1 assal – viii conference on insurance regulation and supervision in latin america regional...

TRANSCRIPT

1

ASSAL – VIII Conference on Insurance Regulation and Supervision in Latin America

Regional Seminar on Capital Adequacy and Risk-based Supervision

Risk Mitigation through Reinsurance and Other Means

May 11, 2007

Bryan Fuller - NAIC Senior Reinsurance Manager

2

Outline

• Purposes and Benefits of Reinsurance

• Types of Reinsurance • Risk Management Framework • Alternative Risk Transfer

• Captives, Finite Risk, Contingent Capital

• Derivatives, Securitization

3

Elements of ReinsuranceReinsurance is a form of insurance.There are only two parties to the reinsurance contract - the Reinsurer and the Reinsured - both of whom are insurers, i.e. entities empowered to insure.The subject matter of a reinsurance contract is the insurance liability of the Reinsured undertaken by it under insurance policies issued to its own policyholders.A reinsurance contract is an indemnity contract.

4

What Reinsurance Does

1. It converts the risk of loss of an insurer incurred by the reinsured under its policies according to its own needs.

2.It redistributes the premiums received by the reinsured, which now belong to the reinsured, according to its own business needs.

5

What Reinsurance Does Not Do

Reinsurance does not:

Convert an uninsurable risk into an insurable risk.

Make loss either more or less likely to happen.

Make loss either greater or lesser in magnitude.

Convert bad business into good business.

It is not Alchemy.

Reinsurance is not banking – it is not the lending of money but it can have the same effect.

Reinsurance is not a security.

6

Five Functions of Reinsurance1. Capacity / Spreading Risk

Ability to write more premium while maximizing

principle of insurance.

2. Loss Control / Catastrophe Protection

Minimize financial impact from losses.

3. FinancingProviding financial resources for growth.

4. StabilizationMinimize variations in financial results.

5. ServicesFacilitate operations of insurance

companies.

7

Capacity

Refers to an insurer’s ability to provide a high limit of insurance for a single risk, often a requirement in today’s market.Reinsurance can help limit an insurer’s loss from one risk to a level with which management and shareholders are comfortable.Most states require that the maximum “net retention” from one risk must be less than 10% of policyholders’ surplus.

8

Catastrophe ProtectionObjective is to limit adverse effects on P&L and surplus from a catastrophic event to a predetermined amount.

Covers multiple smaller losses from numerous policies issued by one primary insurer arising from one event.

9

Financing

It is growing and needs additional surplus to maintain acceptable premium to surplus ratios.

Unearned premium demands reduce surplus.

In a down cycle, underwriting results are bad and reduce surplus.

Investment valuation negatively impacts surplus.

Marketing considerations dictate that an insurer enter new lines of business or new territories.

10

StabilizationMarketing ConsiderationMarketing ConsiderationPolicyholders and stockholders like to be identified with a stable and well managed company.

Management ConsiderationManagement ConsiderationPlanning for long term growth and development requires a more stable environment than an insurance company’s book of business is apt to provide.

11

Services

1. Claims Audit

2. Underwriting

3. Product Development

4. Actuarial Review

5. Financial Advice

6. Accounting, EDP and other systems

7. Engineering - Loss Prevention

12

Excess of Loss

Treaty

Quota Share Surplus Share Per Risk Per Occurrence Aggregate

Pro RataSemi AutomaticOR Automatic

Certificate

Facultative

Reinsurance Contracts

Pro Rata Excess of Loss

Proportional Reinsurance

Non-Proportional Reinsurance

Other Considerations:• Occurrence vs. Claims Made• Prospective vs. Retroactive

Reinsurance Contracts Basics

13

Reinsurance Forms

FacultativeProtects individual risks

Offer and acceptance basis.

Reinsurer retains the right to accept or reject each risk.

Supported by a Certificate

Certificate attaches to the conditions on the underlying insurance policy

Cession is optional

Individual Risk

TreatyProtects a large block of business.The reinsurer does not have the right of rejection on a per risk basis.

