1 chapter 17: finance and corporate strategy copyright © prentice hall inc. 1999. author: nick...

TRANSCRIPT

1

Chapter 17: Finance and Chapter 17: Finance and Corporate StrategyCorporate Strategy

Copyright © Prentice Hall Inc. 1999. Author: Nick Bagley

ObjectiveUnderstanding:

Mergers & AcquisitionsSpinoffs

Real Options

2

Chapter 17 ContentsChapter 17 Contents

• 17.1 Mergers and Acquisitions17.1 Mergers and Acquisitions

• 17.2 Spinoffs17.2 Spinoffs

• 17.3 Investing in Real Options17.3 Investing in Real Options

3

IntroductionIntroduction

• First we analyze corporate decisions First we analyze corporate decisions regarding mergers, acquisitions and regarding mergers, acquisitions and spinoffsspinoffs

• Then we show how option theory may Then we show how option theory may be applied to evaluate management’s be applied to evaluate management’s ability to time the start of an investment ability to time the start of an investment project, to expand it, or to abandon it, project, to expand it, or to abandon it, after it has begunafter it has begun

4

17.1 Mergers and 17.1 Mergers and Acquisitions: DefinitionsAcquisitions: Definitions

• AcquisitionAcquisition– one company acquires a controlling one company acquires a controlling

interest in anotherinterest in another

• MergerMerger– two firms join together to form a new firmtwo firms join together to form a new firm

• SynergySynergy– The incremental value obtained by The incremental value obtained by

combining two companies combining two companies

5

Valid PurposesValid Purposes

• There are three valid reasons why the There are three valid reasons why the shareholders of a firm could be shareholders of a firm could be wealthier after combining two firmswealthier after combining two firms– Synergistic benefits resulting from Synergistic benefits resulting from

eliminating duplicated cost of production, eliminating duplicated cost of production, marketing, administration and researchmarketing, administration and research

– Tax shelters (Unusable tax credits)Tax shelters (Unusable tax credits)– Bargains not recognized by the stock Bargains not recognized by the stock

market (better information / sub-optimal market (better information / sub-optimal management)management)

6

Questionable PurposesQuestionable Purposes

• Monopolistic control over a technology Monopolistic control over a technology (intellectual property rights), a market (intellectual property rights), a market sector, labor, raw materials, production sector, labor, raw materials, production facilities, et cetera, may be acquired by facilities, et cetera, may be acquired by consolidation of ownershipconsolidation of ownership

• This category of synergistic effect may be This category of synergistic effect may be exploited to generate incremental profitsexploited to generate incremental profits– Policies for controlling monopolistic power is Policies for controlling monopolistic power is

a difficult and complex issue for the courts a difficult and complex issue for the courts and legislators of all developed countriesand legislators of all developed countries

7

Invalid PurposesInvalid Purposes

• Corporate DiversificationCorporate Diversification– A merger or an acquisition is one way A merger or an acquisition is one way

to achieve corporate diversification--to achieve corporate diversification--the topic of the next sectionthe topic of the next section

8

Corporate DiversificationCorporate Diversification

– We have learned that the shareholders We have learned that the shareholders of a company can reduce of a company can reduce -risk (to the -risk (to the degree that diversification can reduce degree that diversification can reduce it) at very little costit) at very little cost

– Empirical studies have shown that Empirical studies have shown that consolidation is a costly way to reduce consolidation is a costly way to reduce the the -risk of a business:-risk of a business:

9

Corporate Diversification: Corporate Diversification: Shareholder VantageShareholder Vantage

– In order for the investor to gain from the In order for the investor to gain from the consolidation of two firms, some service consolidation of two firms, some service must be provided that the investor was must be provided that the investor was not able to provide for herselfnot able to provide for herself

– Prior to consolidation, the investor could Prior to consolidation, the investor could own own anyany combination of both firms, but combination of both firms, but after consolidation, only a after consolidation, only a fixedfixed ratio of ratio of the assets may be ownedthe assets may be owned

10

Corporate Diversification: Corporate Diversification: Empirical EvidenceEmpirical Evidence

