1 chapter 11: hedging and insuring copyright © prentice hall inc. 1999. author: nick bagley...

TRANSCRIPT

1

Chapter 11: Hedging and Chapter 11: Hedging and InsuringInsuring

Copyright © Prentice Hall Inc. 1999. Author: Nick Bagley

ObjectiveExplain market mechanisms for

implementing hedges and insurance

2

Chapter 11 ContentsChapter 11 Contents

11.1 Using Forward & Futures 11.1 Using Forward & Futures Contracts to Hedge RisksContracts to Hedge Risks

11.2 Hedging Foreign-11.2 Hedging Foreign-Exchange Risk with Swap Exchange Risk with Swap ContractsContracts

11.3 Hedging Shortfall-Risk by 11.3 Hedging Shortfall-Risk by Matching Assets to Matching Assets to LiabilitiesLiabilities

11.4 Minimizing the Cost of 11.4 Minimizing the Cost of HedgingHedging

11.5 Insuring versus Hedging11.5 Insuring versus Hedging

11.6 Basic Features of 11.6 Basic Features of Insurance ContractsInsurance Contracts

11.7 Financial Guarantees11.7 Financial Guarantees

11.8 Caps & Floors on 11.8 Caps & Floors on Interest RatesInterest Rates

11.9 Options as Insurance11.9 Options as Insurance

11.10 The Diversification 11.10 The Diversification PrinciplePrinciple

11.11 Insuring a Diversified 11.11 Insuring a Diversified PortfolioPortfolio

3

11.1 Using Forward and 11.1 Using Forward and Futures Contracts to Futures Contracts to Hedge RisksHedge Risks• Forward ContractForward Contract

– an agreement between two parties to an agreement between two parties to exchange something at a specified price exchange something at a specified price and timeand time• This is an This is an obligationobligation on both parties on both parties

• Distinguish this from a Distinguish this from a rightright, but not the , but not the obligation, of a party to exchange somethingobligation, of a party to exchange something

• To nullify the contract, you try to negotiate To nullify the contract, you try to negotiate second contract for a +/- cash considerationsecond contract for a +/- cash consideration

4

Definitions of TermsDefinitions of Terms

• Forward PriceForward Price

– Price (agreed to today) of an item to be Price (agreed to today) of an item to be purchased, and paid for, at a given future datepurchased, and paid for, at a given future date

• Spot PriceSpot Price– Price (agreed to today) of an item to be purchased Price (agreed to today) of an item to be purchased

(and paid for) immediately(and paid for) immediately

• Face ValueFace Value– ‘‘Quantity of deliverable’ times ‘forward price’Quantity of deliverable’ times ‘forward price’

5

Definitions of TermsDefinitions of Terms

• Long PositionLong Position– The agreement to buy the item (from The agreement to buy the item (from

the person taking the short position)the person taking the short position)

• Short PositionShort Position– The agreement to sell the item (to the The agreement to sell the item (to the

person taking the long position)person taking the long position)

6

Using Forward and Using Forward and Futures Contracts to Futures Contracts to Hedge RisksHedge Risks• Traditionally, no payment is made on a Traditionally, no payment is made on a

forward contract until the settlement forward contract until the settlement datedate– If the parties to a forward contract do not If the parties to a forward contract do not

trust the other, then add clauses to trust the other, then add clauses to • provide a sureties to a stakeholderprovide a sureties to a stakeholder

• periodically render contract valueless by periodically render contract valueless by making cash settlement equal to its current making cash settlement equal to its current market valuemarket value

7

Using Forward and Using Forward and Futures Contracts to Futures Contracts to Hedge Risks: Futures Hedge Risks: Futures ContractsContracts• Futures contracts for commodities and Futures contracts for commodities and

financial products includes such financial products includes such clauses to protect against unknown clauses to protect against unknown credit risks, and we leave the details of credit risks, and we leave the details of this to Chapter 14this to Chapter 14

• For clarity, the following example For clarity, the following example treats futures as if they were pure treats futures as if they were pure forward contractsforward contracts

8

The Farmer and the Baker The Farmer and the Baker (Example)(Example)

• Jamela is a farmer with a wheat crop Jamela is a farmer with a wheat crop of about 100,000 bushels, 1-month of about 100,000 bushels, 1-month from harvestfrom harvest

• Mohammed is a baker who will need Mohammed is a baker who will need to restock his inventory of wheat for to restock his inventory of wheat for the coming yearthe coming year

9

The Farmer and the BakerThe Farmer and the Baker

• Jamela and Mohammed wish to Jamela and Mohammed wish to reduce price uncertainty because:reduce price uncertainty because:

– Jamela has a mortgage to pay on her Jamela has a mortgage to pay on her farm, and is concerned about wheat farm, and is concerned about wheat prices falling in the next monthprices falling in the next month

– Mohammed wishes to close an Mohammed wishes to close an agreement with a supermarket to supply agreement with a supermarket to supply bread at a fixed price for the coming yearbread at a fixed price for the coming year

10

The Farmer and the BakerThe Farmer and the Baker

• Jamela and Mohammed agree to a Jamela and Mohammed agree to a forward contractforward contract– Jamela agrees to deliver 100,000 Jamela agrees to deliver 100,000

bushels of wheat at $2.00 a bushel in bushels of wheat at $2.00 a bushel in one month, and Mohammed agrees to one month, and Mohammed agrees to pay the $200,000 on deliverypay the $200,000 on delivery

