1 crowd-financing for public-private partnerships in the u ...docs.trb.org/prp/16-6216.pdf1...

TRANSCRIPT

Crowd-financing for Public-Private Partnerships in the U.S. 1

How would it work? 2

3

4

Morteza Farajian, Ph.D. 5

Office of Transportation Public-Private Partnerships 6

600 E. Main St., Suite 2120, Richmond, VA 23219 7

Tel: 804-786-0470; Email: [email protected] 8

9

Brian Ross, MSCEE, MBA, LEED AP 10

InfraShares 11

2713 Belmont Canyon Road, Belmont CA 94002 12

Tel: 415-312-2224; Email: [email protected] 13

14

15

16

17

Word count: 6,016 words text + 4 tables/figures x 250 words (each) = 7,016 words 18

19

20

21

22

23

24

Submission date: July 31, 201525

Farajian, Ross 2

ABSTRACT 1

Public-private partnership (P3) model remains a tool that can facilitate private investment to partially 2

resolve the significant funding need for the aging infrastructure in the U.S. However, the current P3 3

model does not allow for broad based public equity investment in P3 projects. The Jumpstart Our 4

Business Startups (JOBS) Act in 2012 has led to a rapidly changing legislative and regulatory 5

environment, which provides for the ability of new ventures to raise equity and debt investment. 6

This new form of investment crowdfunding, or crowd-financing, provides flexibility for start-ups 7

to raise low cost capital from supporters of their project or business. This flexibility can also be 8

utilized to enhance the P3 model. Due to the novelty of the approach and potential impact to 9

taxpayers, a comprehensive look at the approach is needed. This paper introduces an implication 10

framework for the P3 crowd-financing model and builds on a previous paper that provided a policy 11

review on the model using a SWOT analysis. This paper also highlights similarities between 12

crowd-financing models being implemented in the real estate industry and applications to P3s, and 13

then describes the current regulatory framework for crowd-financing. An outline of how 14

crowd-financing would be implemented for P3s during procurement is provided, including 15

discussions of investment types, SEC exemptions, and crowd-financing platform interaction. 16

17

18

19

Keywords: Public-Private Partnership, Crowd-financing P3 Model, Investment Crowdfunding, 20

Direct Equity Investors, 21

22

Farajian, Ross 3

Introduction 1

2

The need to address aging infrastructure due to growing capacity demands and decreasing 3

economic competiveness is greater than ever in the United States. In fact, this need is becoming a 4

critical issue for the nation and evident in an overall grade of D+ given to American infrastructure 5

by the American Society of Civil Engineers (ASCE) (1). The question is how the needed new 6

infrastructure development and the aging infrastructure maintenance should be funded particularly 7

given U.S. government budgetary constraints and “shortages in lending capacity and more 8

stringent regulation in the banking system” (2). This question has been the core of numerous 9

academic and non-academic studies. In January 2015, President Obama introduced a $302 billion 10

proposal known as the Grow America Act to help federal agencies find new ways to increase 11

infrastructure investments by at least 35% (3). The 2015 Grow America Act, the 2014 Build America 12

Investment initiative and the 2012 Jumpstart Our Business Startups (JOBs) Act all can pave the road 13

to increase private investment in the U.S. infrastructure. 14

15

One of the tools that has been used worldwide, as well as in the U.S., to facilitate private sector 16

investment in the infrastructure is an innovative form of project delivery model which is called 17

Public-Private Partnership (P3). Over the past two decades, P3s in the U.S. have evolved 18

drastically, expanding to over thirty three U.S. states, District of Columbia and one U.S. territory 19

with various P3 approaches and enabling legislations (4). In general, most of the P3 approaches 20

have similar elements in their financial package: public funds, debt and potentially equity. Debt is 21

usually repaid through project revenues which typically come from user fees or availability 22

payments. Different forms of bonds such as Private Activity Bonds (PABs) and Qualified Public 23

Infrastructure Bonds (QPIBs), provide the opportunity for individual or institutional investors to invest 24

in the U.S. infrastructure at the debt level. 25

26

Similar to debt, equity is usually repaid through project revenues if sufficient revenue is available 27

after debt service payments. Therefore, investing at the equity level is riskier than investing at the 28

debt level, and as a result is rewarded at a higher rate of return. While the current P3 model 29

provides the opportunity for individual investors to invest in P3 projects at the municipal debt 30

level, it provides little or no opportunity for individual investors to have a direct equity investment 31

in those projects. Therefore, the current P3 model can be easily criticized since the direct equity 32

opportunity is primarily limited to large infrastructure funds and developers who usually enjoy a 33

high rate of return on their equity. It might be true that equity investment in P3 projects is risky and 34

therefore should be rewarded with a higher rate of return; however, this high rate of return can be 35

justified only if it is determined by the market based on a true interaction between supply and 36

demand. An individual investor can easily criticize the high rate of returns on equity investment in 37

P3 projects by stating that he/she would be willing to take similar risks at a lower return rate 38

compared to investment funds. The only way that this claim can be validated and the criticism can 39

be addressed is providing the equity investment opportunity to such investors. 40

41

Farajian et al. (2015) discuss policy implications of a new P3 model that uses the crowdfunding 42

concept to provide individual investors the opportunity to invest equity in P3 projects (5). Under 43

this new P3 model, part of the equity investment for a P3 project is raised from individual investors 44

(the crowd), particularly the ones in the same region or state, through a competitive process and an 45

intermediary online platform. This new form of investment crowdfunding, or crowd-financing, 46

provides flexibilities that can be utilized in delivery of P3 projects. Although Farajian et al. 47

acknowledge potential financial benefits may be gained through this new approach as a result of 48

Farajian, Ross 4

higher competition at equity level and potential lower cost of capital for equity investments, they 1

mainly focus on policy benefits such as enhanced transparency, providing equal investment 2

opportunities to local stakeholders and users of the facility, and enhanced local stakeholder 3

support. In particular, this new model provides the opportunity to extend the partnership to 4

potential users of the project or people who are impacted by the project and better align their 5