Supported by a contract

Pre-agreed conditions

Cession is obligatory

Acceptance is automatic

Book of Business

14

Types of AgreementsTypes of Agreements

• Quota Share

• Surplus Share

• Excess of Loss

Proportional

15

Types of AgreementsTypes of Agreements

Quota Share: Simplest type, reinsurer and reinsured share in every loss and in the premiums at a fixed percentage.

Example: Retention 80% / Reinsurance 20%

Policy Limit

$100,000

$200,000

Retained Amount – 80%

$ 80,000

$160,000

Reinsured Amount – 20%

$20,000

$40,000

16

Impact of Quota Share Quota Share 80%Commisson Rate 30% 6/30/05 80% 6/30/06Override Commission 5% Before Q/S After

Reinsurance Reinsurance Reinsurance---------------- ------------------------ ----------------------

INCOME STATEMENT------------PREMIUMS WRITTEN 10,000,000 (8,000,000) 2,000,000CHANGE IN UPR 4,000,000 (3,200,000) 800,000------------ ---------------- ------------------------ ----------------------PREMIUMS EARNED 6,000,000 (4,800,000) 1,200,000------------ ---------------- ------------------------ ----------------------LOSSES INCURRED 3,000,000 (2,400,000) 600,000LOSS EXP.INCURRED 550,000 (440,000) 110,000OTHER UND. EXPENSES 3,000,000 (2,800,000) 200,000------------ ---------------- ------------------------ ----------------------UNDERWRITING DEDUCTIONS 6,550,000 (5,640,000) 910,000

---------------- ------------------------ ----------------------UNDERWRITING INCOME (550,000) 840,000 290,000INVESTMENT INCOME 250,000 250,000OTHER INCOME/LOSSTAXES 0 365,000

---------------- ------------------------ ----------------------NET INCOME (300,000) 840,000 175,000

========= ============= ============LOSS RATIO 59.17% 59.17%PW/Surplus 285.71% 57.14%Commission Ratio 30% 10%

17

80% Quota ShareASSETS Before Q/S After Reinsurance--------------- Reinsurance Reinsurance -------------------------------INVESTMENTS & CASH 20,980,000 -5,200,000 15,780,000AGENTS' BALANCES 1,650,000 1,650,000REINSURANCE RECOV. 150,000 150,000MISC. ASSETS 135,000 135,000

---------------------- - -------------------------------TOTAL ASSETS 22,915,000 -5,200,000 17,715,000======= =========== = ===============LIABILITIES---------------LOSSES & LAE 15,250,000 -2,840,000 12,410,000REINSURANCE PAYABLE 450,000 450,000UNEARNED PREMIUMS 4,000,000 -3,200,000 800,000OTHER EXP. & TAXES 150,000 150,000MISC. LIABILITIES 65,000 65,000

---------------------- - -------------------------------TOTAL LIABILITIES 19,915,000 -6,040,000 13,875,000

---------------------- - -------------------------------CAPITAL AND SURPLUSCAPITAL 2,750,000 2,750,000UNASSIGNED SURPLUS 750,000 750,000REINS.BEN. 840,000 840,000

---------------------- - -------------------------------POLICYHOLDERS' SURPLUS 3,500,000 840,000 4,340,000

---------------------- - -------------------------------TOTAL LIAB. AND SURPLUS 23,415,000 -5,200,000 18,215,000

=========== = ===============Ratio of liab. to surplus 569.00% 319.70%

18

Surplus Share: Greater flexibility. Reinsured selects retention each risk, and cedes multiples of the retention (lines) to the reinsurer.

Types of AgreementsTypes of Agreements

Compared ceded amount to policy limit. Create a proportion. Reinsurer chares in that proportion of loss and premiums for each loss under that policy.

