1 case study: gm in china super team b: lee albert, mark craven, annemarie daepp, juhyung kim,...

Post on 22-Dec-2015

215 views

TRANSCRIPT

1

Case Study: GM in China

Super Team B: Lee Albert, Mark Craven, Annemarie Daepp, Juhyung Kim, Albert Krikken, Ken Syme, Monica Trevett

2

• The Business Environment

• GM Current Position

• Opportunities and Threats

• Recommended Future Strategies

Discussion Points

3

Business Environment in Emerging Markets

• Increased privatization and openness of many formerly bureaucratic closed economies

• Removal of legacies and/or reduction of state interventionism

• Systemic changes: privatization, enterprise restructuring, restructuring of banking and finance

• Regional & global integration based on common principles of private property and free markets

4

Business Environment RiskSpecifically in China

• Protectionist Policy & Government Regulations

• Monetary Policy

• Violation of Intellectual Property

• Underdeveloped Financial Practices

• Underdeveloped Corporate Legal System

5

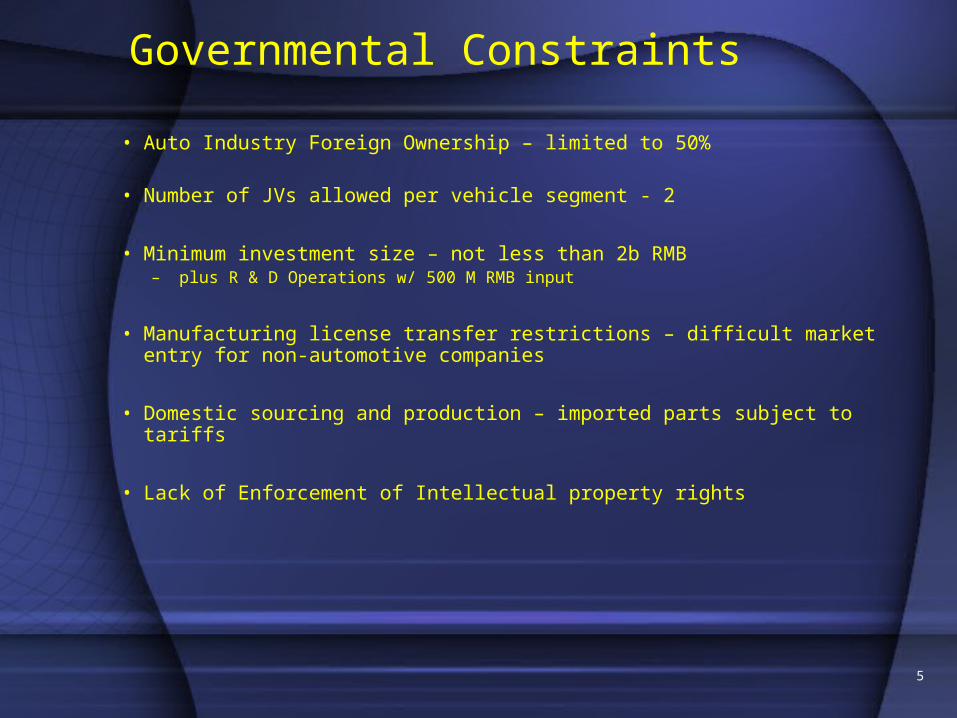

• Auto Industry Foreign Ownership – limited to 50%

• Number of JVs allowed per vehicle segment - 2

• Minimum investment size – not less than 2b RMB– plus R & D Operations w/ 500 M RMB input

• Manufacturing license transfer restrictions – difficult market entry for non-automotive companies