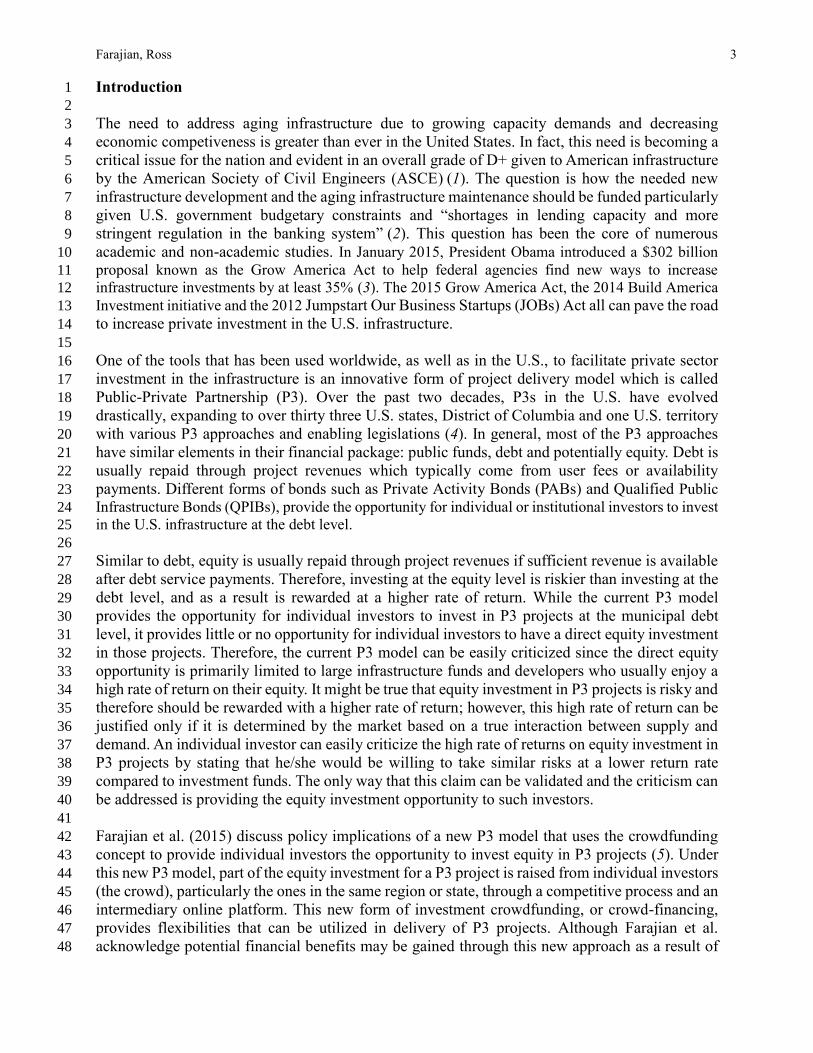

interests with the interests of the public agency and the P3 developer. Figure 1 summarizes the 6

strengths, weaknesses, opportunities and threats of this new P3 approach. 7

8

Figure 1: SWOT Analysis Summary 9

10 Source: Farajian, et al (2015) (5) 11

12

This paper is taking the discussion of the P3 crowd-financing model from the policy level to the 13

application level and intends to address the question that how this concept can be implemented in 14

practice. In particular, this paper discusses (1) precedents in real estate development for a 15

crowd-financed P3 model, (2) available options based on the JOBS Act, SEC regulations and State 16

legislations, and (3) a process to utilize the crowd-financing model in P3 procurement and post 17

procurement. 18

19

Background and Comparison to Current Applications in Real Estate 20

21

The 2012 JOBS Act made significant changes to the ways that new companies can raise capital. 22

Specifically, the JOBS Act lifted the ban on general solicitation thereby allowing, under certain 23

conditions, new companies to sell equity shares and debt instruments (collectively referred to as 24

securities) to the general public via the internet without the onerous process of registering the 25

offering with the SEC as an IPO. The ability to raise small amounts of investment from many 26

more individual investors, referred to in this paper as crowd-financing (as opposed to 27

crowd-funding which refers to raising money through donations), is typically facilitated by online 28

Equal investment opportunity Induced complexity

Return on equity Lack of track record and market confidence

Enhanced stakeholder support Administrative and accounting challenges

Increased transparency Third-party confidential information

Social equality

Strengths Weaknesses

Opportunities Threats

Prioritization Business failure

Idea exchange Fraud

Possible misconceptions

Internal in Origin

Dis

ad

van

tag

es

Ad

van

tag

es

External in Origin

Farajian, Ross 5

platforms that cater to specific industries such as information technology, health products, or real 1

estate development. Small investors who are interested in specific projects can now invest directly 2

in projects they have not been able to previously because such investment opportunities were 3

limited, statutorily and practically, to institutional investors with large sums of investment capital. 4

5

The changes implemented in the JOBS Act apply only to new business ventures, or “start-ups”. 6

Because the Special Purpose Vehicles (SPV) established by the Development Company, equity 7

sponsors, design/build firm, and O&M partners to undertake the P3 is technically a new venture, it 8

is able to take advantage of the regulations established by the JOBS Act. While crowdfunding has 9

received the most recent attention with regard to new venture capital and start-up businesses, the 10

mechanism is also gaining popularity as a tool in civic projects and real estate development 11

investments. This evolution in the use of crowdfunding demonstrates the potential of 12

crowd-financing for P3 projects (5). 13

14

Crowd-financing for a P3 would generally follow the successful model established by the 15

commercial real estate industry for crowdfunding investment in real estate development projects. 16

A recent study from Massolution reports that crowdfunding investors injected $1 billion into the 17

U.S. real estate market last year. By the end of 2015, that number is expected to climb to $2.5 18

billion (6). This empirical data illustrates that investments and operational aspects have far 19

exceeded expectations and websites such as Fundrise.com, Realtyshares.com, and 20

Realtymogul.com exemplify the various regulatory frameworks, security structures, fees, and 21

revenue models employed for crowdfunding investment in real estate, but at a fundamental level 22

the process consists of a developer offering investment in a SPV established to undertake a new 23

real estate development project that will generate returns for the investors. 24

25

Similarly in a P3 project, the P3 developer sets up a SPV and investors purchase debt or equity 26

shares in the SPV. The SPV then makes debt service payments or equity returns depending on the 27

success of the project. The key differences between a typical infrastructure P3 project and a real 28

estate development project are the associated development risks (design, construction, O&M), the 29

size of projects, the duration of projects, the types of customers (the public and public agencies), 30

and the role of public agencies in selection, oversight, and financing of projects. Just as there are 31

numerous real estate crowd-financing platforms that specialize in specific project types (retail, 32

apartments, single family residences, etc.), there is a need for crowd-financing platforms that cater 33

to the unique aspects of infrastructure as an asset class (7). 34

35

Another key difference between crowd-financing for real estate and large transportation P3s is the 36

role of debt. As discussed earlier, the debt financing in a typical transportation P3 project is 37

usually provided through various government loan programs such as the Transportation 38

