041511 2010 annual report.pdf

DESCRIPTION

nnvhkTRANSCRIPT

P W - 1 0 2

M A N I L A E L E C T R I C C O M P A N Y

L O P E Z B U I L D I N G , O R T I G A S A V E N U E ,

P A S I G C I T Y

1 2 - 3 1 1 7 - A 0 5 3 1

Dept. Requiring this Doc.

Total No. of Stockholders

Remarks = pls. use black ink for scanning purposes

S T A M P S

S.E.C Registration Number

Fiscal Year

File Number LCU

CashierDocument I.D.

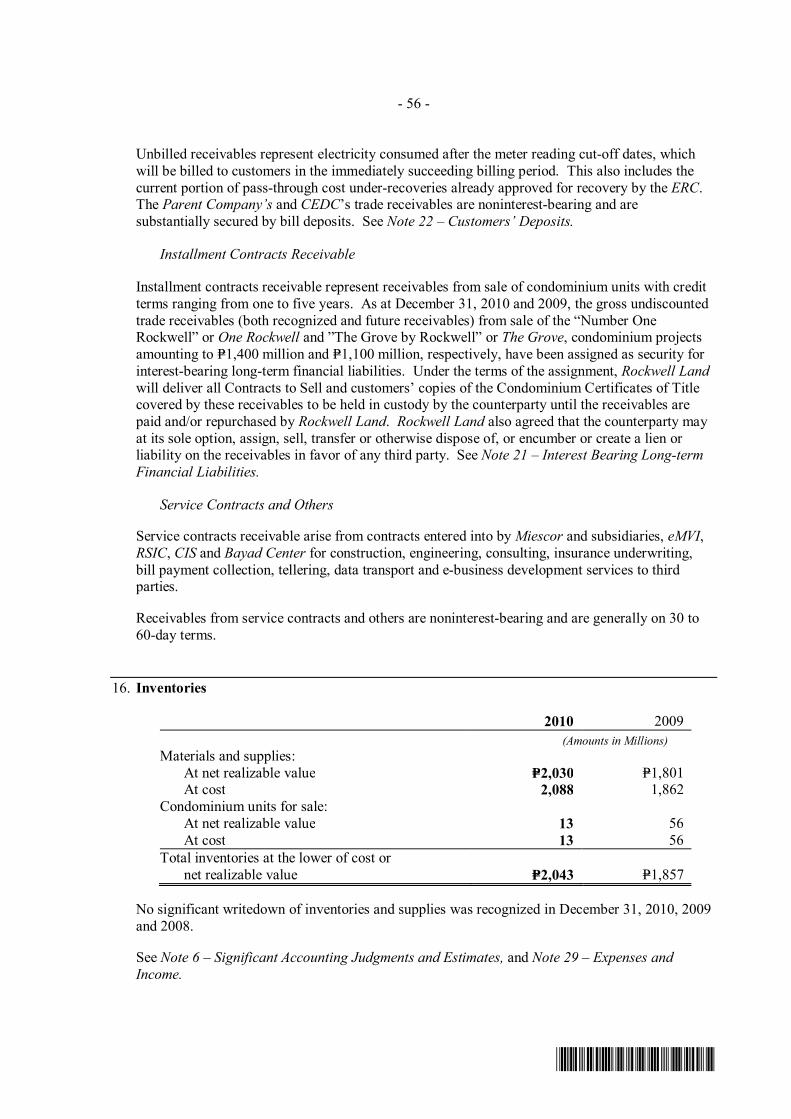

Domestic Foreign

Total Amount of Borrowings

To be accomplished by SEC Personnel concerned

Secondary License Type, if Applicable

Amended Articles Number/Section

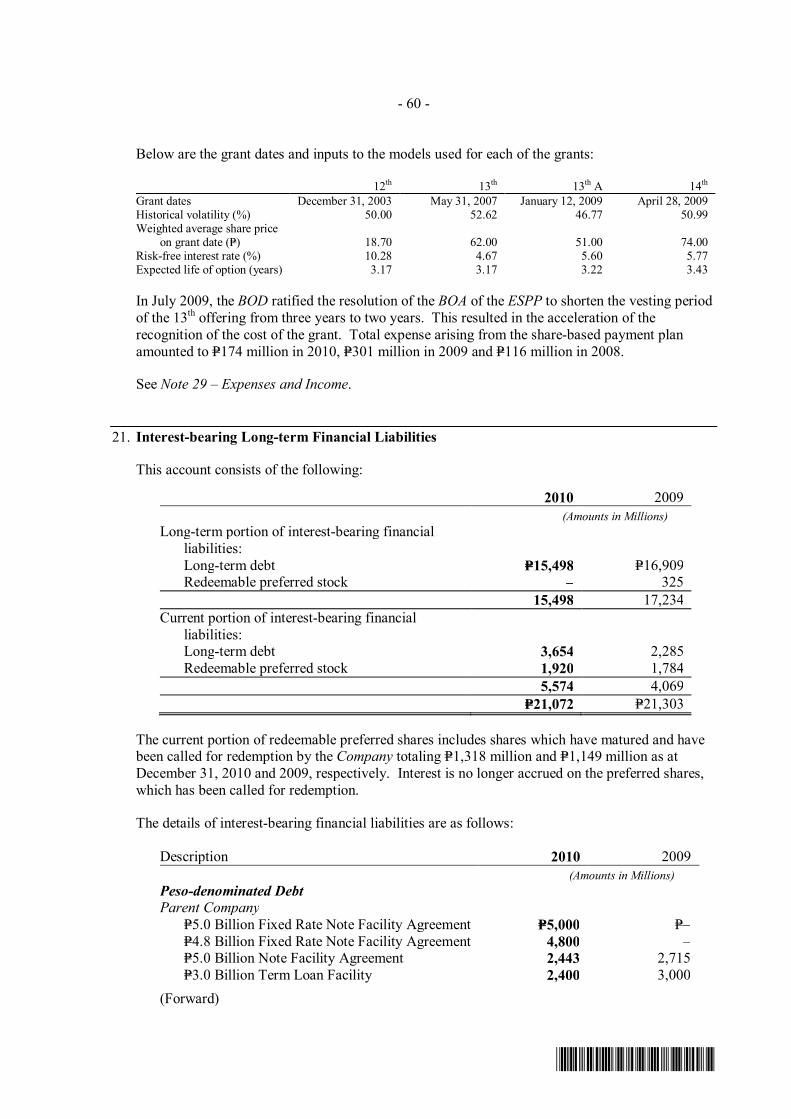

Annual Meeting

COVER SHEET

Contact Person Company Telephone Number

Month Day Month Day

(Company's Full Name)

(Business Address: No. Street City / Town / Province)

ATTY. ANTHONY V. ROSETE 1622-3186

FORM TYPE

TABLE OF CONTENTSTABLE OF CONTENTSTABLE OF CONTENTSTABLE OF CONTENTS

Page No.

PART 1 PART 1 PART 1 PART 1 –––– BUSINESS AND GENERAL INFORMATION BUSINESS AND GENERAL INFORMATION BUSINESS AND GENERAL INFORMATION BUSINESS AND GENERAL INFORMATION

Item 1. Business 5 Item 2. Properties 23 Item 3. Legal Proceedings 52 Item 4. Submission of Matters to a Vote of Security Holders 61

PART II PART II PART II PART II –––– OPERATIONAL AND FINANCIA OPERATIONAL AND FINANCIA OPERATIONAL AND FINANCIA OPERATIONAL AND FINANCIAL INFORMATIONL INFORMATIONL INFORMATIONL INFORMATION

Item 5. Market for Common Equity and Related Stockholders Matters 62 Item 6. Management’s Discussion and Analysis of Financial Condition and Results of Operation 64 Item 7. Financial Statements 122 Item 8. Changes in and Disagreements with Accountants on Accounting and Financial Disclosures 123

PART III PART III PART III PART III –––– CONTROL AND COMPENSATION INFORMATION CONTROL AND COMPENSATION INFORMATION CONTROL AND COMPENSATION INFORMATION CONTROL AND COMPENSATION INFORMATION

Item 9. Directors and Executive Officers 124 Item 10. Executive Compensation 135 Item 11. Security Ownership of Certain Record and Beneficial Owner and Management 137 Item 12. Certain Relationship and Related Transactions 141

PART IV PART IV PART IV PART IV –––– CORPORATE GOVERNANCE CORPORATE GOVERNANCE CORPORATE GOVERNANCE CORPORATE GOVERNANCE

Item 13. Corporate Governance 142

PART V PART V PART V PART V –––– EXHIBITS AND SCHEDULES EXHIBITS AND SCHEDULES EXHIBITS AND SCHEDULES EXHIBITS AND SCHEDULES

Item 14. Exhibits and Reports 154 SIGNATURES 160 INDEX TO FINANCIAL STATEMENTS AND SUPPLEMENTARY SCHEDULES 161

SECURITIES AND EXCHANGE COMMISSIONSECURITIES AND EXCHANGE COMMISSIONSECURITIES AND EXCHANGE COMMISSIONSECURITIES AND EXCHANGE COMMISSION

SEC FORM 17-A

ANNUAL ANNUAL ANNUAL ANNUAL REPREPREPREPORT ORT ORT ORT PURSUANT PURSUANT PURSUANT PURSUANT TO TO TO TO SECTIONSECTIONSECTIONSECTION 17 17 17 17

OFOFOFOF THE THE THE THE SECURITIES SECURITIES SECURITIES SECURITIES REGULATION REGULATION REGULATION REGULATION CODECODECODECODE

AND AND AND AND SECTION SECTION SECTION SECTION 141 141 141 141 OF OF OF OF THE THE THE THE

CORPORATION CORPORATION CORPORATION CORPORATION CODE CODE CODE CODE OF OF OF OF THE THE THE THE PHILIPPINESPHILIPPINESPHILIPPINESPHILIPPINES

1. For the fiscal year ended: December 31, 2010

2. SEC Identification Number: PW-102

3. BIR Tax Identification Number: 350-000-101-528

4. Name of Issuer as specified in its Charter: Manila Electric Company

5. Country of Incorporation: Philippines

6. (SEC use only) Industry Classification Code:

7. Address of principal office: Lopez Building, Ortigas Avenue, Pasig City

Postal Code: 0300

8. Telephone Numbers: 631-5567 Area Code: 0300

9. Former name or former address: Not applicable

10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA: (as of December 31, 2010)

Number of Shares of

Common Stock Outstanding

1,127,271,117

(As of December 31, 2010)

Amount of Debt Outstanding: P21.22 Billion (as of December 31, 2010)

11. Are any or all of these securities listed on the Philippine Stock Exchange:

YES [ x ] NO [ ]

If yes, state the name of such stock exchange and the classes of securities listed therein:

Philippine Stock Exchange

12. Check whether the issuer:

(a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports);

YES [ x ] NO [ ]

(b) has been subject to such filing requirements for the past ninety (90) days:

YES [ x ] NO [ ]

13. State the aggregate market value of the voting stock held by non-affiliates of the registrant. The aggregate market value shall be computed by reference to the price at which the stock was sold, or the average bid and asked prices of such stock, as of a specified date within 60 days prior to the date of filing. If a determination as to whether a particular person or entity is an affiliate cannot be made without involving unreasonable effort and expense, the aggregate market value of the common stock held by non-affiliates may be calculated on the basis of assumptions reasonable under the circumstance, provided the assumptions are set forth in this Form.

