1. 2 your instructor (and fellow entrepreneur) kim brand computer experts, inc. server partners, llc...

TRANSCRIPT

1

2

Your instructorYour instructor(and fellow Entrepreneur)(and fellow Entrepreneur)

Kim BrandKim BrandComputer Experts, Inc.Computer Experts, Inc.Server Partners, LLCServer Partners, LLC

Fax2You, Inc.Fax2You, Inc.

[email protected]@KimBrand.com

3

Your (humble) instructorYour (humble) instructor(and fellow Entrepreneur)(and fellow Entrepreneur)

Kim BrandKim BrandComputer Experts, Inc.Computer Experts, Inc.Server Partners, LLCServer Partners, LLC

Fax2You, Inc.Fax2You, Inc.

[email protected]@KimBrand.com

4

Small Business FinancingSmall Business Financing

How much money do you need to How much money do you need to start your business?start your business?

Do not answer this question based on “gut” feel.Let the numbers talk.

Page 32-CFP and 33-CFP

5

Small Business FinancingSmall Business Financing

The amount you need for start-up includes:

Page 32-CFP and 33-CFP

Start-up Costs: Expenses that are incurred before the first sale is made.

Working Capital: Shortfalls in cash flow when sales are not high enough to cover expenses. Your monthly cash flow projections will tell you how much you will need.

6

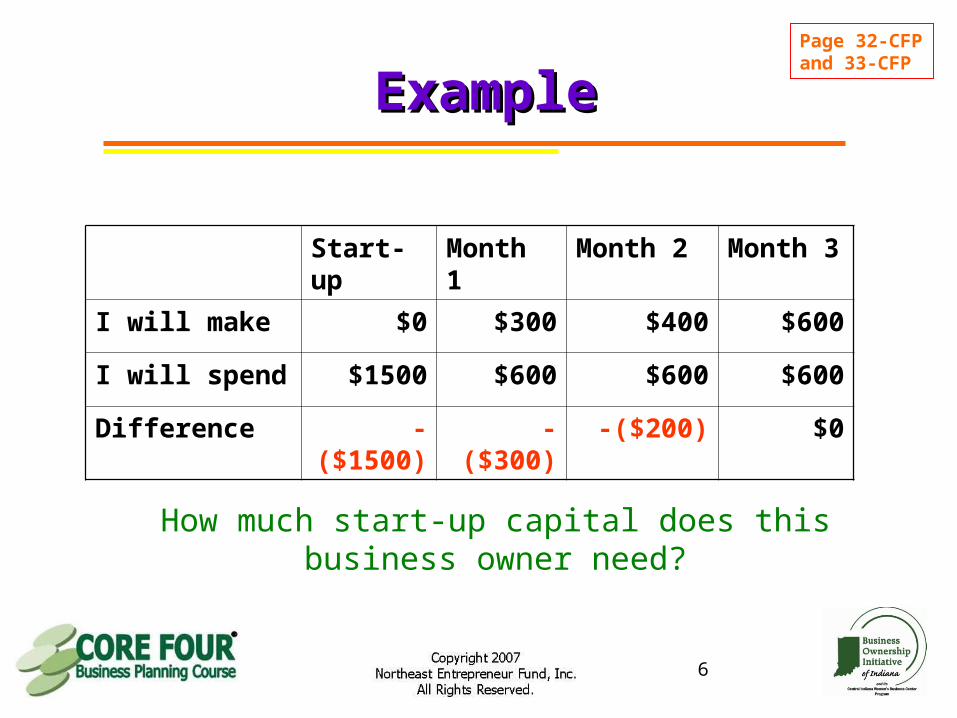

ExampleExamplePage 32-CFP and 33-CFP

Start-up Month 1 Month 2 Month 3

I will make $0 $300 $400 $600

I will spend $1500 $600 $600 $600

Difference -($1500) -($300) -($200) $0

How much start-up capital does this business owner need?

