1 capital adequacy & net worth computation t. rajagopal cab,pune

TRANSCRIPT

1

Capital Adequacy &

Net worth Computation

T. RajagopalCAB,PUNE

Capital Adequacy

Capital adequacy means adequate capital. What is adequate capital is decided by the Regulator

from time to time. Traditional approach to sufficiency of capital does not

capture the risk elements in various types of assets in balance sheet/off balance sheet business.

Basel Committee on Banking Supervision published the Basel I frame work in July 1988 prescribing minimum capital adequacy requirements in banks for maintaining soundness and stability of international banking system.

2

Capital Adequacy UCBs were brought under the capital adequacy discipline

w.e.f. March 31,2002 in a phased manner. CRAR norms uniform for all UCBs @ 9% from March

31,2005. Under capital adequacy framework, Balance sheet

assets/off balance sheet items assigned weights according to the prescribed risk weights for credit risk as well as market risks.

As capital is subjected market risks, UCBs are required to maintain unimpaired minimum capital funds equivalent to the presribed ratio on ongoing basis.

3

Why Capital ?

Capital acts as buffer in times of crisis or poor performance by a bank.

Sufficient capital instills depositors confidence.

Adequacy of capital is precondition for licensing of a new bank and continuation of a bank.

4

Capital Statutory Minimum Capital: Section 11 of BR Act: Aggregate value of its paid up capital

and reserves is not less than Rs.1.00 lakh. Share linking to Borrowings: • Unsecured loans: 5% of borrowings• Secured loans: 2.5% of borrowings.• Maximum limit per borrower: 5% of total paid up capital.• Exemptions: UCBs with CRAR of 12% on continuous basis .

Share linking Not mandatory (w.e.f.15.11.2010) Regulatory capital: Capital supervisory authorities require

banks to set aside in order to meet potential losses. (CRAR)

5

Components of Capital Funds

Capital funds for purpose of capital adequacy standard are segregated in to two broad groups.

Tier I capital: also known as core capital, provides the most permanent and readily available support to bank against unexpected losses.

Tier II capital consists of elements that are less readily available.

6

Components of Tier I Capital

Paid up Share Capital Free Reserves (Statutory Reserve, Building

Fund) Non refundable admission fee Capital Reserves - representing surplus arising

out of sale proceeds of assets Surplus in P&L a/c Perpetual Non Cumulative Preference shares

(PNCPS)- not more than 20% of Tier I capital. Innovative Perpetual Debt Instruments (IDPI).

(No to exceed 15% of total Tier I capital)7

Adjustments from Tier I capital

Amounts to be deducted from Tier I capital:a) Amount of intangible assetsb) Losses in current year/brought forward from

previous years.c) Shortfall in NPA provisionsd) Income wrongly recognized on NPAs.e) Provision required for liability devolved on bank.f) Intangible assets like deferred tax etc.,

8

Components of Tier II Capital

Tier II Capital ( not to exceed 100% of tier I capital)

A.Undisclosed Reserves B.Revaluation Reserves – only 45%C. Investment Fluctuation ReserveD. Hybrid Debt Capital Instruments –Perpetual

Cumulative Preference shares/Redeemable Non-Cumulative Preference shares/Redeemable Cumulative Preference shares /LTDs( not to exceed 50% of Tier I)

E. Subordinated debts.

9

Tier II Capital (contd.,)

F. General Provisions & Loss reserves: (Not exceeding 1.25% of total RWA)

a) Excess BDDR.(subject to not used for net NPA calculation)

b) Standard asset provision (entire)

c) Dividend Equalization Fund.

d) Members Welfare Fund.

e) Charity Fund.

f) Centenary Celebration Fund. 10

Computation of net value of assets

• Before applying risk weight on the book value of assets, we need to compute net value by adjusting the margin with the book value. This margin would be required provisions against that asset class arising out of erosion in its value.

