04 and 05 capacity and smt 9115 2011.ppt

DESCRIPTION

Capacity resources and business cycles. SMT, Inc. caseTRANSCRIPT

1

ESTIMATING AND MANAGING COSTS AND REVENUES

1 and 2. Information systems: theory and practice. How and why to estimate costs?

3. Information systems and process complexity. Seligram case.

4 and 5. Capacity resources and business cycles. SMT, Inc. case.

6 and 7. Activity-based costing. Coffee Services mini-case.

8. Midterm.

9 and 10. Estimating and managing customer profitability. Infinity Bank case.

TACTICAL AND STRATEGIC DECISIONS

2

Capacity Management

Capacity has a cost, whether it is used or not

3

Capacity

• Capacity is the maximum output or producing ability of a machine, person, factory, etc.

• Capacity can be measured in physical terms

– Measure of the amount of work done

– Capacity is the measure of the maximum amount of work that can be done in a given time

4

Capacity

• Capacity = R * T

– R is the rate of output per unit of time

– T is the maximum amount of time available

• Capacity has a cost

– Cost to acquire or rent the facility, machine, operating costs, wages, utilities, insurance, etc.

– The cost is incurred even if capacity is underused

5

Measuring the Cost of Capacity

• Traditional measures do not reflect the cost of capacity usage or over capacity

– Costs are part of overhead and allocated to production

• Focus is on inventory valuation, not managing capacity

• Allocation base is chosen from five alternatives

–Theoretical

»Maximum output when operating continuously at maximum efficiency

6

Measuring the Cost of Capacity

– Practical

» Level of output under current conditions, allowing for normal downtime for setups, maintenance, vacations, etc.

– Normal

» Average level of output achieved or anticipated over several years

– Budget

» Level of output anticipated for the current year

– Actual

» Level of output actually achieved in the current year

7

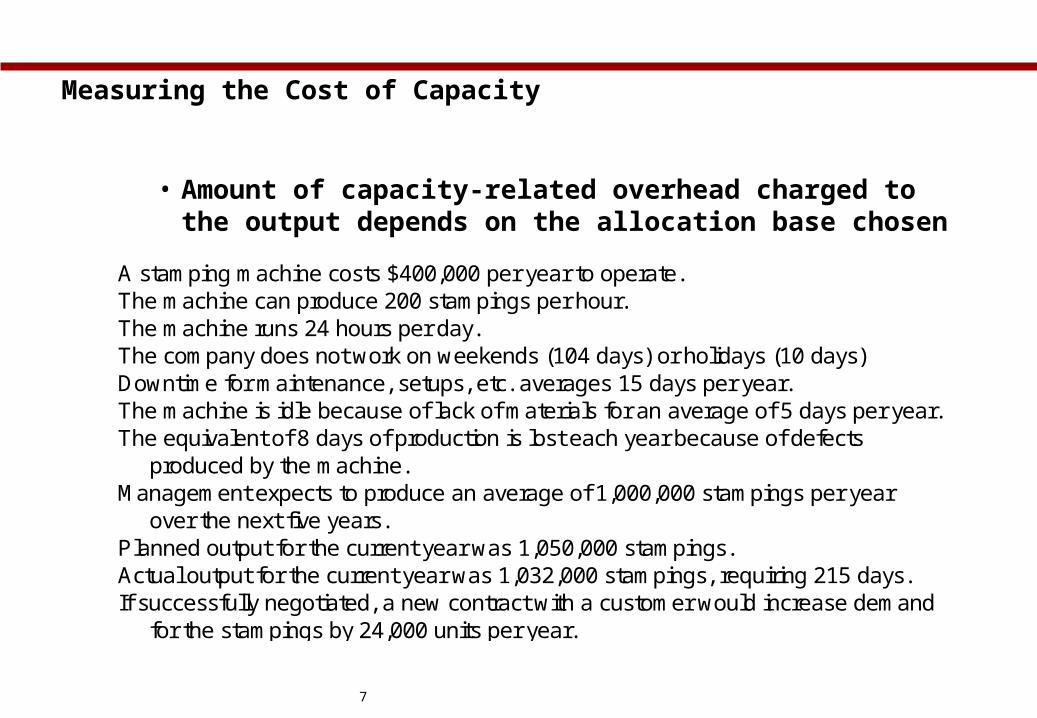

Measuring the Cost of Capacity

• Amount of capacity-related overhead charged to the output depends on the allocation base chosen

A stamping machine costs $400,000 per year to operate.The machine can produce 200 stampings per hour.The machine runs 24 hours per day.The company does not work on weekends (104 days) or holidays (10 days)Downtime for maintenance, setups, etc. averages 15 days per year.The machine is idle because of lack of materials for an average of 5 days per year.The equivalent of 8 days of production is lost each year because of defects produced by the machine.Management expects to produce an average of 1,000,000 stampings per year over the next five years.Planned output for the current year was 1,050,000 stampings.Actual output for the current year was 1,032,000 stampings, requiring 215 days.If successfully negotiated, a new contract with a customer would increase demand for the stampings by 24,000 units per year.