– Assuming the crop doesn't fail, both Assuming the crop doesn't fail, both parties have hedged their obligationsparties have hedged their obligations

11

The Farmer and the BakerThe Farmer and the Baker

• Assume that Jamela and Mohammed Assume that Jamela and Mohammed live miles apart, and don’t know each live miles apart, and don’t know each otherother

• Jamela writes a forward contract with Ms. Jamela writes a forward contract with Ms. Distributor at $1.99/bushelDistributor at $1.99/bushel

• Mohammed writes a forward contracts with Mohammed writes a forward contracts with Mr. Supplier at $2.01/bushelMr. Supplier at $2.01/bushel

• Ms. Distributor, Mr. Supplier, and Dr. Another Ms. Distributor, Mr. Supplier, and Dr. Another hedge with forward contracts at $2.00/bushelhedge with forward contracts at $2.00/bushel

12

The Farmer and the BakerThe Farmer and the Baker

• Move forward a monthMove forward a month– Wheat prices are not $2.00 a bushel, Wheat prices are not $2.00 a bushel,

but $2.20, due to wet conditions in but $2.20, due to wet conditions in other geographic regionsother geographic regions

13

The Farmer and the BakerThe Farmer and the Baker

– Jamela’s crop is 110,000 bushels, and it Jamela’s crop is 110,000 bushels, and it also exceeds the contracted qualityalso exceeds the contracted quality

– She delivers the contracted 100,000b for She delivers the contracted 100,000b for the agreed $2.00/bushel, and receives the agreed $2.00/bushel, and receives $200,000$200,000

– She sells her surplus 10,000b at $2.20 + She sells her surplus 10,000b at $2.20 + $0.10 (a quality premium) to a local baker, $0.10 (a quality premium) to a local baker, and receives $23,000 and receives $23,000

– The total = $223,000The total = $223,000

14

The Farmer and the The Farmer and the Baker:Baker:Alternative StrategyAlternative Strategy

– Jamela buys 100,000 Bushels of Jamela buys 100,000 Bushels of deliverable quality wheat @ $2.2/b for -deliverable quality wheat @ $2.2/b for -$220,000, delivers it to Ms. Distributor, $220,000, delivers it to Ms. Distributor, and receives the agreed $200,000. Loss and receives the agreed $200,000. Loss of of $20,000$20,000

– She sells her 110,000b at $2.20 + $0.10 She sells her 110,000b at $2.20 + $0.10 quality premium to a local baker and quality premium to a local baker and receives $253,000 receives $253,000

– The total = $233,000 ($10,000 more)The total = $233,000 ($10,000 more)

15

The Farmer and the The Farmer and the Baker:Baker:Alternative StrategyAlternative Strategy

• The product to be delivered was to The product to be delivered was to meet or exceed a certain qualitymeet or exceed a certain quality

• Jamela would have been foolish to Jamela would have been foolish to deliver her wheat when a lower deliver her wheat when a lower quality wheat was available for quality wheat was available for delivery at a lower pricedelivery at a lower price

16

The Farmer and the The Farmer and the Baker:Baker:Alternative StrategyAlternative Strategy

• Mohammed bakes a premium breadMohammed bakes a premium bread

• He too could devise a strategy to He too could devise a strategy to reduce risk using the forward reduce risk using the forward contract, contract, butbut also receive premium also receive premium quality wheatquality wheat

17

The Farmer and the The Farmer and the Baker:Baker:Next DevelopmentNext Development

• The forward contracts always specify The forward contracts always specify the minimum deliverable quality, and the minimum deliverable quality, and often a formula for delivering other often a formula for delivering other qualitiesqualities

• A market in forward contracts may be A market in forward contracts may be devised that encourages cash devised that encourages cash settlement, and discourages physical settlement, and discourages physical deliverydelivery

18

The Farmer and the The Farmer and the Baker:Baker:Next DevelopmentNext Development

– Jamela sells forward 200,000b for 1-month Jamela sells forward 200,000b for 1-month delivery @ 2.00 / busheldelivery @ 2.00 / bushel• This This shortshort has no monetary value at this time has no monetary value at this time

– A month later, the spot price of deliverable A month later, the spot price of deliverable wheat is $2.20 / b, and the forward is about wheat is $2.20 / b, and the forward is about to expire, and so is also trading at $2.20 / b to expire, and so is also trading at $2.20 / b

– The contract now has a monetary value. The The contract now has a monetary value. The long position is worth $(2.20 - 2.00) / bushellong position is worth $(2.20 - 2.00) / bushel• Jamela settles her position by paying $20,000Jamela settles her position by paying $20,000

19

The Farmer and the The Farmer and the Baker:Baker:Next DevelopmentNext Development

– Jamela has made a loss of Jamela has made a loss of $20,000$20,000 on on her trade in the hypothetical wheat her trade in the hypothetical wheat forwards marketforwards market

– She recovers this loss when she sells She recovers this loss when she sells her wheather wheat• This is a true hedge. She has lost the This is a true hedge. She has lost the

opportunity to participate in a rise in the opportunity to participate in a rise in the price of wheat in return for down-side price of wheat in return for down-side protectionprotection

20

The Farmer and the The Farmer and the Baker:Baker:Next DevelopmentNext Development

– The baker’s hedge in the forward market The baker’s hedge in the forward market resulted in a settlement of $20,000resulted in a settlement of $20,000

– When he takes physical delivery, he exactly When he takes physical delivery, he exactly offsets higher spot prices with this $20,000offsets higher spot prices with this $20,000