Infrastructure Finance and Innovation Act (TIFIA), tax-exempt project revenue bonds such as 39

PABs, or other bonds that are offered competitively in the bond market. This reduces the need for 40

debt crowd-financing for transportation P3 projects; therefore, this paper focuses on the role of 41

equity crowd-financing used by the P3 SPV. However, if necessary or desirable, the SPV could 42

issue debt securities via crowd-financing platforms, which is common in the real estate investment 43

crowdfunding industry. Debt crowd-financing may also be appropriate for P3s in other 44

infrastructure sectors such as water/waste-water, telecoms and social infrastructure where public 45

debt facilitation is not as advantageous. 46

47

Farajian, Ross 6

Another key comparison to crowd-financing for commercial real estate is the role of pension 1

funds. While pension funds typically have a portion of their assets allocated to commercial real 2

estate, individuals with interest in a pension fund are not able to select specific projects in their 3

community that they want their specific funds to be invested in; they are subject to the investment 4

decisions of the fund managers. As with pension fund investment in infrastructure, the wishes of 5

the individual participants are not a consideration in the fund’s investment decision and therefore 6

investments through pension funds do not represent the same level of benefits that a 7

crowd-financing model can offer. For instance, pension funds do not provide the same level of 8

public engagement and support that can be gained through crowd-financing of direct equity 9

investment from individual investors who may be the users of the project or live close to the 10

project. 11

12

Furthermore, pension funds do not provide the same level of transparency and ongoing 13

engagement that investors will receive as direct equity participants through crowd-financing. 14

Also, the competitive crowd-financing process provides a great opportunity to make the rate of 15

return on equity investment more competitive by offering it to qualified individuals in the same 16

way that bonds are offered in the bond market. Finally, the returns offered to investors through 17

pension funds may be mitigated by management fees and limited project selection due to the 18

Employee Retirement Income Security Act of 1974 (ERISA) restrictions. 19

20

However, while inclusion of pension funds as equity participants in a P3 does not provide the same 21

level of public engagement or economic impact as crowd-financing equity from individuals, 22

pension funds do play a critical role in private investment in public infrastructure and P3s. 23

Because pension funds often desire the long-term, stable, inflation hedged returns of infrastructure 24

assets, they are a natural fit as equity sponsors of P3s and frequent investors in infrastructure funds 25

that participate in P3s. Unfortunately, because the investment thresholds for direct investment in 26

P3s and infrastructure funds can be quite high, typically over $1 million, many smaller pension 27

funds are unable to participate. Crowd-financing for P3s, and potentially infrastructure funds, will 28

allow smaller, local funds to participate alongside individuals and large institutional investors, 29

providing more competitive and resilient sources of equity. 30

31

Initiating Crowd-financing for a P3 32

33

In real estate development crowdfunding, the crowdfunding campaign is initiated by the real estate 34

developer. However, in a P3, the crowd-financing process could be initiated by either the P3 35

developer or the public agency sponsor. P3 developer partners are typically selected by the public 36

agency partner through a competitive RFQ/RFP process. The public agency may include a 37

requirement or preference for some portion of the capital to be raised through crowd-financing in 38

the RFQ/RFP documents. If the evaluation is based on a minimum price that as long as all 39

requirements are met, the lowest bid is selected, a minimum amount to be crowd-financed can be 40

required by the public agency in the procurement document. Under the best value evaluation 41

approach in which a combination of technical and financial scores is used to select the proposal, 42

the public agency can develop scoring criteria for the value placed on the type, or amount, of 43

crowdfunded capital offered to the public. Similar to how points are awarded to innovative design, 44

points could be awarded for innovative financing structures that include community investment. 45

As an example, the City of Oakland recently released a Request for Proposals for the 46

redevelopment of the Henry J. Kaiser Convention Center that included the following language (8): 47

Farajian, Ross 7

1

“Community-based Financing Tools: The City is interested in exploring the viability of new 2

community-based financing models that allow Oakland residents of all income and wealth levels 3

to participate in the profits generated by becoming investors in the project. To the degree possible, 4

and to the degree it is feasible in combination with other financing mechanisms, respondents 5

should consider using community-based financing tools such as community development IPOs or 6

other innovative community financing tools and platforms.” 7

8

In general, less prescriptive requirements allow the developers to become more innovative and 9

compete in terms of public benefit or cost reduction. Theoretically, crowd-financing could provide 10

a lower cost of capital, so developers that propose the largest offering could also potentially 11

provide the best value for money (this needs to be explored further). However, if the P3 developer 12

wishes to limit crowd-financing participation due to lack of overall financial benefits in particular 13

cases but the public agency still believes crowd-financing provides non-financial benefits to the 14

public, a policy decision can be made to mandate a minimum amount of equity to be 15

crowd-financed. Similarly, the public agency can mandate a ceiling on the maximum amount of 16

equity that can be crowd-financed. It is unlikely that equity crowd-financing will replace entirely 17

traditional P3 equity sources such as private sponsor equity (developer/EPC partner), insurance 18

companies, pension funds, and infra funds, but putting a ceiling on the percentage of equity that 19

can be raised through crowd-financing ensures the developer still has enough equity stake “skin in 20

the game” incentivizing its performance. This is necessary to ensure the P3 developer is 21

incentivized to utilize its resources in the most efficient way to increase performance and mitigate 22

the risk of default or bankruptcy. Ultimately, rating agencies would also consider this element as 23

one of their evaluation criteria while providing a rating on debt. 24

25

The crowd-financing process could also be executed as an auction for particular projects, allowing 26

for investors to bid on securities and letting the market establish the risk weighted returns 27

appropriate for the project instead of a limited number of institutional equity sponsors (9). On the 28

other hand, the public agency may decide to define more restrictive terms of the offering to 29

mitigate the potential political risk of riskier crowd-financing offerings. 30

31

Alternatively, the P3 developer may include crowd-financing as part of their proposal without any 32

specific requirement from the public agency; particularly in unsolicited proposals. The P3 33

developer may recognize the benefit of public engagement that crowdfunding offers and highlight 34

it as part of their unsolicited proposal to increase public engagement and transparency in hopes of 35

reducing the chance of political resistance associated with unsolicited proposals. 36