The aggregate market value of voting stock held by non-affiliates of the registrant

as of March 31, 2011:

Shares:

1,127,271,117

Closing Prices: Aggregate:

P258.00 P290.836 Billion

PART I PART I PART I PART I –––– BUSINESS AND GENERAL INFORMATION BUSINESS AND GENERAL INFORMATION BUSINESS AND GENERAL INFORMATION BUSINESS AND GENERAL INFORMATION

Item 1. Business

(1) Business Development

The name of the issuer is Manila Electric Company, also known as Meralco, duly organized on May 7, 1919 under the laws of the Republic of the Philippines. Its core business is distribution of electricity within its franchise area.

Consistent with Meralco’s franchise obligations and applicable laws, subsidiary companies were created to meet the Company’s specific needs for support, service, or enhancement that can either add value, savings, or profitability to, or improve the efficiency of, the core business or mitigate the impact of competition.

The following are the subsidiaries of Meralco, all of them incorporated in the Philippines except for Lighthouse Overseas Insurance Company, Limited.

Meralco Industrial Engineering Services Corporation (MIESCOR) is a subsidiary of Meralco incorporated on December 5, 1973. Miescor, a holder of the highest contractor license Category AAA since 1982, is a contractor/specialist engaged in engineering, construction and maintenance activities related to power generation, transmission and distribution, as well as industrial plants, water resources and telecommunications.

Miescor remains to be Meralco’s reliable provider in electro-mechanical works, engineering, distribution and technical services. It also handles telecommunication projects for Meralco, e-MVI and Philippine Long Distance Telephone Company (PLDT). Among its clients outside Meralco include Bangko Sentral ng Pilipinas (BSP), First Gen Corp., Chevron Philippines, Inc., Maynilad Water Services, Inc., Department of Finance (DOF) and Quezon Power (Phils.) Ltd.

Miescor operations is supported by its subsidiaries: Miescor Builders Inc. (MBI), Landbees Corporation and the recently-established, Miescorrail, Inc. Through their support, Miescor is able to expand and provide more diversified services.

Meralco owns 99% of the company and the remaining 1% by Miescor Provident Fund. Corporate Information Solutions, Inc. (CIS, Inc.) was incorporated in 1974 to provide information technology services and integrated business solutions, focusing on the functional areas that are critical to customers’ business continuity, growth and profitability. In 1997, CIS engaged in the business of bills payment collection which activity was spun off as CIS Bayad Center, Inc. (Bayad Center) formally incorporated in 2006. CBCI is the country’s trailblazer and brand leader in the outsourced over-the-counter (OTC) payment collection industry. With the vision of becoming a global organization and the undisputed leader in transaction-based services, this wholly-owned

Meralco subsidiary is one of the few Philippine companies certified as an “Investor in People” (IiP) by the People Management Association of the Philippines and the UK-based IiP Quality Centre.

Since 1997, Bayad Center continues to be entrusted by top multinational and local organizations with its bills collection requirements. It now accepts payments for over 160 leading brands through its 1,400-strong strategically-located branches nationwide. To complement its bills payment business, Bayad Center now offers electronic wallet services (vehicle insurance), prepaid loading, and applications acceptance.

Moving forward to 2011, Bayad Center will continue to raise the bar in the industry and increase its revenue by forging more strategic corporate partnerships; expanding its branch network in the Philippines and overseas; and introducing innovative business lines. Rockwell Land Corporation (Rockwell Land) is 51%-owned by the Manila Electric Company (Meralco) and 49% by First Philippine Holdings Corporation. Rockwell Land is one of the premier real estate developers in the Philippines. Formed in 1995, Rockwell Land’s ground-breaking master plan transformed the land where Meralco’s former thermal plant was located into a high-end living environment, now referred to as Rockwell Center.

Rockwell Center, the flagship project of Rockwell Land, sits on a 15.5-hectare site in Makati City. It is strategically located between the three major commercial business districts of Makati City, Bonifacio Global City and Ortigas.

In recent years, Rockwell Land has built a strong brand and track record in property development with its most recent projects outside Rockwell Center, namely, The Grove, a 5.4-prime hectare property along E. Rodriguez Avenue (commonly known as C-5 Road) and the Rockwell Business Center within the Meralco Ortigas compound. Its retail and cinema operations provide a continuous revenue stream and growth. Meralco Energy, Inc. (MEI) was established in June 2000 to provide demand-side energy services to Meralco’s key accounts in order to complement its parent company. MEI aims to be the country’s premier energy management company by providing total innovative energy solutions. Included in its mission is to complement Meralco’s vision of uninterrupted energy supply while providing added value through promotion of energy efficiency, renewable energy and innovation.

Presently, it provides a wide array of services related to power factor improvement, facilities management, ice thermal energy system, efficient lighting and renewable energy. It was also able to explore opportunities from emerging technologies that further promote energy efficiency and added key priorities today that focus on energy audit, energy management, HVAC energy solutions, and electric vehicle.

MEI, a wholly-owned Meralco subsidiary, continues to develop superior solutions for various energy related concerns that will allow customers to focus on their core business. e-Meralco Ventures, Inc. (e-MVI) is a 100% owned subsidiary of Meralco. Established on June 22, 2000, it is tasked primarily to leverage Meralco’s Fiber Optic resources and transform them into a profitable new business. It operates a telecommunications infrastructure within the Meralco

franchise area, offering data transport and connectivity services to local and international carriers, internet service providers, data centers and other businesses. eMVI continuously invests for the build-up of a data communication superhighway within Greater Manila Area (GMA) to serve all possible connectivity requirements of different bandwidths and interfaces. It operates on a 1,500 km fiber optic network and has established fiber optic presence in Makati and Ortigas Central business districts by forming alliances with other telecommunications companies.

The services of eMVI include leased line connections, Metro Ethernet connections, disaster recovery transport services and packaged internet bandwidth.

Over the years, eMVI has grown to be the premium data transport provider to the biggest names in the market. It consistently delivers installation lead times that are beyond industry standards and is true to its commitment to operate a future-proof network. Its business has remained profitable and it aims to reach farther, driven to make its mark in the telecommunications industry.

Meralco Financial Services Corporation (Finserve) is a wholly-owned subsidiary of Meralco incorporated on March 19, 2002 to create shareholder value by enhancing the range of value-adding services provided by Meralco through a portfolio of innovative consumer and customer-based products and multi-services that cater to retail and corporate clients.

In servicing the corporate market, Finserve continues to operate its Integrated Direct Marketing (iDM) service which includes direct mail campaigns, targeted advertising and a publication, Current magazine. iDM services are frequently availed by insurance companies, banks, consumer goods companies and educational institutions wanting to reach out to their specific markets.

Also catering to corporate clients, Finserve provides loyalty/rewards program management to aid companies in their marketing and consumer retention programs such as the Meralco Liwanag Card program. Clark Electric Distribution Corporation (CEDC), was organized on February 19, 1997 as a joint venture of Clark Development Corporation (CDC) and Meralco Industrial Engineering Services Corporation (MIESCOR), to serve the requirements of the Clark Economic Zone. As a Freeport Enterprise, Clark Electric is entitled to incentives, including tax and duty-free importation, as may be provided by law, and duly registered with the Incentives Administration Authority of the Freeport Zone under the virtues of Republic Act 9400, “An Act Amending Republic Act 7227, and otherwise known as the Bases Conversion and Development Act of 1992.”

In June 2003, however with the signing of a memorandum of agreement between CEDC, CDC and MIESCOR – with the eventual replacement of CDC by the Angeles Electric Corporation (AEC) – Clark Electric took over and started the integration, distribution and supply of electricity within the Clark Economic Zone.

In 2008, MERALCO took over the shares of MIESCOR in Clark Electric, making the company a 65%-owned subsidiary of MERALCO and 35% owned by Angeles Electric.

Republic Surety and Insurance Company, Inc. (RSIC) is a professional non-life insurance company and a wholly- owned subsidiary of Meralco acquired in 2007 to align with the latter’s recognition of a disciplined approach in managing its risk exposures.

RSIC continues to renew an insurance program that provides coverage to Meralco’s transmission and distribution assets. It aims to be the most dynamic, pro-active risk management and underwriting company – not just for Meralco and its subsidiaries and affiliated companies in terms of synergistic opportunities, but for the insurance industry as a whole, with a commitment to implement risk management methods with the emphasis on risk analysis and mitigation, loss control management and general insurance management.

RSIC is licensed to write the full spectrum of non-life insurance business to include property (fire and allied perils, industrial all risks and commercial all risks) and engineering, casualty, marine and aviation, motor, surety and special packages.

RSIC’s objective is to become an acknowledged leader in the field of risk management and to ensure profitability and market share while adhering to the principles of good corporate governance and corporate social responsibility. It envisions itself to be a total risk solution provider and a major player in the local insurance industry in the near future. Lighthouse Overseas Insurance Company, Limited (LOIL) was incorporated in Bermuda on August 24, 2007. It is registered as a Class 1 insurer under The Bermuda Insurance Act 1978 and Related Regulations and received its license to operate in the territory in March 2008. As Meralco’s captive Reinsurer, LOIL serves as the vehicle to reinsure its parent company’s major catastrophic risk exposure. Together with RSIC, LOIL is part of Meralco’s business risk management model.

[2] [2] [2] [2] Business of Issuer

The principal business of Meralco is the distribution and sale of electric energy through its

distribution network facilities in its franchise area. Its market is categorized into four (4) sectors, with their respective contributions to sales as follows:

2010 2009 2008

RESIDENTIAL 31.54% 32.36% 31.87%

COMMERCIAL 39.11% 39.69% 39.21%

INDUSTRIAL 28.88% 27.43% 28.40%

STREETLIGHTS 0.47% 0.52% 0.52%

TOTAL 100.00% 100.00% 100.00%

Meralco buys power from different power suppliers in the following proportions (in terms of

kWh):

2010 2009 2008

NATIONAL POWER CORPORATION

20.20% 34.37% 44.21%

FIRST GAS POWER CORP. and FGP CORPORATION

34.50% 37.01% 38.00%

QUEZON POWER (PHILS.) LTD. 10.29% 9.01% 9.19%

WHOLESALE ELECTRICITY SPOT MARKET (WESM)

14.02% 12.75% 8.58%

AES CORPORATION (MASINLOC)

4.05% 3.78% 0.00%

THERMA LUZON, INC. (PAGBILAO)

6.04% 1.26% 0.00%

SOUTH PREMIER POWER CORPORATION (ILIJAN)

4.29% 0.00% 0.00%

AP RENEWABLES, INC. (MAKBAN)

2.27% 1.49% 0.00%

SAN MIGUEL ENERGY CORPORATION (SUAL)

1.91% 0.17% 0.00%

SEM-CALACA POWER CORPORATION (CALACA)

2.38% 0.14% 0.00%

PHILIPPINE POWER AND DEVELOPMENT COMPANY

0.01% 0.01% 0.02%

MONTALBAN METHANE POWER CORPORATION

0.04% 0.01% 0.00%

TOTAL 100.00% 100.00% 100.00%

The franchise area of Meralco over specified areas in Luzon is approximately 9,337 square kilometers, covering 31 cities and 80 municipalities. This includes Metro Manila in the National Capital Region, industrial estates and suburban and urban areas of the adjacent provinces.

