03/11/2013lawrence henze | target analytics 1 exploring the top of the gift pyramid: principal...

TRANSCRIPT

03/11/2013 Lawrence Henze | Target Analytics 1

EXPLORING THE TOP OF THE GIFT PYRAMID: PRINCIPAL GIV ING PROSPECT ATTRIBUTESPresented By:

Lawrence C. Henze, J.D.

Principal Consultant

Founder

03/11/2013 Lawrence Henze | Target Analytics 2

PRINCIPAL GIVING – APEX OF YOUR PYRAMID

Annual

Major

Mid

Principal / Lead $250K-$1M+

03/11/2013 Lawrence Henze | Target Analytics 3

• Principal• Lead• Transformational• Inspirational• Ultimate• High-End Planned Giving?

DIFFERENT TERMS, SAME CONCEPT OF GIVING

03/11/2013 Lawrence Henze | Target Analytics 4

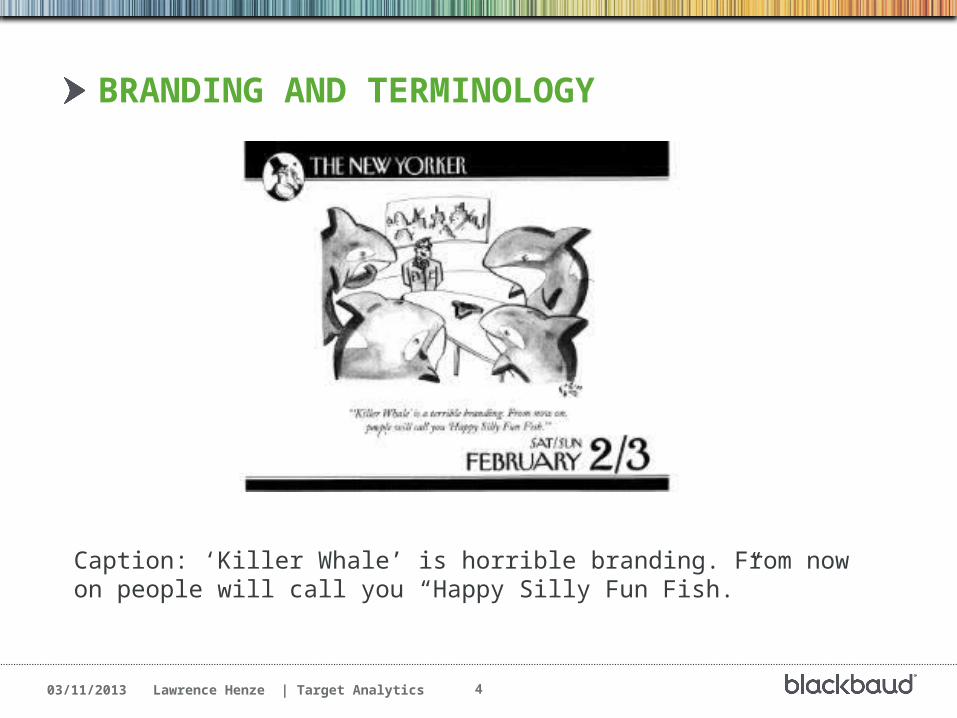

BRANDING AND TERMINOLOGY

Caption: ‘Killer Whale’ is horrible branding. From now on people will call you “Happy Silly Fun Fish.”