37

In all these scenarios, the P3 developer (and possibly the public agency) may engage in a “testing 38

the waters” campaign by providing preliminary information via the crowdfunding platform and 39

soliciting non-binding indications of investment interest from the public. Strong indications of 40

interest may signal strong public support for the project, as well as financial viability. Investors 41

who indicate interest could be contacted prior to the general public once the actual offering is 42

executed. However, “testing the waters” campaigns need to adhere to strict SEC regulations to 43

avoid market tampering (see discussion of Regulation A+ offerings below). 44

45

Regardless of the amount to be offered via crowd-financing, the P3 developer needs to retain 46

responsibility for obtaining the necessary rating and securing financing for the project. The risk on 47

Farajian, Ross 8

assumptions related to rate of return will stay with the P3 developer although some benchmarking 1

protections can be provided by the public agency to mitigate risks associated with market 2

conditions similar to risk protections provided on interest assumed in debt financing. If the P3 3

developer is unsuccessful in raising the planned crowd-financed amount, either it can increase the 4

internal rate of return on crowd-financed portion of the equity to attract more investors or back-fill 5

the gap. In either case since the P3 developer has the responsibility to deliver the proposed 6

financial package, the weighted average cost of equity should stay the same. This means the P3 7

developer will need to reduce the internal rate of return on the other portion of equity which is not 8

crowd-financed. 9

10

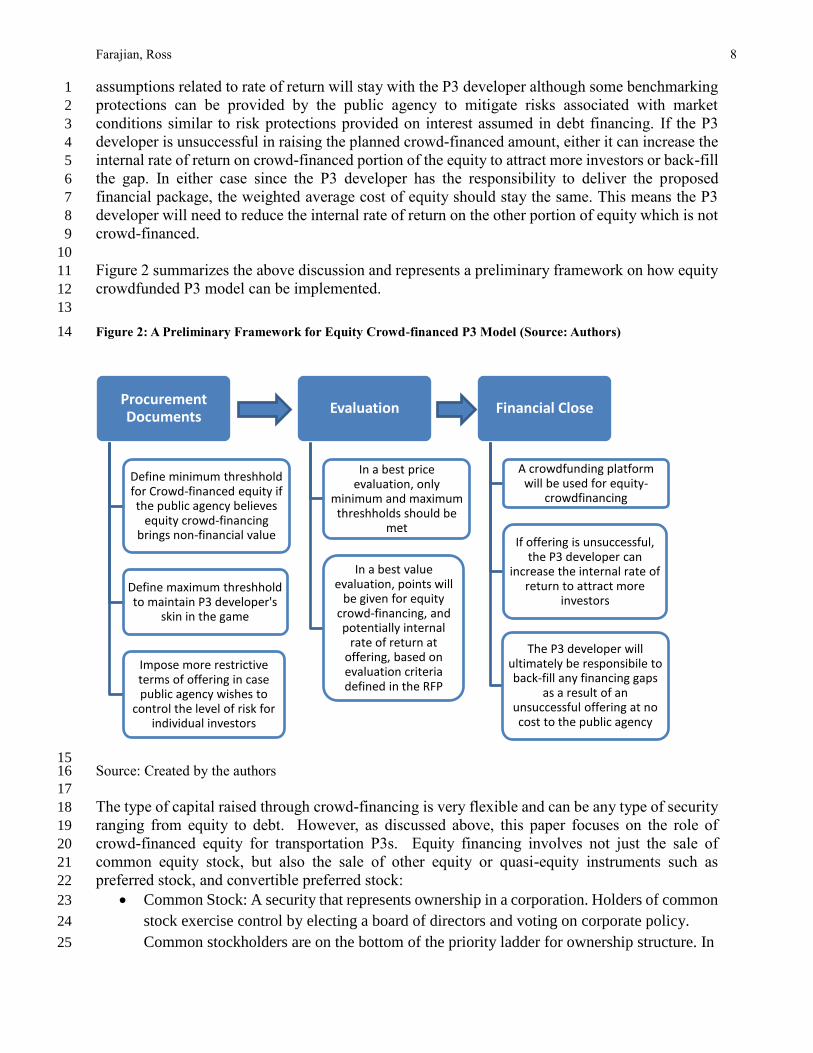

Figure 2 summarizes the above discussion and represents a preliminary framework on how equity 11

crowdfunded P3 model can be implemented. 12

13

Figure 2: A Preliminary Framework for Equity Crowd-financed P3 Model (Source: Authors) 14

15 Source: Created by the authors 16

17

The type of capital raised through crowd-financing is very flexible and can be any type of security 18

ranging from equity to debt. However, as discussed above, this paper focuses on the role of 19

crowd-financed equity for transportation P3s. Equity financing involves not just the sale of 20

common equity stock, but also the sale of other equity or quasi-equity instruments such as 21

preferred stock, and convertible preferred stock: 22

Common Stock: A security that represents ownership in a corporation. Holders of common 23

stock exercise control by electing a board of directors and voting on corporate policy. 24

Common stockholders are on the bottom of the priority ladder for ownership structure. In 25

Procurement Documents

Define minimum threshhold for Crowd-financed equity if the public agency believes

equity crowd-financing brings non-financial value

Define maximum threshhold to maintain P3 developer's

skin in the game

Impose more restrictive terms of offering in case public agency wishes to

control the level of risk for individual investors

Evaluation

In a best price evaluation, only

minimum and maximum threshholds should be

met

In a best value evaluation, points will

be given for equity crowd-financing, and potentially internal

rate of return at offering, based on evaluation criteria defined in the RFP

Financial Close

A crowdfunding platform will be used for equity-

crowdfinancing

If offering is unsuccessful, the P3 developer can

increase the internal rate of return to attract more

investors

The P3 developer will ultimately be responsibile to back-fill any financing gaps

as a result of an unsuccessful offering at no cost to the public agency

Farajian, Ross 9

the event of liquidation, common shareholders have rights to a company's assets only after 1

bondholders, preferred shareholders and other debtholders have been paid in full. 2