Policy Limit

$20,000

$40,000

$60,000

Reinsurer’s Share

0

50%

66.66%

Reinsured’s Share

100%

50%

33.33%

19

Both Always Pay Both Always Pay ProportionateProportionate

Share of Share of AnyAny Loss Loss

Quota Share Vs. Surplus ShareQuota Share Vs. Surplus Share

Cession % the SameCession % the Samefor every riskfor every risk

Protects Cedent’s EntireProtects Cedent’s EntireBookBook

Always ObligatoryAlways Obligatory

Cession % Varies BasedCession % Varies Basedon Size of each Risk andon Size of each Risk andceding company retentionceding company retention

Used Mostly for LargerUsed Mostly for LargerRisksRisks

Can Be Obligatory orCan Be Obligatory orNon-ObligatoryNon-Obligatory

QSQS SurplusSurplus

20

Excess Of LossExcess Of Loss

Reinsured retains a predetermined dollar amount (the retention). The reinsurer then indemnifies loss excess of that retention up to a stated limit.

• Per risk excess of loss

• Per risk aggregate excess of loss

• Per occurrence excess

• Aggregate Excess of Loss (Catastrophe)

21

Excess Of LossExcess Of LossWith excess of loss reinsurance no insurance is ceded and no sharing is involved. The reinsurer promises to reimburse the reinsured company for losses above a set retention in return for a stated premium rather than promising to share premiums and losses based on some proportional basis

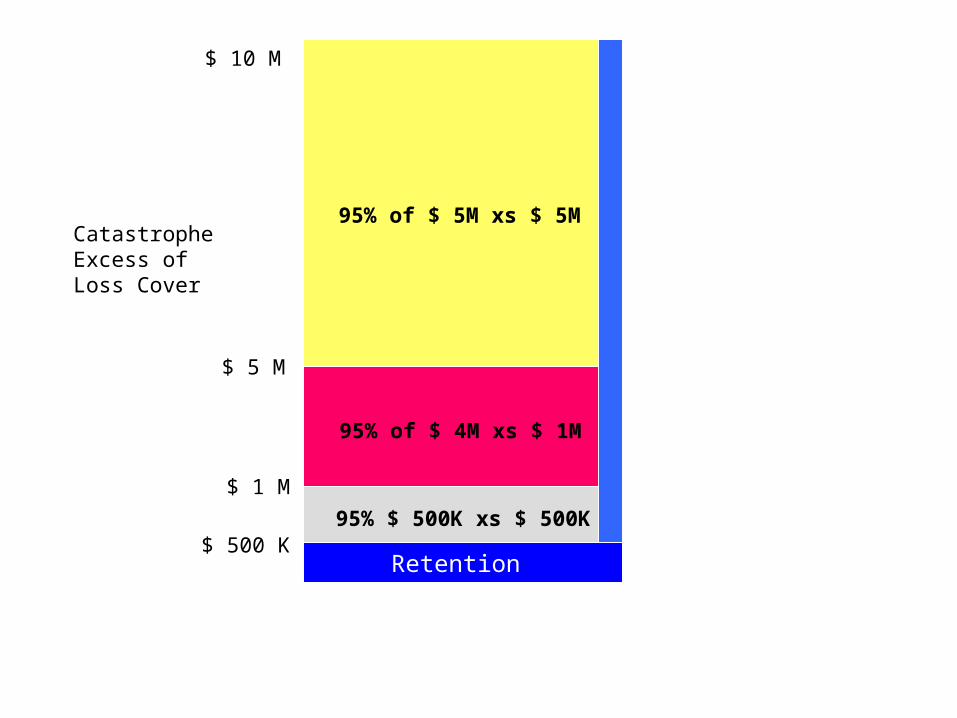

Excess of loss reinsurance is frequently provided in layers with the retention at each layer equal to the reinsured company’s retention plus the reinsurance limit of the layer(s) above. As the limits of the layer are exhausted the next layer of excess reinsurance becomes available.

Retention

20

95% of $ 5M xs $ 5M

95% of $ 4M xs $ 1M

95% $ 500K xs $ 500K

$ 5 M

$ 1 M

$ 500 K

Catastrophe Excess of Loss Cover

$ 10 M

23

Impact of Excess of Loss 500 XS 500 6/30/05 6/30/06Premiums = 12% PW Before After

Reinsurance Reinsurance Reinsurance-------------------- ------------------------------ ----------------------------