– He traded the opportunity of lower wheat He traded the opportunity of lower wheat prices for a known priceprices for a known price• Both gained! Mohammed’s gain (at Jamela Both gained! Mohammed’s gain (at Jamela

expense) is 20/20 hindsight, and should be expense) is 20/20 hindsight, and should be irrelevant to both of themirrelevant to both of them

21

The Farmer and the The Farmer and the Baker:Baker:Next DevelopmentNext Development

• Omar is rich, and wants to get richerOmar is rich, and wants to get richer– He purchases forward 100,000b of wheat He purchases forward 100,000b of wheat

@ $2.00/bushel, for delivery in 1-month@ $2.00/bushel, for delivery in 1-month

– At maturity, deliverable wheat costs At maturity, deliverable wheat costs $2.20/b and he makes a cash settlement, $2.20/b and he makes a cash settlement, gaining $20,000gaining $20,000

– Omar is a speculator profiting from his Omar is a speculator profiting from his purported understanding of the marketpurported understanding of the market

22

The Farmer and the The Farmer and the Baker:Baker:Next DevelopmentNext Development

• Rema wants to get rich tooRema wants to get rich too– She sells forward 100,000b of wheat @ She sells forward 100,000b of wheat @

$2.00/bushel for delivery in 1-month$2.00/bushel for delivery in 1-month

– At maturity, deliverable wheat costs At maturity, deliverable wheat costs $2.20/b but she is unable pay the $2.20/b but she is unable pay the $20,000 she owes $20,000 she owes

– Rema’s default must be made good by Rema’s default must be made good by one or more of the market’s participantsone or more of the market’s participants

23

The Farmer and the The Farmer and the Baker:Baker:Forwards to FuturesForwards to Futures

• To mitigate default-risk exposure To mitigate default-risk exposure – Require a modest surety deposit based on Require a modest surety deposit based on

daily volatilitydaily volatility

– Mark contract to market daily (rendering Mark contract to market daily (rendering them temporally valueless)them temporally valueless)• The small profit/loss is payable immediately The small profit/loss is payable immediately

– Remaining problem: Large daily price Remaining problem: Large daily price movementsmovements

24

The Farmer and the The Farmer and the Baker:Baker:ConclusionConclusion• The farmer and the baker have both The farmer and the baker have both

eliminated specific risks through eliminated specific risks through perfectly anti-correlated assetsperfectly anti-correlated assets

• Speculators are exposed to considerable Speculators are exposed to considerable risk, hoping to enjoy a statistical profitrisk, hoping to enjoy a statistical profit

– They provide liquidity and expertise that They provide liquidity and expertise that push the market further towards efficiencypush the market further towards efficiency

25

Risk Transfer: Three Risk Transfer: Three PointsPoints

• Whether the transaction reduces or increases risk Whether the transaction reduces or increases risk depends upon the particular context in which it is depends upon the particular context in which it is undertakenundertaken

• Both parties to a risk-reducing transaction can Both parties to a risk-reducing transaction can benefit. In retrospect, it may benefit. In retrospect, it may seemseem as if one of the as if one of the parties has gained at the expense of the otherparties has gained at the expense of the other

• Even with no change in total output nor total risk, Even with no change in total output nor total risk, redistributing the way the risk is borne can redistributing the way the risk is borne can improve the welfare of the individuals involvedimprove the welfare of the individuals involved

26

11.2 Hedging Foreign-11.2 Hedging Foreign-Exchange Risk with Swap Exchange Risk with Swap ContractsContracts• Swap ContractSwap Contract

– an agreement between two parties to an agreement between two parties to exchange a series of cash flows, at specific exchange a series of cash flows, at specific intervals, over a specified period of timeintervals, over a specified period of time

– the swap payments are based on an agreed the swap payments are based on an agreed principal amount (the principal amount (the notionalnotional amount) amount)

– there is no immediate payment of money to there is no immediate payment of money to either party as compensation for entering the either party as compensation for entering the contractcontract

27

Hedging Foreign-Hedging Foreign-Exchange Risk with Swap Exchange Risk with Swap ContractsContracts

• A swap may call for the exchange of A swap may call for the exchange of anything, but most swaps are for anything, but most swaps are for the exchange ofthe exchange of– commoditiescommodities

– currenciescurrencies

– securities’ returnssecurities’ returns

28

Currency Swap ExampleCurrency Swap Example

• You have an agreement with a German You have an agreement with a German software distributor for them to market software distributor for them to market the German language version of your the German language version of your financial derivative pricing program for a financial derivative pricing program for a payment of DM100,000/year for 10 yearspayment of DM100,000/year for 10 years

• To hedge foreign exchange risk, immunize To hedge foreign exchange risk, immunize your future DM to $US transactions using your future DM to $US transactions using a currency swap agreementa currency swap agreement

29

Currency Swap ExampleCurrency Swap Example

• This swap arrangement is This swap arrangement is equivalent to a series of forward equivalent to a series of forward foreign exchange contractsforeign exchange contracts

• The notional amount in the swap The notional amount in the swap contract corresponds to the face contract corresponds to the face value of the implied forward value of the implied forward contractscontracts

30

Currency Swap ExampleCurrency Swap Example

• You are still at risk after the swapYou are still at risk after the swap– Default:Default: There is a probability that the There is a probability that the

German company will default on its German company will default on its agreement, either by going bankrupt, or by agreement, either by going bankrupt, or by exercising a performance clause in the exercising a performance clause in the contractcontract