– In order to takeover another firm, the In order to takeover another firm, the acquiring firm must pay a substantial acquiring firm must pay a substantial premium to the shareholders of the targetpremium to the shareholders of the target• You will have noticed that share prices You will have noticed that share prices

generally rise on takeover rumors, and generally rise on takeover rumors, and continue to rise as the managements of the continue to rise as the managements of the two companies negotiate, and third parties two companies negotiate, and third parties enter the biddingenter the bidding

• Contested takeovers result in significant Contested takeovers result in significant legal fees for the acquiring firmlegal fees for the acquiring firm

11

Corporate Diversification:Corporate Diversification:

– The management of the acquiring firm The management of the acquiring firm should believe that (given information it has should believe that (given information it has about the ‘true potential’ of the target firm) about the ‘true potential’ of the target firm) these costs should be more than recoveredthese costs should be more than recovered

– However, if the However, if the onlyonly reason for the takeover reason for the takeover is to reduce risk, then the takeover is almost is to reduce risk, then the takeover is almost certainly certainly notnot in the interests of acquiring in the interests of acquiring firm’s current shareholdersfirm’s current shareholders

12

17.2 Spinoffs17.2 Spinoffs

• Occurs when a corporation divests itself Occurs when a corporation divests itself of one or more of its business units and of one or more of its business units and creates a separate company with assets, creates a separate company with assets, liabilities, and stock of its own.liabilities, and stock of its own.

• Example:Example:

– Pepsico (1997)Pepsico (1997)

– Nabisco (Proposed spring 1999) Nabisco (Proposed spring 1999)

13

• Spinoffs occur when the market value Spinoffs occur when the market value

of the whole is less than the market of the whole is less than the market value of the sum of the partsvalue of the sum of the parts– This may occur because This may occur because

• management is not employing assets management is not employing assets efficiently (Slater-Walker liquidations, U.K. efficiently (Slater-Walker liquidations, U.K. during the 70’s)during the 70’s)

• the market is characterizing a company the market is characterizing a company by one of its divisions Nabisco = tobacco, by one of its divisions Nabisco = tobacco, and so undervaluing the wholeand so undervaluing the whole

• management may not have the management may not have the specialized skills required to manage a specialized skills required to manage a specialized subsidiary effectively (e.g. specialized subsidiary effectively (e.g. pharmaceutical parent with beauty pharmaceutical parent with beauty product subsidiary)product subsidiary)

14

Effect on Debt HoldersEffect on Debt Holders

• Existing debt holders have greater Existing debt holders have greater exposure after a spinoff than beforeexposure after a spinoff than before

15

17.3 Investing in Real 17.3 Investing in Real OptionsOptions

• To date we have ignored management’s To date we have ignored management’s ability to ability to – delay the start of a projectdelay the start of a project

– expand a projectexpand a project

– abandon the projectabandon the project

• Failure to take these options into account Failure to take these options into account will result in an understated NPVwill result in an understated NPV

16

The Movie Industry The Movie Industry (Example)(Example)

• We will examine a decision in the We will examine a decision in the movie industry in order to understand movie industry in order to understand the importance of options in evaluating the importance of options in evaluating projectsprojects

• We add some hypothetical numbers, We add some hypothetical numbers, and to keep the central ideas clearly in and to keep the central ideas clearly in focus, the example will the simplest focus, the example will the simplest possiblepossible

