefits, stock options, etc.;

• Express contractual liability generally excluded - However, liability not arising out of express contract may be specifically excepted from the exclusion.

29Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• D&O policies cover only acts by officers and directors on behalf of the corporate entity. The D&O policy does not cover wrongful acts taken to protect their personal rights and interests. Olsen v. Federal Ins. Co. (1990) 219 Cal. App. 3d 252.

CLAIMS AGAINST D&Os BY INVESTORS

• Loss within the meaning of an insurance contract does not include restoration of ill-gotten gain. Level 3 Communications, Inc. v. Federal Ins Co. (7th Cir. 2001) 272 F.3d 908 (applying Ill. Law)(amount paid by corporation to settle claim for rescission and restitution based on fraud not a covered “loss”)

30Wilson, Elser, Moskowitz, Edelman & Dicker LLP

IMPACT OF CORPORATEINSOLVENCY/BANKRUPTCY

• The duties of the D&Os run primarily to the creditors - not to the shareholders.

• When insolvency or liquidation is imminent, duties of D&Os are expanded to include fiduciary duties to creditors to protect the company’s assets from dissipation.

31Wilson, Elser, Moskowitz, Edelman & Dicker LLP

IMPACT ON CLAIMS AGAINST D&Os

• In Chapter 11 “reorganization”, the corporation becomes “Debtor-in-Possession” -- D&Os take on duties of a bankruptcy trustee with fiduciary duties to the creditors.

• In Chapter 7 “liquidation”, the bankruptcy trustee ousts existing management of the debtor. The trustee, on the estate’s behalf, may pursue claims against the D&O for breach of fiduciary duty, self-dealing, waste and gross mismanagement.

32Wilson, Elser, Moskowitz, Edelman & Dicker LLP

ACTIONS AGAINST D&Os

• Automatic stay does not apply to non-debtors, such as D&Os. Thus, insurer may pursue a coverage action against the D&Os -- as their rights under the D&O policy are not property of the estate. See: In re Pintlar Corp., 124 F.3d 1310 (9th Cir. 1997); In re Spaulding Composites Co., Inc., 207 B.R. 899 (9th Cir. 1997).

• The court can “extend” the stay to enjoin third-party actions against the D&Os. See: § 105(a); A.H. Robbins Co. Inc. V. Piccinin, 788 F.2d 994 (Dalcon Shield Litigation); In re Johns-Manville Corp., 26 B.R. 420 (Bankr. S.D.N.Y. 1983) (Asbestos Litigation).

33Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• “Estate” includes virtually any legal or equitable interest the debtor may have in tangible or intangible property, including the debtor’s insurance policies. In re Minoco Group of Companies Litd., 799 F.2d 517 (9th Cir. 1986); A.H. Robbins v. Piccinin, 788 F.2d 994 (4th Cir. 1986); Matter of Vitek Inc., 51 F.3d 550 (5th Cir. 1995).

PAYMENT OF THE D&Os’ LEGAL COSTS

• The automatic stay bars proceedings against assets of the estate.

34Wilson, Elser, Moskowitz, Edelman & Dicker LLP

Split of authority:

IS THE D&O POLICY AN ASSET OF THE BANKRUPTCY ESTATE?

• Proceeds of D&O policy not property of the estate. See: In re Louisiana World Exhibition, 832 F.2d 1391 (5th Cir. 1987) -- because the policy provided coverage only to the directors and officers and not to the debtor. See also: In re Daisy Systems, 132 B.R. 752 (N.D. Cal. 1991); David v. Gleason, 1990 WL 261364 (N.D. Cal. 1990).

35Wilson, Elser, Moskowitz, Edelman & Dicker LLP

Other courts have limited Louisiana World to its facts -- i.e., where the debtor-corporation had no interest in the policy proceeds.

See: A.H. Robbins v. Piccinin, 788 F.2d 994 (4th Cir.) cert. denied, 479 U.S. 876 (1986); In re Johns-Manville Corp, 26 B.R. 420 (S.D.N.Y. 1985); In re Sacred Heart Hosp. Of Norristown, 182 B.R. 413 (Bankr. E.D. Pa. 1995); Matter of Vitek, Inc., 51 F.3d 530, 534 n.17 (5th Cir. 1995)(limiting its holding in Louisiana World to its facts).

• Proceeds are property of the estate.

36Wilson, Elser, Moskowitz, Edelman & Dicker LLP

SEEK RELIEF FROM STAY

• Acts taken in violation of the automatic stay are void ab initio and may result in a claim for actual damages by an injured party.

• The Insurer should seek relief from the stay before paying fees, thereby avoiding a finding that it acted as volunteer - and avoid “double payment” of Loss.

• Bankruptcy Code § 362(d)(1) provides that upon motion, the court may grant relief from the automatic stay “for cause.” See: In re Sonnax Industries, Inc., 907 F.2d 1280 (2d Cir. 1990).