Government Approval of Principal Products or Services

On June 9, 2003, then President Gloria Macapagal-Arroyo signed into law Republic Act (RA) No. 9209, otherwise known as the “Manila Electric Company Franchise” which took effect on June 28, 2003 and granted the Company a 25-year franchise to construct, operate, and maintain an electric distribution system in the cities and municipalities of Bulacan, Cavite, Metro Manila, and Rizal and certain cities, municipalities, and barangays in the provinces of Batangas, Laguna, Pampanga, and Quezon.

On October 20, 2008, the Energy Regulatory Commission (ERC) granted the Parent

Company a consolidated Certificate of Public Convenience and Necessity (CPCN) for the operation of electric service within its franchise coverage, effective until June 28, 2028, to coincide with the Parent Company’s congressional franchise.

Meralco is involved in the distribution and supply of electricity and is subject to the rate-

making regulations and regulatory policies of the ERC. The Parent Company’s billings to customers are itemized or “unbundled” into a number of bill components that reflect the various costs incurred in providing electric service.

The adjustment of each bill component is governed by mechanisms promulgated and

enforced by the ERC, mainly: (i) the “Rules Governing the Automatic Cost Adjustment and True-up Mechanisms and Corresponding Confirmation Process for Distribution Utilities”, which govern the recovery of pass-through costs, including over- or under-recoveries in the following bill components: Generation Charge, Transmission Charge, System Loss Charge, Lifeline rate subsidies, Local franchise & business taxes; and (ii) the “Rules for the Setting of Distribution Wheeling Rates (RDWR)”, as modified by ERC Resolution No. 20, Series of 2008, which govern the determination of the Company’s Distribution, Supply, and Metering Charges.

Effect of Existing and of Probable Governmental Regulations on the Business

Supreme Court (SC) Decision on Unbundling Rate Case

On May 30, 2003, the ERC issued an Order approving the Company’s unbundled tariffs that resulted in a total increase in distribution-related rates of P0.17 per kWh over May 2003 levels. Subsequently, on August 4, 2003, certain consumer and civil society groups filed with the Court of Appeals (CA) a “Petition for Review” of the ERC’s ruling. On July 22, 2004, the CA set aside the ERC’s ruling and remanded the case back to the ERC. According to the CA, the ERC should have asked the Commission on Audit (COA) to audit the books of the Company. The ERC and the Company filed separate motions asking the CA to reconsider its decision, but the CA denied both motions; thus, the ERC and the Company elevated the case to the Supreme Court of the Philippines (SC).

In an En Banc Decision promulgated on December 6, 2006, the SC set aside and reversed

the CA ruling, saying that a COA audit was not a prerequisite in the determination of a utility’s rates. However, while the SC affirmed the ERC’s authority in rate-fixing, the SC also recognized the potential social impact of the matter. Thus, the SC directed the ERC to request COA to undertake a complete audit of the books, records, and accounts of the Company. On January 15, 2007, in compliance with the SC’s directive, the ERC engaged the COA to conduct an audit of the Company.

The COA audit, which began in September 2008 was completed in August 2009. In an Order dated February 15, 2010, the ERC directed all intervenors in the case to

submit their respective comments on the COA’s Final Audit Report within fifteen days of receiving a copy.

The Company has already submitted its comment on the COA audit report. Similarly, the intervenors have filed their comments to the COA audit report and the Company has responded to the same. The Company is awaiting the action of the ERC on the COA Audit Report.

Transition to Performance-Based Regulation

The Rules for Setting Distribution Wheeling Rates (RDWR), formerly known as the Distribution Wheeling Rate Guidelines (DWRG), embodies a new rate-setting methodology known as Performance-Based Regulation, or PBR. Under the previous Return on Rate Base (RORB) methodology, utility tariffs were based on historical costs plus a reasonable rate of return. On the

other hand, the PBR scheme sets tariffs according to forecasts of capital and operating expenditures to meet a predetermined level of operational performance. The RDWR also penalizes or rewards a utility, depending on its technical and customer service performance. The Company, along with the Dagupan Electric Corporation (DECORP) and Cagayan Electric Power and Light Company (CEPALCO), is a pioneer of PBR in the Philippines.

On August 31, 2007, the ERC issued its Final Determination on Meralco's PBR application,

paving the way for the implementation of the performance incentive scheme and price control arrangements for the Second Regulatory Period (from July 1, 2008 to June 30, 2011). The approved Maximum Average Prices (MAP) were P1.167 per kWh, P1.260 per kWh, P1.361 per kWh, and P1.471 per kWh for the Regulatory Years (RY) 2008, 2009, 2010, and 2011, respectively.

On January 11 and April 1, 2008, the Company subsequently filed separate applications for its proposed translation of the MAP for RY 2008 and 2009, respectively, into different rate schedules for various customer segments. In October 2008, the ERC approved a MAP for the RY 2009 of only P1.2280 per kWh to avoid price shocks and mitigate the rate impact on end-users. The ERC also directed the Company to implement its approved Distribution, Supply, and Metering Charges.

However, the ERC, acting on a motion filed by a group of electricity consumers, deferred the implementation of the approved charges until such time that the ERC can resolve a Motion for Reconsideration (MR) to be filed by the group. The Company eventually received a copy of the consumer group’s MR, to which we filed an Opposition on November 19, 2008. Another intervenor, representing large business consumers, similarly filed an MR on the ERC’s ruling

On April 23, 2009, the ERC resolved the MRs filed by the various consumer groups. The ERC amended its earlier approved MAP for RY 2009 to P1.227 per kWh, which reflects a zero Corporate Income Tax (CIT) component. Further, the ERC also revised downward the previously approved rates for residential end-users, to mitigate the impact of the rate adjustment, and aligned the tariff design closer to ‘cost-to-serve’. Implementation of the approved rates began in May 2009.

On May 28, 2009, a number of consumer groups filed a Petition before the Court of

Appeals to question the ERC’s Decision and Order on the RY 2009 MAP and rate translation application. Eventually, in a Decision dated January 29, 2010, the Court of Appeals dismissed the consumer groups’ Petition, saying:

• While the petitioners question the Decision and Order, what they were actually assailing was the shift to PBR methodology and the factors considered in the determination of Meralco’s Annual Revenue Requirement (ARR), which had been settled in ERC’s Final Determination. The Final Determination had long become final and executory;

• An evaluation of the assumptions used in the approval of Meralco’s rate unbundling is no longer required in this case, since the unbundling used a methodology that had already been abandoned by the adoption of the PBR methodology;

• The ERC’s RY 2009 rate translation rulings were issued after the conduct of the necessary proceedings and were rendered on the basis of the ERC's independent evaluation of the

evidence presented. The rule is well-settled that findings of fact of administrative agencies and quasi-judicial bodies that have acquired expertise because their jurisdiction is confined to specific matters are generally accorded not only great respect but even finality;

• ERC need not wait for the COA audit report on Meralco’s rate unbundling before it could approve Meralco’s rate translation application under PBR. The ERC’s Final Determination is separate and distinct from the Unbundling Decision where a COA audit report was required; and,

• A rate rollback and refund simply on the ground that Meralco’s financial statements for 2003 to 2007 purportedly showed excessive profits cannot be allowed. The ERC had already reviewed the Parent Company’s rate of return and found the petitioners' contention without basis. Meanwhile, on August 7, 2009, the Company filed a petition for the verification of the MAP

for RY 2010 and its translation into tariffs by customer category. In accordance with the ERC’s “Guidelines for RY2010 Rate Reset for First Entrant DUs”, the constrained MAP for RY 2010 was computed to be P1.4917 per kWh.

In a Decision dated December 14, 2009, the ERC approved the Company’s application

and directed the Company to, among other things, adopt the MAP for RY2010 of P1.4917/kWh and implement its approved Distribution, Supply and Metering Charges for its various customer classes starting January 2010 billing.

However, on January 26, 2010, your Company filed a manifestation at the ERC that it will suspend its implementation of the recently-approved MAP for RY 2010. The manifestation is in view of a Motion for Reconsideration (MR) filed by an intervenor on the said decision.

On February 1, 2010, the ERC granted the manifestation, saying that the suspension of the RY 2010 MAP implementation will be until such time that the ERC has resolved the pending MR and addressed all other issues that the other intervenors may raise on the December 14, 2009 decision. While a hearing on the MR was held on February 5, 2010, no intervenors appeared during the hearing. During the hearing, the ERC granted Meralco and other parties to the case 15 days to file their comments on the MR filed by one of the intervenors, Engr. Robert Mallillin. ERC also granted all the intervenors 15 days to comment on the comparison of rates that will be submitted by Meralco. On March 10, 2010 the ERC resolved the pending MR and lifted the suspension of the RY 2010 MAP implementation. The ERC revised the rate schedules to better ensure that there will be no cross-subsidies, other than the lifeline subsidy, in Meralco’s rates, while maintaining a MAP of P1.4917 per kWh. The implementation of the RY 2010 MAP resumed in April 2010.

On April 5, 2010 Meralco filed a verification and translation application for RY 2011, proposing a MAP of P1.6464 per kWh. Hearings were concluded last May 31, 2010 and the ERC ruled on the petition on December 6, 2010. The ERC adopted Meralco’s RY 2011 MAP of P1.6464 per kWh, limited by the side constraints, and S-factor of P 0.0087 per kWh. Meralco implemented the approved rates starting January 2011.

Third Regulatory Period Reset Application. On June 18, 2010, Meralco filed its Application for the approval of the Annual Revenue Requirement (ARR) and Performance Incentive Scheme (PIS) for the Third Regulatory Period (July 1, 2011 to June 30, 2015). Jurisdictional and expository hearings on the case were held last July 14 - 15 and August 9 - 10, 2010, initial pre-trial conference on August 11, 2010, and evidentiary hearings on October 19 and 21, 2010.

The Reset Application incorporates distribution rate under-recoveries incurred by Meralco for RYs 2008 to 2010. In accordance with the ERC’s Rules for Setting Distribution Wheeling Rates (RDWR), as amended, these under-recoveries, estimated at approximately P18,000 million, will be collected over the duration of the Third Regulatory Period.

