1 corporate governance: impact and enforcement by stijn claessens world bank (based on joint work...

TRANSCRIPT

1

Corporate Governance: Impact and Enforcement

By

Stijn ClaessensWorld Bank

(Based on joint work with Erik Bërglof, SITE/SSE)

For Corporate Governance Leadership Program

July 14, Washington, D.C.

World Bank

2

Why does corporate governance matter for growth and development?

1. Increased access to financing investment, growth, employment

2. Lower cost of capital and higher valuation investment, growth

3. Better operational performance better allocation of resources, better management, creates wealth

4. Better relationship with stakeholders environment, social/labor relationships

5. All of it matters for growth, employment, poverty• Empirical evidence has documented these relationships at Empirical evidence has documented these relationships at

the level of country, sector and individual firm and from the level of country, sector and individual firm and from investor perspective using various techniquesinvestor perspective using various techniques

3

Access to financing

• Countries with better property rights, especially better creditor rights and shareholder rights, have deeper and more developed banking and capital markets

• In these countries, firms have greater access to financing, and as a consequence, firms invest more, grow faster. E.g., difference between Quartile 1 and Quartile 3 in financial development has been found to be 1 - 1.5 percentage points extra GDP growth per annum

• Poor corporate governance (and underdeveloped financial and legal systems and higher corruption) means firm growth of smallest firms is most adversely affected and less new, and particularly small firms, start up

4

Access to financing: creditor rights and rule of law

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1 2 3 4

Creditor Rights * Rule of Law

Depth of the financial system

5

Access to financing: quality of shareholder protection

0

10

20

30

40

50

60

70

80

Market capitalization/GDPpercent

Lowest quartile(lowest ranking in shareholder and rule of law)

Highest quartile(highest ranking in shareholder and rule of law)

Degree of capital m

arket development

6

Cost of capital and valuation

• Corporate governance affects cost of capital and valuation

– Cost of capital higher and valuation lower in weaker property rights countries

– Outsiders less willing to provide financing, voting premium higher in lower corporate governance countries, investors apply discount for worse corporate governance firms and countries (e.g., McKinsey survey)

• Conflicts between small and large shareholders greater in weaker corporate governance settings

– Conflicts between control and ownership rights, leading to higher cost of capital/lower valuation, greater in weaker property rights countries, less investment

7

Weak corporate governance translates into higher cost of capital

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

1 2 3 4 5 6

Equity Rights

Med

ian

Vot

ing

Pre

miu

m

Excludes Brazil

8

Firms’ operational performance

• Better corporate governance improves performance – Evidence for US and elsewhere suggests strongly that better

corporate governance leads not only to improved rates on equity and higher valuation, but also to higher profits and sales growth, more capital expenditures, etc.

• Operational performance is also better, but not so clearly – Although access to financing better and valuation higher, effects of

governance on performance less pronounced– Other factors likely affect operational performance: firms may face

better growth opportunities; a reporting bias• Still, rates on return on investment exceed cost of capital only in best