37Wilson, Elser, Moskowitz, Edelman & Dicker LLP

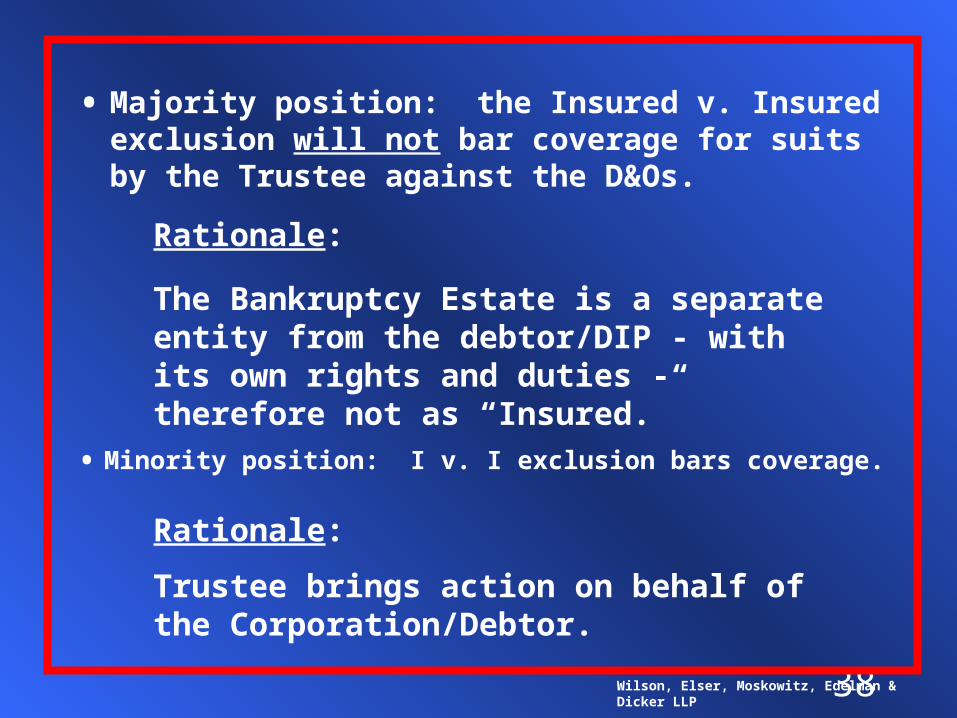

APPLICATION OF INSURED v. INSURED EXCLUSION TO CLAIMS BY THE TRUSTEE

Is an action by the Trustee against the D&Os for pre-petition claims of the estate excluded from coverage because the Trustee stands in the shoes of the corporate entity?

38Wilson, Elser, Moskowitz, Edelman & Dicker LLP

• Majority position: the Insured v. Insured exclusion will not bar coverage for suits by the Trustee against the D&Os.

The Bankruptcy Estate is a separate entity from the debtor/DIP - with its own rights and duties - therefore not as “Insured.”

Rationale:

• Minority position: I v. I exclusion bars coverage.

Rationale:

Trustee brings action on behalf of the Corporation/Debtor.

