1 a ccounting principles, weygandt, kieso, & kimmel

TRANSCRIPT

1

AAccounting Principles, ccounting Principles, Weygandt, Kieso, & KimmelWeygandt, Kieso, & Kimmel

2

After studying this chapter, you should be able to:

CHAPTER CHAPTER 2 2 THE RECORDING PROCESSTHE RECORDING PROCESSCHAPTER CHAPTER 2 2

THE RECORDING PROCESSTHE RECORDING PROCESS

11 what an account is and how it what an account is and how it helps in the recording process.helps in the recording process.

22 Identify the basic steps in the Identify the basic steps in the recording process.recording process.

33What a journal is and how it What a journal is and how it helps in the recording process.helps in the recording process.

44Explain what a ledger is and how Explain what a ledger is and how it helps in the recording process.it helps in the recording process.

3

55 Prepare a trial balance and Prepare a trial balance and explain its purpose.explain its purpose.

CHAPTER CHAPTER 22CHAPTER CHAPTER 22

4

PREVIEW OF CHAPTER PREVIEW OF CHAPTER 22PREVIEW OF CHAPTER PREVIEW OF CHAPTER 22

The Recording Process

Steps in the Recording Process

Journal

Ledger

The Account

Debits and credits

Expansion of basic equation

5

PREVIEW OF CHAPTER PREVIEW OF CHAPTER 22PREVIEW OF CHAPTER PREVIEW OF CHAPTER 22

The Recording Process

The Trial Balance

Limitations of a trial balance

Locating errors

The Recording Process Illustrated

Summary illustration of journalizing and posting

6

STUDY OBJECTIVE STUDY OBJECTIVE 11

Explain what an account is and how Explain what an account is and how it helps in the recording process.it helps in the recording process.Explain what an account is and how Explain what an account is and how it helps in the recording process.it helps in the recording process.

7

THE ACCOUNTTHE ACCOUNTTHE ACCOUNTTHE ACCOUNT

An An accountaccount is an individual is an individual accounting record of increases accounting record of increases and decreases in a specific and decreases in a specific asset, liability, or owner’s asset, liability, or owner’s equity item.equity item.

A company will have separate A company will have separate accounts for such items as accounts for such items as cashcash, , salaries expensesalaries expense, , accounts accounts payablepayable, and so on., and so on.

8

STUDY OBJECTIVE STUDY OBJECTIVE 22

Define debits and credits and Define debits and credits and explain how they are used to explain how they are used to record business transactions.record business transactions.

Define debits and credits and Define debits and credits and explain how they are used to explain how they are used to record business transactions.record business transactions.

9

BASIC FORM OF ACCOUNTBASIC FORM OF ACCOUNTBASIC FORM OF ACCOUNTBASIC FORM OF ACCOUNT

Left or debit side

Title of Account

Right or credit side

Debit balance Credit balance

In its simplest form, an account consists ofIn its simplest form, an account consists of

11 the title of the account, the title of the account,

22 a left or debit side, and a left or debit side, and

33 a right or credit side. a right or credit side. The alignment of these parts resembles the The alignment of these parts resembles the

letter T, and therefore the account form is letter T, and therefore the account form is called a called a T accountT account..

10

STEPS IN THE STEPS IN THE RECORDING PROCESSRECORDING PROCESS

The basic steps in the recording The basic steps in the recording process are:process are:

11 Analyze each transaction for its Analyze each transaction for its effect on effect on the accounts.the accounts.

22 Enter the transaction information in Enter the transaction information in a a journal (book of original journal (book of original entry).entry).

33 Transfer the journal information to Transfer the journal information to the the appropriate accounts in the appropriate accounts in the ledger (book of ledger (book of accounts).accounts).

11

DOUBLE-ENTRY SYSTEMDOUBLE-ENTRY SYSTEM

In a In a double-entry systemdouble-entry system, equal , equal debits and credits are made in the debits and credits are made in the accounts for each transaction. accounts for each transaction.

Thus, the total debits will always Thus, the total debits will always equal the total credits and the equal the total credits and the accounting equation will always accounting equation will always stay in balance.stay in balance.

12

THE JOURNALTHE JOURNAL

Transactions are initially recorded Transactions are initially recorded in chronological order in a in chronological order in a journaljournal before being transferred to the before being transferred to the accounts.accounts.

Every company has a Every company has a general general journaljournal which contains: which contains:11 spaces for dates, spaces for dates,22 account titles and explanations, account titles and explanations,33 references, and references, and44 two amount columns. two amount columns.

13

**THE JOURNAL**THE JOURNAL

The The journaljournal makes several significant makes several significant contributions to the recording process:contributions to the recording process:

11 It discloses in one place the complete It discloses in one place the complete effect of a transaction.effect of a transaction.

22 It provides a chronological record of It provides a chronological record of transactions.transactions.

33 It helps to prevent or locate errors It helps to prevent or locate errors because the debit and because the debit and credit credit amounts for each entry can be readily amounts for each entry can be readily compared.compared.

14

THE LEDGERTHE LEDGER

The entire group of accounts The entire group of accounts maintained by a company is called maintained by a company is called the the ledgerledger..

A A general ledger general ledger contains all the contains all the assets, liabilities, and owner’s assets, liabilities, and owner’s equity accounts.equity accounts.

15

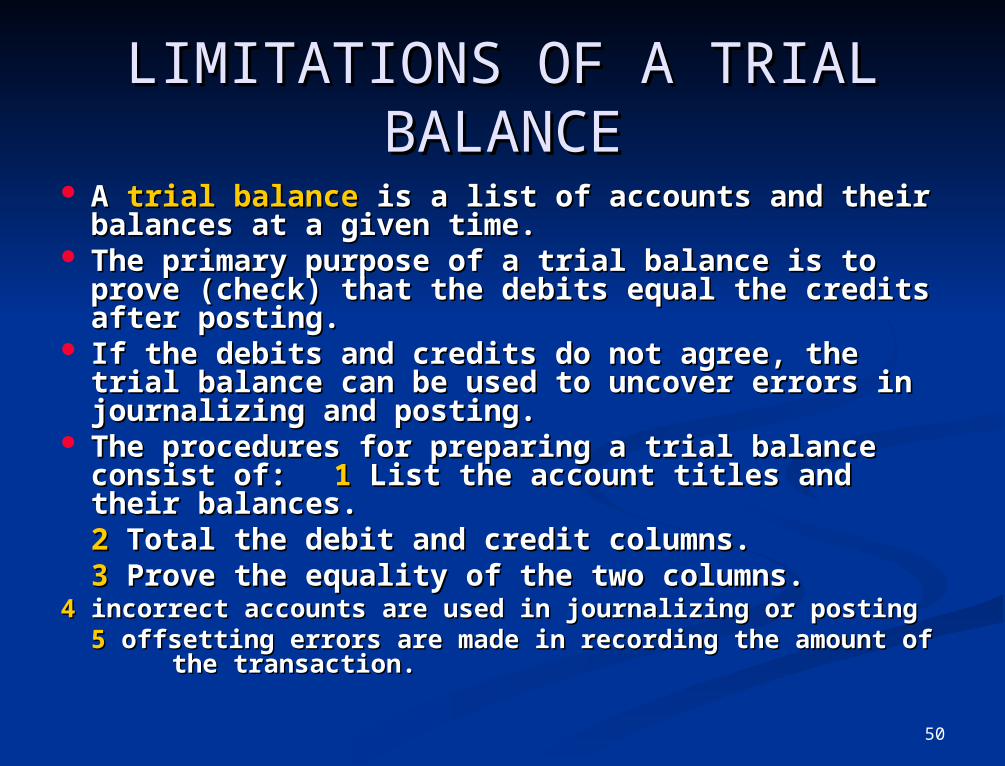

THE TRIAL BALANCE THE TRIAL BALANCE A A trial balancetrial balance is a list of accounts and is a list of accounts and

their balances at a given time.their balances at a given time. The primary purpose of a trial balance is to The primary purpose of a trial balance is to

prove (check) that the debits equal the prove (check) that the debits equal the credits after posting.credits after posting.