Preferred Stock: A class of ownership in a corporation that has a higher claim on the assets 3

and earnings than common stock. Preferred stock generally has a dividend that must be 4

paid out before dividends to common stockholders (preferred return) and the shares usually 5

do not have voting rights. The precise detail as to the structure of preferred stock is specific 6

to each corporation. However, the best way to think of preferred stock is as a financial 7

instrument that has characteristics of both debt (fixed dividends) and equity (potential 8

appreciation). Also known as "preferred shares". 9

Convertible Preferred Stock: Preferred stock that includes an option for the holder to 10

convert the preferred shares into a fixed number of common shares, usually any time after 11

a predetermined date. 12

The type of equity offered could depend on several factors including: investor demand, 13

developer’s determination of the most cost efficient structure, and possibly on the desires of the 14

public agency as outlined in the RFP. However, given that the P3 developer will want to limit the 15

crowd investors involvement in operations (voting rights), and that the public agency will most 16

likely want to shield community investors from severe underperformance of the project 17

(construction risk, ramp-up risk, economic downturn, T&R shortfalls, etc.), preferred stock is the 18

most likely security to be offered. However, preferred stock will naturally offer lower equity 19

returns than common stock. 20

21

The P3 developer will also be responsible for providing the offering documentation required by the 22

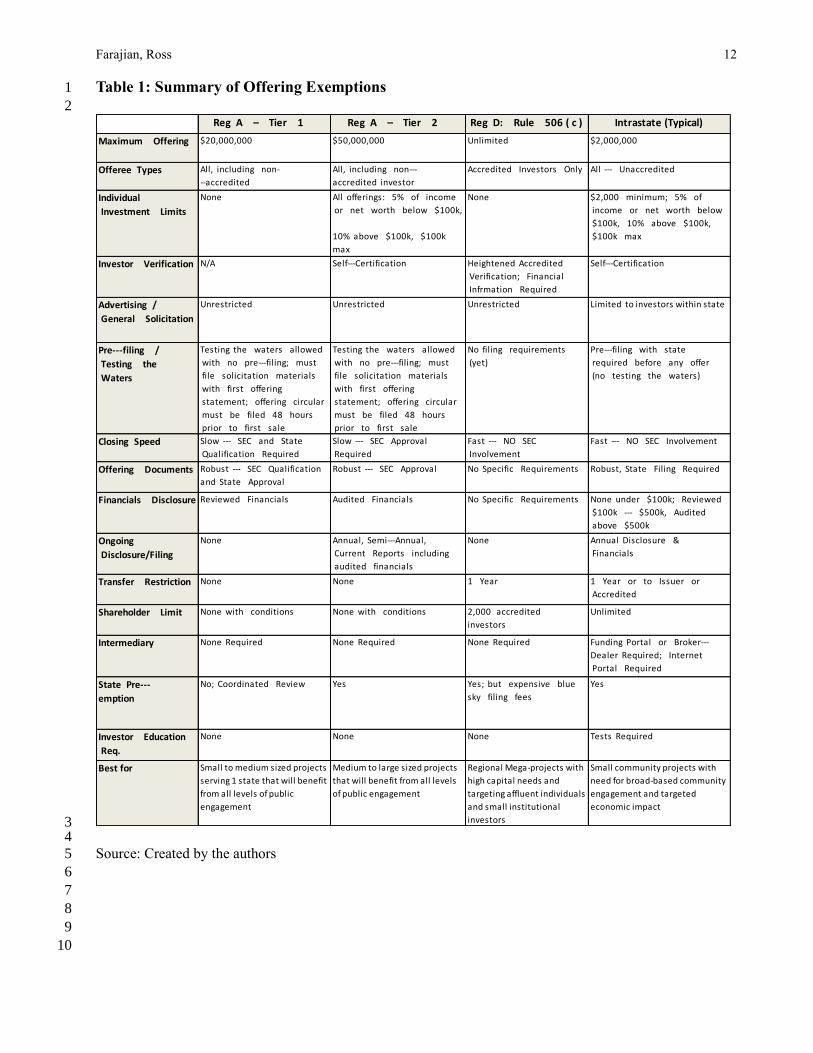

SEC filing exemption being used (e.g. 506(c), Regulation A+, Rule 147, etc. as discussed below). 23

The SEC filing exemption will depend on the capital needs of the developer, the level of 24

community investment required by the public agency, and the nature of the project. The SEC has 25

finalized rule-making on Title II and Title IV of the JOBS Act, enabling Regulation D 506(c) and 26

Regulation A+ offerings. Many states have also enacted “intrastate” crowdfunding regulations 27

which operate under the Rule 147 intrastate offering exemption. 28

29

30

Crowdfunding Regulations and Types of Offering Registration Exemptions 31

32

Regulation 506(c) 33

34

For Regulation D 506(c) general solicitation offerings enabled by the 2012 JOBS Act, the primary 35

benefit is that the amount of capital that can be raised is unlimited (10). 506(c) offerings are the 36

main SEC crowdfunding exemption currently used by commercial real estate crowdfunding 37

platforms, with multiple projects raising over $50 million dollars (11). In addition to being exempt 38

from SEC registration, 506(c) offerings are exempt from state securities registration as well (Blue 39

Sky exemption). Because 506(c) offerings are the most common, there are numerous service 40

providers that facilitate the legal process for low fees. 41

42

Drawbacks to the use of 506(c) offerings include a limit of 2000 investors, and the investors must 43

be accredited (12). This limits participation to investors that have a net worth over $1 million, or 44

made over $200,000 per year in gross income in both of the prior two years (10). An accredited 45

Farajian, Ross 10

investor may also be an entity such as a bank, partnership, corporation, nonprofit or trust, when the 1

entity satisfies certain criteria. Also, the securities sold through 506(c) offerings are restricted 2

from being resold for one year, except under special circumstances, which make them highly 3

illiquid. 4

5

Because of the opportunity for large capital raises, but the restriction to accredited investors, 6

506(c) offerings are best suited for large regional mega-projects that may serve multiple states 7

(power generation, toll roads, oil & gas, etc.). These projects will typically require larger capital 8

raises and will have a risk/return profile more suitable for accredited investors. 9