17

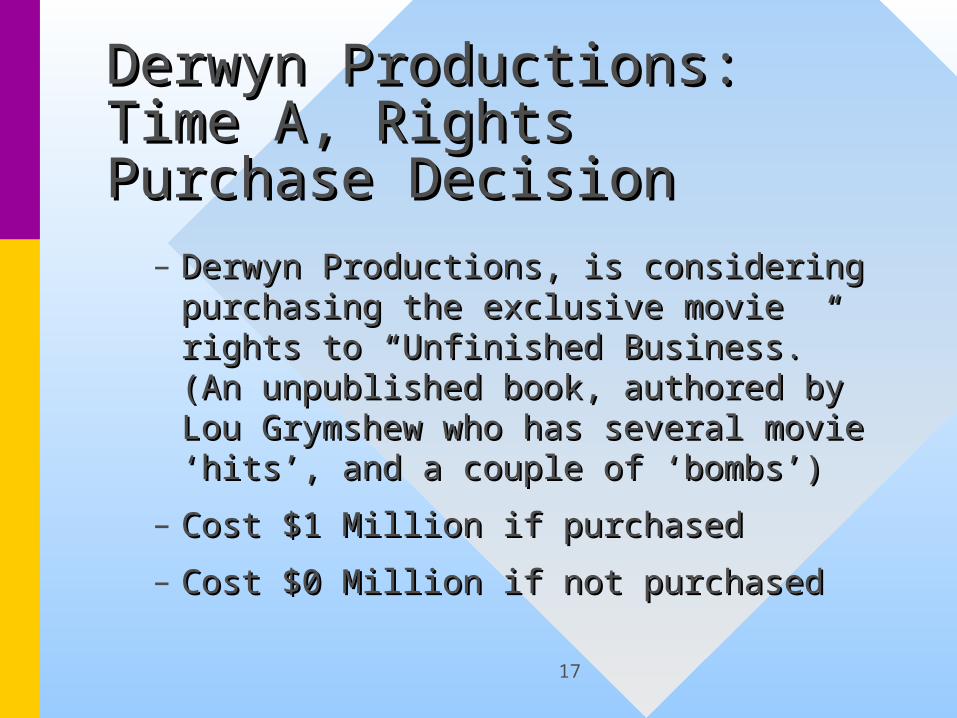

Derwyn Productions: Derwyn Productions: Time A, Rights Purchase Time A, Rights Purchase DecisionDecision

– Derwyn Productions, is considering Derwyn Productions, is considering purchasing the exclusive movie rights purchasing the exclusive movie rights to “Unfinished Business.” (An to “Unfinished Business.” (An unpublished book, authored by Lou unpublished book, authored by Lou Grymshew who has several movie Grymshew who has several movie ‘hits’, and a couple of ‘bombs’)‘hits’, and a couple of ‘bombs’)

– Cost $1 Million if purchasedCost $1 Million if purchased

– Cost $0 Million if not purchasedCost $0 Million if not purchased

18

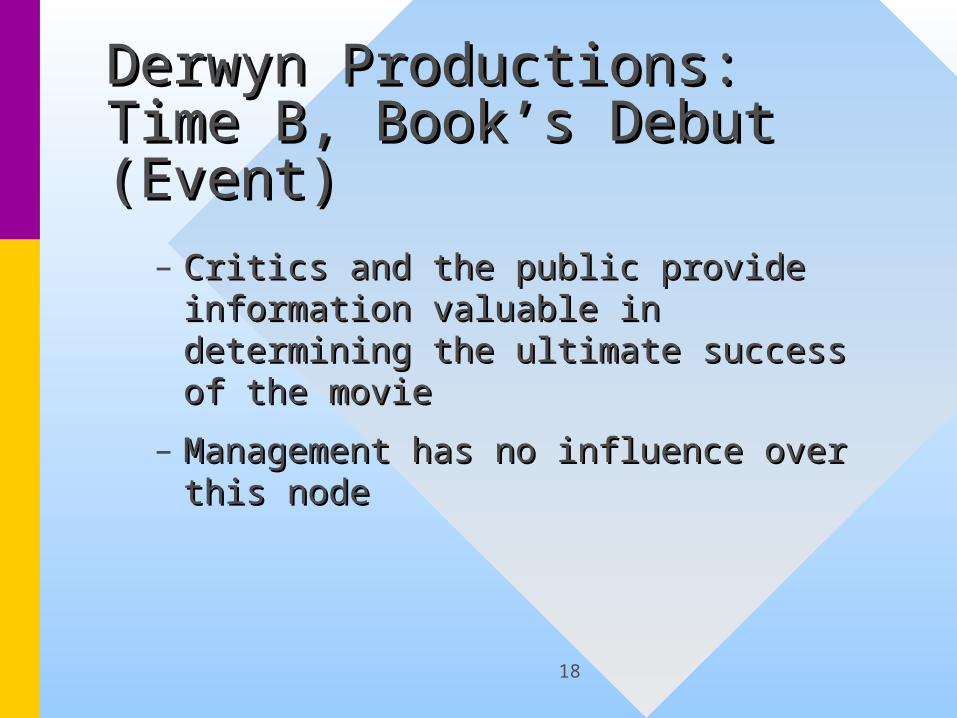

Derwyn Productions: Time Derwyn Productions: Time B, Book’s Debut (Event)B, Book’s Debut (Event)