03/11/2013 Lawrence Henze | Target Analytics 5

WHAT SHAPE IS YOUR PYRAMID? THIS IS A WORTHWHILE EXERCISE

03/11/2013 Lawrence Henze | Target Analytics 6

TRADITIONAL DONOR PYRAMID

03/11/2013 Lawrence Henze | Target Analytics 7

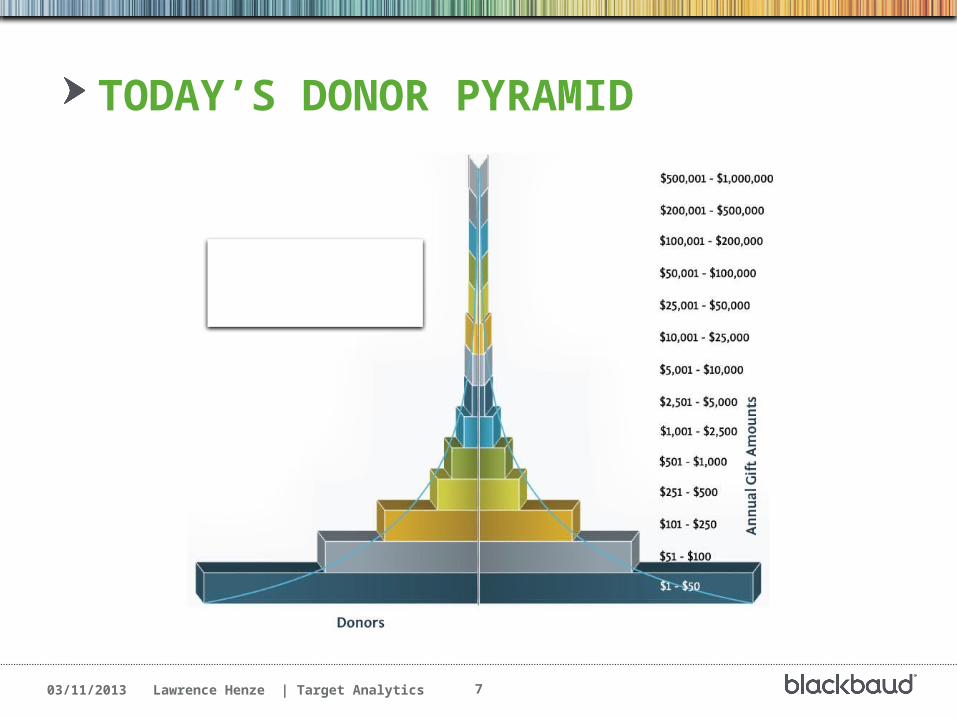

TODAY’S DONOR PYRAMID

03/11/2013 Lawrence Henze | Target Analytics 8

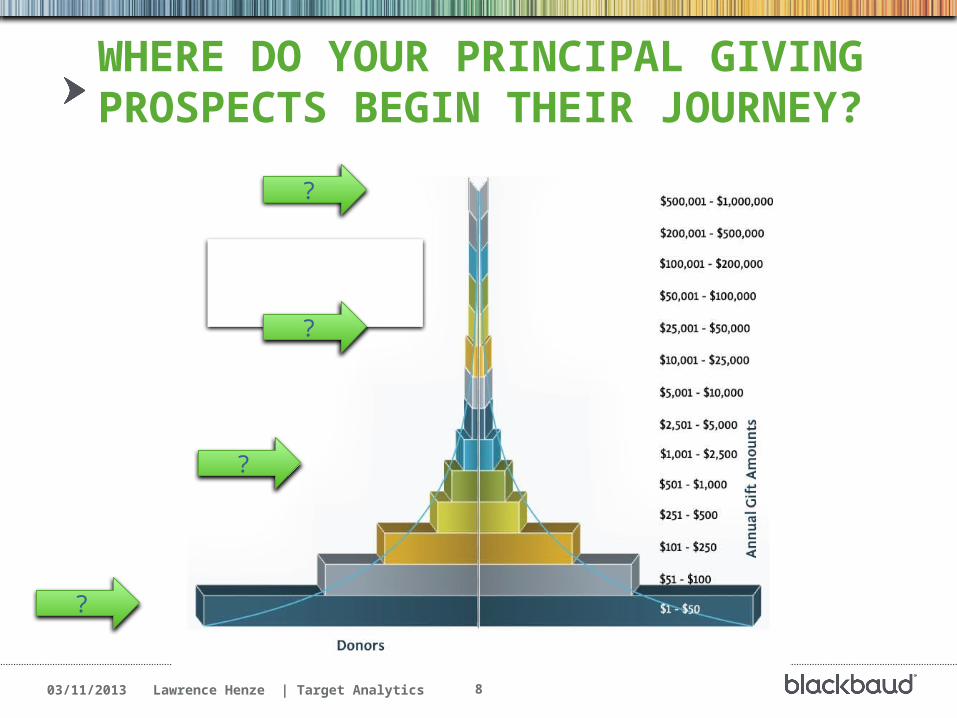

WHERE DO YOUR PRINCIPAL GIVING PROSPECTS BEGIN THEIR JOURNEY?

?

?

?

?