On January 11, 2011, the ERC released its “Draft Determination” on Meralco's Reset Application for public comments. Public consultations were held on February 7 and March 15, 2010. Thereafter, a “Final Determination” will be released, which will set forth the ERC’s approval on Meralco’s ARR, PIS, and MAPs for the Third Regulatory Period, and Meralco will file its Rate Translation Application, which rates are scheduled to be implemented starting the July 2011 billing. Under-recoveries in Pass-Through Costs

Generation Cost Under-recoveries. During the suspension by the ERC of the Automatic Generation Rate Adjustment (AGRA), the Company filed 10 separate applications for the full recovery of generation costs, including value-added tax (VAT), incurred for the supply months of August 2006 to May 2007, which resulted in under-recoveries of P12,679 million for generation charges and P1,295 million for system loss charges.

On January 18, 2008, the ERC allowed the Company to collect P8,829 million of generation charges through a P0.1662 per kWh charge to customers. The charge was implemented beginning February 2008 and continued until January 2010, by which time the amount was fully collected.

On September 3, 2008, an ERC Decision on the remaining P3,850 million of generation charge under-recoveries directed the Company to recover P1,149 million, plus P813 million carrying charges. However, a portion of the Company’s purchases from the Wholesale Electricity Spot Market (WESM) for the period December 2006 to May 2007, amounting P2,701 million of the total amount applied for, was disallowed. Further, the Company was ordered to file a separate application for recovery of P1,295 million of system loss adjustments after the ERC confirms the average transmission rate to be used in the calculation of the system loss rate.

Meralco filed a Motion for Partial Reconsideration on the disallowance of P2,701 million because it believed that these were just and reasonable pass-through costs recoverable from its consumers. On September 21, 2010, the ERC released an Order dated August 16, 2010 granting Meralco’s Motion for Partial Reconsideration. The Order authorized Meralco to collect from its customers the additional generation cost for the period August 2006 to May 2007 of P3,371 million, inclusive of carrying charges.

Meanwhile, during the supply month of February 2010, the cost of generation went up to P6.7704 per kWh and would have translated into a generation charge of P6.76 per kWh for the March 2010 bills to customers an increase of P1.83 per kWh from the preceding month’s level.

The higher generation cost was mainly due to the cost of power sourced from the WESM, which increased from P6.08 per kWh in the January 2010 supply month to P12.16 per kWh in February. Contributing to the tightness in generation supply was the de-rating of almost all hydroelectric power plants in Luzon due to the El Niño phenomenon. The scheduled maintenance shutdown of the Camago-Malampaya pipeline starting February 10, 2010 and some other power plant units also curtailed supply. During the pipeline’s outage, the natural gas plants had to run higher-priced condensate fuel to continue power production.

To mitigate the impact to consumers of the higher generation cost, Meralco petitioned to the ERC on March 9, 2010 that it be allowed deferred recovery of the fuel cost differential pertaining to the use of condensate by the First Gas plants, equivalent to P1,046 million. Under Meralco’s petition, the recovery of this fuel cost differential would be spread over six months starting April 2010, so that the increase in the generation charge would be tempered from P1.83 to P1.38 per kWh.

On March 10, 2010, the ERC issued an Order modifying Meralco’s proposal. In addition to approving the deferred recovery of the condensate cost differential, the ERC limited to the NPC average rate the pricing of WESM purchases beyond 10%. The ERC said that this WESM cost differential amounting to about P1,120 million would undergo further evaluation by the Commission. Thus, the ERC provisionally approved a March 2010 generation charge of P5.8417 per kWh. The hearings on this case have been terminated and Meralco has filed its formal offer of evidence. Meralco is awaiting the ERC’s final decision on the matter of recovery of WESM purchases beyond 10% of Meralco’s total energy requirement. Recovery of Transmission Cost Under-recoveries. In September 2007, Meralco filed an application to recover P5,554 million in transmission charge under-recoveries accumulated between June 2003 to July 2007, along with a corresponding carrying cost. The application was brought about by the implementation of the “Guidelines for the Adjustment of Transmission Rates by Distribution Utilities,” which did not address the current and accumulated over-or under-recoveries in the collection of the transmission charge.

From August 2007 to March 2008, your Company continued to incur additional under-recoveries of P1,868 million. However, beginning April 2008 up to April 2009, over-recoveries of P6,396 million were accumulated, for a net over-recovery of P4,528 million. To address this, on July 29, 2009, the Company filed a petition for the confirmation of transmission charges imposed on customers from August 2007 to April 2009. It also proposed to offset the over-recoveries against the under-recoveries covered in its September 26, 2007 petition, which would result in a net under-recovery of 1,026 million, exclusive of carrying costs.

On October 21, 2009, the ERC issued its decision on the Company’s application to recover P5,554 million of transmission cost under-recoveries covering the period June 2003 to July 2007. The approval is net of certain disallowances by the ERC, which the ERC said the Company failed

to fully substantiate. The Company subsequently filed a Motion for Partial Reconsideration on October 30, 2009, and presented evidences to provide additional explanation and substantiation of the amounts disallowed by the ERC.

Also, on October 21, 2009, the ERC released an Order on a separate application of the Company to offset transmission cost over-recoveries of P4,528 million covering the period August 2007 to April 2009 against the under-recoveries being claimed. The ERC provisionally approved the offsetting proposal and directed the Company to refund over-recoveries amounting to P4,917 million and carrying costs of P257 million. Meralco has filed a manifestation of its intention to implement the Order, without prejudice to the outcome of the October 30, 2009 Motion for Partial Reconsideration and the hearing on the merits for this offsetting. The Company implemented the Decision starting the November 2009 billing.

On December 29, 2009, Meralco received an Order dated December 14, 2009 granting with modification its Motion for Partial Reconsideration of the Decision dated October 12, 2009. In the Order, the ERC reconsidered its earlier Decision and confirmed the total under-recoveries of Meralco in the transmission charges for the period June 2003 to July 2007 in the revised amount of P5,418 million and carrying costs amounting to P1,507 million.

The Company implemented the foregoing Decisions starting November 2009. As at December 31, 2010, the Company is yet to recover P88 million of such under-recoveries and carrying charges. Recovery of Under-recoveries in the Implementation of the Inter-Class Subsidy Removal. Meralco filed a petition for authority on November 14, 2007 to recover P1,054 million of under-recoveries and a corresponding carrying charge, incurred in implementing the Inter-Class Cross Subsidy system.

On November 27, 2009, ERC released its Decision dated November 16, 2009. The Decision approved with modification Meralco’s application, and authorized Meralco to collect the total inter-class cross subsidy under-recovery covering the period June 2003 to October 2006 amounting to P1,048 million, equivalent to P0.0103/kWh. The Decision was implemented beginning the December 2009 billing. Recovery of Under-recoveries in the Implementation of the Lifeline Rates. Finally, on February 19, 2008 the company filed an application with the ERC for the collection of the under-recoveries incurred in the implementation of the lifeline subsidy rate amounting to P864 million, with a corresponding carrying cost.

On November 27, 2009, ERC released its Decision dated November 16, 2009. The Decision approved with modification Meralco’s application, and authorized Meralco recover the total lifeline subsidy under-recovery covering the period June 2003 to December 2007 amounting to P856 million, equivalent to P0.0068/kWh. The Decision was implemented starting the December 2009 billing.

Revision of System Loss Caps

On December 8, 2008, the ERC promulgated Resolution No. 17, Series of 2008, entitled “A Resolution Adopting a New System Loss Cap for Distribution Utilities,” where it resolved to lower the maximum rate of system loss (technical and non-technical) that a utility can pass on to its customers. In the Resolution, the new system loss cap for private utilities shall be the actual system loss but not to exceed 8.5%, starting January 2010, one percentage point lower than the then system loss cap of 9.5%.

The Resolution further stated that company use of electricity shall be treated as part of operation and maintenance expenses in the next reset for utilities under PBR and that the manner by which the utility will be rewarded for its efforts in system loss reduction shall be addressed in the Performance Incentive Scheme (PIS) under PBR.

In a letter dated August 11, 2009, Meralco wrote to the ERC to appeal for a deferment of the imposition of the 8.5% system loss cap in 2010. In the letter, Meralco said that the confluence of certain developments that are beyond the Company's control will make it difficult for Meralco to comply with the new cap in 2010. In particular, the abrupt and substantial decline in industrial energy sales brought about by the economic downturn has reduced Meralco's high voltage sales. This is being aggravated by the continued increase in residential sales, which has pushed up the share of low voltage energy sales to the total consumption in the Meralco area. Meralco had further proposed that, "if there has to be a reduction in the cap, we propose that it be set at no loess than 9.0 percent, consistent with Republic Act No. 7832, until such time that caps based on the technical considerations identified in Republic Act No. 9136 can be determined."

In a letter dated November 23, 2009, while agreeing with the adverse impact on system loss of the reduced share of high voltage sales, the ERC replied that "both the existing and the proposed new caps were set regardless of whether or not the franchise area is highly urbanized". The letter further said that there are "more than sufficient means and incentives" for DUs like Meralco to deter or curb electricity pilferage. As a result, the Commission denied Meralco's request for a deferment of the cap.

On December 8, 2009, the Company filed a Petition to Amend the said Resolution with an urgent prayer for the immediate suspension of the implementation of the new system loss cap of 8.5% starting January 2010. The proposed amendment is aimed at making the Resolution consistent with the provisions of Republic Act No.9136 and Republic Act No. 7832, by increasing the level of system loss cap to not less than 9%. On November 18, 2010, the first and only hearing on the Petition was conducted by the ERC. Thereafter, Meralco was directed to submit its Formal Offer of Evidence (FOE). The Petition is awaiting the resolution by the Commission. Power Supply Option Program

On May 23, 2008, Meralco, together with other industry players, filed a Petition with the ERC for the implementation of Interim Open Access (IOA) in the Luzon and Visayas grids, in accordance with a proposed “Terms of Reference of the Interim Implementation of Open Access”. The Terms of Reference had been adopted by various energy industry players and stakeholders during the 2008 Energy Summit. The Petition sought to allow the eligible customers with an

average peak demand of 1 MW and up to contract and purchase their electricity requirements from Eligible Generating Companies through Retail Electric Suppliers. Eligible Generation Companies are generation companies which meet the mandated generation market share caps of EPIRA. In a Decision dated November 10, 2008, the ERC renamed IOA as the Power Supply Option Program (PSOP) and approved the Petition subject to the following conditions:

• Distribution utilities shall act as the default supplier and be accountable for the accounting and settlement of imbalances.

• The PSOP shall initially be implemented within the Luzon Grid.

• The implementation of the PSOP shall commence from the transfer of the operation of the Calaca privatized NPC generation assets.

• The PSOP shall cease to be operational upon commencement of actual Open Access and Retail Competition. All contracts and related transactions shall automatically terminate once actual Open Access and Retail Commission is declared by the ERC.