11

CRAR – Risk weights

Important Risk weights: Balances with RBI -- 0% Balances with banks -- 20% Investment in GOI Sec. -- 2.5% Investment in State Govt Sec. – 22.5% Loans and advances: Loans guaranteed by GOI/Stae Govt. -0% Real Estate exposure: Resd. Ind.Housing Loan upto Rs.30 lakh ( LTV < 75%) -- 50% Resd. Ind.Housing Loan above Rs.30 lakh (LTV < 75%)-- 75% LTV > 75% irrespective of the amount --100% Gold/silver loan upto Rs.1.0 lakh -- 50%

12

CRAR – Risk weights (contd.,)

• Commercial Real Estate Exposure --100%• Co-op / group housing societies --100%• Consumer/ personal loan --125%• Loans against security of shares/ debentures --127.5%• Secured staff loan --20%• Premises, furniture & fixtures --100%• Other assets --100%• Bills discounted against LC of banks --20%• Genral LC, BG issued -100%• Certain transaction related LCs --50%

13

New Guidelines

Advances guaranteed by Credit Risk Guarantee Fund Trust for Low Income Housing (CRGFTLIH):

It will attract zero risk weight If NPA, it will attract zero provisioning.

14

New Guidelines As maintenance of the Special reserve created under sec

36(1) (viii) of the Income Tax Act, 1961 leads only to a timing difference of tax liability, as per the Accounting Standard 22 of ICAI on ‘Accounting for taxes on income’, Deferred tax liability (DTL) would have to be created on this Special Reserve. Hence, only the net amount of such Reserves (net of tax payable) should be taken into account for the purpose of computation of Tier I capital -August 8, 2013

IFR would qualify for T II capital for T II banks only if it is more than 5%,

full IFR eligible for TII for T I banks

15

Computation of CRAR Off-Balance Sheet items: Multiply the face amount of each of the

balance sheet items by “credit conversion factors” and again multiply by the weights attributable to the relevant counter-party in order to get the amount of exposure.

Net Off: banks may net off the following from the outstanding balances (funded and non funded) before assignment of risk weights.

• i)advances collateralized by cash margins or deposits• ii)Provisions made for depreciation or bad debts(BDDR and IDR)

• iii)Claims received from DICGC/ECGC . Total Capital funds to be divided by total risk weighted asset

including off balance sheet items and multiplied by 100. The result will be CRAR in percentage

16

CRAR Calculation

• On Balance Sheet Assets (OBSA)

17

Asset Book value Risk Wight Risk Weighted Value (RWV)

Cash 100 0 0

Bank balances 150 20 30

Advances 400 100 400

Investments 200 50 100

Fixed Assets 100 100 100

Other assets 100 20 20

Total (X) 1050 650

CRAR calculation• Off-Balance sheet Items (OBSI)

18

Item Book value(BV)

Credit conversion factor (CCF)

Credit Equivalent (CE)

Risk Weight(RW)% RWV

Bank Guarantee

200 50 100 100 100

Letters of credit

500 20 100 50 50

Total (Y) 700 - - - 150

CRAR Calculation

• Total Risk Weighted Assets (TRWA)=(RWA of OBSA)+(RWV of OBSI)

• = (X+Y)=(650+150)=800.• Since prescribed CRAR is 9% • Capital funds required would be 9% of TRWA

i.e., 9% of 800=72

19

Networth

• Net worth means real or exchangeable value of the bank’s paid up capital and reserves.-{direct}

• The excess of realizable value of assets over the aggregate outside liabilities would represent the net worth.{indirect}

• It is nothing but assessing the financial soundness of a bank.