If the debits and credits do not agree, the If the debits and credits do not agree, the trial balance can be used to uncover errors trial balance can be used to uncover errors in journalizing and posting.in journalizing and posting.

The procedures for preparing a trial The procedures for preparing a trial balance consist of:balance consist of:11 List the account titles and their balances. List the account titles and their balances.22 Total the debit and credit columns. Total the debit and credit columns.33 Prove the equality of the two columns. Prove the equality of the two columns.

16

LIMITATIONS OF A TRIAL LIMITATIONS OF A TRIAL BALANCEBALANCE

A trial balance does not prove that all A trial balance does not prove that all transactions have been recorded or that transactions have been recorded or that the ledger is correct.the ledger is correct.

Numerous errors may exist even though Numerous errors may exist even though the trial balance columns agree.the trial balance columns agree.

The trial balance may balance even when:The trial balance may balance even when:11 a transaction is not journalized, a transaction is not journalized,22 a correct journal entry is not posted, a correct journal entry is not posted,33 a journal entry is posted twice, a journal entry is posted twice,44 incorrect accounts are used in incorrect accounts are used in journalizing or postingjournalizing or posting55 offsetting errors are made in recording offsetting errors are made in recording the amount of the amount of the transaction. the transaction.

17

DEBITS AND CREDITSDEBITS AND CREDITSDEBITS AND CREDITSDEBITS AND CREDITS

The term The term debit debit means left and means left and creditcredit means right means right respectively.respectively.

The act of entering an amount on the The act of entering an amount on the leftleft side of side of an account is called debiting the account and an account is called debiting the account and making an entry on the making an entry on the rightright side is crediting the side is crediting the account.account.

When the debit amounts exceed the credits, an When the debit amounts exceed the credits, an account has a account has a debitdebit balance; when the reverse is balance; when the reverse is true, the account has a true, the account has a creditcredit balance. balance.DR CR

18

ILLUSTRATION ILLUSTRATION 2-2 2-2 TABULAR SUMMARY COMPARED TO TABULAR SUMMARY COMPARED TO

ACCOUNT FORMACCOUNT FORM

ILLUSTRATION ILLUSTRATION 2-2 2-2 TABULAR SUMMARY COMPARED TO TABULAR SUMMARY COMPARED TO

ACCOUNT FORMACCOUNT FORM

Tabular Summary

Cash

$15,000- 7,000

1,2001,500

- 1,700- 250

600- 1,300

CashDebit Credit

15,0001,2001,500

600

7,0001,700

1,300250

Balance

Account Form

$ $ 8,0508,050

$8,050(Debit)

19

Cash

Debits Credits

15,000

Example: Example: The owner makes an initial The owner makes an initial investment of $15,000 to start investment of $15,000 to start the business. Cash is debited the business. Cash is debited as the owner’s Capital is as the owner’s Capital is credited.credited.

Example: Example: The owner makes an initial The owner makes an initial investment of $15,000 to start investment of $15,000 to start the business. Cash is debited the business. Cash is debited as the owner’s Capital is as the owner’s Capital is credited.credited.

DEBITING AN ACCOUNTDEBITING AN ACCOUNTDEBITING AN ACCOUNTDEBITING AN ACCOUNT

20

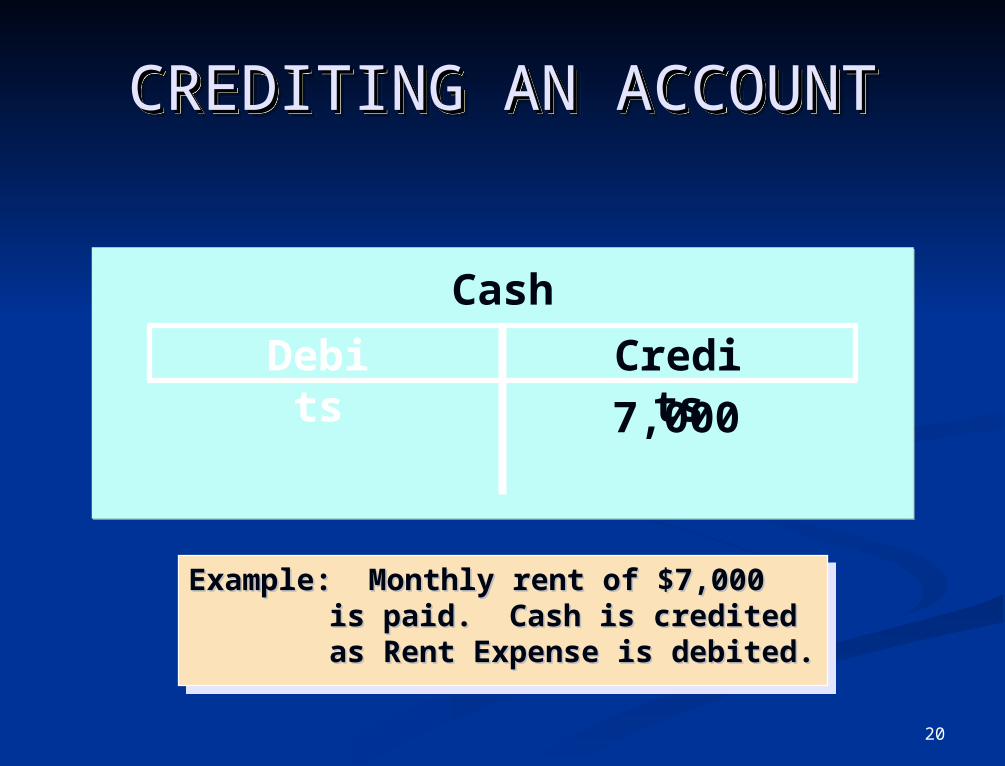

Example: Monthly rent of $7,000 is Example: Monthly rent of $7,000 is paid. Cash is credited as paid. Cash is credited as Rent Expense is debited.Rent Expense is debited.

Example: Monthly rent of $7,000 is Example: Monthly rent of $7,000 is paid. Cash is credited as paid. Cash is credited as Rent Expense is debited.Rent Expense is debited.

CREDITING AN ACCOUNTCREDITING AN ACCOUNTCREDITING AN ACCOUNTCREDITING AN ACCOUNT

Cash

Debits Credits

7,000

21

DOUBLE-ENTRY SYSTEMDOUBLE-ENTRY SYSTEMDOUBLE-ENTRY SYSTEMDOUBLE-ENTRY SYSTEM

In a In a double-entry systemdouble-entry system, equal , equal debits and credits are made in the debits and credits are made in the accounts for each transaction. accounts for each transaction.