• The PSOP shall be strictly implemented in accordance with program rules to be promulgated by the ERC.

Meanwhile, on January 23, 2009, Suez Energy, the winning bidder of the 600-megawatt

Calaca coal-fired power plant, backed out from the deal to purchase the asset. In light of this development, the ERC on March 12, 2009 directed the PSOP proponents to submit comments on whether the precondition of privatizing Calaca will be maintained. The proponents, including your company, indicated that they are inclined to maintain the said precondition.

On September 14, 2009, the ERC released an Order stating that it takes judicial notice of the prospective sale and transfer of Calaca which could actually increase the number of competing entities in the PSOP should the winning bidder be a new player. The Order also states that the PSOP shall commence 90 days after completion of either of the following conditions, whichever comes earlier:

a) The transfer of the operation of the Calaca Generation Assets to the private generation companies concerned or its equivalent in terms of capacity; or

b) The privatization of at least 70% of the total capacity of generating assets of NPC in Luzon and Visayas.

Eventually, on December 3, 2009, the Power Sector Assets and Liabilities Management

Corporation (PSALM) turned over the 600-MW Calaca Coal-Fired Power Plant to Sem-Calaca Power Corporation, after the conduct of a negotiated sale of the power plant. Thus, the target commencement date for PSOP shall be on March 4, 2010.

On January 25, 2010, ERC approved the “Rules for the Power Supply Option Program (PSOP)”. According to the approved Rules, participating suppliers will not be required to be direct WESM members. The ERC also removed the provisions on retail settlement from the approved PSOP Rules. However, on January 27 2010, the ERC directed the PSOP proponents to submit to ERC harmonized procedures for retail settlement by February 23, 2010.

On February 26, 2010, the Philippine Electricity Market Corporation filed a Manifestation with the ERC, taking the position that it could not exercise a role beyond that of market operator under the WESM Rules. PEMC, however, stated that it was willing to provide data to the distribution utility (DU) or Supplier to calculate the settlement amounts of PSOP customers.

Meanwhile, on the same date, Meralco filed a Manifestation with the ERC, taking the

position that the PEMC is best suited to take on the role of the Settlement Agent because it has the necessary infrastructure, systems, procedures and policies to fulfill the role. The ERC released an Order on March 8, 2010 directing other Petitioners to comment on the Manifestations. The matter is still pending with the ERC. PEZA-ERC Jurisdiction

Meralco and the Private Electric Power Operators Association (PEPOA) had been holding compromise talks with the Philippine Economic Zone Authority (PEZA) to resolve the injunction case filed by the distribution utilities at the Pasig Regional Trial Court (RTC) against PEZA’s registration and open access guidelines namely, the “Guidelines in the Registration of Electric Power Generation Facilities/Utilities/Entities Operating Inside the Ecozones” and the “Guidelines for the Supply of Electric Power in Ecozones.”

The foregoing Guidelines effectively give PEZA franchising and regulatory powers in ecozones. PEZA can potentially carve out ecozones from a DUs’ service coverage and allow entities other than the franchise DU to provide distribution service within ecozones. PEZA may also set the tariffs and operating parameters of such electric distribution service providers. The situation may be aggravated by PEZA declaring additional ecozones in a DUs’ franchise area.

After a series of negotiations between PEPOA, your Company, and PEZA, the parties agreed to settle their differences. Through a letter dated June 6, 2008 from PEZA Director General Lilia B. De Lima, PEZA proposed the following to address the concerns of the PEPOA and the Company:

1. In the case of power utilities or entities currently operating a power distribution system inside the ecozone, the PEZA Board shall approve the registration of such entities upon compliance of all registration requirements.

2. The franchised distribution utility operating immediately outside a newly proclaimed ecozone shall have the right of first refusal to operate a power distribution system subject to compliance with all registration requirements.

3. Until such time that PEZA has fixed the appropriate Electric Power Distribution Charge, the current distribution and other distribution related charges shall prevail.”

These proposals were accepted by Meralco through a letter dated June 30, 2008, with

clarification on item no. 3, which the Company proposed to be rephrased as follows:

“Until such time that PEZA and ERC have agreed on principles of asset recognition and boundaries for rate-setting and PEZA has fixed the appropriate distribution charge, the prevailing distribution and other distribution-related charges, as may be adjusted in accordance with ERC’s guideline, shall apply.”

In a response letter dated July 3, 2008, PEZA Director General Lilia De Lima accepted this counter-proposal. Subsequently, the Company and PEPOA filed their motions to withdraw as plaintiffs in the case. Pending resolution of both motions, the Philippine Independent Power Producers Association (PIPPA) filed a Motion for Intervention, which was granted by the Court on September 2, 2008. Currently, both motions to withdraw by the Company and PEPOA are awaiting decision by the Court.

Meantime, in support of the government’s objective of providing lower cost power to ecozone locators, the Company entered into a Memorandum of Agreement with the NPC on September 17, 2007 for the provision of special ecozone rates to high load factor PEZA-accredited industries. The ERC allowed the immediate implementation the program.

On March 6, 2009, Meralco submitted an Application for Registration to PEZA to apply as an Economic Zone Utilities Enterprise for the establishment, operation, and maintenance of distribution facilities at the Carmelray Industrial Park II (CIP II) Special Economic Zone. This was in preparation for the turn-over of electric distribution and supply services within CIP II from CIP Power to Meralco. The PEZA Board subsequently approved the application via its Resolution No. 09-161, subject to the Company’s signing of a Registration Agreement under certain terms and conditions.

On January 18, 2010, Meralco signed the Registration Agreement with PEZA as an Economic Zone Utilities Enterprise at CIP II in Calamba, Laguna. Shutdown of TransCo's Sucat-Araneta Transmission Line

The Sucat-Araneta-Balintawak 230kV Transmission Line Project was conceptualized in the early 1990s to improve the overall electric system reliability and efficiency in Metro Manila. The construction of the said transmission line started in 1994 and was finished and energized in July 2000. This line completes the 230kV line loop within Metro Manila and addresses the congesting electricity traffic in the metropolis due to ever growing demand for electricity. The project has two main parts: (1) the Araneta to Balintawak leg; and (2) the Sucat to Araneta leg. Prior to 2001, the authority and responsibility to operate and develop the nationwide grid belonged to NPC. Upon the effectivity of EPIRA in June 2001, this authority and responsibility were transferred to the National Transmission Corporation.

The distribution lines of the Company are “physically connected” to the transmission grid of TransCo. More importantly, the Company’s distribution facilities are configured to operate in synchronicity with the lines of TransCo. The subject Sucat-Araneta-Balintawak 230kV Transmission Line is one of the important lines of TransCo and is located in the heart of your Company’s franchise area. Thus, the unrestrained operation of the said line is very vital to Company’s ability to deliver continuous electricity to every household and business establishment within its franchise area.

On March 10, 2000, the residents of Tamarind Road, Dasmariñas Village, Makati filed a case with the Regional Trial court of Makati City (RTC-Makati) against the National power Corporation (NPC) to enjoin the latter from further preparing and installing high voltage cables to the steel pylons erected near the plaintiffs’ homes and from energizing and transmitting high

voltage electric current through said cables, citing alleged health risks and danger posed by the same. On March 13, RTC-Makati initially issued an order directing the parties to maintain the status quo, and three weeks later granted the preliminary injunction prayed for by the plaintiffs. However, the CA subsequently reversed the orders. On appeal, the SC, in its Order issued on March 23, 2006, reinstated the orders of the RTC-Makati restraining NPC.

When the aforesaid Order of the SC became final, the plaintiffs then moved for the execution of the orders rendered by RTC-Makati. Subsequently, a writ of execution was issued on October 13, 2008 by RTC-Makati. The Company, although initially not a party to the case, was constrained to file an Omnibus Motion (1) for Leave to Intervene and to admit Answer in Intervention, (2) to lift orders, and (3) to maintain status quo due to the significant impact of the de-energization of the Sucat-Araneta line to the public and the economy. In the said Omnibus Motion, your Company argued that the shutdown of the 230 kV line would result in widespread and rotating brownouts across its franchise area, including the major financial districts in Metro Manila. Likewise, as much as 505 MW capacity from power plants from the south would be prevented from running their full capacities, resulting in a much higher additional purchased power cost for the Company which, in turn, would translate to significant increase in the price of electricity charge to its consumers.

On November 28, 2008, the RTC-Makati issued an Order accepting the Company’s Omnibus Motion and holding in abeyance the writ of execution until after the trial court finally rules on the Company’s Omnibus Motion for intervention and other incidents.

On September 11, 2009, the RTC-Makati issued an Omnibus Order dated September 8, 2009, granting the motions for intervention filed by the Company and the National Grid Corporation of the Philippines (NGCP) and dissolved the Writ of Preliminary Injunction issued pursuant to the Orders of the trial court dated April 3, 2000 and October 13, 2008 upon the posting of a counter bond by defendant NPC in the amount of P10.0 million, intervenors Meralco and NGCP in the amount of P2.5 million each, subject to the condition that defendant NPC and intervenors will pay all damages which the plaintiffs may suffer by the dissolution of the Writ of Preliminary Injunction. Expanded Senior Citizens Act of 2010 (ESCA)

Republic Act No. 9994, otherwise known as the Expanded Senior Citizens Act of 2010 (ESCA), was signed into law on February 16, 2010. The ESCA amends certain provisions of Republic Act No. 9257, which mandates the grant of benefits to senior citizens and to institutions catering to senior citizens.

The ESCA grants senior citizens a minimum 5% discount on the monthly electric bill, for services that are registered in the name of the senior citizen and whose monthly consumption does not exceed 100 kWh. Moreover, the law gives a discount of at least 50% on the consumption of electricity by senior citizens centers and residential care/group homes.

The ESCA took effect on April 22, 2010 and its Implementing Rules and Regulations (IRR) were promulgated by the Department of Social Welfare and Development (DSWD) on June 18, 2010. The IRR provides that utility-regulatory agencies (such as the ERC) shall, within six months after the IRR takes effect, “formulate supplemental guidelines to cover recovery rate mechanisms

and/or sharing of burden, among other concerns of the distribution utilities,” in the implementation of the discounts provided under the law.

On January 5, 2011, the ERC released Resolution No. 23, Series of 2010 adopting the “Rules Implementing the Discounts to Qualified Senior Citizen End-Users and Subsidy from the Subsidizing End-Users on Electricity Consumption under Sections 4 and 5 of Republic Act No. 9994”. Meralco implemented the discount starting the February 2011 billing.

Costs and Effects of Compliance with Environmental Laws

Compliance with environmental laws is part of Meralco’s good governance and enhances its relationships with environmental pressure groups. Specific programs such as solid waste management, water conservation, air pollution control, and wastewater management have been implemented by the Company to ensure compliance with environmental laws and preservation of the natural resources covered by its franchise area. Meralco has incurred a total amount of P515,000.00 representing renewal and application of permits for new or expansion projects; P1,500,000.00 accounted for the maintenance of Sewage Treatment Plants (STPs) and P300,000 for waste collection and disposal.