– Critics and the public provide Critics and the public provide information valuable in determining the information valuable in determining the ultimate success of the movieultimate success of the movie

– Management has no influence over this Management has no influence over this nodenode

19

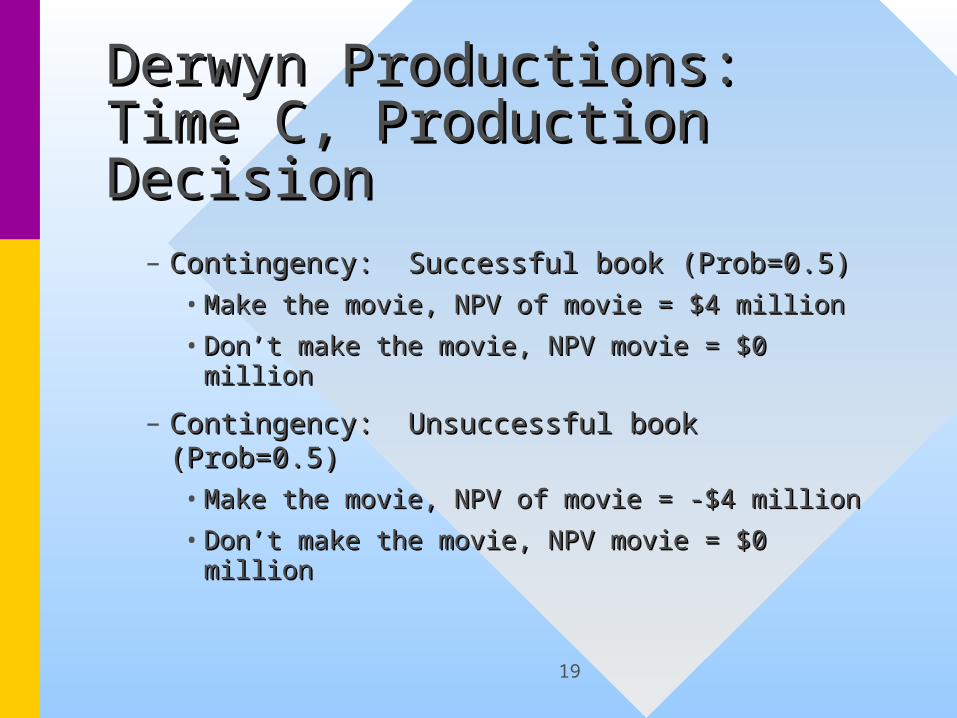

Derwyn Productions: Derwyn Productions: Time C, Production Time C, Production DecisionDecision

– Contingency: Successful book (Prob=0.5)Contingency: Successful book (Prob=0.5)• Make the movie, NPV of movie = $4 millionMake the movie, NPV of movie = $4 million

• Don’t make the movie, NPV movie = $0 millionDon’t make the movie, NPV movie = $0 million

– Contingency: Unsuccessful book (Prob=0.5)Contingency: Unsuccessful book (Prob=0.5)• Make the movie, NPV of movie = -$4 millionMake the movie, NPV of movie = -$4 million

• Don’t make the movie, NPV movie = $0 millionDon’t make the movie, NPV movie = $0 million

