1 chapter 7: principles of asset valuation copyright © prentice hall inc. 1999. author: nick bagley...

TRANSCRIPT

1

Chapter 7: Principles of Chapter 7: Principles of Asset ValuationAsset Valuation

Copyright © Prentice Hall Inc. 1999. Author: Nick Bagley

ObjectiveExplain the principles of

asset evaluation

2

Chapter 7 ContentsChapter 7 Contents• 1 The relationship 1 The relationship

between an asset’s between an asset’s value & pricevalue & price

• 2 Value maximization & 2 Value maximization & financial decisionsfinancial decisions

• 3 The law of one price 3 The law of one price & arbitrage& arbitrage

• 4 Arbitrage & the law of 4 Arbitrage & the law of one priceone price

• 5 Interest rates & the 5 Interest rates & the law of one pricelaw of one price

• 6 Exchange rates & 6 Exchange rates & triangular arbitragetriangular arbitrage

• 7 Valuation using 7 Valuation using comparablescomparables

• 8 Valuation Models8 Valuation Models

• 9 Accounting measures 9 Accounting measures of valueof value

• 10 How information is 10 How information is reflected in security reflected in security pricesprices

• 11 The efficient markets 11 The efficient markets hypothesishypothesis

3

IntroductionIntroduction

• The key to asset valuation is The key to asset valuation is comparison of “equivalent” assets - comparison of “equivalent” assets - that is comparison of assets with that is comparison of assets with virtually identical characteristicsvirtually identical characteristics

• By the By the law of one pricelaw of one price, the price of , the price of all equivalent assets must be the all equivalent assets must be the samesame

4

7.1 Relationship between 7.1 Relationship between Asset Value and PriceAsset Value and Price

• Definition: Definition:

• An asset’s An asset’s fundamental valuefundamental value is the is the price well informed investors must price well informed investors must pay to purchase it in a free and pay to purchase it in a free and competitive marketcompetitive market

5

Relationship between Relationship between Asset Value and PriceAsset Value and Price

• There can exist temporary differences There can exist temporary differences between the market price of an asset between the market price of an asset and its fundamental valueand its fundamental value– Security analysts make their living by Security analysts make their living by

discovering these aberrationsdiscovering these aberrations

– Many well-informed professionals are Many well-informed professionals are looking for these aberrations. A reasonable looking for these aberrations. A reasonable initial assumption is that aberrations are initial assumption is that aberrations are smallsmall

6

7.2 Value Maximization 7.2 Value Maximization and Financial Decisionsand Financial Decisions

• Financial decisions can be made Financial decisions can be made rationally purely on the basis of value rationally purely on the basis of value maximization, and without regard to maximization, and without regard to risk preferences and expectationsrisk preferences and expectations

• Markets for financial assets provide Markets for financial assets provide the information needed to choose the information needed to choose between some alternativesbetween some alternatives

7

7.3 The Law of One Price7.3 The Law of One Price

• Law of One Price: Law of One Price: – In a competitive market, if two assets In a competitive market, if two assets

are equivalent, they will tend to have are equivalent, they will tend to have the same pricethe same price

8

The Law of One Price and The Law of One Price and ArbitrageArbitrage

• The The law of one pricelaw of one price is enforced by is enforced by a process called a process called arbitragearbitrage

• Arbitrage is the purchasing of a set Arbitrage is the purchasing of a set of assets, and immediate sale of of assets, and immediate sale of another set of assets, in such a way another set of assets, in such a way as to earn a sure profit from price as to earn a sure profit from price differencesdifferences

9

The Law of One Price and The Law of One Price and ArbitrageArbitrage

• ArbitrageursArbitrageurs engage in the business of engage in the business of trading similar assets with a price trading similar assets with a price differential that cannot be justified by differential that cannot be justified by transaction- and transformation-coststransaction- and transformation-costs

• Example: Gold in any two parts of the Example: Gold in any two parts of the country should not differ by more than country should not differ by more than the the transaction coststransaction costs of moving it of moving it

10

7.4 Arbitrage and the 7.4 Arbitrage and the Prices of Financial AssetsPrices of Financial Assets

• Arbitraging by shipping a physical Arbitraging by shipping a physical commodity (gold) involves higher commodity (gold) involves higher transaction costs than arbitraging transaction costs than arbitraging financial assets (shares of stock)financial assets (shares of stock)

• We expect the same financial We expect the same financial commodity trading on two markets commodity trading on two markets to be priced very closelyto be priced very closely

11

Arbitrage and the Prices Arbitrage and the Prices of Financial Assetsof Financial Assets