Government Approval and Regulation

Meralco is subject to regulation by the Energy Regulatory Commission (ERC) and recognizes the rate-making policies of the ERC.

Human Resource Profile

Number of Employees Meralco has a total of 6,203 regular employees for the year ended 2010. This is one percent (1%) higher than 2009’s year-end count of 6,112. The increase in manpower is attributable to Management’s strategy to augment the core and frontline positions directly involved in the delivery of services to the growing customer base. The table below illustrates the comparative count based on employee classification according to the role they perform in the organization.

YEAREND COUNT CLASSIFICATION

DEFINITION 2009 2010

% INC/DEC

Leadship 1,238 1,212 -2.10%

1. Top Management Department / Group Heads 36 41 13.89%

2. Middle Management Division Heads 141 144 2.13%

3. Junior Management Team Leaders and Supervisors 1,061 1,027 -3.20%

Non-Leadship 4,874 4,991 2.40%

1. Professional / Technical

Consists of employees who carry out professional functions in engineering, medical, legal, accounting, HR and education, and other fields. Work requires consistent exercise of discretion and judgment.

1,256

1,307

4.06%

2. Office Operations Consists of personnel who provide direct support to processes/operation of the organization

1,089

1,096

0.64%

4. General Administrative

Consists of administrative / clerical personnel who provide support to the resource management function of the Office of the Head.

286

289

1.05%

4. Skilled / Trade Workers in this group are engaged in tasks, using and operating hand tools and motorized equipment to fabricate, construct, process, install or repair materials, equipment and structural parts utilizing special techniques, training and experience.

2,243

2,299

2.50%

Total 6,112 6,203 1.49%

Labor Unions

Meralco has two (2) Labor Unions, namely, Meralco Employees and Workers Association (MEWA) and First Line Association of Meralco Supervisory Employees (FLAMES). MEWA (with total number of members equal to 803 employees) is the authorized bargaining agent for regular pay grade (PG) I-VI employees; while FLAMES (with 2,054 members) represents the regular PG VII-XII employees.

Year 2010 is a remarkable year for the Labor Unions as this is the first time in the Company’s history that Collective Bargaining Agreements (CBAs) for both MEWA and FLAMES were formally signed simultaneously. The negotiations were concluded after 5 and 4 negotiation meetings for MEWA and FLAMES, respectively, which were both within record time and within budget.

Highlights of the CBAs for both MEWA and FLAMES include the payout of one-time lump sum; and the increase in Outside Medical and Surgical Treatment for all Rank & File and Supervisory employees.

Item 2. Properties

Attached are the following:

• Update of Leased Offices

• Update of Leased Substations

• Schedule of Property Plant and Equipment

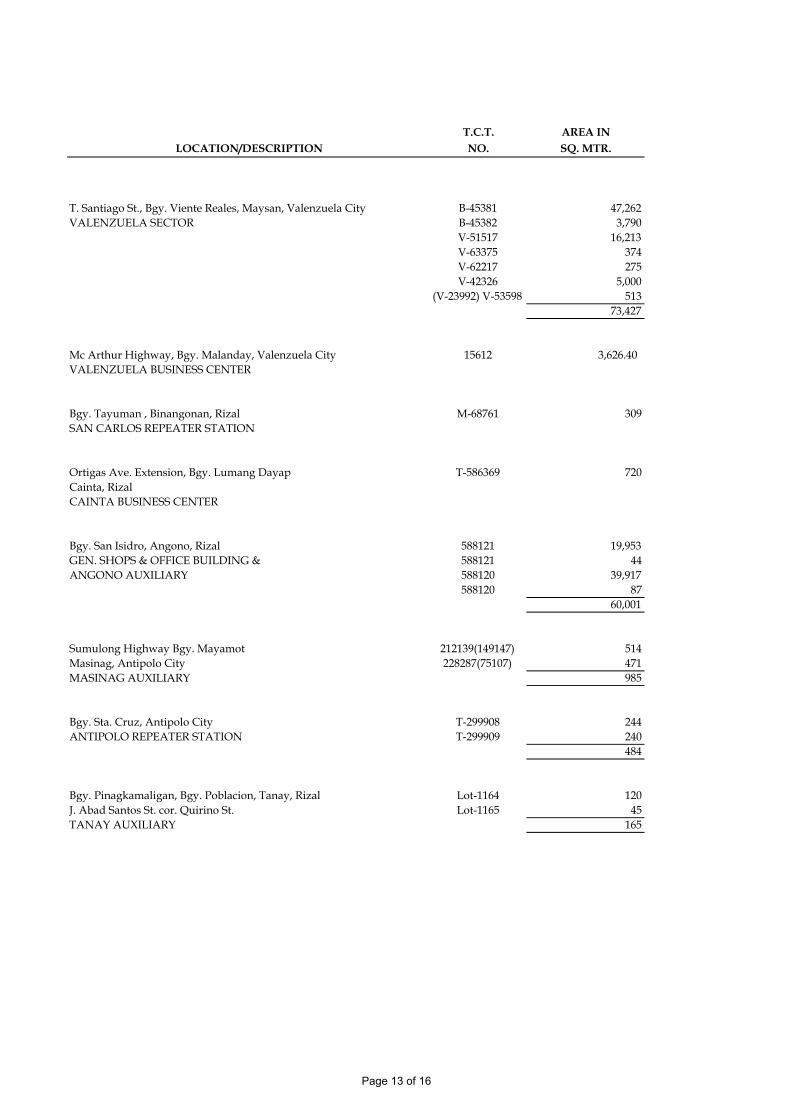

• Summary of Land Account (location and description) The real properties enumerated in the Summary of Land Account are used as sites for the

Company’s transmission lines, substations, operating/service centers, and principal/district/branch offices.

LESSOR OFFICE LOCATION AREA PRINCIPAL VAT BASIC EWT NET OF TAX LEASE TERM

A Extension/Payment Offices

1 Judge Noe A. Amado Corporation San Mateo Payment Office No.503 Gen. Luna St., Malanday, San Mateo, Rizal 85.00 P 40,000.00 P 0.00 P 40,000.00 P 2,000.00 P 38,000.00 Dec. 1, 2009 to Nov. 30, 2010

P 40,000.00 P 0.00 P 40,000.00 P 2,000.00 P 38,000.00 Dec. 1, 2010 to Nov. 30, 2011

2 Mrs. Regina D. Dimaraan Trece Martirez Extension 162 Luciano St. Trece Martirez City, Cavite 207.80 P 60,591.94 P 0.00 P 60,591.94 P 3,029.60 P 57,562.34 Sept. 1, 2009 to Aug. 31, 2010

P 60,591.94 P 0.00 P 60,591.94 P 3,029.60 P 57,562.34 Sept. 1, 2010 to Aug. 31, 2011

3 L.S.E. Trading Corporation Bahayang Pag-Asa Payment Corner of Bahayang Pag-Asa Road & Molino Road, 86.40 P 30,144.22 P 3,617.31 P 33,761.53 P 1,507.21 P 32,254.32 Jan. 1, 2010 to Dec. 31, 2010

Ms. Evelyn E. Eusebio Bacoor, Cavite

4 TSP General Trading, Inc - GMA Extension Office Governor's Drive, Brgy. Bulihan, Silang, Cavite 510.00 79,860.00 P 9,583.20 P 89,443.20 P 3,993.00 P 85,450.20 Sept. 1, 2009 to Aug. 31, 2010

Mr. Tomas San Pedro 87,846.00 P 10,541.52 P 98,387.52 P 4,392.30 P 93,995.22 Sept. 1, 2010 to Aug. 31, 2011

5 Mr. Ernesto H. Belardo Silang Extension No. 132 J. Rizal St., Silang, Cavite 98.86 P 51,602.72 P 6,192.33 P 57,795.05 P2,580.14 P 55,214.91 Dec. 1, 2009 to Nov. 30, 2010

6 Manuela Corporation Metropolis Extension South Superhighway, Alabang, Muntinlupa City, 133.00 P 119,741.23 P 14,368.95 P 134,110.18 P 5,987.06 P 128,123.12 June 1, 2009 to May 31, 2010

P 119,741.23 P 14,368.95 P 134,110.18 P 5,987.06 P 128,123.12 June 1, 2010 to May 31, 2011

7 Mr. Jose M. Abalos Los Baños Payment Office National highway, Barangay Anos, Los Baños, Laguna 104.00 P 51,476.69 P 6,177.20 P 57,653.89 P 2,573.83 P 55,080.06 Nov. 1, 2009 to Oct. 31, 2010

P 54,050.52 P 6,486.06 P 60,536.58 P 2,702.53 P 57,834.06 Nov. 1, 2010 to Oct. 31, 2011

8 Ms. Mayla L. Reyes Mauban Extension 33 Quezon Extension, Mauban, Quezon 64.00 P 4,537.52 P 0.00 P 4,537.52 P 226.88 P 4,310.64 Sept. 1, 2009 to Aug. 31, 2010

P 5,000.00 P 0.00 P 5,000.00 P 250.00 P 4,750.00 Sept. 1, 2010 to Aug. 31, 2011

9 Epifanio & Cecilia Guillermo Marilao Extension Unit No. 7, Commercial Building, along McArthur Highway, 140.00 P 25,898.59 P 3,107.83 P 29,006.42 P 1,294.93 P27,711.49 Jan. 1, 2010 to Dec. 31, 2010

10 Mrs. Rebecca S. David San Miguel Extension 53 Tecson Street, Poblacion, San Miguel, Bulacan 109.00 P 29,464.29 P 3,535.71 P 33,000.00 P 1,473.21 P 31,526.79 Nov. 1, 2009 to Oct. 31, 2010

11 ACC Farmer's Development Corp. Hagunoy Extension Along Sto. Nino St., Hagonoy, Bulacan 83.00 P 37,202.78 P 4,464.33 P 41,667.11 P 1,860.14 P 39,806.97 Feb. 1, 2009 to Jan. 31, 2010

P 37,202.78 P 4,464.33 P 41,667.11 P 1,860.14 P 39,806.97 Feb. 1, 2010 to Jan. 31, 2011

P 39,062.92 P 4,687.55 P 43,750.47 P1,953.15 P 41,797.32 Feb. 1, 2011 to Jan. 31, 2012

12 Mr. Rodolfo Garcia Sapang Palay Extension Area I, Block 29, Lot 2, Sapang Palay, 93.18 P 15,192.68 P 1,823.12 P 17,015.80 P 759.63 P 16,256.17 Feb. 1, 2009 to Jan. 31, 2010

P 15,192.68 P 1,823.12 P 17,015.80 P 759.63 P 16,256.17 Feb. 1, 2010 to Jan. 31, 2011