7

Bank Financing TerminologyBank Financing Terminology

Term (or Installment) Loan

Line of Credit

SBA Loan

8

Bank FinancingBank Financing

When reviewing your application for a loan, a lender will consider the 5 Cs of Credit:

Capacity: How will the company repay the loan?

Capital: What other sources of capital are being used?

Collateral: What can you use to secure the loan?

Conditions: What is the current local economic climate for the industry?

Character: Are you likely to be able to successfully run this business and appropriately manage the finances to repay the loan?

9

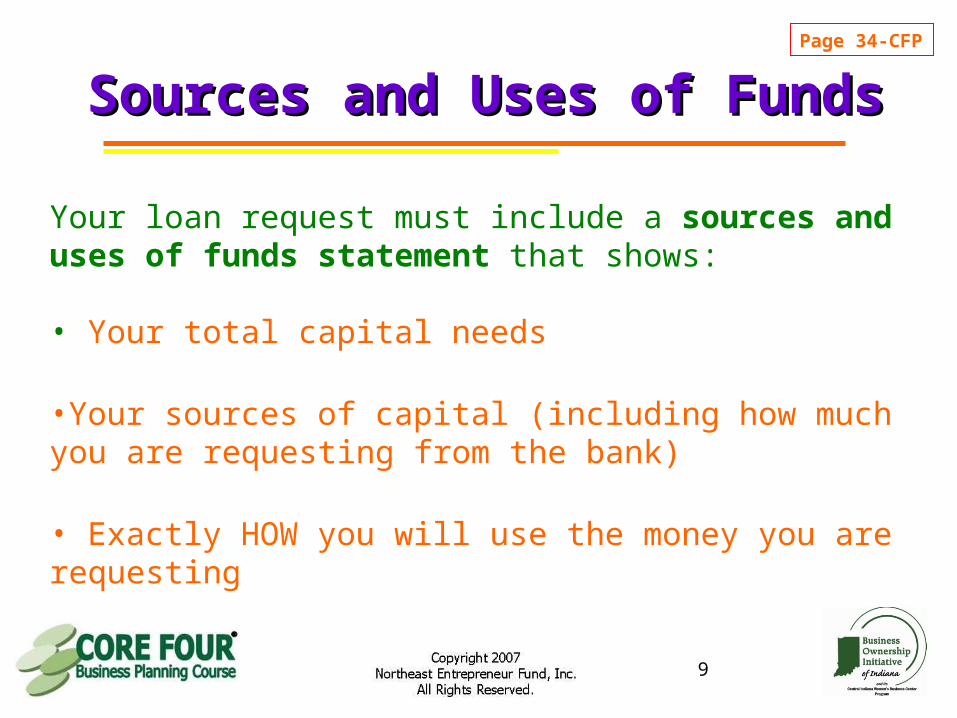

Sources and Uses of FundsSources and Uses of Funds

Your loan request must include a sources and uses of funds statement that shows:

• Your total capital needs

•Your sources of capital (including how much you are requesting from the bank)

• Exactly HOW you will use the money you are requesting

Page 34-CFP

10

Case StudyCase Study

Would you loan this business money?

What are the strengths and weaknesses of this loan request?

11

Before you apply for a loanBefore you apply for a loan

•Check your credit history and know your credit score. Begin cleaning it up if necessary

•Find a lending institution that regularly lends to small business and is familiar with your industry. Start developing the relationship early

•Create a solid business plan with adequate market research and complete financial projections.

•Be prepared – know how much you need, how you will use it, and how you will repay it.

•If an existing business, get your business records in order. Most lending institutions will want to see your Financial Statements and tax returns.

12

13

Operations PlanningOperations Planning

“Operations – Where it all comes

together”

Page 1-OP

14

Do your researchDo your researchPage 1-OP

As the business owner, you are responsible and accountable for meeting the legal

obligations of your business.