– Default driven Exchange Risk:Default driven Exchange Risk: Should Should default occur, you reacquire exchange risk default occur, you reacquire exchange risk through the residual swap agreementthrough the residual swap agreement

31

Currency Swap ExampleCurrency Swap Example

• Suppose the spot exchange rate is Suppose the spot exchange rate is $0.50/DM$0.50/DM

• You and the counterparty agree that You and the counterparty agree that the forward exchange rates should the forward exchange rates should decline from the current spot by 2% decline from the current spot by 2% per year (rounded) for 5 years, and per year (rounded) for 5 years, and then remain staticthen remain static

32

Currency Swap ExampleCurrency Swap Example

• The forward rates are then agreed to be: The forward rates are then agreed to be: 0.49, 0.48, 0.47, 0.46, 0.45, 0.45, 0.45, 0.45, 0.45, 0.450.49, 0.48, 0.47, 0.46, 0.45, 0.45, 0.45, 0.45, 0.45, 0.45

• Assume the actual spot rates are:Assume the actual spot rates are: 0.50, 0.51, 0.53, 0.51, 0.49, 0.48, 0.48, 0.47, 0.45, 0.430.50, 0.51, 0.53, 0.51, 0.49, 0.48, 0.48, 0.47, 0.45, 0.43

• The flows from/ The flows from/ toto the counterparty are the counterparty are computed as (Forward - Spot)*notional computed as (Forward - Spot)*notional amountamount

33

Currency Swap ExampleCurrency Swap Example

• (0.49-0.50)*100,000 DM = (0.49-0.50)*100,000 DM = $1,000 $1,000 (Year 1)(Year 1)

• (0.48-0.51)*100,000 DM = (0.48-0.51)*100,000 DM = $3,000 $3,000 (Year 2)(Year 2)

• (0.47-0.53)*100,000 DM = (0.47-0.53)*100,000 DM = $6,000 $6,000 (Year 3)(Year 3)

• (0.46-0.51)*100,000 DM = (0.46-0.51)*100,000 DM = $5,000 $5,000 (Year 4)(Year 4)

• (0.45-0.49)*100,000 DM = (0.45-0.49)*100,000 DM = $4,000 $4,000 (Year 5)(Year 5)

• (0.45-0.48)*100,000 DM = (0.45-0.48)*100,000 DM = $3,000 $3,000 (Year 6)(Year 6)

• (0.45-0.48)*100,000 DM = (0.45-0.48)*100,000 DM = $3,000 $3,000 (Year 7)(Year 7)

• (0.45-0.47)*100,000 DM = (0.45-0.47)*100,000 DM = $2,000 $2,000 (Year 8)(Year 8)

• (0.45-0.45)*100,000 DM = (0.45-0.45)*100,000 DM = $0,000 $0,000 (Year 9)(Year 9)

• (0.45-0.43)*100,000 DM = $2,000 (Year 10)(0.45-0.43)*100,000 DM = $2,000 (Year 10)

34

Currency Swap ExampleCurrency Swap Example

• In the first year, the agreed forward rate In the first year, the agreed forward rate is lower than the actual spot, resulting in is lower than the actual spot, resulting in a flow from your USA-based company a flow from your USA-based company toto the counter-party of $1,000the counter-party of $1,000

• The sale of DM yields The sale of DM yields • 100,000DM*0.50$/DM = $50,000100,000DM*0.50$/DM = $50,000

• After payment to counterparty = $49,000After payment to counterparty = $49,000

35

Currency Swap ExampleCurrency Swap Example

• Whatever the spot rate in year 1, the Whatever the spot rate in year 1, the agreement absorbs the variance, and agreement absorbs the variance, and you receive a net $49,000 (guaranteed)you receive a net $49,000 (guaranteed)

• Assuming no default, the guaranteed Assuming no default, the guaranteed net cash flows ($ ’000) arenet cash flows ($ ’000) are

• Year 1 = 49, year 2 = 48, year 3 = 47, Year 1 = 49, year 2 = 48, year 3 = 47, year 4 = 46, year 5 through year 10 = 45year 4 = 46, year 5 through year 10 = 45

36

Currency Swap ExampleCurrency Swap Example

– If you prefer a dollar annuity, negotiate:If you prefer a dollar annuity, negotiate:• a fixed forward rate with the counterpartya fixed forward rate with the counterparty Assume a single forward rate (rather than a schedule Assume a single forward rate (rather than a schedule

based on market expectations formed from the $ & DM based on market expectations formed from the $ & DM yield curves). With the passage of time, the expected yield curves). With the passage of time, the expected market value of the swap will diverge more from zero. market value of the swap will diverge more from zero. This generates higher credit risk for the counterparty, This generates higher credit risk for the counterparty, which translates into higher costs for youwhich translates into higher costs for you

a new DM payment schedule that, when a new DM payment schedule that, when coupled with the swap, generates a coupled with the swap, generates a constant $ payment scheduleconstant $ payment schedule

37

11.3 Hedging Shortfall-11.3 Hedging Shortfall-Risk by Matching Assets Risk by Matching Assets to Liabilitiesto Liabilities

• Assume a credit union borrows using Assume a credit union borrows using 1-year CDs, and lends using 30-year 1-year CDs, and lends using 30-year mortgagesmortgages– If interest rates riseIf interest rates rise

• the market value of the mortgages will fallthe market value of the mortgages will fall

• mortgage cash flows won’t fully pay the mortgage cash flows won’t fully pay the CDsCDs

– Result? Insolvency and ruin!Result? Insolvency and ruin!

