070910 morgan final

TRANSCRIPT

Morgan Stanley 10Morgan Stanley 10 thth Annual Annual Latin America ConferenceLatin America Conference

London, September 11 & 12, 2007

2 2

Information and ProjectionThis notice may contain estimates for future events. These estimates merely reflect the expectations of the

Company’s management, and involve risks and uncertainties. The Company is not responsible for investment

operations or decisions taken based on information contained in this communication. These estimates are

subject to changes without prior notice.

This material has been prepared by TAM S.A. (“TAM“ or the “Company”) includes certain forward-looking

statements that are based principally on TAM’s current expectations and on projections of future events and

financial trends that currently affect or might affect TAM’s business, and are not guarantees of future

performance. They are based on management’s expectations that involve a number of business risks and

uncertainties, any of each could cause actual financial condition and results of operations to differ materially

from those set out in TAM’s forward-looking statements. TAM undertakes no obligation to publicly update or

revise any forwardlooking statements.

This material is published solely for informational purposes and is not to be construed as a solicitation or an

offer to buy or sell any securities or related financial instruments. Likewise it does not give and should not be

treated as giving investment advice. It has no regard to the specific investment objectives, financial situation or

particular needs of any recipient. No representation or warranty, either express or implied, is provided in relation

to the accuracy, completeness or reliability of the information contained herein. It should not be regarded by

recipients as a substitute for the exercise of their own judgment.

3 3

Low OperatingCosts

UndisputableBetter Service

CompetitivePrices

Sustainable Strategyto Maintain Market

Leadershipand Profi tabil i ty

TAM is a low cost company with better service at competitive prices

4 4

Previousperiod

Currentperiod

J FMAM J J A SOND J FMAM J J A SOND J FMAM J J A SOND J FMAM J J8085

9095

100

105110115

120125

130

Domestic Market - Variation

2004

Source: ANAC

Accum. market growth 2006

12%

The domestic market growth still strong in 2007, reaching 13% in the first 7 months of the year

Accum. market growth 2005

19%

Accum. market growth 2004

12%

Accum. market growth 2007

13%

200720062005

5 5

33,0%35,8%

47,8% 49,3%43,5%

2003 2004 2005 2006 Jan - Jul

TAM 50,6%

GOL 36,9%

BRA 4,1%

Varig 2,7%

Other 5,6%

We have been domestic market leaders since 2003, ending July with 49,3%

Domestic Market Share - July/07

Domestic Market Share (RPK’s)

Source: ANAC

TAM 49,6%

GOL 40,1%

BRA 2,7%

Varig 3,8%

Other 3,7%

Domestic Market Share – 2Q07

6 6

Previousperiod

Market

TAM

J F MAM J J ASOND J FMAM J J A SOND J F MAM J J A SOND J FMAM J J40

60

80

100

120

140

160

180

200

International Market - Variation(vs previous year)

Source: ANAC

The international market (among Brazilian carriers) is recuperating

Accum. market growth 20048%

Accum. market growth 20057%

Accum. market

decrease 2006 30%

Accum. market decrease 2007

24%

Acum TAM 200641%

Acum TAM 2007 75%

Acum TAM 200540%

Acum. TAM 200430%

2004 20072005 2006

7 7

12,00% 14,3%

37,3%

65,6%

18,8%

2003 2004 2005 2006 Jan - Jul

TAM 64,3%

GOL 15,6%

Varig 14,2%

Other 5,8%

International Market Share– July/07

International Market Share

Since July 2006, we are international market leaders among the Brazilian companies

Source: ANAC

TAM 70,8%

Varig10,7%

GOL 13,3%

Other5,2%

International Market Share – 2Q07

8 8

In the past 5 years, we have improved every operational metric…

No. take-offs (K)

Load Factor - LF Dom - LF IntMarket Share Dom

MS/CS Domestic

Aircraft Utilization (block hrs/day)

- Narrow bodies - Wide bodies

2003

76 147

61%58%71%33%

0.97

7.6

5.87.3

TAM S.A.2004

76151

66%64%71%36%

0.98

9.0

6.9 12.6

2005

81 210

71%70%73%44%

1.00

11.4

10.2 14.2

2006

92245

74%73%76%48%

1.02

12.7

12.4 15.1

No. operating aircraft

2002

102 219

55%53%61%35%

0.94

9.5

9.2 10.0

1H07

101130

71%71%70%49%

1.03

12.8

12.4 15.7

9 9

…resulting in an outstanding improvement in our financial metrics

Net revenues

EBITDAR

% EBITDAR EBIT

% EBIT

Net Income

% Net Income

2002

3,429

475

13.9%

(236)

-6.9%

(606)

-17.7%

2003

3,667

775

21.1%

(32)