Thus, the total debits will always Thus, the total debits will always equal the total credits and the equal the total credits and the accounting equation will always accounting equation will always stay in balance.stay in balance.

22

ILLUSTRATION ILLUSTRATION 2-3 2-3 DEBIT AND CREDIT EFFECTS — DEBIT AND CREDIT EFFECTS —

ASSETS AND LIABILITIESASSETS AND LIABILITIES

ILLUSTRATION ILLUSTRATION 2-3 2-3 DEBIT AND CREDIT EFFECTS — DEBIT AND CREDIT EFFECTS —

ASSETS AND LIABILITIESASSETS AND LIABILITIES

Debits CreditsIncrease assets Decrease assets Increase assets Decrease assets

Decrease liabilities Increase liabilitiesDecrease liabilities Increase liabilities

23

NORMAL BALANCENORMAL BALANCENORMAL BALANCENORMAL BALANCE

Every account classification has a Every account classification has a normalnormal balance, whether it is a debit or balance, whether it is a debit or credit.credit.

For that particular account, the For that particular account, the opposite side entries should never opposite side entries should never exceed the normal balance.exceed the normal balance.

24

ILLUSTRATION ILLUSTRATION 2-4 2-4 NORMAL BALANCES — ASSETS AND LIABILITIESNORMAL BALANCES — ASSETS AND LIABILITIES

ILLUSTRATION ILLUSTRATION 2-4 2-4 NORMAL BALANCES — ASSETS AND LIABILITIESNORMAL BALANCES — ASSETS AND LIABILITIES

AssetsIncrease Decrease Debit CreditDecrease Increase Debit Credit

Liabilities

Normal BalanceNormal Balance

Normal Normal BalanceBalance

25

ILLUSTRATION ILLUSTRATION 2-5 2-5 DEBIT AND CREDIT EFFECTS — OWNER’S CAPITALDEBIT AND CREDIT EFFECTS — OWNER’S CAPITAL

ILLUSTRATION ILLUSTRATION 2-5 2-5 DEBIT AND CREDIT EFFECTS — OWNER’S CAPITALDEBIT AND CREDIT EFFECTS — OWNER’S CAPITAL

Debits CreditsDecrease owner’s capital Increase owner’s capitalDecrease owner’s capital Increase owner’s capital

26

ILLUSTRATION ILLUSTRATION 2-6 2-6 NORMAL BALANCE — OWNER’S CAPITALNORMAL BALANCE — OWNER’S CAPITALILLUSTRATION ILLUSTRATION 2-6 2-6

NORMAL BALANCE — OWNER’S CAPITALNORMAL BALANCE — OWNER’S CAPITAL

Owner’s Capital

Decrease Increase Debit Credit

Normal Normal BalanceBalance

27

ILLUSTRATION ILLUSTRATION 2-7 2-7 DEBIT AND CREDIT EFFECTS — OWNER’S DRAWINGDEBIT AND CREDIT EFFECTS — OWNER’S DRAWING

ILLUSTRATION ILLUSTRATION 2-7 2-7 DEBIT AND CREDIT EFFECTS — OWNER’S DRAWINGDEBIT AND CREDIT EFFECTS — OWNER’S DRAWING

Debits CreditsIncrease owner’s drawing Decrease owner’s drawingIncrease owner’s drawing Decrease owner’s drawing

28

ILLUSTRATION ILLUSTRATION 2-8 2-8 NORMAL BALANCE — OWNER’S DRAWINGNORMAL BALANCE — OWNER’S DRAWING

ILLUSTRATION ILLUSTRATION 2-8 2-8 NORMAL BALANCE — OWNER’S DRAWINGNORMAL BALANCE — OWNER’S DRAWING

Owner’s Drawing

Normal Normal BalanceBalance

Increase Decrease Debit Credit

29

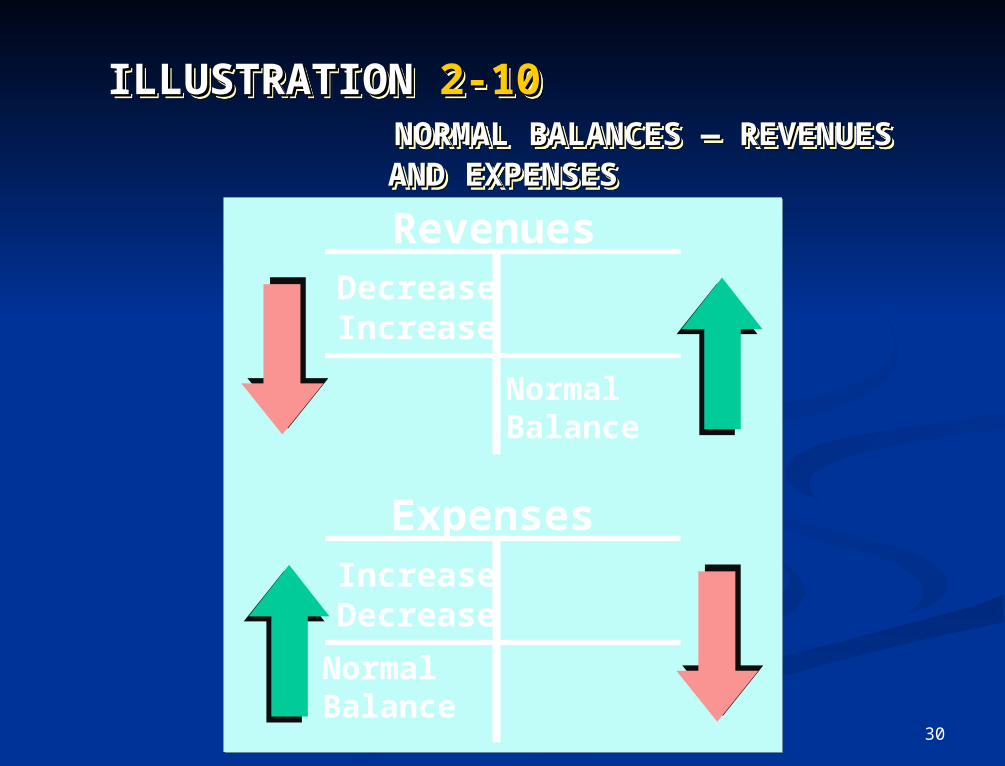

ILLUSTRATION ILLUSTRATION 2-9 2-9 DEBIT AND CREDIT EFFECTS — REVENUES AND EXPENSESDEBIT AND CREDIT EFFECTS — REVENUES AND EXPENSES

ILLUSTRATION ILLUSTRATION 2-9 2-9 DEBIT AND CREDIT EFFECTS — REVENUES AND EXPENSESDEBIT AND CREDIT EFFECTS — REVENUES AND EXPENSES

Decrease revenues Increase revenues Decrease revenues Increase revenues

Increase expenses Decrease expensesIncrease expenses Decrease expenses

Debits Credits

30

ILLUSTRATION ILLUSTRATION 2-10 2-10 NORMAL BALANCES — REVENUES AND EXPENSESNORMAL BALANCES — REVENUES AND EXPENSES

ILLUSTRATION ILLUSTRATION 2-10 2-10 NORMAL BALANCES — REVENUES AND EXPENSESNORMAL BALANCES — REVENUES AND EXPENSES

Increase Decrease Debit Credit

Expenses

RevenuesDecrease Increase Debit Credit

NormalBalance

NormalBalance

31

ILLUSTRATION ILLUSTRATION 2-11 2-11 EXPANDED BASIC EQUATION AND EXPANDED BASIC EQUATION AND

DEBIT/CREDIT RULES AND EFFECTSDEBIT/CREDIT RULES AND EFFECTS

ILLUSTRATION ILLUSTRATION 2-11 2-11 EXPANDED BASIC EQUATION AND EXPANDED BASIC EQUATION AND

DEBIT/CREDIT RULES AND EFFECTSDEBIT/CREDIT RULES AND EFFECTS

LiabilitiesAssets Owner’s Equity

= + -

+=

+ -

Assets

Dr. Cr.+ -

Liabilities

Dr. Cr.- +

Dr. Cr.