38

Value of 30-Year Mortgage 5-Years Out (6%)

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

1% 3% 5% 7% 9% 11%

Market Interest Rate

Mar

ket

Val

ue

of

Mo

rtg

age

Market Value of Mortgages

Book Value of Mortgages

39

InterpretationInterpretation

– Five years later, interest rates will have risen Five years later, interest rates will have risen or fallenor fallen• The more rates have risen above the The more rates have risen above the

mortgages’ coupon rate, the larger the mortgages’ coupon rate, the larger the unrealized capital loss, but liabilities remain unrealized capital loss, but liabilities remain essentially constantessentially constant

• The more rates have fallen below the The more rates have fallen below the mortgages’ coupon rate, the higher the mortgages’ coupon rate, the higher the unrealized capital gain, but the more likely unrealized capital gain, but the more likely borrowers will refinance. (Graph assumes no borrowers will refinance. (Graph assumes no refinancing)refinancing)

40

Cash from Mortgages and Cash Needed for CDs

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12%

Current Interest Rate

Cas

h F

low

s F

rom

Mo

rtg

ages

an

d t

o

CD

s

CD Interest Payments

Mortgage Interest Payments

41

InterpretationInterpretation

• As interest rates rise, so too does As interest rates rise, so too does the rate demanded by the lendersthe rate demanded by the lenders

• The mortgage borrowers continue to The mortgage borrowers continue to provide the same cash flowprovide the same cash flow

• The result is a reduction in the cash The result is a reduction in the cash flows that service the CDsflows that service the CDs

42

Remedial Action to Remedial Action to Prevent further DamagePrevent further Damage

– Match exposure of assets and liabilitiesMatch exposure of assets and liabilities• Sell mortgages & invest in short-term Sell mortgages & invest in short-term

lendinglending– Participate in GNMA, FNMA, … programsParticipate in GNMA, FNMA, … programs

• Get lenders to invest in longer-term notesGet lenders to invest in longer-term notes

• Lend using adjustable rate mortgagesLend using adjustable rate mortgages

• Issue longer-term bonds Issue longer-term bonds

– Hedge using interest-rate forwards, Hedge using interest-rate forwards, futures, options, or swapsfutures, options, or swaps

43

11.4 Minimizing the Cost 11.4 Minimizing the Cost of Hedgingof Hedging

• There are sometimes several ways There are sometimes several ways to hedge a transactionto hedge a transaction– Choose the one that minimizes the cost Choose the one that minimizes the cost

of achieving the desired level of risk of achieving the desired level of risk reduction after considering transaction reduction after considering transaction costs, and taxescosts, and taxes

44

11.5 Hedging versus 11.5 Hedging versus InsuringInsuring

– Hedging:Hedging: A contract “to purchase A contract “to purchase 100,000 perfume bottles, six months from 100,000 perfume bottles, six months from now @ $0.25/bottle, payment on receipt” is now @ $0.25/bottle, payment on receipt” is a forward contract (obligation to purchase)a forward contract (obligation to purchase)

– Insuring:Insuring: A contract “to purchase A contract “to purchase up toup to 100,000 perfume bottles, six months from 100,000 perfume bottles, six months from now @ $0.25/bottle, payment on receipt” is now @ $0.25/bottle, payment on receipt” is a a notnot a forward contract (right but no a forward contract (right but no obligation to purchase)obligation to purchase)

45

Hedging versus InsuringHedging versus Insuring

• Recall Recall – Hedging is symmetric, you sacrifice the Hedging is symmetric, you sacrifice the

upside risk to protect you against the upside risk to protect you against the downside riskdownside risk

– Insuring is asymmetric, you maintain Insuring is asymmetric, you maintain the upside risk, but dispose of the the upside risk, but dispose of the downside riskdownside risk

46

Hedging v. Insuring

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

0 0.5 1 1.5 2 2.5 3 3.5 4

Price of Wheat

Revenue from Wheat Hedged Insured

47

11.6 Basic Features of 11.6 Basic Features of Insurance ContractsInsurance Contracts

• ExclusionsExclusions

• CapsCaps

• DeductiblesDeductibles

• Co-paymentsCo-payments

48

11.7 Financial Guarantees11.7 Financial Guarantees

• Financial guaranteesFinancial guarantees are insurance are insurance against credit risk--the risk to you against credit risk--the risk to you that the counterparty will defaultthat the counterparty will default

• A A loan guaranteeloan guarantee is a contract that is a contract that obliges the guarantor to make the obliges the guarantor to make the promised payment on a loan if the promised payment on a loan if the borrower fails to do soborrower fails to do so

49

11.8 Caps and Floors on 11.8 Caps and Floors on Interest RatesInterest Rates

• Some financial instruments, such as Some financial instruments, such as ARMs, offer an interest rate that ARMs, offer an interest rate that varies with a specified prime rate, varies with a specified prime rate, the T-bill rate, LIBOR, et ceterathe T-bill rate, LIBOR, et cetera

• A clause may provide for annual A clause may provide for annual floors, annual caps, global floors, or floors, annual caps, global floors, or global caps on interest rate changesglobal caps on interest rate changes

50

11.9 Options as Insurance11.9 Options as Insurance

• A call (put) option is the right, but not the A call (put) option is the right, but not the obligation, to purchase (sell) a given asset obligation, to purchase (sell) a given asset according to a schedule of prices and according to a schedule of prices and timestimes