• Domestic sourcing and production – imported parts subject to tariffs

• Lack of Enforcement of Intellectual property rights

Governmental Constraints

6

The GM Chevrolet Spark and the Chery QQ

7

Chinese Market

• Mature market

• Sluggish growth

• Low margins

• Consolidated

• Immature market

• Rapid growth

• High margins

• Fragmented

Global Market

8

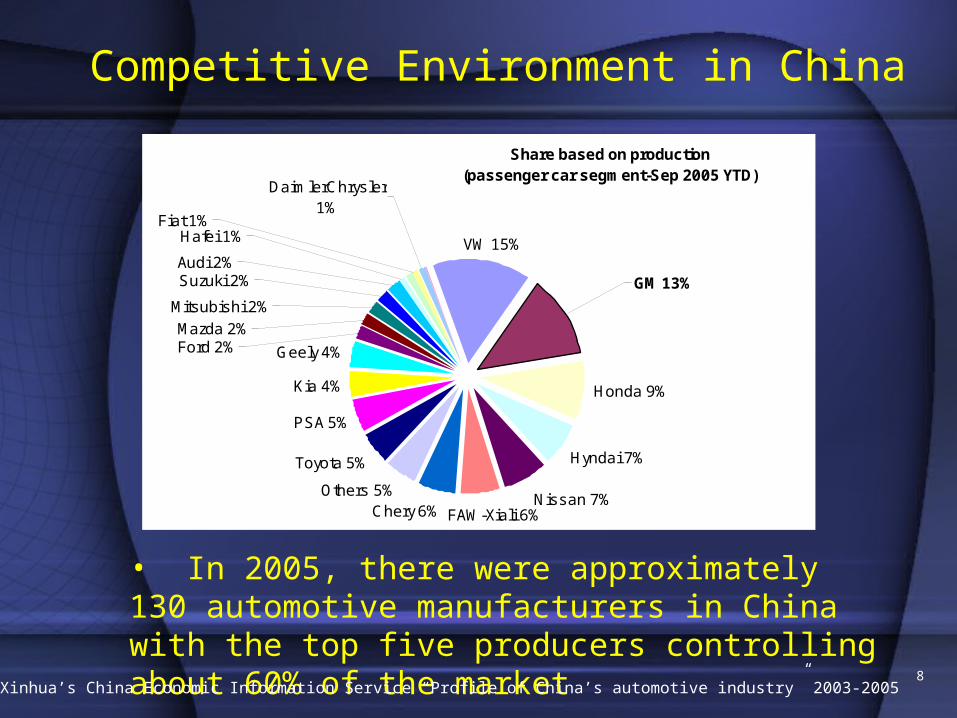

Share based on production(passenger car segment-Sep 2005 YTD)

Nissan 7%FAW-Xiali 6%Chery 6%

Others 5%

Toyota 5%

PSA 5%

Kia 4%

Geely 4%

Hyndai 7%

Honda 9%

VW 15%

GM 13%

DaimlerChrysler 1%

Fiat 1%

Mitsubishi 2%

Audi 2%

Hafei 1%

Suzuki 2%

Mazda 2%Ford 2%

• In 2005, there were approximately 130 automotive manufacturers in China with the top five producers controlling about 60% of the market

Source: Xinhua’s China Economic Information Service “Profile of China’s automotive industry” 2003-2005

Competitive Environment in China

9

• Buyers/Suppliers: Low to medium market influence

• Internal Rivalries: Significant pressure

• Barriers to Entry: Foreign investment regulation and continued intervention post joining WTO