• The rule of one price is the most The rule of one price is the most fundamental valuation principle in fundamental valuation principle in finance.finance.– If two very similar securities trade at If two very similar securities trade at

significantly different prices, we first significantly different prices, we first suspectsuspect• Interference with normal market operationInterference with normal market operation

• Some unrecognized difference between the Some unrecognized difference between the two assets two assets

12

7.5 Interest Rates and the 7.5 Interest Rates and the Law of One PriceLaw of One Price

• If two organizations with similar If two organizations with similar creditworthiness issue bonds with creditworthiness issue bonds with similar terms, then their interest rates similar terms, then their interest rates will be similarwill be similar

– Take care to ensure that there are no subtle Take care to ensure that there are no subtle differences indifferences in• the tax status of the bondsthe tax status of the bonds

• the value of collateral or backing of the the value of collateral or backing of the bondsbonds

13

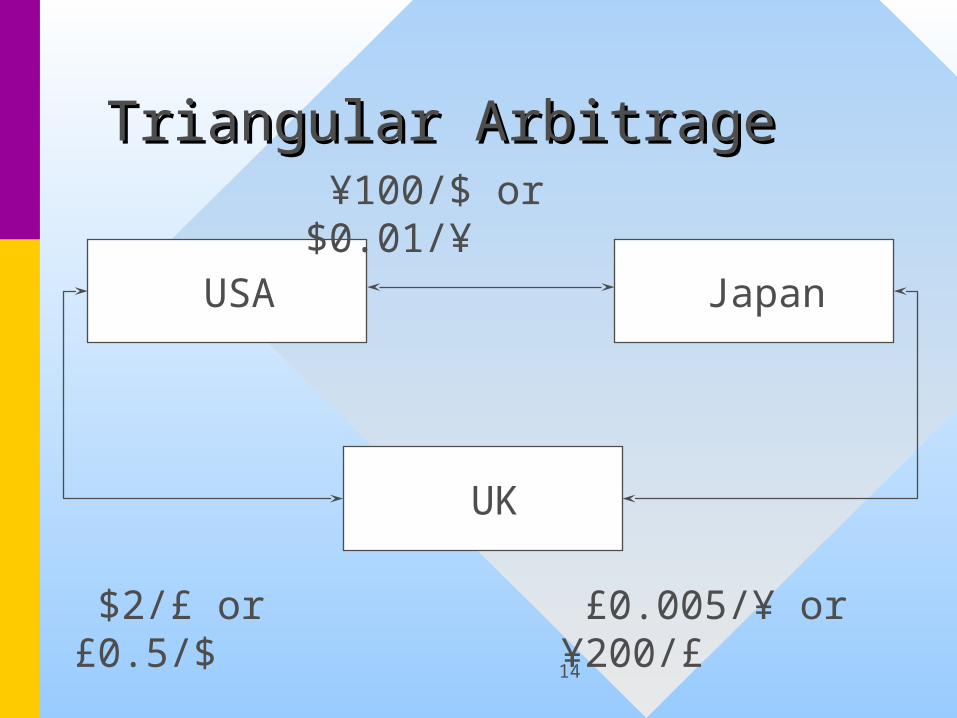

7.6 Exchange Rates and 7.6 Exchange Rates and Triangular ArbitrageTriangular Arbitrage

• The law of one price also applies to The law of one price also applies to foreign exchange marketsforeign exchange markets

• If three currencies are freely If three currencies are freely convertible in competitive markets, convertible in competitive markets, then it is enough know any two then it is enough know any two exchange rates to compute the exchange rates to compute the third exchange ratethird exchange rate

14

Triangular ArbitrageTriangular Arbitrage

USA Japan

UK

¥100/$ or $0.01/¥

£0.005/¥ or ¥200/£

$2/£ or £0.5/$

15

Triangular ArbitrageTriangular Arbitrage

• Every country has its own conventions Every country has its own conventions for expressing exchange rates for expressing exchange rates – Traders in the U.K. express exchange rates Traders in the U.K. express exchange rates

as foreign currency per poundas foreign currency per pound

– Traders in the U.S.A. express exchange rates Traders in the U.S.A. express exchange rates as dollars per unit of foreign currencyas dollars per unit of foreign currency

– In the case of $/£ exchange rates, dealers in In the case of $/£ exchange rates, dealers in both countries use the same rate, say 2 $/£ both countries use the same rate, say 2 $/£