• European options have a single strike or European options have a single strike or exercise price, and a single exercise dateexercise price, and a single exercise date

• American options have a single strike or American options have a single strike or exercise price, and may be exercised at any exercise price, and may be exercised at any time before their expiration or maturity datetime before their expiration or maturity date

51

Options as Insurance: Put Options as Insurance: Put IllustrationIllustration

• You have 100 shares of XYZ stock You have 100 shares of XYZ stock currently trading at $100/share, and currently trading at $100/share, and a planning time horizon of 3-monthsa planning time horizon of 3-months

• You wish to pay a small premium to You wish to pay a small premium to insure the current price in 3-monthsinsure the current price in 3-months

• You wish to benefit from any stock You wish to benefit from any stock price risesprice rises

52

Options as Insurance: Put Options as Insurance: Put IllustrationIllustration

• Strategy:Strategy:– Retain your holding of 100 shares in XYZ Retain your holding of 100 shares in XYZ

currently valued at $10,000currently valued at $10,000

– Purchase one round lot of 100 XYZ Purchase one round lot of 100 XYZ European put options with a strike price European put options with a strike price of $100 for a premium of $729.51of $100 for a premium of $729.51

– At the end of 3-months, your holding, as At the end of 3-months, your holding, as a function of XYZ new share price, is:a function of XYZ new share price, is:

53

Hedging with a Put

-2000

0

2000

4000

6000

8000

10000

12000

14000

16000

50 60 70 80 90 100 110 120 130 140 150

Share Price

Share Holding

Value Puts

FV Premium

Total Wealth

54

Put Option on a BondPut Option on a Bond

• The value of a bond depends upon The value of a bond depends upon – the risk-free rate for bonds of that the risk-free rate for bonds of that

maturity maturity

– the value of the bond’s collateralthe value of the bond’s collateral

• Purchasing a put option on the bond Purchasing a put option on the bond gives downside protection, while gives downside protection, while preserving upside potentialpreserving upside potential

55

11.10 The Diversification 11.10 The Diversification PrinciplePrinciple• Diversification:Diversification:

– splitting an investment among many splitting an investment among many risky assets instead of concentrating it risky assets instead of concentrating it all in only oneall in only one

• Diversification Principle:Diversification Principle:– by diversifying across risky assets by diversifying across risky assets

people can sometimes achieve a people can sometimes achieve a reduction in their overall risk exposure reduction in their overall risk exposure with no reduction in their returnwith no reduction in their return

56

Diversification of Diversification of Uncorrected RisksUncorrected Risks

• Assume that you are offered a number Assume that you are offered a number of investment opportunities in various of investment opportunities in various biotechnology firmsbiotechnology firms– The outcome of any of the investments has The outcome of any of the investments has

no effect on any of the others (independent)no effect on any of the others (independent)

– You believe that each firm has a 50% You believe that each firm has a 50% chance of quadrupling your investment, and chance of quadrupling your investment, and a 50% chance of total lossa 50% chance of total loss

57

Invest $100,000 in any Invest $100,000 in any one of the firms:one of the firms:

– If the firm fails (p = 0.50)If the firm fails (p = 0.50)• the expected contribution to your pay-the expected contribution to your pay-

out is 0.50 * $0 = out is 0.50 * $0 = $0$0

– If the firm is successful (p = 0.50)If the firm is successful (p = 0.50)• the expected contribution to your pay-the expected contribution to your pay-

out is 0.5 * 4 * $100,000 = out is 0.5 * 4 * $100,000 = $200,000$200,000

– Expected Pay-off = $0 + $200,000 = Expected Pay-off = $0 + $200,000 = $200,000$200,000

58

Invest $50,000 in any of Invest $50,000 in any of the firms, & $50,000 in the firms, & $50,000 in anotheranother

– If both firm fails (p = 0.25)If both firm fails (p = 0.25)

• the expected contribution to your pay-out is 0.25 * the expected contribution to your pay-out is 0.25 * $0 = $0 = $0$0

– If one firm is successful (p = 0.50)If one firm is successful (p = 0.50)

• the expected contribution to your pay-out is 0.5 * 4 * the expected contribution to your pay-out is 0.5 * 4 * $50,000 = $50,000 = $100,000$100,000

– If both firm are successful (p = 0.25)If both firm are successful (p = 0.25)

• the expected contribution to your pay-out is 0.25 * 4 the expected contribution to your pay-out is 0.25 * 4 * 2 * $50,000 = * 2 * $50,000 = $100,000$100,000

– Expected Pay-off = $0 + $100,000 + 100,000 = Expected Pay-off = $0 + $100,000 + 100,000 = $200,000$200,000

59

ConclusionConclusion

• Investing in one or in two firms has Investing in one or in two firms has the same expected returnthe same expected return

• But...But...

60

But...But...