Owner’s Drawing

+ -

Dr. Cr.

Revenues

- +Dr. Cr.

Expenses

+ -

Dr. Cr.

Owner’s Capital

- +

32

STUDY OBJECTIVE STUDY OBJECTIVE 33

Identify the basic steps in the recording process.Identify the basic steps in the recording process.Identify the basic steps in the recording process.Identify the basic steps in the recording process.

33

ILLUSTRATION ILLUSTRATION 2-12 2-12 THE RECORDING THE RECORDING

PROCESSPROCESS

ILLUSTRATION ILLUSTRATION 2-12 2-12 THE RECORDING THE RECORDING

PROCESSPROCESS

11 Analyze each transactionAnalyze each transaction

22 Enter transaction in a journalEnter transaction in a journal

33 Transfer journal information to ledger accountsTransfer journal information to ledger accounts

JOURNAL

JOURNAL

LEDGER

34

STUDY OBJECTIVE STUDY OBJECTIVE 44

Explain what a journal is and how Explain what a journal is and how it helps in the recording process.it helps in the recording process.Explain what a journal is and how Explain what a journal is and how it helps in the recording process.it helps in the recording process.

35

THE JOURNALTHE JOURNALTHE JOURNALTHE JOURNAL

Transactions are initially recorded in Transactions are initially recorded in chronological order in a chronological order in a journaljournal before before being transferred to the accounts.being transferred to the accounts.

Every company has a Every company has a general journalgeneral journal which contains:which contains:

11 spaces for dates, spaces for dates,

22 account titles and explanations, account titles and explanations,

33 references, and references, and

44 two amount columns. two amount columns.

36

The The journaljournal makes several significant contributions makes several significant contributions to the recording process:to the recording process:

11 It discloses in one place the complete effect of a It discloses in one place the complete effect of a transaction.transaction.

22 It provides a chronological record of transactions. It provides a chronological record of transactions.

33 It helps to prevent or locate errors because the It helps to prevent or locate errors because the debit and debit and credit amounts for each entry can be credit amounts for each entry can be readily compared.readily compared.

THE JOURNALTHE JOURNALTHE JOURNALTHE JOURNAL

37

JOURNALIZINGJOURNALIZINGJOURNALIZINGJOURNALIZING

Entering transaction data in the Entering transaction data in the journal is known as journal is known as journalizingjournalizing..

Separate journal entries are made for Separate journal entries are made for each transaction.each transaction.

A complete entry consists of:A complete entry consists of:

11 the date of the transaction, the date of the transaction,

22 the accounts and amounts to be the accounts and amounts to be debited and debited and credited, andcredited, and

33 a brief explanation of the transaction. a brief explanation of the transaction.

38

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZING

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZINGThe date of the transaction is entered in the date column.The date of the transaction is entered in the date column.The date of the transaction is entered in the date column.The date of the transaction is entered in the date column.

39

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZING

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZINGThe The debitdebit account title is entered at the extreme account title is entered at the extreme left margin of the Account Titles and Explanation left margin of the Account Titles and Explanation column. The column. The creditcredit account title is indented on the account title is indented on the next line.next line.

The The debitdebit account title is entered at the extreme account title is entered at the extreme left margin of the Account Titles and Explanation left margin of the Account Titles and Explanation column. The column. The creditcredit account title is indented on the account title is indented on the next line.next line.

40

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZING

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZINGThe amounts for the The amounts for the debitsdebits are recorded are recorded in the Debit column and the amounts for in the Debit column and the amounts for the the creditscredits are recorded in the Credit are recorded in the Credit column.column.

The amounts for the The amounts for the debitsdebits are recorded are recorded in the Debit column and the amounts for in the Debit column and the amounts for the the creditscredits are recorded in the Credit are recorded in the Credit column.column.

41

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZING

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZINGA brief explanation of the transaction is given.A brief explanation of the transaction is given.A brief explanation of the transaction is given.A brief explanation of the transaction is given.

42

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZING

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZINGA space is left between journal entries. The A space is left between journal entries. The blank space separates individual journal entries blank space separates individual journal entries and makes the entire journal easier to read.and makes the entire journal easier to read.

A space is left between journal entries. The A space is left between journal entries. The blank space separates individual journal entries blank space separates individual journal entries and makes the entire journal easier to read.and makes the entire journal easier to read.

43

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZING

ILLUSTRATION ILLUSTRATION 2-13 2-13 TECHNIQUE OF TECHNIQUE OF

JOURNALIZINGJOURNALIZINGThe column entitled Ref. is left blank at the time The column entitled Ref. is left blank at the time journal entry is made and is used later when the journal entry is made and is used later when the journal entries are transferred to the ledger journal entries are transferred to the ledger accounts.accounts.

The column entitled Ref. is left blank at the time The column entitled Ref. is left blank at the time journal entry is made and is used later when the journal entry is made and is used later when the journal entries are transferred to the ledger journal entries are transferred to the ledger accounts.accounts.

44

If an entry involves only two accounts, one If an entry involves only two accounts, one debit and one credit, it is considered a debit and one credit, it is considered a simple simple entryentry..

If an entry involves only two accounts, one If an entry involves only two accounts, one debit and one credit, it is considered a debit and one credit, it is considered a simple simple entryentry..

SIMPLE AND COMPOUND SIMPLE AND COMPOUND JOURNAL ENTRIESJOURNAL ENTRIES

SIMPLE AND COMPOUND SIMPLE AND COMPOUND JOURNAL ENTRIESJOURNAL ENTRIES

45

When three or more accounts are When three or more accounts are required in one journal entry, the entry required in one journal entry, the entry is referred to as a is referred to as a compound entrycompound entry..

When three or more accounts are When three or more accounts are required in one journal entry, the entry required in one journal entry, the entry is referred to as a is referred to as a compound entrycompound entry..