A. UPDATED LIST OF EXTENSION/PAYMENT OFFICES AND SECTOR LEASED BY MERALCO

AS OF DECEMBER 2010

Page 1 of 2

LESSOR OFFICE LOCATION AREA PRINCIPAL VAT BASIC EWT NET OF TAX LEASE TERM

A. UPDATED LIST OF EXTENSION/PAYMENT OFFICES AND SECTOR LEASED BY MERALCO

AS OF DECEMBER 2010

13 Ms. Virginia A. Casas San Jose Del Monte Extension KM. 30, Tungkong Mangga, San Jose Del Monte, Bulacan 97.00 P 32,680.80 P 3,921.70 P 36,602.50 P 1,634.04 P 34,968.46 Sept. 1, 2009 to Aug. 31, 2010

P 35,948.85 P 4,313.86 P 40,262.71 P 1,797.44 P 38,465.27 Sept. 1, 2010 to Aug. 31, 2011

14 Dr. Angelo P. Aquino Camarin Extension 2194 Zapote St., Camarin D. Kalookan City 148.00 P 70,785.00 P 8,494.20 P 79,279.20 P 3,539.25 P 75,739.95 Jan. 1, 2010 to Dec. 31, 2010

Franglo

15 Asian Cathay Finance & Leasing Meralco Consumer Assistance Unit 506, Pacific Center Condominium, San Miguel Avenue, 101.90 P 26,970.00 P 3,236.40 P 30,206.40 P 1,348.50 P 28,857.90 Oct. 12, 2009 to Oct. 15, 2010

Corporation Office - Condo unit & parking space San Antonio, Pasig City

Integral Realty Corporation Meralco Consumer Assistance Pacific Center Condominium, San Miguel Avenue, 12.00 P 2,500.00 P 300.00 P 2,800.00 P 125.00 P 2,675.00 Oct. 2, 2009 to Sept. 30, 2010

Office - Additional parking space San Antonio, Pasig City P 2,500.00 P 300.00 P 2,800.00 P 125.00 P 2,675.00 Oct. 2, 2010 to Sept. 30, 2011

B Alabang Sector (add'l area reqt.)

1 Greenfield Development Corp. Alabang Service Center Hilssborough Subd., Bgy. Cupang, Alabang, Muntinlupa City 721.00 P 27,037.50 P 3,244.50 P 30,282.00 P 1,351.88 P 28,930.13 Dec. 4, 2009 to Dec. 3, 2010

P 30,282.00 P 3,633.84 P 33,915.84 P 1,514.10 P 32,401.74 Dec. 4, 2010 to Dec. 3, 2011

Prepared by: Approved by: Noted by:

B. F. Arandela C. U. Dacanay G. R. Montemayor

Realty Staff Team Leader, Realty Head, Tax Management & Realty Services

Page 2 of 2

No. Due Date PAYEE PARTICULAR LOCATION AREA PRINCIPAL VAT BASIC EWT NET OF TAX COVERAGE REMARKS

1 Jan. 01, 2010 Atty. Emigdio Tanjuatco Tanay Substation Site Along National Road, Bo. Suyoc, 695.50 P 12,600.00 P 1,512.00 P 14,112.00 P 630.00 P 13,482.00 Jan. 01, 2010 to Dec. 31, 2010 Yearly

Tanay, Rizal P 13,230.00 P 1,587.60 P 14,817.60 P 661.50 P 14,156.10 Jan. 01, 2011 to Dec. 31, 2011

P 13,891.50 P 1,666.98 P 15,558.48 P 694.58 P 14,863.90 Jan. 01, 2012 to Dec. 31, 2012

P 14,586.08 P 1,750.33 P 16,336.41 P 729.30 P 15,607.11 Jan. 01, 2013 to Dec. 31, 2013

2 Jan. 15, 2010 City Government of Batangas Batangas City Substation Site Bo. Bolbok, Batangas City 1,400.00 P 42,000.00 P 0.00 P 42,000.00 P 0.00 P 42,000.00 Nov. 1, 2009 to Oct. 31, 2010 Yearly

-

Under Negotiation.

Pending advise from

Legal Office of

Batangas City

3 Jan. 31, 2010 Madrigal Business Park Commercial Ayala-Alabang Alabang, Muntinlupa City 2,400.00 P 118,800.00 P 0.00 P 118,800.00 P 0.00 P 118,800.00 Jan. 01, 2010 to Dec. 31, 2010

Estate Association, Inc Substation Site

Association Dues P 106,920.00 P 0.00 P 106,920.00 P 0.00 P 106,920.00 (net of 10% discount) Yearly

Common Area (P5.64 per sq. m.) P 13,536.00 P 0.00 P 13,536.00 P 0.00 P 13,536.00

4 Feb. 10, 2010 DENR-National Capital Region Binondo Substation Site Dasmariñas, Binondo, Manila 177.00 P 550.50 Feb. 9, 2009 to Feb. 8, 2010 Yearly

revocable permit Feb. 9, 2010 to Feb. 8, 2011

Application No.

V-4870 (E.V. 1651)

5 Feb. 15, 2010 Makati Commercial Estate Legaspi Substation Site Legazpi Village, Makati City 2,447.00 P 12,235.00 P 0.00 P 12,235.00 P 0.00 P 12,235.00 Jan. 1, 2010 to Dec. 31, 2010

Association, Incorporated (MACEA)

Association Dues P 11,011.50 P 0.00 P 11,011.50 P 0.00 P 11,011.50 (net of 10% Discount if paid Yearly

within the period Jan 1 to Mar. 31.)

6 May 01, 2010 University of the Philippines System IRRI - UP Los Baños National Highway, Brgy. Maahas, 2,500.00 P 2,196,150.00 P 0.00 P 2,196,150.00 P 0.00 P 2,196,150.00 May 3, 2009 - May 2, 2010 Yearly

Substation Site Los Baños, Laguna P 2,415,765.00 P 0.00 P 2,415,765.00 P 0.00 P 2,415,765.00 May 2, 2010 - May 2, 2011

7 Jun. 15, 2010 Philippine National Railways Tutuban Substation Site No. 943 C.M. Recto Ave., Tutuban 2,475.00 P 230,625.00 P 0.00 P 230,625.00 P 0.00 P 230,625.00 Jun. 15, 2009 to Jun. 14, 2010

Station, Tondo Manila P 124,921.88 P 0.00 P 124,921.88 P 0.00 P 124,921.88 Jun. 15, 2010 to Dec. 31, 2010

Level Crossing, Malolos, Bulacan Malolos, Bulacan 192.00 P 129,479.59 P 0.00 P 129,479.59 P 0.00 P 129,479.59 Jan. 1, 2010 to Dec. 31 2010 For finalization of

Lease Contract

B. UPDATED LIST OF LEASED SUBSTATION SITES

AS OF DECEMBER 2010

For finalization of

Lease Contract

1 of 2

No. Due Date PAYEE PARTICULAR LOCATION AREA PRINCIPAL VAT BASIC EWT NET OF TAX COVERAGE REMARKS

B. UPDATED LIST OF LEASED SUBSTATION SITES

AS OF DECEMBER 2010

Tondo Substation Tondo, Manila 1,250.00 P 1,668,194.52 P 0.00 P 1,668,194.52 P 0.00 P 1,668,194.52 Aug. 01, 2009 to Jul. 31, 2010

P 764,589.16 P 0.00 P 764,589.16 P 0.00 P 764,589.16 Aug. 01, 2010 to Dec. 31,2010

8 Jul. 10, 2010 DENR-National Capital Region Binondo Substation Site Dasmariñas, Binondo, Manila 506.00 -

Yearly, Renewal of

lease under

negotiation

9 University of Philippines Diliman Substation Site Diliman, Quezon City 7,984.00 - Aug. 11, 1993 - Aug. 10, 2023

(Usufruct for 30 years)

10 Manila International Airport Authority NAIA 3 Substation Site Villamor Air Base, Pasay City 1,831.00 P 62,169.77 P 7,460.37 P 69,630.14 P 3,108.49 P 66,521.65 Feb. 1, 2009 to Jan. 31, 2010 Monthly

P 62,169.77 P 7,460.37 P 69,630.14 P 3,108.49 P 66,521.65 Feb. 1, 2010 to Jan. 31, 2011

11 VCGT Realty Corporation Manggahan Substation Site Manggahan, Pasig City 2,816.26 P 175,762.78 P 21,091.53 P 196,854.31 P 8,788.14 P 188,066.17 Jul. 01, 2009 to Jun. 30, 2010 Monthly

P 188,942.88 P 22,673.15 P 211,616.03 P 9,447.14 P 202,168.88 Jul. 01, 2010 to Jun. 30, 2011

P 203,108.67 P 24,373.04 P 227,481.71 P 10,155.43 P 217,326.28 Jul. 01, 2011 to Jun. 30, 2012

P 218,344.63 P 26,201.36 P 244,545.99 P 10,917.23 P 233,628.75 Jul. 01, 2012 to Jun. 30, 2013

P 234,707.10 P 28,164.85 P 262,871.95 P 11,735.36 P 251,136.60 Jul. 01, 2013 to Jun. 30, 2014

P 252,308.73 P 30,277.05 P 282,585.78 P 12,615.44 P 269,970.34 Jul. 01, 2014 to Jun. 30, 2015

P 271,234.00 P 32,548.08 P 303,782.08 P 13,561.70 P 290,220.38 Jul. 01, 2015 to Jun. 30, 2016

Prepared by: Approved by: Noted by:

B. F. Arandela C. U. Dacanay G. R. Montemayor

Realty Staff Team Leader, Realty Head, Tax Management & Realty Services

For finalization of

Lease Contract

2 of 2

No. PAYEE PARTICULAR LOCATION AREA RENTAL PRINCIPAL VAT BASIC EWT NET OF TAX COVERAGE REMARKS

1 Aquilana Pedraja BTL - R/W at Junction, Cainta, Rizal Junction, Cainta, Rizal P 6,600.00 P 6,600.00 P 0.00 P 6,600.00 P 0.00 P 6,600.00 Jan. 01, 2010 - Dec. 31, 2010 Yearly

Tax Exempt

2 Office of the Non-Fund Permit Fee of 115 KV P 8,500.00 P 8,500.00 P 0.00 P 8,500.00 P 0.00 P 8,500.00 Feb. 8, 2009 - Feb. 7, 2010 Yearly

HHSG, PA, Fort Bonifacio Transmission Line (Rockwell/Malibay) P 8,500.00 P 8,500.00 P 0.00 P 8,500.00 P 0.00 P 8,500.00 Feb. 8, 2010 - Feb. 7, 2011

3 Camilo D. Briones Mt. Banoy Repeater Station Site Brgy. Talumpok Silangan, Batangas City121.00 P 106,989.47 P 106,989.47 P 0.00 P 106,989.47 P 5,349.47 P 101,640.00 Sept. 1, 2009 - Aug. 31, 2010 Yearly

Net of 5% EWT P 106,989.47 P 0.00 P 106,989.47 P 5,349.47 P 101,640.00 Sept. 1, 2010 - Aug. 31, 2011