10

Regulation A+ 11

12

Regulation A+ exempt offering rules were finalized by the SEC in June 2015 and are currently 13

allowed for implementation. Reg A+ offerings are split into two tiers of offering with the ability to 14

raise up to $20 million under tier 1 offerings and $50 million for tier 2 offerings (13). While the 15

amount that can be raised is limited, unlike 506(c) offerings, Regulation A+ offerings are open to 16

both accredited and unaccredited investors; with certain restriction on unaccredited investors for 17

tier 2 offerings. Another benefit of Regulation A+ offerings is that the securities sold are 18

un-restricted, meaning they can be sold at will by the investors; this adds liquidity to the securities 19

making them more valuable to short-term investors. Regulation A+ also allows for “test the 20

waters” campaigns that allow developers to gauge interest in a potential offering prior to any filing 21

with the SEC. 22

23

Because Regulation A+ offerings are open to all investors, the SEC requires that tier 1 offerings 24

are qualified within each state where securities will be sold. Because each state has different 25

securities regulations (Blue Sky Laws), this requirement makes it impractical for Regulation A+ 26

tier 1 offerings to be sold in more than just a few targeted states. Unlike 506(c) offerings, most 27

Regulation A+ offerings will require that investors are provided annual reviewed or audited 28

financial statements by the P3 SPV. While most intrastate offering regulations (discussed below) 29

also allow for accredited and unaccredited investors, intrastate offerings typically require the 30

offeror to be located in the state of the offering and have much lower limits for amounts that can be 31

raised. Another benefit of regulation A+ offerings is that they can be combined with 506(c) 32

offerings. 33

34

Rule 147 - Intrastate Crowdfunding 35

36

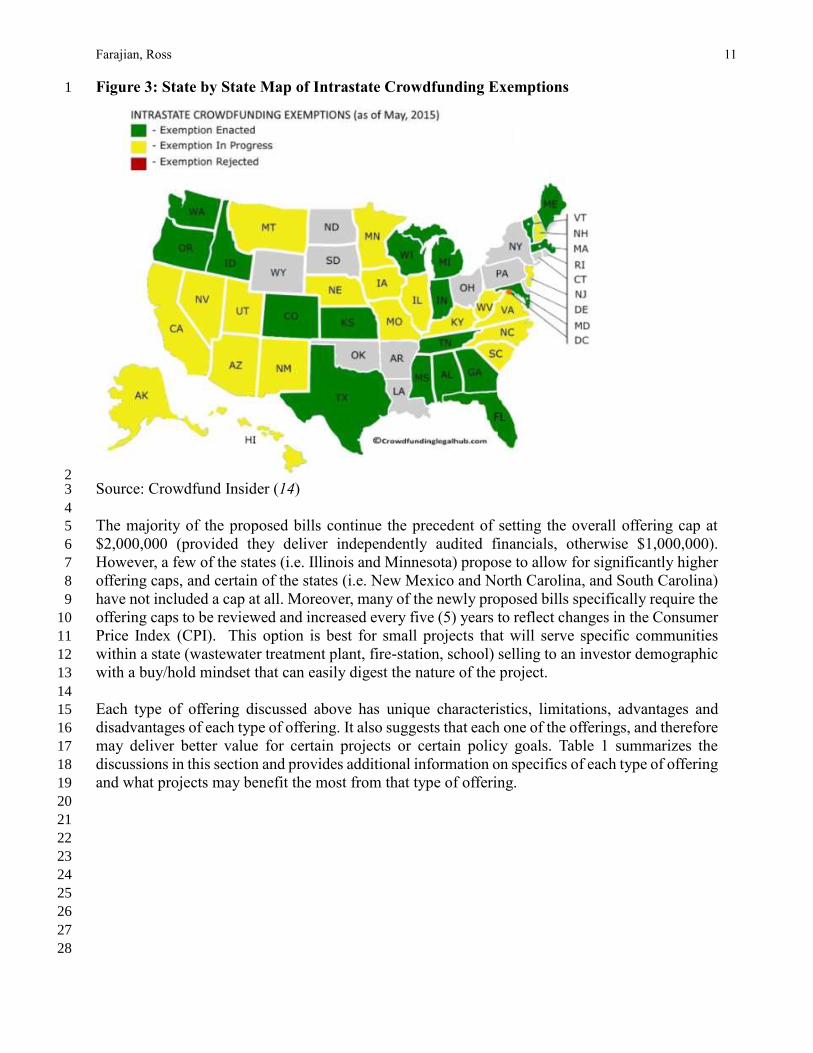

Not wanting to wait for full the SEC to finalize Title III of the JOBS Act, several states have passed 37

intrastate crowdfunding laws to allow for businesses that operate solely in their state to raise 38

crowdfunded capital from any local (residents of the state) investors (14). States active in 39

transportation P3s such as Florida, Texas, Georgia, Colorado and Indiana have all passed intrastate 40

crowdfunding legislation, while many other states are in the process of passing legislation or 41

investing (see Figure 3 below). 42

43

44

45

46

47

Farajian, Ross 11

Figure 3: State by State Map of Intrastate Crowdfunding Exemptions 1

2 Source: Crowdfund Insider (14) 3

4

The majority of the proposed bills continue the precedent of setting the overall offering cap at 5

$2,000,000 (provided they deliver independently audited financials, otherwise $1,000,000). 6

However, a few of the states (i.e. Illinois and Minnesota) propose to allow for significantly higher 7

offering caps, and certain of the states (i.e. New Mexico and North Carolina, and South Carolina) 8

have not included a cap at all. Moreover, many of the newly proposed bills specifically require the 9

offering caps to be reviewed and increased every five (5) years to reflect changes in the Consumer 10

Price Index (CPI). This option is best for small projects that will serve specific communities 11

within a state (wastewater treatment plant, fire-station, school) selling to an investor demographic 12

with a buy/hold mindset that can easily digest the nature of the project. 13

14

Each type of offering discussed above has unique characteristics, limitations, advantages and 15

disadvantages of each type of offering. It also suggests that each one of the offerings, and therefore 16

may deliver better value for certain projects or certain policy goals. Table 1 summarizes the 17

discussions in this section and provides additional information on specifics of each type of offering 18

and what projects may benefit the most from that type of offering. 19

20

21

22

23

24

25

26

27

28

Farajian, Ross 12

Table 1: Summary of Offering Exemptions 1

2

3 4

Source: Created by the authors 5

6

7

8

9

10

Reg A – Tier 1 Reg A – Tier 2 Reg D: Rule 506 ( c ) Intrastate (Typical)