INCOME STATEMENT---------------PREMIUMS WRITTEN 10,000,000 (1,200,000) 8,800,000CHANGE IN UPR 4,000,000 (600,000) 3,400,000--------------- -------------------- ------------------------------ ----------------------------PREMIUMS EARNED 6,000,000 (600,000) 5,400,000--------------- -------------------- ------------------------------ ----------------------------LOSSES INCURRED 3,000,000 (420,000) 2,580,000LOSS EXP.INCURRED 550,000 0 550,000OTHER UND. EXPENSES 3,000,000 0 3,000,000--------------- -------------------- ------------------------------ ----------------------------UNDERWRITING DEDUCTIONS 6,550,000 (420,000) 6,130,000

-------------------- ------------------------------ ----------------------------UNDERWRITING INCOME (550,000) (180,000) (730,000)INVESTMENT INCOME 250,000 250,000OTHER INCOME/LOSSTAXES 0 0

-------------------- ------------------------------ ----------------------------NET INCOME (300,000) (180,000) (480,000)

========== =============== ==============LOSS RATIO 59.17% 57.96%PW/Surplus 285.71% 265.06%Commission Ratio 30% 30%

24

Impact of Excess of LossBalance Sheet 6/30/05 6/30/06ASSETSINVESTMENTS & CASH 20,980,000 -1,200,000 19,780,000AGENTS' BALANCES 1,650,000 1,650,000REINSURANCE RECOV. 150,000 150,000MISC. ASSETS 135,000 135,000

---------------------- ------------------------- -------------------------------TOTAL ASSETS 22,915,000 -1,200,000 21,715,000======= =========== ============ ===============LIABILITIES---------------LOSSES & LAE 15,250,000 -420,000 14,830,000REINSURANCE PAYABLE 450,000 450,000UNEARNED PREMIUMS 3,500,000 -600,000 2,900,000OTHER EXP. & TAXES 150,000 150,000MISC. LIABILITIES 65,000 65,000

---------------------- ------------------------- -------------------------------TOTAL LIABILITIES 19,415,000 -1,020,000 18,395,000

---------------------- ------------------------- -------------------------------CAPITAL AND SURPLUSCAPITAL 2,750,000 2,750,000UNASSIGNED SURPLUS 750,000 750,000REINS.BEN. -180,000 -180,000

---------------------- ------------------------- -------------------------------POLICYHOLDERS' SURPLUS 3,500,000 -180,000 3,320,000

---------------------- ------------------------- -------------------------------TOTAL LIAB. AND SURPLUS 22,915,000 -1,200,000 21,715,000

=========== ============ ===============Ratio of liab. to surplus 554.71% 554.07%

Types of AgreementsTypes of Agreements

EXCESS OF LOSS REINSURANCE

Type of Loss

Type of Reinsurance

Per RiskExcess of

Loss

Per Occurrence

Excess of Loss

AggregateExcess of Loss

Single LossExceeding Retention

CoveredSometimes

CoveredNot Covered

Accumulation of Losses in Single OccurrenceExceeding Retention

Not Covered Covered Not Covered

Total Net RetainedLosses Over YearExceeding Retention

Not Covered Not Covered Covered

26

Catastrophe

2nd Excess1st Excess

Surplus Share

RetentionQuotaShare

Reinsurance Program Example

$ L

oss

$ L

oss

ProportionalProportional

Non-Non-ProportionalProportional

27

Purpose of Reinsurance Regulation

Police the Solvency of Reinsurers and Ceding Insurers

Ensure the Collectability of Reinsurance Recoveries

Establish and Maintain a Method of Accurate Reporting of Financial Information Relied Upon by Regulators, Insurers and Investors

Lacks the Consumer Protection Component Necessary for Primary Insurers

Focuses on the Reinsurance Transaction

28

Regulation of Reinsurers

U.S. reinsurers are subject to the same entity regulation as U.S. primary insurers, e.g., risk-based capital, holding company laws, state licensing laws, annual statement requirements, triennial examinations and investment laws.

The exception is no regulation of rates and forms.

29

Risk Management Framework

UnderwritingCreditMarketOperationalLiquidityStrategic

Insurer key risks might be categorized under the following major headings:

30

Underwriting

Underwriting risks are those associated with both the perils covered by the specific line of insurance (fire, death, motor accident, windstorm, earthquake, etc.) and the risk mitigation processes used to manage the insurance business.