Get your information straight from the source (i.e. IRS, City zoning office) or from experts

(i.e. Certified Public Accountant (CPA), Attorney). Don’t take a friend or family

member’s word for it.

15

Business Compliance Business Compliance ConsiderationsConsiderations

Pages 2-OP through 18-OP

Registering Your Business Name with the Appropriate Authorities

• Involves selecting a legal form of business

Registering with taxing agencies to obtain tax ID numbers for the business

Paying all appropriate taxes – in the right amount and the right time – It’s not your money!

16

Business Compliance Business Compliance ConsiderationsConsiderations

Obtaining any required licenses and permits based on your type of business

Ensuring you are complying with any zoning regulations for your location

Obtaining appropriate insurance coverage, both to comply with the law and protect yourself

Having a separate business banking account and keeping appropriate records of business income and expenses

Pages 2-OP through 18-OP

17

Your Professional AdvisorsYour Professional Advisors

Start building your team of professional advisors to help keep you in compliance, help you protect your business, and help you grow your business:

A CPA (certified public accountant)

An Attorney

A Banker

An Insurance Agent

Page 19-OP and 20-OP

18

RecordkeepingRecordkeeping

Why keep records?

What information can a good recordkeeping system provide the

business owner?

Page 21-OP thru 23-OP

19

RecordkeepingRecordkeepingDesign a recordkeeping system that will allow you to:

• Find information on a historical transaction• When did Mrs. Smith last pay me and for what?

•Summarize the results of historical transactions• What were my total sales last month?

• Keep track of who owes you (accounts receivable) and who you owe (accounts payable)

• Did Mr. Jones pay his last invoice? If not, how late is he in making payment?

Page 21-OP thru 23-OP

20

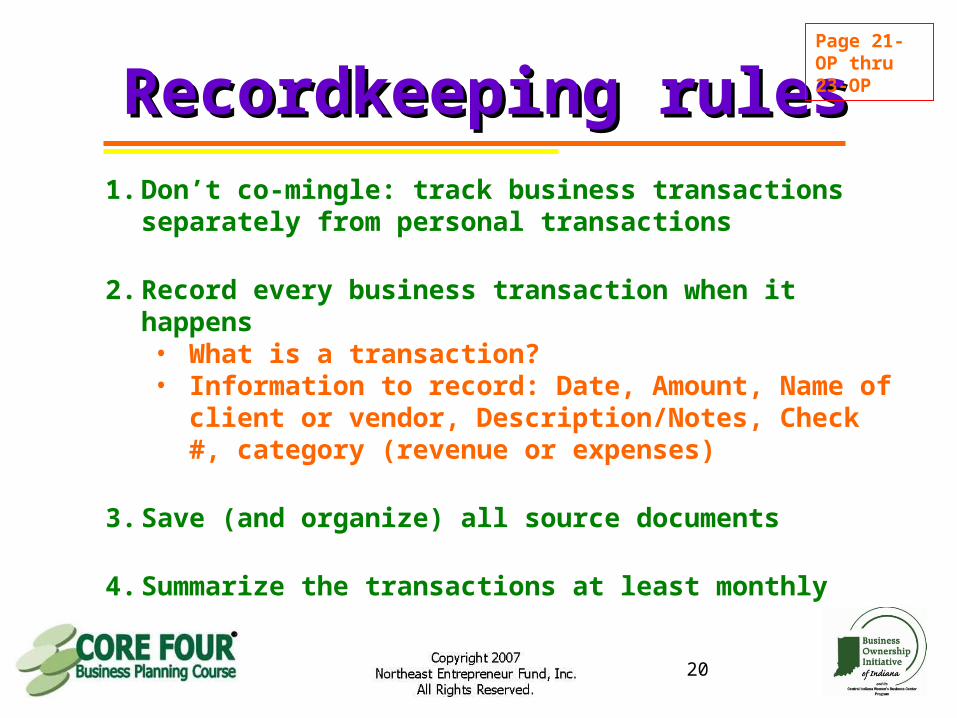

Recordkeeping rulesRecordkeeping rules1. Don’t co-mingle: track business transactions separately

from personal transactions

2. Record every business transaction when it happens• What is a transaction?• Information to record: Date, Amount, Name of client or

vendor, Description/Notes, Check #, category (revenue or expenses)