8

Measuring the Cost of Capacity

Traditional cost allocation measures

OutputOperating

costCost per

unitTheoretical capacityUnits per hour 200 Hours per day * 24 Days per year * 365 Theoretical capacity = 1,752,000 $400,000 $0.228

Practical capacityUnits per hour 200 Hours per day * 24 Operating days per year* * 231 Practical capacity = 1,108,800 $400,000 $0.361* 365-104-10-15-5=231 days

Normal capacityExpected 5 year average output 1,000,000 $400,000 $0.400

Budget capacityPlanned output for the current year 1,050,000 $400,000 $0.381

Actual capacityActual output for the current year 1,032,000 $400,000 $0.388

9

Traditional Cost AccountingTraditional Cost Accounting

The predetermined The predetermined overhead rate is based overhead rate is based on budgeted activity. on budgeted activity.

This results in applying This results in applying overhead costs of overhead costs of

unused, or idle, unused, or idle, capacity.capacity.

Traditional Cost AccountingTraditional Cost Accounting

The predetermined The predetermined overhead rate is based overhead rate is based on budgeted activity. on budgeted activity.

This results in applying This results in applying overhead costs of overhead costs of

unused, or idle, unused, or idle, capacity.capacity.

Activity BasedActivity BasedCostingCosting

Products are charged for Products are charged for the costs of capacity the costs of capacity they use – not for the they use – not for the costs of capacity they costs of capacity they

don’t use.don’t use.

Activity BasedActivity BasedCostingCosting

Products are charged for Products are charged for the costs of capacity the costs of capacity they use – not for the they use – not for the costs of capacity they costs of capacity they

don’t use.don’t use.

Cost of Idle Capacity

10

Difference Between ABC and Traditional Product Costs

Batch-level or product-Batch-level or product-level costs will level costs will

ordinarily shift overhead ordinarily shift overhead costs from high-volume costs from high-volume products produced in products produced in large batches to low-large batches to low-

volume products volume products produced in small produced in small

batches. batches.

Batch-level or product-Batch-level or product-level costs will level costs will

ordinarily shift overhead ordinarily shift overhead costs from high-volume costs from high-volume products produced in products produced in large batches to low-large batches to low-

volume products volume products produced in small produced in small

batches. batches.

Under ABC both Under ABC both manufacturing and manufacturing and nonmanufacturing nonmanufacturing

costs may be assigned costs may be assigned to products. to products.

Organization-sustaining Organization-sustaining costs and the costs of costs and the costs of idle capacity are not idle capacity are not

assigned to products.assigned to products.

Under ABC both Under ABC both manufacturing and manufacturing and nonmanufacturing nonmanufacturing

costs may be assigned costs may be assigned to products. to products.

Organization-sustaining Organization-sustaining costs and the costs of costs and the costs of idle capacity are not idle capacity are not

assigned to products.assigned to products.

11

Capacity

• Capacity can be expressed in several

ways, including:

Total labor hours.

Total machine hours.

Total units of output.

12

Alternative Denominator-Level Concepts

Theoretical capacity

Practical capacity

Normal capacity

Master-budget capacity

13

Capacity

» Theoretical Capacity: Maximum productive output possible over a given period of time.

» Practical capacity: Theoretical capacity reduced by normal, expected work stoppages.

» Normal capacity: Average annual operating capacity needed to satisfy expected sales demand.

» Master-budget capacity: the expected level of capacity utilization for the current budget period

» Excess Capacity: Extra machinery and equipment available when regular facilities are being repaired or when expected volume is greater.

14

Budgeted Fixed ManufacturingOverhead Rate

Lloyd’s Bicycles produces bicycle partsfor domestic and foreign markets.

Fixed overhead costs are $200,000 within therelevant range of the various capacity volume.