-0.9%

174

4.7%

2004

4,520

1,038

23.0%

294

6.5%

342

7.6%

2005

5,649

1,140

20.2%

426

7.5%

187

3.3%

2006

7,345

1,817

24.7%

996

13.6%

556

7.6%

BR GAAP 1H07

3,322

593

15.6%

120

3.2%

31

0.8%

10 10

And a solid balance sheet improvement R$ million - BRGAAP 2007 2006 2005 2004

Cash 2.511 2.453 995 297

Short-Term Debt 445 363 216 204

Long-Term Debt 1.770 895 425 399

Total Debt 2.214 1.258 641 603

Shareholder's Equity 1.473 1.449 760 191

Capitalization 3.242 2.344 1.185 590

Aircraft and flight equipment leases 6.013 5.032 4.389 4.557

Total Debt Adjusted 8.227 6.290 5.030 5.160

Total Capitalization Adjusted 9.255 7.376 5.574 5.147

Debt / Capitalization 68% 54% 54% 102%

Adjusted Debt / Adjusted Capitalization

89% 85% 90% 100%

Adjusted Debt / EBITDAR 5,6x 3,5x 4,4x 5,0x

Adjusted Net Debt / EBITDAR 3,9x 2,1x 3,5x 4,7x

11 11

RASKCASK

2002 2003 2004 2005 2006 1Q07 2Q0715

20

25

RASK/CASK (R$ Cents)BR GAAP

EBITMargin

Spread

-7.1%

-1.1

-0.9%

-0.2

6.5%

1.4

7.5%

1.5

13.6%

2.8

4.8%

0.9

1.7%

0.3

However the competitive dynamic in the domestic market lead to a reduction of our spread in the 1H07

12 12

Structure of legal authorities involved in the industry

AIR FO R C EC O MMAN D

D EC EAAIR TRAFFIC/ SPACE

CONTROLCivil & Military Aircraft

N AVYC O MMAN D

ARMYC O MMAN D

C EN IP AAccident Investigation and Prevention Board

Air Traffic Control

A&I Investigation

National Civil Aviation Agency

M IN IS TR Y O F M IN IS TR Y O FD EFEN S ED EFEN S E

P R E S ID EN TP R ES ID EN T

C O N ACNational Civil

Aviation Council

DesignManufacturing

OperationsMaintenance

LicensingAirportsRegister

FacilitationSecurity

Air ServicesIntl. Air Navigation

ErgonomicsHuman Factors

IN FR AER O

13 13

CONAC announced guidelines for future implementation (1/2) Resolution no. 6, dated July 20, 2007, states that:

By ANAC

ANAC´s supervisory duties will be enhanced in order to assure unrestricted support to the victim´s family members

In 60 days, the take-off and landing rights at Congonhas will be reviewed, restricting them to point-to-point, direct flights

New international flights will be allocated outside the São Paulo terminal (Guarulhos and Congonhas)

No charter flights are allowed out of Congonhas

A permanent contingency plan for aircraft and crew must be established

14 14

CONAC announced guidelines for future implementation (2/2)

By ANAC and Air Force Command

Further restrict the use of Congonhas for General Aviation purposes

In 90 days, submit a study on possible locations for a new aiport site in São Paulo

By Infraero

In 90 days, submit a study for expansion and redesigning of airports in São Paulo

Seek clearance from the courts for spaces currently occupied by companiese under bankrupcy or reorganization

Promptly adopt redistribution of spaces to permit accomodation of a larger number of passengers at Guarulhos