• Substitutes: Population migration to cities, access to public transportation

Strategic Market Analysis

10

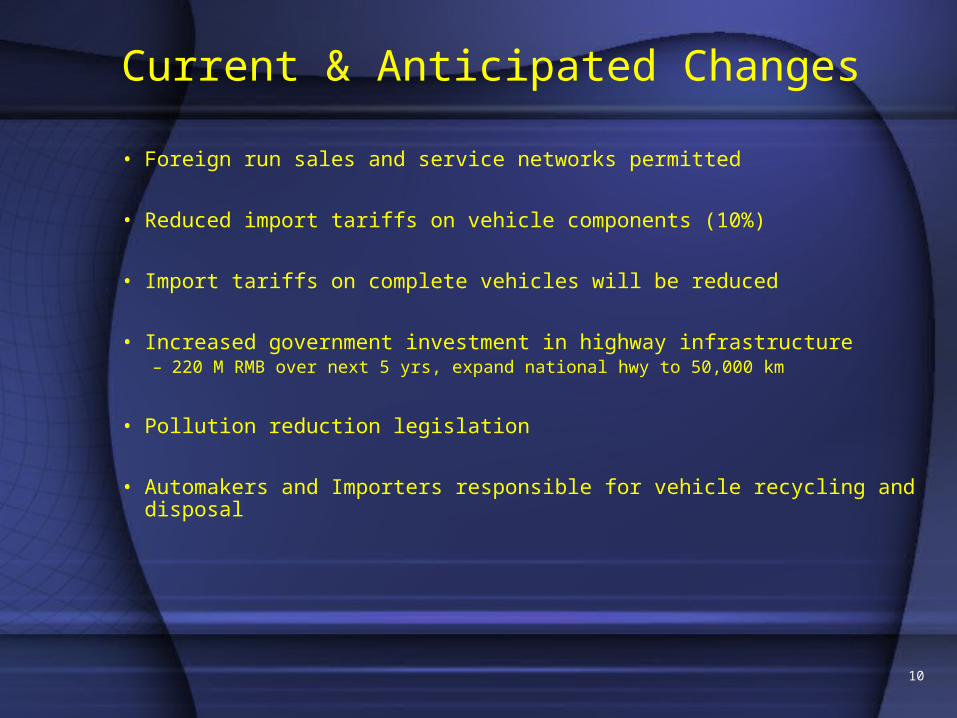

• Foreign run sales and service networks permitted

• Reduced import tariffs on vehicle components (10%)

• Import tariffs on complete vehicles will be reduced

• Increased government investment in highway infrastructure – 220 M RMB over next 5 yrs, expand national hwy to 50,000 km

• Pollution reduction legislation

• Automakers and Importers responsible for vehicle recycling and disposal

Current & Anticipated Changes

11

General Motors in China

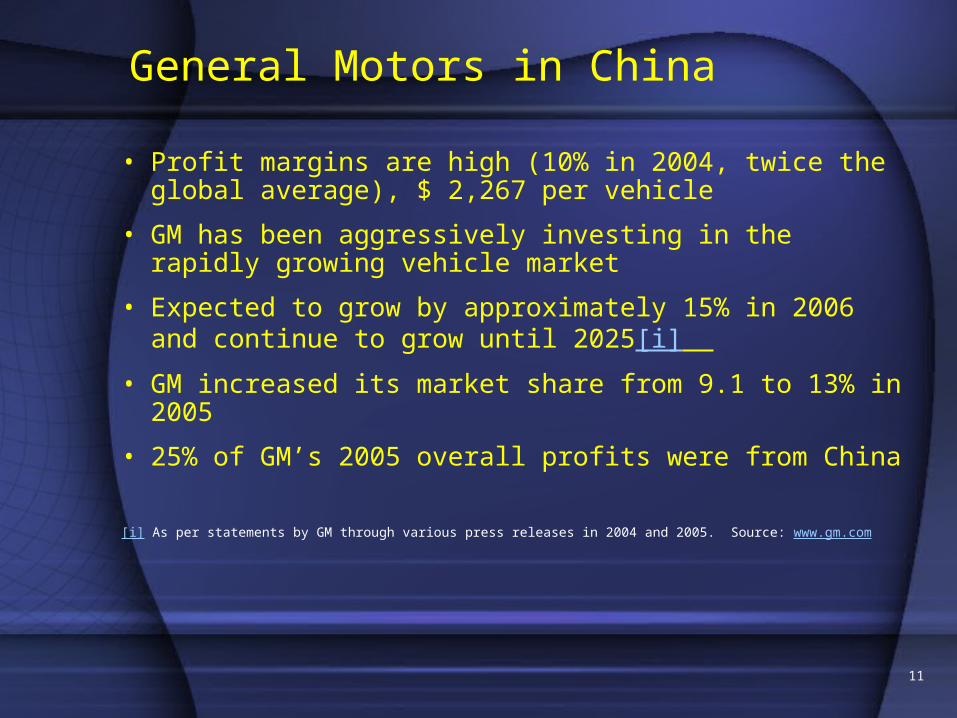

• Profit margins are high (10% in 2004, twice the global average), $ 2,267 per vehicle