(P8,470.00/month)

4 Marbe De Torres Contreras, et. Al. Mt. Banahaw Repeater Station Site Samil, Lucban, Quezon 197.00 P 96,049.80 P 96,049.80 P 0.00 P 96,049.80 P 4,802.49 P 91,247.31 Sept. 1, 2009 - Aug. 31, 2010 Yearly

Non VAT Registered P 105,654.78 P 0.00 P 105,654.78 P 5,282.74 P 100,372.04 Sept. 1, 2010 - Aug. 31, 2011

5 Sps. Danilo G. Reyes and Sariaya Repeater Site Mamala, Sariaya, Quezon 500.00 P 216,000.00 P 216,000.00 P 0.00 P 216,000.00 P 10,800.00 P 205,200.00 Dec. 1, 2009 - Nov. 30, 2010 Yearly

Melinda P. Reyes Bo. Mamala - 2 Non VAT Registered P 234,000.00 P 0.00 P 228,000.00 P 11,700.00 P 216,300.00 Dec. 1, 2010 - Nov. 30, 2011

P 252,000.00 P 0.00 P 240,000.00 P 12,600.00 P 227,400.00 Dec. 1, 2011 - Nov. 30, 2012

P 270,000.00 P 0.00 P 252,000.00 P 13,500.00 P 238,500.00 Dec. 1, 2012 - Nov. 30, 2013

P 288,000.00 P 0.00 P 264,000.00 P 14,400.00 P 249,600.00 Dec. 1, 2013 - Nov. 30, 2014

P 306,000.00 P 0.00 P 276,000.00 P 15,300.00 P 260,700.00 Dec. 1, 2014 - Nov. 30, 2015

P 324,000.00 P 0.00 P 288,000.00 P 16,200.00 P 271,800.00 Dec. 1, 2015 - Nov. 30, 2016

P 342,000.00 P 0.00 P 300,000.00 P 17,100.00 P 282,900.00 Dec. 1, 2016 - Nov. 30, 2017

P 360,000.00 P 0.00 P 312,000.00 P 18,000.00 P 294,000.00 Dec. 1, 2017 - Nov. 30, 2018

6 Bayan Telecoms, Incorporated Mt. Landing Repeater Station Site Jala Jala, Rizal P 12,000.00 P 10,714.29 P 1,285.71 P 12,000.00 P 535.71 P 11,464.29 Sept. 1, 2009 to August 31, 2010 Monthly

Sept. 1, 2010 to August 31, 2011

7 Hospicio De San Jose 2 Steel Towers & 2 Steel Poles R/W Isla de Convalescencia, Manila 1,812.00 P 69,200.00 P 61,785.71 P 7,414.29 P 69,200.00 P 3,089.29 P 66,110.71 June 1, 2005 to June 30, 2023 Monthly

plus donation (VAT inclusive)

Fixed rate

Prepared by: Approved by: Noted by:

B. F. Arandela C. U. Dacanay G. R. Montemayor

Realty Staff Team Leader, Realty Head, Tax Management & Realty Services

C. UPDATED LIST OF LEASED REPEATER STATION SITES AND TOWER/TRANSMISSION LINES R/W

AS OF DECEMBER 2010

T.C.T. AREA IN

NO. SQ. MTR.

Botocan Transmission Lines (110 KV) Santol Street- E. Rodriguez Sr. Blvd. Route 46811 24,493

E. Rodriguez Sr. Blvd. - San Juan River Route 35913 42,919

San Juan River - Katipunan Ave. Route 46812 219,07635915 54,250

273,326

Katipunan Ave. - Marikina River Route 35915 36,40546813 11,074

47,479

Bgy. Sucat, Muntinlupa City S-79863 3,975Gardner Transmission Line Right of Way

Bgy. Camarin, Caloocan CityTransmission Right of Way 22310 2,713

Ibayo-Napindan, Taguig, Metro Manila OCT-691 215Ibayo-Napindan Transmission Right-of-Way

Sta. Mesa, Manila to Marikina City tract of land

Sta. Ana, Manila to Junction, Pasig City tract of land

Bgy. Botocan, Majayjay, Laguna T-92138 10,391Site I - Substation SiteBOTOCAN SUBSTATION

Bgy. Botocan, Majayjay, Laguna T-43563 18,909Site II - Trans. Right of Way O-1431 4,741Between Botocan & Balanas Liners 23,650

Bgy. Suyok (Kay Buto) Tanay, Rizal M-81342 337Tanay Transmission Line Right-of-Way

LOCATION/DESCRIPTION

MANILA ELECTRIC COMPANY

SUMMARY OF LAND AND LAND RIGHTS - UTILITY

AS OF DECEMBER 31, 2010

Page 1 of 16

T.C.T. AREA IN

NO. SQ. MTR.LOCATION/DESCRIPTION

Bgy. May-Iba, Antipolo City, Rizal 26774 1,170Antipolo Transmission Line Right-of-Way 399524 1,050

2,220

Kaayusan cor. Kaluwagan St. (PT-84312) 86541 591.20Karangalan Village, Santolan, Pasig city (PT-84313) 86542 1,133.20Botocan 115KV Line (Meralco Tower) 1,724.40

San Guillermo, Morong, Rizal no tct yet 573

Bgy. Dolores, Taytay, Rizal 699325 4,372

9th Ave., cor Sevilla St. cor D. Aquino St., (14962) 11001 1,300Caloocan CityGRACE PARK SUBSTATION

A. Flores St., Ermita, Manila 48429 1,639ERMITA SUBSTATION

J. Rizal Street, Bgy. Pamplona, Las Piñas City S-79858 2,082LAS PIÑAS SUBSTATION

Bgy. Ibayo, Las Piñas City 47102 740ZAPOTE SUBSTATION T-78492 711

T-47095 34243647/S-78299 467

T-105438 1952,455

Sta. Cecilla Road, Sitio Kubo-Kob, Bgy. Pamplona 40739 7,915Mapulang Lupa, Las Piñas CityPAMPLONA SUBSTATION

McKinley Road, Forbes Park, Makati City 64899 1,000FORBES PARK SUBSTATION

Vito Cruz cor Kakarong Street, Makati City S-51742 1,791MAKATI SUBSTATION

Kamagong St. cor Ayala Ave. Ext., Makati City S-77241 1,378KAMAGONG SUBSTATION

Page 2 of 16

T.C.T. AREA IN

NO. SQ. MTR.LOCATION/DESCRIPTION

Amorsolo St. cor Lumbang St., Kayamanan C S-79682 4,900Subdivision, Makati City S-51743 2,096MALIBAY SUBSTATION 6,996

L. Guinto St. cor Dagonoy St., Malate, Manila 22048 369.20MALATE SUBSTATION 22049 1,029.70

1,398.90

M. H. Del Pilar, L Roque, Bgy. Tugatog, T-94885 7,476Provincial Road, Malabon CityMALABON SUBSTATION

Bgy. Camarin, Caloocan City C-322885 8,962CAMARIN SUBSTATION C-322886 152

9,114

EDSA, Bgy. Wack-Wack, Mandaluyong City 12100 1,264MANDALUYONG SUBSTATION (Wack-Wack) 12097 769

2,033

EDSA SHOEMART-SHANGRI-LA, Mandaluyong City 9152 604SM - SHANGRILA SUBSTATION 11368 500

1,104

From Miriam College to Bgy Malanday, Marikina City N-39141 2,137Marikina (A.C. 34.5 Feederline) N-46245 958

N-38764 3,1976,292

East Drive, Santan St., Marikina Heights, N-30467 5,050Bgy. Parang, Marikina CityPARANG SUBSTATION

Kapitan Moy Street, Sta. Elena, Marikina City N-30471 894MELI SUBSTATION

Katipunan Ave., Loyola Heights, Quezon City 46813 3,463MARIKINA SUBSTATION

Madrigal Business Park, Phase 3, T-210119 2,400Bgy. Alabang, Muntinlupa CityAYALA-ALABANG SUBSTATION/BUSINESS CENTER

Page 3 of 16

T.C.T. AREA IN

NO. SQ. MTR.LOCATION/DESCRIPTION

Plaza Dilao, Paco, Manila (61536) 240564 1,034.40PACO SUBSTATION (137786) 240519 209.90

(180640) 240517 209.70(137785) 240920 209.80(137784) 240515 342.30(137783) 240921 422.60(180641) 240518 250.00

(196644) 240514 896.60

(69456) 240513 245.60

(152094) 240922 784.10

(152095) 240923 1,142.20

(152096) 240924 1,112.50

(152097) 240925 164.50

7,024.20

Isla de Provisor, D. Romualdez St., Paco, Manila 146850 10,891.30TEGEN SUBSTATION

Quirino Ave., Bgy. Tambo, Parañaque City S-79855 1,157PARAÑAQUE SUBSTATION

Sun Valley Subd., Bgy. La Huerta, Parañaque City S-79859 1,612.50SUN VALLEY SUBSTATION T-44095 583.00

2,195.50

Sta. Cecilia St., Bgy. San Dionisio, T-120937 6,898Parañaque CityB. F. PARAÑAQUE SUBSTATION

S. Antonio Avenue/ Pilapil Sts., Bgy. Kapasigan, 12098 1,450Pasig City -41550PASIG SUBSTATION

Elisco Road, Kalawaan Sur, Taguig, Metro Manila 308397 5,021(Inside National Steel Corp. Compound)TAGUIG SUBSTATION

Canley Road cor Orambo Drive, Bgy. Bagong PT-105095 198.50Ilog, Pasig City PT-105096 320.00HILLCREST SUBSTATION PT-105097 217.00

PT-105098 347.50PT-105094 227.00

1,310.00

Page 4 of 16

T.C.T. AREA IN

NO. SQ. MTR.LOCATION/DESCRIPTION

EDSA, San Roque near BLTB Terminal, Pasay City 4385 2,500PASAY SUBSTATION

P. Tuazon St., Gen. Romulo, Cubao, Quezon City 33825 1,970CUBAO SUBSTATION

Along Banawe Ave. cor Del Monte Avenue, RT-53270(30108) 792.20Quezon City RT-53270(30108) 600.00LA LOMA SUBSTATION 1,392.20

Quirino Hi-way, Novaliches, Quezon City 63451 7,677NOVALICHES SUBSTATION

P. dela Cruz St., Bgy. San Bartolome, N-136291 3,704Novaliches, Quezon CityKAYBIGA SUBSTATION

Scout Santiago Rallos St., Diliman, Quezon City 17720 797.20QUEZON CITY SUBSTATION 17721 784.70

1,581.90

A. H. Lacson St. (formerly Gov. Forbes St.) 28895 375Sampaloc, Manila 28215 1,000SAMPALOC SUBSTATION 1,375

N. Domingo St., San Juan, Metro Manila 42264 1,334SAN JUAN SUBSTATION

Santol Street, Bgy. San Isidro, Quezon City 46811 10,569.00STA. MESA SUBSTATION 107627 16.50