ILLUSTRATION ILLUSTRATION 2-14 2-14 COMPOUND JOURNAL ENTRYCOMPOUND JOURNAL ENTRY

ILLUSTRATION ILLUSTRATION 2-14 2-14 COMPOUND JOURNAL ENTRYCOMPOUND JOURNAL ENTRY

2

1

3

46

COMPOUND JOURNAL ENTRYCOMPOUND JOURNAL ENTRYCOMPOUND JOURNAL ENTRYCOMPOUND JOURNAL ENTRY

This is the wrong format; all debits must This is the wrong format; all debits must be listed before the credits are listed.be listed before the credits are listed.This is the wrong format; all debits must This is the wrong format; all debits must be listed before the credits are listed.be listed before the credits are listed.

47

STUDY OBJECTIVE STUDY OBJECTIVE 55

Explain what a ledger is and how Explain what a ledger is and how it helps in the recording process.it helps in the recording process.Explain what a ledger is and how Explain what a ledger is and how it helps in the recording process.it helps in the recording process.

48

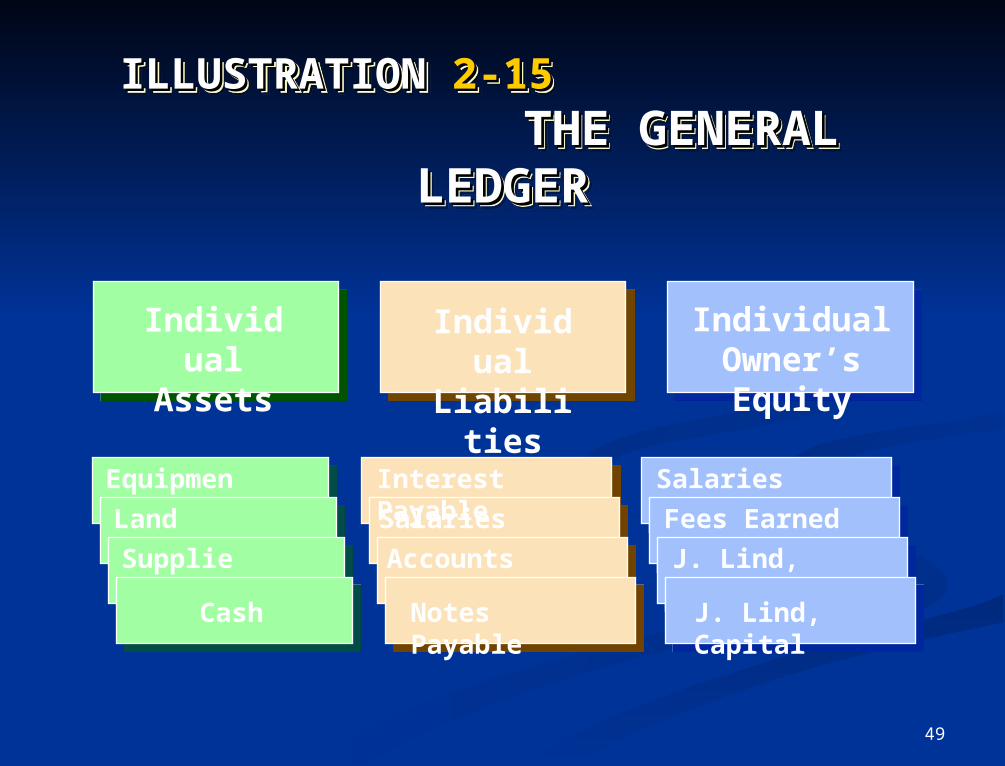

THE LEDGERTHE LEDGERTHE LEDGERTHE LEDGER

The entire group of accounts maintained The entire group of accounts maintained by a company is called the by a company is called the ledgerledger..

A A general ledger general ledger contains all the assets, contains all the assets, liabilities, and owner’s equity accounts.liabilities, and owner’s equity accounts.

GENERAL LEDGER

49

Individual Liabilities

Individual Assets

Individual Owner’s Equity

ILLUSTRATION ILLUSTRATION 2-15 2-15 THE GENERAL LEDGERTHE GENERAL LEDGER

ILLUSTRATION ILLUSTRATION 2-15 2-15 THE GENERAL LEDGERTHE GENERAL LEDGER

Equipment

Land

Supplies

Cash

Interest Payable

Salaries Payable

Accounts Payable

Notes Payable

Salaries Expense

Fees Earned

J. Lind, Drawing

J. Lind, Capital

50

LIMITATIONS OF A TRIAL LIMITATIONS OF A TRIAL BALANCEBALANCE

A A trial balancetrial balance is a list of accounts and their is a list of accounts and their balances at a given time.balances at a given time.

The primary purpose of a trial balance is to prove The primary purpose of a trial balance is to prove (check) that the debits equal the credits after (check) that the debits equal the credits after posting.posting.

If the debits and credits do not agree, the trial If the debits and credits do not agree, the trial balance can be used to uncover errors in balance can be used to uncover errors in journalizing and posting.journalizing and posting.

The procedures for preparing a trial balance The procedures for preparing a trial balance consist of:consist of: 11 List the account titles and their List the account titles and their balances.balances.22 Total the debit and credit columns. Total the debit and credit columns.33 Prove the equality of the two columns. Prove the equality of the two columns.

44 incorrect accounts are used in journalizing or posting incorrect accounts are used in journalizing or posting55 offsetting errors are made in recording the amount of offsetting errors are made in recording the amount of the transaction. the transaction.

51

STUDY OBJECTIVE STUDY OBJECTIVE 66

Explain what posting is and how Explain what posting is and how it helps in the recording process.it helps in the recording process.Explain what posting is and how Explain what posting is and how it helps in the recording process.it helps in the recording process.

52

ILLUSTRATION ILLUSTRATION 2-17 2-17 POSTING A JOURNAL ENTRYPOSTING A JOURNAL ENTRY

ILLUSTRATION ILLUSTRATION 2-17 2-17 POSTING A JOURNAL ENTRYPOSTING A JOURNAL ENTRY

In the ledger, enter in the appropriate columns of the account(s) In the ledger, enter in the appropriate columns of the account(s) debited the debited the datedate, , journal pagejournal page, and , and debit amountdebit amount shown in the journal. shown in the journal.

53

ILLUSTRATION ILLUSTRATION 2-17 2-17 POSTING A JOURNAL ENTRYPOSTING A JOURNAL ENTRY

ILLUSTRATION ILLUSTRATION 2-17 2-17 POSTING A JOURNAL ENTRYPOSTING A JOURNAL ENTRY

In the reference column of the journal, write the In the reference column of the journal, write the account account numbernumber to which the debit amount was posted. to which the debit amount was posted.

54

ILLUSTRATION ILLUSTRATION 2-17 2-17 POSTING A JOURNAL ENTRYPOSTING A JOURNAL ENTRY

ILLUSTRATION ILLUSTRATION 2-17 2-17 POSTING A JOURNAL ENTRYPOSTING A JOURNAL ENTRY

In the ledger, enter in the appropriate columns of the account(s) credited In the ledger, enter in the appropriate columns of the account(s) credited the the datedate, , journal pagejournal page, and , and credit amountcredit amount shown in the journal. shown in the journal.

55

ILLUSTRATION ILLUSTRATION 2-17 2-17 POSTING A JOURNAL ENTRYPOSTING A JOURNAL ENTRY

ILLUSTRATION ILLUSTRATION 2-17 2-17 POSTING A JOURNAL ENTRYPOSTING A JOURNAL ENTRY

In the reference column of the journal, write the In the reference column of the journal, write the account account numbernumber to which the credit amount was posted. to which the credit amount was posted.