03/11/2013 Lawrence Henze | Target Analytics 9

IDENTIFYING PRINCIPAL GIFT PROSPECTS: BEST PRACTICES

Past Behavior

Predictive Modeling

Wealth Screening Research Field

Qualification

03/11/2013 Lawrence Henze | Target Analytics 10

PRINCIPAL GIVING RESEARCH – MODELING AND WEALTH ANALYSIS

Your Database

Wealth AnalysisAnalysis of hard assets for

complete assessment of donors and prospects

Propriety Models for Inclination and Capacity

Developed by examining over 150 organizations and

100M gift transactions

Giving History Analysis

Examination of the trends and

patterns of giving in your

house file

Principal Giving Pool

$250K prospect

Naming opportunity $1M+

prospect

03/11/2013 Lawrence Henze | Target Analytics 11

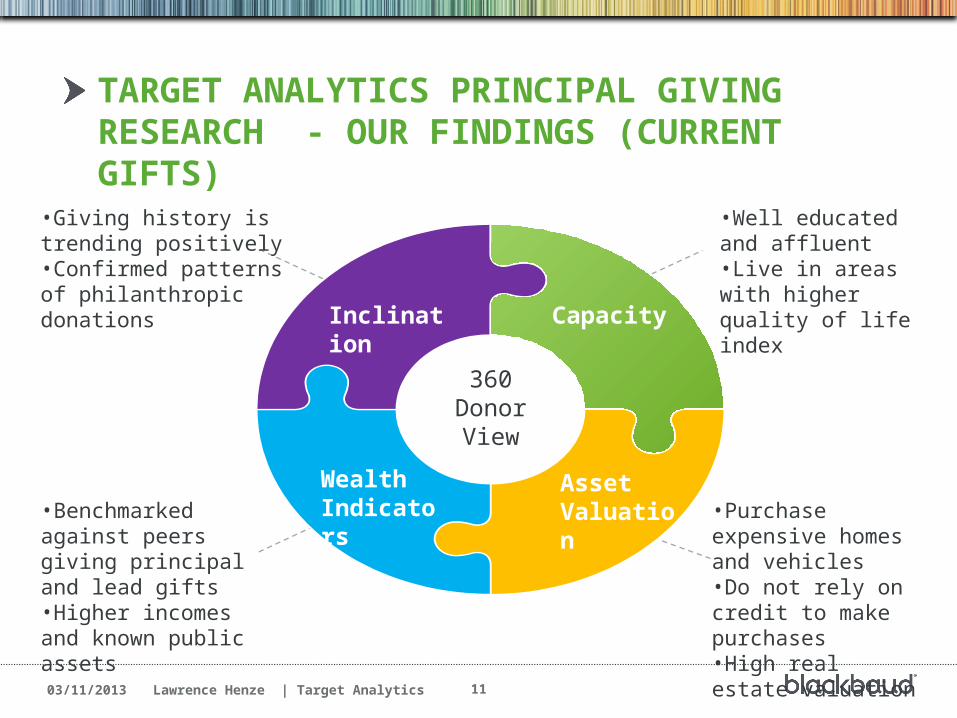

TARGET ANALYTICS PRINCIPAL GIVING RESEARCH - OUR FINDINGS (CURRENT GIFTS)

360 Donor View

•Giving history is trending positively•Confirmed patterns of philanthropic donations

•Well educated and affluent•Live in areas with higher quality of life index

•Benchmarked against peers giving principal and lead gifts•Higher incomes and known public assets

•Purchase expensive homes and vehicles•Do not rely on credit to make purchases•High real estate valuation

Inclination

WealthIndicators

Capacity

Asset Valuation

03/11/2013 Lawrence Henze | Target Analytics 12

E X P L ORING H IGH NE TW ORT H P HIL ANT HROP Y

03/11/2013 Lawrence Henze | Target Analytics 13

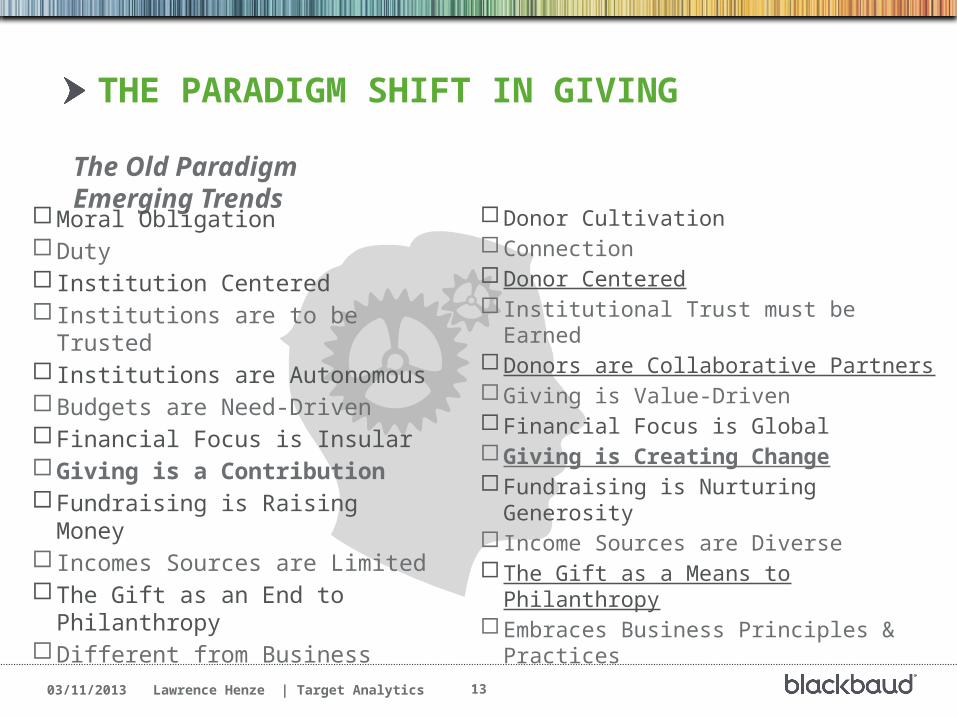

THE PARADIGM SHIFT IN GIVING

The Old Paradigm Emerging Trends

Moral Obligation Duty Institution Centered Institutions are to be Trusted Institutions are Autonomous Budgets are Need-Driven Financial Focus is Insular Giving is a Contribution Fundraising is Raising Money Incomes Sources are Limited The Gift as an End to

Philanthropy Different from Business

Donor Cultivation Connection Donor Centered Institutional Trust must be Earned Donors are Collaborative Partners Giving is Value-Driven Financial Focus is Global Giving is Creating Change Fundraising is Nurturing Generosity Income Sources are Diverse The Gift as a Means to Philanthropy Embraces Business Principles &