31

Underwriting

Underwriting Process RiskPricing RiskProduct Design RiskClaims Risk (for each peril)Economic Environment RiskNet Retention RiskPolicyholder Behavior RiskReserving (Provisioning) Risk

32

Credit Risk

Credit risk is the inability or unwillingness of a counterparty to fully meet its on- or off balance sheet contractual financial obligations. The counterparty could be an issuer, a debtor, a borrower, a broker, a policyholder, a reinsurer, or a guarantor.

33

Credit Risk

Asset classes in which it is willing to invest Government and corporate bonds, mortgages, equities, etc.

Type of credit activity, collateral security, or real estate and type of borrower;Range of exposures in each asset class

Government bonds 10–20%, marketable corporate bonds 20–40%, mortgages 10–30%, equities 5–10%)

Maximum exposure to a given credit, issuer, industry sector, or counterparty

Chosen to limit the possible impact of a default on the surplus of the insurer)

Transactions or exposures involving connected or related entities.

An insurer might define its credit risk in terms of:

34

Market RiskMarket risks relate to the volatility of the market values of assets and liabilities due to future changes of asset prices(/yields/returns). In this respect, the following should be taken into account:

Market risk applies to all assets and liabilities.

35

Market RiskMarket risk must recognize the profit sharing linkages between the asset cash flows and the liability cash flows (e.g., liability cash flows are based on asset performance).Market risk includes the effect of changed policyholder behavior on the liability cash flows due to changes in market yields and conditions.

36

Operational RiskThe identification of insurer operational risk involves considering all the key functional areas of the insurer from each of the following perspectives:

Human capital risk (for example, employing people with the appropriate skills and experience)Management control risk (for example, including appropriate sets of controls ininternal processes and using and communicating those controls effectively)

37

Operational RiskSystem risks (for example, ensuring that systems used in the operation of the insurer are adequate, appropriate, reliable, and scalable, and have adequate security, backups, and disaster recovery plans)Strategic risks (for example, addressing threats to operations from competitors)Legal risk (for example, complying with all laws and regulations in the jurisdictions in which the insurer operates; employing best business practices and standards of corporate governance; pro-actively addressing policyholder expectations).

38

Risk Aggregation

39

Solvency I - ReinsuranceAccording to the present EU legislation (Solvency I) you will get a relief on capital up to 50 % for non-life insurance (30 % quota share will give 30 % relief while 60 % will give 50 %). This will change with Solvency II and the quality of the reinsurer will also be taken account of in the form a credit risk rating.

40

Solvency II - Aims

Establish solvency standard to match risksEncourage risk control in line with IAIS principlesHarmonise across the EUAssets and liabilities on fair value basis consistent with IASB if possible

41

Solvency II – New RegulationsSome European supervisors are already attempting to meet the aims set for Solvency II

United Kingdom, Switzerland, Sweden (Life Insurance Only)

In all cases, the new regulation is based on marking assets and liabilities to market and capital requirements based on scenario tests or economic modelling.

42

Findings – Technical Provisions

Problem areas noted were:Lack of resources, time and experienceLack of data and choosing actuarial assumptionsDerivation of Risk MarginsTreatment of Reinsurance

Wide range of methods used by companies to produce results

43

Credit Risk – Factor ApproachRating CEIOPS Rating Bucket Factor

AAA I – Extremely Strong 0.008%

AA II – Very Strong 0.056%

A III – Strong 0.66%

BBB IV – Adequate 1.312%

BB V – Speculative 2.032%

B VI – Very Speculative 4.446%

CCC or Lower

VII – Extremely Speculative

6.95%

Unrated VIII – unrated 1.6%

SCR credit risk = MV of exposure * duration * factor

44

Solvency II – Reinsurance Implications

Reinsurance constitutes exchange of insurance risk (primarily underwriting & accumulation) for asset risk:

Asset risk carries a lower capital charge than insurance risk, thus reinsurance can be an effective way to manage regulatory capital needs