16

Triangular ArbitrageTriangular Arbitrage

• If we select the form of the rate correctly, If we select the form of the rate correctly, we obtain the relationshipwe obtain the relationship

• RR£/¥ £/¥ = R= R£/$ £/$ * R* R$/¥$/¥

• Under the conditions specified, this Under the conditions specified, this equilibrium relationship must hold (or a equilibrium relationship must hold (or a risk-free, almost cost-less, arbitrage will risk-free, almost cost-less, arbitrage will immediately reestablish the equilibrium)immediately reestablish the equilibrium)

17

Triangular ArbitrageTriangular Arbitrage

• More generallyMore generally

• RRA/C A/C = R= RA/B A/B * R* RB/CB/C

• RRA/B A/B = 1/R= 1/RB/AB/A

18

Triangular ArbitrageTriangular Arbitrage

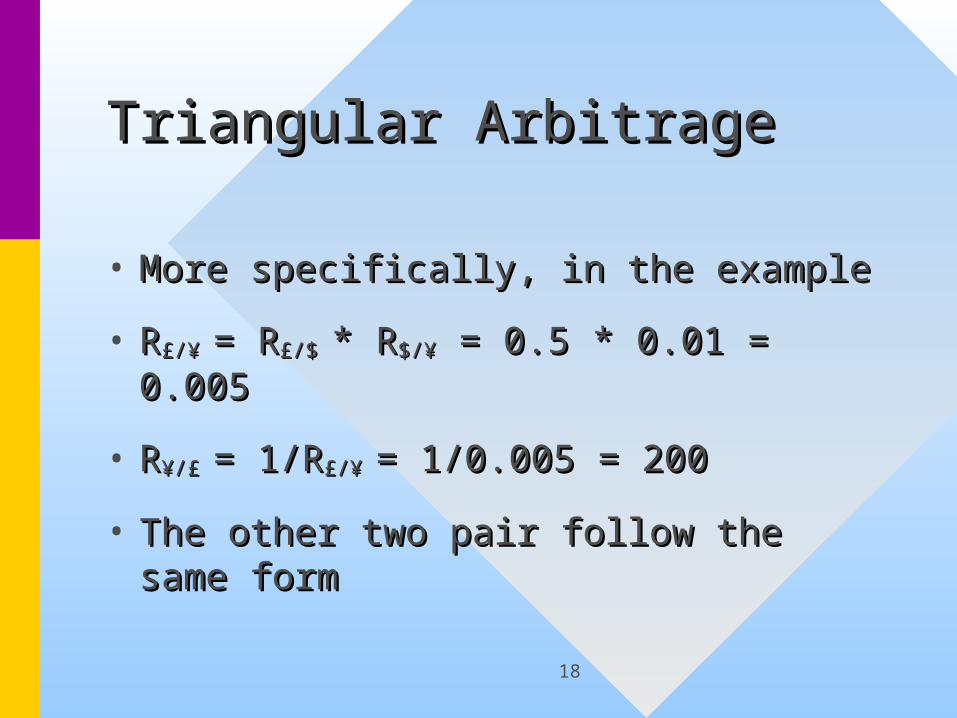

• More specifically, in the exampleMore specifically, in the example

• RR£/¥ £/¥ = R= R£/$ £/$ * R* R$/¥$/¥ = 0.5 * 0.01 = 0.005 = 0.5 * 0.01 = 0.005

• RR¥/£ ¥/£ = 1/R= 1/R£/¥ £/¥ = 1/0.005 = 200= 1/0.005 = 200

• The other two pair follow the same The other two pair follow the same formform

19

Triangular ArbitrageTriangular Arbitrage

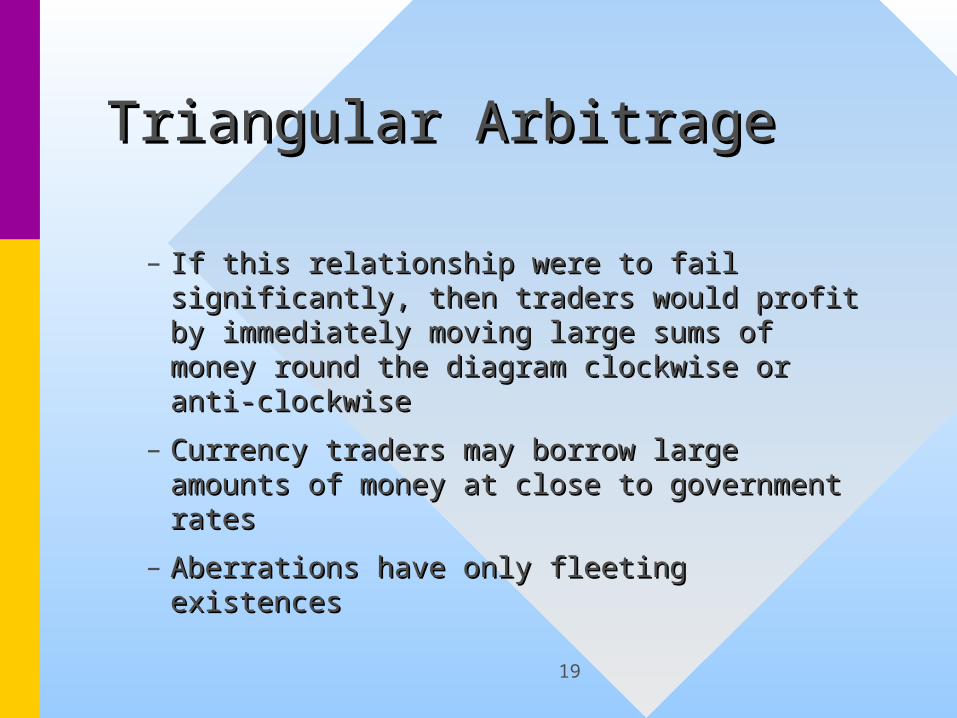

– If this relationship were to fail If this relationship were to fail significantly, then traders would profit by significantly, then traders would profit by immediately moving large sums of money immediately moving large sums of money round the diagram clockwise or anti-round the diagram clockwise or anti-clockwise clockwise

– Currency traders may borrow large Currency traders may borrow large amounts of money at close to government amounts of money at close to government ratesrates

– Aberrations have only fleeting existencesAberrations have only fleeting existences

20

7.7 Valuation Using 7.7 Valuation Using ComparablesComparables

• Some assets are not traded, or are Some assets are not traded, or are only traded infrequently, but we still only traded infrequently, but we still need to evaluate themneed to evaluate them

• The The law of one pricelaw of one price may be used to may be used to evaluate assets, even when evaluate assets, even when arbitrage can not be used to enforce arbitrage can not be used to enforce the lawthe law

21

Valuation Using Valuation Using ComparablesComparables

• Two casesTwo cases– a work of art in an estate that needs to a work of art in an estate that needs to

be evaluated for computation of estate be evaluated for computation of estate taxestaxes

– a home that needs to be evaluated to a home that needs to be evaluated to ensure the fairness of property taxesensure the fairness of property taxes

22

Valuation Using Valuation Using ComparablesComparables