15

Budgeted Fixed ManufacturingOverhead Rate

Assume that the theoretical capacity is10,000 machine-hours, practical capacity

is 85%, normal capacity is 75%, andmaster-budget capacity is 60%.

What is the budgeted fixed manufacturingoverhead rate at the various capacity levels?

16

Budgeted Fixed ManufacturingOverhead Rate

Theoretical 100%:$200,000 ÷ 10,000 = $20.00/machine-hour

Practical 85%:$200,000 ÷ 8,500 = $23.53/machine-hour

Normal 75%:$200,000 ÷ 7,500 = $26.67/machine-hour

Master-budget 60%:$200,000 ÷ 6,000 = $33.33/machine-hour

17

Choosing a capacity level

Understand the major factorsmanagement considers in choosing

a capacity level to compute thebudgeted fixed overhead cost rate.

18

Choosing a Capacity Level

What factors are consideredin choosing a capacity level?

Productcosting

Pricingdecision

Performanceevaluation

Financialstatements

Regulatoryrequirements

Difficulty

19

Decision Making

Assume that Lloyd’s Bicycles’ standardhours are 2 hours per unit.

What is the budgeted fixed manufacturingoverhead cost per unit?

20

Decision Making

Theoretical capacity: $20 × 2 = $40.00

Practical capacity: $23.53 × 2 = $47.06

Normal capacity: $26.67 × 2 = $53.34

Master-budget capacity: $33.33 × 2 = $66.66

21

Explain how the capacitylevel chosen to calculate

the budgeted fixed overheadcost rate affects the

production-volume variance.

22

Effect on Financial Statements

Assume that Lloyd’s Bicycles actually used8,400 machine-hours during the year.

What is the production volume variance?

23

Production Volume Variance

Production volume variance= (Denominator level – Actual level)

× Budgeted fixed manufacturing overhead rate

Theoretical capacity:(10,000 – 8,400) × $20.00 = $32,000 U

Practical capacity:(8,500 – 8,400) × $23.53 = $2,353 U

24

Production Volume Variance

Normal capacity:(7,500 – 8,400) × $26.67 = $24,003

Master-budget capacity:(6,000 – 8,400) × $33.33 = $79,992

25

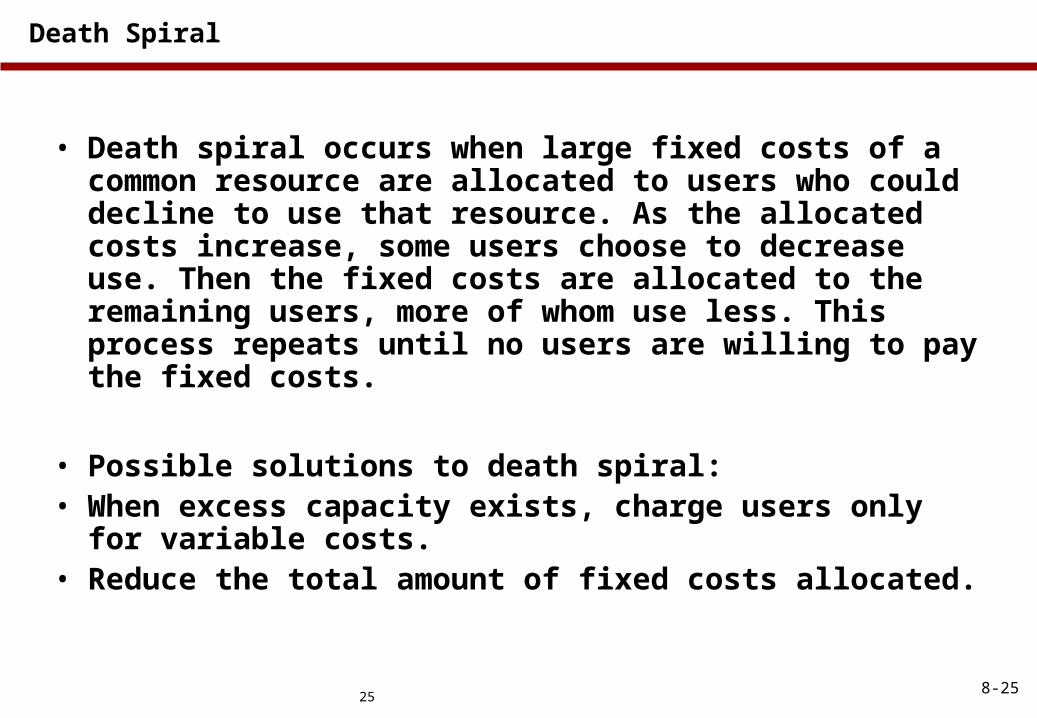

Death Spiral

• Death spiral occurs when large fixed costs of a common resource are allocated to users who could decline to use that resource. As the allocated costs increase, some users choose to decrease use. Then the fixed costs are allocated to the remaining users, more of whom use less. This process repeats until no users are willing to pay the fixed costs.