corporate governance countries

9

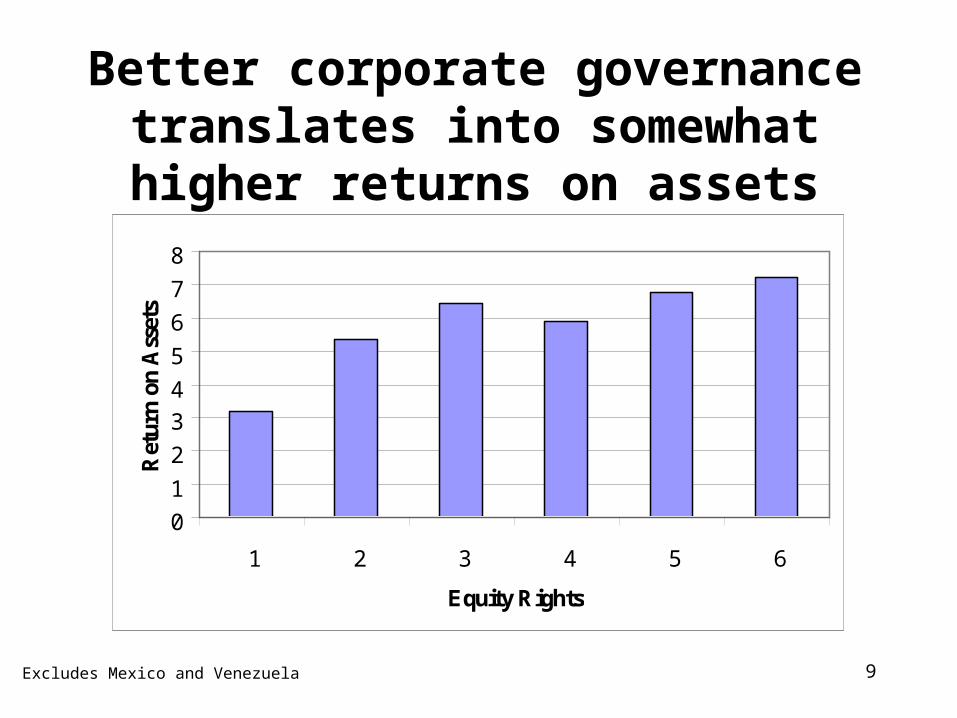

Better corporate governance translates into somewhat higher returns on assets

0

1

2

3

4

5

6

7

8

1 2 3 4 5 6

Equity Rights

Ret

urn

on A

sset

s

Excludes Mexico and Venezuela

10

But much better higher returns on investment relative to cost of capital

0.5

0.6

0.7

0.8

0.9

1

1.1

1 2 3 4 5 6

Equity Rights

Ret

urn

on

In

vest

men

t re

lati

ve t

o C

osts

of

Cap

ital

11

Other stakeholders

• Besides principal (owner), public and private corporations face many other stakeholders: banks, bondholders, labour, etc.– Each will monitor, discipline, motivate and affect the

management/firm, in exchange for some control rights• Each will have its own comparative advantage

– Banks: more, inside knowledge, state-contingent rights – Debt and debt structure: important disciplining factor, limit free

cash flow/private benefits– Labour: market for managers; employees; others

• Responsible towards all stakeholders can pay – Social corporate responsible can be good business for all and

goes with good corporate governance

12

Developing countries’ challenges

• Often abundant in labor, but short in physical and human capital

• Gap in capital per worker remains large because private returns to investment low and risky– Poor protection of investors

– Poor governance inside firms

– Poor incentives to accumulate human capital

• With rapid integration with international markets, institutional weaknesses affect macro-stability

World Bank

13

Financial markets development key to bridge gap

• Financial markets depend on legal environment

• Legal environment incomplete without enforcement

• But, enforcement part of development. North (1991): “single most important determinant of economic performance”

• How to think of enforcement? Link to corporate governance?

– What are alternative enforcement mechanisms?

– What is enforcement problem in corporate governance?

– What are corporate governance mechanisms that can work in weak contracting environments?

– What are the policy and new research issues?

World Bank

14

Capital markets and corporate governance

• For capital markets, corporate governance key

– Provides commitment towards stakeholders, in particular external investors (shareholders and creditors) affects firms’ external financing, cost and volume (access)

– Mitigates moral hazard problems

– Facilitates collective action with multiple investors / stakeholders

• But corporate governance is also about balancing multiple stakeholders’ interests, so perfect enforcement of every contract is not necessarily always first best

World Bank

15

Capital markets and corporate governance

0

10

20

30

40

50

60

70

80

Market capitalization/GDPpercent

Lowest quartile(lowest ranking in shareholder and rule of law)

Highest quartile(highest ranking in shareholder and rule of law)