20

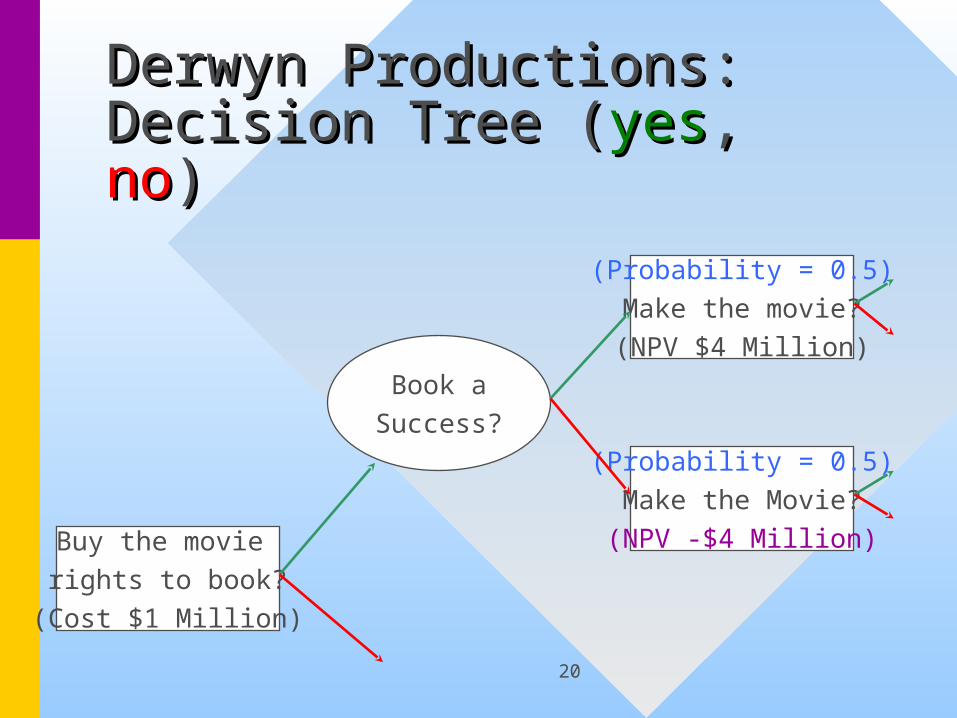

Derwyn Productions: Derwyn Productions: Decision Tree (Decision Tree (yesyes, , nono))

Buy the movie rights to book?

(Cost $1 Million)

(Probability = 0.5)Make the Movie?(NPV -$4 Million)

(Probability = 0.5)Make the movie?(NPV $4 Million)

Book aSuccess?

21

Decision to Acquire RightsDecision to Acquire Rights

– If the decision to undertake the project is If the decision to undertake the project is made under the assumption of a single made under the assumption of a single up-front decisionup-front decision

– then the project must always be rejectedthen the project must always be rejected

– But…But…• If Derwyn makes the logical managerial If Derwyn makes the logical managerial

decision at each stage, then (as long as the decision at each stage, then (as long as the cost of capital for the project is less than cost of capital for the project is less than 100%) the project 100%) the project shouldshould be undertaken be undertaken

22

Volatility and Project Volatility and Project EvaluationEvaluation

– There is a common notion that risk in There is a common notion that risk in investment decisions is something that investment decisions is something that needs to be penalized: Risky cash flows needs to be penalized: Risky cash flows are often discounted at a higher rateare often discounted at a higher rate

– But … we have just seen an investment But … we have just seen an investment decision containing an option-like feature, decision containing an option-like feature, and we know that options always become and we know that options always become more valuable with higher volatilitymore valuable with higher volatility

23

““Unfinished Business” Unfinished Business”

– The publisher also has another book, The publisher also has another book, “Risky Business,” and Derwyn believes “Risky Business,” and Derwyn believes that it’s identical to “Unfinished Business” that it’s identical to “Unfinished Business” in all economic respects other than the in all economic respects other than the payoff, which is (-$8 million, 8 million)payoff, which is (-$8 million, 8 million)

– Running the numbers shows:Running the numbers shows:• the more volatile project increases the more volatile project increases

shareholders’ wealth more than the less shareholders’ wealth more than the less volatile onevolatile one

24

SummarySummary

– Some projects are naturally rich in valuable Some projects are naturally rich in valuable managerial options (R&D), while other managerial options (R&D), while other projects have options that are relatively projects have options that are relatively hard to find, and then discovered, are not hard to find, and then discovered, are not particularly valuable (fast-food franchisee)particularly valuable (fast-food franchisee)

– Sometimes, management’s ability to Sometimes, management’s ability to recognize the options in a business situation recognize the options in a business situation is the key that distinguishes a winning is the key that distinguishes a winning business from its less successful siblingsbusiness from its less successful siblings

25

Applying the Black-Applying the Black-Scholes Formula to value Scholes Formula to value Real OptionsReal Options