• Possible solutions to death spiral:• When excess capacity exists, charge users only for

variable costs.• Reduce the total amount of fixed costs allocated.

8-25

26

Death Spiral Example: Internal Services

• Internal Telecommunications Department:• Telecommunications service department allocates fixed costs to

users. • If some users are allowed to switch to outside phone company, the

fixed costs allocated to remaining users increase.• Eventually, the number of users of the telecommunications

department is so small that the department is closed.

8-26

27

Death Spiral Example: Cost-based Contracts

• Military Aircraft (not in text):• Defense contractors working on advanced

technology incur large fixed cost over-runs that are allocated to each aircraft manufactured.

• Government reduces number of aircraft purchased and that causes average cost to increase on remaining orders.

• Government responds by ordering even fewer aircraft.

• Eventually, the entire project is abandoned before all fixed costs are recovered.

8-27

28

Death Spiral in Reverse!

• Clay Sprays:• Increasing the allocation base for fixed costs can

lead to misleading product line profit figures.• Decisions should be consistent with an overall

economic strategy and a meaningful understanding of the impacts of accounting practices.

• “I left this to the accountants” would not cut it in today’s business environment.

8-28

29

Illustration of decision-making pitfall:

consequence of normal absorption costing;

particularly dangerous in cyclical industries.

Intro to measuring and managing capacity resources:

for decision support;

to generate signals for management attention.

One solution: practical capacity approaches.

PRIMARY CASE-STUDY OBJECTIVES

30

1997 1998 1999 2000 2001

Budgeted line 6 OH (000s) 2 512$ 2 520$ 2 696$ 2 678$ 2 768$ Expected line 6 MHs 4 380 7 008 7 183 5 256 3 504