• GM has been aggressively investing in the rapidly growing vehicle market

• Expected to grow by approximately 15% in 2006 and continue to grow until 2025[i]

• GM increased its market share from 9.1 to 13% in 2005

• 25% of GM’s 2005 overall profits were from China

[i] As per statements by GM through various press releases in 2004 and 2005. Source: www.gm.com

12

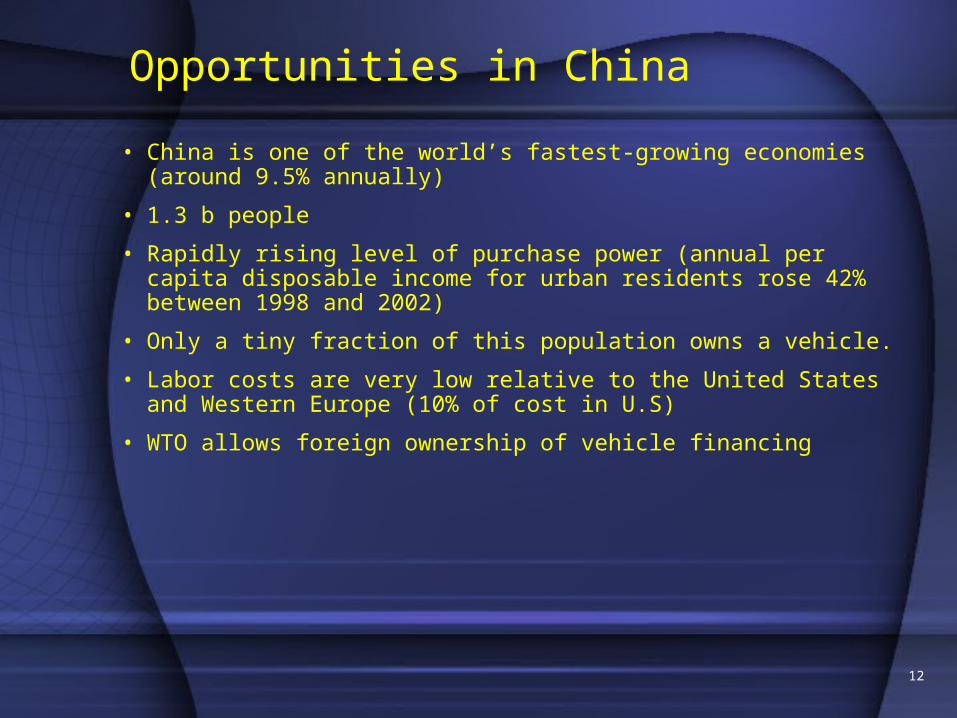

• China is one of the world’s fastest-growing economies (around 9.5% annually)

• 1.3 b people

• Rapidly rising level of purchase power (annual per capita disposable income for urban residents rose 42% between 1998 and 2002)

• Only a tiny fraction of this population owns a vehicle.

• Labor costs are very low relative to the United States and Western Europe (10% of cost in U.S)

• WTO allows foreign ownership of vehicle financing

Opportunities in China

13

• Changes in government policy

• Slower Growth

• Increased Competition

• Overcapacity

• Reduced Margins

• Intellectual Property Risks

Threats in China

14

Strategic Alternatives for GM’s Business in China

• Alternative Fuel R & D

• Convert existing excess capacity to exports

15

Factors in Favor of Alternative Fuel R & D

• 2nd largest oil importer

• “China has six of the world’s ten most polluted cites.”

• Government has set timelines for emissions standards

• Immature infrastructure – opportunity to leap forward to clean-energy technologies

• Access to skilled – low cost human capital

16

Factors Against Alternative Fuel R & D

• Application of technology worldwide not readily accepted

• Infrastructure not immediately ready to support advanced technologies

• Conflicting demands on GM’s R&D resources

17

Factors Against Alternative Fuel R & D

• Recommend that GM don’t pursue specifically for Chinese market• Risk is too high / Payback too long• GM Investment Funds.

