02.05.2014, investing in excellence: golomt bank, munkhbat davaatseren

TRANSCRIPT

INVESTING IN EXCELLENCE: GOLOMT BANK

MUNKHBAT Davaatseren, CEO of Golomt Securities LLC

April 30th, 2014

London

YOUR PARTNER IN MONGOLIA

www.golomtbank.com

www.golomtsecurities.com

MONGOLIA

“Mongolia has a globally unparalleled young population and a wealth of resources, and has potential for unlimited growth.”

-Shinzo Abe, Prime Minister of Japan, March 2013

ABUNDANT UNEXPLOITED natural resources located close to some of the LARGEST commodity

MARKETS

VAST LAND 1

$12.2 bn 11.7% $4,164

GDP Growth GDP/Capita Nominal GDP

Relatively YOUNG POPULATION with a HIGH LITERACY rate among emerging economies YOUNG

POPULATION

2

NATURAL

RESOURCES

3

SUCCESSFULLY implemented 7 CONSECUTIVE ELECTIONS, with significantly improving

TRANSPARENCY

FLOURISHING

DEMOCRACY

4

LARGEST land per capita, with mostly UNTAPPED 1.5 MILLION square kilometers of beautiful landscape

2

Land of Growth

One of the fastest growing economies globally

Large mineral resource base that can be leveraged for business growth

High demand from neighboring markets

Attractive environment for FDI and trade

Strengthening financial sector

4.6 6.2

8.8 10.3

12.2

16.0

18.9

23.7

0

5

10

15

20

25

2009 2010 2011 2012 2013 2014F 2015F 2016F

USD bln

3

Source: National Statistics Office of Mongolia, International Monetary Fund

GDP Growth

12.5%

9.2%

12.1%

4.6%

8.0%

9.5%

5.5%

3.4% 3.1%

11.7%

5.0%

6.3% 5.2% 5.1%

6.4%

1.5%

6.6%

7.80%

Mon

golia

Vie

tnam

Nig

eria

Bol

ivia

Ukr

aine

Sri

Lank

a

Leba

non

Phi

lippi

nes

Chi

na

YoY Inflation Real GDP Growth

GDP growth rate VS Inflation

-1.3%

6.4%

17.5%

12.3% 11.7% 12.9%

7.7% 8.8%

7.7%

9.7%

7.9% 6.7% 6.5% 6.7%

6.8% 6.5%

-5%

0%

5%

10%

15%

20%

2009 2010 2011 2012 2013 2014F 2015F 2016F

% GDP growth East Asia average

GDP growth rate

Source: National Statistics Office of Mongolia, International Monetary Fund

Mongolia maintained 3 consecutive years of double digit growth , fuelled by industrial and mining

developments. This growth pace is expected to maintain due to further mining developments and

government focus on developing other sectors.

4

Inflation and FX rate

1.9%

14.3%

11.1%

14.2% 12.5%

12.0%

11.0%

6.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2009 2010 2011 2012 2013 2014F 2015F 2016F

Inflation

0.5% 5.0%

17.4%

-12.9%

9.4%

1.6%

19.9%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2007 2008 2009 2010 2011 2012 2013

FX rate (MNT / USD)

Source: Bank of Mongolia

Bank of Mongolia is making policies to decrease inflation, ensure financial stability and allow exchange rate

flexibility. To effect its policy, BoM relies on 6 key tools

- Policy rate - FX market operations

- Reserve requirements - Repo facilities

- Open market operations - Medium-term price stabilization program

5

Financial Sector

Source: Bank of Mongolia (Central bank)