Factor based models do not distinguish between proportion and non-proportional reinsurance

Risk mitigating effect of non-proportional reinsurance compared to ceding of profits are reflected more adequately within simulation based models

45

Effect of Reinsurance on Solvency RulesReinsurance provides:

Capital relief in MCR (Minimum Capital Requirement) and SCR (Solvency Capital Requirement):

Rating of Reinsurers to be factored in -The higher the rating of a reinsurer the lesser capital is neededIncreasing tendency to cover credit risk arising from reinsurance recoverables

• Retrospective and prospective coverage reinsurance solutions

Concentration of Credit RiskUK FSA monitors annual premium ceded to one reinsurer (20%) and total recoverables from any one insurance group to not exceed 100% of capital resources

46

Risk Based Capital

Due to the diversification ability of the reinsurer, more capital is freed up on the cedent’s side than is bound on the reinsurer’s side. Therefore, the cost of assuming the risk is lower for the reinsurer than for the cedent.

47

U.S. RBC Reinsurance Charge10% charge for reinsurance recoverables.

Rationale for the Reinsurance Charge• The apparently high charge on reinsurance recoverables

was motivated by reinsurance collectibility problems contributed to several major insurance company insolvencies in the mid-1980s.

Criticism of the Reinsurance ChargeIncentives:Quality of Reinsurer:Collateralization.

48

Types of Life Reinsurance

IndemnityTraditional Spread or Lessen RiskFinancial Meets Financial GoalsNon-Proportional Catastrophe, Stop LossRetrocession Reinsurance of Reinsurance

AssumptionTransfers Business Permanently

49

Reasons for Indemnity Reinsurance

Transfer Mortality/Morbidity Risk

Transfer Lapse or Surrender Risk

Transfer Investment Risk

Help Ceding Insurer Finance Acquisition Costs

50

Reasons for Indemnity Reinsurance

Provide Ceding Company• Underwriting Assistance• Product Expertise• Tax Planning• Help Manage Capital and Surplus and/or RBC