Practices

03/11/2013 Lawrence Henze | Target Analytics 14

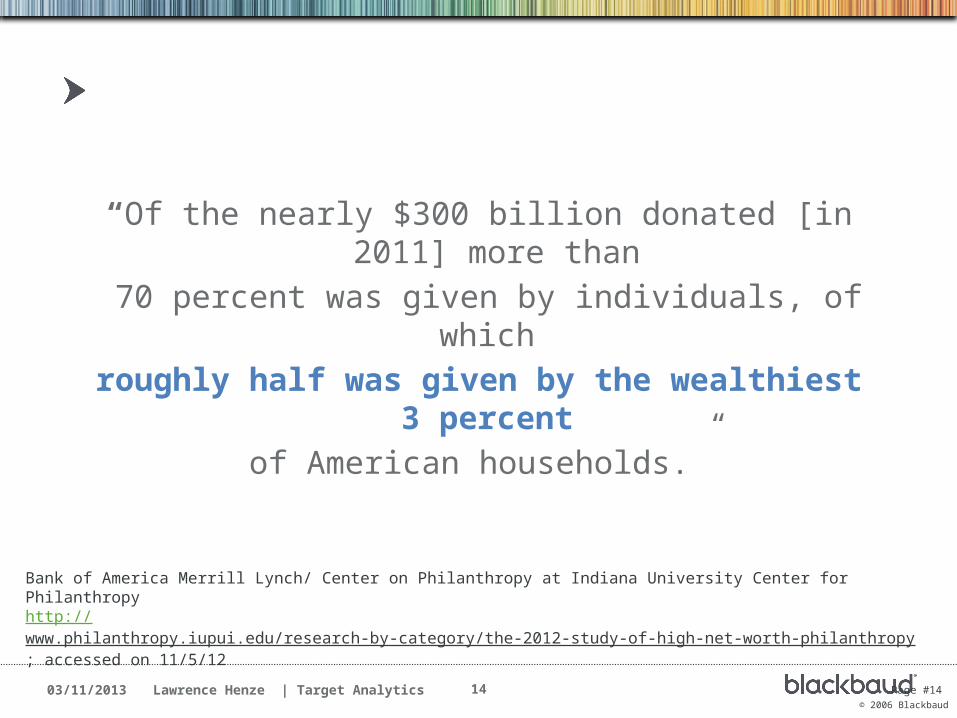

“Of the nearly $300 billion donated [in 2011] more than

70 percent was given by individuals, of which

roughly half was given by the wealthiest 3 percent

of American households.”

Page #14© 2006 Blackbaud

Bank of America Merrill Lynch/ Center on Philanthropy at Indiana University Center for Philanthropy http://www.philanthropy.iupui.edu/research-by-category/the-2012-study-of-high-net-worth-philanthropy ; accessed on 11/5/12

03/11/2013 Lawrence Henze | Target Analytics 15

• Financial industry term used to group individuals and families with investible assets are $30 million or more

• Major giving capacity for this population is at least $1.5 million

• On average they own 8 cars, 4 homes and over three-fourths of this group own a plane and/or a yacht

ULTRA HIGH NET WORTH INDIVIDUALS

03/11/2013 Lawrence Henze | Target Analytics 16

• Estimate there are currently 103,000 Ultra HNWI worldwide

- Population grew by 10.2% in 2010 and wealth grew by 11.5%

- Ultra HNWI in the U.S. have a combined wealth of $6.4 trillion dollars

• Most banks, financial institutions and luxury brands have divisions dedicated solely to this population

ULTRA HIGH NET WORTH INDIVIDUALS

03/11/2013 Lawrence Henze | Target Analytics 17

• Annual household income of $200,000+ and/or household net worth of $1 million+ (excluding the value of primary residence)

• 95.4% gave to non-profit organizations in 2011- Compares to 65% of the entire US Population

• Donate an average of 8.4% and a median of 3.1% of household income- This is less than 2007 and 2009 responses- Over the next 3-5 years, about half plan to keep their contributions

the same and about a quarter plan to increase contribution levels

• Correlation between volunteering and giving- The more an individual volunteered, the more they gave

• Nearly 50% make philanthropic decisions with their spouse/partner and 33% involve children in their giving