1,948

2,354 21%

2,071 -12%

2,800 35%

5,238 25%

6,585 26%

8,141 23%

68

189 462

374

330

295

317

40

93 121

90

73

110

150

3.3%

7.2%

17.4%

11.5%

5.8%

4.2% 3.7% 4.2%

3.9% 4.4% 2.1%

2.0% 2.6%

3.5%

2007 2008 2009 2010 2011 2012 2013

Performing Loans Non-performing Past-due NPL Ratio Golomt bank NPL Ratio

6

The Bank of Mongolia’s policy

objectives are two fold

Maintain inflation at low and stable levels

Allow exchange rate flexibility in line with

macroeconomic fundamentals

To effect its policy, the Bank of

Mongolia relies on 6 key tools:

The Policy Rate to directly target inflation

Reserve Requirements to affect broad

money supply

Open Market Operations to absorb excess

liquidity

FX Market Intervention to control exchange

rate volatility

Repo Facilities to manage intra-day liquidity

Medium-term Price stabilization program

with the Government

Golomt - Best Bank in Mongolia

7

Strengthened the bank’s operation through

multichannels

Introduced new products and services

Expanded the cooperation with valued

partners

Self Service Banking

The first Banking applications for smart phones

Launched the first internationally accepted MasterCard

card (MNT)

Became the only Bank which offers eTax pay service in

cooperation with Mongolian General Tax Authority

Became a founding member bank of UnionPay

International

Continued the corrospondent banking cooperation with

leading international banks welcoming Duetsche Bank,

Standard Chartered Bank and Sber Bank

19%

21%

21%

25%

27%

28%

29%

30%

50%

Assets

Net loans

Total Capital

Total Deposits

Individual Deposits

Corporate loans

Mortgage loans

Demand & Term Deposits

Card RetailTransactions

Continued the dominant market share

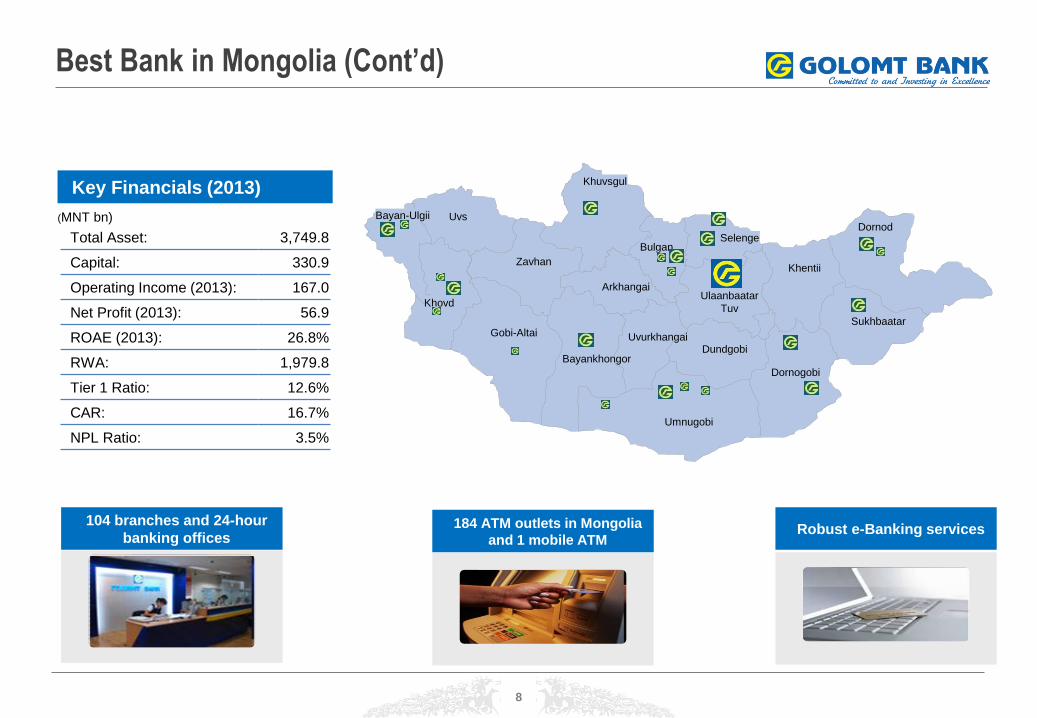

Best Bank in Mongolia (Cont’d)