39Wilson, Elser, Moskowitz, Edelman & Dicker LLP

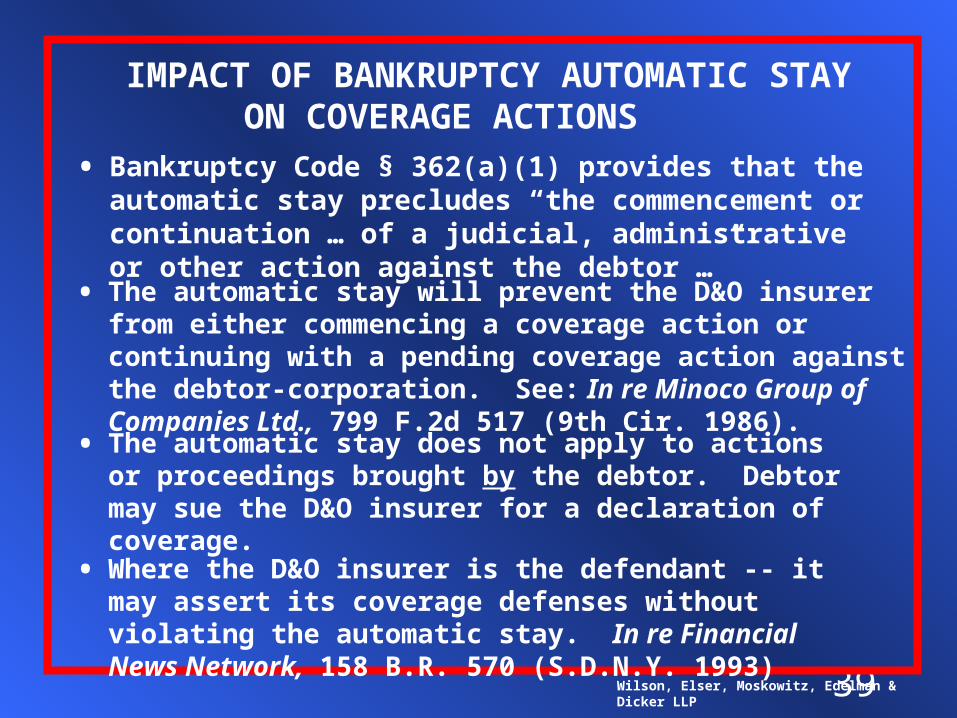

IMPACT OF BANKRUPTCY AUTOMATIC STAY ON COVERAGE ACTIONS

• Bankruptcy Code § 362(a)(1) provides that the automatic stay precludes “the commencement or continuation … of a judicial, administrative or other action against the debtor …”

• The automatic stay does not apply to actions or proceedings brought by the debtor. Debtor may sue the D&O insurer for a declaration of coverage.

• Where the D&O insurer is the defendant -- it may assert its coverage defenses without violating the automatic stay. In re Financial News Network, 158 B.R. 570 (S.D.N.Y. 1993)

• The automatic stay will prevent the D&O insurer from either commencing a coverage action or continuing with a pending coverage action against the debtor-corporation. See: In re Minoco Group of Companies Ltd., 799 F.2d 517 (9th Cir. 1986).

40

CURRENT TRENDS IN D&O

41

Privately-Held Corporations

42

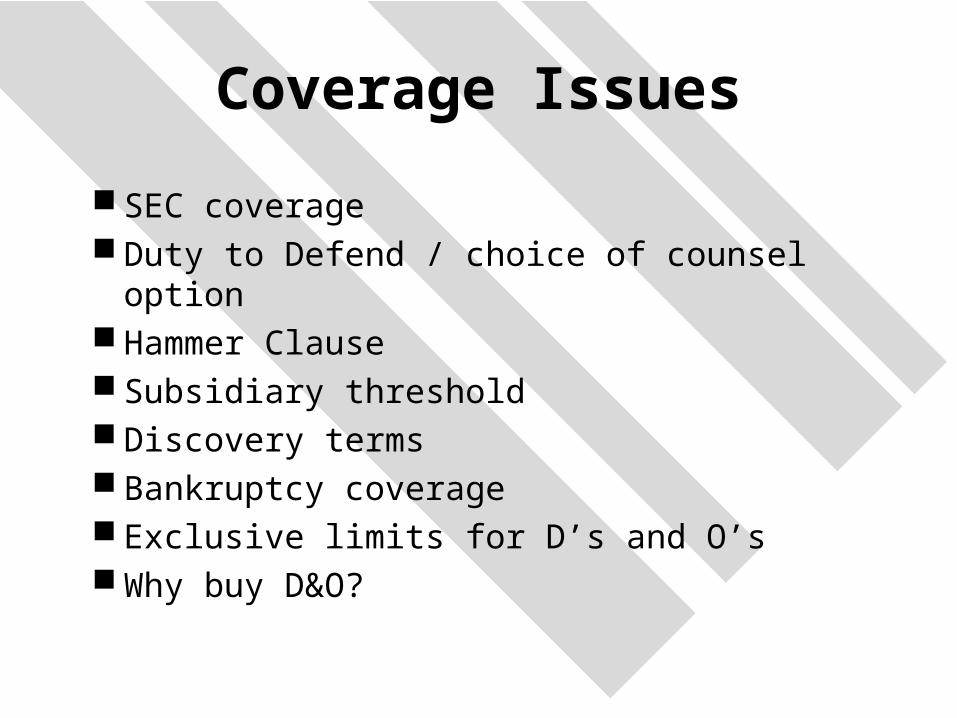

Coverage Issues

SEC coverage Duty to Defend / choice of counsel option Hammer Clause Subsidiary threshold Discovery terms Bankruptcy coverage Exclusive limits for D’s and O’s Why buy D&O?