Maximum Offering

$20,000,000 $50,000,000 Unlimited $2,000,000

Offeree Types All, including non-

‐accredited

investor

All, including non‐‐‐

accredited investor

Accredited Investors Only

All ‐‐‐ Unaccredited

Individual

Investment Limits

None All offerings: 5% of income

or net worth below $100k,

10% above $100k, $100k

max

None $2,000 minimum; 5% of

income or net worth below

$100k, 10% above $100k,

$100k max

Investor Verification

N/A Self‐‐‐Certification Heightened Accredited

Verification; Financial

Infrmation Required

Self‐‐‐Certification

Advertising /

General Solicitation

Unrestricted Unrestricted Unrestricted Limited to investors within state

Pre-‐filing /

Testing the

Waters

Testing the waters allowed

with no pre‐‐‐filing; must

file solicitation materials

with first offering

statement; offering circular

must be filed 48 hours

prior to first sale

Testing the waters allowed

with no pre‐‐‐filing; must

file solicitation materials

with first offering

statement; offering circular

must be filed 48 hours

prior to first sale

No filing requirements

(yet)

Pre‐‐‐filing with state

required before any offer

(no testing the waters)

Closing Speed Slow ‐‐‐ SEC and State

Qualification Required

Slow ‐‐‐ SEC Approval

Required

Fast ‐‐‐ NO SEC

Involvement

Fast ‐‐‐ NO SEC Involvement

Offering Documents

Robust -‐ SEC Qualification

and State Approval

Robust ‐‐‐ SEC Approval No Specific Requirements Robust, State Filing Required

Financials Disclosure

Reviewed Financials Audited Financials No Specific Requirements None under $100k; Reviewed

$100k ‐‐‐ $500k, Audited

above $500k

Ongoing

Disclosure/Filing

None Annual, Semi‐‐‐Annual,

Current Reports including

audited financials

None Annual Disclosure &

Financials

Transfer Restriction

None None 1 Year 1 Year or to Issuer or

Accredited

Shareholder Limit None with conditions None with conditions 2,000 accredited

investors

Unlimited

Intermediary None Required None Required None Required Funding Portal or Broker‐‐‐

Dealer Required; Internet

Portal Required

State Pre‐‐‐

emption

No; Coordinated Review Yes Yes; but expensive blue

sky filing fees

Yes

Investor Education

Req.

None None None Tests Required

Best for Small to medium sized projects

serving 1 state that will benefit

from all levels of public

engagement

Medium to large sized projects

that will benefit from all levels

of public engagement

Regional Mega-projects with

high capital needs and

targeting affluent individuals

and small institutional

investors

Small community projects with

need for broad-based community

engagement and targeted

economic impact

Farajian, Ross 13

The Crowdfunding Campaign and Internet Platform Function 1

2

In terms of timing, the crowdfunding campaign will begin once the P3 project has been awarded 3

and the P3 terms are agreed to (commercial close). Then the private developer works with a 4

crowdfunding platform, such as www.infrashares.com, that specializes in crowdfunding 5

investment for P3s to develop and run the crowdfunding campaign (15) The length of the 6

campaign is determined by the financial close schedule, but will need to be long enough for the 7

developer to promote the project and for investors to evaluate and make an investment decision. 8

9

Retail investor traffic is driven to the crowdfunding platform through the use of public agency 10

outreach, social media, traditional media, search engine optimization (SEO, google AdWords) and 11

complimentary sites such as other investment crowdfunding sites targeting other industries. A 12

teaser summary is posted on the site that can be viewed by potential investors that includes 13

summary commercial terms and a video describing the project. Investors visiting the site can 14

browse by project type, geography, security type, IRR, etc. to find an offering that fits their 15

investment objectives. The site will also offer comparison and analysis tools to help investors 16

determine which projects are right for them. If an investor is interested in a specific project, then 17

they request access to the full offering materials such as offering statements, financial models, 18

concession agreements, credit rating agency reviews, etc. 19

20

If, after reviewing the offering documents and performing any other due diligence, they decide to 21

invest, they make a pledge to invest upon successful completion of the campaign. Campaigns are 22

considered successful if they reach the funding goal determined by the P3 developer. However, 23

the crowdfunding platform may retain the option to backfill any shortfall with its own funds. As 24

discussed earlier, since the P3 developer financing plan shouldn’t be structured to be dependent on 25

the crowd-financing campaign, an unsuccessful campaign does not, in anyway, jeopardize 26

reaching financial close. Under this scenario the P3 developer should readily have access to equity 27

which should backfill the gap at no additional cost to the public agency (under certain 28

circumstances the public agency may choose to develop a risk sharing mechanism). 29

30

In order to make management of the crowd-financed equity investors as easy as possible for the P3 31

developers, the crowdfunding platform forms a discrete project fund LLC for each offering to act 32

as intermediary between the P3 developer and the crowd investors. The project fund LLC acts on 33

behalf of the crowd investors when dealing with the P3 developers in issues such as voting rights, 34

management and consent, if granted. If a board seat is warranted, the platform management will 35

represent the LLC. In general, the crowd investors will be passive investors in the project fund 36

LLC, but the details of this relationship will vary by project. All disclosures, reports, financial 37

statements issued by the P3 developer are distributed through the platform project fund LLC to 38

investors. Third party escrow/ACH services (as required by the SEC) are used to facilitate the 39

collection of investment monies and disbursement of returns. This structure removes P3 40

developers concerns regarding management of multitudes of individual investors. 41

42

In order to facilitate this structure, the P3 developer enters into a private placement agreement with 43

the project fund LLC, whereupon success of the crowdfunding campaign, securities of the P3 44

operating company are purchased from the P3 developer by the project fund LLC. The project 45

fund LLC then subsequently issues securities of its ownership to the crowd investors through a 46

506c, Regulation A+ or intrastate offering. The project fund LLC securities are backed by the 47

Farajian, Ross 14

performance of the P3 project. This is the structure used by many of the commercial real estate 1

crowdfunding sites1. 2

3

In addition to mitigating P3 developer concern over crowd investor management, the project fund 4

LLC structure allows the P3 developer to avoid any SEC registration or navigation of 5

crowdfunding regulation. SEC compliance is left to the experts at the platform who can leverage 6

technology and industry acumen to manage the mechanics of the fund as efficiently as possible. 7