Key Financials (2013)

(MNT bn)

Total Asset: 3,749.8

Capital: 330.9

Operating Income (2013): 167.0

Net Profit (2013): 56.9

ROAE (2013): 26.8%

RWA: 1,979.8

Tier 1 Ratio: 12.6%

CAR: 16.7%

NPL Ratio: 3.5%

Arkhangai Uvs Bayan-Ulgii

Arkhangai

Zavhan

Khovd

Khuvsgul

Gobi-Altai

Bulgan

Ulaanbaatar

Tuv

Uvurkhangai

Bayankhongor Dundgobi

Umnugobi

Khentii

Dornogobi

Dornod

Sukhbaatar

Selenge

184 ATM outlets in Mongolia

and 1 mobile ATM Robust e-Banking services

104 branches and 24-hour

banking offices

8

19%

17%

17% 16%

16%

4%

11%

Mining & Exploration

Electricity & Oil

Manufacturing

Trade - Whole & Ret.

Construction

Tourism

Others

Balanced Growth and Increasing Diversification

Key Business Segments Total Assets

(MNT bn)

1,013

1,574

2,135 2,527

3,750

2009 2010 2011 2012 2013

Others Net Loan Financial Investments Cash

While growing at a substantial rate, we have been

proactively diversifying our assets with balanced

distribution of business.

9

% Contribution to

Profit Before Tax

(2013)

% Contribution to

Profit Before Tax

(2012)

38.9% 28.9% Corporate banking

Retail Banking

Treasury /

Investment Bank

36.8% 29.3%

24.3% 41.9%

Industry Breakdown

(%)

Corporate Banking Overview

Increasing Profitability

The bank had net operational income of MNT 167 billion

with total increase of MNT 77 billion or 85 per cent. These

achievements were due to increases of net interest income of

MNT 49 billion and non-interest income of MNT 28 billion

Gain from foreign currency increased by MNT 21 billion

or 122%:

The number of foreign currency transactions increased

by 153% since 2012

Net fees & commission income increased by 27%:

Successful cooperation with the Bank of Mongolia and

the Government on financing of strategically important

projects

Operating Income

Relatively High Non-Interest Income Mix-2013

(% non-interest income to operating income)

36%

29% 33%

0%

10%

20%

30%

40%

37 46

78 90

167

2009 2010 2011 2012 2013

Non Interest Income (net)

Net Interest Income

Operating Income

Billion MNT

10

Lean operations with a cost to income ratio of 40.7% in 2013

Generated ROAE of 26.8% in 2013

Strongest underwriting standards and customer service

orientation

Network of 98 branches, but captures 25% of the retail loan

market

Efficient Bank Generating High Return

54.4

101.7

134.6

162.7

200.1

2009 2010 2011 2012 2013

13.4 13.5 12.9 13.3

16.7

10.9

8.8 9.5

11.2 12.6

2009 2010 2011 2012 2013

CAR Tier1

Solid Capital and Liquidity Positions

Total Capital(1),(2)

(US$ mm)

Capital adequacy ratio was at 16.7%. substantially in excess

of the minimum level of 14%, imposed by The Bank of

Mongolia, and Basel II recommendation of 7%

We maintain adequate liquidity ratio that is higher than the

average of local banks

Capital Adequacy and Tier 1 Ratio

(%)

11

High Liquidity with Well-Managed LDR(4)

63.5 59.6

67.9 69.4 71.5

2009 2010 2011 2012 2013

(%)

Portfolio Overview

Loan / Deposit Profile (2013)

5.4

6.2

10.6

16.3

41.7

19.9

0–30 Days 1–3 Months

3–6 Months 6–12 Months

1–5 Years Over 5 Years

(%)