• We have not analyzed riskWe have not analyzed risk– We will now compute the standard We will now compute the standard

deviations of both strategiesdeviations of both strategies

61

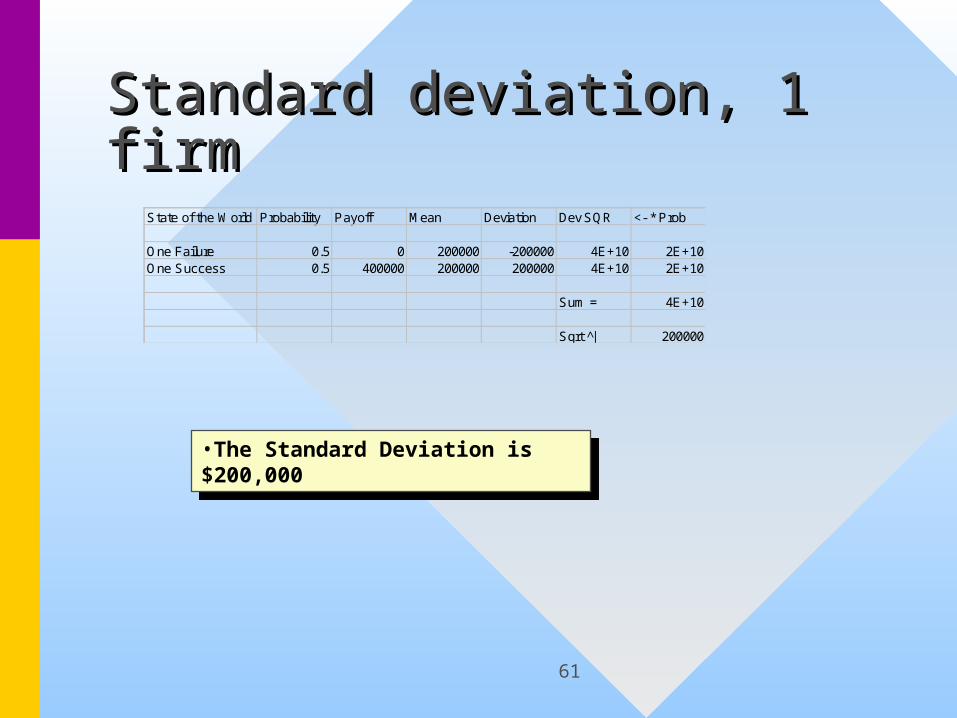

Standard deviation, 1 firmStandard deviation, 1 firmState of the World Probability Payoff Mean Deviation Dev SQR <- * Prob

One Failure 0.5 0 200000 -200000 4E+10 2E+10One Success 0.5 400000 200000 200000 4E+10 2E+10

Sum = 4E+10

Sqrt |̂ 200000

•The Standard Deviation is $200,000•The Standard Deviation is $200,000

62

Standard deviation, 2 Standard deviation, 2 firmsfirms

State of the World Probability Payoff Mean Deviation Dev SQR <- * Prob

One Failure 0.25 0 200000 -200000 4E+10 1E+10One Success 0.5 200000 200000 0 0 0Two Successes 0.25 400000 200000 200000 4E+10 1E+10

Sum = 2E+10

Sqrt |̂ 141421.356

•The Standard Deviation is about $141,000 (c.f. $200,000)

•The Standard Deviation is about $141,000 (c.f. $200,000)

63

Standard deviation, equal Standard deviation, equal investment in “n” firmsinvestment in “n” firms

• Generalizing the argument, it is easy to Generalizing the argument, it is easy to prove that the standard deviation in this prove that the standard deviation in this case is just $200,000/SqrareRoot(n)case is just $200,000/SqrareRoot(n)

• Conclusion: Given the facts of this Conclusion: Given the facts of this example, the risk may be made as close example, the risk may be made as close to zero as we wish if there are sufficient to zero as we wish if there are sufficient securities! In reality, however … securities! In reality, however … n is must be finite, and pharmaceutical projects have a non-zero correlationsn is must be finite, and pharmaceutical projects have a non-zero correlations

64

Correlated Homogeneous Correlated Homogeneous SecuritiesSecurities

• Pharmaceutical projects do have Pharmaceutical projects do have positive correlation (Why?)positive correlation (Why?)

• Loosen the assumptions made Loosen the assumptions made about the correlation, and set it to about the correlation, and set it to ρ, and use the generalization ofρ, and use the generalization of

2,1212122

22

21

21

2 2 wwwwp

65

Correlated Homogeneous Correlated Homogeneous SecuritiesSecurities

• We obtain the relationshipWe obtain the relationship

σσportport= σ= σsecsec *QSRT(ρ + 1/n) *QSRT(ρ + 1/n)

• In the case of n -> Infinity, there In the case of n -> Infinity, there remains the termremains the term

σσportport= σ= σsecsec *QSRT(ρ) *QSRT(ρ)