Because of the rapid growth of the crowdfunding industry, there has been a proliferation of 8

white-label providers that offer SEC filing, accreditation, escrow, payment distribution, document 9

management, signature, and Customer Relationship manager (CRM) services. These vendors are 10

offering commodity services that allow the platform to drive operational expenses very low 11

relative to what a P3 developer would have to expend on their own. 12

13

Post Financial Close 14

15

Following investment and financial close of the P3, the crowdfunding platform will act as an 16

ongoing engagement tool for the investors. The platform will distribute all financial statements, 17

disclosures and construction/O&M updates issued by the SPV. The platform will also facilitate all 18

disbursements of returns to investors and allow investors to track the performance of their 19

individual investments or portfolio of projects. Any secondary market for existing securities will 20

also be facilitated by the platform allowing investors to buy and sell securities as their individual 21

liquidity needs require. This ongoing interaction between investors and the P3 project provides 22

high levels of transparency and public oversight, making sure the developers incentives are 23

aligned with crowd-financed investors over the long-term. 24

25

Disclosure documents that would be publicly accessible on the crowdfunding platform for 26

interested investors may include: the project risk register; all publicly available procurement 27

documents; any available Public Offering Statement or Official Statement for bonds; contract 28

agreement documents; and project studies, such as ridership or traffic and revenue studies. After an 29

investment is made, updated documents, audited financial statements, quarterly progress reports or 30

any other relevant documentation would also be provided to equity shareholders to give them 31

necessary information to evaluate the performance of their investment. 32

33

Summary of Discussions and Future Research Need 34

35

The goal of the crowd-financed P3 model is to facilitate involvement of the public, especially local 36

communities, as a major partner in the current P3 model. In addition, aligning the interest of P3 37

developer, public agency and the crowd-financed equity investors who may be the users of the 38

project or local stakeholders impacted by the project can act as catalyst to facilitate delivery of the 39

project. This engagement provides the opportunity to use the interests and power of the crowd to 40

bring down the investment barrier under the current P3 model and create opportunities for 41

additional transparency and enhanced public engagement in the policy decisions. 42

43

This paper explains how the crowd-financed P3 model can be implemented in practice. The 44

lessons from utilizing crowdfunding in civic projects and commercial real estate can be used to 45

1 See Fundrise “Project Dependent Notes”:

https://fundrise.desk.com/customer/portal/articles/1596433-what-is-a-project-payment-dependent-note-.

Farajian, Ross 15

design an implementation framework for the crowd-financed P3 model. Based on policy goals, 1

project characteristics and market conditions different provisions can be added to procurement 2

documents to define the rules around this implementation framework. Those provisions should 3

instruct the P3 developers on how crowdfunding can be used in their financial proposals. The 4

detail of those provisions and potential risk sharing mechanisms that can be utilized under the 5

crowd-financed P3 model to achieve certain policy objectives can be the subject of future research 6

studies. 7

8

In summary, the benefits of the crowd-financed P3 model and its readiness to be implemented 9

make it an attractive topic both for public agencies and P3 developers. However, additional 10

research is still needed to further study the implication of the crowd-financed P3 model, 11

particularly to provide more information on popularity of the crowd-financed P3 model among 12

individual investors and their appetite for infrastructure investing. Also, additional data on rate of 13

the return that those individual investors may demand and a comparison against what investment 14

funds or institutional investors demand will better enable decision makers to evaluate financial 15

benefits of the crowd-financed P3 model. 16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

Farajian, Ross 16

References: 1

2

1. American Society of Civil Engineers. (2013). Report Card for America’s Infrastructure 3

2. McKinsey Global Institute. (2013). Infrastructure productivity: How to save $1 trillion a 4

year. Mckinsey and Company 5

3. Dynan, K. (2015, January 16). Build America Investment Initiative- Expanding 6

Opportunities to Invest in America's Infrastructure. Retrieved on July 20, 2015 from U.S. 7

Department of the Treasury: 8

http://www.treasury.gov/connect/blog/Pages/Build-America-Investment-Initiative---Expa9

nding-Opportunities-to-Invest-in-America%E2%80%99s-Infrastructure.aspx 10

4. Federal Highway Administration (2015). State P3 Legislation. Retrieved on July 20, 2015 11

from http://www.fhwa.dot.gov/ipd/p3/state_legislation/ 12

5. Farajian, M., Lauzon, A., Cui,Q. (2015) An Introduction to a Crowdfunded Public-Private 13

Partnership Model in the U.S.: A Policy Review on Crowdfund Investing.Transportation 14

Research Record Journal 15

6. Massolution (2015). 2015CF-RE Crowdfunding for Real Estate 16

http://reports.crowdsourcing.org/index.php?route=product/product&product_id=54 17

7. Ross, B. (2015, January 27). Opportunities for Crowdfunding in the P3 Industry. Retrieved 18

July 27, 2015, from InfraShares: www.infrashares.com 19

8. City of Oakland (2014, September 22). Request for Proposals. Retrieved July 27, 2015, 20

from 21

http://www2.oaklandnet.com/oakca1/groups/ceda/documents/webcontent/oak049322.pdf 22

9. Masscatalyst. (2015). Price Discovery with our Auction Market Platform. Retrieved on 23

July 26, 2015 from https://www.masscatalyst.com/how-it-works/auction 24

10. U.S. Securities and Exchange Commission. (2013, September 22). Eliminating the 25

Prohibition Against General Solicitation and General Advertising in Rule 506 and Rule 26

144A Offering. Retrieved on July 27, 2015 from 27

https://www.sec.gov/info/smallbus/secg/general-solicitation-small-entity-compliance-gui28

de.htm 29

11. Drake, D. (2014, November 4). Five Realty Crowdfunding Projects Raising $50M Or 30

More. Retrieved on July 26, 2015 from 31

http://www.forbes.com/sites/groupthink/2014/11/04/five-realty-crowdfunding-projects-ra32

ising-50m-or-more/ 33

12. Levine, M. L., & Feigin, P. A. (2014). Crowdfunding Provisions under the New Rule 34

506(c): New Opportunities for Real Estate Capital Formation. The CPA Journal, 46-51. 35

13. Bergman, M. H. (2014). SEC Proposes rules to update regulation A. Insights; the 36

Corporate & Securities Law Advisor, 32-35. 37

14. Zeoli, A. (2015, May 7). State of the States: An Update On Interstate 38

Crowdfunding.Retrieved on July 27, 2015 from 39

http://www.crowdfundinsider.com/2015/05/67394-state-of-the-states-an-update-on-intrast40

ate-crowdfunding-2/ 41

15. Cho, A. (2015, April 20). Entrepreneurs Hope To Bring Crowdfunding To P3 Projects. 42

Engineering News-Record, pp. 22-23. 43

44