20

COMPUTATION OF NETWORTH

1 PAID UP SHARE CAPITAL COLLECTED FROM REGULAR MEMBERS HAVING VOTING POWERS

2 + PERPETUAL NON-CUMULATIVE PREFERENCE SHARES (PCNPS) 3 + CONTRIBUTIONS RECIVED FROM ASSOCIATES/NOMINAL

MEMBERS WHERE THE BYE LAWS PERMIT ALLOTMENT OF SHARES TO THEM AND PROVIDED THERE ARE RESTRICTIONS ON WITHDRAWALS OF SUCH SHARES AS APPLICABLE TO REGULAR MEMBERS

4 +CONTRIBUTION /NON REFUNDABLE ADMISSION FESS COLLECTED FROM THE NOMINAL AND ASSOCIATE MENMBERS WHICH IS HELD SEPARATELY AS RESERVES UNDER AN APPROPRIATE HEAD SINCE THESE ARE NOT REFUNDABLE

5 +FREE RESERVES INCLUDING BUILDING FUND CAPITAL RESERVES ETC BUT EXCLUDING REVALUATION RESERVES

6 +CREDIT BALANCE IN P&L A/C7 (-) DEBIT BALANCE IN P&L A/C8 (-) AMOUNT OF INTANGIBLE ASSETS

NET WORTH BOOK VALUE

21

ADJUSTMENTS FOLLOWING INSPECTION FINDINGS

9 (+) ANY ITEMS INCLUDED UNDER LIABILITIES OTHER THAN PROVISIONS WHICH MAY NOT BE OUTSIDE LIABILITIES

10 (+) ANY EXCESS OF SURPLUS PROVISIONS OR PROVISIONS NO LONGER REQUIRED TO THE EXTENT IT IS NOT ADJUSTED FOR COMPUTATION OF NET NPAs

11 (-) ADDITIONAL LOAN LOSS PROVISIONS REQUIRED12 (-)ADDITIONAL INVESTMENT (DEPRECITATION) PROVISION REQUIRED13 (-) PROVISION REQUIRED FOR LOSSES IN OTHER ASSETS14 (-) PROVISIONS REQUIRED FOR LIKELY LOSSES IN OFF BALANCE SHEET

ITEMS15 (-) ADDITIONAL PROVISIONS REQUIRED FOR ANY OTHER LIABILITIES (e.g

PAYMENT OF INTEREST ON DEPOSITS /BORROWINGS, TAX, GRATUITY PENSION, BONUS ETC

16 (-)ANY LIABILITIES LIKELY TO DEVOLVE ON THE BANK BUT NOT RECOGNISED

17 (-) INTANGIBLES18 (-)UNRELIASED INTEREST ON NPAs TAKEN TO INCOME19 (-)MISCELLANEOUS EXPENDITURE CAPITALISED20 (-) SHORTFALL IN PROVISIONING IN ANY OTHER ITEM