OH Rate/MH 574$ 360$ 375$ 510$ 790$

Sunnyvale Line 6 Annual OH Rates

SMT OH RATES – Sunnyvale Line 6

31

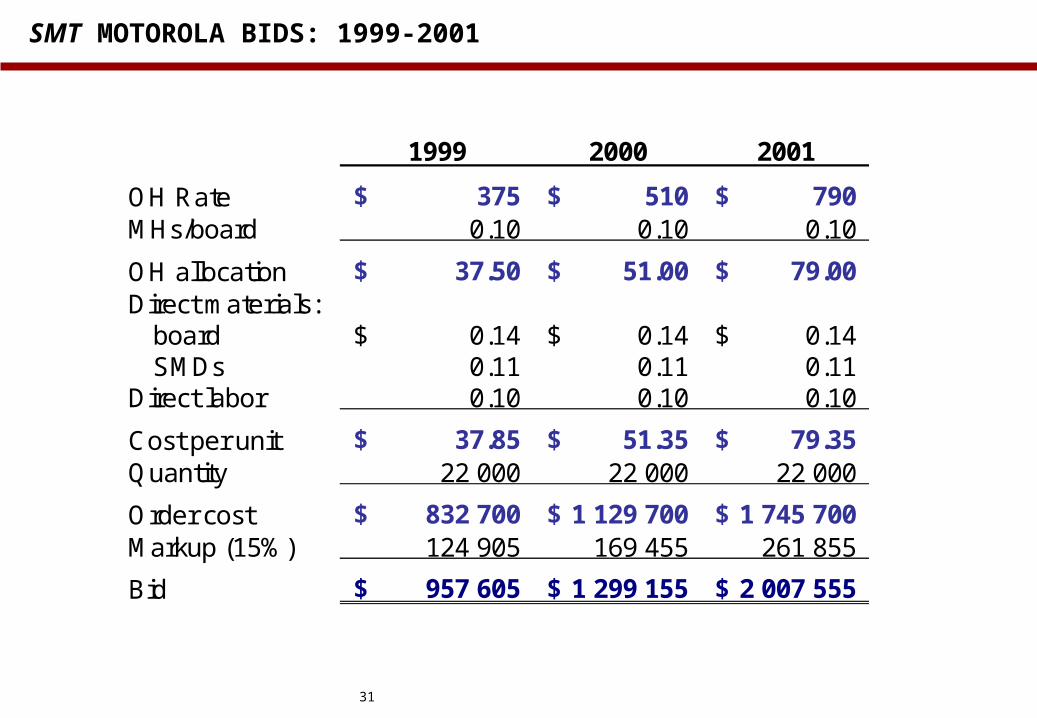

1999 2000 2001

OH Rate 375$ 510$ 790$ MHs/board 0.10 0.10 0.10

OH allocation 37.50$ 51.00$ 79.00$ Direct materials: board 0.14$ 0.14$ 0.14$ SMDs 0.11 0.11 0.11

Direct labor 0.10 0.10 0.10

Cost per unit 37.85$ 51.35$ 79.35$ Quantity 22 000 22 000 22 000

Order cost 832 700$ 1 129 700$ 1 745 700$ Markup (15%) 124 905 169 455 261 855

Bid 957 605$ 1 299 155$ 2 007 555$

SMT MOTOROLA BIDS: 1999-2001

32

Selling price = $107. Annual volume about 10 000.

Materials content $1.32. Labor $0.31.

Processing requirements 0.2 MHs / unit.

Profitability of this contract from 1999 - 2001?

PROJECT HP-HDC-32

33

1999 2000 2001

MHs per unit 0.2 0.2 0.2OH Rate 375$ 510$ 790$

OH allocation 75$ 102$ 158$ DM 1.32 1.32 1.32DL 0.31 0.31 0.31

Product cost 77$ 104$ 160$

Price 107$ 107$ 107$

Profit/unit 30$ 3$ (53)$

Annual volume 10 000 10 000 10 000

Annual profit 303 700$ 33 700$ (526 300)$

Annual revenues 1 070 000$ 1 070 000$ 1 070 000$

PROJECT HP-HDC-32

SALES VOLUMES

MACRO, INDUSTRY,COMPETITION, OTHERREASONS

OH RATES

REPORTED PRODUCTCOSTS

OH COSTS DO NOT

DECREASEAS FAST

AS VOLUMES

PRICES ?

CUT

PRODUCTS?

34

35

€0

€2,000,000

€4,000,000

€6,000,000

€8,000,000

€10,000,000

€12,000,000

200

400

600

800

1,00

01,

200

1,40

01,

600

1,80

02,

000

UNITS

Current operations

EXAMPLE

36

EXAMPLE

2,000 Units Forecast.

€ 10,000,000 / 2,000 = € 5,000 Cost Per Unit

Competitor enters our market; we lose 700 units, expect 1,300 units next year. 1,300 Units Forecast.

€ 10,000,000 / 1,300 = € 7,692 Cost Per Unit

Problems?

EXAMPLE: OVERHEAD ESTIMATION USING PRACTICAL CAPACITY —

€ 5,000 COST PER UNIT REGARDLESS OF EXPECTED PRODUCTION

37

€0

€2,000,000

€4,000,000

€6,000,000

€8,000,000

€10,000,000

€12,000,000

200

400

600

800

1,00

01,

200

1,40

01,

600

1,80

02,

000

UNITS

€0

€2,000,000

€4,000,000

€6,000,000

€8,000,000

€10,000,000

€12,000,000

200

400

600

800

1,00

01,

200

1,40

01,

600

1,80

02,

000

UNITS

€ 6.5 Million

USEDcapacity

€ 3.5 Million

EXCESScapacity

EXAMPLE: OVERHEAD ESTIMATION USING PRACTICAL CAPACITY —

€ 5,000 COST PER UNIT; 1,300 UNITS FORECAST

38

39

SMT: OH RATES WITH PRACTICAL CAPACITY

1997 1998 1999 2000 2001

Line 6 overhead 2,512,000$ 2,520,000$ 2,696,000$ 2,678,000$ 2,768,000$ Practical capacity (MHs) 7,066 7,014 7,186 6,986 7,256

OH Rate / MH $356 $359 $375 $383 $381

40

1999 2000 2001

OH Rate 375$ 383$ 381$ MHs/board 0.10 0.10 0.10

OH allocation 37.50$ 38.30$ 38.10$ Direct materials: board 0.14$ 0.14$ 0.14$ SMDs 0.11 0.11 0.11