56

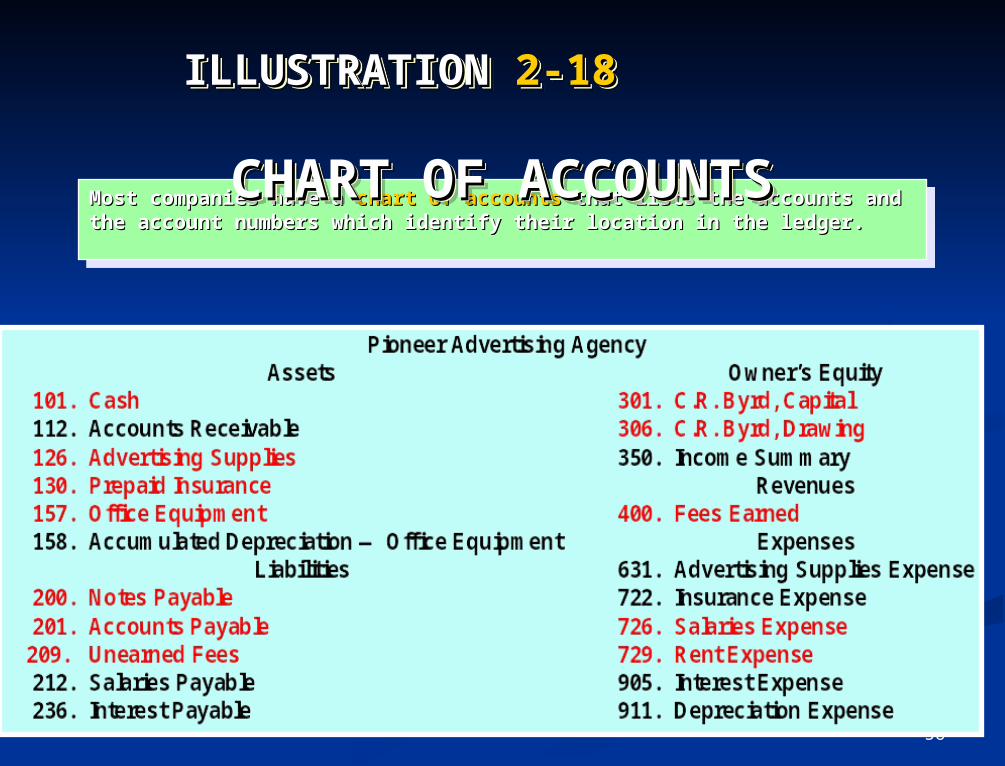

Most companies have a Most companies have a chart of accountschart of accounts that lists the accounts and that lists the accounts and the account numbers which identify their location in the ledger.the account numbers which identify their location in the ledger.

Most companies have a Most companies have a chart of accountschart of accounts that lists the accounts and that lists the accounts and the account numbers which identify their location in the ledger.the account numbers which identify their location in the ledger.

ILLUSTRATION ILLUSTRATION 2-18 2-18

CHART OF CHART OF ACCOUNTSACCOUNTS

ILLUSTRATION ILLUSTRATION 2-18 2-18

CHART OF CHART OF ACCOUNTSACCOUNTS

57

ILLUSTRATION ILLUSTRATION 2-19 2-19 INVESTMENT OF CASH BY OWNERINVESTMENT OF CASH BY OWNERILLUSTRATION ILLUSTRATION 2-19 2-19 INVESTMENT OF CASH BY OWNERINVESTMENT OF CASH BY OWNER

BasicAnalysis

Debit-CreditAnalysis

TransactionOctober 1, C.R. Byrd invests $10,000 cash in an advertising venture to be known as the Pioneer Advertising Agency.

The asset Cash is increased $10,000, and owner’s equity C. R. Byrd, Capital is increased $10,000.

Debits increase assets: debit Cash $10,000.Credits increase owner’s equity: credit C.R. Byrd, Capital $10,000.

58

ILLUSTRATION ILLUSTRATION 2-19 2-19 INVESTMENT OF CASH BY OWNERINVESTMENT OF CASH BY OWNERILLUSTRATION ILLUSTRATION 2-19 2-19 INVESTMENT OF CASH BY OWNERINVESTMENT OF CASH BY OWNER

JOURNAL ENTRYJOURNAL ENTRY

POSTINGPOSTING

59

ILLUSTRATION ILLUSTRATION 2-20 2-20 PURCHASE OF OFFICE EQUIPMENTPURCHASE OF OFFICE EQUIPMENTILLUSTRATION ILLUSTRATION 2-20 2-20 PURCHASE OF OFFICE EQUIPMENTPURCHASE OF OFFICE EQUIPMENT

BasicAnalysis

Debit-CreditAnalysis

TransactionOctober 1, office equipment costing $5,000 is purchased by signing a 3-month, 12%, $5,000 note payable.

The asset Office Equipment is increased $5,000, and the liability Notes Payable is increased $5,000.

Debits increase assets: debit Office Equipment $5,000. Credits increase liabilities: credit Notes Payable $5,000.

60

ILLUSTRATION ILLUSTRATION 2-20 2-20 PURCHASE OF OFFICE EQUIPMENTPURCHASE OF OFFICE EQUIPMENTILLUSTRATION ILLUSTRATION 2-20 2-20 PURCHASE OF OFFICE EQUIPMENTPURCHASE OF OFFICE EQUIPMENT

JOURNAL ENTRYJOURNAL ENTRY

POSTINGPOSTING

61

ILLUSTRATION ILLUSTRATION 2-21 2-21 RECEIPT OF CASH FOR FUTURE SERVICERECEIPT OF CASH FOR FUTURE SERVICEILLUSTRATION ILLUSTRATION 2-21 2-21 RECEIPT OF CASH FOR FUTURE SERVICERECEIPT OF CASH FOR FUTURE SERVICE

BasicAnalysis

Debit-CreditAnalysis

TransactionOctober 2, a $1,200 cash advance is received from R. Knox, a client, for advertising services that are expected to be completed by December 31.

The asset Cash is increased $1,200; the liability Unearned Fees is increased $1,200 because the service has not been rendered yet. Note that although many liabilities have the word “payable” in their title, unearned fees are considered a liability even though the word payable is not used.

Debits increase assets: debit Cash $1,200. Credits increase liabilities: credit Unearned Fees $1,200.

62

ILLUSTRATION ILLUSTRATION 2-21 2-21 RECEIPT OF CASH FOR FUTURE SERVICERECEIPT OF CASH FOR FUTURE SERVICEILLUSTRATION ILLUSTRATION 2-21 2-21 RECEIPT OF CASH FOR FUTURE SERVICERECEIPT OF CASH FOR FUTURE SERVICE

JOURNAL ENTRYJOURNAL ENTRY

POSTINGPOSTING

63

ILLUSTRATION ILLUSTRATION 2-22 2-22 PAYMENT OF MONTHLY RENTPAYMENT OF MONTHLY RENT

ILLUSTRATION ILLUSTRATION 2-22 2-22 PAYMENT OF MONTHLY RENTPAYMENT OF MONTHLY RENT

BasicAnalysis

Debit-CreditAnalysis

Transaction October 3, office rent for October is paid in cash, $900.