Deg

ree

of c

apit

al m

arke

t dev

elop

men

t

World Bank

16

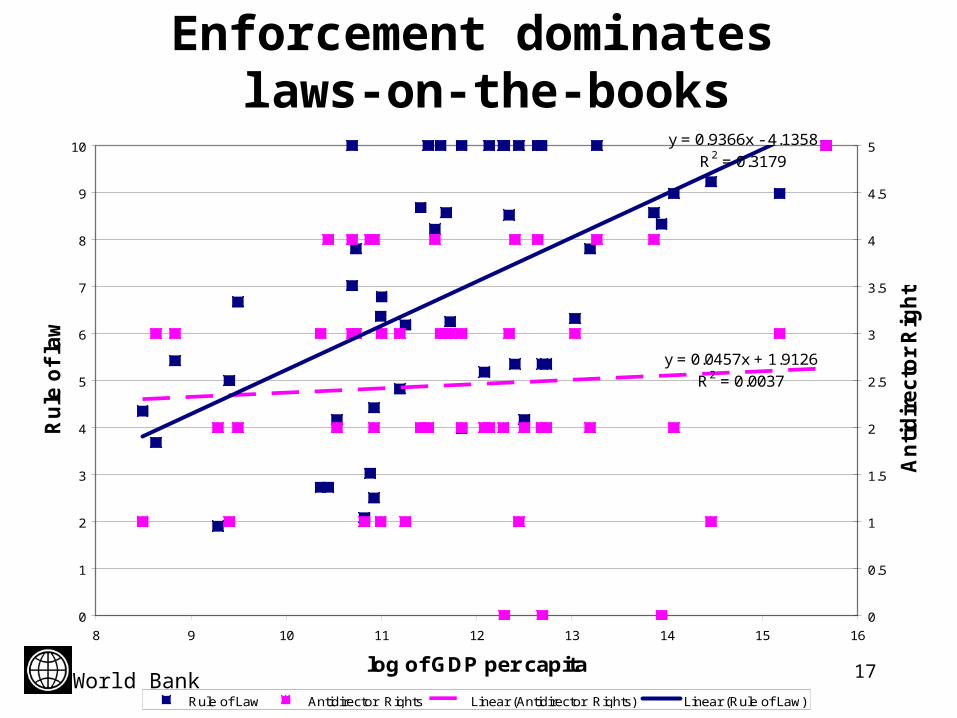

Corporate governance and enforcement

• Corporate governance requires enforcement. Or even stronger: corporate governance is enforcement

• Each mechanism (Concentrated shareholdings, Hostile takeovers, Proxy fights, Board activity, Executive comp., Litigation, Bank monitoring, Public opinion and media, Other stakeholders) depends (to differing extents) on enforcement

• Enforcement more important than laws. Evidence:– Laws: extensiveness vs. effectiveness– Insider trading rules: adoption vs. prosecution– Law and finance literature: suggestive

World Bank

17

Enforcement dominates laws-on-the-books

y = 0.0457x + 1.9126

R2 = 0.0037

y = 0.9366x - 4.1358

R2 = 0.3179

0

1

2

3

4

5

6

7

8

9

10

8 9 10 11 12 13 14 15 16

log of GDP per capita

Ru

le o

f la

w

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

An

tid

ire

cto

r R

igh

ts

Rule of Law Antidirector Rights Linear (Antidirector Rights) Linear (Rule of Law)World Bank

18

What enforcement mechanisms? Continuum of alternative tools

• Private ordering– Exception rather than norm– Unilateral, bilateral and multilateral, with multilateral

mechanisms especially often used in finance

• Private law enforcement – Litigation most important tool

• Public law/regulation enforcement – Traditional view of enforcement

• State-ownership/control – Has many problems, but may be considered

World Bank

19

Private ordering

• Unilateral mechanisms– Create valuable assets, most common reputation,

involving sunk costs, e.g., advertising, or investments – Needs repeated dealings for it to work

• Bilateral mechanisms– Use reputation, others’ enforcement, e.g., auditors– Self-enforcing agreements, e.g., split of functions,

delegating of actions; joint investments, such as in JVs, vertical integration; hostages with firm-specific assets

– Shareholder agreements: can be more specific; have covenants of hostage nature; and rely on other courts

World Bank

20

Private ordering

• Multilateral mechanisms– Financial intermediaries, e.g., banks, investment banks,

rating agencies, clearing houses

– Self-regulatory associations, e.g., industry organizations, codes of conduct/punishments (expel), minority shareholders associations

– Self-regulatory organizations, e.g., stock exchanges, with listing standards and penalties

– Arbitration, e.g., as in JVs, possibly backed up internationally, e.g., through NY convention

World Bank

21

Private ordering: evidence

• Unilateral and bilateral mechanisms– Can work, e.g., voluntary adoption of CG, FDI– Up to a limit, however, as effectiveness depends on the

overall institutional environment, country vs. firm

• Multilateral mechanisms– Can depend on size/number of market, scope for

entrenchment, degree of competition, multiple equilibriums. Many practical issues, e.g., arbitration: when to arbitrate and whom to use; which law?