HIGH NET WORTH INDIVIDUALS

03/11/2013 Lawrence Henze | Target Analytics 18

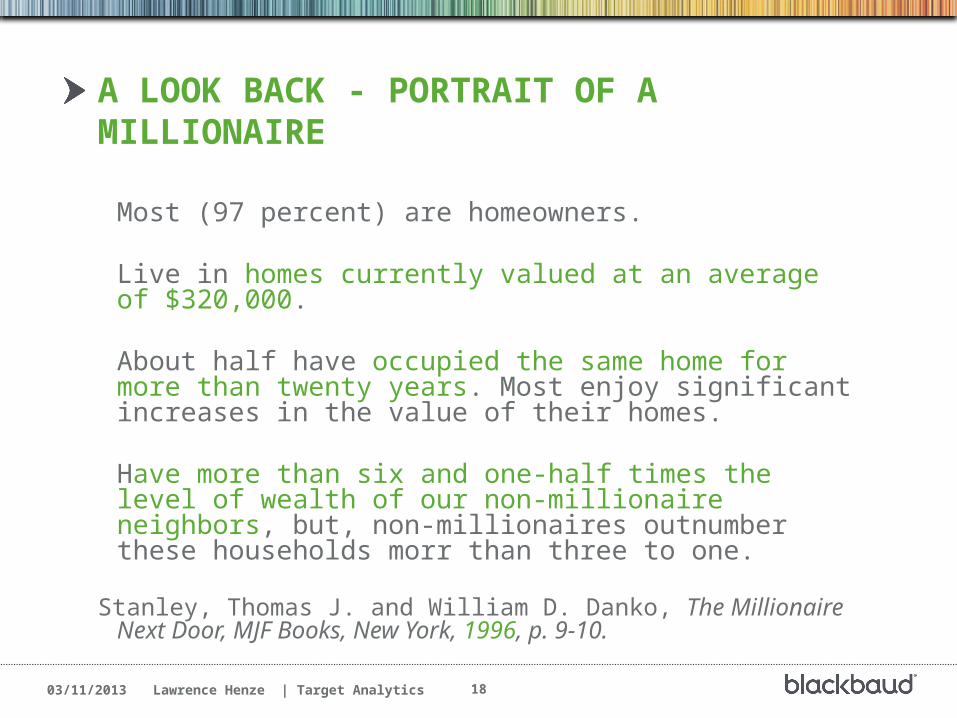

A LOOK BACK - PORTRAIT OF A MILLIONAIRE

Most (97 percent) are homeowners.

Live in homes currently valued at an average of $320,000.

About half have occupied the same home for more than twenty years. Most enjoy significant increases in the value of their homes.

Have more than six and one-half times the level of wealth of our non-millionaire neighbors, but, non-millionaires outnumber these households morr than three to one.

Stanley, Thomas J. and William D. Danko, The Millionaire Next Door, MJF Books, New York, 1996, p. 9-10.

03/11/2013 Lawrence Henze | Target Analytics 19

• A bequest is a provision in your will or trust to pass money to a charitable organization upon your death. - Typical clauses include an outright amount, a percentage of the

assets, or the residual of the estate

• Wills are often the first estate planning tool• Charitable bequests are easy to talk about and understand • Two primary age groups: late 40s to late 50s, and mid 60s to late

70s• About 75% of wills are never changed

- Only 1%-3% of charitable bequests are ever revoked

• More than two-thirds of planned gift donors also make current annual gifts- Research confirms planned gift donors are significantly

more philanthropic than non-planned gift donors

PRIMER ON PLANNED GIFT VEHICLES – BEQUESTS

03/11/2013 Lawrence Henze | Target Analytics 20

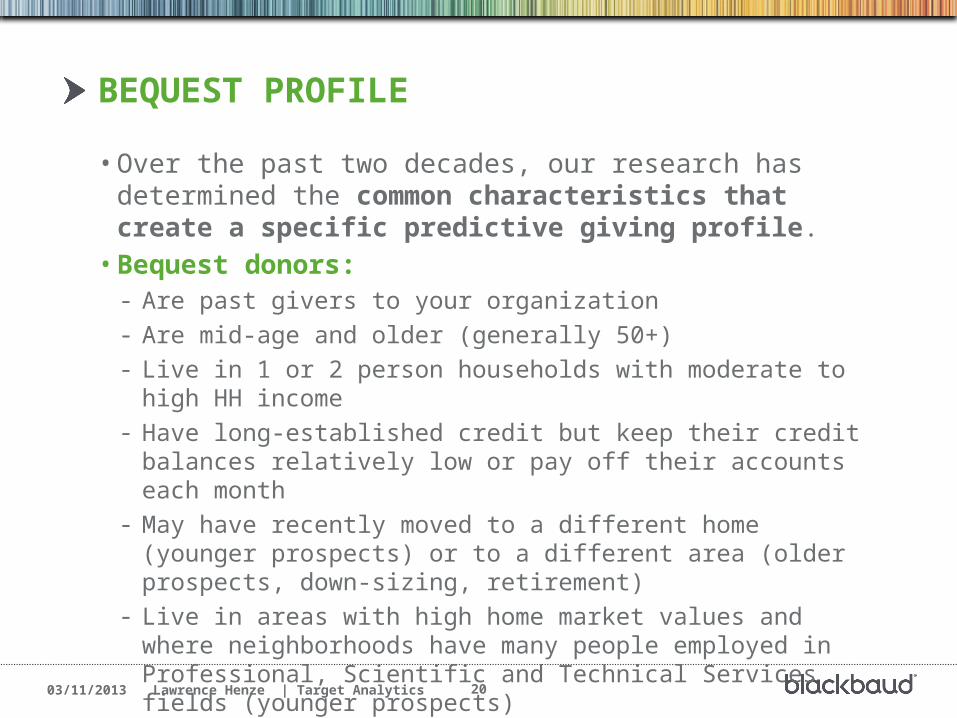

• Over the past two decades, our research has determined the common characteristics that create a specific predictive giving profile.