Direct labor 0.10 0.10 0.10

Cost per unit 37.85$ 38.65$ 38.45$ Quantity 22 000 22 000 22 000

Order cost 832 700$ 850 300$ 845 900$ Markup (15%) 124 905 127 545 126 885

Bid 957 605$ 977 845$ 972 785$

Motorola bid MOT-F-23

BIDS WITH PRACTICAL CAPACITY RATES

41

EXCESS CAPACITY REPORTS

1997 1998 1999 2000 2001

Good production 4 380 7 008 7 183 5 256 3 504 Practical capacity 7 066 7 014 7 186 6 986 7 256

Utilization % 62% 100% 100% 75% 48%

Excess capacity:Machine hours 2 686 6 3 1 730 3 752 Rate 356$ 359$ 375$ 383$ 381$

Excess capacity 956 216$ 2 154$ 1 125$ 662 590$ 1 429 512$

Sunnyvale Line 6 Capacity Analysis (Forecasts)

42

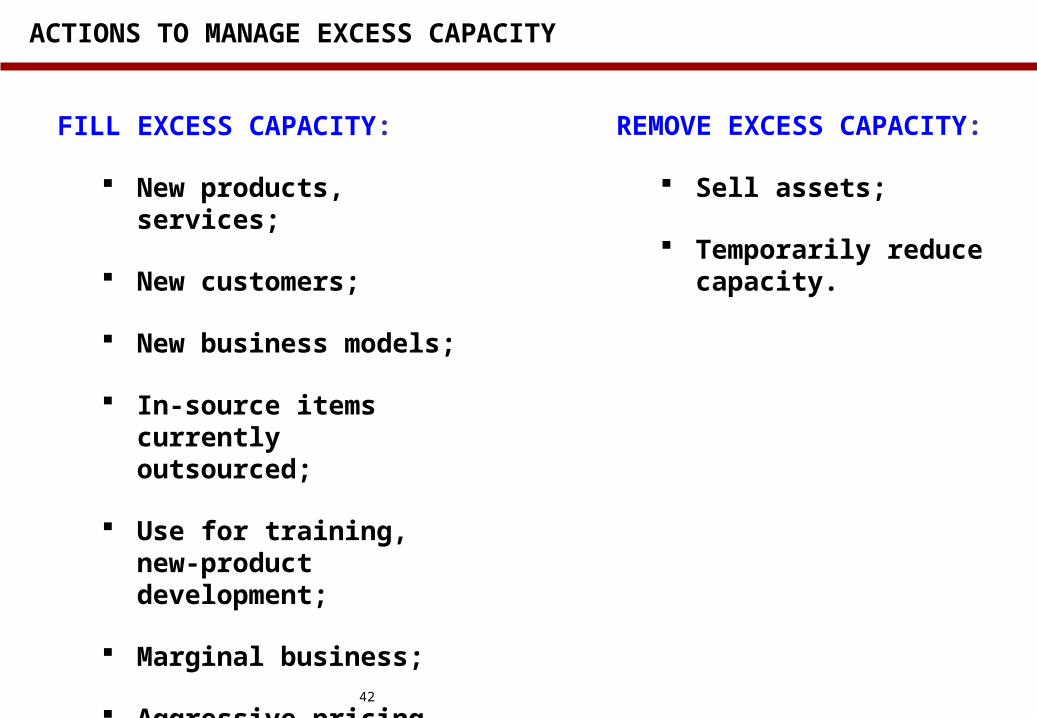

REMOVE EXCESS CAPACITY:

Sell assets;

Temporarily reduce capacity.

ACTIONS TO MANAGE EXCESS CAPACITY

FILL EXCESS CAPACITY:

New products, services;

New customers;

New business models;

In-source items currently outsourced;

Use for training, new-product development;

Marginal business;

Aggressive pricing.

43

PRACTICAL CAPACITY ADVANTAGES

1. Avoids the “death spiral”;

2. Generates signals about our capacity utilization;

3. Avoids wild fluctuations in OH costs;

4. Products do not incorporate the cost of our inefficient capacity utilization.

Remaining problem – still doesn’t tell us:

i. why we have excess capacity;

ii. how to determine the right level of excess capacity;

iii. how to get to that level.

44

Standard OH allocation techniques introduce a common decision pitfall when industry or macroeconomic conditions change.

The death spiral is a dangerous consequence of relying on budgeted capacity utilization to allocate costs.

Practical capacity is a solution to the death-spiral problem.

In addition, practical capacity approaches generate valuable signals about underutilized capacity.

KEY TAKEAWAYS – SMT