The expense Rent is increased $900 because the payment pertains only to the current month; the asset Cash is decreased $900.

Debits increase expenses: debit Rent Expense $900. Credits decrease assets: credit Cash $900.

64

ILLUSTRATION ILLUSTRATION 2-22 2-22 PAYMENT OF MONTHLY RENTPAYMENT OF MONTHLY RENT

ILLUSTRATION ILLUSTRATION 2-22 2-22 PAYMENT OF MONTHLY RENTPAYMENT OF MONTHLY RENT

JOURNAL ENTRYJOURNAL ENTRY

POSTINGPOSTING

65

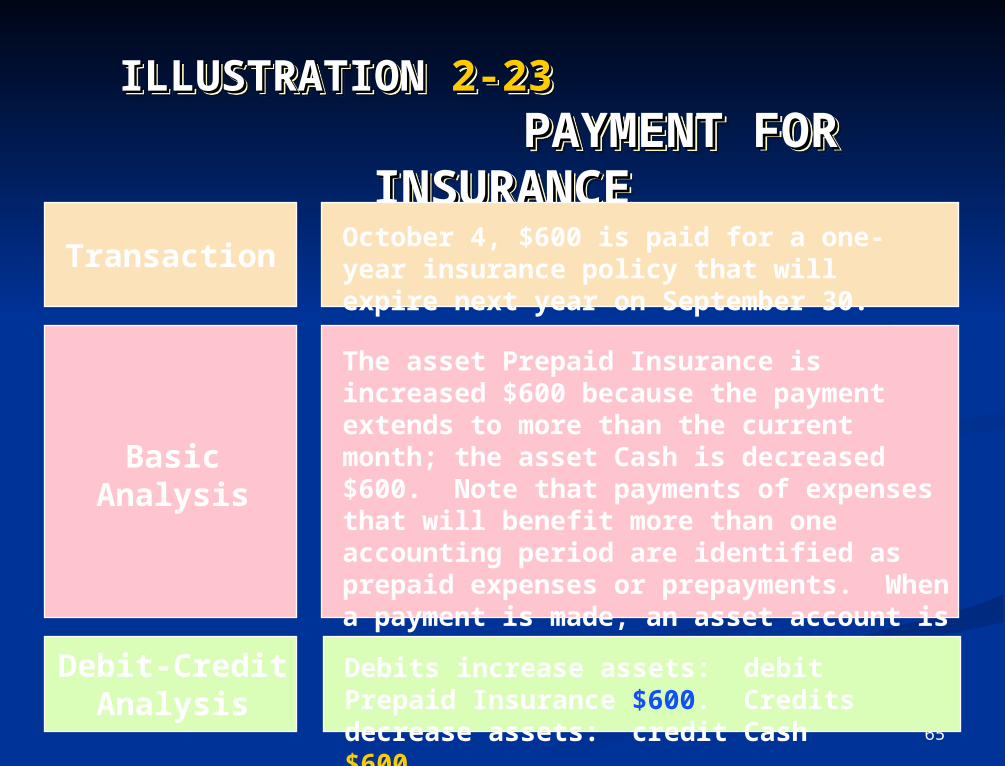

ILLUSTRATION ILLUSTRATION 2-23 2-23 PAYMENT FOR INSURANCEPAYMENT FOR INSURANCE

ILLUSTRATION ILLUSTRATION 2-23 2-23 PAYMENT FOR INSURANCEPAYMENT FOR INSURANCE

The asset Prepaid Insurance is increased $600 because the payment extends to more than the current month; the asset Cash is decreased $600. Note that payments of expenses that will benefit more than one accounting period are identified as prepaid expenses or prepayments. When a payment is made, an asset account is debited in order to show the service or benefit that will be received in the future.

TransactionOctober 4, $600 is paid for a one-year insurance policy that will expire next year on September 30.

Debit-CreditAnalysis

Debits increase assets: debit Prepaid Insurance $600. Credits decrease assets: credit Cash $600.

BasicAnalysis

66

ILLUSTRATION ILLUSTRATION 2-23 2-23 PAYMENT FOR INSURANCEPAYMENT FOR INSURANCE

ILLUSTRATION ILLUSTRATION 2-23 2-23 PAYMENT FOR INSURANCEPAYMENT FOR INSURANCE

JOURNAL ENTRYJOURNAL ENTRY

POSTINGPOSTING

Prepaid Insurance 130 Oct. 4 600

67

ILLUSTRATION ILLUSTRATION 2-24 2-24 PURCHASE OF SUPPLIES ON CREDITPURCHASE OF SUPPLIES ON CREDITILLUSTRATION ILLUSTRATION 2-24 2-24

PURCHASE OF SUPPLIES ON CREDITPURCHASE OF SUPPLIES ON CREDIT

BasicAnalysis

Debit-CreditAnalysis

TransactionOctober 5, an estimated 3-month supply of advertising materials is purchased on account from Aero Supply for $2,500.

The asset Advertising Supplies is increased $2,500; the liability Accounts Payable is increased $2,500.

Debits increase assets: debit Advertising Supplies $2,500. Credits increase liabilities: credit Accounts Payable $2,500.

68

ILLUSTRATION ILLUSTRATION 2-24 2-24 PURCHASE OF SUPPLIES ON CREDITPURCHASE OF SUPPLIES ON CREDITILLUSTRATION ILLUSTRATION 2-24 2-24

PURCHASE OF SUPPLIES ON CREDITPURCHASE OF SUPPLIES ON CREDIT

JOURNAL ENTRYJOURNAL ENTRY

POSTINGPOSTING

69

ILLUSTRATION ILLUSTRATION 2-25 2-25 HIRING OF EMPLOYEESHIRING OF EMPLOYEES

ILLUSTRATION ILLUSTRATION 2-25 2-25 HIRING OF EMPLOYEESHIRING OF EMPLOYEES

BasicAnalysis

Debit-CreditAnalysis

Transaction

October 9, hire four employees to begin work on October 15. Each employee is to receive a weekly salary of $500 for a 5-day work week, payable every 2 weeks -- first payment made on October 26.

A business transaction has not occurred. There is only an agreement between the employer and the employees to enter into a business transaction beginning on October 15.

A debit-credit analysis is not needed because there is no accounting entry.

70

ILLUSTRATION ILLUSTRATION 2-26 2-26 WITHDRAWAL OF CASH BY OWNERWITHDRAWAL OF CASH BY OWNERILLUSTRATION ILLUSTRATION 2-26 2-26 WITHDRAWAL OF CASH BY OWNERWITHDRAWAL OF CASH BY OWNER

BasicAnalysis

Debit-CreditAnalysis

Transaction October 20, C. R. Byrd withdraws $500 cash for personal use.

The owner’s equity account C. R. Byrd, Drawing is increased $500; the asset Cash is decreased $500.

Debits increase drawings: debit C. R. Byrd, Drawing $500. Credits decrease assets: credit Cash $500.