• Bequest donors:- Are past givers to your organization- Are mid-age and older (generally 50+)- Live in 1 or 2 person households with moderate to high HH income- Have long-established credit but keep their credit balances relatively

low or pay off their accounts each month- May have recently moved to a different home (younger prospects)

or to a different area (older prospects, down-sizing, retirement)- Live in areas with high home market values and where

neighborhoods have many people employed in Professional, Scientific and Technical Services fields (younger prospects)

BEQUEST PROFILE

03/11/2013 Lawrence Henze | Target Analytics 21

• Bequests- Established home ownership- Children in college or evidence of college-related debt- Charitable gifts to other organizations (lower gift amounts)- Volunteerism- Other types of loyalty factors

• Membership• Ticket buying• Monthly contributor• Board, committee participation• Long-term event participation

RESEARCH COMPONENTS

03/11/2013 Lawrence Henze | Target Analytics 22

PRIMER ON PLANNED GIFT VEHICLES - CGAS

• A charitable gift annuity (CGA) is a contract between one or two donors and your organization. In exchange for making a gift to your organization, you promise to pay the donor(s) a fixed amount regularly for life- Although part of the annuity payments are taxable, the donor(s) also

receives an upfront charitable income tax deduction for the amount of the original gift that is estimated to remain at the donor’s/donors’ death

• 5%-6% of all planned gifts are CGAs- Next most common planned gift vehicle in U.S.

• Primary age group is mid 70s and older• Annuities can range from a little as $5,000 to over $1,000,000• Over 4 in 5 annuitants learned about gift annuities through the

organization’s own marketing and promotion• Many, if not most gift annuitants do multiple annuities

03/11/2013 Lawrence Henze | Target Analytics 23

• Over the past two decades our research has determined the common characteristics that create a specific predictive giving profile.

• Annuity donors:- Tend be some of our oldest planned gift donors (70+)- Exhibit consistent giving behavior to your organization- May have recently moved to a different home or to a different area

(high value senior living communities for example)- Continue to enjoy high incomes (better off than they believe)- Are fiscally conservative individuals who are afraid to carry ongoing

debt- Use credit for convenience and pay off the debt immediately

ANNUITANT PROFILE

03/11/2013 Lawrence Henze | Target Analytics 24

RESEARCH COMPONENTS

• Charitable Gift Annuities- Evidence of retired status- Marital Status: single, widowed or divorced- Annual giving at the $100 level or less

• Ticket buying• Membership• Connection to your organization

- Charitably inclined• Giving to multiple organizations (member of legacy society)

- Evidence of stock holdings, retirement plans or commercial annuities• Current or former business ownership

- No evidence of children or grandchildren• The fewer children and grandchildren, higher average gift

03/11/2013 Lawrence Henze | Target Analytics 25

PRIMER ON PLANNED GIFT VEHICLES - CRTS

• A charitable remainder trust is an irrevocable financial holding set up to move liquid or illiquid assets out of an individual’s possession into a giving vehicle with charitable intent. The trust pays a specified annual amount to one or more people for a fixed number of years, or for the life of the individual(s) who benefit from the trust’s distributions- At the end of the term, the remaining trust property is distributed to

your organization and any other specified charities• 1%-2% of all planned gifts are CRTs

- Third most common planned gift vehicle in the U.S.• Primary age group is mid 50s through early 70s• CRTs are useful for changing real estate, business assets and other

relatively illiquid assets • Many CRT holders make charitable bequests as well

03/11/2013 Lawrence Henze | Target Analytics 26

• Over the past two decades, our research has determined the common characteristics that create a specific predictive giving profile.

• CRT donors:- Are committed donors to your organization with consecutive year

gifts- Are approaching or just passed retirement age (ages 55-70)- Enjoy high incomes and keep their credit account balances at

low or modest levels- Many are actually retired; those still working tend to cluster in

high income or entrepreneurial occupations such as Management, Professional Technical and Sales positions

• These prospects are likely to have one spouse that is retired or does not work outside the home

CHARITABLE REMAINDER TRUST PROFILE

03/11/2013 Lawrence Henze | Target Analytics 27

RESEARCH COMPONENTS

• Charitable Remainder Trusts- Evidence of wealth- Evidence of major giving- Multiple property ownership- Charitably inclined