15 15

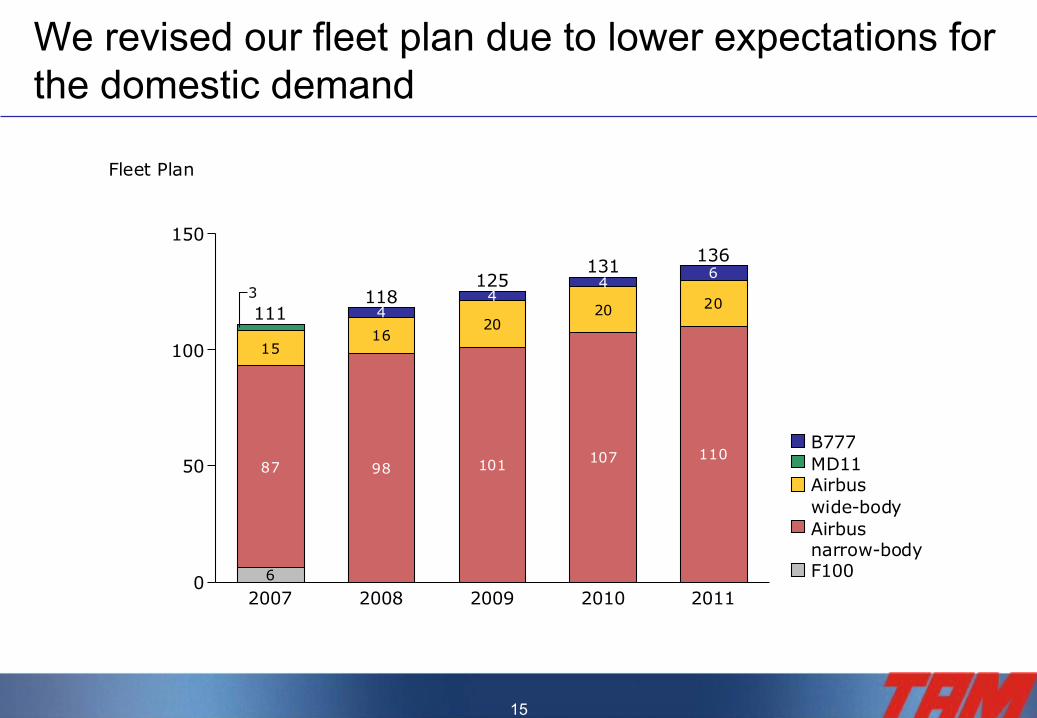

We revised our fleet plan due to lower expectations for the domestic demand

3

15

87

6

4

16

98

4

20

101

4

20

107

6

20

110

2007 2008 2009 2010 2011

111118

125131

136

0

50

100

150

Fleet Plan

F100

Airbusnarrow-body

Airbuswide-body

MD11B777

16 16

Average domestic market share above 50% Average domestic load factor at approximately 70% Aircraft utilization per day (block hour) higher than

13 hours Reduction of 7% in total CASK ex-fuel in BR GAAP

yoy Opportunity in the international market

Third frequency to ParisInauguration of two new international long haul

frequencies

Market demand growth from 10% to 15% (in RPK terms)

Guidance 2007

TAM

Market

However, our guidance for 2007, disclosed in December 2006, is still the same

12.6%*

1S07

• Since January• Milan (March),

Frankfurt and Madrid (December)

49.3%*

72.1%*12.8

9.2%

* Accumulated from January to July

17 17

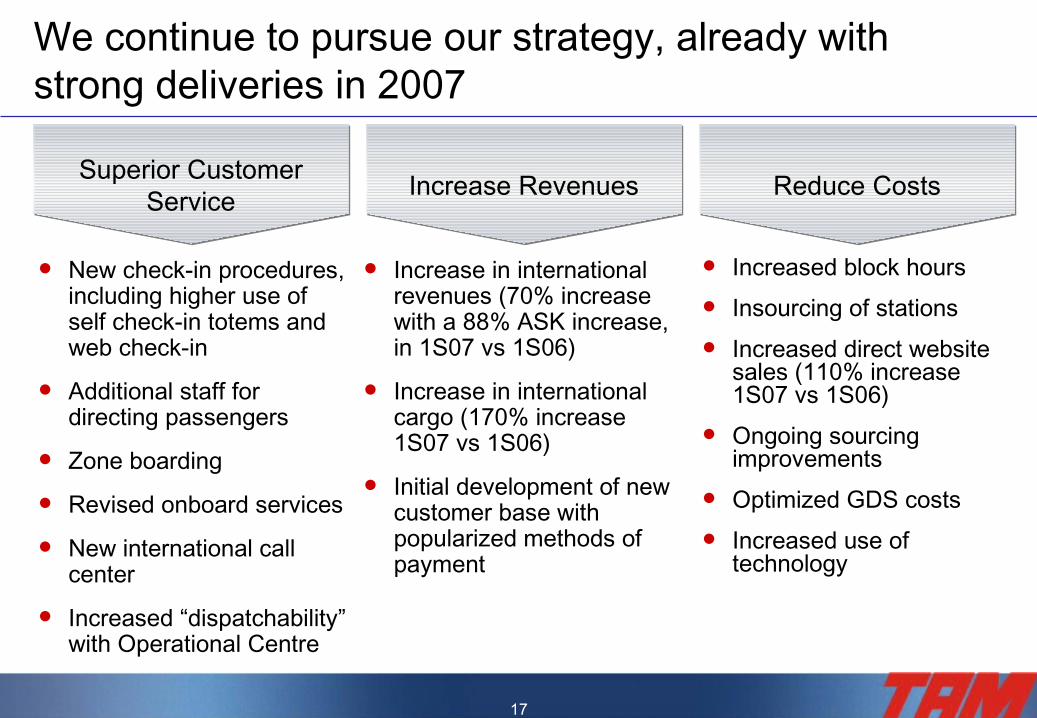

Increased block hours Insourcing of stations Increased direct website

sales (110% increase 1S07 vs 1S06)

Ongoing sourcing improvements

Optimized GDS costs Increased use of

technology

New check-in procedures, including higher use of self check-in totems and web check-in

Additional staff for directing passengers

Zone boarding

Revised onboard services

New international call center

Increased “dispatchability” with Operational Centre

Superior Customer Service

Increase Revenues Reduce Costs

We continue to pursue our strategy, already with strong deliveries in 2007

Increase in international revenues (70% increase with a 88% ASK increase, in 1S07 vs 1S06)

Increase in international cargo (170% increase 1S07 vs 1S06)

Initial development of new customer base with popularized methods of payment

18 18

We are well positioned to serve every part of the client spectrum (from leisure to business)

Launching new methods of payment Payment at lottery stores Billing slips Automatic debit Financing for passengers via direct consumer credit with the main retail banks

Providing specific products for the different segments

19 19