3. Save (and organize) all source documents

4. Summarize the transactions at least monthly

Page 21-OP thru 23-OP

21

RecordkeepingRecordkeeping

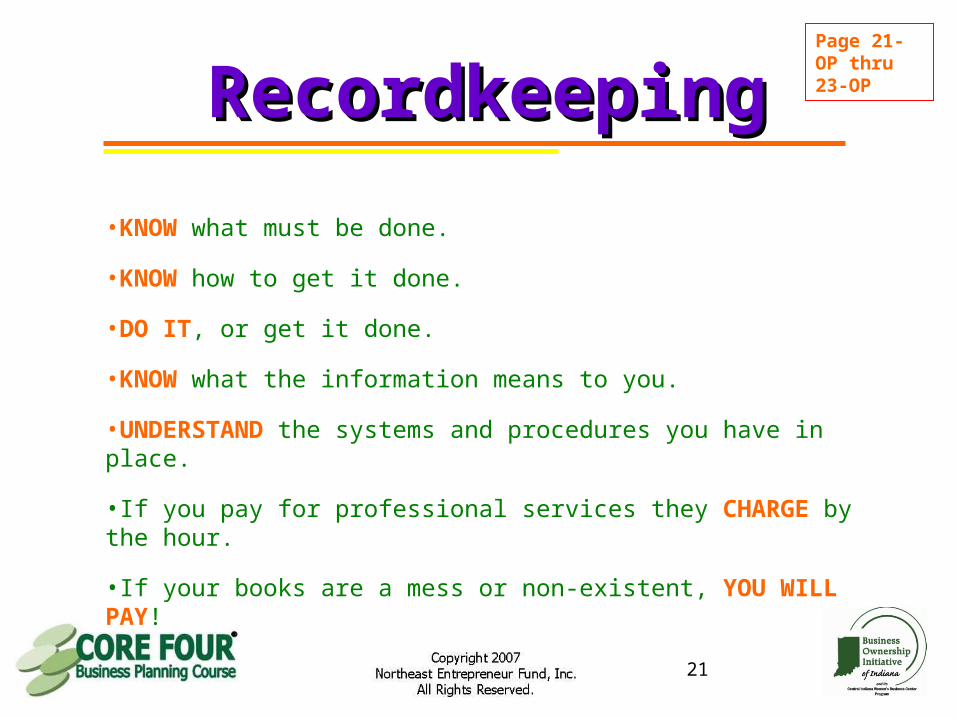

•KNOW what must be done.

•KNOW how to get it done.

•DO IT, or get it done.

•KNOW what the information means to you.

•UNDERSTAND the systems and procedures you have in place.

•If you pay for professional services they CHARGE by the hour.

•If your books are a mess or non-existent, YOU WILL PAY!

Page 21-OP thru 23-OP

22

Your Next StepsYour Next Steps Complete as much of the business plan as you can based on what was covered during this course.

Decide if your business idea is desirable, feasible, and viable for you at this time and if you choose to move forward with it.

Continue to meet with your counselor and have your progress reviewed.

23

Your Next StepsYour Next Steps When you’re ready, register for additional programs:

3-2-1 Launch! June 28 and 30, 6–8 pm

Becoming An Official Business: June 15, 6–8 pm

Establishing Your Brand Identity: June 14, 6–8 pm

Intro to QuickBooks: June 21 and 22, 6–8:30 pm

BOI networking event: June 27, 5:30–7:30 pm

24