Objectives

Limit Adverse Effects of Catastrophic Events

Help Enter New Market

51

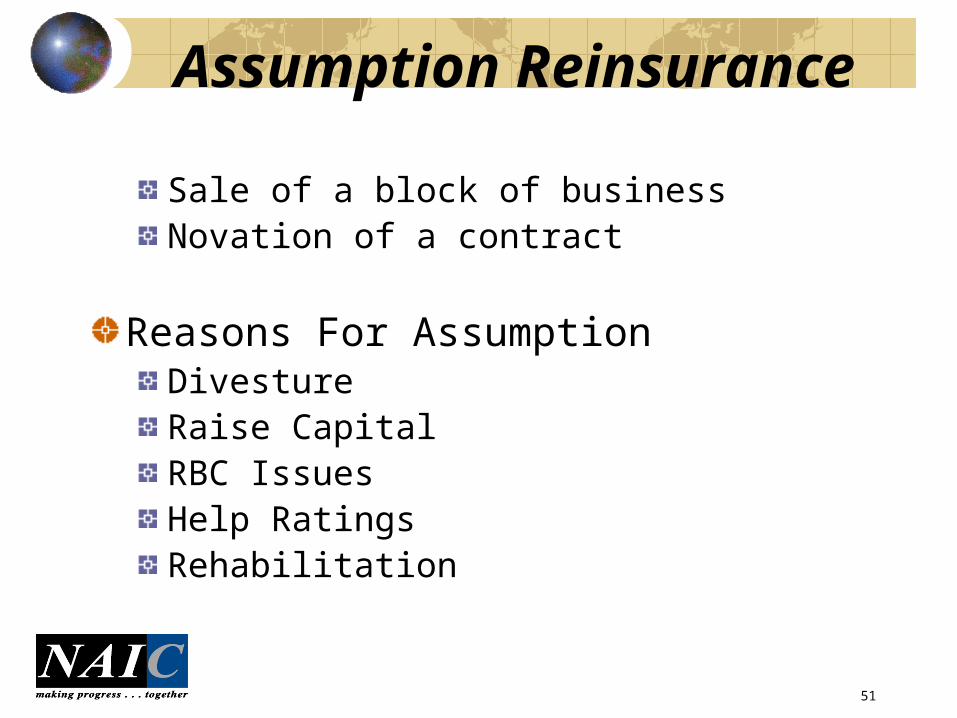

Assumption Reinsurance

Sale of a block of businessNovation of a contract

Reasons For AssumptionDivestureRaise CapitalRBC IssuesHelp RatingsRehabilitation

52

Alternative Risk Transfer

CaptivesFinite RiskContingent CapitalDerivativesSecuritization

Techniques other than traditional insurance and reinsurance to provide risk bearing entities with coverage or protection :

53

Captives

Single Parent CaptiveAn insurance or reinsurance company formed primarily to insure the risks of its non-insurance parent or affiliates.

Association Captive A company owned by a trade, industry or service group for the benefit of its members.

Group Captive A company, jointly owned by a number of companies, created to provide a vehicle to meet a common insurance need.

Agency Captive A company owned by an insurance agency or brokerage firm so they may reinsure a portion of their clients risks through that company.

Rent-a-Captive A company that provides 'captive' facilities to others for a fee, while protecting itself from losses under individual programs, which are also isolated from losses under other programs within the same company. This facility is often used for programs that are too small to justify establishing their own captive.

Established with the specific objective of financing risks emanating from their parent group or groups :

54

Captives

SPV - Although used extensively in the past for various financing arrangements, recently they have been used for catastrophe bonds and reinsurance sidecars. SPC - SPCs can be formed as a rent-a-captive facility to enable those companies who lack sufficient insurance premium volume, or who are averse to establishing their own insurance subsidiary, access to many of the benefits associated with an offshore captive.

Two other types of insurance company which have developed recently are special purpose vehicles (SPV) and segregated portfolio companies (SPC):

55

Captives Captives are becoming an increasingly important component of the risk management and risk financing strategy of their parent. A number of reasons have been put forward as the basis for the growth in the use of captives:

heavy and increasing premium costs in almost every line of insurance coverage. difficulties in obtaining cover certain types of risk. differences in coverage in various parts of the world. Inflexible credit rating structures which reflect market trends rather than individual loss experience. insufficient credit for deductibles and/or loss control efforts.

56

Finite Risk, Defined

Usually multiple-year

Insured (or reinsured) pays significant portion of the losses

Time value of money plays an important role in transaction value for both insurer and insured

Relatively narrow band between potential profit and potential loss to counterparties

Historically, long term budgeting and financial reporting have been key considerations

57

Does the level of risk match the accounting treatment?

Crux of the issue because it impacts the solvency of the cedentCan’t always tell by the contract languageNeed to review and challenge assumptions underlying the cash flow modelsAre there “side” agreements that undo the initial risk transfer?

58

What is the right amount of risk transfer?

“significant” loss (10/10?)Both Underwriting and timing

“taking a drop of risk and putting in a loan and calling it insurance is problematic” (Robert Herz, Chairman of FASB)

No matter where line is drawn, products will be designed to just get over the minimum.

59

• Retrospective PremiumsRetrospective Premiums - Premium rate is adjusted based on loss experience.

• Sliding Scale CommissionsSliding Scale Commissions - Commission rate is adjusted based on loss experience.

• Contingent CommissionsContingent Commissions - Additional commission based on profit

• Floating RetentionsFloating Retentions - Ceding company’s retention is adjusted based on the experience of the contract, last dollar paid contracts.

• Accumulating RetentionsAccumulating Retentions - Aggregate covers

• Loss Ratio Corridors / Loss Ratio CapsLoss Ratio Corridors / Loss Ratio Caps - Additional retention by the ceding company for a lower cost of reinsurance.

Provisions that require careful analysis:

Red FlagsRisk Transfer

60

Contingent Capital

The capital injected can be ( subordinated ) debt, preferred shares etc.Other than with a normal (“knock in” ) option, the contingency is a different risk than that of the asset underlying the option. For example, triggers can be related to natural hazards, the financial market, the price level of certain commodities, the state of the economy etc.