ASSESSESSED NET WORTH OF REAL OR ECCHANGEABLE VALUE OF PAID UP CAPITAL AND RESERVES

22

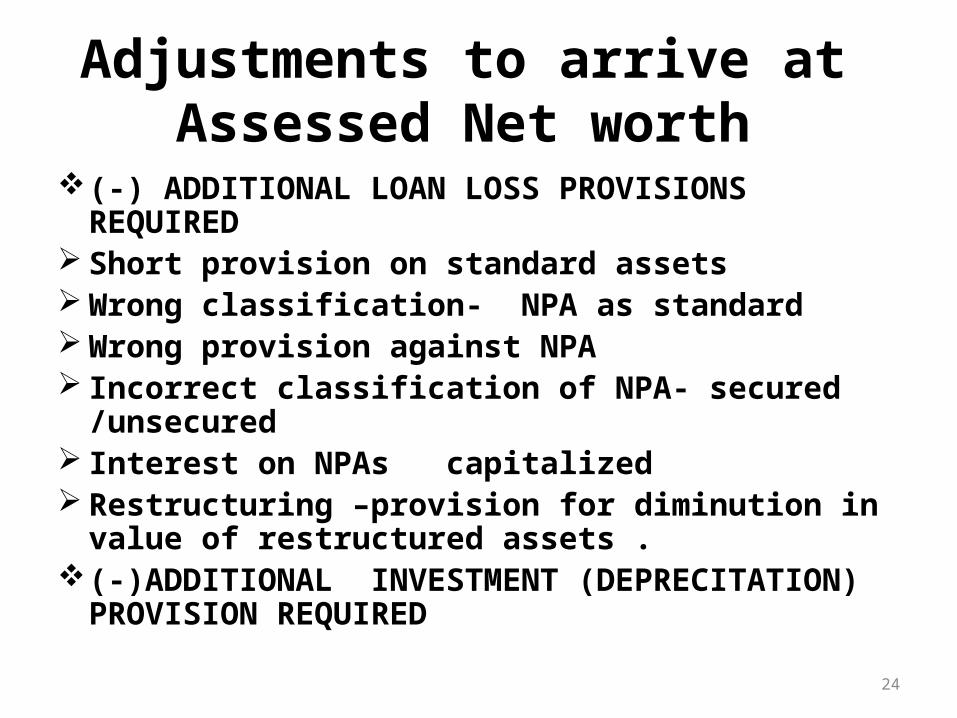

Adjustments to arrive at Assessed Net worth

(+) ANY ITEMS INCLUDED UNDER LIABILITIES OTHER THAN PROVISIONS WHICH MAY NOT BE OUTSIDE LIABILITIES

(+) ANY EXCESS OF SURPLUS PROVISIONS OR PROVISIONS NO LONGER REQUIRED TO THE EXTENT IT IS NOT ADJUSTED FOR COMPUTATION OF NET NPAs

Standard Assets provision (surplus) IFR Surplus BDDR

23

Adjustments to arrive at Assessed Net worth

(-) ADDITIONAL LOAN LOSS PROVISIONS REQUIRED Short provision on standard assets Wrong classification- NPA as standard Wrong provision against NPA Incorrect classification of NPA- secured /unsecured Interest on NPAs capitalized Restructuring –provision for diminution in value of

restructured assets .(-)ADDITIONAL INVESTMENT (DEPRECITATION)

PROVISION REQUIRED

24

Adjustments to arrive at Assessed Net worth

PROVISION REQUIRED FOR LOSSES IN OTHER ASSETS Inter branch reconciliation. Inter bank reconciliation – fraud/ regulatory comfort

Long outstanding entries. Suspense debit entries. unpaid expenditures. Charging of depreciation. Non bkg asset–track record? Hiding NPAs?.Selling to same

borrower group. Accumulated loss, unamortised amounts. Inter branch adjustment A/c

25

Adjustments to arrive at Assessed Net worth

Premises, Furniture, Stationery stock. Interest receivable on G. Sec, FDs, Deep

discount bonds, T Bills.Gratuity, leave encashment, pension• (-) PROVISIONS REQUIRED FOR LIKELY LOSSES IN

OFF BALANCE SHEET items • (-) ADDITIONAL PROVISIONS REQUIRED FOR ANY

OTHER LIABILITIES • PAYMENT OF INTEREST ON DEPOSITS

/BORROWINGS,

26

Adjustments to arrive at Assessed Net worth

(-)ANY LIABILITIES LIKELY TO DEVOLVE ON THE BANK BUT NOT RECOGNISED

(-)Fraud • (-) INTANGIBLES• (-)UNRELIASED INTEREST ON NPAs TAKEN TO INCOME• (-)MISCELLANEOUS EXPENDITURE CAPITALISED• (-) SHORTFALL IN PROVISIONING IN ANY OTHER ITEM • After adjustments we get ASSESSESSED NET WORTH OR

REAL AND EXCHANGEABLE VALUE OF PAID UP CAPITAL AND RESERVES

27

Net Worth V/S Capital (why difference)

CRAR• Revaluation Reserve

availabel (45%)• Entire Stnd. asset provision

and excess BDDR provisions (1.25% of RW) is eligible.

• Funds raised through IPDI & Debt Capital Instruments , LTDs– permitted

• TIER II capital not to exceed TIER I in CRAR.

Net worth• Revaluation Reserve not

applicable• only excess stnd. asset

provision and excess BDDR eligible,( no ceiling of 1.25% of RW )

• not part of net worth.

28

29

THANK YOU