71

ILLUSTRATION ILLUSTRATION 2-26 2-26 WITHDRAWAL OF CASH BY OWNERWITHDRAWAL OF CASH BY OWNERILLUSTRATION ILLUSTRATION 2-26 2-26 WITHDRAWAL OF CASH BY OWNERWITHDRAWAL OF CASH BY OWNER

JOURNAL ENTRYJOURNAL ENTRY

POSTINGPOSTING

72

ILLUSTRATION ILLUSTRATION 2-27 2-27 PAYMENT OF SALARIESPAYMENT OF SALARIES

ILLUSTRATION ILLUSTRATION 2-27 2-27 PAYMENT OF SALARIESPAYMENT OF SALARIES

BasicAnalysis

Debit-CreditAnalysis

TransactionOctober 26, employee salaries of $4,000 are owed and paid in cash. (See October 9 transaction.)

The expense account Salaries Expense is increased $4,000; the asset Cash is decreased $4,000.

Debits increase expenses: debit Salaries Expense $4,000. Credits decrease assets: credit Cash $4,000.

73

ILLUSTRATION ILLUSTRATION 2-27 2-27 PAYMENT OF SALARIESPAYMENT OF SALARIES

ILLUSTRATION ILLUSTRATION 2-27 2-27 PAYMENT OF SALARIESPAYMENT OF SALARIES

JOURNAL ENTRYJOURNAL ENTRY

POSTINGPOSTING

Salaries Expense 726 Oct. 26 4,000

74

ILLUSTRATION ILLUSTRATION 2-28 2-28 RECEIPT OF CASH FOR FEES EARNEDRECEIPT OF CASH FOR FEES EARNED

ILLUSTRATION ILLUSTRATION 2-28 2-28 RECEIPT OF CASH FOR FEES EARNEDRECEIPT OF CASH FOR FEES EARNED

BasicAnalysis

Debit-CreditAnalysis

TransactionOctober 31, received $10,000 in cash from Copa Company for advertising services rendered in October.

The asset Cash is increased $10,000; the revenue Fees Earned is increased $10,000.

Debits increase assets: debit Cash $10,000. Credits increase revenues: credit Fees Earned $10,000.

75

ILLUSTRATION ILLUSTRATION 2-28 2-28 RECEIPT OF CASH FOR FEES EARNEDRECEIPT OF CASH FOR FEES EARNED

ILLUSTRATION ILLUSTRATION 2-28 2-28 RECEIPT OF CASH FOR FEES EARNEDRECEIPT OF CASH FOR FEES EARNED

JOURNAL ENTRYJOURNAL ENTRY

POSTINGPOSTING

76

STUDY OBJECTIVE STUDY OBJECTIVE 77

Prepare a trial balance and explain its purposes.Prepare a trial balance and explain its purposes.Prepare a trial balance and explain its purposes.Prepare a trial balance and explain its purposes.

77

THE TRIAL BALANCETHE TRIAL BALANCETHE TRIAL BALANCETHE TRIAL BALANCE

A A trial balancetrial balance is a list of accounts and their is a list of accounts and their balances at a given time.balances at a given time.

The primary purpose of a trial balance is to prove The primary purpose of a trial balance is to prove (check) that the debits equal the credits after (check) that the debits equal the credits after posting.posting.

If the debits and credits do not agree, the trial If the debits and credits do not agree, the trial balance can be used to uncover errors in balance can be used to uncover errors in journalizing and posting.journalizing and posting.

The procedures for preparing a trial balance consist The procedures for preparing a trial balance consist of:of:

11 List the account titles and their balances. List the account titles and their balances.

22 Total the debit and credit columns. Total the debit and credit columns.

33 Prove the equality of the two columns. Prove the equality of the two columns.

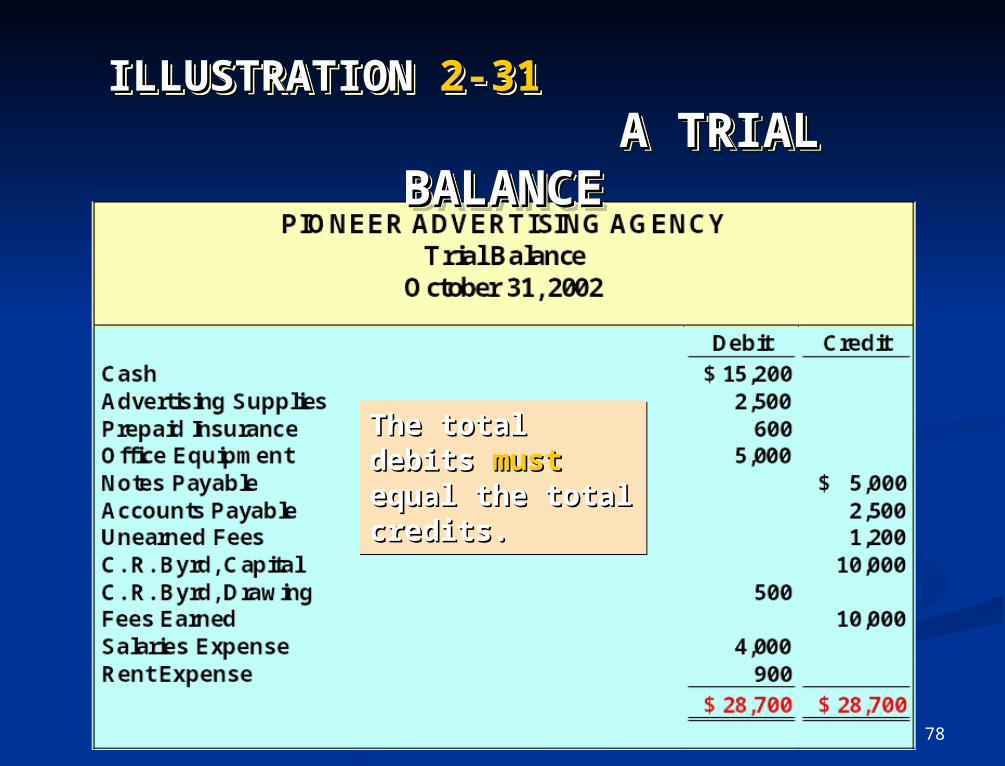

78

The total The total debits debits mustmust equal the total equal the total credits.credits.

The total The total debits debits mustmust equal the total equal the total credits.credits.

ILLUSTRATION ILLUSTRATION 2-31 2-31 A TRIAL BALANCEA TRIAL BALANCE

ILLUSTRATION ILLUSTRATION 2-31 2-31 A TRIAL BALANCEA TRIAL BALANCE

79

LIMITATIONS OF A LIMITATIONS OF A TRIAL BALANCETRIAL BALANCE

LIMITATIONS OF A LIMITATIONS OF A TRIAL BALANCETRIAL BALANCE

A trial balance does not prove that all A trial balance does not prove that all transactions have been recorded or that the transactions have been recorded or that the ledger is correct.ledger is correct.

Numerous errors may exist even though the trial Numerous errors may exist even though the trial balance columns agree.balance columns agree.

The trial balance may balance even when:The trial balance may balance even when:

11 a transaction is not journalized, a transaction is not journalized,

22 a correct journal entry is not posted, a correct journal entry is not posted,

33 a journal entry is posted twice, a journal entry is posted twice,

44 incorrect accounts are used in journalizing or incorrect accounts are used in journalizing or postingposting

55 offsetting errors are made in recording the offsetting errors are made in recording the amount of amount of the transaction. the transaction.