43

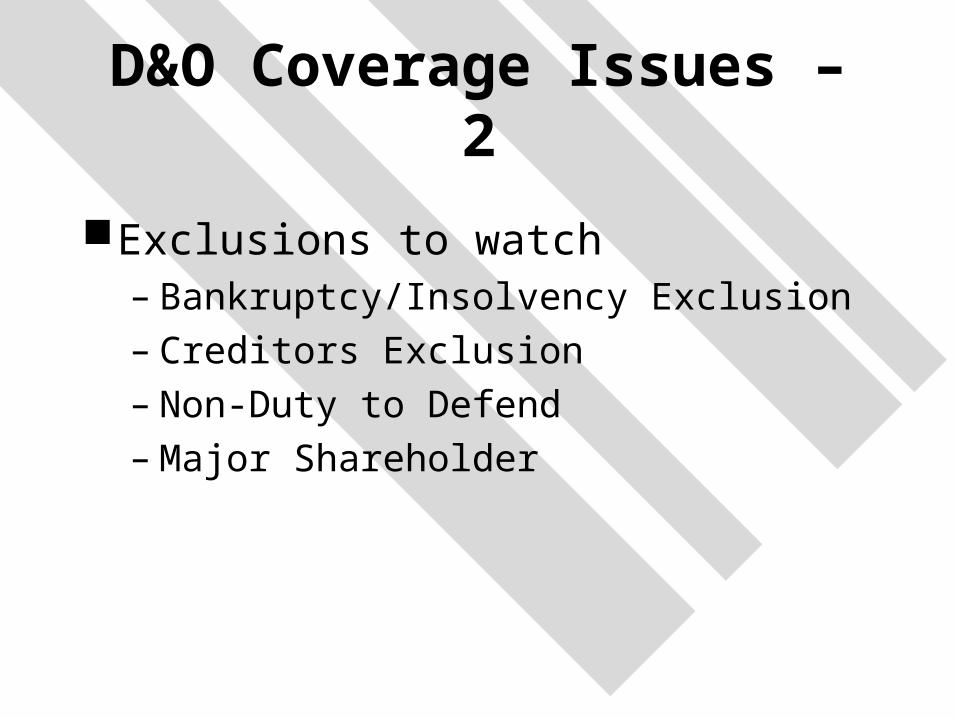

D&O Coverage Issues – 2

Exclusions to watch– Bankruptcy/Insolvency Exclusion– Creditors Exclusion– Non-Duty to Defend– Major Shareholder

44

Non-Profit Organizations

45

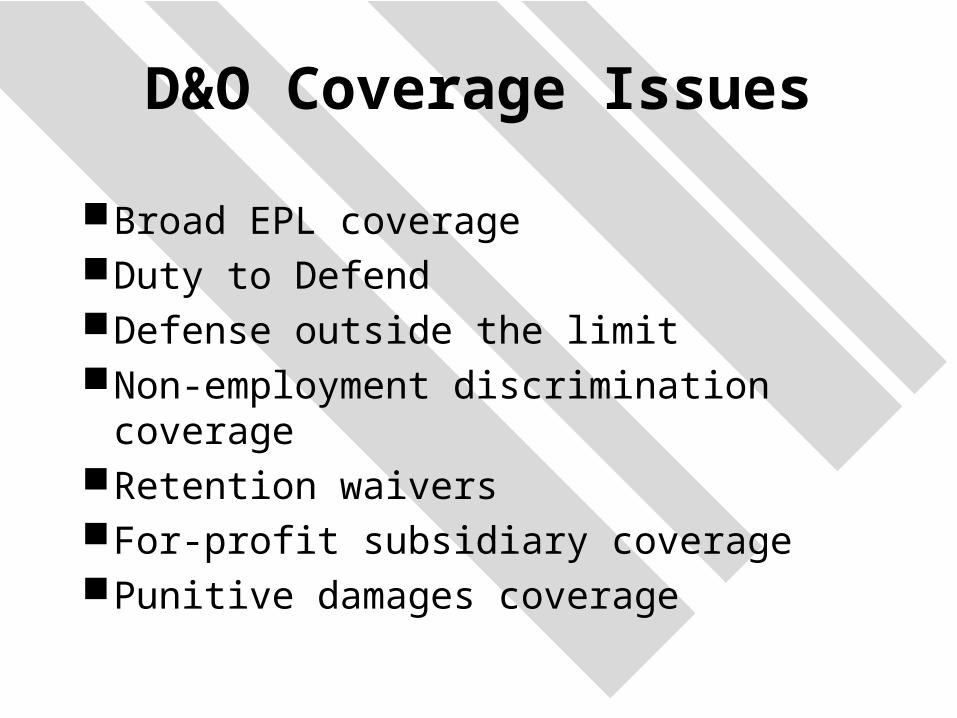

D&O Coverage Issues

Broad EPL coverageDuty to Defend Defense outside the limitNon-employment discrimination coverageRetention waiversFor-profit subsidiary coveragePunitive damages coverage

46

Managing Clients’ Expectations in a Hard Market

Meet with client early and oftenSet realistic Premium/Retention IncreasesExplain coverage changesPreserve Coverage on RenewalDiscuss challenges of “Moving” Coverage

(i.e. Continuity Issues)Explain Marketing Efforts

47

How to obtain positive D&O terms

Start EarlySubmit complete submissionUse a themeDetermine prioritiesUnderwriter meeting / conference callDon’t hide problemsEmphasize Relationships