• This risk is not diversifiableThis risk is not diversifiable

66

Standard Deviations of Portfolios, rho = 0.2, sig = 0.2

0.000.020.040.060.080.100.120.140.160.180.20

0 5 10 15 20 25 30 35 40 45 50

Portfolio Size

Sta

nd

are

Dev

iati

on

67

Standard Deviations of Portfolios, rho = 0.8, sig = 0.2

0.000.020.040.060.080.100.120.140.160.180.20

0 5 10 15 20 25 30 35 40 45 50

Portfolio Size

Sta

nd

are

Dev

iati

on

68

Standard Deviations of Portfolios, rho = 0.5, sig = 0.2

0.000.020.040.060.080.100.120.140.160.180.20

0 5 10 15 20 25 30 35 40 45 50

Portfolio Size

Sta

nd

are

Dev

iati

on

69

Standard Deviations of Portfolios, rho = 0.2, sig = 0.2

0.000.020.040.060.080.100.120.140.160.180.20

0 5 10 15 20 25 30 35 40 45 50

Portfolio Size

Sta

nd

are

Dev

iati

on

Diversifiable Security Risk

Nondiversifiable Security Risk

70

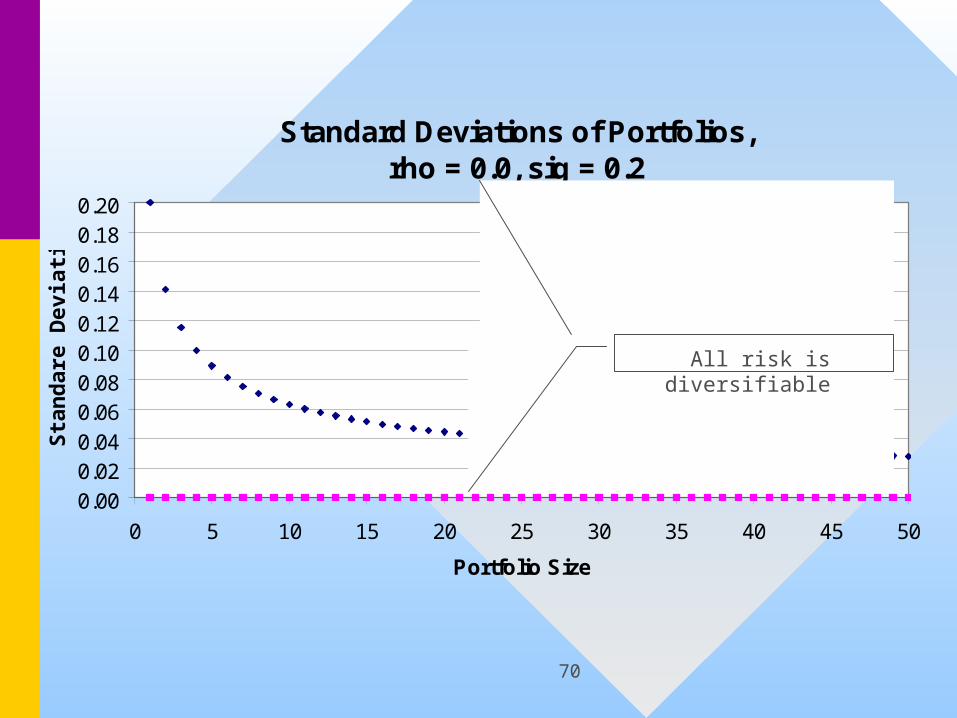

Standard Deviations of Portfolios, rho = 0.0, sig = 0.2

0.000.020.040.060.080.100.120.140.160.180.20

0 5 10 15 20 25 30 35 40 45 50

Portfolio Size

Sta

nd

are

Dev

iati

on

All risk is diversifiable All risk is diversifiable

71

Negative CorrelationNegative Correlation

• Note that as the correlation ranges Note that as the correlation ranges from one to zerofrom one to zero

– the percentage of undiversifiable risk fallsthe percentage of undiversifiable risk falls

– the number of securities necessary to the number of securities necessary to approach this level increasesapproach this level increases

• ……and just for fun, let’s look at a and just for fun, let’s look at a negative correlationnegative correlation

72

Standard Deviations of Portfolios, rho = 1/(1-50) = -0.0204, sig = 0.2

0.000.020.040.060.080.100.120.140.160.180.20

0 5 10 15 20 25 30 35 40 45 50

Portfolio Size

Sta

nd

are

Dev

iati

on

73

Nondiversifiable RiskNondiversifiable Risk

• The graphs illustrate an important The graphs illustrate an important pointpoint– For homogeneous securities (at least), For homogeneous securities (at least),

there is an asymptotic value for the there is an asymptotic value for the least risk a portfolio may containleast risk a portfolio may contain

– For correlations that are strictly For correlations that are strictly positive, there appears to be a level of positive, there appears to be a level of risk that can’t be diversified awayrisk that can’t be diversified away

74

Nondiversifiable RiskNondiversifiable Risk

• For a fund manager, the cost of holding For a fund manager, the cost of holding her assets in either (1) a well diversified her assets in either (1) a well diversified portfolio, or (2) a single stock, differ by portfolio, or (2) a single stock, differ by only (quite low) transaction costsonly (quite low) transaction costs

• In this world of homogeneous securities, In this world of homogeneous securities, she may reduce risk by diversifying she may reduce risk by diversifying some of the risk away at (almost) no some of the risk away at (almost) no costcost

75

LanguageLanguage

• The following groups of word are The following groups of word are similessimiles– Diversifiable risk, individual risk, Diversifiable risk, individual risk,

security-specific risk, irrelevant risksecurity-specific risk, irrelevant risk

– Nondiversifiable risk, market risk, Nondiversifiable risk, market risk, relevant riskrelevant risk

76

11.11 Diversification & 11.11 Diversification & the Cost of Insurancethe Cost of Insurance

• When you purchase insurance, the When you purchase insurance, the premium, p, may be divided into two premium, p, may be divided into two portionsportions– a, the actuary value of the good-faith riska, the actuary value of the good-faith risk

– b, the sales, administration, profits, and b, the sales, administration, profits, and fraudfraud

• The ratio a/p not always as high as one The ratio a/p not always as high as one would like would like

77

Self-InsuranceSelf-Insurance

• Accordingly, accepting some of the risk Accordingly, accepting some of the risk yourself may be advisable in some yourself may be advisable in some situationssituations– When the correlation between risks is not When the correlation between risks is not

highhigh

– when the number of risks is relatively highwhen the number of risks is relatively high

– when the risks are of the same magnitudewhen the risks are of the same magnitude