• This section shows how to apply the This section shows how to apply the Black-Scholes option pricing formula Black-Scholes option pricing formula in capital budgeting by using two in capital budgeting by using two examplesexamples

26

Raider’s Takeover of Raider’s Takeover of Target using an optionTarget using an option

• Suppose that Raider Inc. is considering Suppose that Raider Inc. is considering acquiring Target Inc. Assume:acquiring Target Inc. Assume:– that both companies are 100% financed by that both companies are 100% financed by

equity divided into 1-million shares equity divided into 1-million shares

– that Target is worth $100,000,000that Target is worth $100,000,000

– Target offers Raider the option to purchase Target offers Raider the option to purchase 100% of Target’s shares one year from now100% of Target’s shares one year from now

– RRff=6%, cost of option $6 million, =6%, cost of option $6 million, TargetTarget=0.20=0.20

27

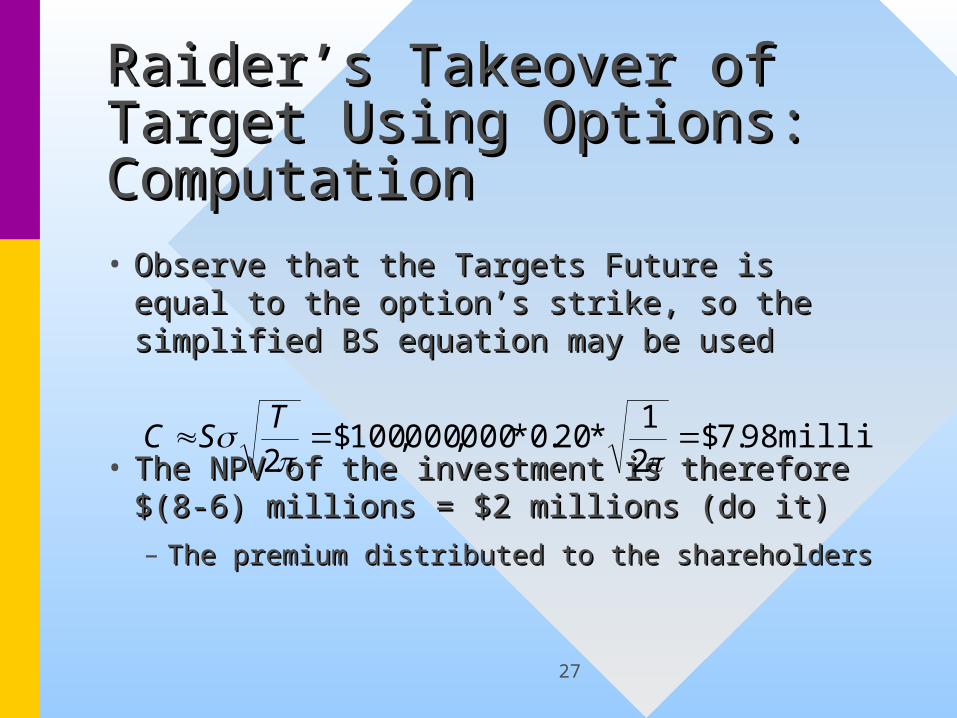

Raider’s Takeover of Raider’s Takeover of Target Using Options: Target Using Options: ComputationComputation• Observe that the Targets Future is equal Observe that the Targets Future is equal

to the option’s strike, so the simplified to the option’s strike, so the simplified BS equation may be usedBS equation may be used

• The NPV of the investment is therefore The NPV of the investment is therefore $(8-6) millions = $2 millions (do it)$(8-6) millions = $2 millions (do it)