• To evaluate the non-trading asset, one To evaluate the non-trading asset, one finds comparable prices of traded assetsfinds comparable prices of traded assets

– It is useful to think of asset prices in a It is useful to think of asset prices in a feature-time frameworkfeature-time framework• Similar assets have prices that tend to move Similar assets have prices that tend to move

up and down together in timeup and down together in time

• At a particular time, differences in asset At a particular time, differences in asset prices are largely accountable in terms of prices are largely accountable in terms of differences in featuresdifferences in features

23

7.8 Valuation Models7.8 Valuation Models

• A A valuation modelvaluation model is a quantitative is a quantitative method used for estimating an asset’s method used for estimating an asset’s value from known prices of other assets value from known prices of other assets that are not its exact equivalentthat are not its exact equivalent

• The valuation model employed may The valuation model employed may depend on the purpose of the evaluationdepend on the purpose of the evaluation– traditional shareholder v. take-over specialisttraditional shareholder v. take-over specialist

24

Stock Evaluation using Stock Evaluation using P/EsP/Es

• The price-over-earnings ratios of similar The price-over-earnings ratios of similar companies are determinedcompanies are determined

• Based on these, an estimate is made of Based on these, an estimate is made of the p/e ratio of the non-priced firmthe p/e ratio of the non-priced firm

• The earnings of the firm are multiplied The earnings of the firm are multiplied by this p/e ratio to obtain an evaluationby this p/e ratio to obtain an evaluation

25

Stock Evaluation using Stock Evaluation using P/EsP/Es

• The accuracy of this method The accuracy of this method depends on the appropriateness of depends on the appropriateness of the exemplar firmsthe exemplar firms

• Future profitability, accounting Future profitability, accounting methods, leverage, technology, and methods, leverage, technology, and a host of other factors, will affect a host of other factors, will affect the exemplars’ p/e ratiosthe exemplars’ p/e ratios

26

Valuation Model Valuation Model RefinementRefinement

• You are a security analyst for an asset You are a security analyst for an asset

• You have developed a valuation model You have developed a valuation model you believe is superior to valuation you believe is superior to valuation models used by other traders models used by other traders

• Assuming the superior model remains Assuming the superior model remains proprietary, it may be difficult to exploit itproprietary, it may be difficult to exploit it

27

P/E Ratio or NPV?P/E Ratio or NPV?