• Board membership- Evidence of stock holdings, retirement plans

• Former business ownership

03/11/2013 Lawrence Henze | Target Analytics 28

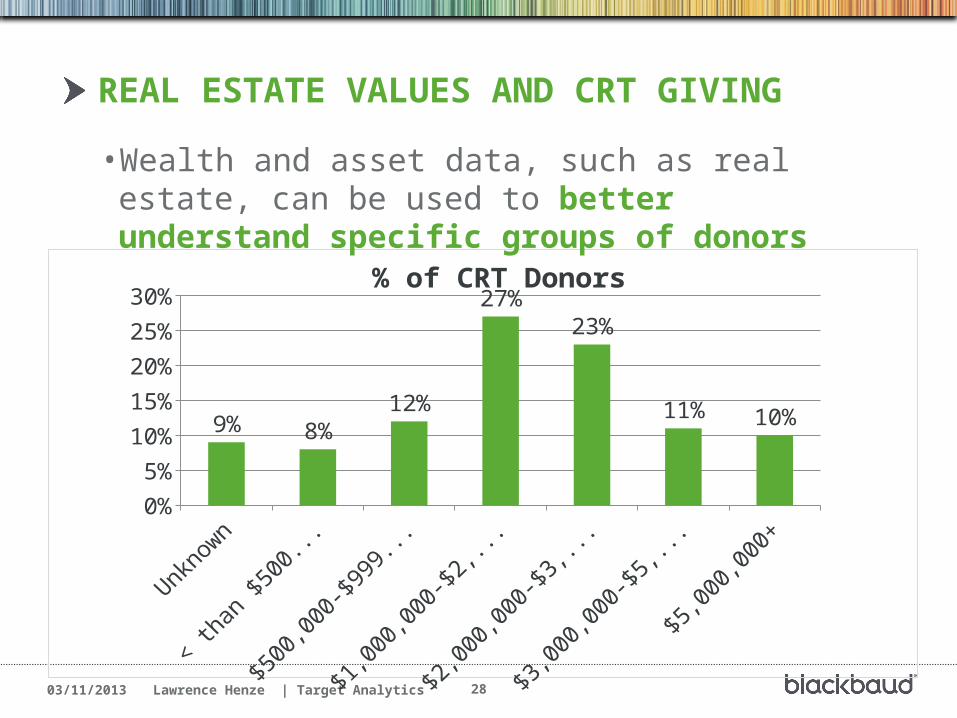

0%

5%

10%

15%

20%

25%

30%

9% 8%12%

27%23%

11% 10%

% of CRT Donors

REAL ESTATE VALUES AND CRT GIVING

• Wealth and asset data, such as real estate, can be used to better understand specific groups of donors

03/11/2013 Lawrence Henze | Target Analytics 29

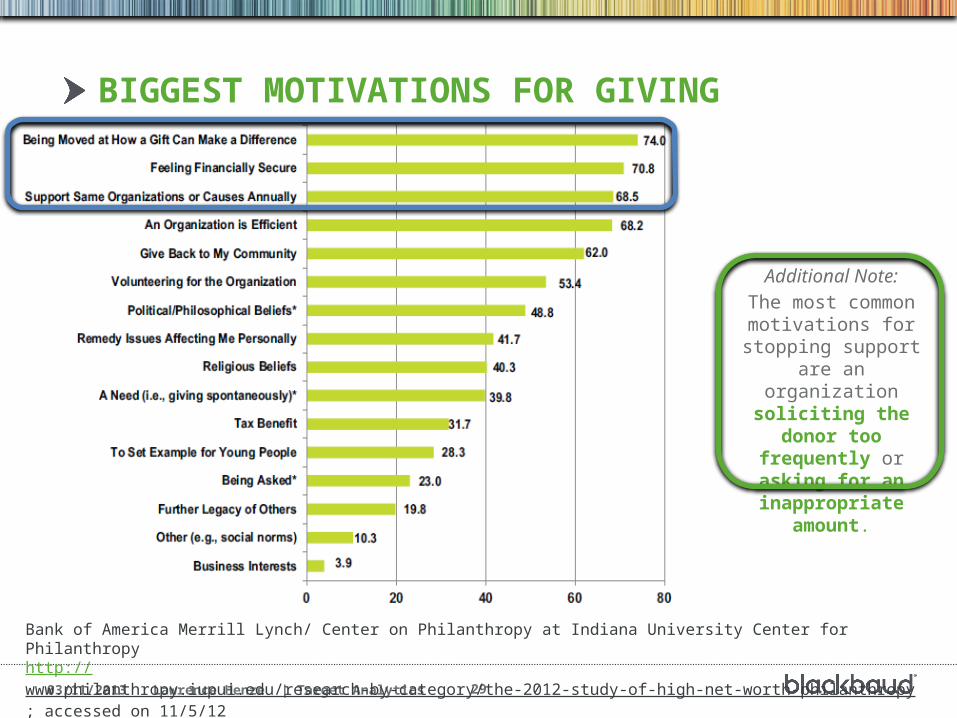

Additional Note:

The most common motivations for stopping

support are an organization soliciting

the donor too frequently or asking for

an inappropriate amount.

BIGGEST MOTIVATIONS FOR GIVING

Bank of America Merrill Lynch/ Center on Philanthropy at Indiana University Center for Philanthropy http://www.philanthropy.iupui.edu/research-by-category/the-2012-study-of-high-net-worth-philanthropy ; accessed on 11/5/12