Contingent Capital is an option which gives the holder the right to raise capital from the optionprovider at predefined terms upon the occurrence of a pre-agreed event

61

Contingent Capital Immediate and (long) term availability of capital at predefined costs after “catastrophic” or unexpected events.Prevents from having to retain large liquid sources of capital on the balance sheet (“off balance sheet reserve”)Balance sheet protection against possibly difficult to insure risks. Reduces on-balance sheet capital without increasing overall risk profile of company (helps e.g. solvency ratio, capital adequacy )

62

Derivatives

Risk that interest rates may move up or down and thus affecting the value of assets and liability holdings.Basis risk which occurs when asset and liability portfolios are not matched and therefore interest rate changes will have a different affect on their total values.Inflation risk affects the value of asset holdings and may cause consumers to switch away from insurance products unless returns compensate for reduced purchasing power.Foreign currency risk which occurs when investments or assets are held in a currency which devalues relative to the home currency.Movements in stock prices, which means that the value of investments in stock markets affect the ability of insurance firms to pay out competitive rates of return to their policy holders.

Such activities expose insurance companies to systematic or financial market risk; that is, the risk of asset and liability holdings being affected by external (to the company) market factors. For the insurance sector, the most important financial market risk factors are:

63

Derivatives

Forwards are contracts negotiated over the counter between two private parties. They involve the obligation to either buy or sell an underlying asset at a prespecified price and date in the future and are privately negotiated between two parties. They have the advantage of being highly flexible with regard to terms and conditions. However, they have the possibility to provide counterparty credit risk and low trading liquidity because of non-standardised negotiated terms.Futures contracts also involve the obligation to buy or sell an underlying asset at a prespecified price and date in the future. Unlike forwards, they are standardised with regard to delivery, quantity, and quality. They are listed and traded on formal exchanges in which the clearing house manages and coordinates all trades and guarantees delivery or settlement of the contract. Moreover, they require maintenance margins that are settled daily by the clearing house, thus, virtually eliminating credit risk. Consequently, such contracts generally provide high trading liquidity.

There are four major derivative instruments:

64

Derivatives Swaps are private contracts between two participants who agree to exchange their different cash flows that might arrive in the future. A common example is an ‘interest rate swap’, whereby the parties agree to exchange the cash flows arising from fixed and variable interest rate payments on specified principal amounts.Options provide the buyer the right, but not the obligation, to buy or sell the underlying asset at a pre-specified time and price in the future. Options have a number of characteristics that are similar to an insurance contract. For the purchaser of a call option returns on the upside are unlimited.

For example, a contract to buy stock at $100 will be invoked if the stock is trading for any amount greater than $100 at the expiration of the contract. However, on the downside the loss is limited to the price of the call option. This call option contract protects the holder against price rises that will potentially occur in the future and is a similar payoff to taking out insurance that is conditional on a specified event occurring (such as flood). On the other hand, the writer of the option undertakes to cover the call upside risk (or downside for a put option) in return for the price of the written option. This is a similar position to the writer of an insurance contract.

65

Securitization

Insurance company transfers underwriting risks to the capital markets by transforming underwriting cash flows into tradable financial securitiesCash flows (e.g., repayment of interest and/or principal) are contingent upon an insurance event / risk

Securitization of insurance risks enables insurers to transfer their insurance risk directly to investors in the capital markets:

Factors Affecting Insurance Securitization

Recent catastrophe experienceReassessment of catastrophe riskDemand for and pricing of reinsuranceReinsurance supply issues

Capital market developmentsDevelopment of new asset classes and asset-backed marketsSearch for yield and diversification

Restructuring of insurance industry

Possible Reasons for Securitization

CapacityRisk of huge catastrophe lossesWould severely impair P/C industry capitalCapital markets could handle

InvestmentCatastrophe exposure is uncorrelated with overall capital markets. Thus, uncorrelated with existing portfolios.Diversification potential

Potential Success of Insurance Securitization?

Difficult to understandCapital marketsInsurance markets

Separation of insurance and finance functions in many companiesInformation and technologyDifficult to priceExpensive (vs. cat. reinsurance market)Legal / tax / accounting issues

69