• You already have enough theoretical You already have enough theoretical knowledge to price a small business knowledge to price a small business correctly using NPVcorrectly using NPV

• Traditionally, small businesses were Traditionally, small businesses were priced using P/Es (sub-optimal model)priced using P/Es (sub-optimal model)

• This leads to price aberrations from This leads to price aberrations from which you can still benefit (use NPV)which you can still benefit (use NPV)

28

7.9 Accounting Measures 7.9 Accounting Measures of Valueof Value

• Owner’s equity is not an accurate Owner’s equity is not an accurate indicator of the firm’s market valueindicator of the firm’s market value– Assets and liabilities are not market pricedAssets and liabilities are not market priced

• markingmarking the balance sheet the balance sheet to marketto market helps helps

– Intangibles are under-included Intangibles are under-included • a firm is a going concern, not just its a firm is a going concern, not just its

physical assets and liabilitiesphysical assets and liabilities

29

7.10 How Information is 7.10 How Information is reflected in Security reflected in Security PricesPrices• Sometimes a stock price will rise sharply Sometimes a stock price will rise sharply

with the release of informationwith the release of information– An important drug has achieved an important An important drug has achieved an important

step on its road to being marketedstep on its road to being marketed

– Poor trading results are announced, but they Poor trading results are announced, but they are better than those anticipated by tradersare better than those anticipated by traders

– An unanticipated positive Fed announcementAn unanticipated positive Fed announcement

30

How Information is How Information is reflected in Security reflected in Security PricesPrices

• Market traders form probability Market traders form probability distributions of key stock-price distributions of key stock-price determinants (Example, sales revenue)determinants (Example, sales revenue)

• When these distributions change to When these distributions change to assimilate new information, the stock assimilate new information, the stock market market reactsreacts, and the price changes, and the price changes– This leads to the efficient market This leads to the efficient market

hypothesishypothesis

31

7.11 Efficient Market 7.11 Efficient Market HypothesisHypothesis

• The The efficient market hypothesisefficient market hypothesis states states – an asset’s current price reflects all an asset’s current price reflects all

publicly available information about publicly available information about future economic fundamentals future economic fundamentals affecting market priceaffecting market price

32

Efficient Market Efficient Market HypothesisHypothesis

• The mechanism leading to the The mechanism leading to the efficient market’s hypothesis efficient market’s hypothesis – Collection of relevant informationCollection of relevant information

– Analysis of this information to obtain a Analysis of this information to obtain a priceprice

– Trading on this analysis until the price Trading on this analysis until the price aberration is eliminatedaberration is eliminated

33

Collection of Relevant Collection of Relevant InformationInformation

• Collect information or “facts” about a Collect information or “facts” about a company, and the factors that may company, and the factors that may affect itaffect it– SEC filings, annual reports, clipping services, SEC filings, annual reports, clipping services,

conferences with CEO /CFO, industry conferences with CEO /CFO, industry analyses, patent filings, rumors, discussions analyses, patent filings, rumors, discussions with competitors and customers, informal with competitors and customers, informal market surveys, advertising campaigns, market surveys, advertising campaigns, recruitment activity, technological surveys… recruitment activity, technological surveys…

34

Analysis of this Analysis of this InformationInformation

• At one time, analysts were content to At one time, analysts were content to form just a point estimate of the priceform just a point estimate of the price

• Today, analysts try to incorporate Today, analysts try to incorporate probability into their pricing, by probability into their pricing, by working with ranges, for instanceworking with ranges, for instance

• The more accurate the information, the The more accurate the information, the smaller the price dispersion -> less risksmaller the price dispersion -> less risk

35

Trading on this AnalysisTrading on this Analysis

• Based on her estimates, the analyst may Based on her estimates, the analyst may recommend a traderecommend a trade– The magnitude of resulting trades depend on The magnitude of resulting trades depend on

her past successes and her current statusher past successes and her current status

– Barriers to entry are low, and successful Barriers to entry are low, and successful analysts are well rewarded & gain influenceanalysts are well rewarded & gain influence

• Result: Knowledgeable individuals keep Result: Knowledgeable individuals keep the market efficientthe market efficient