26%

18% 56%

Current Accounts Demand Deposits Time Deposits

56%

40%

4%

Households Corporates Public entities

Loan Maturity Profile Deposit by Type Deposit by Depositor

12

Gross Loans and Advances Breakdown

56.9 61.3 60.9 57.4 52.6 43

28.8 25.5 20.4 17.1 21

28

8.8 7.3 10.2

15.4 17.3 22

5.4 5.9 8.5 10.1 9.1 8

2008 2009 2010 2011 2012 2013

Consumer

Mortgage

Small Business

Corporate

Golomt has a strong capital base supported by the Bank’s prudent approach to lending

Selects high quality loans and utilizes risk based pricing

Results in low NPLs and high ROEs

Exhibited resilient growth even during the financial crisis

Retail portfolio expanded tremendously in the last several years

Increasing diversification of revenue sources

Highlights

Management Team

13

Management team with an average tenure of 13 years, has grown hand-in-hand with the Bank

Joined Golomt Bank in 1995

Has served as a VP since the bank was founded in 1995

Prior to joining Golomt Bank, served as a senior accountant for the Trade & Development Bank

Chimegmunkh Munkhuu

Vice President & Director of Financial

Management Division

Bolormaa Luvsandorj

Executive Vice President & Director

of Investment Banking Division

Joined Golomt Bank in 2001

Previous roles in Golomt Bank include Officer at the Financial Control Division, Senior economist at the Credit Department,

Nyamsuren Tumur-Ochir Director of Credit Division

Joined Golomt Bank in 2001

Prior to joining Golomt Bank, served as a bank supervisor within the Bank of Mongolia beginning in 2000

Chingun Munkhsaruul

Vice President & Director of Risk

Management Division

Joined Golomt Bank in 1999

Previous roles in Golomt Bank include Auditor at the Audit Division, Loan Officer at the Credit and Economics Department, Operational Risk Management Department Director of the Audit Division

Batsuren Rentsenbat

Director of Internal Audit Division

Joined Golomt Bank in 2008

Previous role in Golomt Bank include Director of Marketing Department

Enkhtuya Bilegbadrakh

Vice President & Director of Retail Banking Division

Joined Golomt Bank in 1996

Previous roles in Golomt Bank include Economist, Director of Credit Department, VP & Director of Corporate Banking Division, and Director of Operations Division

Prior to joining Golomt Bank, he graduated from the School of Economics from the National University of Mongolia

Munkhtur Dagva

Executive Vice President & COO

Joined Golomt Bank in 1999

Previous role in Golomt Bank include Director of the Project Loan Department

Prior to joining Golomt Bank, served as Director of Dobl Co. Ltd, Manager at Most Feeling Co. Ltd in Prague

Oyun-Erdene Lamjav

Vice President & Director of Corporate

Banking Division

Joined Golomt Bank in 2000

Previous roles in Golomt Bank include COO, VP & Director of Support Division

Prior to joining Golomt Bank, he was the secretary general to the Democratic Union Coalition and the first deputy chief for the prime minister

Ganbold Galsan

Chief Executive Officer

Joined Golomt Bank in 2003

Previous roles in Golomt Bank include Dealer and Senior Dealer in Treasury Division

Munkhbaatar

Batjargal

Director of Treasury Division

13

Joined Golomt Bank in 2014

Founder and President of Bodhi Financial Advisory Services LLC

Has served as the First Deputy CEO at the Development Bank of Mongolia, and Industry Portfolio Manager at the Deutche Bank AG

13

Golomt Bank Head Office

Chinggis Khan Square - 3

Ulaanbaatar 210260A, Mongolia

Fax: +976-11-313155

Email: [email protected]

Website: www.golomtbank.com

Dial: (976) 7011 7676

Corporate Banking : ext 1212

Investment Banking : ext 1401

Treasury : ext 1374

Financial Institutions: ext 1379

Retail Banking : ext 1001

Contact Details:

14 14