– Private ordering can be the basis for public law

• Most need some form of public enforcement

World Bank

22

Private laws enforcement • Either the government creates the rules, but delegates the

enforcement to others – Delegation of public enforcement to SRO/SRAs (e.g., stock

exchanges) can be more efficient if more information, better tools/incentives

• Or initiation of enforcement lies with private parties, with litigation the most important– The norm in securities markets (LSV, 2005)– Depends on standards set in the law, e.g., bright lines– Depends on legal system and institutional setup, e.g., class

action suits, role of stock exchanges depends on competition, etc. especially with many constituencies

World Bank

23

Public law/regulation enforcement

• SEC, other regulator type of approach, with courts– Seems less effective than private enforcement in

securities markets, especially when institutional environment is weak

• Public law enforcement depends on– Extensiveness and effectiveness of law: some laws are

easier enforced than others, affects scope for enforcement and scope for misuse (bright line)

– Independence (financially, politically, tenure) of the regulators and the checks and balances in the system

– Efficiency of the court system, since backup is needed

World Bank

24

Extensiveness of laws and origins

• What needs to be codified in the first place? – How does codification vary with level of development, social

and economic features? How does codification interacts with various enforcement mechanisms?

• Extensiveness of law affects enforcement problem – With imprecise laws, private ordering and private

enforcement may be costly or uncertain, and the benefits for parties to deviate may be too big

– But, broader laws allow for more evolution

• Transplanting of laws/systems – Leads to less effective formal institutions, higher legality

with voluntary adoption

World Bank

25

State control

• State ownership

– Can be justified to deal with market failures, externalities, public goods, coordination issues, etc

• Golden share– A more targeted approach to certain concerns

• Regulations covering various areas have also corporate governance functions, especially with other stakeholders

• Full control, through ownership or centrally planned economy/lack of market economy

World Bank

26

Choice of enforcement technologies

• Overall environment – Social and other norms, civic capital, general political

• Costs and benefits of each technology/issues – Outside options vary; Multistage issues, need several

technologies; Public to back up

• Path dependence, certain technology can stick– Technological progress can change choices

• Mix of technologies will always be used– Vary by country, issue to be enforced

• Rules and political economy– Tollbooth view: rules can create rent-seeking

World Bank

27

What enforcement mechanisms work in securities markets?

• La Porta, Lopez-de-Silanes and Shleifer (2005), “What works in securities laws?” construct: – Private enforcement index = “Disclosure” and “Burden of

proof” – Public enforcement index = “Supervisor”, “Investigative

powers”, “Orders” and “Criminal”

• Find for sample of 49 countries: – Securities market development is more associated with

private enforcement index– Public enforcement works in developed countries only– More efficient institutional choice will often be private

enforcement of public rules

World Bank

28

Private enforcement and market capitalization

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

0 0.2 0.4 0.6 0.8 1 1.2

Private enforcement index

Sto

ck

ma

rket

ca

pit

aliz

atio

n

Private enforcement often works better in securities markets

Each point represents one of 49 countries. Data from LLS (2005).World Bank

29

Limits to what firms can dowhen environment is weak

• Many consider corporate governance a firm specific issue. True mostly in developed countries. But in many developing countries, general enforcement environment is weak and few traditional CG mechanisms are effective

• Almost all the variation in governance ratings across firms in less developed countries is attributable to country characteristics (only 50% in developed countries; rest is firm characteristics) (Doidge, Karloyi, and Stulz, 2004)

• Access to global markets sharpens firm incentives to improve governance, and decreases the importance of home-country (formal) legal protection of minority investors, but does not eliminate problem

World Bank

30

With weak enforcement

• Predominant form of corporate governance in weak contracting environment is large blockholders and high ownership/control concentration

• But this mechanism has important costs

– Main corporate governance conflict for public firms: controlling owners vs. minority shareholders

– But also corporate governance weaknesses impact private firms’ ability to raise financing and to grow

– Overall adverse impact on corporate governance environment, institutional development

• Limited scope for policy intervention

World Bank

31

Large blockholders dominate, with costs though and limited scope for policy

Corporate governance mechanism Large blockholders

Private ordering Natural Outcome

Private law enforcement Shareholders suits

Public enforcement Governance codes evolving into corporate and securities

law

Relative importance in developing and transition

countries

Likely to be the most important governance

mechanism

Scope for policy intervention Strengthen rules protecting minority investors without

removing incentives to hold controlling blocks

World Bank

32

What is scope for other corporate governance mechanisms?

• Ownership concentration the outcome, yet has costs.