• However local, skilled low cost labor should be used to help global alternative fuel development

• Capture benefit of Collaborative agreement with Shanghai’s Jiaotung University and Tongi University

18

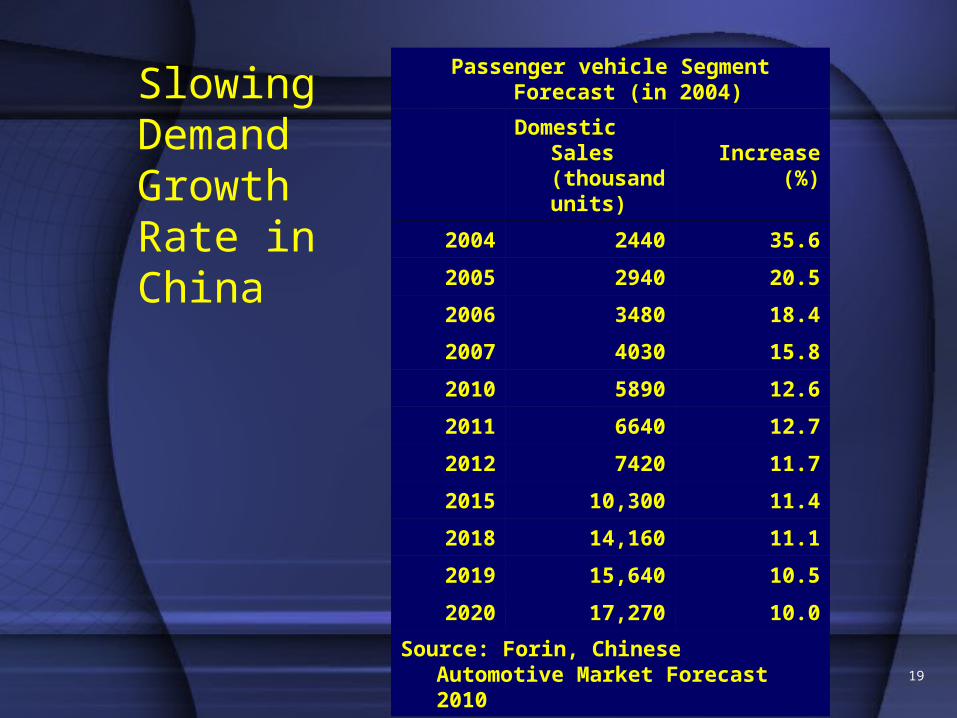

Converting Existing Excess Capacity to Exports

• Domestic and foreign manufacturers will invest more than $15 b by 2008

• Competition in China reduces vehicle prices and profit margin

• Capacity triples to 7 million vehicles

• Most plants are operating at less than 50% capacity.

• Estimated vehicle demand growth rate of 40% required to consume excess capacity

• Predicted growth rates decline

19

Slowing Demand Growth Rate in China

Passenger vehicle Segment Forecast (in 2004)

Domestic Sales

(thousand units)

Increase (%)

2004 2440 35.6

2005 2940 20.5

2006 3480 18.4

2007 4030 15.8

2010 5890 12.6

2011 6640 12.7

2012 7420 11.7

2015 10,300 11.4

2018 14,160 11.1

2019 15,640 10.5

2020 17,270 10.0

Source: Forin, Chinese Automotive Market Forecast 2010

20

Recommendations

• Convert some existing capacity to dedicated export facility

• Use Honda model as benchmark

• Select multiple JV partners

• Use of supply-chain leverage to co-locate key suppliers

21

Strategic Outcomes

• Competitive advantage for global markets

• Opportunity to export low cost parts to global markets

• Opportunity to buyout JV partners should regulations relax

• Hedge against risk of future government policy change

22

Thank you.

Xie Xie.

Cheers!

23