03/11/2013 Lawrence Henze | Target Analytics 30

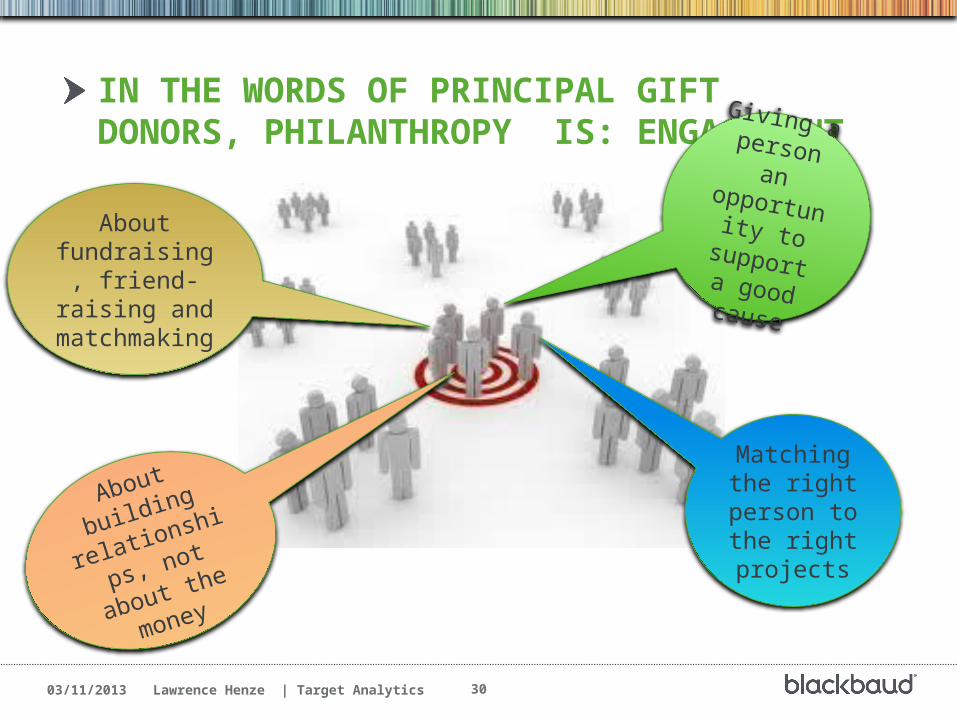

IN THE WORDS OF PRINCIPAL GIFT DONORS, PHILANTHROPY IS: ENGAGEMENT

Giving a person an opportunity to support a good cause

Matching the right

person to the right projects

About building

relationships,

not about the

money

About fundraising,

friend-raising and

matchmaking

03/11/2013 Lawrence Henze | Target Analytics 31

P OS IT IONING Y OURORGANIZ AT ION F OR S UCCE S SIDENT IF ICAT ION

03/11/2013 Lawrence Henze | Target Analytics 32

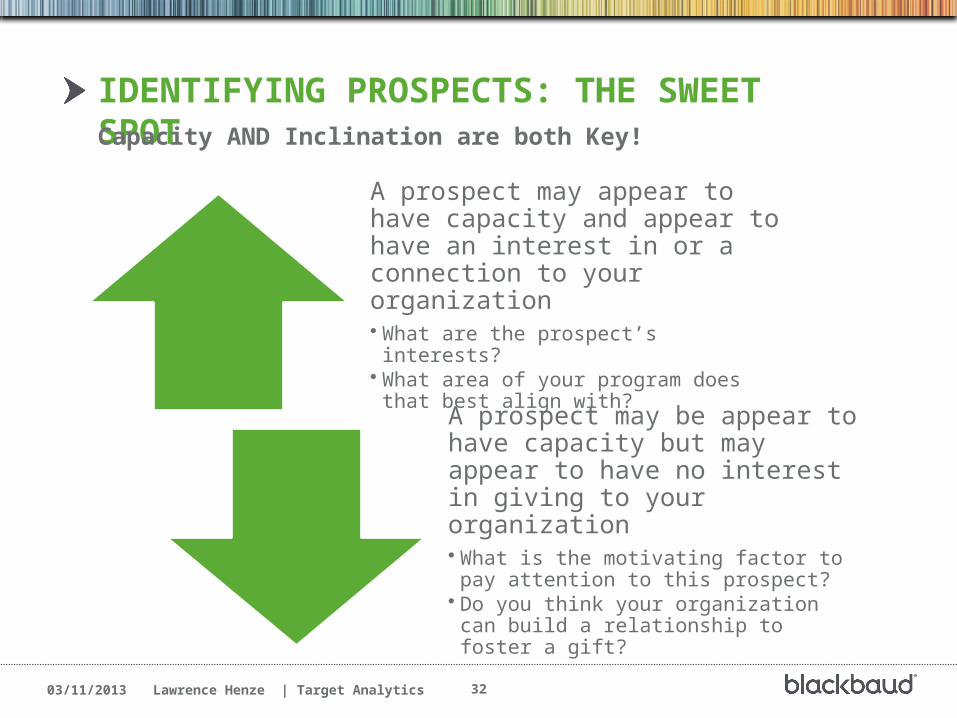

IDENTIFYING PROSPECTS: THE SWEET SPOT

A prospect may appear to have capacity and appear to have an interest in or a connection to your organization• What are the prospect’s interests?• What area of your program does that best

align with?

A prospect may be appear to have capacity but may appear to have no interest in giving to your organization• What is the motivating factor to pay attention

to this prospect?• Do you think your organization can build a

relationship to foster a gift?

Capacity AND Inclination are both Key!

03/11/2013 Lawrence Henze | Target Analytics 33

OBSTACLES TO PROSPECT DEVELOPMENT: THE SILO APPROACH

Annual giving

Donor relations

CRM

Shadow database

Membership

Special events

Major giving

Planned giving

Prospect Research

Prospects

03/11/2013 Lawrence Henze | Target Analytics 34

• Contact me:

Lawrence Henze, J.D., Principal ConsultantBased in Walnut Creek, CA_______________________________________________________ Target Analytics, a division of Blackbaud, Inc. 1981 Robin Ridge CourtWalnut Creek, CA 94597Blackbaud cell: 843-991-9921

White Papers: http://www.blackbaud.com/company/resources/whitepapers/whitepapers.aspx

QUESTIONS

03/11/2013 Lawrence Henze | Target Analytics 35

WHY I PREFER ‘LAWRENCE’