• Most other mechanisms need some enforcement technology and tools, e.g, exit, collateral, bankruptcy, etc.

• Will not work well with weak enforcement. What to do?

– What to expect from private ordering, private law enforcement, public enforcement?

– What is relative importance of each mechanism in developing countries?

– What policy interventions can help reduce costs and reinforce specific mechanisms?

World Bank

33

Scope for policy interventions for other corporate governance mechanisms

Corporate governance mechanism

Scope for policy intervention

Large blockholdersStrengthen rules protecting minority investors without removing

incentives to hold controlling blocksMarket for corporate

controlRemove some managerial defenses; disclosure of ownership and

control; develop banking system

Proxy fightsTechnology improvements for communicating with and among

shareholders; disclosure of ownership and control

Board activityIntroduce elements of independence of directors; training of

directors; disclosure of voting; cumulative voting possibly Executive

compensationDisclosure of compensation schemes, conflicts of interest rules

Bank monitoringStrengthen banking regulation and institutions; encourage

accumulation of information on credit histories; develop supporting credit bureaus and other information intermediaries;

World Bank

34

Scope for policy interventions for other corporate governance mechanisms

Corporate governance mechanism

Scope for policy intervention

Employee monitoringDisclosure of information to employees; possibly require board

representation; assure flexible labor markets

LitigationFacilitate communication among shareholders; encourage class-

action suits with safeguards against excessive litigationMedia and social

controlEncourage competition in and diverse control of media; active public

campaigns can empower publicReputation and self

enforcement Depend on growth opportunities and scope for rent seeking.

Encourage competition in factor marketsBilateral private

enforcement mechanisms

Requiring functioning civil/commercial courts

Arbitration, auditors, other multilateral

mechanisms

Facilitate the formation of private third party mechanisms (sometimes avoid forming public alternatives); deal with conflicts of

interest; ensure competition

Encourage interaction among shareholders. Strengthen minority Shareholder Activism

World Bank

35

Have to consider the political economy of enforcement

• Laws and enforcement evolve under many pressures– Vested interests may block progress– Wealth concentration hinders reform

• Enforcement is a difficult investment – Long-term payoffs, many bodies, subject to many parties,

low political payoff

• Enforcement is a public good, with few champions– Can be indirect effects of financial sector development,

changes in ownership structures, real sector reform on desires for enforcement and institutional reform

World Bank

36

Implementation of the Acquis Communautaires (company law)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

1997 1998 1999 2000 2001 2002 2003Year

Ind

ex

Bulgaria

Czech Republic

Estonia

Hungary

Latvia

Lithuania

Poland

Romania

Slovak Republic

Slovenia

World Bank

37

Variation in laws and in enforcement,but change is possible

CountryInside-Shares Income

Related-Trans Owners CGSection

AR-Disclosure

AR-Disclosure_dif

Bulgaria 1.00 0.00 0.50 1.00 0.00 2.50 -1.00

Czech Republic 0.50 0.50 0.50 1.00 0.00 2.50 0.31

Estonia 1.00 0.00 0.50 1.00 0.00 2.50 0.36

Hungary 0.00 0.50 0.00 1.00 0.00 1.50 0.13

Latvia 0.00 0.00 0.50 1.00 0.00 1.50 -0.06

Lithuania 1.00 0.50 0.50 1.00 0.00 3.00 -0.69

Poland 0.50 0.00 0.50 1.00 0.00 2.00 -0.38

Romania 0.00 0.00 0.50 1.00 0.00 1.50 -0.13

Slovak Republic 0.00 0.00 0.00 1.00 0.00 1.00 0.50

Slovenia 0.00 0.50 0.50 1.00 0.00 2.00 -0.14

Total (laws) 0.50 0.28 0.45 1.00 0.00 2.22 -0.14

Total (enforced) 0.42 0.30 0.39 0.86 0.11 2.08

Source: Berglof and Pajuste (2005)World Bank

38

Possible research topics on enforcement • Appropriate balance between private enforcement of public

standards and public enforcement in corporate governance in different contexts

• Tradeoffs between the extensiveness of laws and their effectiveness in different contexts

• Effectiveness of self-regulatory agencies and organizations in encouraging better standards and greater enforcement

• Role of competition (factor markets and regulatory) in improving the environment for enforcement

• Both case studies and cross-country research can help clarify what is best suited to needs of different countries

World Bank