– The premium distributed to the shareholdersThe premium distributed to the shareholders

million 98.7$21

*20.0*000,000,100$2

TSC

28

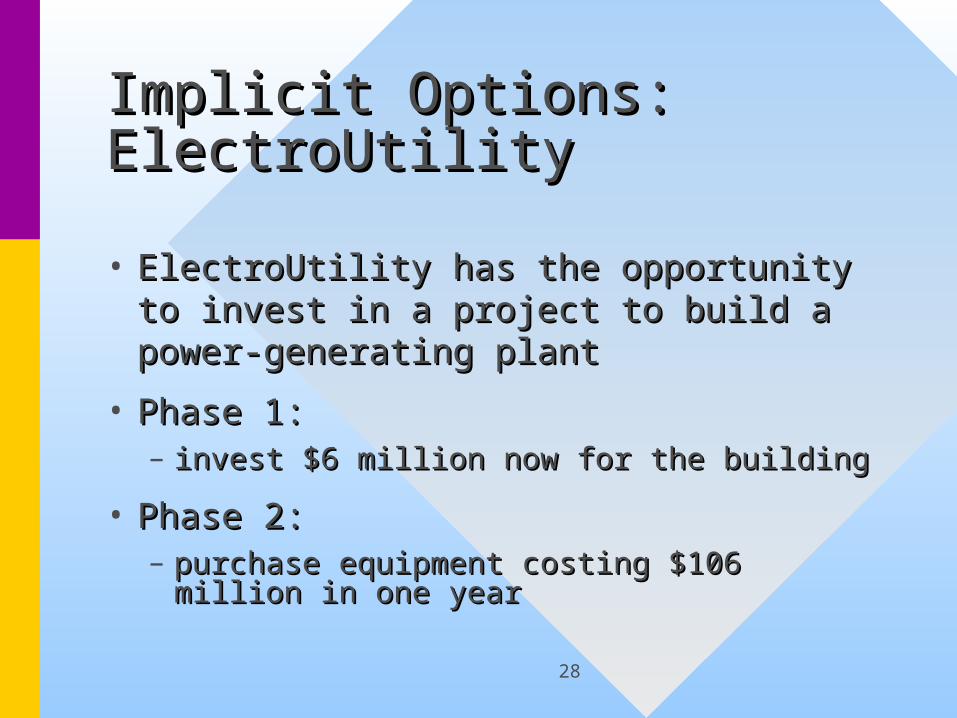

Implicit Options: Implicit Options: ElectroUtilityElectroUtility

• ElectroUtility has the opportunity to ElectroUtility has the opportunity to invest in a project to build a power-invest in a project to build a power-generating plantgenerating plant

• Phase 1:Phase 1:– invest $6 million now for the buildinginvest $6 million now for the building

• Phase 2:Phase 2:– purchase equipment costing $106 million purchase equipment costing $106 million

in one yearin one year

29

Implicit Options: Implicit Options: ElectroUtilityElectroUtility

• Suppose that, viewed from today’s Suppose that, viewed from today’s perspective, perspective, – the value of the completed plant is the value of the completed plant is

$112 $112

– the standard deviation of the capital the standard deviation of the capital return from the project is 0.20return from the project is 0.20

30

Implicit Options: Implicit Options: ElectroUtilityElectroUtility

• The expected value of the cash flow The expected value of the cash flow from the plant a year from now is from the plant a year from now is $(122-106) million$(122-106) million– The initial project outlay is $6 million, The initial project outlay is $6 million,

so a conventional DCF would so a conventional DCF would rejectreject this this project (for any positive cost of capital)project (for any positive cost of capital)

– But:But:

31

Implicit Options: Implicit Options: ElectroUtilityElectroUtility

• But:But:– management management willwill abandonabandon the project (and the project (and

not invest the additional $106 million) if not invest the additional $106 million) if the value of the plant is less than $106 the value of the plant is less than $106 millionmillion

– The cash flows of ElectroUtility are The cash flows of ElectroUtility are identical to those of Raider, so taking the identical to those of Raider, so taking the option into account, the project has a NPV option into account, the project has a NPV of $2 millionof $2 million

32

Implicit OptionsImplicit Options

– We conclude that accounting for We conclude that accounting for managerial flexibility explicitly always managerial flexibility explicitly always increases the value of a projectincreases the value of a project

– From option theory, we know that From option theory, we know that increasing volatility always increases an increasing volatility always increases an option’s value. Using simplified BS:option’s value. Using simplified BS:• a sigma of 0.40 gives the NPV of the project a sigma of 0.40 gives the NPV of the project

of $(16-6) million = $10 million: an increase of $(16-6) million = $10 million: an increase of $8 million over the sigma of 0.20 caseof $8 million over the sigma of 0.20 case